Caviar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

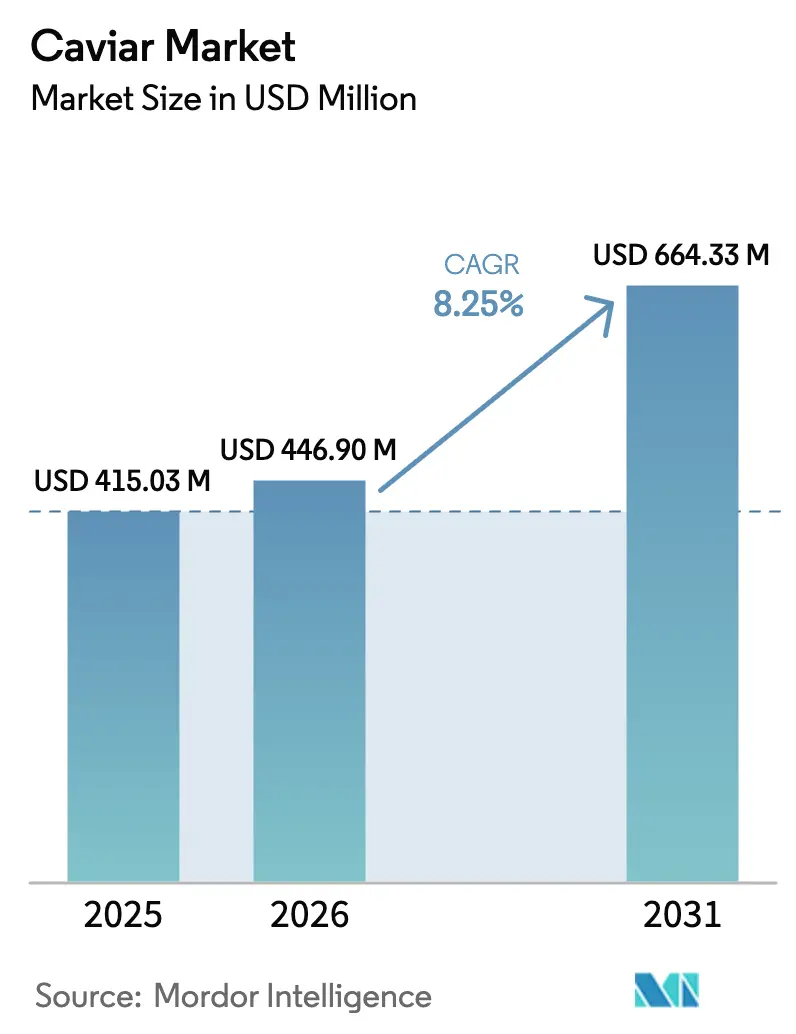

| Market Size (2026) | USD 446.90 Million |

| Market Size (2031) | USD 664.33 Million |

| Growth Rate (2026 - 2031) | 8.25% CAGR |

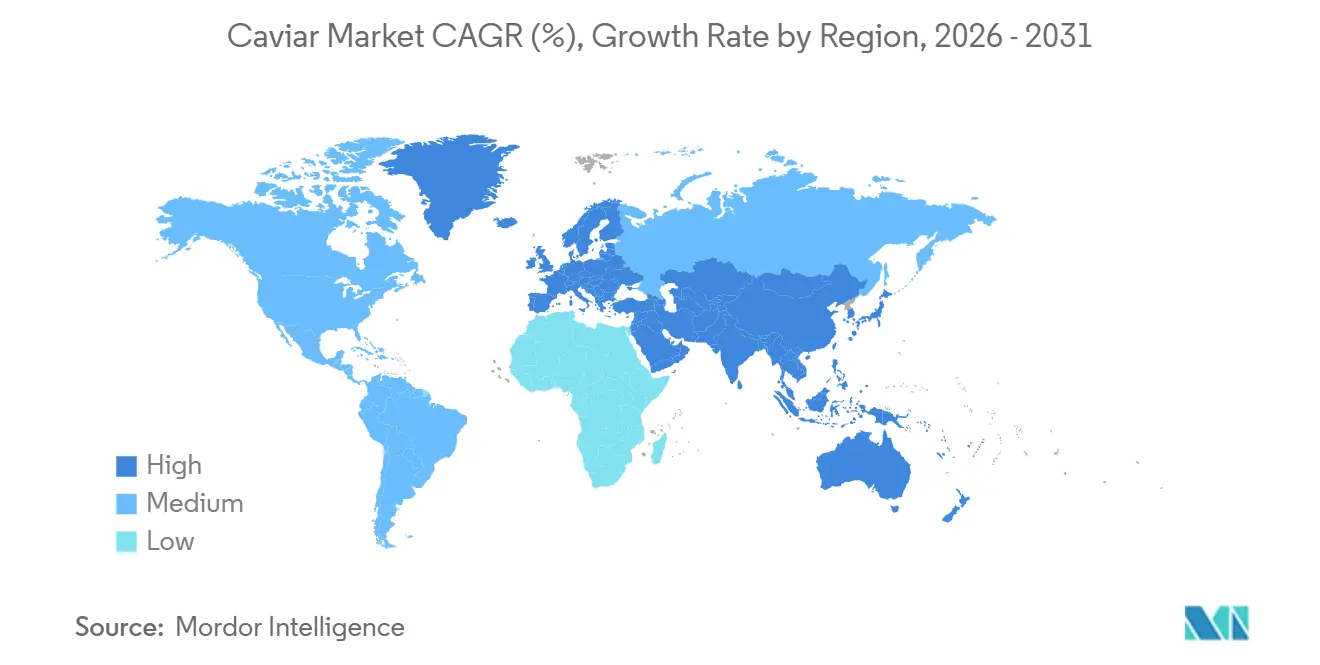

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Caviar Market Analysis by Mordor Intelligence

The caviar market size is expected to grow from USD 415.03 million in 2025 to USD 446.90 million in 2026 and is forecast to reach USD 664.33 million by 2031 at an 8.25% CAGR over 2026-2031.

Advancements in aquaculture, a global cold-chain expansion, and rising disposable incomes in regions such as the Asia Pacific and the Middle East are accelerating growth in the caviar market by empowering farm-raised producers to bypass traditional importers through digital platforms. Highlighting the significance of these advancements, the U.S. Department of Agriculture notes China's extensive network: with 230 million m³ dedicated to refrigerated storage and 432,000 temperature-controlled vehicles, the nation can ensure same-day delivery for premium perishables. On the production side, Vietnam inaugurated a sturgeon farm capable of housing a million fish in 2025. Concurrently, Spain's AZTI has introduced a DNA-based sex determination method, slashing juvenile rearing costs by a notable 40%. While farmed roe is projected to dominate the caviar market with a 92.82% share of the 2025 volume, wild quotas, albeit regulated, are on an upward trajectory, expected to grow at a 9.78% CAGR. This cautious reopening of fisheries by Caspian states is under the watchful eye of CITES. Beyond traditional avenues, the caviar market has found its way into airlines, luxury hotels, and e-commerce platforms, broadening its consumer base well past niche boutiques. These innovations are reinforcing structural competitiveness within the caviar market.

Key Report Takeaways

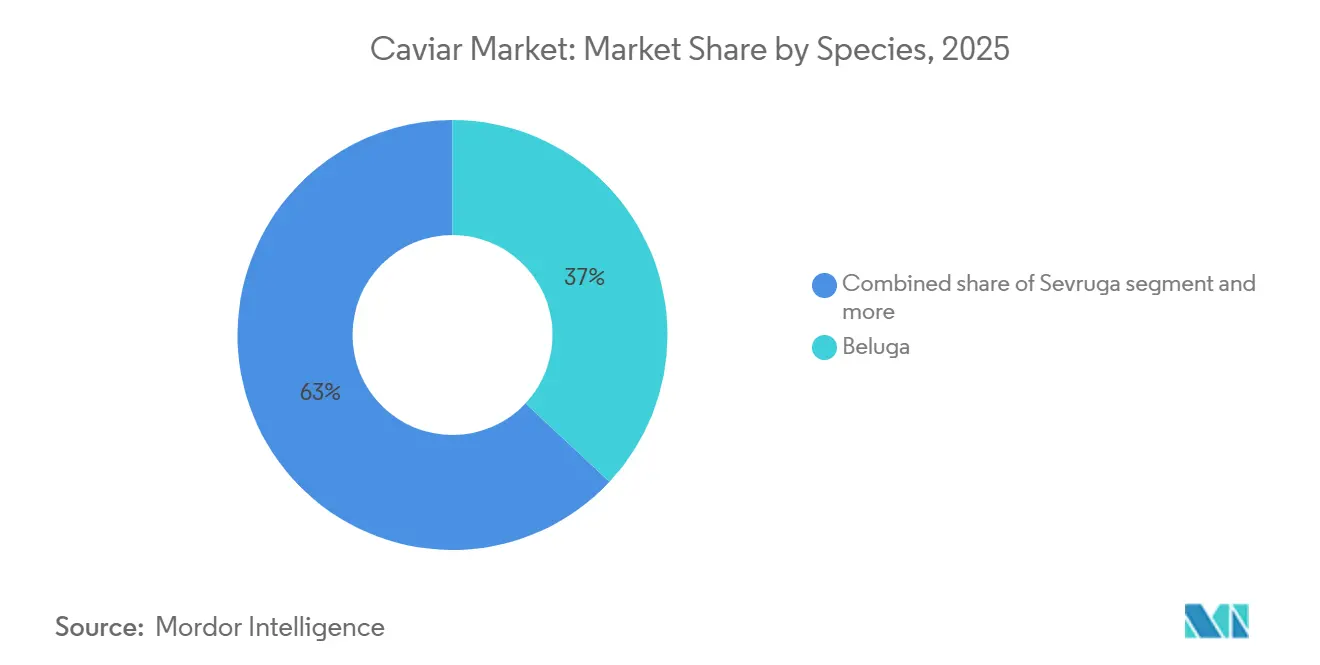

- By species, Beluga led with 36.96% of the caviar market share in 2025; Sevruga is forecast to post a 9.80% CAGR through 2031.

- By form, fresh caviar captured 49.74% of the 2025 volume, whereas frozen products are projected to expand at a 10.03% CAGR through 2031.

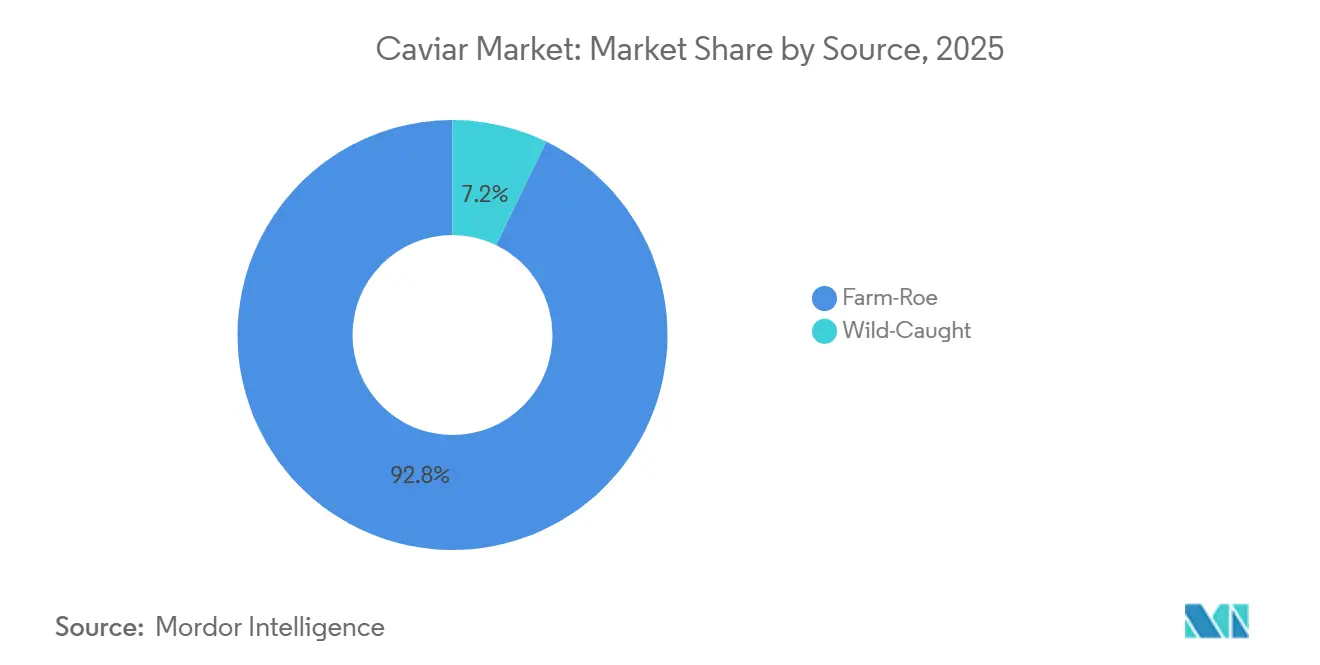

- By source, farmed-roe dominated with a 92.82% caviar market share in 2025, while wild-caught supply is poised for a 9.78% CAGR to 2031.

- By distribution channel, off-trade platforms commanded 62.57% of sales in 2025; on-trade venues are expected to register a 10.36% CAGR to 2031.

- By geography, the Asia Pacific generated 35.43% of 2025 revenue, while Europe is set to record the fastest regional growth at 9.56% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Caviar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health benefits awareness increases caviar's nutritional appeal | +1.2% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Growth of e-commerce and direct-to-consumer logistics | +1.5% | Global, led by Asia Pacific and North America | Short term (≤ 2 years) |

| Aquaculture advancements improve the quality of farmed caviar | +1.8% | Asia Pacific core, spillover to Europe and the Middle East | Long term (≥ 4 years) |

| Luxury food trends drive premium caviar product demand | +1.3% | Global, with emphasis on the Middle East and the Asia Pacific | Medium term (2-4 years) |

| Growth in the hospitality sector supports fine food markets | +1.0% | Global, particularly the Middle East and North America | Short term (≤ 2 years) |

| Rising disposable incomes support luxury food preferences | +0.9% | Asia Pacific and Middle East, selective North America segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aquaculture advancements improve quality of farmed caviar

Ultrasound-guided maturity sensors in recirculating aquaculture systems have reduced production cycle variability by 30%, strengthening efficiency across the caviar market. This advancement allows producers to harvest roe with optimal lipid profiles, achieving a texture comparable to that of wild-caught roe. In a significant move, Vietnam, as reported by its Ministry of Agriculture and Rural Development, is set to commission a 1-million-fish sturgeon farm by 2025. This venture, the largest single-site investment in the sector, aims for an ambitious target of 50 tonnes of annual output by 2028. In 2025, AZTI introduced a groundbreaking DNA-based sex determination method[1]Source: AZTI, “DNA-Based Sex Determination in Sturgeon,” azti.es. This innovation empowers hatcheries to identify and cull male fish at the fingerling stage, a significant leap from the previous 3-year feed investment. As a result, hatcheries can reduce juvenile rearing costs by 40% and optimize tank space for revenue-generating females. Iran's Fisheries Organization, eyeing a 200-tonne caviar production by 2026, is strategically leveraging state-subsidized feed and tax incentives to regain share in the global caviar market. This move aims to reclaim market share that was lost during the Caspian moratorium. In Sweden, Arctic Roe has pioneered a non-lethal milking technique that improves sustainability metrics within the caviar market. This method permits multiple harvests from the same fish over a decade, slashing the effective cost per kilogram by 25% when juxtaposed with traditional slaughter methods. Meanwhile, Fourier-transform infrared spectroscopy has emerged as a game-changer. It offers real-time insights into ovarian fat content, enabling tailored finishing diets. This innovation not only curbs lipid oxidation but also extends the refrigerated shelf life of products from 6 to 9 days, all without the need for pasteurization.

Growth of E-commerce and direct-to-consumer logistics

Digital platforms have streamlined the traditional distribution model in the caviar market, once reliant on importers, wholesalers, and retailers, into a single, swift shipment. This shift has allowed participants in the caviar market to capture margins that previously inflated retail prices by 60% to 80%. In 2024, Quince ventured into online caviar sales, debuting Royal Osetra caviar at USD 125 per tin. They offered a promotional price of USD 100 for purchases of two or more tins, effectively undercutting specialty-store prices by 30% to 40%. Brooklyn's Pearl Street Caviar boasts next-day delivery across the contiguous U.S., ensuring cold-chain integrity with gel-pack insulation, rated for 18 hours at ambient temperatures up to 32°C. The Food and Drug Administration's New Era of Smarter Food Safety Blueprint, rolled out in 2024, emphasizes digital traceability for high-risk foods, caviar included. It mandates QR codes linking to blockchain-verified harvest dates and CITES export permits. By 2023, China's cold-chain infrastructure expanded to 230 million cubic meters of refrigerated storage and 432,000 temperature-controlled vehicles, strengthening logistics across the caviar market [2]Source: USDA Foreign Agricultural Service, “China Cold Chain Report 2023,” usda.gov. This advancement enabled Kaluga Queen to deliver orders in Shanghai within 4 hours of harvest. In Abu Dhabi, Emirates AquaTech poured over USD 100 million into a vertically integrated facility, reflecting consolidation trends in the caviar market. This facility processes, tins, and ships its Yasa brand caviar (priced at approximately USD 200 per 100 grams) within 48 hours of extraction, deftly sidestepping European re-export hubs.

Luxury food trends drive premium caviar product demand

Michelin-starred restaurants are increasingly offering caviar as an upsell, expanding premium positioning within the caviar market beyond just traditional enthusiasts. In New York, Momofuku debuted a USD 600 fried chicken dish adorned with caviar. Meanwhile, LittleMad sprinkles a USD 20 caviar garnish on its seasonal offerings, and Figure Eight prices 30 grams of Kaluga hybrid caviar at USD 48. These pricing strategies are making caviar a more commonplace indulgence for affluent millennials. In December 2024, Caesars Palace Las Vegas unveiled Caspian's Cocktails & Caviar, boasting a caviar bar with pairings curated by a certified sommelier, underscoring the casino industry's shift towards experiential dining. Set to debut in September 2025 at the Mileo Hotel on The Palm Dubai, Cut Caviar is part of a broader trend, with 1,500 new food venues springing up in Dubai in the first five months of 2024. In August 2024, Qatar Airways rolled out caviar service in Business Class across 13 routes, including key destinations like London, Paris, and Sydney, strengthening visibility for the caviar market. This move underscores the Middle Eastern carriers' strategy, positioning sustainably sourced caviar as a premium differentiator. In 2024, White Dubai transitioned from a nightclub to an upscale dining lounge, serving Beluga caviar at AED 2,050 (around USD 558) per serving, catering to ultra-high-net-worth clientele who value exclusivity over cost.

Growth in hospitality sector supports fine food markets

In the wake of the pandemic, luxury hotels and resorts have turned their focus to signature dining experiences, justifying their premium growth in the caviar market. Notably, caviar has taken center stage, gracing both tasting menus and in-room services. As we look ahead, caviar's presence on U.S. restaurant menus is set to rise, thanks to casual-fine dining concepts that are making luxury more accessible through smaller, creatively presented portions. In 2025, Emirates Airlines reported a 30% year-on-year surge in onboard caviar consumption. The most sought-after routes were London, Paris, Sydney, and Moscow, where first-class passengers indulged in an average of 50 grams per flight. Sturia, a French supplier, caters to Michelin-starred restaurants with its Beluga caviar, priced at EUR 172 for 30 grams and exceeding EUR 1,000 for 200 grams. Their strategy? Direct contracts that sidestep wholesale intermediaries, ensuring healthy margins. Meanwhile, Acipenser in Madagascar is making waves, producing caviar for European Michelin establishments. With a monthly feed consumption of 60 tonnes, they export exclusively to France, Italy, and Spain, all under stringent cold-chain protocols that promise a swift 72-hour delivery. On the other hand, the Thai Royal Project, a brainchild of Queen Sirikit, has ventured into sturgeon farming in Chiang Mai. Their Silapacheep Caviar brand, a testament to their success, was showcased at the 2022 APEC Leaders' Summit in Bangkok, marking domestic production as a coveted diplomatic gift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prices limit access for mass consumers globally | -1.4% | Global, most acute in South America and Africa | Long term (≥ 4 years) |

| Illegal poaching disrupts the wild sturgeon population's sustainability | -0.8% | Caspian Basin, Lower Danube, North America Pacific Coast | Medium term (2-4 years) |

| Limited shelf life affects distribution and profitability | -0.6% | Global, particularly the Asia-Pacific and the Middle East | Short term (≤ 2 years) |

| Substitutes like soy pearls impact the caviar market share | -0.7% | Europe and North America, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High prices limit access for mass consumers globally

Premium Beluga caviar commands retail prices exceeding USD 200 for just 30 grams, limiting accessibility across the broader caviar market, making it unaffordable for median-income households in many regions. This pricing confines its volume growth primarily to high-net-worth individuals. Sturia's Beluga is priced at EUR 172 for 30 grams and surpasses EUR 1,000 for 200 grams. Meanwhile, Emirates AquaTech's Yasa brand is available for around USD 200 per 100 grams, a price point that restricts repeat purchases to the top 5% of earners. Data from the Bank of America Institute, dated January 2025, reveals that U.S. luxury spending per household has seen a year-on-year decline for 10 straight quarters, continuing through Q4 2024. While luxury fashion took a hit, down 12% in 2023 and another 9% in 2024, high-end travel and hotel expenditures managed to outshine the retail sector. According to FAO Fisheries and Aquaculture, feed costs for sturgeon aquaculture hover around USD 2.50 per kilogram. Given that a female sturgeon needs 8 to 12 years of feeding before its first harvest, this translates to a break-even price close to USD 80 for 100 grams. Such tight margins leave scant opportunity for downmarket expansion. Thailand's Sturgeon Farm, located in Hua Hin, faces a hefty monthly electricity bill of USD 9,000. This cost is essential to maintain their recirculating systems at a steady 21°C and to keep winter rooms between 6°C and 15°C. These fixed expenses act as a barrier, preventing any price reductions, even as production ramps up. Quince's Royal Osetra, priced at USD 125 per tin, sets the lower limit for premium caviar pricing. Yet, this price is still a staggering 10 times the per-gram cost of wild-caught salmon roe, making it less appealing to budget-conscious seafood enthusiasts.

Illegal poaching disrupts wild sturgeon population sustainability

WWF estimates that illegal fishing for the Caspian sturgeon is 3 to 5 times the legal catch, undermining CITES quotas and creating reputational risks for the caviar market. In 2022, California authorities arrested 9 individuals in a significant white sturgeon poaching ring, recovering roe valued at over USD 1 million, underscoring enforcement gaps even in regulated markets. WWF documented 337 illegal fishing cases in the Lower Danube, coinciding with a 90% decline in beluga sturgeon populations since 1990. A 2023 genetic analysis found that 21% of European caviar, labeled as farm-raised, actually came from wild-caught sturgeon. This not only violates CITES traceability requirements but also exposes retailers to potential prosecution under the Lacey Act in the U.S. California's 2024 estimate puts the legal-size white sturgeon population at about 6,447 fish, a stark drop from a historical baseline of over 150,000, attributed to habitat loss and illegal harvesting. Despite a 2005 U.S. ban on beluga caviar imports from the Black and Caspian Seas, customs seizures persist, averaging 200 kilograms annually, pointing to enduring smuggling networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Beluga Premiums Persist Despite Sevruga Acceleration

Beluga, with its 15-to-20-year maturation cycle and distinctive pearl-gray roe, accounted for 36.96% of caviar market revenue in 2025. Sevruga, forecasted to grow at a 9.80% CAGR through 2031, is set to experience the fastest species-level growth within the caviar market. Producers are optimizing 7-year cycles and targeting mid-tier buyers. Osetra, a favorite among Michelin-starred chefs, is celebrated for its nutty flavor profile and medium-sized grains, making it a perfect pairing with blinis and crème fraîche. Sterlet and Hackleback cater to entry-level consumers and catering operations, prioritizing cost over prestige. Meanwhile, other species like paddlefish and hybrid crosses are innovating through selective breeding, shortening maturation times. Kaluga-Amur hybrids now reach harvest weight in 6 years, compared to 10 years for purebred Kaluga.

CITES has implemented universal labeling requirements, mandating details like species code, source, origin, year, processor code, and lot identifier on every tin. While these regulations have heightened compliance costs, they've simultaneously bolstered consumer trust in the authenticity of farm-raised products. Iran's Fisheries Organization has set a 2026 target of 200 tonnes, distributing 60% to Beluga and 40% to Osetra. They're leveraging state subsidies to undercut Chinese pricing by 15% to 20%. In Sweden, Arctic Roe has pioneered non-lethal milking for Siberian sturgeon. This innovation permits repeat harvests over a decade and slashes the effective cost per kilogram by 25%. Since 2005, a U.S. ban on Caspian beluga imports has shifted demand towards farm-raised substitutes. Notably, Tsar Nicoulai's 2024 acquisition of Sterling Caviar has consolidated 40% of the domestic Beluga-substitute production. To address the 21% mislabeling rate found in European markets in 2023, TRAFFIC is piloting genetic traceability tools, such as mitochondrial DNA sequencing.

By Form: Frozen Formats Gain Share Through HPP Innovation

Fresh caviar, known for its delicate texture and lack of thermal processing, accounted for 49.74% of the 2025 volume. Frozen formats are projected to grow at a 10.03% CAGR through 2031 due to high-pressure processing, which preserves organoleptic qualities and extends shelf life. A barramundi caviar study showed pasteurization at 60°C-65°C extended refrigerated shelf life to over 21 days, compared to under 7 days for unpasteurized products. High-pressure processing at 600 megapascals achieved similar microbial reduction without texture degradation. Food and Drug Administration guidelines for reduced-oxygen-packaged caviar require a 6-log reduction of Clostridium botulinum, achievable through pasteurization at 90°C for 10 minutes or validated HPP protocols. The UK Food Standards Agency sets a default 10-day shelf life for vacuum-packed chilled foods stored at 3°C-8°C unless processors validate factors like salt concentration above 3.5% or water activity below 0.97.

Airline catering and cruise-line operations use dried, pressed, and pasteurized formats for ambient-stable inventory. Denmark’s CaviArt produces kelp-based caviar with a 12-month shelf life, supplying 70%-80% of Danish restaurant caviar. The Food and Drug Administration's 2024 New Era of Smarter Food Safety Blueprint emphasizes digital traceability and cold-chain sensors, increasing compliance costs by 5% but reducing spoilage by 15%-20%[3]Source: FDA Center for Food Safety and Applied Nutrition, “Fish and Fishery Products Hazards Guide 2025,” fda.gov. In January 2024, Modern Plant Based Foods launched vegan Kaviar in Wasabi, Original, and Salmon flavors, with an 8-to-10-month refrigerated shelf life, targeting e-commerce and restaurants. Xoma AB and Arctic Roe of Scandinavia plan to develop vegetarian caviar from Caulerpa algae, with pilot production set for late 2026.

By Source: Aquaculture Dominance Masks Wild-Caught Quota Revival

In 2025, farm-roe caviar accounted for 92.82% of the total volume in the caviar market, driven by CITES restrictions on wild harvesting and investments in recirculating aquaculture systems in China, Europe, and the Middle East. Wild-caught caviar, sourced from regulated quotas, is projected to grow at a 9.78% CAGR through 2031 as Caspian states cautiously reopen fisheries under CITES monitoring, targeting annual quotas of 50 to 80 tonnes shared among Iran, Russia, Kazakhstan, Azerbaijan, and Turkmenistan. In 2024, China produced an estimated 260 tonnes of farm-raised caviar, representing 35% of global output, with Kaluga Queen exporting 84% of its production to the European Union. Vietnam's 2025 commissioning of the world's largest sturgeon farm, with a capacity of 1 million fish, targets 50 tonnes of annual output by 2028, leveraging its tropical climate to accelerate growth rates by 20% compared to temperate facilities.

Emirates AquaTech in Abu Dhabi invested over USD 100 million in a vertically integrated facility housing 300,000 sturgeon and targeting 35 tonnes annually under its Yasa brand, with first shipments in 2024. Royal Caviar Company, also in Abu Dhabi, reported 18 tonnes on-site and 124 tonnes in delivery contracts, with its first batch harvested in 2012. Arctic Roe in Sweden, which began commercial shipments in 2019, pioneered non-lethal milking, enabling repeat harvests over a 10-year lifespan. Wild-caught caviar commands a 30% to 50% premium over farm-raised equivalents due to perceived authenticity, but a 2023 genetic analysis revealed 21% of European farm-labeled caviar originated from wild sturgeon, eroding price differentiation. CITES data from 2000 to 2015 shows aquaculture's share rising from 30% to 95%, with no export quotas for shared wild stocks published since 2010, reflecting the collapse of Caspian fisheries.

By Distribution Channel: On-Trade Venues Outpace Retail Growth

In 2025, off-trade channels, spanning supermarkets, specialty stores, and e-commerce, accounted for 62.57% of sales. However, on-trade venues, such as restaurants, hotels, and airlines, are projected to experience a robust growth rate of 10.36% CAGR through 2031 in the caviar market. This surge is attributed to a rebound in hospitality capital expenditure and a strategic positioning of caviar as a premium upsell by operators. Over the last decade, a New York restaurateur noted a significant market fragmentation, with the supplier base ballooning from "2 to 3 competitors to 20 to 30." This expansion has empowered chefs to negotiate contracts directly, sidestepping wholesale markups. In December 2024, Caspian's Cocktails & Caviar debuted at Caesars Palace Las Vegas, boasting a caviar bar with pairings curated by a certified sommelier. Meanwhile, Cut Caviar is set to launch at the Mileo Hotel on The Palm Dubai in September 2025, riding the wave of 1,500 new food establishments that sprouted in Dubai in the first five months of 2024.

In 2025, Emirates Airlines witnessed a 30% year-on-year surge in onboard caviar consumption, with London, Paris, Sydney, and Moscow routes leading the demand. Qatar Airways, in August 2024, introduced caviar service to Business Class on 13 routes, prominently featuring Doha–London, Doha–Paris, and Doha–Sydney. E-commerce is rapidly gaining traction in the off-trade sector, with platforms like Quince, which kicked off online caviar sales in 2024 at USD 125 per tin for Royal Osetra, and Brooklyn's Pearl Street Caviar, offering next-day delivery across the contiguous United States. China's cold-chain infrastructure, boasting 230 million cubic meters of refrigerated storage and 432,000 temperature-controlled vehicles by 2023, has facilitated same-day delivery in tier-1 cities, as reported by the USDA Foreign Agricultural Service. The Food and Drug Administration's 2024 finalized "New Era of Smarter Food Safety Blueprint" introduces QR codes that link to blockchain-verified harvest dates and CITES export permits. While this raises compliance costs, it significantly boosts consumer trust in online purchases.

Geography Analysis

In 2025, the Asia Pacific accounted for 35.43% of global caviar market revenue, driven by China's role as the top producer and a growing consumer. Kaluga Queen produces 260 tonnes annually, about 35% of global supply, while Chinese exports reached 276 tonnes worth USD 82.7 million in 2023. The EU sourced 84% of its caviar imports from China in 2020, highlighting Beijing's supply chain dominance. Thailand's Royal Project launched the Silapacheep Caviar brand, featured at the 2022 APEC Leaders' Summit, elevating domestic production. Japan's Miyazaki Prefecture targets affluent consumers with locally sourced caviar priced at JPY 12,000 (USD 80) per 20 grams. Singapore serves as a distribution hub for Southeast Asia, re-exporting to Indonesia, Malaysia, and the Philippines under cold-chain protocols, ensuring 48-hour delivery. India, an emerging market, sees imports concentrated in Mumbai and Delhi five-star hotels, with per-capita consumption 50 times lower than China's, signaling long-term potential.

Europe is projected to grow at a 9.56% CAGR through 2031, led by heritage markets in France, Italy, and Spain leveraging Protected Geographical Indication frameworks. France, the largest producer of farmed Siberian sturgeon caviar, supplies Michelin-starred restaurants through Sturia, with prices reaching EUR 1,000 for 200 grams. Post-Brexit customs delays have increased UK logistics costs by 10%, creating opportunities for domestic aquaculture in Scotland and Wales. Germany, the fourth-largest importer globally, saw prominent imports in 2024, with Berlin and Munich specialty stores reporting 15% growth in 2024. Belgium, a re-export hub, expanded Antwerp's cold-storage capacity in 2023 to handle luxury goods.

North America's retail sales are rising, led by the U.S., with Canada contributing. Tsar Nicoulai's 2024 acquisition of Sterling Caviar consolidated 40% of U.S. farm-raised output, enabling direct supply to Whole Foods and Williams Sonoma. Mexico's luxury hotels in Cancún, Los Cabos, and Mexico City have adopted caviar as a signature amenity, with imports up 25% year-on-year in 2024, according to the Mexico Secretariat of Economy. The Middle East and Africa are growing rapidly, driven by ultra-high-net-worth populations and expanding hospitality. Emirates AquaTech in Abu Dhabi invested over USD 100 million in a facility targeting 35 tonnes annually under its Yasa brand. Dubai added 1,500 food establishments in early 2024, many featuring caviar. South Africa and Morocco are piloting sturgeon aquaculture, aiming for 10 to 15 tonnes annually by 2028, though regulatory frameworks lag behind CITES-compliant markets in Europe and North America.

Competitive Landscape

The global caviar market is moderately fragmented. The top five producers, Kaluga Queen, Sturia, Agroittica Lombarda, Tsar Nicoulai, and Petrossian, command an estimated 40% share. Over the past decade, the supplier base has surged from 2-3 competitors to 20-30, as noted by a New York restaurateur. This shift is largely due to direct-to-consumer platforms and regional aquaculture ventures challenging established distribution networks. Consolidation is on the rise: Tsar Nicoulai's 2024 acquisition of Sterling Caviar has birthed the largest U.S. producer, seamlessly merging hatchery, grow-out, and processing operations. This entity now supplies retailers such as Whole Foods and Williams Sonoma. Technological advancements are redefining competitive benchmarks across the caviar industry. For instance, AZTI's DNA-based sex determination, validated in 2025, slashes juvenile rearing costs by 40%. Meanwhile, Arctic Roe of Scandinavia's non-lethal milking technique permits repeat harvests over a decade, trimming the effective cost per kilogram by 25%. The market is also eyeing plant-based substitutes as a lucrative avenue. CaviArt dominates, supplying 70%-80% of Denmark's restaurant caviar. In January 2024, Modern Plant-Based Foods debuted its vegan Kaviar, appealing to flexitarian consumers who value sustainability over traditional authenticity. South Korea's CellMEAT has crafted a cell-based Osetra prototype, bolstered by an impressive USD 8.1 million in Series A funding. They're establishing a facility in Seoul, boasting a 100-kilogram-per-day capacity, though they're navigating uncertain regulatory approval timelines.

New players are making waves: Vietnam's sturgeon farm, boasting a million fish and aiming for 50 tonnes of annual output by 2028, was commissioned in 2025. Meanwhile, Emirates AquaTech has invested USD 100 million in an Abu Dhabi facility, integrating hatchery, grow-out, processing, and retail under the Yasa brand. However, not all incumbents are thriving. Russian producers have seen their export volumes plummet, and Caspian wild-harvest cooperatives, grappling with stock depletion, haven't reported CITES quotas since 2010. CITES' universal labeling mandates, detailing species code, source, origin, year, processor code, and lot identifier, have raised compliance costs by 8%-12% across the caviar industry. Yet, they've bolstered consumer trust and erected barriers for smaller operators lacking traceability.

The Food and Drug Administration's 2024 digital traceability mandates, part of the New Era of Smarter Food Safety Blueprint, require QR codes linked to blockchain-verified harvest dates, further tightening the market around vertically integrated players. These regulations, combined with advancements in technology and the rise of plant-based and cell-based alternatives, are reshaping the competitive landscape. As the market evolves, players with robust traceability infrastructure and innovative production methods are better positioned to capitalize on emerging opportunities while navigating the increasing demands for compliance.

Caviar Industry Leaders

The Caviar Co.

L’Osage Caviar Company., Inc.

Black River Caviar

Russian Caviar House Company

Tsar Nicoulai Caviar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ultra Fish Group acquired Severny Kristall, a producer of frozen, chilled, salted, and dried fish products, including premium salmon caviar, with the facility capable of producing up to 20 tons of finished products daily, enhancing the company's processing capabilities and market reach.

- February 2025: Choice Holding has announced plans to invest in an aquaculture project along Kazakhstan’s Caspian Sea coast. The initiative aims to produce between 100 and 600 tons of sturgeon and around 100 tons of caviar annually.

- February 2025: Plaza Premium Group introduced Numero Uno Caviar Bars at Dubai International Airport and Zayed International Airport. These luxurious culinary destinations are located at the Plaza Premium Lounge in Dubai International's Terminal 3 and the Pearl Lounge in Zayed International's Terminal A.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the caviar market as revenue generated from salt-cured roe obtained exclusively from sturgeon species, whether farm-raised or legally wild-caught, and sold in fresh, pasteurized, or frozen form to retail, food-service, and industrial buyers. We track values in constant 2024 USD across all supply chains.

Scope Exclusion: Substitute fish roe (salmon, lumpfish, cod, etc.) and plant-based or lab-cultivated "vegan caviar" are excluded from this assessment.

Segmentation Overview

- Species

- Beluga

- Osetra

- Sevruga

- Sterlet

- Hackleback/Other Sturgeon

- Other Types

- Form

- Fresh

- Frozen

- Dried/Pressed/Pasturised

- Source

- Farm-Roe

- Wild-Caught

- Distribution Channel

- On-trade

- Off-trade

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Peru

- Colombia

- Chile

- Rest of South America

- Middle East and Africa

- South Africa

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held interviews with sturgeon farmers, gourmet importers, fine-dining chefs, and fisheries regulators across Europe, North America, China, and the Gulf. Follow-up surveys clarified production costs, shrinkage rates, menu penetration, and allowable labeling tolerances, letting us refine conversion factors and close information gaps.

Desk Research

Mordor analysts first screened open datasets such as FAO aquaculture output, UN Comtrade sturgeon-roe HS codes, CITES export permits, Eurostat external fishery statistics, and USDA import bulletins, which anchor species-wise production and trade flows. Complementary context was gathered from the Federation of European Aquaculture Producers, luxury food trade magazines, and peer-reviewed studies detailing curing yields and price benchmarks.

We then mined company filings, gourmet-retailer price lists, and investor decks to benchmark average selling prices, while D&B Hoovers and Dow Jones Factiva supplied financial clues on leading processors and distributors. The sources mentioned are illustrative; many additional public references helped us validate data points and narrative nuances.

Market-Sizing & Forecasting

A top-down production and trade reconstruction provided the initial 2025 demand pool; we corroborated totals through selective bottom-up supplier roll-ups and menu channel checks. We fed the model with live-biomass estimates, permitted harvest ratios, average roe yield per kilogram, luxury-hotel dish penetration, and inflation-adjusted retail ASPs. Missing artisanal volumes were bridged through triangulated import invoices and ferry-route shipment logs.

Multivariate regression combined with ARIMA smoothing projected each driver through 2030, and scenario analysis gauged impacts from tighter CITES quotas or faster aquaculture tech adoption.

Data Validation & Update Cycle

Our analysts benchmark outputs against luxury-goods indices and export earnings; anomalies trigger re-engagement with experts before sign-off.

Reports refresh annually, with interim updates for material events such as disease outbreaks or trade bans, and an analyst reviews every calculation before client delivery.

Why Mordor's Caviar Baseline Commands Reliability

Published estimates often diverge because firms apply different definitions, pricing layers, and refresh cadences. According to Mordor Intelligence, strict inclusion of only sturgeon-derived roe and yearly data rolls create a tighter baseline.

Key gaps surface when other studies fold in non-sturgeon eggs, apply wholesale rather than retail mark-ups, or freeze currency conversions at 2024 rates. Mordor's hybrid top-down and bottom-up crosswalk and rolling refresh dilute these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 412.65 million (2025) | Mordor Intelligence | |

| USD 448.6 million (2024) | Global Consultancy A | Includes non-sturgeon roe and gourmet condiments, older base year |

| USD 394.5 million (2024) | Industry Database B | Uses customs values without channel mark-ups and assumes uniform ASP |

These comparisons show that Mordor's disciplined scope control, variable selection, and annual refresh deliver a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

How large is the caviar market in 2026?

The caviar market size is expected to grow from USD 415.03 million in 2025 to USD 446.90 million in 2026 and is forecast to reach USD 664.33 million by 2031 at an 8.25% CAGR over 2026-2031.

Which region generates the most revenue in the caviar market?

Asia Pacific accounts for 35.43% of 2025 revenue, driven by China’s production scale and advanced cold-chain infrastructure.

What species leads global revenue?

Beluga commanded a 36.96% caviar market share in 2025, thanks to its scarcity and high price premium.

Why are frozen formats gaining ground?

High-pressure processing extends shelf life to 21 days without compromising texture, supporting a 10.03% CAGR for frozen products through 2031.

How are airlines influencing demand?

Premium carriers such as Emirates and Qatar Airways added caviar service on long-haul routes, contributing to a 30% increase in onboard consumption during 2025.

What is the main challenge facing wild-caught supply?

Persistent illegal poaching in the Caspian and Danube regions undermines sustainability and crimps legal quota expansion despite robust demand.

Page last updated on: