Flexible Electrical Conduit Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

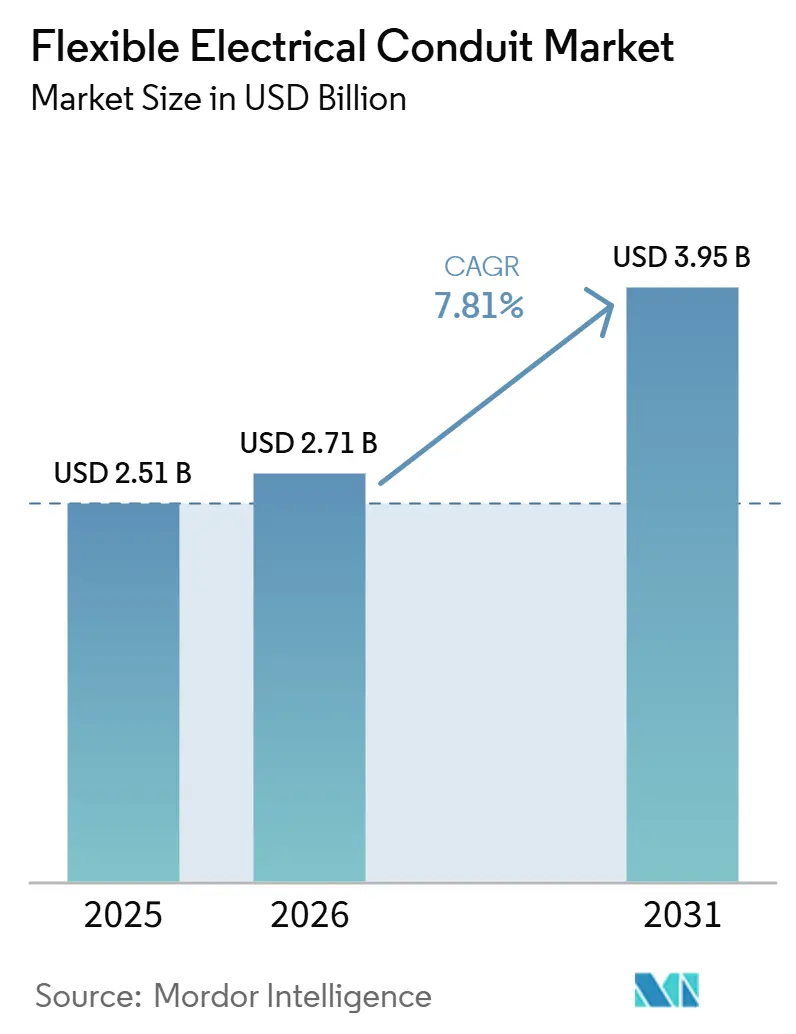

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 3.95 Billion |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

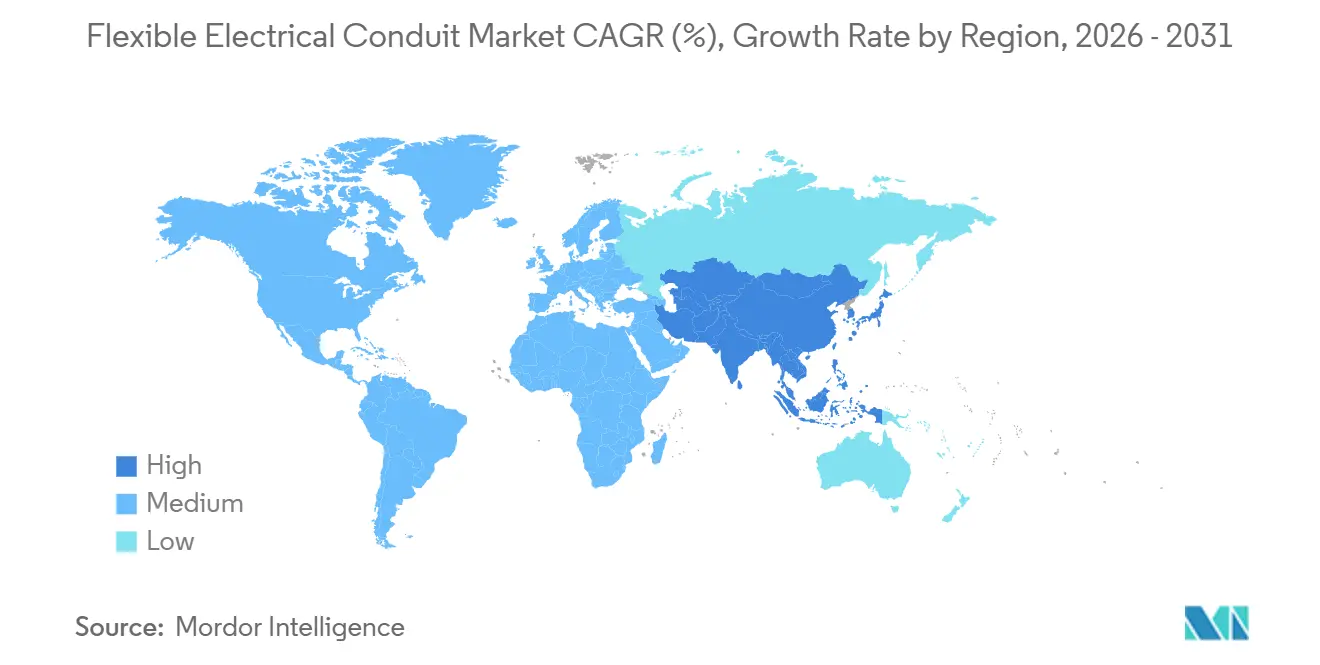

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Electrical Conduit Market Analysis by Mordor Intelligence

The Flexible Electrical Conduit Market size is expected to grow from USD 2.51 billion in 2025 to USD 2.71 billion in 2026 and is forecast to reach USD 3.95 billion by 2031 at 7.81% CAGR over 2026-2031. The expansion of data center construction, 5G network densification, and infrastructure modernization is increasing the demand for liquid-tight and flame-retardant products. Public-sector grid upgrades in countries such as China, India, and Brazil are driving multi-year procurement cycles for conduits, fittings, and accessories. The growing adoption of robotics in manufacturing and electric vehicle (EV) battery production lines is boosting the need for ultra-flexible, EMI-shielded variants capable of withstanding millions of bend cycles. Additionally, halogen-free building codes in Europe and Asia are accelerating the shift from PVC to low-smoke zero-halogen (LSZH) compounds, despite their 10-15% price premium. Meanwhile, volatility in metal prices, such as a 20.7% increase in steel, a 33.0% rise in aluminum, and copper reaching USD 6.01 per lb in January 2026, is prompting manufacturers to adjust their portfolios toward non-metallic alternatives.

Key Report Takeaways

- By type, flexible metallic tubing led with 30.2% of the flexible electrical conduit market share in 2025, while liquid-tight flexible non-metallic conduit is projected to expand at a 9.4% CAGR through 2031.

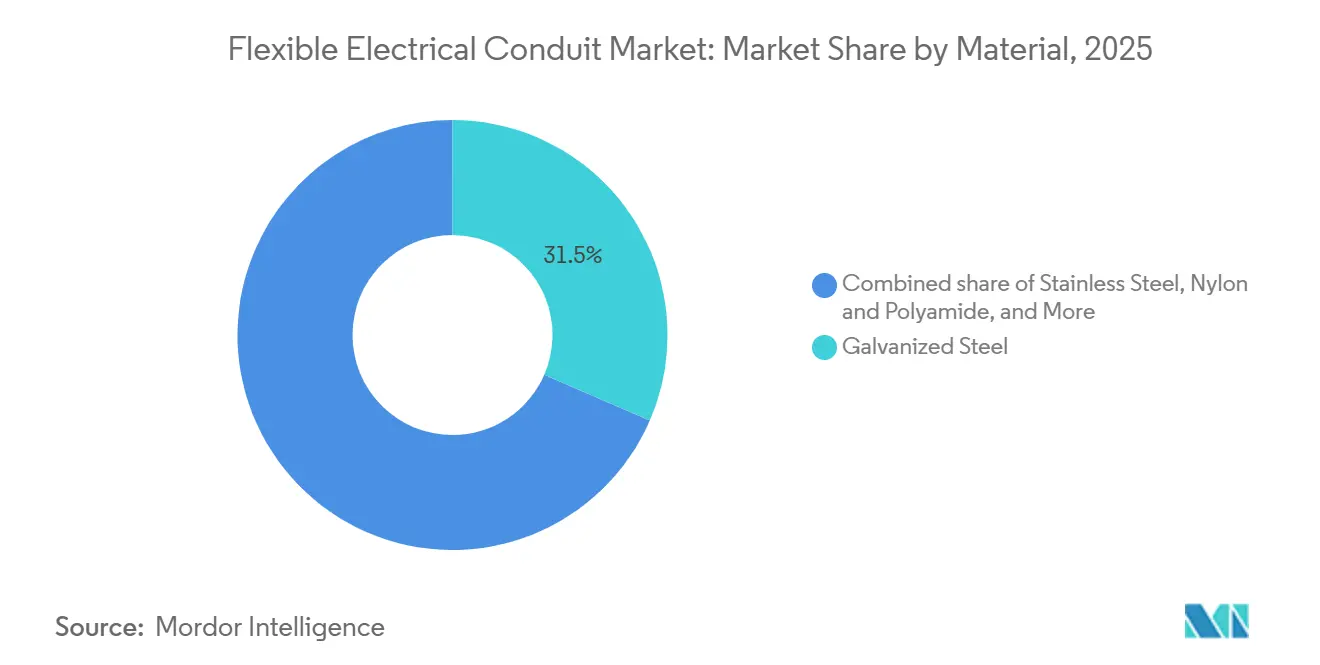

- By material, galvanized steel accounted for 31.5% share of the flexible electrical conduit market size in 2025, and nylon/polyamide is forecasted to advance at a 10.1% CAGR between 2026 and 2031.

- By application, power distribution held 27.8% revenue in 2025; data communication and signal transmission are accelerating at a 10.5% CAGR through 2031.

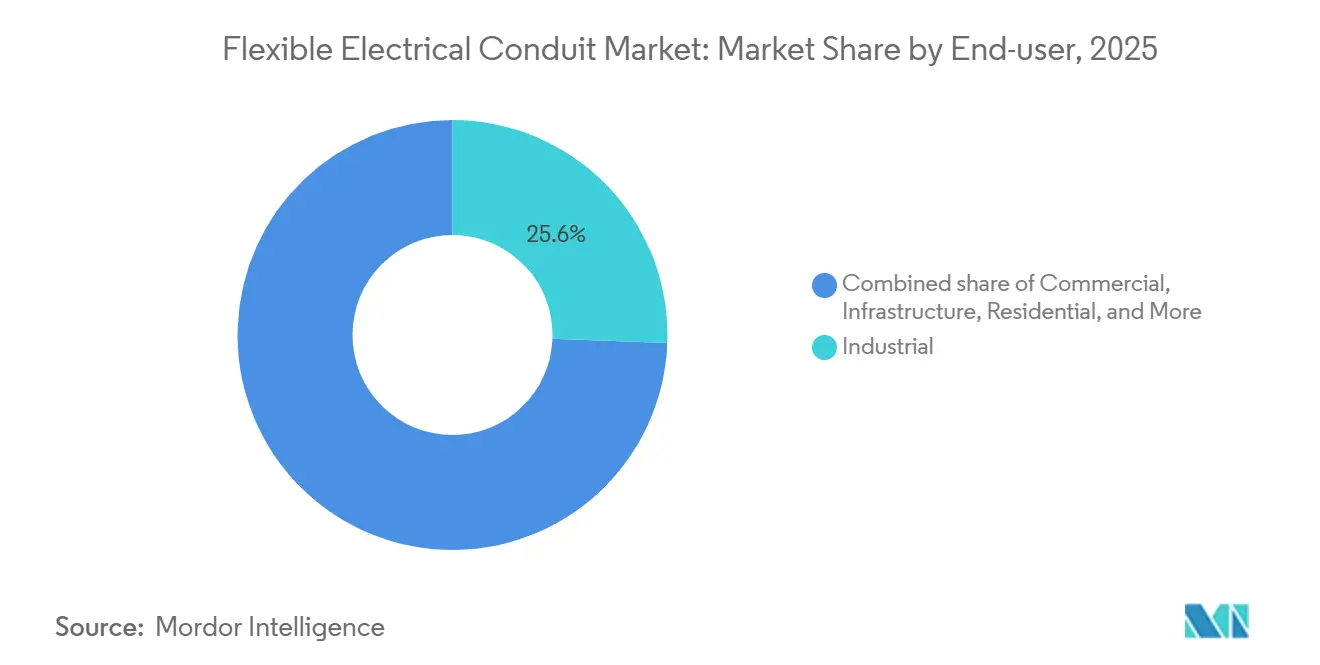

- By end-user, industrial facilities represented 25.6% of demand in 2025, whereas infrastructure projects are expanding at a 9.0% CAGR to 2031.

- By geography, North America captured 35.0% of 2025 revenue, yet Asia-Pacific is the fastest-growing region at an 8.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flexible Electrical Conduit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of data-center & 5G cabling needs | +1.80% | Global, with concentration in North America, China, India, ASEAN | Medium term (2-4 years) |

| Urban infrastructure retrofits favouring flexible installs | +1.20% | North America & Europe, with spillover to urbanized Asia-Pacific metros | Short term (≤ 2 years) |

| Renewables build-out requiring UV/corrosion-resistant conduit | +1.50% | Global, with early gains in India, China, Brazil, Middle East GCC | Long term (≥ 4 years) |

| Stricter industrial safety codes for liquid-tight & flame-retardant wiring | +1.00% | Global, led by North America (NEC), Europe (IEC), China (GB standards) | Medium term (2-4 years) |

| Robotics boom driving demand for ultra-flex dynamic conduit | +0.70% | Asia-Pacific (China, Japan, South Korea), North America, Germany | Medium term (2-4 years) |

| EMI-shielded conduit adoption in EV battery lines | +0.60% | Asia-Pacific (China, South Korea), North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Data-Center and 5G Cabling Needs

Hyperscale facilities necessitate high-density cable routes that are frequently reconfigured, making flexible metallic tubing and liquid-tight variants essential for hot-aisle containment and overhead ladder racks. China’s State Grid is projected to invest USD 574 billion in distribution upgrades during 2026-2030, with a significant portion directed toward AI data hubs. Additionally, 5G macro and small-cell sites depend on UV-stable nylon conduit to protect fiber and power feeds from temperature fluctuations and moisture ingress. The Asian Development Bank earmarked USD 10 billion for the ASEAN Power Grid, including cross-border links that support edge-computing nodes. (1)Asian Development Bank, “ASEAN Power Grid Initiative,” bidsfactory.comThe U.S. Department of Energy projects AI-server electricity demand could reach 165-325 TWh by 2028, sustaining investment in power and signal pathways.(2)Asian Power, “AI Server Electricity Forecast,” asian-power.com

Urban Infrastructure Retrofits Favouring Flexible Installs

Aging buildings are incorporating EV chargers, rooftop solar panels, and battery systems, requiring contractors to route conduit through tight spaces where rigid EMT is unsuitable. Flexible products reduce labor hours by 20-30% in retrofit projects, as bends can be shaped manually without the need for specialized tools. U.S. rail agencies updating to NFPA 130 standards are specifying LSZH conduit in tunnels for smoke-toxicity compliance. (3)NFPA, “National Electrical Code 2026,” nfpa.org Brazilian distribution companies have planned investments totaling BRL 235.7 billion (USD 43.5 billion) for upgrades between 2025 and 2029. Of this, nearly BRL 91 billion is allocated for improvements and renewals, with a significant focus on flexible solutions. Additionally, rooftop HVAC retrofits increasingly utilize liquid-tight conduit due to its ability to withstand thermal expansion without cracking.

Renewables Build-Out Requiring UV and Corrosion-Resistant Conduit

Photovoltaic farms, offshore wind turbines, and desert substations require conduits capable of withstanding salt spray, solar radiation, and continuous temperatures of up to 90°C. India’s Central Electricity Authority has outlined a transmission investment of INR 7.93 trillion (USD 85 billion) to integrate 900 GW of non-fossil fuel capacity by 2036, driving demand for LSZH and stainless-steel conduits. Brazil plans to construct 8,400 km of new transmission lines by 2039, with a budget of BRL 40 billion (USD 7.4 billion). Offshore installations in the North Sea utilize stainless-steel flexible conduits within nacelles to resist vibration and salt fog, which would otherwise corrode galvanized steel in a matter of months. Submarine cable landing stations in Laos and Cambodia employ corrosion-resistant nylon conduits as part of the ASEAN Power Grid roadmap.

Stricter Industrial Safety Codes for Liquid-Tight and Flame-Retardant Wiring

NFPA 70 Article 501 permits the use of liquid-tight flexible metal conduit in Class I, Division 1 zones, leading chemical and petrochemical facilities to upgrade pump-motor connections with compliant fittings. Standards such as UL 360 and UL 1660 specify requirements for oil resistance, sunlight durability, and flexibility at –40 °C, encouraging their use in outdoor refinery environments. In Europe, the ATEX Directive 2014/34/EU mandates the use of CE-marked conduits in explosive atmospheres, thereby limiting the number of eligible suppliers. China’s GB 50217 requires low-smoke zero-halogen products in subways and hospitals, pushing manufacturers to reformulate PVC or shift to specialty thermoplastics. (4)IEC, “Low-Smoke Halogen-Free Standards EN 50267 & IEC 61249,” iec.ch Semiconductor fabs demand UL 94 V-0 conduit to minimize particulate generation in clean rooms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material (metal, PVC) price volatility | -1.30% | Global, with acute pressure in North America and Europe due to tariffs | Short term (≤ 2 years) |

| Competition from low-cost cable-tray solutions | -0.90% | North America & Europe commercial construction, with limited impact in hazardous locations | Medium term (2-4 years) |

| Halogen-free building codes hitting PVC demand | -0.60% | Europe, China, Australia, with spillover to North America transit projects | Medium term (2-4 years) |

| Geopolitical supply risk for specialty nylon & SS braid | -0.40% | Global, with concentration risk in adiponitrile (US, France) and stainless steel (China, India) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility Constraining Margin Expansion

Metal conduit manufacturers face challenges due to significant increases in the prices of steel, aluminum, and copper, which surpass their ability to adjust quarterly contract pricing. In January 2026, steel prices averaged 20.7% higher compared to the previous year, aluminum prices increased by 33%, and copper reached USD 6.01 per pound. These cost pressures have reduced gross margins on galvanized products by 200-300 basis points. Additionally, a 50% tariff on certain imports into the United States has forced producers to rely on North American smelters or redirect supply chains through USMCA partners, resulting in longer lead times. While PVC prices declined by 26% in 2025, an oversupply in Asia prevented North American extruders from benefiting from freight cost reductions, further narrowing the price differential with imported pipes. Nylon supply remains constrained by the limited number of adiponitrile plants globally, only four facilities, which makes the supply chain vulnerable to disruptions, impacting industries such as robotics and electric vehicles.

Competition from Low-Cost Cable-Tray Solutions

Open-ceiling offices and data halls utilize ladder trays, reducing installation labor by up to 50% as multiple circuits share a single pathway. Prefabricated electrical skids, delivered with pre-installed tray wiring, replace several kilometers of conduit per project. However, demand for flexible electrical conduit continues in hazardous, underground, and EMI-sensitive areas where ladder trays are prohibited under NEC Article 392. Hybrid approaches, such as using trays for main runs and conduit for last-meter drops, or complete substitution, are employed, though price pressures remain high in standard commercial applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Liquid-Tight Variants Gain Share in Corrosive Environments

Flexible metallic tubing accounted for 30.2% of the flexible electrical conduit market in 2025, reflecting its cost-effectiveness and compliance with NEC standards for dry-location branch circuits. In contrast, liquid-tight flexible non-metallic conduit (LFNC) is projected to grow at a compound annual growth rate (CAGR) of 9.4% through 2031, driven by demand from wastewater plants, food processors, and marine operators for corrosion-resistant solutions.

Labor efficiency is a key factor in LFNC adoption. Weighing 40% less than liquid-tight flexible metallic conduit (LFMC), LFNC allows for longer spans with fewer supports, reducing retrofit labor costs by up to 20%. Additionally, EV-charging stations increasingly specify sunlight-resistant, UL 1660-listed LFNC for pedestal runs capable of withstanding temperature cycles from –40 °C to 80 °C. Ultra-flexible metal conduit with high-tensile stainless steel braid is becoming a standard for robotic end-effectors, which require bend radii under 40 mm and the ability to endure millions of cycles. While flexible metallic conduit remains widely used in mid-rise commercial cores, its market share is expected to decline gradually due to evolving codes and heightened concerns over corrosion risks.

By Material: Nylon & Polyamide Surge on Robotics and Automotive Demand

Galvanized steel accounted for 31.5% of the projected 2025 revenue, highlighting its mechanical strength and cost advantage in the flexible electrical conduit market. Nylon and polyamide are expected to grow at a compound annual growth rate (CAGR) of 10.1% through 2031, driven by demand from robot manufacturers and electric vehicle (EV) powertrains requiring abrasion-resistant and flexible pathways.

Adiponitrile supply constraints have kept nylon 66 prices at a 45% premium over PVC. However, original equipment manufacturers (OEMs) are absorbing these higher costs to prevent downtime in high-speed assembly operations. Stainless-steel conduit, while currently holding a single-digit market share, is gaining traction in pharmaceutical clean rooms due to 316L stainless steel's resistance to chloride corrosion and its superior electromagnetic interference (EMI) shielding properties. Aluminum is being utilized to address load restrictions in offshore platforms and aircraft hangars. Additionally, European Construction Product Regulation (CPR) standards (EN 50267/50575) and China’s GB 50217 have restricted the use of standard PVC in many public settings, accelerating the shift to low-smoke zero-halogen (LSZH) formulations. While LSZH materials increase costs, they enhance fire safety credentials, aligning with regulatory requirements.

By Application: Data Communication Fastest on Cloud Infrastructure Boon

In 2025, power distribution accounted for a 27.8% share; however, it is losing relative momentum to data communication and signal transmission, which are growing at a CAGR of 10.5% due to the increasing number of hyperscale campuses. The demand for flexible electrical conduit in server farms is supported by the strict segregation of power and fiber channels to reduce crosstalk.

For underground utilities, PVC and HDPE are preferred materials for duct banks, while above-grade rack power drops are increasingly using shielded metallic conduit to minimize electromagnetic noise. The HVAC and refrigeration segments remain stable but are characterized by mature markets, driven primarily by replacement activities rather than new installations. Additionally, the development of EV-charging corridors is contributing to incremental demand for outdoor liquid-tight conduit, with each fast-charger island requiring 20-30 meters of conduit for power, control, and network cabling.

By End-User: Infrastructure Leads Growth on Climate-Resilient Mandates

Industrial facilities are projected to account for 25.6% of 2025 sales, driven by the use of explosion-proof LFMC and LSZH variants to meet NEC and ATEX requirements. However, infrastructure applications, including airports, subways, and tunnels, are expected to grow at a compound annual growth rate (CAGR) of 9.0% through 2031, representing the fastest-growing segment within the flexible electrical conduit market.

Airports in regions such as the United States, the Gulf Cooperation Council, and India are upgrading terminals with LSZH stainless conduits to comply with NFPA 415 and ICAO smoke-toxicity standards. In Brazil, the BRL 40 billion (~USD 7.75 billion) grid expansion pipeline is driving consistent demand for transmission-yard raceways. Residential adoption of flexible electrical conduits is closely linked to housing starts and renovation activities. Additionally, distributed energy retrofits, including solar and storage systems, are increasing the number of conduit installations per dwelling. Utilities and renewable energy developers are specifying corrosion-resistant options for substations located in coastal areas prone to salt spray and high humidity.

Geography Analysis

North America accounted for 35.0% of the global revenue in the flexible electrical conduit market for 2025, driven by data-center clusters in Virginia, Texas, and Oregon. Strict enforcement of the National Electrical Code (NEC) sustains demand for liquid-tight and armored conduit variants. However, higher interest rates are expected to moderate commercial real estate developments in 2026. In Canada, corridor projects in Ontario and British Columbia depend on conduit for grid interconnections, while Mexico's growing automotive industry increases demand for hazardous-area conduit solutions.

The Asia-Pacific region is projected to achieve the highest compound annual growth rate (CAGR) globally, at 8.8% through 2031. China's annual grid investment of RMB 800 billion (USD 115 billion) and India's INR 7.93 trillion (USD 85 billion) transmission infrastructure plan create substantial opportunities for conduit deployment. The ASEAN region's USD 10 billion interconnector initiative drives demand for corrosion-resistant conduit in submarine cable landing zones. Additionally, semiconductor manufacturing facilities in Japan and South Korea require ultra-flexible and EMI-shielded conduit solutions for ISO-class clean rooms, further boosting market volumes.

Europe's market growth is steady and primarily driven by regulatory compliance. EN 50267 and ATEX standards are phasing out PVC conduit, promoting the adoption of low-smoke zero-halogen (LSZH) conduit in metropolitan areas such as Paris and Warsaw. Offshore wind platforms in the North Sea and Baltic Sea specify stainless-steel flexible conduit with salt spray resistance, as per IEC 60068-2-52 standards. In Southern Europe, energy storage facilities favor aluminum or nylon conduit to reduce structural loads on roof-mounted solar arrays.

In South America, Brazil leads the market with an investment of BRL 235.7 billion (USD 45.65 billion) through 2029 for distribution network upgrades, incorporating conduit in every feeder bay. In the Middle East, Gulf nations are advancing gigawatt-scale solar projects, necessitating UV-stable nylon conduit capable of withstanding ambient desert temperatures of up to 50 °C.

Competitive Landscape

The flexible electrical conduit market is moderately fragmented. Key global players, including Atkore, Eaton, ABB, Legrand, and Schneider Electric, leverage vertical integration and material research and development (R&D) to manage raw material volatility. Hubbell's acquisition of DMC Power for USD 825 million in 2025 expanded its fittings portfolio and added two manufacturing facilities in the United States. Atkore divested its Tectron Tube line in 2025 and plans to close three plants in fiscal Q2 2026, aiming for annual savings of USD 30 million.

Regional specialists such as HellermannTyton, Electri-Flex, and Anamet focus on differentiation through high-flex robotics products and quick-turn custom lengths tailored for original equipment manufacturers (OEMs). Asian competitors like Delikon Tubing and CTUBE compete by offering prices 15-20% lower than multinational companies, along with halogen-free grades designed for Chinese GB 50217 projects. R&D efforts are concentrated on composite conduits with metallic cores for electromagnetic interference (EMI) shielding and thermoplastic over-jackets for corrosion resistance. Patent activity is focused on push-lock fittings, which reduce installation times by 30% compared to threaded hubs.

Rising input cost pressures are driving market consolidation. Olympus Partners merged International Wire Group, Hussey Copper, EMS ElektroMetall, and Special Corde under Pantheon Electric in 2026 to secure copper cathode supplies and provide turnkey solutions from busbars to conduits. Sustainability is becoming a key differentiator: ABB's 2026 roadmap aims to achieve 80% recycled steel usage in its metallic conduits by 2030, while Atkore has pilot-tested bio-PVC formulations containing 30% plant-based plasticizer at its Phoenix facility.

Flexible Electrical Conduit Industry Leaders

Atkore International Group Inc.

ABB Ltd.

Eaton Corporation plc

Schneider Electric SE

HellermannTyton

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Pantheon Electric has introduced a new platform that integrates International Wire Group, Hussey Copper, EMS Elektro Metall, and Special Corde. This initiative creates a vertically integrated supplier of copper conductors, busbars, flexible busbars, and high-current connectors, with support from Olympus Partners. The consolidation aims to enhance margins across the electrical value chain and deliver comprehensive solutions for data centers, renewable energy projects, and industrial automation.

- May 2025: Schneider Electric has commenced a USD 73.6 million expansion at its Columbia, Missouri facility. The project will enhance warehouse capacity and introduce new production lines for commercial circuit breaker components. Scheduled for completion by March 2026, the expansion is projected to generate 241 jobs. This initiative is part of Schneider Electric's broader USD 700 million U.S. investment program, planned through 2025, to support electrification and renewable energy integration.

- January 2025: ABB and Wieland Electric introduced a modular electrical distribution platform designed to reduce on-site conduit installation time by 70% and decrease total costs by 30%.

- August 2024: The U.S. Department of Energy has allocated USD 2.2 billion to 18 states to enhance grid resilience, including new bidding opportunities for corrosion-resistant LFMC installations in transmission rebuild projects.

Global Flexible Electrical Conduit Market Report Scope

Flexible electrical conduit is a durable, bendable tube, typically made of metal or plastic with a corrugated or spiral design, used to protect electrical wiring in confined spaces, corners, or areas that require vibration resistance. It is commonly used to connect junction boxes to electrical equipment, providing a flexible alternative to rigid pipes.

The Flexible Electrical Conduit Market is segmented into type, material, application, end-user, and geography. By type, the market is segmented into flexible metallic conduit, liquidtight flexible non-metallic conduit, liquidtight flexible metal conduit, and flexible metallic tubing. By material, the market is segmented into galvanized steel, stainless steel, aluminum, PVC, nylon, polyamide, and others. By application, the market is segmented into power distribution, data communication, HVAC, machinery, underground wiring, and others. By end-user, the market is segmented into commercial, industrial, residential, infrastructure, utilities, transportation, and others. The report also covers the market size and forecasts for the flexible electrical conduit market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Flexible Metallic Conduit |

| Liquidtight Flexible Non-Metallic Conduit (LFNC) |

| Liquidtight Flexible Metal Conduit (LFMC) |

| Flexible Metallic Tubing (FMT) |

| Galvanized Steel |

| Stainless Steel |

| Aluminum |

| Polyvinyl Chloride (PVC) |

| Nylon & Polyamide |

| Others |

| Power Distribution |

| Data Communication & Signal Transmission |

| HVAC & Refrigeration |

| Machinery & Equipment |

| Underground Wiring |

| Others |

| Commercial |

| Industrial |

| Residential |

| Infrastructure (Airports, Rail, Tunnels, etc.) |

| Utilities & Energy |

| Transportation (Marine, Automotive, Railways) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Flexible Metallic Conduit | |

| Liquidtight Flexible Non-Metallic Conduit (LFNC) | ||

| Liquidtight Flexible Metal Conduit (LFMC) | ||

| Flexible Metallic Tubing (FMT) | ||

| By Material | Galvanized Steel | |

| Stainless Steel | ||

| Aluminum | ||

| Polyvinyl Chloride (PVC) | ||

| Nylon & Polyamide | ||

| Others | ||

| By Application | Power Distribution | |

| Data Communication & Signal Transmission | ||

| HVAC & Refrigeration | ||

| Machinery & Equipment | ||

| Underground Wiring | ||

| Others | ||

| By End-user | Commercial | |

| Industrial | ||

| Residential | ||

| Infrastructure (Airports, Rail, Tunnels, etc.) | ||

| Utilities & Energy | ||

| Transportation (Marine, Automotive, Railways) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the flexible electrical conduit market?

It stands at USD 2.71 billion in 2026 and is projected to reach USD 3.95 billion by 2031.

Which region offers the fastest growth prospects?

Asia-Pacific is set to expand at an 8.8% CAGR thanks to grid upgrades in China, India, and ASEAN states.

Which conduit type is growing quickest?

Liquidtight flexible non-metallic conduit is expected to grow at a 9.4% CAGR through 2031.

How are halogen-free regulations affecting material choices?

They are reducing PVC usage in Europe and China and boosting LSZH, nylon, and stainless-steel alternatives.

What impact do metal price swings have on suppliers?

Steel, aluminum, and copper volatility squeezes margins and encourages a shift toward non-metallic conduit lines.

Where is robotics adoption driving conduit demand?

Japan, South Korea, Germany, and U.S. EV battery plants use ultra-flex nylon conduit to support dynamic cable motion.

Page last updated on: