Fondaparinux Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 714.88 Million |

| Market Size (2030) | USD 980.56 Million |

| Growth Rate (2025 - 2030) | 6.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

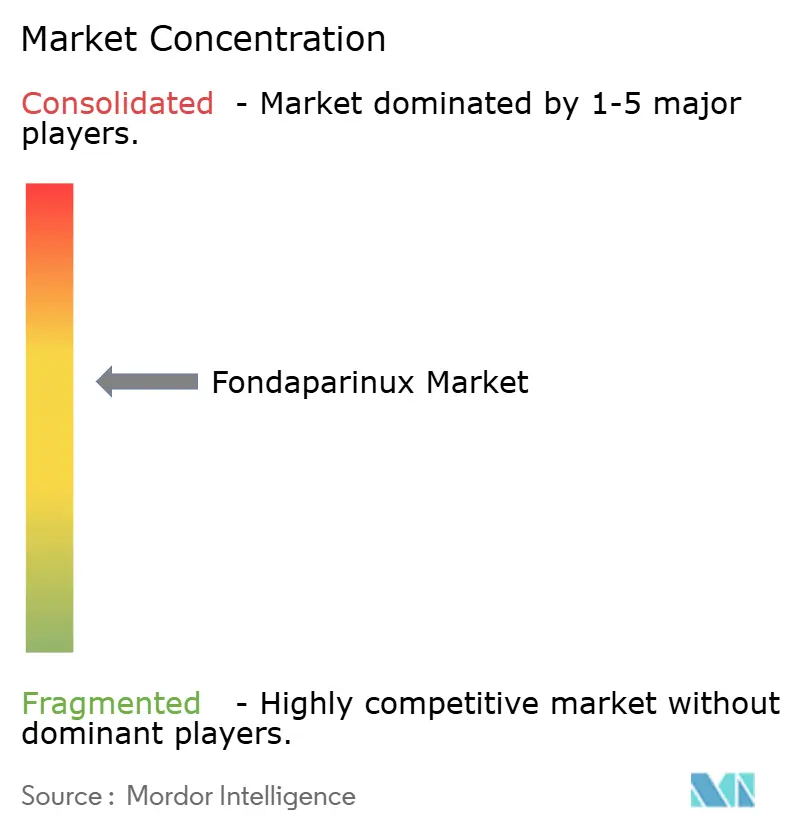

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fondaparinux Market Analysis by Mordor Intelligence

The global fondaparinux market stood at USD 714.88 million in 2025 and is forecast to reach USD 980.56 million by 2030, advancing at a 6.52% CAGR. Uptake is anchored in its role as a synthetic factor Xa inhibitor that offers negligible cross-reactivity for patients with heparin-induced thrombocytopenia, making it a preferred option when conventional anticoagulants are unsuitable.[1]Harlan M. Krumholz, “Antiplatelet and Anticoagulant Therapy in the 2025 ACC/AHA Guideline for Acute Coronary Syndromes,” JACC, jacc.org Growth reflects wider clinical adoption in orthopedic surgery, cardiology protocols and outpatient settings, while the patent cliff has opened space for competitively priced generics that now dominate volume. Competitive intensity is moderate: established manufacturers rely on production expertise for the complex pentasaccharide synthesis and leverage regulatory experience to protect positions. At the same time, direct oral anticoagulants exert pricing pressure and highlight the need for continuous supply-chain vigilance.

Key Report Takeaways

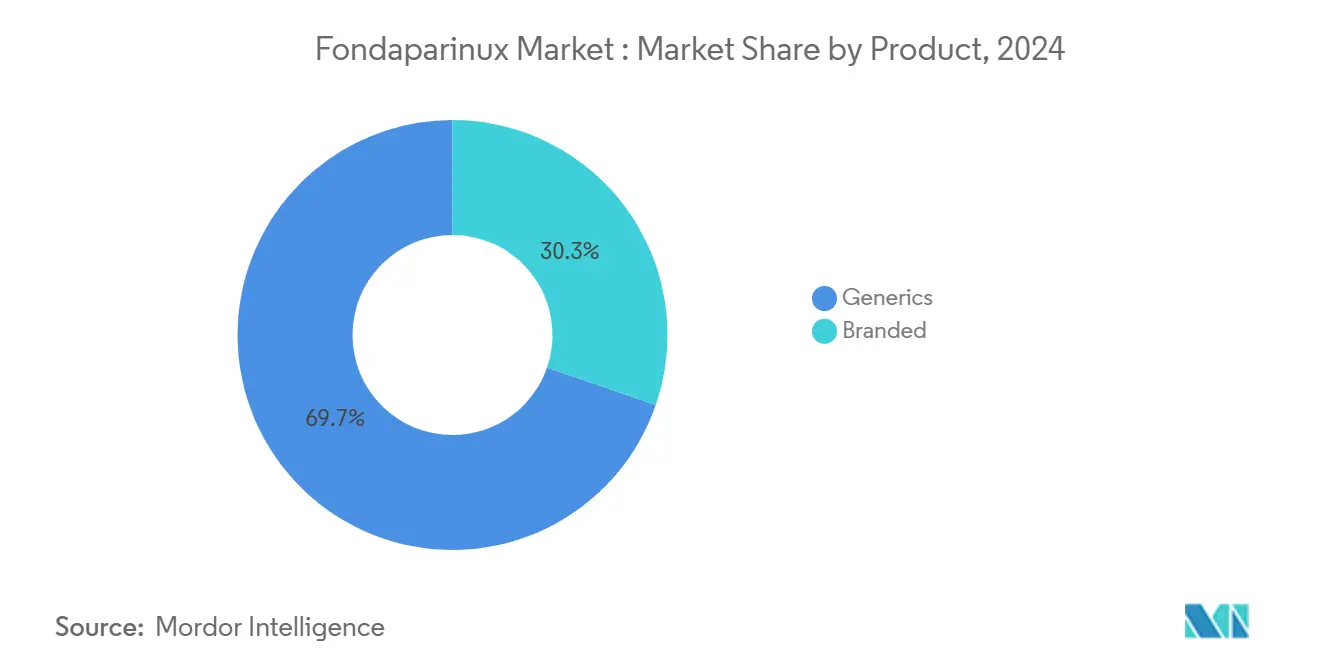

- By product type, generics led with 69.72% of fondaparinux market share in 2024; branded products trail, and generics are growing fastest at a 9.57% CAGR through 2030.

- By indication, deep-vein thrombosis (DVT) prophylaxis in orthopedics captured 44.34% of the fondaparinux market size in 2024, whereas heparin-induced thrombocytopenia (HIT) management is projected to expand at a 9.23% CAGR to 2030.

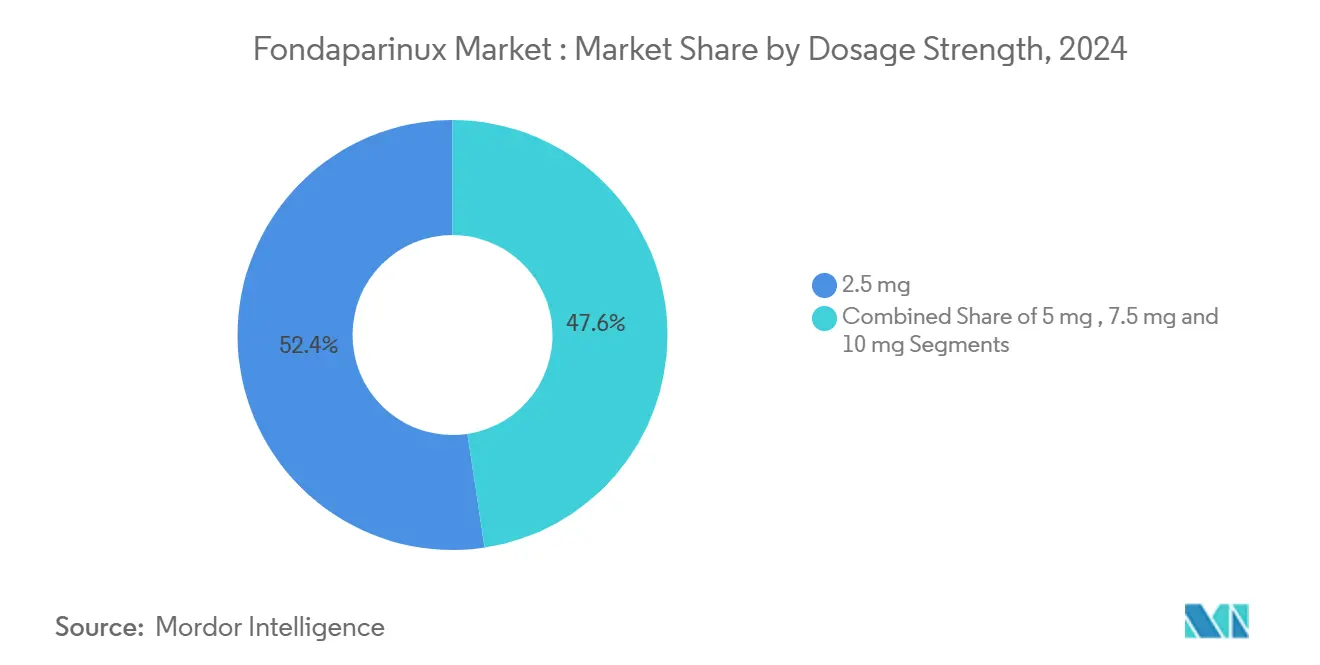

- By dosage strength, 2.5 mg formulations accounted for 52.38% of the fondaparinux market size in 2024, while the 10 mg dose is set to rise the fastest at an 8.65% CAGR.

- By distribution channel, hospital pharmacies held 61.23% share of the fondaparinux market size in 2024, yet online pharmacies deliver the highest projected CAGR at 10.65% through 2030.

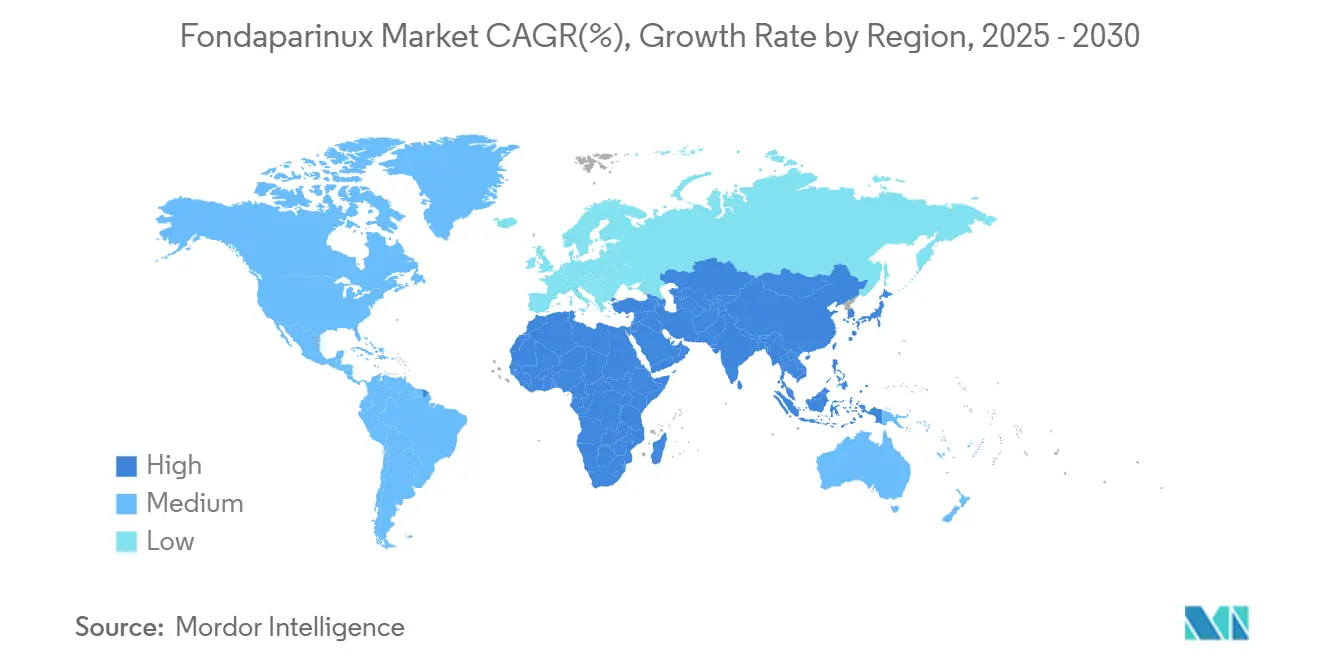

- By geography, North America commanded 33.62% fondaparinux market share in 2024; Asia-Pacific is the quickest-growing region at a 9.03% CAGR to 2030.

Global Fondaparinux Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Cardiovascular & Thrombo-Embolic Disease | +1.8% | Global, with higher impact in aging populations of North America & Europe | Long term (≥ 4 years) |

| Increasing Geriatric Population | +1.5% | Global, concentrated in developed markets with aging demographics | Long term (≥ 4 years) |

| Rise In Orthopedic & Trauma Surgeries Requiring VTE Prophylaxis | +1.2% | Global, with accelerated growth in APAC emerging markets | Medium term (2-4 years) |

| Expansion Of Outpatient / Home-Based Anticoagulation Protocols | +0.9% | North America & Europe leading, expanding to APAC | Medium term (2-4 years) |

| Growing Clinical Preference In HIT Patients Due To Negligible Cross-Reactivity | +0.7% | Global, with higher adoption in advanced healthcare systems | Short term (≤ 2 years) |

| Rapid Generic Approvals Driving Price Erosion In EMs | +0.4% | Emerging markets in APAC, Latin America, and MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing burden of cardiovascular and thrombo-embolic disease

Cardiovascular and thrombo-embolic disorders continue to rise, prompting broader deployment of specialized anticoagulation. Chinese orthopedic data showed in-hospital venous thromboembolism rates of 0.1% with fondaparinux versus 0.8% using low-molecular-weight heparin, confirming clinical advantage in complex patients.[2]Donglin Fu, “Fondaparinux sodium and low molecular weight heparin for venous thromboembolism prophylaxis in Chinese patients with major orthopedic surgery or trauma,” BMC Surgery, biomedcentral.com Updated 2025 ACC/AHA guidelines recommend fondaparinux for non-ST-segment elevation acute coronary syndrome when early angiography is not planned, expanding its footprint beyond surgery. Clinicians value its once-daily subcutaneous dosing and predictable pharmacokinetics, especially for elderly or multi-morbid patients requiring steady anticoagulation without routine monitoring.

Increasing geriatric population

Global aging broadens the pool of patients who need anticoagulants yet are sensitive to drug-drug interactions. Japanese evidence shows fondaparinux performs consistently across age brackets, provided renal function guides dosing. The fifth-edition ASRA guidelines advise longer peri-procedural windows in older adults, reflecting the molecule’s prolonged half-life. Simple daily injections and minimal interaction potential dovetail with polypharmacy realities, supporting adherence.

Rise in orthopedic & trauma surgeries requiring VTE prophylaxis

Surgical volumes are climbing worldwide, particularly elective hip and knee replacements and high-energy trauma repair. European peri-operative guidance places fondaparinux among first-line options for bariatric and high-BMI patients because of superior prophylaxis in high-risk profiles.[3]Juan Ignacio Arcelus, “European Guidelines on Peri-operative Venous Thromboembolism Prophylaxis: First Update,” European Journal of Anaesthesiology, lww.com Asia-Pacific consensus statements echo the finding, highlighting lower VTE incidence than enoxaparin but cautioning on bleeding risk, necessitating judicious candidate selection. These recommendations underpin the segment’s positive momentum.

Expansion of outpatient / home-based anticoagulation protocols

Healthcare delivery is shifting toward ambulatory care. German prospective data report favorable tolerance for fondaparinux in hospital-at-home pathways, easing the burden on inpatient beds. Subcutaneous bioavailability reaches 100% and eliminates laboratory monitoring, which fits remote management models. Payer incentives around bundled payments and telemedicine further encourage drugs that can be self-administered safely.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Clinician Familiarity In LMIC Hospitals | -0.8% | Low and middle-income countries, particularly in APAC and Africa | Medium term (2-4 years) |

| Competition From Oral DOACs (Rivaroxaban, Apixaban, Etc.) | -1.2% | Global, with higher impact in developed markets | Short term (≤ 2 years) |

| Absence Of A Dedicated Reversal Agent Increases Bleeding-Risk Concerns | -0.6% | Global, with higher concern in emergency care settings | Long term (≥ 4 years) |

| Complex Synthetic Supply Chain Causing Intermittent Shortages | -0.4% | Global, with higher impact during supply disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited clinician familiarity in LMIC hospitals

Protocols for dosing and renal adjustment may be unfamiliar in lower-resource settings. Indian expert panels have created decision pathways to bridge this gap, but steady training is still required. Without dedicated coagulation laboratories, some providers hesitate to adopt unfamiliar injectables despite the lack of monitoring requirements.

Competition from oral DOACs

The convenience of once-daily tablets such as rivaroxaban or apixaban undermines injectables. First-wave generics heighten affordability, lowering the barrier to switch. Although fondaparinux excels in HIT and patients needing parenteral therapy, oral alternatives remain compelling for broad VTE prevention.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Generics Dominate Market Dynamics

Generics occupied 69.72% of fondaparinux market share in 2024 and are growing at 9.57% CAGR through 2030. Viatris, Dr. Reddy’s Laboratories and other seasoned API producers channel complex chemistry capabilities into large-scale manufacturing, enabling cost-efficient supply. Branded formulations retain a foothold in institutions with entrenched purchasing contracts, yet their expansion lags amid price-sensitive procurement. Vertical integration, as demonstrated by Amphastar’s end-to-end control of its enoxaparin business, underscores the importance of quality oversight in injectable anticoagulant production.

The fondaparinux market continues to pivot toward scale economics. Generics supply emerging economies where hospital budgets demand low-cost alternatives, reinforcing their volume lead. However, technical barriers keep the field relatively consolidated, mitigating a total race-to-the-bottom on pricing.

By Indication: DVT Prophylaxis Leads While HIT Management Accelerates

DVT prophylaxis in major orthopedic surgery generated 44.34% of the fondaparinux market size in 2024 and remains the anchor volume, propelled by aging populations undergoing joint replacements. In parallel, HIT therapy is on track for a 9.23% CAGR, the fastest of all indications, thanks to mounting evidence of zero cross-reactivity and superior safety. Acute DVT/PE treatment and select acute coronary syndrome protocols complement the mix, benefiting from 2025 cardiology guideline updates.

Clinical practice is widening beyond surgery. Investigators report favorable outcomes in cancer-associated VTE and pregnancy cases, broadening real-world experience. Nevertheless, adoption remains highest where evidence is longest standing, namely postsurgical prophylaxis and HIT rescue therapy.

By Dosage Strength: Lower Doses Dominate, Higher Strengths Show Promise

The 2.5 mg presentation comprised 52.38% of the fondaparinux market size in 2024, mirroring its standard prophylaxis role. Yet the 10 mg vial is forecast at an 8.65% CAGR as clinicians treat heavier patients and complex thromboses. Mid-range 5 mg and 7.5 mg doses fulfil weight-based protocols and renal-adjusted regimens. Japanese data on 7.5 mg post-arthroplasty illustrate high efficacy when coupled with vigilant bleeding surveillance.

Dosing flexibility underpins clinician confidence. ASRA’s 2025 guidance details renal thresholds and age-related modifications that direct dose selection. As therapeutic windows across diverse body masses become clearer, uptake of higher strengths is expected to climb.

By Distribution Channel: Hospital Dominance Faces Digital Disruption

Hospital pharmacies supplied 61.23% of fondaparinux market size in 2024, reflecting its inpatient and peri-operative usage. The online segment, though smaller, is rising quickest at 10.65% CAGR as telemedicine and home-infusion services proliferate. Programs like Prescription Hope offer a fixed USD 60 monthly price for Arixtra, illustrating alternative distribution paths that improve affordability for chronic users.

Handling requirements—cold chain, trained administration and needlestick disposal—remain hurdles for broad community pharmacy penetration. Still, as outpatient surgeries increase, blended models that combine hospital initiation with e-pharmacy refills are likely to expand.

Geography Analysis

North America upholds its leadership with 33.62% share, bolstered by guideline endorsement, seasoned prescribers and ample reimbursement. Hospitals widely integrate fondaparinux into orthopedic and cardiology protocols, while specialty pharmacies supply chronic-use patients discharged to home care. Regulatory openness to generics sustains price competition but does not erode fondaparinux’s distinct positioning for HIT or renal-adjusted cases.

Asia-Pacific’s 9.03% CAGR rests on urbanizing populations, higher elective surgery counts and government insurance expansion. Provincial tenders in China now routinely list fondaparinux alongside enoxaparin, attesting to procurement acceptance. Japanese clinicians apply data from local VTE registries that confirm effectiveness in seniors, thereby aligning with the country’s super-aged demographic.

Europe’s steady uptake benefits from mature venous-thromboembolism prevention frameworks. German prospective safety findings underpin continued hospital purchases, while EMA harmonization simplifies cross-border supply. Eastern European health systems are progressively adding fondaparinux to formularies as cost-effective generics arrive, narrowing historical access gaps.

Latin America and MEA markets evolve more slowly, constrained by budget and cold-chain bottlenecks. Targeted educational programs, often run in partnership with generic manufacturers, aim to upskill clinicians on dose selection and HIT protocols, paving the way for incremental adoption.

Competitive Landscape

Market concentration is moderate. Top generic suppliers combine vertical integration with proven cGMP histories. Viatris leverages a portfolio of 1,400 molecules to strengthen procurement leverage and manufacturing economies of scale. Dr. Reddy’s Laboratories trades on its complex API track record to guarantee uninterrupted fondaparinux intermediate supply. Amphastar’s in-house approach to synthesis and fill-finish underlines how quality assurance differentiates players in a molecule with no therapeutic substitutes once shortages arise.

R&D activity focuses less on molecule innovation and more on process optimization, including yield maximization and impurity-profile reduction. That keeps barriers high for new entrants yet affords incumbents predictable revenue tails. Competitive threat stems mostly from oral agents and upcoming factor XI inhibitors, although their distinct mechanisms mean fondaparinux preserves relevance in niches requiring injectable therapy or HIT avoidance.

Supply resilience is an emerging battleground. Drug-shortage alerts, reported at historic highs for hematology agents, motivate hospitals to dual-source and favor firms with redundant plants. Accordingly, manufacturers publicize capacity expansions, such as BrightGene’s new U.S.-approved line for fondaparinux injections, to reassure buyers.

Fondaparinux Industry Leaders

Dr. Reddy’s Laboratories Ltd.

Aurobindo Pharma Ltd

GSK plc

Viatris, Inc.

Jiangsu Hengrui Pharmaceuticals Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: BrightGene Bio-Medical Technology secured U.S. FDA approval for its fondaparinux sodium injection.

- December 2024: Lee Pharmaceutical activated a pre-filled syringe line that lifts capacity for volume-based-procurement products, including fondaparinux sodium injection and nadroparin calcium injection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fondaparinux market as the worldwide sales revenue generated from branded and generic formulations of fondaparinux sodium that are administered subcutaneously for venous thromboembolism prophylaxis and treatment, acute coronary syndromes, and heparin-induced thrombocytopenia. The sizing spans 17 key countries across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with values expressed in constant 2024 US dollars.

Synthetic factor Xa inhibitors other than fondaparinux, oral anticoagulants, and compounded hospital preparations are excluded.

Segmentation Overview

- By Product Type

- Branded

- Generics

- By Indication

- DVT Prophylaxis (Orthopedic Surgery)

- Acute DVT / PE Treatment

- Acute Coronary Syndrome

- Heparin-Induced Thrombocytopenia Management

- By Dosage Strength

- 2.5 mg

- 5 mg

- 7.5 mg

- 10 mg

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts conducted interviews with hospital pharmacists, vascular surgeons, and procurement heads across major economies to validate unit-use patterns, generic substitution rates, and price erosion assumptions. Follow-up surveys with regional distributors clarified channel mark-ups and emerging online pharmacy volumes, ensuring that our desk findings were grounded in day-to-day realities.

Desk Research

We first assembled foundational datasets from open-access health ministries, the World Health Organization, and agencies such as the Centers for Medicare and Medicaid Services, which record procedure and hospitalization counts for orthopedic surgeries and cardiac events. Trade statistics from UN Comtrade and customs portals helped us gauge finished-dose export flows, while association portals such as the International Society on Thrombosis and Haemostasis provided prevalence estimates for deep vein thrombosis. Financial filings and investor decks supplied average selling prices and the mix between branded and generic strengths. Select paid databases, notably D&B Hoovers for company revenues and Dow Jones Factiva for transaction news, enriched company-level splits. This list is illustrative; many other public and subscription sources informed the desk analysis.

Market-Sizing and Forecasting

A top-down model converts country-level procedure counts (hip and knee arthroplasties, coronary interventions) and venous thromboembolism incidence into eligible patient pools, to be further filtered through guideline-based fondaparinux penetration and dosage regimens. Results are then tested against bottom-up proxies such as sampled supplier invoices and channel checks, and adjusted where gaps appear. Key variables tracked include annual hip-replacement volumes, prevalence of VTE per 100,000 population, generic share progression, median ASP per 2.5 mg syringe, hospital-pharmacy capture, and 65+ population growth. Forecasts employ multivariate regression blended with ARIMA to project each driver, after which scenario analysis aligns with expert consensus on guideline shifts or biosimilar launches.

Data Validation and Update Cycle

Mordor analysts run anomaly and variance checks, compare outputs with independent hospital purchase audits, and escalate outliers for senior review before sign-off. The model refreshes every twelve months, with interim revisions triggered by major regulatory or supply events; a final sense check is performed just before report release so our clients receive the latest view.

Why Our Fondaparinux Baseline Stands Up to Scrutiny

Published estimates often diverge because firms pick different inclusion rules, currencies, and refresh cadences. We anchor the baseline by matching the therapeutic scope to real-world guidelines, by cross-checking procedure pools with pharmacy take-off, and by updating annually rather than every few years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 714.9 Mn (2025) | Mordor Intelligence | - |

| USD 688.0 Mn (2024) | Global Consultancy A | Excludes online pharmacy sales and adjusts prices with 2021 exchange rates |

| USD 691.9 Mn (2024) | Industry Journal B | Uses uniform 2.5 mg dosing for all indications, inflating volume counts |

| USD 574.9 Mn (2022) | Regional Consultancy C | Applies conservative penetration assumptions and does not annualize post-Covid elective surgeries |

In short, our disciplined triangulation of procedure data, price realities, and channel shifts delivers a balanced baseline that clients can trace back to transparent variables and repeatable steps, giving decision-makers confidence in every forecast we publish.

Key Questions Answered in the Report

What is the current global fondaparinux market size?

The fondaparinux market is valued at USD 714.88 million in 2025 and is projected to reach USD 980.56 million by 2030.

Which product segment holds the largest fondaparinux market share?

Generic formulations lead the market, accounting for 69.72% of global volume in 2024 and growing at a 9.57% CAGR.

Why do clinicians choose fondaparinux for patients with heparin-induced thrombocytopenia?

Fondaparinux lacks cross-reactivity with heparin-dependent antibodies, and multicenter studies report zero in-hospital mortality for HIT cases treated with the drug.

What dosage strength is most frequently prescribed?

The 2.5 mg dose dominates usage, covering 52.38% of 2024 demand due to its alignment with standard prophylaxis protocols.

Page last updated on: