Pectin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

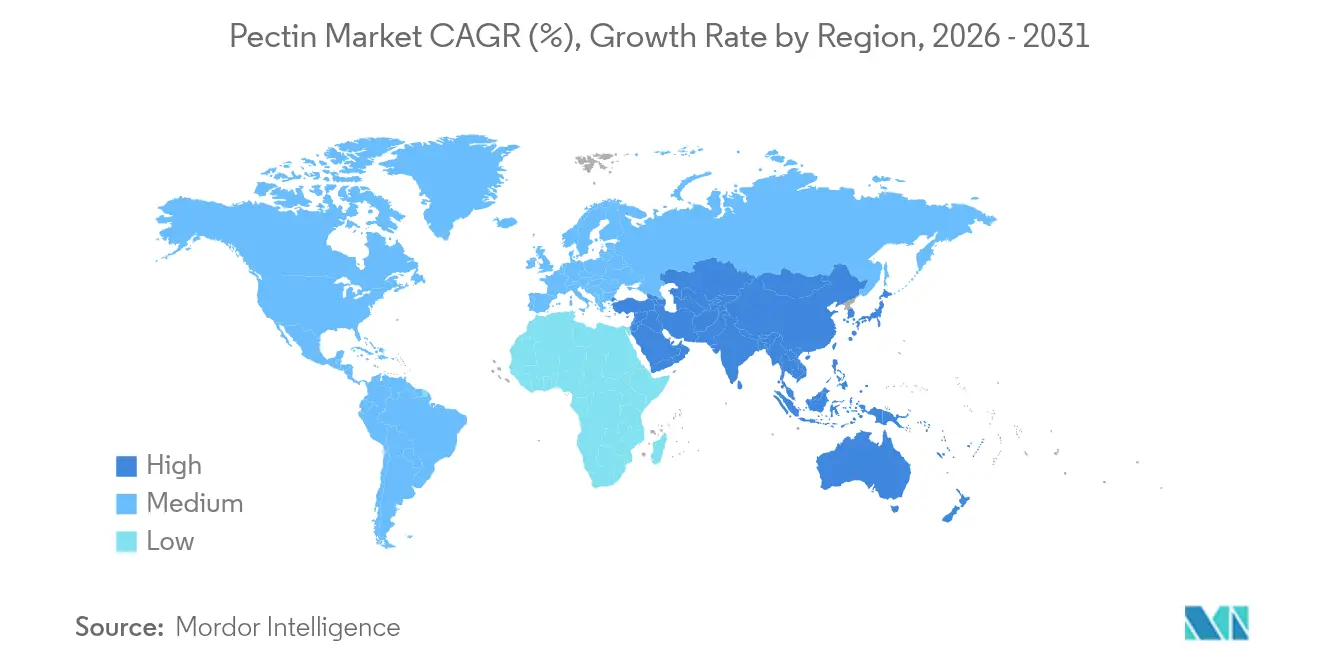

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

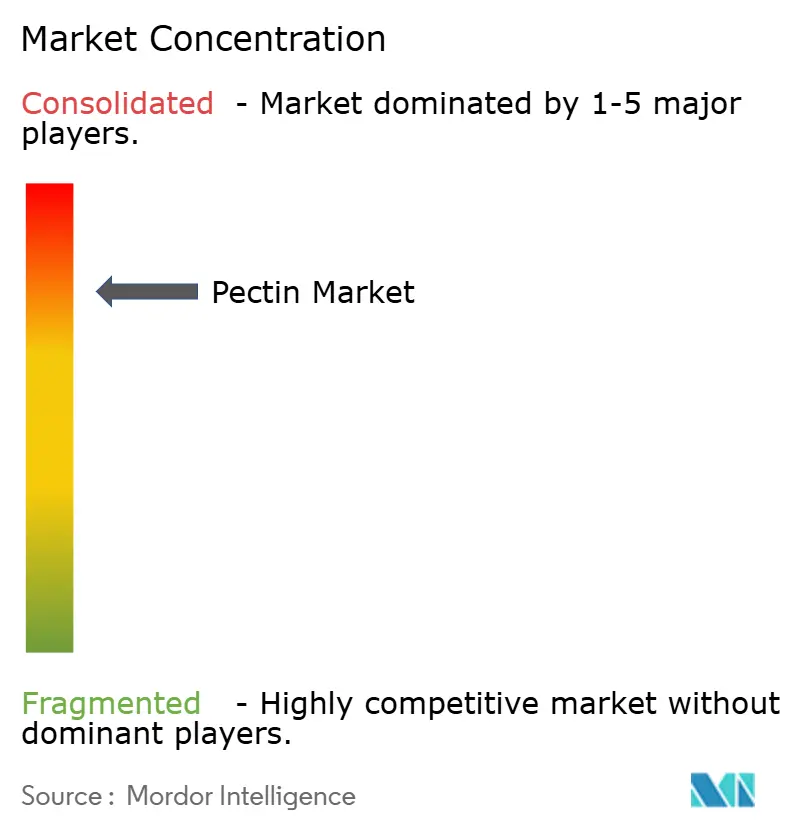

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pectin Market Analysis by Mordor Intelligence

The pectin market size is expected to grow from USD 1.07 billion in 2025 to USD 1.13 billion in 2026 and is forecast to reach USD 1.52 billion by 2031 at 6.05% CAGR over 2026-2031. Regulatory pressures on synthetic hydrocolloids are intensifying, while demand surges for recognizable ingredients[1]Source: European Commission,"New rules enter into force for a more sustainable and competitive packaging economy", environment.ec.europa.eu. Additionally, the functional applications of these ingredients are expanding in pharmaceuticals and packaging, driving steady market growth. Citrus-derived pectin, known for its superior gelation properties, remains the frontrunner. However, a 24% dip in Brazil's citrus output, coupled with a greening disease impacting 40% of plantations, is straining the availability of this raw material and pushing prices higher. Europe leads the charge, bolstered by stringent mandates on recyclable packaging, which in turn fuel investments in natural polymers. These regulations are encouraging manufacturers to explore sustainable alternatives, further solidifying Europe's position in the market. Meanwhile, the Asia-Pacific region is witnessing the swiftest demand growth, clocking in at a 7.19% CAGR. This surge is partly attributed to China's recent endorsement of pectin-based candies, beverages, and chocolates in draft regulations, which is expected to open new opportunities for manufacturers in the region. In the pharmaceutical realm, 3D bioprinting and personalized medicine are emerging as lucrative avenues. Pectin hydrogels, celebrated for their biocompatibility, are carving out niches in drug delivery and tissue engineering systems, offering innovative solutions for advanced medical applications.

Key Report Takeaways

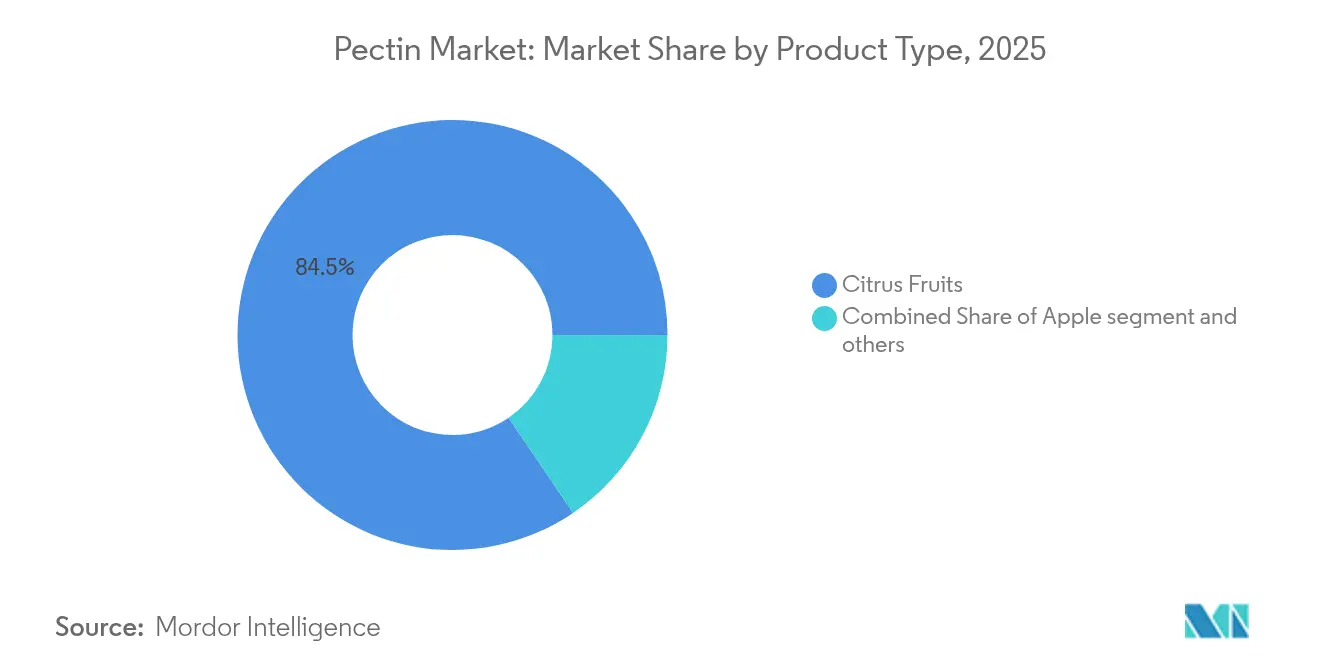

- By source, citrus accounted for 84.48% of pectin market share in 2025 and apple is projected to expand at a 6.38% CAGR from 2026 to 2031.

- By type, high-methoxyl pectin led with 58.35% revenue in 2025, whereas low-methoxyl variants are set to grow at a 6.42% CAGR through 2031.

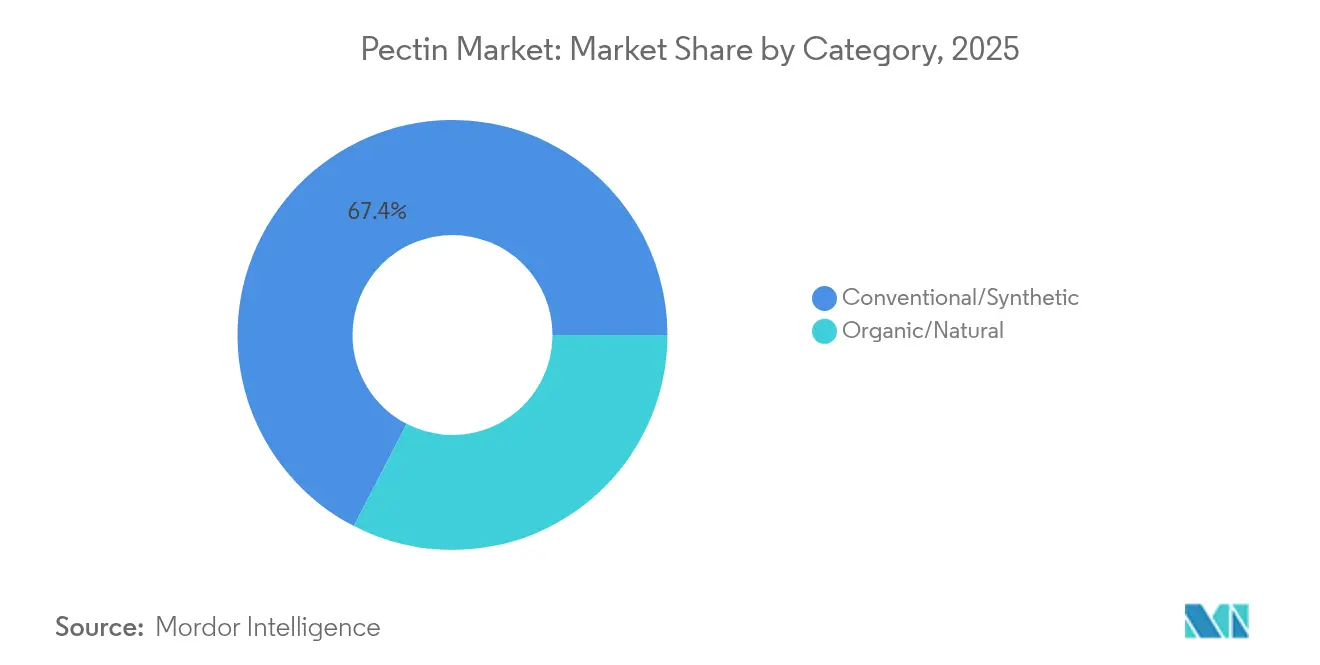

- By category, conventional grades held 67.42% share of the pectin market size in 2025, but organic grades are forecast to post a 6.79% CAGR to 2031.

- By application, food and beverages contributed 75.25% of 2025 revenue; pharmaceutical uses register the highest expected CAGR at 6.74% during 2026-2031.

- By geography, Europe captured 29.60% in 2025, while Asia-Pacific is projected to deliver the quickest advance at a 7.03% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pectin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for natural and clean-label ingredients | +1.8% | Global, with premium markets in North America and EU leading adoption | Medium term (2-4 years) |

| Rising consumption of packaged food products | +1.2% | Asia-Pacific core, spill-over to Latin America and MEA | Long term (≥ 4 years) |

| Growing shift to plant-based/vegan confectionery | +0.9% | North America and EU, expanding to urban Asia-Pacific markets | Short term (≤ 2 years) |

| Expansion of pectin-enabled 3-D bioprinting and personalized medicines | +0.7% | North America, EU, with early gains in Boston, Basel, Copenhagen research hubs | Long term (≥ 4 years) |

| Adoption of pectin in biodegradable food-packaging films | +0.6% | EU regulatory leadership, expanding to California, Canada | Medium term (2-4 years) |

| Circular-economy regulations valorizing agro-waste | +0.5% | EU, with emerging frameworks in Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for natural and clean-label ingredients

As consumers increasingly scrutinize ingredient lists, manufacturers are replacing artificial thickeners with pectin, which boasts a GRAS status and fiber benefits. Pectin, derived from natural sources such as citrus fruits and apples, aligns with the growing demand for clean-label products and offers functional benefits such as improved texture and stability in food formulations. The U.S. FDA's decision to exclude natural color additives from environmental assessments signals a clear endorsement of plant-derived inputs, further encouraging the use of natural ingredients[2]Source: Federal Register," Filing of Color Additive Petition From Phytolon Ltd.", www.federalregister.gov. In Europe, retailers are tagging shelves with “free-from” labels, favoring recognizable hydrocolloids like pectin. This trend is prompting processors to invest more in traceable and sustainably sourced pectin, as these attributes resonate with environmentally conscious consumers and align with regulatory requirements. Furthermore, brand owners who conduct and publish comprehensive supply-chain audits are witnessing quicker shelf turnover, underscoring the commercial advantage for suppliers who prioritize transparency, sustainability, and ethical sourcing practices.

Packaged-food consumption growth

As urbanization rises and dual-income households become the norm in the Asia-Pacific, there's a growing dependence on shelf-stable foods due to their convenience, affordability, and extended shelf life. Pectin, a natural polysaccharide derived from plant cell walls, is widely used in food applications for its ability to enhance viscosity, improve mouthfeel, and retain moisture. It plays a pivotal role in sauces, desserts, and ready meals by ensuring that portion-controlled packaging can withstand prolonged logistics cycles without relying on synthetic stabilizers. This functionality makes pectin an essential ingredient in the production of high-quality, shelf-stable food products, particularly in a region where logistical challenges and diverse consumer preferences are prominent. In a bid to cater to local tastes while upholding global quality benchmarks, multinational giants like Kraft Heinz are establishing regional innovation hubs in Singapore. These centers focus on developing recipes tailored to regional preferences, leveraging local insights to create products that resonate with consumers. This strategic approach has significantly boosted regional contract volumes for pectin, further driving its demand in the market and solidifying its role in the evolving food industry landscape.

Shift toward plant-based confectionery

In 2023, the majority of new gummy launches favored pectin over gelatin, aiming to meet the demands of vegan and halal markets while highlighting a broader consumer preference for alternatives to animal-derived ingredients. This transition reflects growing consumer demand for plant-based alternatives, driven by ethical, dietary, and environmental considerations. A retail price-premium analysis reveals that pectin gummies fetch unit margins up to 12% higher than their gelatin counterparts, effectively balancing out ingredient-cost disparities for brand owners. These texture advantages are also being leveraged in fruit snacks and low-sugar jellies, where pectin's functional properties, such as improved gelling, stability, and compatibility with clean-label formulations, play a crucial role. This trend has been instrumental in driving sustained double-digit SKU growth in convenience channels, as manufacturers continue to innovate to meet evolving consumer preferences. Additionally, the adoption of pectin aligns with the increasing focus on health-conscious and sustainable product offerings, further solidifying its position in the market.

3D Bioprinting and personalized medicines

Stable matrices at physiological pH make pectin hydrogels ideal for encapsulating active pharmaceutical ingredients in 3D printed dosage forms. These hydrogels provide a controlled release mechanism, ensuring the stability and efficacy of the active ingredients. In 2025, the FDA approved the inaugural human trial of a pectin-based 3D bioprinted implant, setting a significant regulatory precedent and highlighting the growing acceptance of bioprinting technologies in healthcare. This approval underscores the potential of pectin-based materials in advancing personalized medicine and regenerative therapies. Specialty ingredient manufacturers are increasingly collaborating with med-tech startups to co-create bioinks, which are critical for the development of advanced bioprinted products. These partnerships aim to leverage the unique properties of pectin for innovative applications, paving the way for a lucrative vertical that shifts revenue streams from traditional food applications to high-value medical and pharmaceutical uses. This diversification not only enhances profitability but also positions these manufacturers as key players in the rapidly evolving bioprinting market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of lower-cost synthetic hydrocolloids | -1.4% | Global, with price pressure most acute in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Volatile citrus-fruit supply and price swings | -1.1% | Global supply chain, with Brazil and Florida disruptions affecting worldwide pricing | Medium term (2-4 years) |

| High capex for industrial-scale "green" extraction technologies | -0.8% | Manufacturing regions in Europe, North America, and developed Asia-Pacific | Long term (≥ 4 years) |

| ESG scrutiny of acid-based extraction's carbon footprint | -0.6% | EU and North America, expanding to ESG-conscious multinational supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of lower-cost synthetic hydrocolloids

Mass-market food brands in price-sensitive economies are increasingly tempted by chemically derived thickeners, like modified starches and carboxymethyl cellulose, which are often priced 35% lower than pectin on a solids basis. These alternatives provide a cost-effective solution for manufacturers aiming to reduce production expenses without compromising product functionality. When clean-label claims take a backseat, procurement managers are more likely to make substitutions, limiting the uptake of pectin in specific bakery and dairy products. This trend poses a challenge for pectin adoption, particularly in regions where cost sensitivity outweighs consumer demand for natural ingredients. In response, top pectin suppliers are now offering bundled technical service packages, aiming to optimize dosage levels, enhance product performance, and bridge the cost gap. These service packages often include formulation support, application testing, and cost-reduction strategies, enabling manufacturers to achieve desired product quality while managing expenses effectively.

Volatile citrus supply and price swings

Brazil's citrus crop, severely impacted by greening disease, experienced a substantial decline for the 2024-2025 season compared to the previous year. This sharp reduction significantly affects the global pectin market, as the majority of pectin inputs are derived from peels generated during juice processing. Any shortages in citrus peels disrupt the supply chain, influencing contract pricing and extending lead times for pectin production. The reduced availability of citrus peels has created a ripple effect, impacting not only pectin refiners but also downstream industries reliant on pectin as a key ingredient, such as food and beverage manufacturers. In response to these dynamics, juice futures have nearly doubled since 2023, further driving up input costs for pectin refiners and creating additional financial pressures across the supply chain. To mitigate these challenges, major buyers are diversifying their sourcing strategies by turning to apple and sugar-beet derivatives. However, they continue to face difficulties in adapting formulations to accommodate the differing rheological properties of these alternative sources, which impacts product consistency, performance, and overall production efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Supply Diversification Beyond Citrus

In 2025, citrus-derived pectin commands a dominant 84.48% share of the market. This stronghold underscores the robust processing infrastructure backing citrus sources, coupled with their prized gelling traits sought after in numerous applications. Yet, challenges loom for Brazil's citrus peel supply, grappling with shortages and disease threats, likely keeping prices elevated until at least 2027. In light of this, leading European processors are pivoting, channeling investments into multi-feedstock processing lines to broaden their raw material base. Suppliers, too, are casting their nets wider, turning to alternatives like sunflower and sugar-beet pulp. These moves aim to align with regional waste-valorization mandates, though replicating citrus pectin's gel strength poses a technical hurdle. With supply security taking center stage, brand owners are locking in multi-year contracts with integrated juice firms, ensuring a consistent flow of peel volumes.

Conversely, apple-derived pectin is on a growth trajectory, with projections indicating a compound annual growth rate (CAGR) of 6.38%. This surge is primarily fueled by confectionery and dairy sectors scouting dependable alternatives in light of looming citrus shortages. Innovations in extraction, especially ultrasound-assisted methods, are giving apple pectin an edge. These advancements, predominantly seen in China and Turkey, not only amplify extraction yields but also curtail solvent consumption by up to 30%, bolstering both sustainability and cost-effectiveness. Such strides empower apple pectin to vie more fiercely in arenas once ruled by its citrus counterparts. In essence, the swift ascent of the apple-derived segment underscores a paradigm shift in buyer preferences, weighing supply consistency alongside functional and eco-friendly attributes.

By Type: High-Methoxyl Strength and Low-Methoxyl Momentum

In 2025, high-methoxyl pectin, accounting for 58.35% of total revenue, dominates the market, primarily due to its essential role in high-sugar preserves and bakery fillings. This segment's supremacy stems from the prevalent use of high-methoxyl pectin in products necessitating gelation in sugary settings, where it adeptly forms robust, stable gels. Its long-standing application in traditional jam and filling recipes guarantees consistent demand and notable market revenue. The pivotal role of high-methoxyl pectin in achieving desired textures and shelf life in preserves underscores its irreplaceability, especially in markets prioritizing these attributes. Furthermore, manufacturers find an advantage in its relatively simple processing demands when juxtaposed with more intricate pectin varieties. Collectively, the significant market presence of high-methoxyl pectin underscores its vital role in traditional food sectors.

Conversely, low-methoxyl pectin is the pectin market's fastest-growing segment, boasting a projected CAGR of 6.42% through 2031, outstripping the overall market's growth. This surge is driven by a rising appetite for low-sugar and reduced-calorie offerings, alongside a growing interest in pharmaceutical and nutraceutical uses. Low-methoxyl pectin's distinctive capability to gel in low-sugar settings via calcium-induced crosslinking positions it as a prime choice for healthier formulations, such as reduced-sugar jams. The market for these jams hit USD 264 million in 2025, with an anticipated annual growth rate of 7.4%. Yet, crafting with low-methoxyl pectin demands meticulous control of pH and calcium levels, posing challenges for smaller producers without sophisticated ion monitoring tools. The segment also excels in dietary supplement gummies, where it achieves the desired texture sans sucrose, and in pharmaceuticals, facilitating the encapsulation of delicate bioactives without risking protein denaturation. Such pioneering applications play a pivotal role in its swift market ascent.

By Category: Conventional Volumes and Organic Premiums

In 2025, conventional pectin grades commanded a dominant market share of 67.42%. This stronghold can be attributed to integrated citrus processors leveraging economies of scale, enabling them to produce pectin both efficiently and cost-effectively. With established supply chains and robust processing infrastructures, these processors ensure consistent volumes and competitive pricing, solidifying conventional pectin's status as the preferred choice for numerous manufacturers. Even amidst a growing emphasis on sustainability, conventional pectin retains its appeal in mainstream markets, thanks to its lower production costs and widespread availability. Furthermore, processors favoring conventional methods often turn to acid hydrolysis. While this method is less eco-friendly, its established nature and scalability make it a go-to choice. Such a solid foundation guarantees that conventional pectin holds its ground, even as alternative segments gain traction.

On the other hand, organic pectin is emerging as the fastest-growing segment, boasting a projected compound annual growth rate (CAGR) of 6.79% through 2031. However, its current volumes lag behind those of conventional grades. The surge in organic pectin's popularity is largely fueled by retailer-led initiatives aimed at eradicating synthetic chemical residues. This move resonates with consumers who prioritize cleaner, more natural ingredients in their products. Yet, producing organic pectin comes with its challenges. Costs such as certification fees, segregated storage, and the necessity for traceable peel sourcing inflate expenses by an additional USD 2.50 to 3.00 per kilogram compared to conventional pectin. While premium food and supplement brands often shoulder these costs, they seamlessly pass them onto health-conscious consumers who are more than willing to pay a premium for organic certification. Stricter regulations, like the EU Regulation 2025/40, which tightens claims on sustainability and recyclability, bolster genuine organic suppliers and act as a deterrent against greenwashing. Moreover, processors are increasingly turning to enzyme-assisted extraction techniques, a shift from traditional mineral acids. This not only aligns with organic standards but also curtails wastewater discharge by approximately 20%. Looking ahead, the sustainability of organic pectin production hinges on the adoption of continuous-flow processing technologies. These innovations promise efficient scaling of output while strictly adhering to certification mandates.

By Application: Food Core and Pharma Upside

In 2025, the food and beverage sector dominated the pectin market, accounting for a substantial 75.25% of total revenue. Pectin's entrenched role in products like jams, fruit preparations, and as a stabilizer in dairy underscores its significance. Its unique ability to provide texture, gelation, and stability makes it irreplaceable. Additionally, confectionery brands are now favoring pectin gummies over gelatin, appealing to vegan consumers and ensuring thermal stability in warmer regions. Beverage makers are also adopting amidated low-methoxyl pectin to suspend fruit pulp clearly, broadening its application in premium juices. These entrenched and evolving uses solidify pectin's leading position in the market.

On the other hand, while the pharmaceutical sector currently boasts a smaller revenue share, it is emerging as the fastest-growing market for pectin, with a notable CAGR of 6.74%. This surge is driven by innovations in biofabrication, wound dressings, and controlled drug release, many nearing the end of clinical trials. Collaborative efforts between universities and ingredient manufacturers are paving the way for pectin-based buccal films, designed for the swift absorption of pain medications. Furthermore, while beauty brands are eyeing pectin for its potential in enhancing skin feel in creams, its uptake in this domain is still in its infancy. Leveraging pectin's biocompatibility and versatility, the pharmaceutical sector is poised for significant growth, especially as new medical technologies and therapeutic systems evolve. This shift underscores pectin's transition from its traditional food-centric role to a pivotal player in health and wellness innovations.

Geography Analysis

In 2025, Europe commanded a significant 29.60% share of sales, buoyed by its rich traditions in jams and dairy, alongside policy initiatives championing recyclable packaging. Germany and France, benefiting from their closeness to Spanish citrus peel processors, jointly represent two-thirds of the region's volume. The region's strong infrastructure for citrus peel processing and its focus on sustainability have further strengthened its position in the market. Meanwhile, the Single-Use Plastics Directive is catalyzing research and development grants for pectin-film composites, positioning local suppliers as pioneers in the natural packaging domain. This directive not only encourages innovation but also provides a competitive edge to European suppliers in the global market.

Asia-Pacific is on track to register a 7.03% CAGR from 2026 to 2031. China, expanding its health-foods repertoire, is the primary driver of this demand surge. The country's increasing focus on health-conscious products and its growing middle-class population are key factors contributing to this growth. Concurrently, updates from India's Food Safety and Standards Authority, aligning vitamin-gummy regulations with international standards, are prompting contract manufacturers in Gujarat and Maharashtra to invest in continuous pectin-jelly cookers. These investments are expected to enhance production efficiency and meet the rising demand for pectin-based products. In Indonesia, Cargill's 2024 blending-plant expansion is streamlining the supply of texturants for local brands, enabling regional manufacturers to reduce dependency on imports and cater to the growing demand for high-quality texturants.

While North America showcases steady growth, the U.S. is carving a niche in pectin-driven 3D bioprinting trials, particularly along the Boston-to-San Diego biotech corridor. The US jam, jelly, and preserves segment drives steady demand for high-methoxyl pectin in traditional formulations. This innovation is expected to revolutionize the healthcare and pharmaceutical sectors, further solidifying the region's leadership in advanced applications of pectin.

Latin America's landscape is a study in contrasts: Brazil, while a source of vital peel feedstock, grapples with domestic export shortfalls due to supply chain inefficiencies and fluctuating production levels. In contrast, Mexico's confectionery sector is leveraging pectin to meet U.S. vegan import standards, which are becoming increasingly stringent. Adoption in the Middle East and Africa is gradual, yet bolstered by investments from multinational beverage firms in the Gulf Cooperation Council countries. These investments are driving the development of local production facilities and increasing the availability of pectin-based products in the region.

Competitive Landscape

The Global Pectin Market exhibits moderate consolidation. In November 2024, Tate & Lyle's acquisition of CP Kelco for USD 1.8 billion positioned the combined entity as a leading player in the global pectin market, significantly strengthening global supply chains and enhancing market competitiveness. Concurrently, DSM-Firmenich's newly established Parma complex and Ingredion's USD 50 million investment in upgrading its Iowa facility highlight a strong commitment to sustainable practices, including green extraction methods and the development of biodegradable packaging solutions.

Key strategic priorities in the market include advancing multi-feedstock flexibility, adopting enzyme-assisted extraction techniques, and exploring opportunities in pharmaceutical bioinks. Smaller regional players strive to differentiate themselves by focusing on organic-grade products and utilizing local fruit waste streams. However, rising costs associated with ESG compliance and the increasing need for advanced research and development capabilities place these smaller entities at a heightened risk of acquisition by larger competitors.

Mid-tier firms are capitalizing on licensing agreements for patented low-methoxyl formulations, enabling them to access profitable market segments without the significant investment typically required for extensive research and development facilities. These agreements allow firms to utilize advanced formulations developed by others, reducing time-to-market and operational costs. Additionally, the implementation of digital traceability platforms, which rely on QR code scanning on peel consignments, improves audit readiness by providing real-time tracking and detailed product histories. This not only ensures compliance with regulatory standards but also fosters stronger connections with customers by enhancing transparency and trust in the supply chain.

Pectin Industry Leaders

-

Cargill Incorporated

-

Herbstreith and Fox Corporate Group

-

International Flavors & Fragrances

-

Silvateam S.p.A.

-

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: In a strategic move, Tate & Lyle, a prominent player in the food and beverage sector, finalized a USD 1.8 billion (EUR 1.6 billion) acquisition of CP Kelco, a US-based manufacturer renowned for its nature-derived specialty ingredients. This acquisition not only bolstered Tate & Lyle's offerings but also brought CP Kelco's esteemed portfolio, including products such as pectin and citrus fiber, under its umbrella.

- January 2024: IFF has introduced Grindsted Pectin FB 420, tailored specifically for baking applications. This new offering boasts unique sensory attributes, making it perfect for bake-stable fruit fillings, all while being label-friendly and process-efficient.

- December 2023: In Milan, Italy, Herbstreith & Fox GmbH & Co. KG unveiled its latest subsidiary, H&F Italy SRL, marking a strategic move into the Italian market. This new subsidiary aims to strengthen the H&F Group's presence and operations in Italy, catering to the growing demand for its products and services in the region.

Global Pectin Market Report Scope

Pectin is a structural acidic heteropolysaccharide found in the primary and middle lamellae and cell walls of terrestrial plants. It is made from real fruit, and its forms, from dry pectin to liquid pectin to mass-produced commercial pectin, are sourced entirely from plants.

The market studied is segmented by source, application, type, and geography. By source, the market studied is segmented into citrus fruits, sugar beet, apple, and other sources. By application, the market studied is segmented into beauty and personal care, food and beverages, pharmaceuticals, and other applications. The food and beverages segment is further classified into jam, jelly, and preserves, baked goods, dairy products, and other food and beverages. The other applications segment is further classified into edible films and coatings, paper substitutes, and foams and plasticizers. By type, the market studied is segmented into high methoxyl pectin and low methoxyl pectin. Based on geography, the market studied is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

For each segment, the market sizing and forecasting have been done in value terms USD.

| Citrus Fruits |

| Apple |

| Other Sources |

| High-Methoxyl (HM) Pectin |

| Low-Methoxyl (LM) Pectin |

| Conventional |

| Organic/Natural |

| Food and Beverage | Jam, Jelly and Preserve |

| Baked Goods | |

| Dairy Products | |

| Other Foods and Beverages | |

| Beauty and Personal Care | |

| Pharmaceuticals | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Source | Citrus Fruits | |

| Apple | ||

| Other Sources | ||

| By Type | High-Methoxyl (HM) Pectin | |

| Low-Methoxyl (LM) Pectin | ||

| By Category | Conventional | |

| Organic/Natural | ||

| By Application | Food and Beverage | Jam, Jelly and Preserve |

| Baked Goods | ||

| Dairy Products | ||

| Other Foods and Beverages | ||

| Beauty and Personal Care | ||

| Pharmaceuticals | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the pectin market in 2026?

The pectin market size stands at USD 1.13 billion in 2026 and is forecast to reach USD 1.52 billion by 2031.

Which region grows fastest through 2031?

Asia-Pacific posts the quickest advance with a 7.03% CAGR thanks to expanding health-food and confectionery applications.

What segment leads the pectin market by source?

Citrus-derived grades dominate with 84.48% of 2025 revenue, though apple pectin is the fastest-growing alternative.

Why is low-methoxyl pectin gaining popularity?

Low-methoxyl variants gel at low sugar levels and enable vegan or reduced-sugar formulations, supporting growth in gummies and pharmaceuticals.

How does supply volatility affect pricing?

A 24% drop in Brazilian citrus harvests and greening disease inflate peel costs, raising pectin prices and encouraging diversification into apple and beet sources.

Page last updated on: