Focal Segmental Glomerulosclerosis (FSGS) Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

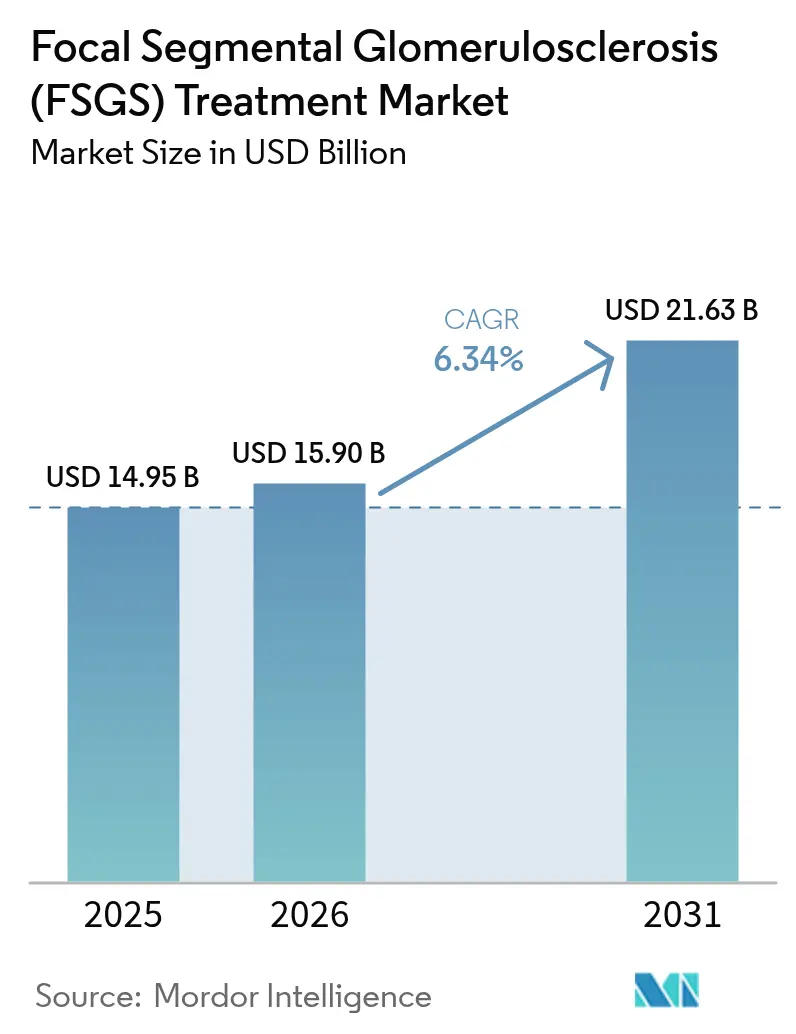

| Market Size (2026) | USD 15.9 Billion |

| Market Size (2031) | USD 21.63 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Focal Segmental Glomerulosclerosis (FSGS) Treatment Market Analysis by Mordor Intelligence

The Focal Segmental Glomerulosclerosis Treatment Market size is expected to grow from USD 14.95 billion in 2025 to USD 15.9 billion in 2026 and is forecast to reach USD 21.63 billion by 2031 at 6.34% CAGR over 2026-2031.

The steady rise reflects the worldwide surge in disease recognition, rapid adoption of immunomodulating drugs and the launch of first-in-class therapies that directly target podocyte injury. The FSGS treatment market is also benefiting from a robust orphan-drug pipeline, streamlined approval pathways and the growing use of biomarker-guided regimens that shorten time to response. Precision medicine is reshaping prescribing behaviour, while value-based care agreements are helping payers manage the high upfront cost of novel biologics. Competitive activity remains intense, with large pharma firms buying promising biotech assets to gain an early foothold in the FSGS treatment market.

Key Report Takeaways

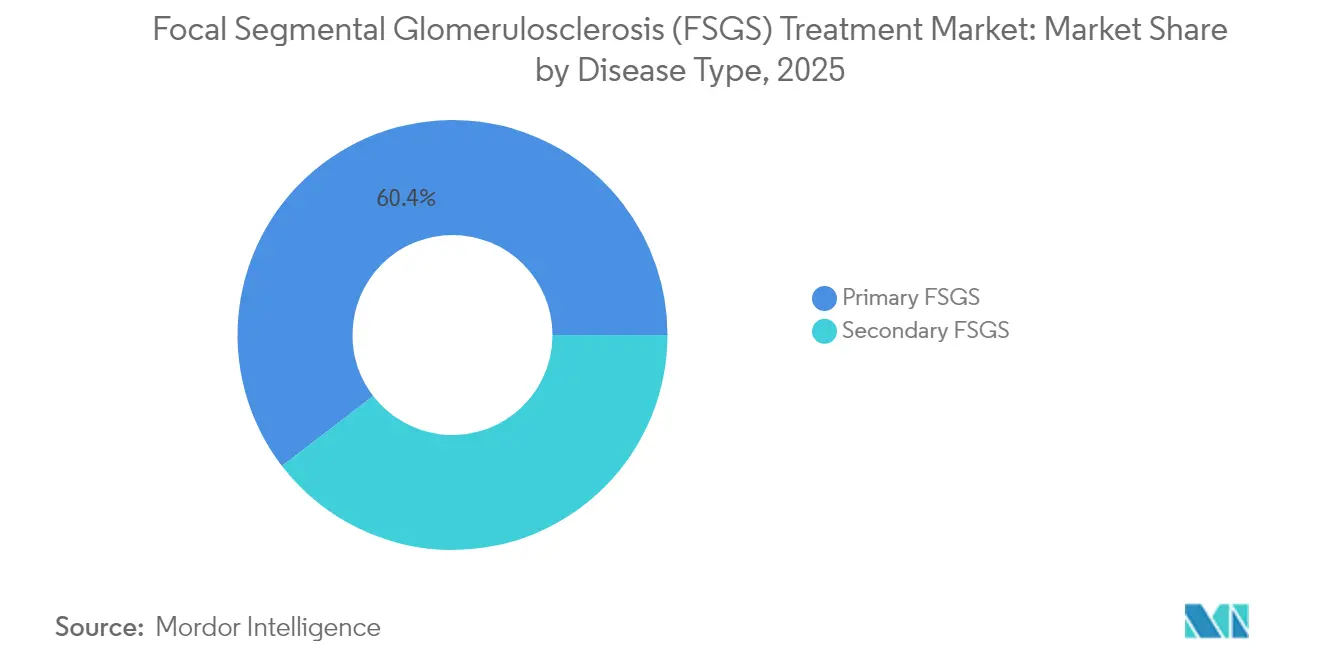

- By disease type, primary FSGS led with 60.42% revenue share in 2025 and is projected to grow at a 8.67% CAGR through 2031.

- By disease management, treatment accounted for 69.95% of the FSGS treatment market size in 2025 while advancing at a 11.82% CAGR over the same period.

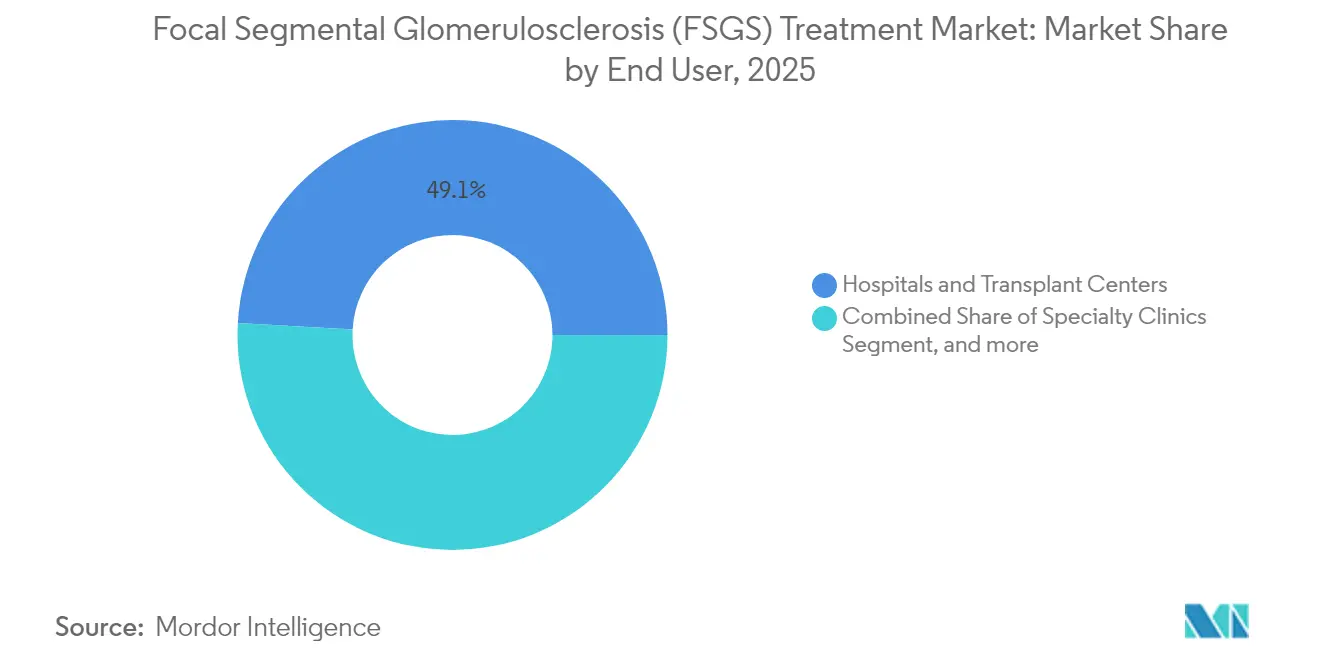

- By end user, hospitals and transplant centres held 49.12% of the FSGS treatment market share in 2025, whereas specialty clinics and nephrology practices are forecast to register a 13.02% CAGR up to 2031.

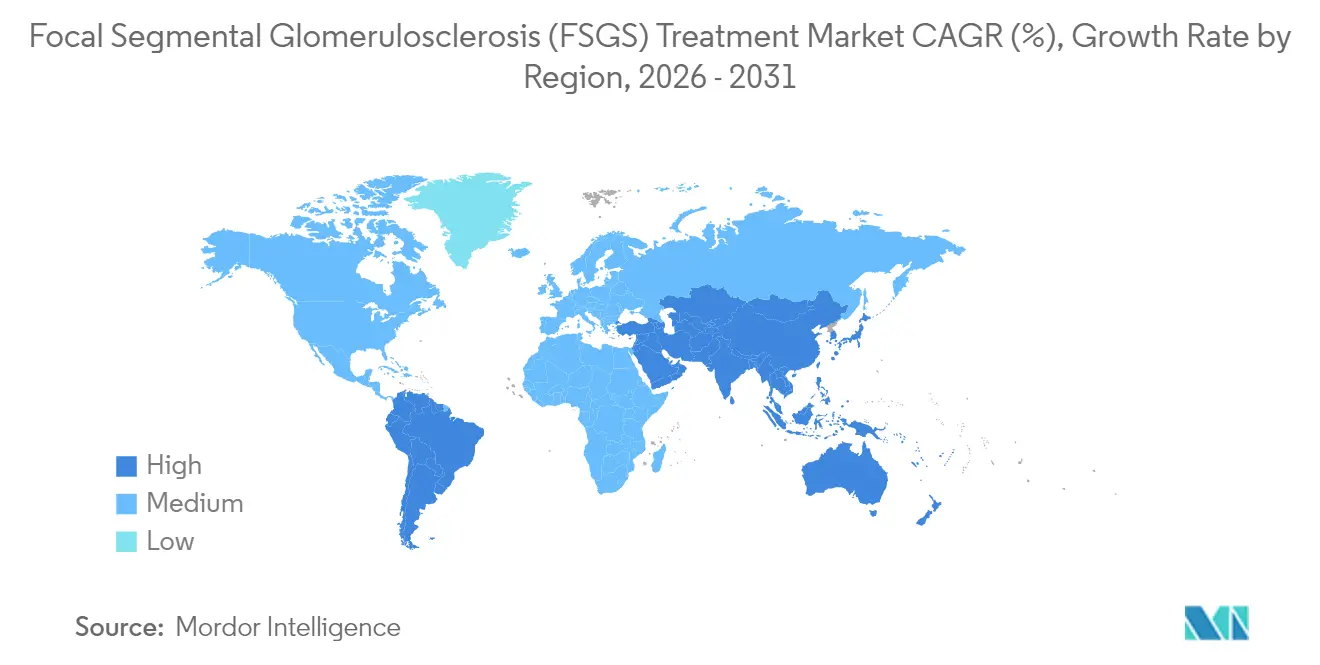

- By geography, North America captured 38.29% of 2025 sales, yet Asia Pacific is set to expand at an 17.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Focal Segmental Glomerulosclerosis (FSGS) Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence of FSGS Linked to Metabolic Disorders | +1.2% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Robust Therapeutic Pipeline & R&D Funding | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Regulatory Incentives for Rare Kidney Disease Drugs | +1.1% | North America & EU primary, expanding to APAC | Short term (≤ 2 years) |

| Advances in Single-Cell Renal Transcriptomics Enabling Precision Targets | +0.9% | Global, led by North America research hubs | Long term (≥ 4 years) |

| Rising Health-Equity Initiatives Expanding Early Biopsy in High-Risk Ethnic Populations | +0.7% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Increasing Adoption of Kidney Function Biomarkers for Early Diagnosis | +0.8% | Global, with faster adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of FSGS Linked to Metabolic Disorders

The continuing rise of diabetes and obesity is directly fuelling FSGS incidence, as metabolic stress accelerates podocyte loss and glomerular sclerosis.[1]Elke Schaefer, “Metabolic Drivers of Podocytopathy,” Springer Nature, springer.com Pharmaceutical developers are therefore testing dual-pathway agents that modulate both metabolic and renal signals. Earlier screening of hypertensive and diabetic patients is boosting diagnostic volumes, which in turn enlarges the addressable base of the FSGS treatment market. Clinicians are embedding metabolic control measures into care pathways, creating long-term demand for combo regimens that integrate glycaemic and lipid management with podocyte-protective drugs.

Robust Therapeutic Pipeline & R&D Funding

Vertex’s inaxaplin, Travere’s sparsentan and several antisense constructs have secured FDA Breakthrough Therapy or Orphan Drug designations, shortening regulatory timelines. Venture funding for kidney startups jumped 45% in 2024, which is encouraging smaller biotechs to pursue complement inhibitors, podocyte-regeneration biologics and gene-silencing molecules. Pipeline breadth is making the FSGS treatment market increasingly attractive to strategic investors, accelerating deal flow and advancing first-time modalities toward commercial launch.

Regulatory Incentives for Rare Kidney Disease Drugs

The FDA has issued more than 12 orphan designations for FSGS therapeutics since 2024, each conferring seven-year market exclusivity after approval.[2]U.S. Food and Drug Administration, “Approved Orphan Drug Designations: 2024-2025,” fda.gov Parallel EMA PRIME designations are shaving roughly 18 months off traditional European timelines. Regulators are validating surrogate endpoints such as proteinuria reduction, allowing pivotal trials of manageable size. Smaller firms can thus compete with larger incumbents, widening the spectrum of mechanisms entering the FSGS treatment market and strengthening long-term growth prospects.

Advances in Single-Cell Renal Transcriptomics Enabling Precision Targets

Single-cell sequencing has exposed distinct podocyte and immune-cell subsets within diseased glomeruli, revealing patient-specific signalling patterns.[3]National Center for Biotechnology Information, “Single-Cell Transcriptomics in Glomerular Disease,” ncbi.nlm.nih.gov Drug developers are pairing these insights with AI-guided analytics to uncover high-value targets and build companion diagnostics that stratify candidates at the point of care. Precision mapping of cell states promises to raise response rates, cut exposure to ineffective therapy and lower systemic toxicity. The resulting improvements in clinical utility support premium pricing and reinforce the value proposition of the FSGS treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Limited Access to Dialysis and Transplant | -0.8% | Global, more severe in emerging markets | Long term (≥ 4 years) |

| Clinical Trial Recruitment Challenges in Rare Disease | -0.6% | Global, particularly in regions with limited research infrastructure | Medium term (2-4 years) |

| Adverse Effects & Relapse Rates with Current Immunosuppressants | -0.9% | Global, with higher impact in regions with limited monitoring capabilities | Medium term (2-4 years) |

| Limited Long-Term Data for APOL1-Targeted Therapies | -0.4% | North America & Europe primarily, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Access to Dialysis and Transplant

Annual U.S. dialysis expenditure averages USD 89,000 per patient and a kidney transplant costs about USD 442,500. Limited transplant supply and long waiting lists amplify the burden. Payers therefore scrutinize the cost-effectiveness of every new entrant and are slow to endorse high-price cell or gene therapies without long-term outcome data. In low- and middle-income countries, dialysis capacity constraints create a stark treatment gap and temper uptake of premium drugs, muting part of the FSGS treatment market’s growth potential.

Clinical Trial Recruitment Challenges in Rare Disease

With only 7 cases per 100,000 population, FSGS trials must operate across multiple continents to find enough participants. Genotypic stratification further narrows eligibility, stretching timelines and budgets. The pandemic exacerbated delays by curtailing elective biopsies. Regulators now allow adaptive designs and Bayesian statistics, yet these complex methods demand specialised expertise that remains scarce outside large academic centres, adding operational risk and slowing evidence generation for the FSGS treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Primary FSGS Drives Therapeutic Innovation

Primary FSGS captured 60.42% of the FSGS treatment market in 2025 and is set to post a 8.67% CAGR through 2031. The strong share reflects sensitivity to immunomodulators and emerging targeted agents that block immune-mediated podocyte loss. APOL1 genotyping has become routine, and patients with high-risk alleles are enrolling in trials of genotype-specific inhibitors such as inaxaplin. The FSGS treatment market size for primary disease is therefore projected to outpace secondary FSGS, whose therapy still hinges on addressing diabetes, hypertension or drug toxicity.

Genetic testing is spawning micro-segments defined by APOL1 status, collapsing sub-populations into discrete commercial opportunities. AI-enhanced digital pathology further refines classification, allowing drug makers to align compounds with the most responsive cohorts. These precision tactics increase trial success probability and heighten investor confidence, reinforcing the central role of primary FSGS in steering the overall trajectory of the FSGS treatment market.

By Disease Management: Drug Therapy Transforms Treatment Landscape

Therapeutic interventions dominated with 69.95% share in 2025, and the drug-therapy slice alone is advancing at 11.82% CAGR. The recent acceptance of sparsentan’s supplemental NDA for an FSGS label heralds a new era of disease-modifying regimens. APOL1 inhibitors, complement blockers and regen-therapies are widening physician choice and gradually eroding reliance on corticosteroids. The diagnostic arm biopsy, biomarker panels and next-generation sequencing continues its steady climb as clinicians adopt less-invasive tests that accelerate decision-making.

Dialysis and transplant remain life-saving fallbacks, yet their growth is capped by capacity, cost and patient reluctance. The FSGS treatment market size for drug therapy is expected to surpass as oral small molecules and subcutaneous biologics push treatment into ambulatory settings. AI-based renal-pathology engines that classify lesions with 90% accuracy lower biopsy repeat rates and shorten the care pathway, bolstering uptake of targeted drugs.

By End User: Specialty Clinics Lead Care Transformation

Hospitals and transplant centres held 49.12% of global revenue in 2025, supported by multidisciplinary expertise and access to surgical infrastructure. Yet specialty nephrology clinics are the fastest risers, projected to grow 13.02% annually to 2031. Value-based networks such as InterWell Health showcase how early risk stratification, telemonitoring and integrated behavioural support can curb progression and reduce hospital admissions.

The migration of care from inpatient to outpatient settings is accelerating as once-weekly injectables and oral APOL1 inhibitors reach the market. Digital platforms allow nephrologists to track proteinuria and eGFR remotely, prompting real-time medication adjustments. Dialysis chains face federal scrutiny for potential anticompetitive practices, pushing regulators to ensure open referral pathways. Academic-medical centres remain central to late-phase trials, underpinning their relevance in moving experimental therapies into standard practice within the FSGS treatment market.

Geography Analysis

North America led with 38.29% of 2025 revenue on the back of early biologic uptake, concentrated nephrology expertise and broad insurance coverage. The United States alone hosts more than 40,000 diagnosed patients, forming the largest single-country pool for upcoming precision therapies. Canada benefits from universal reimbursement that smooths access, while Mexico’s expanding private-care segment is stimulating demand for advanced nephrology services.

Europe ranks second, supported by the EMA’s PRIME pathway and coordinated health-technology assessment that fast-track high-need drugs. Germany, France and the United Kingdom spearhead usage of proteinuria-lowering agents, whereas Southern Europe leverages EU structural funds to upgrade renal-care infrastructure. Conditional marketing approvals granted after interim phase-3 readouts are allowing earlier patient access and reinforcing the FSGS treatment market’s momentum across the continent.

Asia Pacific is the fastest-growing arena, scheduled to post an 17.95% CAGR to 2031. China’s drive to include rare-disease drugs on provincial formularies is widening the reimbursement base, and Japan’s established nephrology culture accelerates new-drug uptake. Korea’s Kidney Health Plan 2033 commits to nationwide early detection, tele-nephrology and biopsy standardisation. India and Australia present divergent dynamics: India faces rural-urban access gaps yet offers the largest volume upside, while Australia leverages strong research networks to lead regional trials. Together, these forces ensure that the FSGS treatment market continues to globalise, with multinational firms tailoring launch plans to varied reimbursement and infrastructure realities.

Regulatory Landscape

Regulation of focal segmental glomerulosclerosis (FSGS) therapies is anchored in rare-disease frameworks that accelerate development while tightening evidence expectations for narrow subpopulations. In the United States, the FDA has expanded use of orphan-drug incentives for FSGS programs, and in April 2026 it granted full approval to Travere Therapeutics FILSPARI (sparsentan) to reduce proteinuria in patients aged 8 years and older with FSGS without nephrotic syndrome. This approval, the first FDA-approved medicine specifically for FSGS, also established proteinuria as a viable label-supporting endpoint for the indication.

Across Europe, trials and post-authorization evidence generation are handled through the EU Clinical Trials Information System (CTIS), which lists ongoing authorized FSGS studies, including a 2025 CTIS-authorized trial. Initiatives such as PARASOL (Proteinuria and Other Biomarkers as Endpoints for Clinical Trials in Kidney Disease) have supported regulators' acceptance of proteinuria reduction as a surrogate endpoint, enabling pivotal studies with more feasible sample sizes for rare kidney diseases. At the same time, regulators have increased scrutiny of enrichment strategies, biomarker alignment, and subgroup performance when supporting labeling.

Competitive Landscape

The FSGS treatment market is moderately fragmented but trending toward consolidation as large pharma seeks scale and genetic-medicine expertise. Novartis detailed a USD 1.7 billion agreement to buy Regulus Therapeutics for its miR-based renal portfolio. Vertex acquired Alpine Immune Sciences for USD 4.9 billion to augment its APOL1 franchise. These deals underscore the view that targeted FSGS assets can secure premium pricing and long exclusivity due to orphan status.

Competition is shifting from broad immunosuppression to precision-validated modalities. Companies are co-developing companion diagnostics that flag APOL1 risk or complement-activation status, aiming to pre-select patients with the highest likelihood of response. AI-powered patient-finder algorithms are becoming table stakes; firms deploying such tools gain earlier market penetration and stronger real-world-evidence loops.

White-space opportunities endure in paediatric indications, regenerative podocyte therapy and drug-device combinations such as wearable dialysis filters. Barriers to entry remain high given the need for renal-biopsy infrastructure and specialised endpoints. Nonetheless, niche biotech innovators with first-in-class mechanisms continue to draw partnership interest, ensuring a dynamic pipeline that feeds sustained long-term growth of the FSGS treatment market.

Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry Leaders

F. Hoffmann-La Roche Ltd.

Genentech Inc.

Novartis AG

Merck KGaA

Travere Therapeutics Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The April 2026 FDA approval of FILSPARI (sparsentan) for proteinuria reduction in FSGS creates a clearer commercial and clinical pathway for therapies that can show meaningful proteinuria benefit, particularly for programs that align surrogate endpoints with PARASOL. The milestone also creates room for differentiated mechanisms beyond broad immunosuppression, including APOL1-targeted approaches and other precision strategies that combine treatment with genotyping, biomarker panels, and nephrology workflow tools used in hospitals, transplant centers, and specialty clinics.

Pipeline breadth also points to whitespace in earlier-line targeted regimens and pediatric care pathways that require age-appropriate dosing and safety evidence, supported by FILSPARI labeling down to age 8. Development activity further indicates ongoing demand for providers that can reduce rare-disease trial friction. For example, Akebia Therapeutics initiated a Phase 2 study of praliciguat in FSGS in December 2025 (ClinicalTrials.gov registry), reinforcing the need for specialized trial networks, patient identification, and longitudinal renal outcome monitoring to support faster evidence generation and more efficient market access planning.

Recent Industry Developments

- April 2026: Travere Therapeutics announced full FDA approval of FILSPARI (sparsentan) to reduce proteinuria in adults and pediatric patients aged 8 years and older with FSGS without nephrotic syndrome. The decision established the first FDA-approved medicine specifically indicated for FSGS, resetting competitive benchmarks around proteinuria-based benefit. It also gives Travere a near-term commercialization lever by extending its existing nephrology commercial footprint into a new labeled population.

- May 2025: Travere Therapeutics reported FDA acceptance of its supplemental New Drug Application for FILSPARI in FSGS, setting a PDUFA target action date of January 13, 2026. The filing formalized the company's regulatory path toward an FSGS label and signaled that proteinuria-based evidence could support an approvable package. The review timeline intensified competitive urgency for other late-stage programs pursuing differentiated endpoints and patient subgroups.

- April 2024: Vertex Pharmaceuticals advanced inaxaplin (VX-147) into the Phase 3 portion of its adaptive clinical program for APOL1-mediated kidney disease, including patients with FSGS, supported by FDA Breakthrough Therapy designation. Moving into Phase 3 increased visibility for genotype-directed approaches and reinforced APOL1 testing as a practical segmentation lever in nephrology clinics. The step-up in development stage also raised the importance of companion diagnostics and trial site capabilities focused on genetically defined cohorts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues linked to managing focal segmental glomerulosclerosis (FSGS), including diagnosis services used to confirm the condition and drug based treatment used to control proteinuria and slow kidney damage across major regions.

Scope exclusions: Procedures and services that are not tied to FSGS specific diagnosis or treatment decisions (such as general renal wellness programs) are not counted.

Segmentation Overview

- By Disease Type

- Primary FSGS

- Secondary FSGS

- By Disease Management

- Diagnosis

- Kidney Biopsy

- Creatinine Test

- Other Diagnostics

- Treatment

- Drug Therapy

- Corticosteroids

- Calcineurin Inhibitors

- Immunosuppressants

- Biologics

- APOL1 Inhibitors & Emerging Therapies

- Dialysis

- Hemodialysis

- Peritoneal Dialysis

- Kidney Transplant

- Drug Therapy

- Diagnosis

- By End User

- Hospitals & Transplant Centers

- Specialty Clinics & Nephrology Practices

- Dialysis Centers

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with aligning the disease definition and care pathway so we do not mix FSGS with broader CKD value pools. Public sources are used to anchor epidemiology and treatment patterns, such as CDC and NIH pages for kidney disease context, WHO health statistics, national payer or health ministry publications, and peer reviewed nephrology journals that describe diagnosis rules and common lines of therapy.

We also screen sources that explain pricing and utilization signals in a practical way, such as US FDA labels and approval databases for relevant therapies, clinical trial registries for pipeline timing, and customs or trade statistics where supportive medicines show import signals. Company filings, investor presentations, and reputable press are used to confirm launch timing and geographic focus, and paid subscriptions for company financials, news, and patent databases are used to cross check claims and fill gaps. These sources are illustrative only, and additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to sanity check the care pathway assumptions, including how often biopsy confirmation happens, when steroids or immunosuppressants are used, and how relapse and resistance affect duration of therapy. We speak with a mix of clinicians, hospital pharmacy stakeholders, and industry participants across Americas, EMEA, and APAC so regional reimbursement and access differences are reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | APAC: 46% |

| Mid tier: 50% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 19% | Managers: 46% | Americas: 23% |

Market-Sizing & Forecasting

The core model is built using a top-down, patient pool based demand build where prevalence and diagnosed share are converted into treated patients, and then filtered by typical regimen mix and treatment duration to reach annual spend. To keep the output realistic, the totals are corroborated with selective bottom-up checks like sampled therapy pricing by country, channel level uptake discussions, and supplier level signals where public financials allow a reasonability test.

Key inputs that are tracked include the estimated FSGS prevalence and diagnosis rate, biopsy confirmation tendencies, steroid resistance and relapse rates, share of patients moving to second line immunosuppressants or supportive care, and the mix between diagnosis activity and treatment spending. Price assumptions are handled using a simple ASP progression approach that reflects list price changes, expected discounting, and mix shift toward newer therapies where applicable, and then converted into USD using a consistent currency timing for the base year.

For forecasting, we use scenario analysis supported by trend smoothing on core drivers, because access changes and pipeline events can move uptake faster than historic patterns. When bottom-up checks cannot be run for a country due to limited public disclosure, we bridge gaps using regional analogs that match reimbursement type and nephrology center density, followed by expert validation before locking the final series.

Data Validation & Update Cycle

Outputs are validated through cross checks against independent signals such as epidemiology ranges, therapy utilization logic in guidelines, and country level access constraints, and then the main variances are reviewed by a second analyst before sign off. When a value looks off, the driver assumptions are re-opened and targeted follow ups are done with experts to confirm whether it is a real change or a modeling artifact.

Reports are refreshed annually, and interim updates are triggered when there are material events like approvals, safety warnings, or sharp pricing changes that affect ASPs and treatment mix. Before delivery, the model gets a fresh pass so the final numbers reflect the latest public releases and primary feedback available at that time.

Mordor Intelligence's Focal Segmental Glomerulosclerosis Treatment Market Size Versus Other Published Estimates

Published market sizes for FSGS treatment often do not line up because the boundary between diagnosis spend, drug therapy, dialysis, and transplant related costs is not handled the same way. Differences also come from the year used for currency conversion, how prices are trended forward, and whether the publisher refreshes assumptions right after major clinical or regulatory updates.

A refresh-led view usually explains the biggest spread, because if ASP logic is updated using the latest list price moves and expected discounting, and currency conversion is locked to a consistent base-year window, the total will move even when patient counts are stable, which is a step applied in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.90 B (2026) | |

| Global Consultancy A | USD 2.39 B (2025) | This figure appears to be scoped around treatment modalities like dialysis, drug therapy, and transplant with a narrower revenue capture, which can exclude diagnosis spend and broader supportive management that is tied to FSGS follow up. |

| Industry Publisher B | USD 14.75 B (2024) | This estimate is presented as an FSGS drugs only view with a different base year, so it can diverge due to excluding diagnosis services and using a separate price growth curve and FX timing versus a combined disease management view. |

The table shows that scope boundaries and the timing of price and currency assumptions matter as much as the patient pool itself. By keeping each input tied to a visible care pathway step and by rechecking key pricing and access assumptions during updates, the model stays traceable and easier to reproduce when clients want to test scenarios.

Key Questions Answered in the Report

What is the current value of the FSGS treatment market?

The FSGS treatment market size is USD 15.9 billion in 2026, with a forecast value of USD 21.63 billion by 2031.

How fast is the market expected to grow?

Global revenue is projected to expand at a 6.34% CAGR from 2026 to 2031.

Which disease type represents the largest revenue share?

Primary FSGS leads with 60.42% of global sales in 2025 and is also the fastest-growing disease type.

Which region is expanding most rapidly?

Asia Pacific is forecast to grow at an 17.95% CAGR, driven by improved nephrology infrastructure and wider access to precision therapies.

What therapeutic modality is seeing the highest growth?

Drug therapy within disease management is registering a 11.82% CAGR, propelled by APOL1 inhibitors and other targeted agents.

Who are the leading companies in this space?

Travere Therapeutics, Vertex Pharmaceuticals, Novartis and Amicus Therapeutics are among the prominent players advancing late-stage assets and strategic acquisitions.

Page last updated on: