Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.30 Billion |

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 2.85 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France E-Bike Market Analysis by Mordor Intelligence

The France e-bike market size is expected to grow from USD 2.30 billion in 2025 to USD 2.38 billion in 2026 and is forecast to reach USD 2.85 billion by 2031 at 3.62% CAGR over 2026-2031. Resilient growth reflects sustained government infrastructure spending, generous purchase subsidies, and rising urban mobility demand. Policy support under the Plan Vélo 2023-2027, coupled with the country’s status as Europe’s third-largest e-bike market, underpins long-term volume stability despite post-pandemic volatility [1]“Plan Vélo 2023-2027,” Ministère de l’Économie, economie.gouv.fr. Premiumization strengthens margins as affluent riders gravitate toward mid-drive systems and belt drives, while logistics firms accelerate cargo e-bike fleet roll-outs to comply with tightening emission rules. Declining lithium-ion battery costs broaden access, although supply-chain dependence on Asian cell suppliers poses a lingering risk. Competitive intensity is shaped by EU anti-dumping duties on Chinese imports, protecting domestic makers but capping low-price segment growth.

Key Report Takeaways

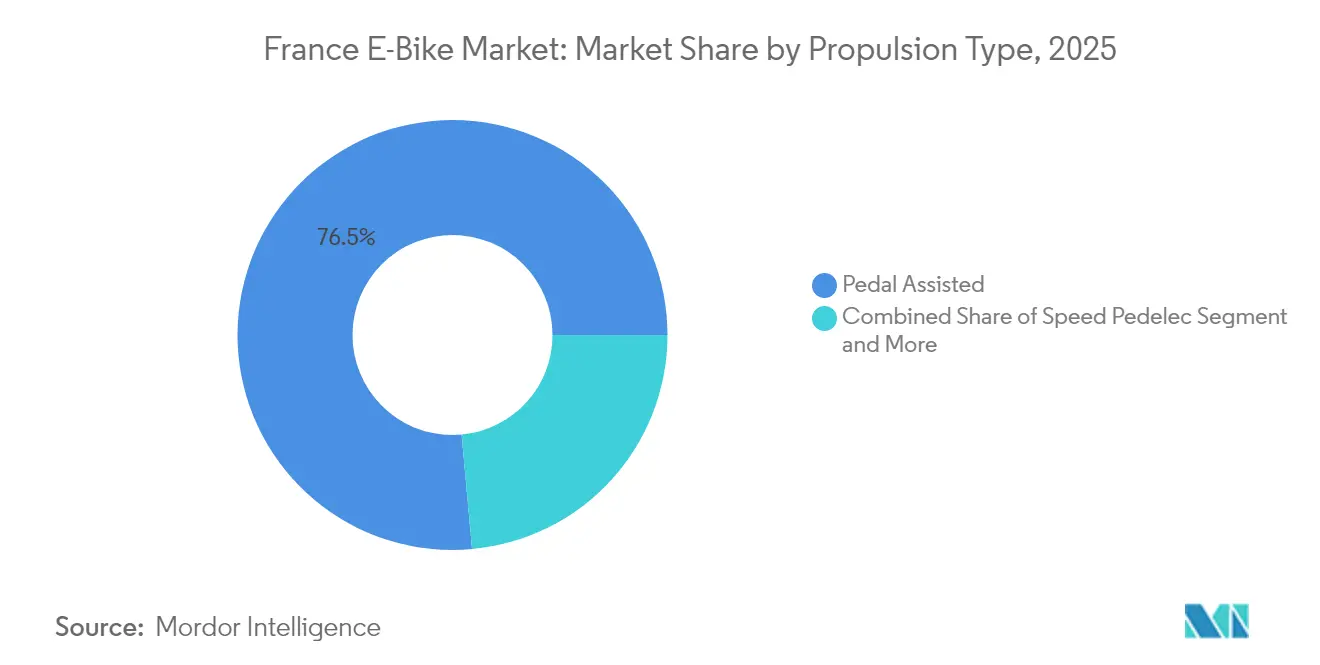

- By propulsion type, pedal-assisted systems led with a 76.45% France e-bike market share in 2025, while speed-pedelecs post the fastest 3.74% CAGR through 2031.

- By application type, city/urban use captured 76.02% share of the France e-bike market size in 2025; cargo/utility is advancing at a 3.76% CAGR to 2031.

- By battery type, lithium-ion batteries controlled 100.00% of the France e-bike market share in 2025, growing in lockstep with the overall 3.62% CAGR outlook.

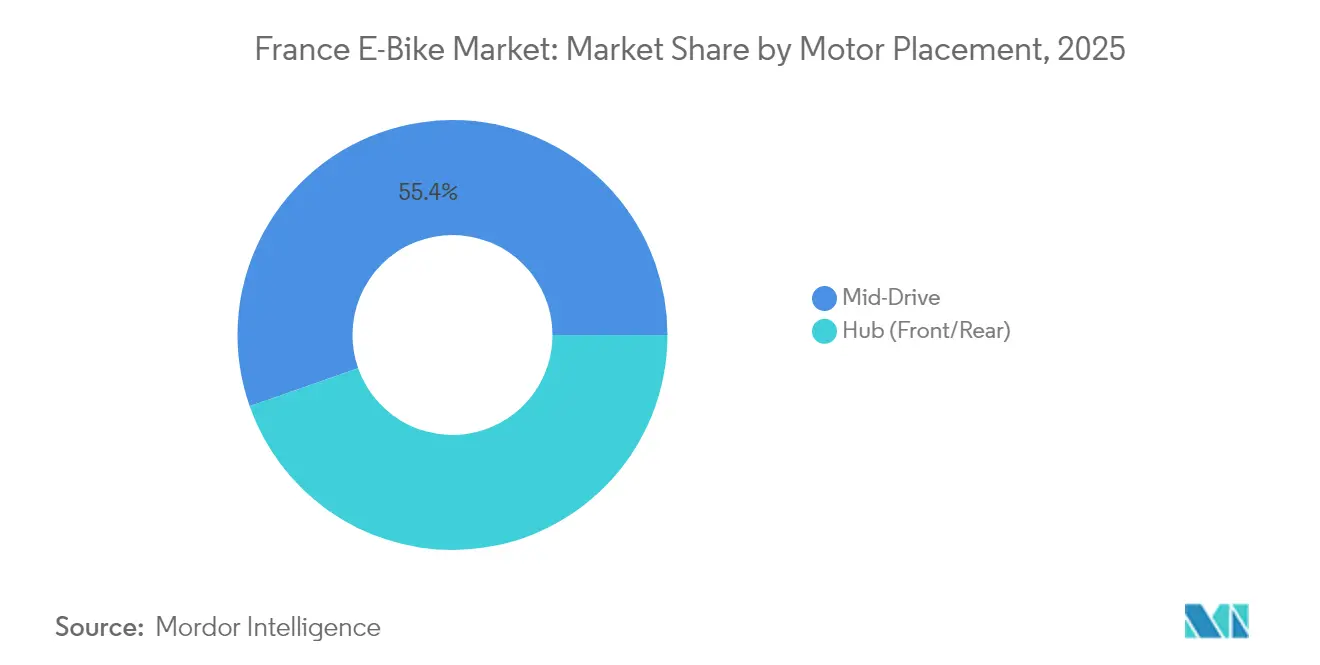

- By motor placement, mid-drive motors accounted for 55.38% of the France e-bike market size in 2025 and will rise at a 3.98% CAGR through 2031.

- By drive systems, chain drives captured 83.60% in 2025, while belt drives are projected to expand at a 5.07% CAGR, outpacing chain drives.

- By motor power, below 250 W segment controlled 88.12% share in 2025, while 501-600 W will lead growth at a 5.71% CAGR thanks to cargo and performance uses.

- By price band, USD 1,500-2,499 band held 31.84% share of the France e-bike market size in 2025, whereas the USD 3,500-5,999 band is the fastest riser at 4.42% CAGR.

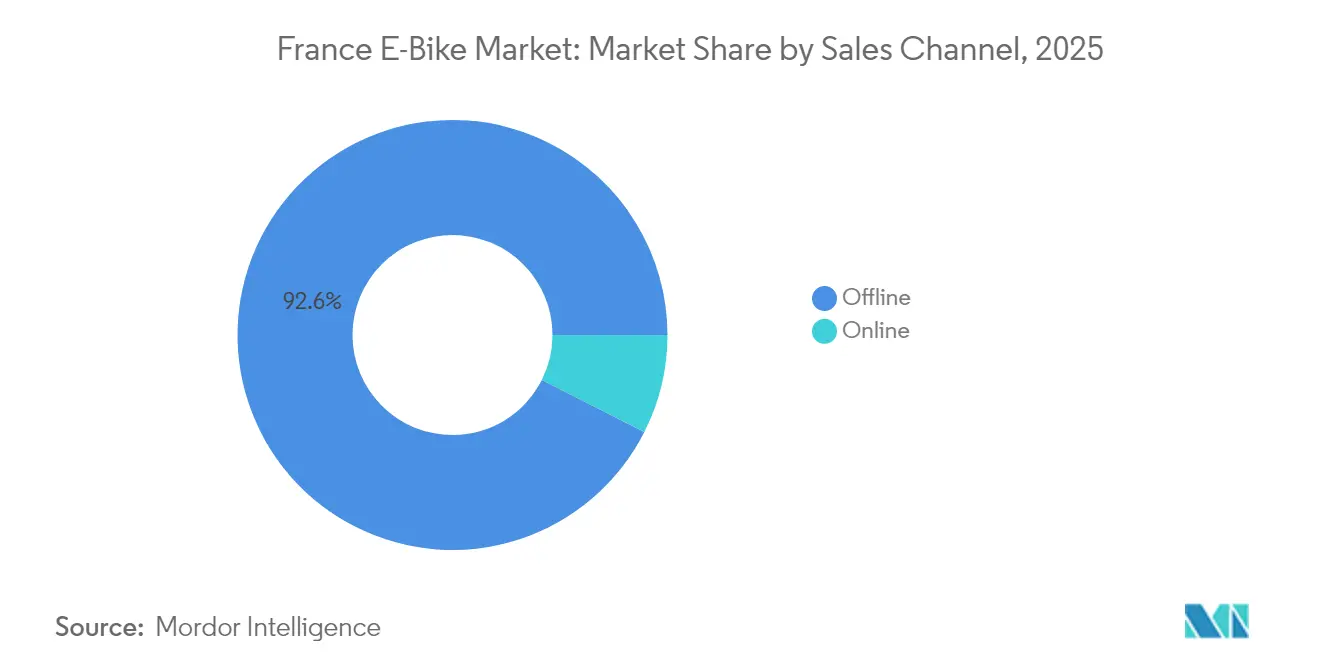

- By sales channel, offline retail dominated 92.55% of the France e-bike market share in 2025, although online sales record a 6.74% CAGR.

- By end use, personal and family use retained 66.88% share in 2025, but commercial delivery fleets expand quickest at a 5.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France E-Bike Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cycling Plan (2023-2027) | +0.8% | National—metro focus | Medium term (2-4 years) |

| Declining Battery Pack Prices | +0.7% | Global supply—national demand | Medium term (2-4 years) |

| Purchase Subsidies and Tax Incentives | +0.6% | National—urban skew | Short term (≤ 2 years) |

| Corporate Fleet Decarbonization Mandates | +0.5% | Urban logistics zones | Medium term (2-4 years) |

| Rapid Growth of Leasing | +0.4% | Nationwide | Short term (≤ 2 years) |

| Integration of Batteries into V2G Schemes | +0.3% | Pilot smart-grid areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Cycling Plan 2023-2027 (EUR 2 B Infrastructure Push)

France is investing EUR 2 billion (~USD 2.3 billion) to extend protected cycling lanes from 57,000 km to 80,000 km by 2027, a network upgrade forecast to expand cycling’s modal share by 2030. Enhanced infrastructure is improving perceived safety, particularly among risk-averse groups. Women are increasingly becoming a significant segment of e-bike purchasers, showcasing a notable shift in consumer demographics over time. Premium e-bikes that maximize range and comfort benefit disproportionately because longer, safer routes make daily commuting feasible. Intermodal links to rail hubs heighten utility, sustaining ridership even after subsidies expire. The program synchronizes with new urban developments, embedding long-term demand anchors that stabilize the France e-bike market.

Declining Battery Pack Prices (Below EUR 300 for 500 Wh by 2027)

Global cell prices fell 14% year-on-year in 2024, and scale economies should drive them below by 2027 [2]“Global EV Outlook 2024,” International Energy Agency, iea.org. Since batteries make up 30-40% of bill-of-materials, every 10% cost cut can unlock fresh demand without sacrificing margins. Entry-level bikes become more attainable, while premium brands channel savings into connectivity and smart-system upgrades. Cost deflation counterbalances subsidy tapering, ensuring that total cost of ownership keeps trending downward for the France e-bike market.

Purchase Subsidies and Tax Incentives up to EUR 1,500

National and regional rebates trim sticker prices, while the Forfait Mobilités Durables lets employers deliver a tax-free mobility credit per worker. Income-based rules segment demand: lower-income buyers access basic models, whereas affluent commuters use partial subsidies to upgrade to mid-drive or belt-drive systems. Corporate buyers witness notable tax reductions on financed fleets, propelling the USD 3,500-5,999 segment. Uptake is densest in Île-de-France, where richer subsidies overlap with robust infrastructure, creating clustered pockets of high France e-bike market penetration.

Corporate Fleet Decarbonization Mandates (Urban Logistics)

EU emissions caps and city-center vehicle bans compel couriers to adopt cargo e-bikes, whose delivery costs are lower than diesel vans. Paris has implemented subsidies to support the adoption of professional cargo bikes. At the national level, the popularity of cargo e-bikes has significantly increased in recent years. Demonstrating the potential for scalability, operators such as Les Cargonautes now utilize an all-electric fleet of Douze Cycles bikes, catering to a growing number of riders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Asian Supply | -0.4% | Nationwide | Medium term (2-4 years) |

| EU Anti-Dumping Duties on Bikes | -0.3% | Nationwide | Medium term (2-4 years) |

| Fire-Safety Concerns in Housing | -0.3% | Urban high-rise zones | Short term (≤ 2 years) |

| Price Sensitivity and Secondhand Drift | -0.2% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Asian Battery and Motor Supply Chain

China is the dominant producer of e-bike battery cells globally, putting French assemblers at risk of geopolitical disruptions and shipping delays, especially through the Strait of Malacca. EU anti-dumping duties shield final-bike assembly but raise input costs, inflating domestic manufacturing expenses above Chinese competitors. Paris has seeded a significant fund to localize component production, yet scale parity will take years. In the interim, volatility in freight rates and currency can squeeze margins and slow budget-segment expansion, trimming France e-bike market CAGR.

EU Anti-Dumping Duties on Low-End Chinese E-Bikes

Tariffs on Chinese imports, extended through the mid-term, aim to curb predatory pricing but inadvertently alienate budget-conscious consumers. While these measures provide domestic companies with opportunities to expand, smaller retailers face challenges due to limited access to discounted inventory that could have encouraged new customers. This balance between protecting local businesses and ensuring affordability has slightly impacted the growth trajectory of France e-bike market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Pedal-assist stability with speed-pedelec upside

Pedal-assist models dominated the France e-bike market with 76.45% share in 2025. Regulatory simplicity keeps uptake high as riders enjoy cycle-path access without insurance hassles. Speed-pedelecs grow at 3.74% CAGR, fueled by rural commuters seeking faster journeys. The France e-bike market share of throttle-assist remains negligible because non-pedal activation triggers moped regulation. Over time, policy tweaks that ease speed-pedelec infrastructure access could unlock further upside, especially if employers reimburse longer intercity commutes.

Consumer surveys indicate that first-time buyers often choose pedal-assist for its health benefits, while many consider regulatory ease a significant factor. Speed-pedelecs appeal to performance enthusiasts ready to accept helmet and registration requirements in exchange for 45 km/h top speeds. Specialized dealers bundle insurance and training packages, mitigating compliance friction. If speed-pedelec volumes grow further by 2031, they could nudge the France e-bike market toward higher average selling prices and encourage manufacturers to develop modular frames that accept both propulsion modes.

By Application Type: Urban leadership, cargo surge

City/urban bikes held 76.02% of the France e-bike market size in 2025 and continue to command a significant volume thanks to dense metropolitan commuting needs. Based on corporate fleet decarbonization mandates, cargo/utility models are set to rise 3.76% by 2031. Trekking and mountain e-bikes leverage France’s vast tourism assets yet remain seasonal.

Urban riders prioritize low-maintenance drivetrains and theft-proof locking, prompting OEMs to integrate GPS trackers and belt drives. Cargo bike makers refine frame ergonomics and capacity, responding to grocers and parcel firms. Municipal subsidies covering a notable share of cargo-bike cost supercharge adoption. Trekking models benefit from battery capacities exceeding 750 Wh, enabling multi-day tours along the Loire à Vélo route and thereby expanding geographic reach of the France e-bike market.

By Battery Type: Lithium-ion hegemony amid green compliance

Lithium-ion chemistry holds 100% France e-bike market share and mirrors the 3.62% headline CAGR. EU Regulation 2023/1542 demands recycled content declarations from 2027, compelling brands to adopt easy-swap pack designs. Standardization around certain battery modules balances range and weight. The France e-bike market size for batteries will gain from falling cell costs, yet recyclability expenses offset some margin relief.

Safety-focused LFP packs, known for being more affordable than NMC, are gaining traction in new shipments. OEMs market LFP’s thermal stability to apartment dwellers wary of fires. Digital battery passports boost residual values by verifying cycle counts, a win for the burgeoning second-hand segment.

By Motor Placement: Mid-drive premium edge

Mid-drive units represented 55.38% share of the France e-bike market size in 2025 and expand at 3.98% CAGR, outpacing rear hubs. Weight centralized at the bottom bracket improves handling on narrow Parisian streets, justifying higher prices. Hub motors stick to entry-level and rental fleets where simplicity trumps torque finesse.

Bosch’s Smart System and Shimano’s EP8 integrate OTA diagnostics, lifting perceived value. As mid-drive component costs fall annually, uptake in the USD 1,500-2,499 bracket rises, balancing performance with affordability. Nevertheless, front hubs stay relevant for conversion kits, maintaining a foothold in the France e-bike market.

By Drive Systems: Chain legacy versus belt innovation

Chains still dominated 83.60% of 2025 volume, yet belt systems will climb 5.07% by 2031. Couriers cherish grease-free belts that cut downtime, while commuters welcome silent running. Despite higher upfront costs, Gates Carbon Drive emphasizes its significantly longer service intervals compared to traditional chains, making the total cost of ownership (TCO) appealing.

OEMs offer belt upgrades bundled with internal gear hubs, appealing to riders fatigued by derailleur tuning. If belt drives grow further by 2031, aftermarket service shops must adapt skillsets, a subtle but meaningful shift in the France e-bike market ecosystem.

By Motor Power: 250 W norm under legal cap

Sub-250 W bikes captured 88.12% France e-bike market share in 2025, safeguarded by bicycle legal status. The 501-600 W tier, pivotal for cargo loads, posts 5.71% CAGR. Brands design torque-limiting software so higher-power motors comply with speed limits, avoiding reclassification.

Paris may allow heavier cargo bikes in specific lanes, spurring demand for 600 W setups. Conversely, proposals to raise the 250 W cap remain politically sensitive due to safety debates. Thus, power segmentation will retain its dual-track nature.

By Price Band: Mid-range volume, premium value

Bikes priced USD 1,500-2,499 secured 31.84% France e-bike market share in 2025. Leasing schemes cap monthly outlays, supporting this sweet spot. The USD 3,500-5,999 tier logs 4.42% CAGR as riders chase integrated lighting, ABS brakes, and connectivity. Sub-USD 1,499 volumes erode under tariff-inflated costs and second-hand competition.

Dealers push subscription models, bundling maintenance, and keeping residuals high. If battery costs keep sliding, OEMs may hold sticker prices steady while adding smart-system features, lifting perceived value without eroding margins.

By Sales Channel: Bricks first, clicks rising

Offline outlets handled 92.55% of 2025 unit sales. Buyers often insist on test rides and on-site fittings for premium purchases. Nevertheless, online brands such as Canyon are experiencing significant growth, fueling a 6.74% CAGR for e-commerce. Hybrid paths emerge: web orders ship to local dealers for assembly, preserving service revenue while broadening reach.

Click-and-collect mitigates shipping damage risks and builds long-term customer relations through scheduled maintenance plans. As warranty complexity grows with smart components, omnichannel models will dominate the France e-bike market.

By End Use: Personal lead, delivery sprint

Personal-use bikes captured 66.88% of the France e-bike market size in 2025. Daily commuters and recreational cyclists value subsidy offsets and hassle-free parking. Commercial delivery fleets, while smaller, book a 5.39% CAGR as emission zones tighten. Operators are experiencing short payback periods due to savings on fuel and parking.

Service companies, from mobile mechanics to street-food vendors, explore e-bike platforms, diversifying commercial demand. Municipalities test cargo e-bike sharing for waste collection, hinting at fresh institutional end-use cases by 2031.

Geography Analysis

France demonstrates notable activity in the European e-bike market. However, e-bike adoption in France remains relatively lower than in other countries, indicating substantial growth potential for the French e-bike market. Urban clusters such as Île-de-France, Auvergne-Rhône-Alpes, and Provence-Alpes-Côte d’Azur capture a notable share of national sales thanks to dense infrastructure and higher regional subsidies. Paris alone supports over 1,000 km of protected lanes, a magnet for commuters shifting from métro to pedals.

Regional disparities persist: Grand Est and Hauts-de-France lag due to lower purchasing power and fewer safe routes. Targeted funds in the Plan Vélo aim to bridge this gap, potentially adding 8,000 km of lanes prioritizing provincial and rural areas by 2027. Tourism hotspots, the Loire Valley, Burgundy wine trails, and Alpine resorts record surging rental demand, adding seasonal spikes that smooth factory order books.

Cross-border supply flows from Belgium and Germany simplify component sourcing for northern assemblers, whereas Mediterranean plants lean on port deliveries from Asia. Logistics proximity subtly shapes manufacturing clusters, reinforcing the geographic mosaic that defines the France e-bike market.

Competitive Landscape

France's e-bike market is moderately fragmented, with several brands achieving significant annual sales volumes. Moustache Bikes, O2feel, and Reine Bike are prominent players in domestic production, though their combined market share remains relatively limited. German heavyweights Riese & Müller and KTM exploit scale to span price bands, while Taiwanese-owned Giant leverages global sourcing to defend mid-range niches.

Trade barriers on Chinese finished bikes shift competition toward quality rather than price. OEMs differentiate via software: Bosch’s flow-app diagnostics, Valeo’s integrated gearbox-motor Cyclee™, and Yamaha’s automatic-assist modes [3]“Cyclee Product Announcement,” Valeo, valeo.com. Sustainability claims become challenging requirements as EU battery passports loom, a compliance hurdle favoring capital-rich incumbents.

Consolidation whispers grow louder; some smaller French assemblers are eyeing joint purchasing cooperatives to counter input price swings. Dealers also consolidate, with Accell-owned Veloland expanding its network. In essence, brand equity, after-sales reach, and regulatory readiness now outweigh cheap hardware in shaping success within the French e-bike market.

France E-Bike Industry Leaders

Giant Manufacturing Co. Ltd.

CYCLE ME (Moustache Bikes)

Decathlon S.A.

Trek Bicycle Corporation

Lapierre SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Voi Technology won a Paris tender to deploy 6,000 shared e-bikes, the largest contract in its history, highlighting municipal faith in shared micromobility.

- June 2025: Valeo confirmed it will unveil Cyclee™ powertrains at Eurobike 2025, underscoring growing automotive cross-overs into premium e-bike systems.

France E-Bike Market Report Scope

Pedal Assisted, Speed Pedelec, Throttle Assisted are covered as segments by Propulsion Type. Cargo/Utility, City/Urban, Trekking are covered as segments by Application Type. Lead Acid Battery, Lithium-ion Battery, Others are covered as segments by Battery Type.By Propulsion Type

| Pedal Assisted |

| Speed Pedelec |

| Throttle Assisted |

By Application Type

| Cargo/Utility |

| City/Urban |

| Trekking/Mountain |

By Battery Type

| Lead Acid Battery |

| Lithium-ion Battery |

| Others |

By Motor Placement

| Hub (Front/Rear) |

| Mid-Drive |

By Drive Systems

| Chain Drive |

| Belt Drive |

By Motor Power

| Below 250 W |

| 251-350 W |

| 351-500 W |

| 501-600 W |

| Above 600 W |

By Price Band

| Up to USD 1,000 |

| USD 1,000-1,499 |

| USD 1,500-2,499 |

| USD 2,500-3,499 |

| USD 3,500-5,999 |

| Above USD 6,000 |

By Sales Channel

| Online |

| Offline |

By End Use

| Commercial Delivery | Retail and Goods Delivery |

| Food and Beverage Delivery | |

| Service Providers | |

| Personal and Family Use | |

| Institutional | |

| Others |

| By Propulsion Type | Pedal Assisted | |

| Speed Pedelec | ||

| Throttle Assisted | ||

| By Application Type | Cargo/Utility | |

| City/Urban | ||

| Trekking/Mountain | ||

| By Battery Type | Lead Acid Battery | |

| Lithium-ion Battery | ||

| Others | ||

| By Motor Placement | Hub (Front/Rear) | |

| Mid-Drive | ||

| By Drive Systems | Chain Drive | |

| Belt Drive | ||

| By Motor Power | Below 250 W | |

| 251-350 W | ||

| 351-500 W | ||

| 501-600 W | ||

| Above 600 W | ||

| By Price Band | Up to USD 1,000 | |

| USD 1,000-1,499 | ||

| USD 1,500-2,499 | ||

| USD 2,500-3,499 | ||

| USD 3,500-5,999 | ||

| Above USD 6,000 | ||

| By Sales Channel | Online | |

| Offline | ||

| By End Use | Commercial Delivery | Retail and Goods Delivery |

| Food and Beverage Delivery | ||

| Service Providers | ||

| Personal and Family Use | ||

| Institutional | ||

| Others | ||

Market Definition

- By Application Type - E-bikes considered under this segment include city/urban, trekking, and cargo/utility e-bikes. The common types of e-bikes under these three categories include off-road/hybrid, kids, ladies/gents, cross, MTB, folding, fat tire, and sports e-bike.

- By Battery Type - This segment includes lithium-ion batteries, lead-acid batteries, and other battery types. The other battery type category includes nickel-metal hydroxide (NiMH), silicon, and lithium-polymer batteries.

- By Propulsion Type - E-bikes considered under this segment include pedal-assisted e-bikes, throttle-assisted e-bikes, and speed pedelec. While the speed limit of pedal and throttle-assisted e-bikes is usually 25 km/h, the speed limit of speed pedelec is generally 45 km/h (28 mph).

| Keyword | Definition |

|---|---|

| Pedal Assisted | Pedal-assist or pedelec category refers to the electric bikes that provide limited power assistance through torque-assist system and do not have throttle for varying the speed. The power from the motor gets activated upon pedaling in these bikes and reduces human efforts. |

| Throttle Assisted | Throttle-based e-bikes are equipped with the throttle assistance grip, installed on the handlebar, similarly to motorbikes. The speed can be controlled by twisting the throttle directly without the need to pedal. The throttle response directly provides power to the motor installed in the bicycles and speeds up the vehicle without paddling. |

| Speed Pedelec | Speed pedelec is e-bikes similar to pedal-assist e-bikes as they do not have throttle functionality. However, these e-bikes are integrated with an electric motor which delivers power of approximately 500 W and more. The speed limit of such e-bikes is generally 45 km/h (28 mph) in most of the countries. |

| City/Urban | The city or urban e-bikes are designed with daily commuting standards and functions to be operated within the city and urban areas. The bicycles include various features and specifications such as comfortable seats, sit upright riding posture, tires for easy grip and comfortable ride, etc. |

| Trekking | Trekking and mountain bikes are special types of e-bikes that are designed for special purposes considering the robust and rough usage of the vehicles. These bicycles include a strong frame, and wide tires for better and advanced grip and are also equipped with various gear mechanisms which can be used while riding in different terrains, rough grounded, and tough mountainous roads. |

| Cargo/Utility | The e-cargo or utility e-bikes are designed to carry various types of cargo and packages for shorter distances such as within urban areas. These bikes are usually owned by local businesses and delivery partners to deliver packages and parcels at very low operational costs. |

| Lithium-ion Battery | A Li-ion battery is a rechargeable battery, which uses lithium and carbon as its constituent materials. The Li-Ion batteries have a higher density and lesser weight than sealed lead acid batteries and provide the rider with more range per charge than other types of batteries. |

| Lead Acid Battery | A lead acid battery refers to sealed lead acid battery having a very low energy-to-weight and energy-to-volume ratio. The battery can produce high surge currents, owing to its relatively high power-to-weight ratio as compared to other rechargeable batteries. |

| Other Batteries | This includes electric bikes using nickel–metal hydroxide (NiMH), silicon, and lithium-polymer batteries. |

| Business-to-Business (B2B) | The sales of e-bikes to business customers such as urban fleet and logistics company, rental/sharing operators, last-mile fleet operators, and corporate fleet operators are considered under this category. |

| Business-to-Customers (B2C) | The sales of electric scooters and motorcycles to direct consumers is considered under this category. The consumers acquire these vehicles either directly from manufacturers or from other distributers and dealers through online and offline channel. |

| Unorganized Local OEMs | These players are small local manufacturers and assemblers of e-bikes. Most of these manufacturers import the components from China and Taiwan and assemble them locally. They offer the product at low cost in this price sensitive market which give them advantage over organized manufacturers. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Dockless e-Bikes | Electric bikes that have self-locking mechanisms and a GPS tracking facility with an average top speed of around 15mph. These are mainly used by bike-sharing companies such as Bird, Lime, and Spin. |

| Electric Vehicle | A vehicle which uses one or more electric motors for propulsion. Includes cars, scooters, buses, trucks, motorcycles, and boats. This term includes all-electric vehicles and hybrid electric vehicles |

| Plug-in EV | An electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. In this report we use the term for all-electric vehicles to differentiate them from plug-in hybrid electric vehicles. |

| Lithium-Sulphur Battery | A rechargeable battery that replaces the liquid or polymer electrolyte found in current lithium-ion batteries with sulfur. They have more capacity than Li-ion batteries. |

| Micromobility | Micromobility is one of the many modes of transport involving very-light-duty vehicles to travel short distances. These means of transportation include bikes, e-scooters, e-bikes, mopeds, and scooters. Such vehicles are used on a sharing basis for covering short distances, usually five miles or less. |

| Low Speed Electric Vehicls (LSEVs) | They are low speed (usually less than 25 kmph) light vehicles that do not have an internal combustion engine, and solely use electric energy for propulsion. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms