Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

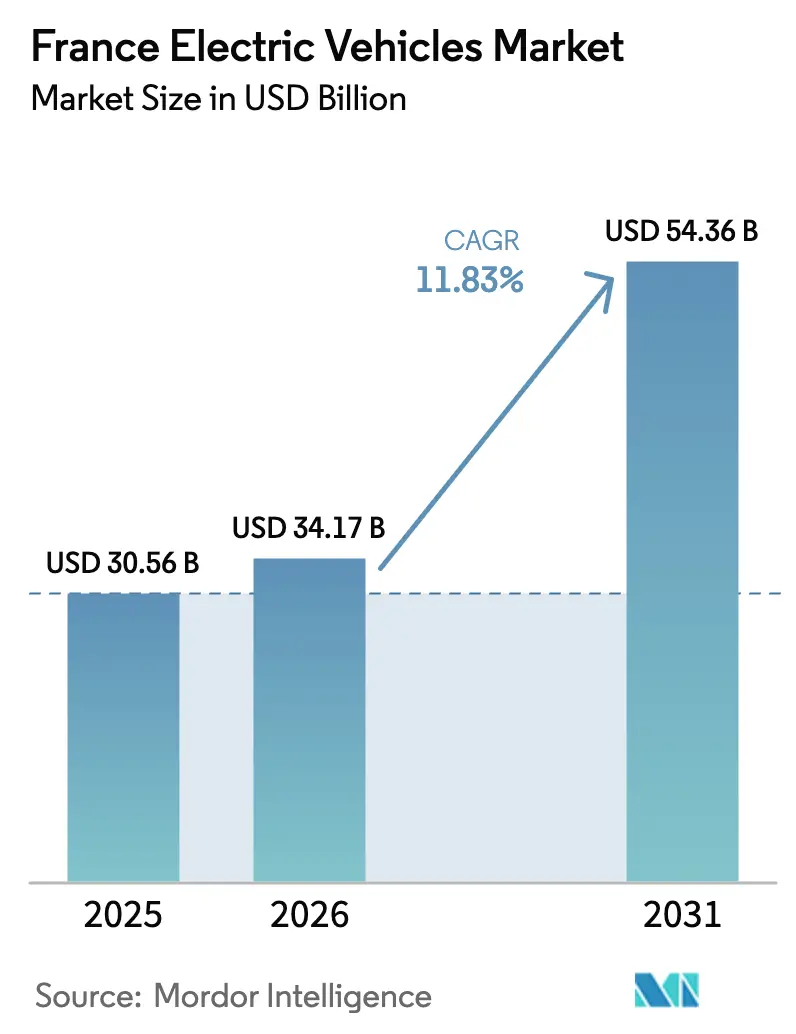

| Base Year Market Size (2025) | USD 30.56 Billion |

| Market Size (2026) | USD 34.17 Billion |

| Market Size (2031) | USD 54.36 Billion |

| Growth Rate (2026 - 2031) | 11.83% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Electric Vehicles Market Analysis by Mordor Intelligence

The French electric vehicle market size is expected to grow from USD 30.56 billion in 2025 to USD 34.17 billion in 2026 and is forecast to reach USD 54.36 billion by 2031 at 11.83% CAGR over 2026-2031. Incentives like the ecological bonus, an add-on for European-sourced battery cells, and reduced road-tax bands are narrowing purchase price gaps and boosting demand. The installation of rapid chargers, large-scale battery-cell production, and corporate fleet mandates have created economies of scale, reducing the total cost of ownership. Battery packs now priced below a certain threshold are hastening the shift towards parity with traditional cars. Additionally, domestic gigafactories in Hauts-de-France and Nouvelle-Aquitaine provide OEMs a buffer against supply shocks. Partnerships between automakers, utilities, and mobility platforms are not only accelerating the electrification of shared fleets but also opening up new revenue avenues, including vehicle-to-grid services.

Key Report Takeaways

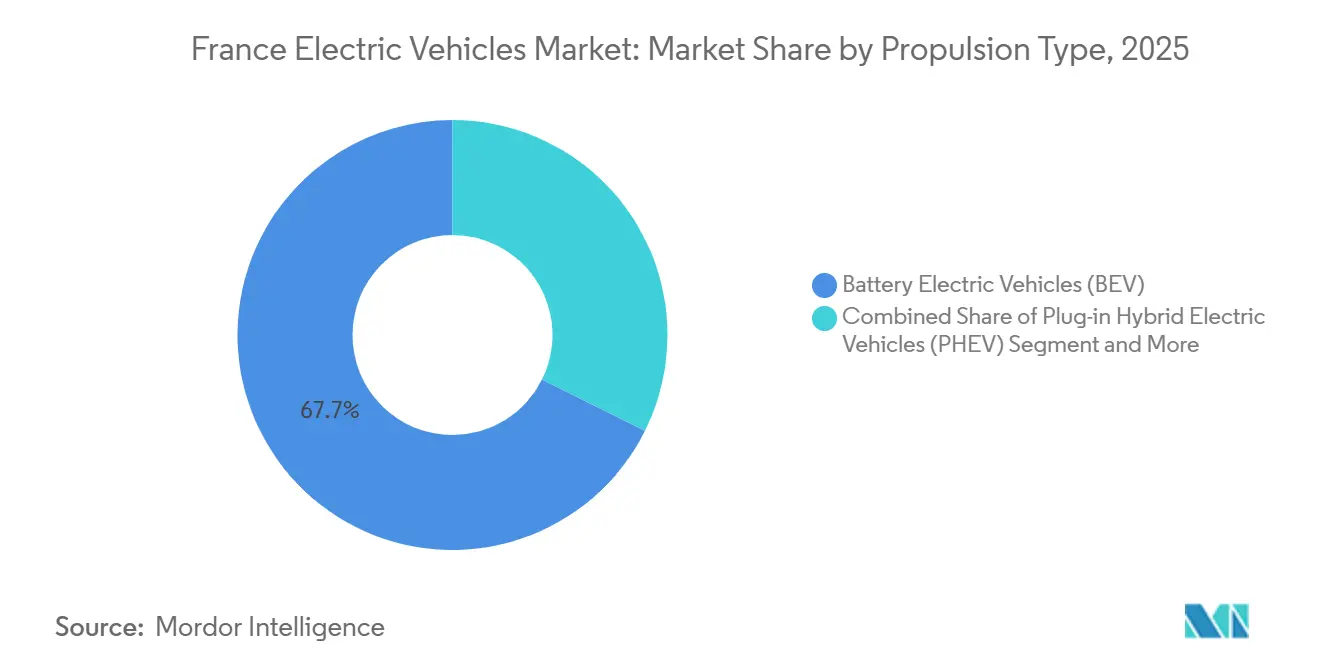

- By propulsion type, battery-electric vehicles account for 67.65% of the French electric vehicle market share in 2025; fuel-cell electric vehicles are forecast to grow at a 18.37% CAGR through 2031.

- By vehicle type, passenger cars accounted for 95.26% of the French electric vehicle market in 2025, while heavy trucks are expected to record the highest projected CAGR of 17.03% from 2026 to 2031.

- By charging type, AC units with a capacity of 22 kW or higher held a 73.92% share in 2025; ultra-fast DC chargers with a capacity above 150 kW are expected to expand at a 13.62% CAGR through 2031.

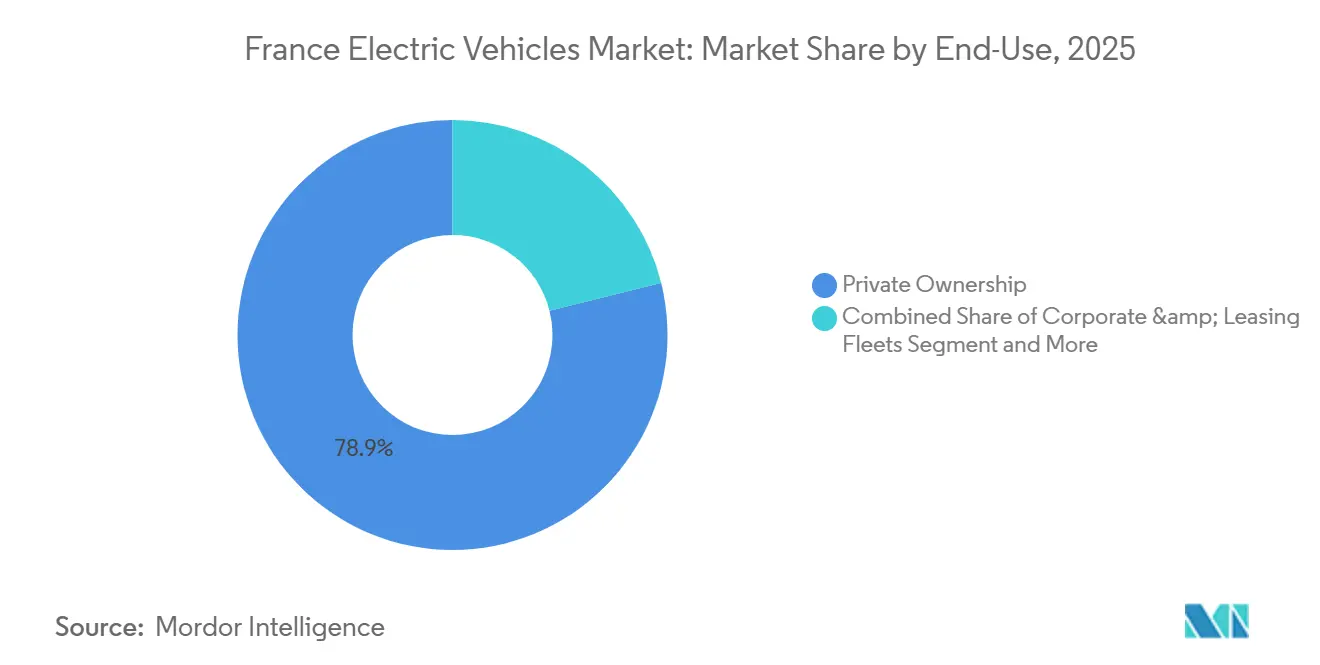

- By end-use, private ownership accounted for 78.88% of the 2025 volume, while shared mobility is projected to grow at an 18.56% CAGR through 2031.

- By battery capacity, 50–75 kWh packs controlled 49.04% share in 2025; packs above 75 kWh are expected to post a 13.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Electric Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Purchase and Tax Incentives | +2.8% | Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d'Azur, Hauts-de-France | Short term (≤ 2 years) |

| Fast-Charger Roll-Out | +2.3% | Nouvelle-Aquitaine, Occitanie, Grand Est, Pays de la Loire, Bretagne | Medium term (2-4 years) |

| Lithium-Ion Battery Cost | +2.0% | Hauts-de-France, Nouvelle-Aquitaine, Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| Corporate Fleet Electrification | +1.5% | Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d'Azur | Short term (≤ 2 years) |

| Second-Life Battery Resale | +0.9% | Centre-Val de Loire, Hauts-de-France, Nouvelle-Aquitaine | Long term (≥ 4 years) |

| Vehicle-to-Grid Revenue Streams | +0.7% | Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d'Azur | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Purchase and Tax Incentives

In 2025, government rebates for qualifying battery electric cars effectively reduced up-front costs and boosted registrations. A social-leasing initiative, set at EUR 100 (USD 117.87) monthly, enabled 50,000 low-income households to access electric vehicles, especially in urban areas. Localized cell production at Stellantis ACC and Verkor plants not only satisfies the incentive's origin stipulation but also strengthens supply chains. Although bonus amounts will decrease post-2026, falling battery prices are expected to counterbalance the diminishing subsidies. This policy framework not only propels immediate sales but also steers the market towards sustainable cost competitiveness in the long run.

Nationwide Fast-Charger Roll-Out

Public-private grants underpin corridor and workplace charging, lifting installed ports to roughly 147,000 by late 2025. Ultra-fast DC hubs from Mobilize and other networks triple charging speed for 75 kWh packs, improving convenience for long-distance travel. Regional disparities persist, yet the planned 25,000 ultra-rapid ports by 2030 will narrow gaps along the Atlantic and Mediterranean highways. Dynamic in-road wireless charging pilots on the A10 near Paris validate solutions for heavy trucks at highway speed. Sustained expansion prevents charging queues from constraining fleet growth in high-penetration zones.

Lithium-Ion Battery Cost Curve Compression

Pack prices fell significantly in 2025, breaching USD 115/kWh and bringing total-cost parity within sight for mass-market cars by 2027. Automakers shift toward lithium-iron-phosphate chemistries that trade energy density for affordability in models such as the Scenic E-Tech. Domestic gigafactories scaling from 13 GWh to 40 GWh mitigate currency and freight risk. Supply-chain initiatives, including a nickel-cobalt refinery scheduled for 2028, aim to localize upstream value and buffer volatility in raw materials. The result is a steady erosion of sticker-price premiums versus internal-combustion vehicles.

Corporate Fleet Electrification Mandates

The mobility-orientation law obliges fleets with more than 100 vehicles to reach a 40% low-emission share by 2027 and 70% by 2030[1]"LOM Law: everything you need to know about renewing vehicle fleets", SoFLEET, sofleet.eu. Compliance drives bulk procurement of vans and trucks, spurring OEM volume and stabilizing residual values. Heavy-truck adoption is accelerating in low-emission zones such as Paris, Lyon, and Marseille, where diesel restrictions are tightening. Dedicated truck-stop charging and 400-kilometer battery ranges enable regional logistics without route disruption. Non-compliant fleets face fines and reputational risk, reinforcing the conversion trend.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher EV Sticker Price vs ICE | -1.8% | Hauts-de-France, Nouvelle-Aquitaine, Bretagne, Normandie | Short term (≤ 2 years) |

| Uneven Rural Charging Coverage | -1.2% | Bretagne, Normandie, Centre-Val de Loire, Bourgogne-Franche-Comté | Medium term (2-4 years) |

| Supply Bottlenecks | -0.8% | Hauts-de-France, Nouvelle-Aquitaine, Auvergne-Rhône-Alpes | Long term (≥ 4 years) |

| Dealership Capability Gap | -0.5% | Occitanie, Grand Est, Pays de la Loire | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Up-Front EV Sticker Price vs ICE

Average battery-electric cars retailed a significant price premium over internal-combustion equivalents. Incentives close only part of the gap for households in regions where the median income trails the national average by more than 10%. Entry-level models priced below EUR 25,000 (USD 29,467) capture a limited share, leaving most buyers in higher price bands. Automaker price cuts signal competitive pressure yet threaten margins. Until battery prices fall near USD 100/kWh, price-sensitive consumers, especially in rural departments, will postpone purchases.

Uneven Rural Charging Coverage

Department-level charging density varies widely, with several low-population areas hosting fewer than 150 chargers. Highway and workplace grant programs favor urban corridors, leaving secondary roads underserved. Range anxiety discourages rural households that rely on public infrastructure rather than home parking. The high capital costs of ultra-fast DC units limit private investment in sparsely populated areas. Unless municipal budgets or cooperative models bridge the gap, regional adoption will lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Hydrogen Gains as BEVs Plateau

Battery-electric vehicles commanded a 67.65% share in 2025, on the back of dense charging grids in metropolitan areas. Fuel-cell electric vehicles scale at an 18.37% CAGR, supported by EUR 9 billion in hydrogen funding and a target of 1,000 refueling stations by 2030. Domestic production of fuel-cell van models at Hordain offers a 400-kilometer range with five-minute refueling, making it suitable for logistics operators. Plug-in hybrids decline as buyers migrate to pure-battery formats once infrastructure anxiety subsides.

Fuel-cell adoption centers on heavy-duty and high-utilization fleets where payload preservation outweighs hydrogen costs. Passenger fuel-cell models remain scarce, yet supplier capacity for stacks and tanks has matured. Government station targets imply investment of EUR 3-5 million (USD 3.54-5.89 million) per site, challenging but achievable if electrolyzer projects align with surplus renewable generation. Hydrogen, therefore, supplements rather than displaces the dominant battery segment in the French electric vehicle market.

By Vehicle Type: Heavy Trucks Outpace Passenger Surge

Passenger cars accounted for 95.26% of 2025 registrations, driven by broad model variety, falling battery prices, and consumer familiarity with home charging. Heavy trucks, starting from a low 2,000-unit base, post a 17.03% CAGR as freight companies navigate low-emission zones in Paris, Lyon, and Marseille, triggering mandatory diesel phase-outs. High-capacity chargers sited every 60–80 kilometers along the A7 and A10 corridors reduce dwell times to 45 minutes, making 400-kilometer electric drayage runs commercially viable. Municipal subsidies for electric refuse, construction, and delivery vehicles further widen the addressable market. As a result, freight electrification begins to narrow the historical gap in volume between commercial and passenger demand in the French electric vehicle market.

Light commercial vehicles, including the Renault Kangoo E-Tech and Citroën ë-Berlingo, appeal to artisans who can charge vans overnight at depots in Hauts-de-France and Nouvelle-Aquitaine. City and inter-city buses, powered by Alstom’s Aptis and Iveco’s E-Way platforms, reached 0.8% share as municipalities enforced zero-emission public-transport targets. Rapid truck uptake is attracting battery-leasing models that capex-shift packs off carrier balance sheets and guarantee end-of-life value recovery. Truck manufacturer Scania has revealed that its electric trucks are expected to start using the commercially available Megawatt Charging System (MCS) in early 2026[2]"Scania launches MCS rapid charging solution at EVS38 – a new era for heavy electric transport", Scania. Meanwhile, dedicated pilots for the MCS, set for 2026, aim to reduce dwell times to under 30 minutes, paving the way for genuine long-haul electrification. Together, these developments hint at a significant boost for the freight segments in France's electric vehicle market.

By Charging Type: Ultra-fast Infrastructure Emerges as Growth Leader

AC charging above 22 kW held a 73.92% share in 2025 because its average hardware cost fits residential, workplace, and curbside budgets. Ultra-fast DC ports over 150 kW deliver a 13.62% CAGR, enabling 75 kWh packs to reach approximately 80% state of charge in under 20 minutes and supporting high-turnover business models such as ride-hailing. Highway clusters along the Paris-Lyon-Marseille corridor reduce intercity travel times and support the use of electric trucks. The expanding network also anchors tourist flows toward Provence-Alpes-Côte d’Azur and Nouvelle-Aquitaine, where seasonal peaks once strained slower public chargers. Consequently, charging infrastructure diversity widens the market’s demographic reach while sustaining balanced growth.

Dynamic in-road wireless pilots on the A10 confirm the technical feasibility of continuous charging at highway speeds, though capital intensity delays large-scale deployment. AC remains the default for daily residential and workplace cycles, benefiting from lower tariffs and ample dwell time. At the same time, DC ultra-fast serves time-critical travel segments that demand quick turnarounds. New tariff structures that reward off-peak charging encourage users to split energy intake between slow overnight top-ups and rapid daytime boosts. Sustained roll-out of both technologies will underpin seamless nationwide coverage for the France electric vehicle market.

By End-Use: Shared Mobility Scales Fastest

Private Ownership retained a 78.88% share in 2025, buoyed by strong household demand in Île-de-France and Auvergne-Rhône-Alpes, where public charging density is significantly high. Corporate leasing fleets face quotas that climb to 70% low-emission share by 2030, propelling bulk orders for vans and pool cars. Government and municipal fleets accounted for 4.5%, driven by clean-air mandates covering taxis, refuse trucks, and public-service vehicles. Shared mobility is projected to grow fastest as app-based operators expand electric fleets to cut operating costs and qualify for city access perks. This mix demonstrates the market’s shift from early-adopter households to more diversified, utilization-heavy customer groups.

Ride-hailing platforms in Paris and Lyon offer electric-only booking options, attracting environmentally conscious passengers who are willing to pay a modest fare premium. Car-sharing schemes leverage discounted residential parking licenses and congestion charge exemptions, allowing fleets to scale profitably in high-density districts. Peer-to-peer rental apps add idle, privately owned EVs to the supply pool, boosting utilization rates and soaking up residual capacity. Government fleet commitments guarantee a robust secondary market for three- to five-year-old EVs, supporting residual values and lowering lease prices for subsequent owners. Together, these factors accelerate the transition toward service-based mobility models within the France electric vehicle market share landscape.

By Battery Capacity: Larger Packs Gain Share

Battery packs of 50–75 kWh held 49.04% share in 2025, balancing 350- to 450-kilometer range with price points near EUR 35,000 (USD 41,254) for mainstream buyers. Sub-EUR 30,000 (USD 35,360) models like the upcoming Renault 5 leverage lithium-iron-phosphate cells to position within this sweet spot. Packs above 75 kWh post a 13.61% CAGR as premium SUVs and executive sedans demand 550-kilometer ranges and rapid 250 kW charging capability. Cities with dense ultra-fast infrastructure, notably Paris and Marseille, exhibit higher uptake of these larger-capacity vehicles. The tiered battery landscape, therefore, aligns closely with regional income gradients and charging network maturity.

By 2027, ongoing innovations in cell chemistry are set to drive the cost of mid-range kWh packs below EUR 100 (USD 117.87) per kWh, solidifying their central role in the French electric vehicle market. OEMs are delving into high-manganese and semi-solid electrolyte formats, eyeing substantial energy-density boosts without the use of cobalt. In Île-de-France, premium buyers are opting for larger kWh packs, ideal for long-distance commutes and trips to second homes in Provence or Brittany. Meanwhile, micro-city cars equipped with smaller kWh packs cater to low-income, urban-centric users prioritizing sticker price over range. These micro-cars gain added traction from the EUR 100 (USD 117.87) monthly social-leasing program. This dynamic has birthed a three-tier capacity structure, adeptly aligning with France's varied mobility patterns.

Geography Analysis

Île-de-France captured the majority of 2025 registrations due to incomes significantly above the national median and over 25,000 public charging ports. Zero-emission zone mandates in Paris and the presence of abundant corporate headquarters create a virtuous cycle of private and fleet demand. Ultra-fast charger density supports high utilization among ride-hailing operators, while vehicle-to-grid pilots leverage the region’s tariff spreads. Auvergne-Rhône-Alpes benefits from electric power-train manufacturing clusters in Lyon and early adoption by local logistics fleets. High-altitude road networks around the Alps highlight the importance of range retention in cold conditions, prompting widespread installation of 150 kW chargers along the A43 and A48 motorways.

Provincial cities such as Grenoble incentivize curbside AC charging through discounted parking fees and expanded residential access. Provence-Alpes-Côte d’Azur's share is driven by tourist traffic and solar-rich grids that align with daytime charging economics. Coastal highway corridors host dense ultra-fast hubs, enabling long-range trips into neighboring Spain and Italy. Municipal fleet electrification in Marseille and Nice anchors public demand, while high solar generation creates intraday price volatility, maximizing vehicle-to-grid earnings.

Hauts-de-France, Nouvelle-Aquitaine, and Occitanie together accounted for 25% of volume, aided by ADVENIR-funded highway corridors yet constrained by rural charging gaps. Bretagne and Normandie lagged at under 10% combined share, reflecting low charger deployment in sparsely populated cantons. Targeted public funding schemes and community energy cooperatives aim to close these regional disparities and unlock consistent nationwide growth of the French electric vehicle market.

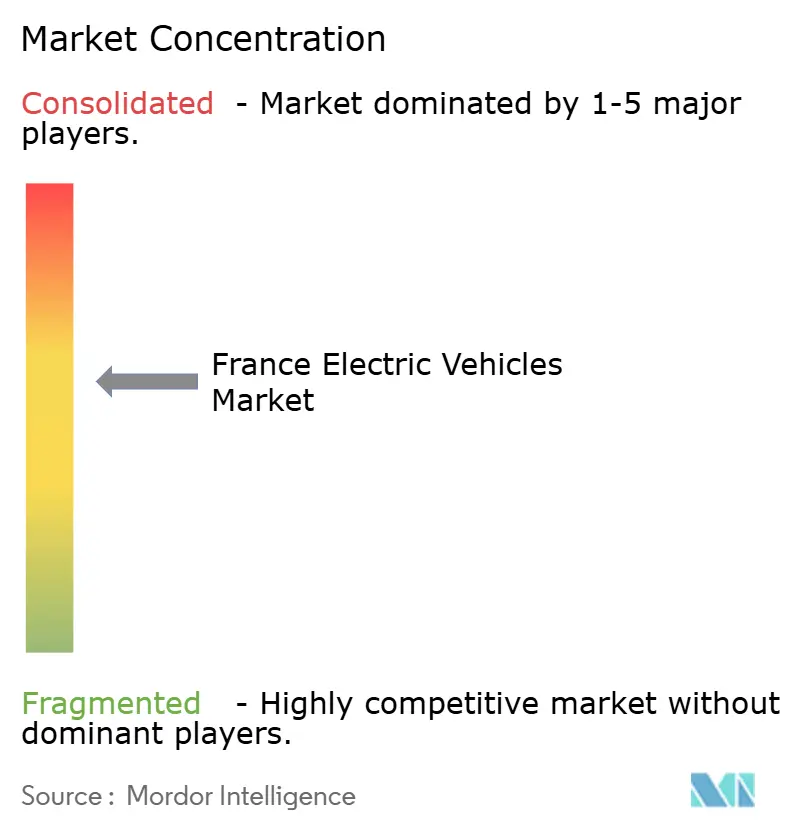

Competitive Landscape

The France electric vehicle market exhibits moderate concentration, yet this oligopoly faces erosion from Chinese entrants BYD and MG Motor (SAIC), which rank France as their third-largest destination. Domestic leaders hold strong but face sharper import rivalry. Renault Group sold 277,297 electric units domestically in 2024 on the back of the Renault 5 and Megane E-Tech lines. Stellantis placed 452,900 electrified models across Peugeot, Citroën, and DS, and invested EUR 1.5 billion (~USD 1.7 billion) in Leapmotor International to accelerate the development of low-cost platforms.

Tesla sustains brand equity but trims margins through price cuts to defend share. Volkswagen and Hyundai trail domestic incumbents due to limited France-specific production, opening room for challengers. Chinese brands BYD and MG Motor evaluate domestic assembly sites, leveraging cost-competitive models to chip away at the premium defined by import duties.

White-space opportunities cluster below EUR 25,000 (USD 29,467), where only two high-volume models compete, and in passenger fuel-cell cars, where no mainstream entries exist. Technology differentiation now centers on bidirectional charging; Renault’s Mobilize offers certified vehicle-to-grid services, a feature absent from Tesla’s French line-up. Compliance with ISO 15118-20 from 2027 will level the technical playing field and reward OEMs that accelerate integration across model ranges.

France Electric Vehicles Industry Leaders

-

Volkswagen AG

-

Renault S.A.

-

Tesla Inc.

-

Hyundai Motor Group

-

Stellantis N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: France inaugurated a 1.5-kilometer dynamic wireless charging pilot on the A10 motorway, enabling trucks to charge at highway speed.

- June 2025: Polestar entered France, making its complete battery-electric portfolio available to local consumers.

- May 2025: Nissan unveiled the fully electric sixth-generation Micra, reviving a popular B-segment nameplate for European buyers.

- January 2025: Kempower partnered with Mobilize to deploy fast DC hubs near Renault dealerships and highway routes across France.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the France electric vehicles market as the annual value generated from new battery-electric, plug-in hybrid, and fuel-cell cars and commercial vehicles that are registered for on-road use in mainland France. It captures factory-gate revenue and, where that is not disclosed, recalculates ex-factory value from average transaction data that Mordor analysts standardize to constant 2024 USD.

Scope Exclusion: Low-speed two-wheelers, off-highway machinery, and stand-alone charging equipment are outside the frame of this analysis.

Segmentation Overview

-

By Propulsion Type

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Fuel-Cell Electric Vehicles (FCEV)

-

By Vehicle Type

-

Passenger Cars

- Hatchback

- Sedan

- SUV (Sports Utility Vehicle)

- MUV (Multi Utility Vehicle)

-

Commercial Vehicles

- Light Commercial Vehicles (LCV)

- Heavy Trucks

- City & Inter-city Buses

-

Passenger Cars

-

By Charging Type

- AC (greater than equals) 22 kW (Normal)

- DC 22-150 kW (Fast)

- DC Less than 150 kW (Ultra-fast)

-

By End-use

- Private Ownership

- Corporate & Leasing Fleets

- Government & Municipal Fleets

- Shared Mobility (Car-share/Ride-hail)

-

By Battery Capacity

- Less than 50 kWh

- 50-75 kWh

- Above 75 kWh

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview French dealer groups, fleet-leasing managers, grid planners, and battery recyclers across Ile-de-France, Auvergne-Rhone-Alpes, and Nouvelle-Aquitaine. The conversations supply fresh insight on retail mark-ups, charger availability, and expected incentive cuts, which we merge with a short online survey of prospective EV buyers to refine elasticity assumptions.

Desk Research

We begin by mapping the universe of vehicles and regulatory triggers through freely available tier-one sources such as Eurostat new-car registrations, the French Ministry for Ecological Transition's CO2 database, International Energy Agency EV stock tables, and ACEA quarterly fuel-type dashboards. Company filings, investor decks, and press releases reveal OEM launch calendars, battery sourcing plans, and indicative average selling prices, which are then validated through D&B Hoovers and Dow Jones Factiva queries. Trade flows for lithium-ion packs are reconstructed from Volza shipment data to gauge import dependence. These materials anchor our historical demand curve and price ladder.

Macroeconomic series, household disposable income, electricity tariffs, and Brent-linked fuel costs are collected from INSEE, CRE, and EIA respectively, helping us explain switching incentives. The examples above are illustrative; many additional open and subscription sources inform data collection, sense-checks, and clarification.

Market-Sizing & Forecasting

A top-down model starts with annual light-vehicle sales and stock, then applies propulsion-specific penetration rates, average battery capacities, and calibrated ASPs to derive revenue pools. Select bottom-up checks, supplier roll-ups for the five leading OEM plants and sampled dealer invoices, test reasonableness and flag gaps before totals are adjusted. Key variables tracked include bonus ecologique amounts, charger density per 1,000 inhabitants, battery pack $/kWh, and petrol-diesel price spreads. Forward projections use a multivariate regression blended with ARIMA to capture both structural policy shifts and short-term macro shocks, with scenario adjustments from expert consensus when incentives change mid-cycle. Missing inputs are filled through weighted interpolation from contiguous years and comparable cohorts.

Data Validation & Update Cycle

Every draft passes a two-step analyst review: statistical outlier detection followed by variance cross-checks against independent datasets. Material deviations trigger a call-back to at least one earlier respondent. We refresh the model each year and issue interim updates within four weeks of major policy announcements.

Why Our France Electric Vehicles Baseline Commands Reliability

Published estimates differ because firms choose dissimilar scopes, discount rates, and refresh cadences.

Key gap drivers include whether chargers are bundled with vehicles, the treatment of fleet leasing revenue, exchange-rate timing, and how aggressively scrap-age profiles are applied to forecast sales replacement.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 34.17 B (2025) | Mordor Intelligence | - |

| USD 40.03 B (2024) | Global Consultancy A | Includes chargers and two-wheelers; relies on list prices without ASP normalization |

| USD 21.56 B (2025) | Regional Consultancy B | Omits commercial vehicles and uses conservative bonus ecologique sunset scenario |

| USD 14.20 B (2023) | Industry Databook C | Counts only passenger cars and reports pre-tax factory revenue |

Taken together, the comparison shows that when scope, incentives, and pricing are aligned in a disciplined way, Mordor's balanced approach produces a dependable baseline that decision-makers can trace to transparent variables and repeatable steps.

Key Questions Answered in the Report

How large was the France electric vehicle market in 2025?

In 2025, the French electric vehicle market reached a size of USD 30.56 billion.

Which vehicle type is growing fastest in France?

Heavy trucks post the highest growth, advancing at a 17.03% CAGR as freight operators respond to low-emission zone rules.

What share do battery electric cars hold?

Battery electric vehicles accounted for 67.65% of registrations in 2025, far ahead of plug-in hybrids and fuel-cell models.

How many public chargers does France have?

The network exceeded 147,000 ports in late 2025, with ultra-fast units above 150 kW expanding rapidly along major highways.

Page last updated on: