Spain Data Center Water Consumption Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

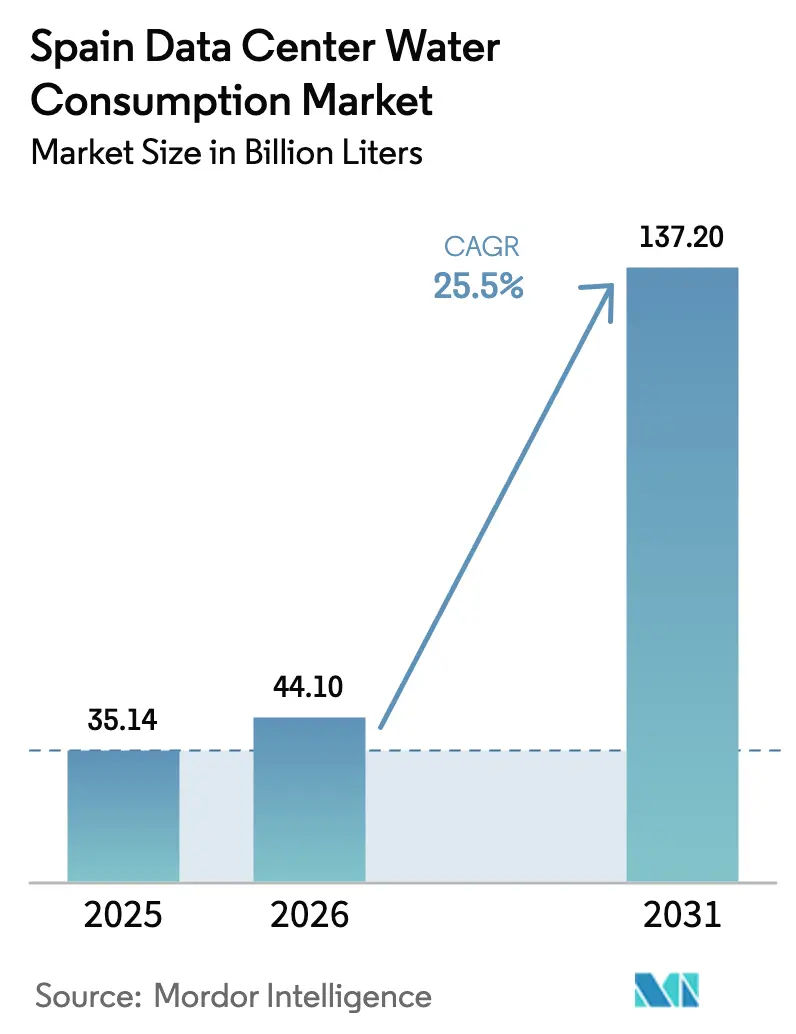

| Base Year Market Size (2025) | 35.14 Billion liters |

| Market Volume (2026) | 44.1 Billion liters |

| Market Volume (2031) | 137.2 Billion liters |

| Growth Rate (2026 - 2031) | 25.50% CAGR |

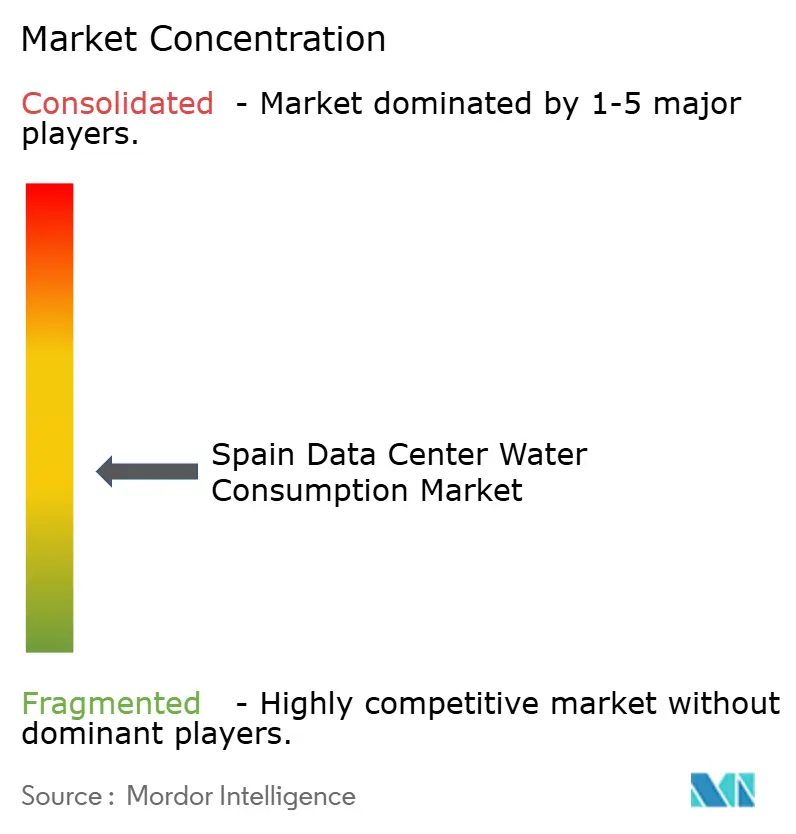

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Data Center Water Consumption Market Analysis by Mordor Intelligence

Spain data center water consumption market size in 2026 is estimated at 44.1 billion liters, growing from 2025 value of 35.14 billion liters with 2031 projections showing 137.2 billion liters, growing at 25.50% CAGR over 2026-2031. The expansion corresponds with Spain’s rapid digitalization, the proliferation of AI workloads, and the country’s growing role as an inter-regional connectivity hub. Operators now weigh conventional chilled-water systems against water-lean alternatives under a regulatory and societal backdrop of mounting water scarcity. Multinational cloud providers, scaling out in Madrid, Barcelona, and Aragon, add further momentum while simultaneously pledging aggressive water-positivity goals. Supply-side innovation—from grey-water reuse to on-site desalination, coupled with fiscal nudges such as progressive water tariffs, is repositioning water stewardship as both a compliance imperative and a source of long-term cost advantage across the Spain data center water consumption market.[1]Comunidad de Madrid, "La Comunidad de Madrid actualiza las tarifas.", Comunidad de Madrid, comunidad.madrid

Key Report Takeaways

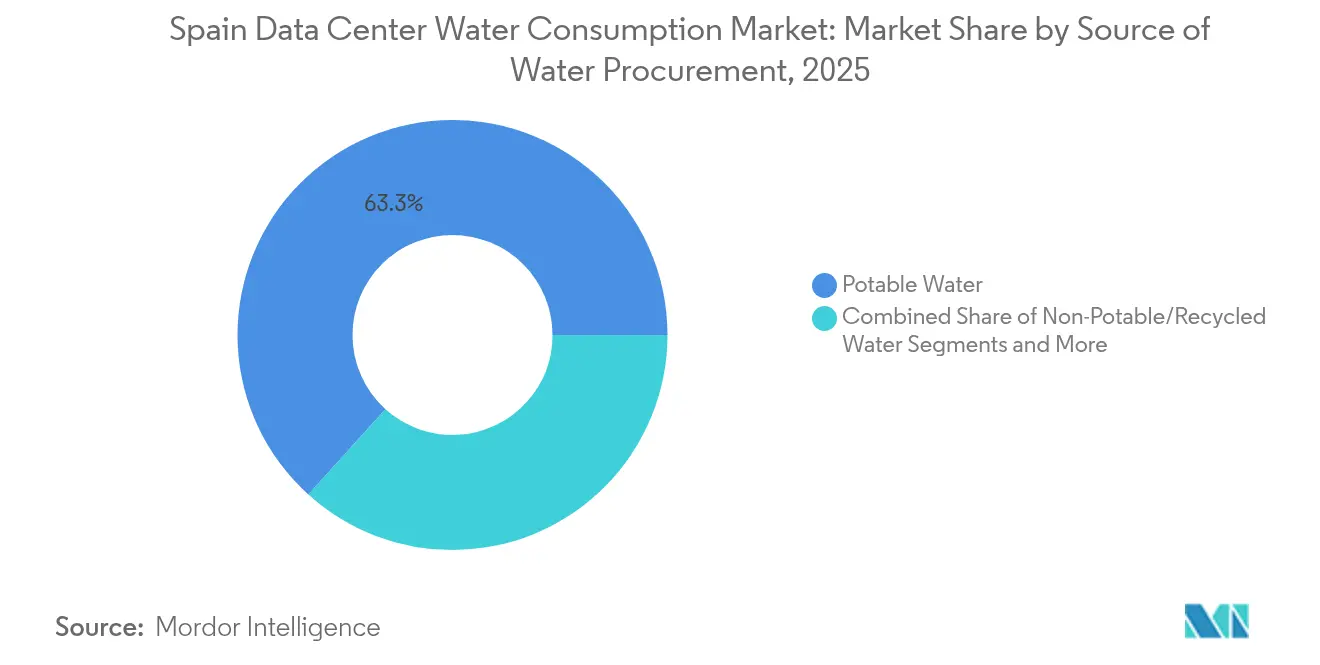

- By source of water procurement, potable water dominated with a 63.30% of Spain data center water consumption market size in 2025, whereas non-potable/recycled water will register a 26.05% CAGR to 2031.

- By data-center type, colocation captured 48.40% of Spain data center water consumption market size in 2025; cloud service providers are projected to grow at 28.0% CAGR between 2026-2031.

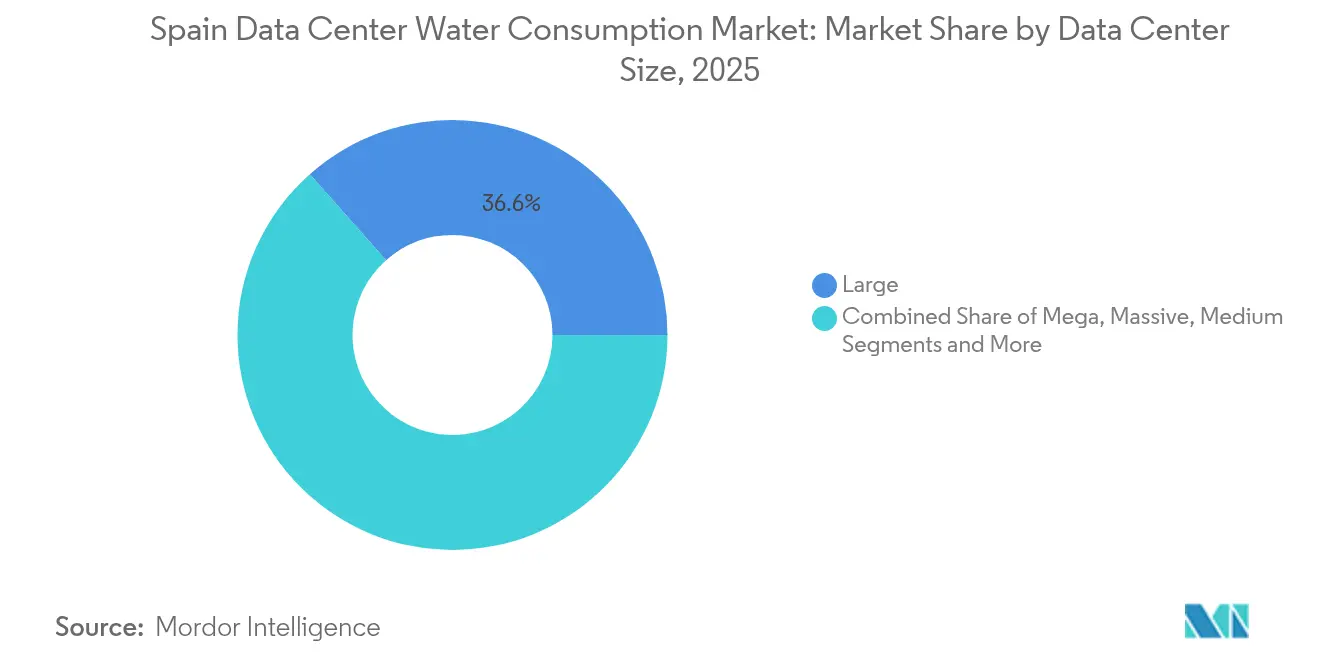

- By data center size, large data centers accounted for 36.55% of Spain data center water consumption market size in 2025; mega facilities are poised to rise at 26.7% CAGR over the same period.

- By cooling technology, chilled-water systems led with 51.30% of Spain data center water consumption market size in 2025, while liquid immersion cooling is forecast to advance at a 25.9% CAGR through 2031.

- By geography, Madrid and Central held 57.40% of Spain data center water consumption market size in 2025; the Basque Country and Navarre are set to expand at a 27.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in Spain connect differently with activity unfolding across other parts of the world. In the global data center water consumption market coverage, Mordor Intelligence integrates these into a single analytical framework.

Spain Data Center Water Consumption Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Hyperscale Campuses in Madrid and Barcelona Driving Municipal-Water Demand | +7.5% | Madrid and Central, Catalonia | Medium term (2-4 years) |

| Aggressive Renewable-Powered Cooling Mandates by Spanish Regulators Elevating Grey-Water Re-use Projects | +6.2% | National, with early implementation in Madrid and Barcelona | Medium term (2-4 years) |

| Corporate Net-Zero Water Pledges (AWS, Microsoft) Accelerating On-site Desalination Pilots | +5.8% | Madrid and Central, Catalonia, Basque Country and Navarre | Long term (≥ 4 years) |

| Agrivoltaic-Data-center Symbiosis Unlocking Water Capture and Sharing in Semi-Arid Regions | +4.3% | Andalusia, Valencia and Murcia | Long term (≥ 4 years) |

| Rising Electricity Tariffs Shifting Preference toward Adiabatic Cooling with Lower Power–Water Trade-off | +3.2% | National | Short term (≤ 2 years) |

| REPowerEU Funds Ring-Fenced for Green IT Catalysing Water-Efficiency Retrofits in Legacy Facilities | +2.8% | National, with early gains in Madrid and Central | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Hyperscale Campuses in Madrid and Barcelona

The Spain data center water consumption market continues to feel the pull of hyperscale capital. Meta’s Talavera facility alone is projected to draw 665 million liters annually, accentuating the municipal water burden in Spain’s digital corridor. Subsea cables that shorten latency to Africa and the Americas amplify demand for low-latency hosting, propelling Madrid’s installed capacity to 147 MW in 2023, up 25.6% year-on-year. With new European rules mandating public disclosure of water metrics, operators have accelerated the roll-out of closed-loop and immersion systems that decouple capacity growth from potable-water draw. Municipal planners now assess campus proposals through a water-use lens, intertwining land approvals with quantified WUE commitments. As a result, water efficiency is evolving from a cost center into a key selection criterion for hyperscale site procurement teams shaping the Spain data center water consumption market.

Renewable-Powered Cooling Mandates by Spanish Regulators

A tightening policy environment is pushing the Spain data center water consumption market toward circular water loops. Spain’s adoption of the Climate Neutral Data Centre Pact caps WUE at 0.4 L/kWh in stressed areas by 2025. Edged Energy’s Barcelona plant already operates at 0.00 L/kWh, demonstrating regulatory feasibility while cutting energy overhead 74% relative to global baselines.[2]Spain DC, "The Data Centre Sector in Madrid", Spain DC, spaindc.com Obligations to source 10% of load through PPAs further align water and energy targets, as solar and wind projects often bundle grey-water infrastructure to secure community acceptance. Consequently, the Spain data center water consumption market sees a rising premium on sites that can integrate renewable feeds with ready access to treated effluent streams.

Corporate Net-Zero Water Pledges Driving Innovation

AWS and Microsoft have turned water positivity into a core procurement filter. AWS has already met 41% of its 2030 pledge through replenishment projects, such as reclaimed-wastewater systems at Villanueva de Gallego. Microsoft’s tie-up with Aganova leverages AI leak detection to offset campus demand while improving municipal networks near Madrid. These high-visibility moves oblige competitors to publicize equally ambitious roadmaps. Vendor ecosystems, from desalination skid makers to digital twin providers—benefit as operators seek turnkey solutions that verify savings. The virtuous cycle cements corporate stewardship as a durable growth vector for the Spain data center water consumption market.

Agrivoltaic-Data-Center Symbiosis in Semi-Arid Regions

Gran Canaria’s pilot agrivoltaic-data-center project demonstrates how dual-use solar arrays curb evaporative losses for adjacent crops, delivering 20% irrigation savings while powering IT loads. The model resonates in Andalusia and Valencia, where farming and digital infrastructure compete for scarce water. By sharing captured condensation and desalinated brine, data centers unlock local stakeholder support and diversify their water portfolio. The framework directly advances 11 UN SDGs and is now referenced in regional development plans, giving the concept regulatory momentum within the Spain data center water consumption market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity Surcharges by Canal Isabel II Increasing Opex for Potable Water Users | -2.1% | Madrid and Central | Medium term (2-4 years) |

| Lengthy Permitting Cycles for Ground-Water Extraction in Coastal Zones | -1.7% | Catalonia, Valencia and Murcia | Short term (≤ 2 years) |

| Community Opposition to Mega-Campus Water Draws in Catalonia | -1.3% | Catalonia | Medium term (2-4 years) |

| Limited Availability of Treated Waste-Water in Rural Colocation Locations | -0.9% | Andalusia, Rest of Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity Surcharges by Canal Isabel II

Progressive tariffs introduced in June 2024 add 15% to bills for users exceeding 60 m³ per two-month cycle, a threshold many data centers cross in summer peaks.[3]Canal de Isabel II, "Canal actualiza tarifa agua para fomentar ahorro", Canal de Isabel II, canaldeisabelsegunda.esThe measure could raise €598 million between 2025-2030 for network upgrades, yet it also inflates operating costs, intensifying the hunt for grey-water sources. In response, several Madrid campuses have filed for tariff exemptions tied to demonstrable potable-water reductions, reinforcing the financial stakes of efficiency within the Spain data center water consumption market.

Lengthy Permitting Cycles for Ground-Water Extraction

Coastal regions impose rigorous hydro-geological assessments that can extend borehole approvals beyond 18 months. These lags impede project timelines in Valencia and Murcia, where seawater desalination is technically viable yet still subject to exhaustive environmental impact reviews. Operators either shift capacity inland or over-specify air-based cooling, both options diluting economies of scale in the Spain data center water consumption market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Water Procurement: Potable Water Dominates Amid Diversification

Potable water accounted for 63.30% of Spain data center water consumption market size in 2025, equivalent to 22.24 billion liters concentrated in legacy hubs with reliable municipal supply. Economic pressures from scarcity tariffs and regulatory scrutiny now spur operators toward reclaimed streams, pushing non-potable/recycled water to a projected 26.05% CAGR. AWS’s reclaimed-wastewater loop in Villanueva de Gallego demonstrates potable-water displacement without compromising system reliability. Alternative sources—including seawater and harvested rain—gain traction in coastal builds, especially where desalination co-locates with renewable power.

Investment momentum indicates potable water will shrink below 50% share by 2031, yet absolute use may still climb given overall market growth. Corporate sustainability dashboards increasingly track liters-per-megawatt metrics, turning water provenance into a board-level KPI. As financing covenants integrate WUE targets, diversified sourcing emerges as a prerequisite for green-bond eligibility, reinforcing the strategic weight of water portfolio management within the Spain data center water consumption market.

By Data Center Type: Cloud Providers Accelerate Water-Efficient Expansion

Colocation facilities commanded 48.40% of Spain data center water consumption market share in 2025, benefiting from established client bases in Madrid. However, cloud service providers are set to outpace with a 28.0% CAGR, buoyed by EUR 22.3 billion (USD 24.53 billion) of hyperscale commitments in Aragon alone. Hyperscalers deploy advanced liquid immersion and reclaimed-water loops from day one, compressing the liter-per-kilowatt gap versus incumbents.

Colocation operators respond by integrating modular adiabatic chillers and negotiating grey-water supply contracts to defend price competitiveness. Enterprise data centers, though smaller, pilot edge-oriented waterless cooling to meet latency and stewardship mandates simultaneously. Competitive trajectories thus hinge on how quickly each archetype internalizes water-efficiency playbooks across the Spain data center water consumption market.

By Data Center Size: Mega Facilities Drive Efficiency Through Scale

Large facilities (10–25 MW) held 36.55% share in 2025, yet mega facilities (>50 MW) will lead growth at 26.7% CAGR. Scale enables investment in heat-to-agriculture recovery, on-site desalination and AI-driven cooling orchestration that smaller peers cannot economically replicate. Investor surveys show 23% favouring 50–100 MW builds, citing better power-purchase leverage and holistic sustainability reporting.

Medium and small data centers continue to satisfy edge latency pockets, especially near 5G densification corridors. Nonetheless, mega-campus design principles, low WUE, dual-source water routing, circular heat reuse, trickle down, gradually lifting baseline expectations across the Spain data center water consumption market. Funding partners now benchmark proposals against mega-site performance, reinforcing a virtuous diffusion of water-sparing practices.

By Cooling Technology: Liquid Immersion Disrupts Traditional Approaches

Chilled-water systems retained a 51.30% share in 2025, anchored by proven reliability in high-density halls. Yet liquid immersion cooling is forecast to register 25.9% CAGR, slashing water use up to 91% and energy draw 35%. Adiabatic units provide an intermediary step, exploiting evaporative cycles only during heat peaks, while rear-door heat exchangers appeal in space constrained builds.

Regulatory thresholds (0.4 L/kWh WUE) accelerate transition timelines, and vendors such as Submer now market dry-cooled immersion enclosures that sidestep external water entirely. Project approvals increasingly hinge on technology roadmaps that commit to immersion or waterless operation by year five, making cooling selection a critical gating decision in the Spain data center water consumption market.

Geography Analysis

Madrid and Central dominates Spain data center water consumption market with 57.40% share, but escalating scarcity surcharges have elevated water efficiency from optional to essential. Canal Isabel II’s fourth tariff block adds 15% to potable-water costs beyond 60 m³ bimonthly.Microsoft’s regional campus mitigates exposure by running direct evaporative cooling only 15% of the year, demonstrating a template for future builds Microsoft. Madrid’s robust fiber density and capital market access continue to attract projects, yet WUE clauses now feature prominently in municipal planning approvals.

Basque Country and Navarre, though smaller in absolute capacity, registers the highest projected growth rate as investors value its superior water-energy-food nexus performance. Regional authorities’ pro-innovation stance supports pilots such as Ibercom’s advanced closed-loop plant, which aligns with local decarbonization targets. Renewable hydro and wind availability further cements the region’s appeal, enabling integrated power-water procurement contracts that de-risk long-term utility costs for Spain data center water consumption market participants.

Catalonia experiences pronounced community resistance after its 2024 drought. AtlasEdge still advanced a 10 MW Barcelona site by pledging zero-water cooling and transparent consumption dashboards. Edged Energy’s facility, operational since January 2025, shows PUE 1.15 with no water consumed for IT cooling. These proof points gradually rebuild stakeholder confidence, yet future Catalonian projects must front-load community engagement and water impact mitigation to secure social license, reinforcing differentiated regional trajectories within the Spain data center water consumption market.

Mordor Intelligence's coverage of the data center water consumption market extends across other regions including Europe, North America, and South America, while country-specific intelligence is also available for Germany, France, United States, Brazil, United Kingdom, and Netherlands, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The Spain data center water consumption market exhibits moderate concentration, with Equinix, Digital Realty and AWS anchoring capacity while regional specialists capture niche demand. Transparent water reporting, mandated by the European Commission effective 2024, has turned WUE metrics into a customer procurement criterion. AWS claims 41% progress toward water positivity, leveraging replenishment projects to offset municipal draws. Digital Realty bundles green PPAs and grey-water reuse guarantees into its service-level contracts, seeking differentiation via integrated sustainability offerings.

Innovative startups such as Submer (immersion cooling) and AquaReturn (grey-water treatment skids) partner with incumbents, bridging technology gaps and accelerating compliance readiness. Partnerships like nLighten-Shell bundle on-site solar with thermal storage, indirectly lowering water and carbon overhead Digital Infra Network. The resultant ecosystem rewards firms that integrate water, energy and circularity within one business case, driving a strategic realignment across the Spain data center water consumption market toward holistic resource stewardship.

Spain Data Center Water Consumption Industry Leaders

-

Microsoft Corporation

-

Equinix Inc.

-

Digital Realty (Incl. Interxion)

-

Amazon Web Services

-

Digital Data Centre Bidco SL (Nabiax)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AtlasEdge acquired land for a second Barcelona data center, targeting 10 MW by 2027 with expansion to 24 MW. The move underscores strategic confidence in solving Catalonia’s water constraints through zero-water cooling designs.

- March 2025: Microsoft and Aganova launched an AI-enabled water-replenishment project near Madrid to advance Microsoft’s 2030 water-positive goal.

- February 2025: The EIB invested EUR 550 million (USD 605 million) in Spanish water infrastructure, bolstering resources for data-center water-efficiency retrofits.

- January 2025: Edged Energy and Merlin Properties completed a zero-water, PUE 1.15 data center in Barcelona, setting a new efficiency benchmark.

Spain Data Center Water Consumption Market Report Scope

The study tracks the critical applications of water in large data centers, such as cooling and power generation. It includes key applications based on water consumption in data centers and quantifies overall water usage in billion liters across regions. The study also identifies underlying trends and developments conceptualized by leading industry data center operators.

The Spain Water Consumption Market is Divided Into Segments Based On Water Procurement (Potable Water, Non-Potable Water, and Other Alternate Sources), Data Center Type (Enterprise, Colocation, and Cloud Service Providers (CSPs)), and Data Center Size (Mega, Massive, Large, Medium, and Small). The Report Provides Market Size and Forecasts for all These Segments, Measured in Volume (Billion Liters).

| Potable Water |

| Non-Potable / Recycled Water |

| Alternate Sources (Ground-, Surface-, Sea-, Rain-water and Produced Water) |

| Enterprise |

| Colocation |

| Cloud Service Providers |

| Mega |

| Massive |

| Large |

| Medium |

| Small |

| Chilled-Water Systems |

| Adiabatic / Direct-Evaporative Cooling |

| Rear-Door Heat Exchangers |

| Liquid Immersion Cooling |

| Air-Cooled (Minimal Water) |

| Madrid and Central |

| Catalonia |

| Basque Country and Navarre |

| Andalusia |

| Valencia and Murcia |

| Rest of Spain |

| By Source of Water Procurement | Potable Water |

| Non-Potable / Recycled Water | |

| Alternate Sources (Ground-, Surface-, Sea-, Rain-water and Produced Water) | |

| By Data Center Type | Enterprise |

| Colocation | |

| Cloud Service Providers | |

| By Data Center Size | Mega |

| Massive | |

| Large | |

| Medium | |

| Small | |

| By Cooling Technology | Chilled-Water Systems |

| Adiabatic / Direct-Evaporative Cooling | |

| Rear-Door Heat Exchangers | |

| Liquid Immersion Cooling | |

| Air-Cooled (Minimal Water) | |

| By Spanish Region | Madrid and Central |

| Catalonia | |

| Basque Country and Navarre | |

| Andalusia | |

| Valencia and Murcia | |

| Rest of Spain |

Key Questions Answered in the Report

What is the projected growth of the Spain data center water consumption market between 2026 and 2031?

The market is forecast to rise from 44.1 billion liters in 2026 to 137.2 billion liters by 2031, reflecting a 25.50% CAGR.

Which cooling technology will grow fastest in Spain’s data centers?

Liquid immersion cooling is expected to post a 25.9% CAGR through 2031 while cutting water use by up to 91%.

Why are hyperscalers focusing on Aragon for new campuses?

AWS and Microsoft committed EUR 22.3 billion (USD 24.53 billion) to Aragon due to abundant renewables and land availability, enabling water-efficient mega-facilities.

How are progressive water tariffs affecting data center operations in Madrid?

Canal Isabel II’s 15% surcharge on high-consumption blocks is elevating opex, prompting rapid adoption of grey-water reuse and waterless cooling.

What regulatory target must new Spanish data centers meet for water usage?

Facilities in water-stressed zones must achieve a maximum WUE of 0.4 L/kWh by 2025 under the Climate Neutral Data Centre Pact.

Which Spanish region is projected to grow fastest for data center water consumption?

Basque Country & Navarre is forecast at a 27.4% CAGR thanks to superior water-energy-food nexus efficiency and supportive renewable infrastructure.

Page last updated on: