Electric Insulator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.32 Billion |

| Market Size (2031) | USD 31.98 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

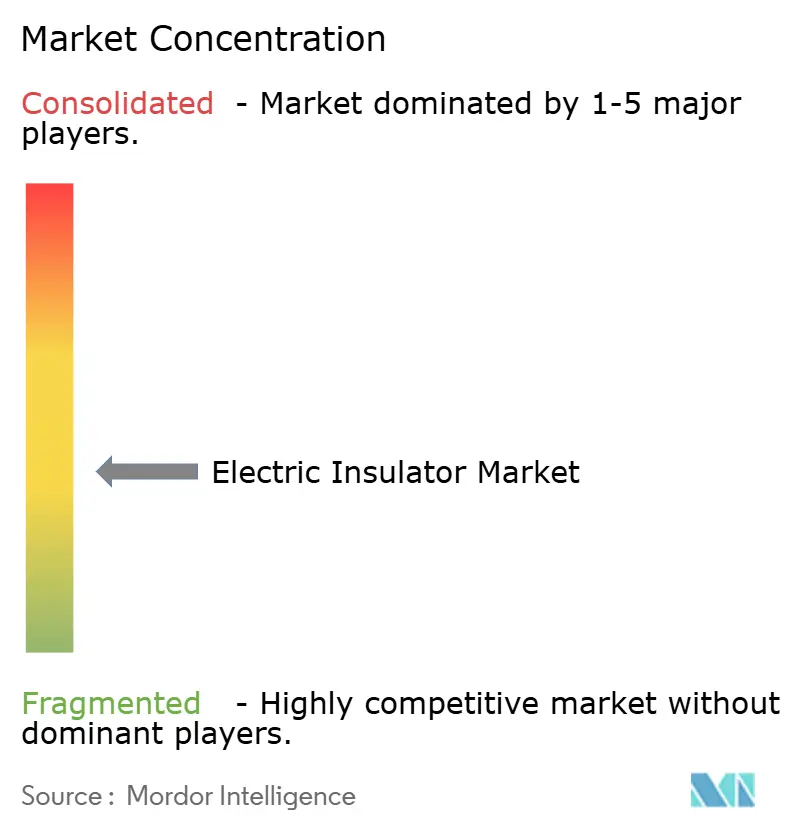

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Insulator Market Analysis by Mordor Intelligence

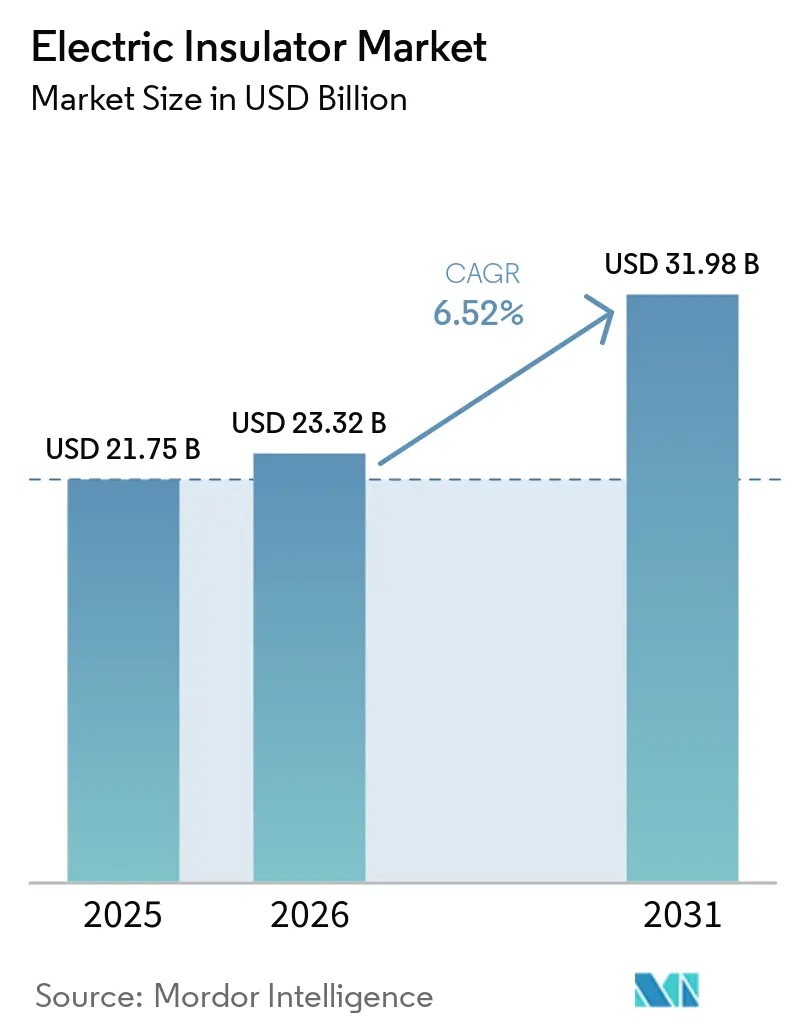

The Electric Insulator Market size is projected to expand from USD 21.75 billion in 2025 and USD 23.32 billion in 2026 to USD 31.98 billion by 2031, registering a CAGR of 6.52% between 2026 to 2031.

This growth trajectory reflects a structural shift in power infrastructure priorities as utilities worldwide confront climate-induced grid failures, accelerate HVDC interconnections, and the electrification of transport corridors. Sustained grid-hardening programs, the rapid adoption of >220 kV HVDC links, and the electrification of transport corridors are reshaping capital-spending priorities and lifting replacement demand, driven by China’s ultra-high-voltage build-out and India’s renewable-evacuation corridors. Competitive intensity is rising as Chinese manufacturers, Dalian Insulator Group, Zhejiang TCI, scale composite production to half the landed cost of Western incumbents, triggering quality disputes and safety recalls that have prompted IEC 62217 tightening and utility pre-qualification audits extending beyond 18 months in OECD markets.

Key Report Takeaways

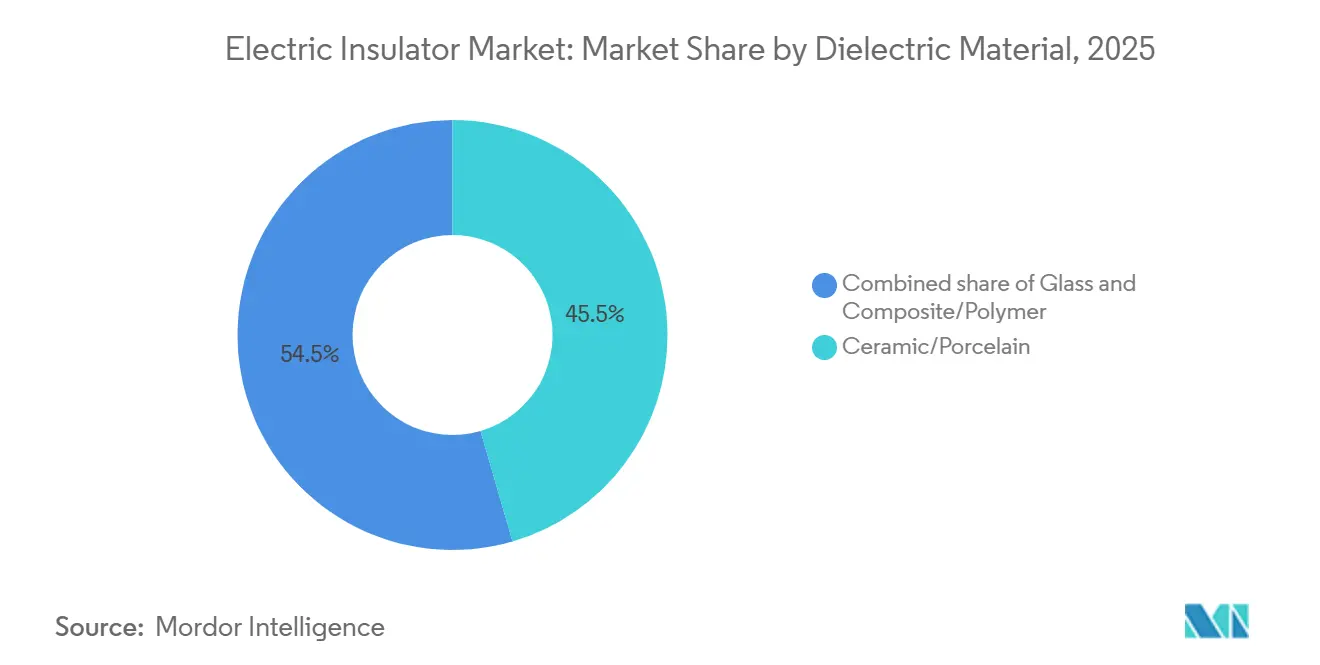

- By dielectric material, ceramic and porcelain held 45.5% of the electric insulator market share in 2025, while composite and polymer variants are expected to post a 7.7% CAGR through 2031.

- By voltage rating, medium-voltage products captured 40.2% of the electric insulator market size in 2025, and extra-high voltage units (>765 kV) are projected to expand at a 7.8% CAGR between 2026 and 2031.

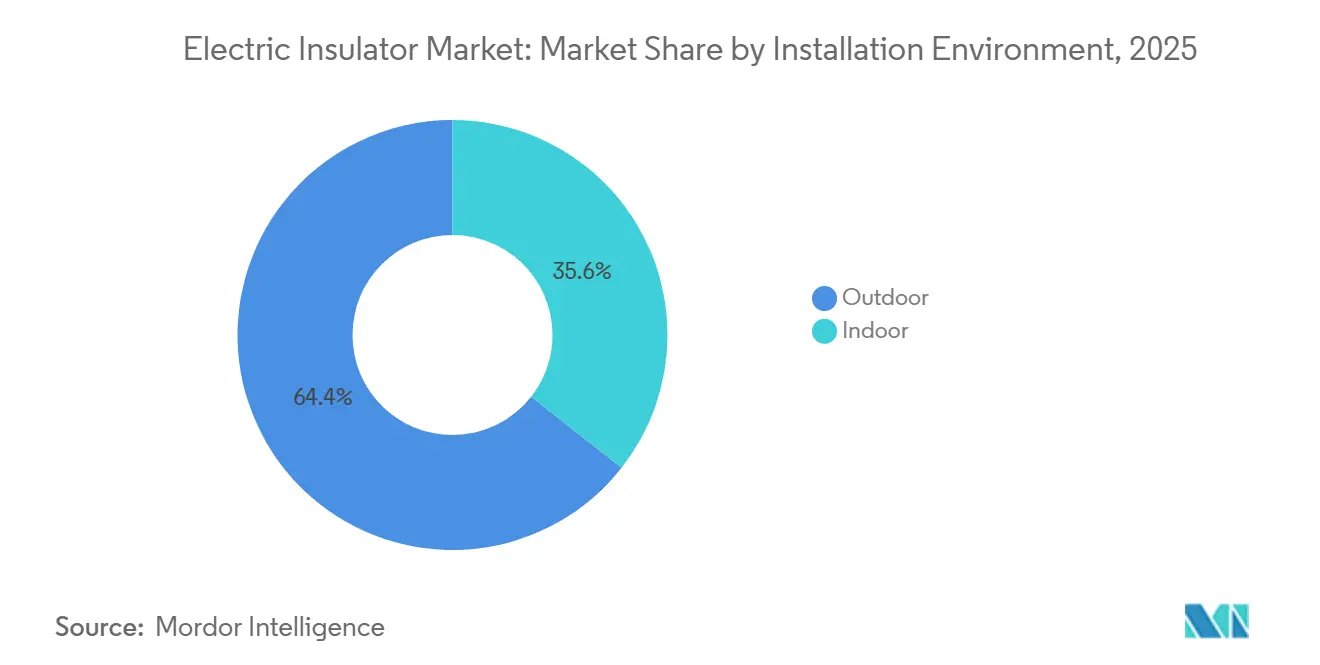

- By installation environment, outdoor insulators accounted for 64.4% revenue share in 2025 and are expected to advance at a 7.0% CAGR through 2031.

- By application, transmission lines led with 41.8% share of the electric insulator market size in 2025; within that category, HVDC lines are expected to grow at a 7.5% CAGR to 2031.

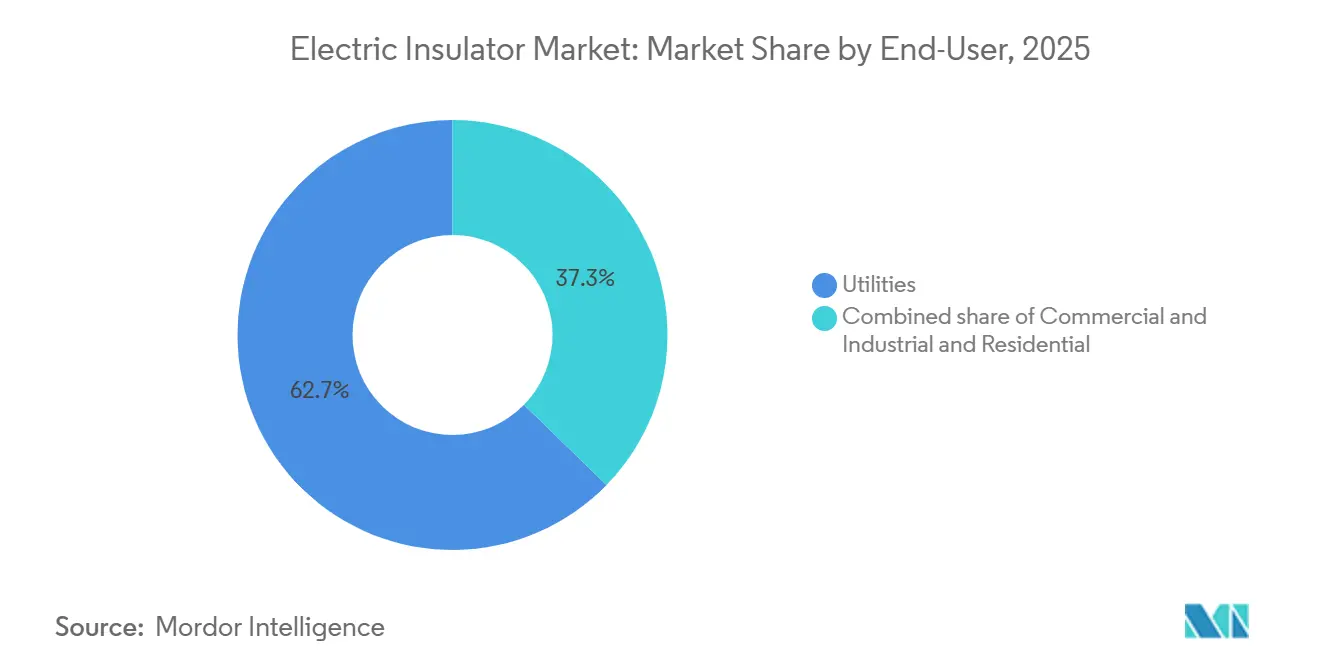

- By end user, utilities dominated with 62.6% electric insulator market share in 2025 and are expected to expand at a 7.2% CAGR over the forecast window.

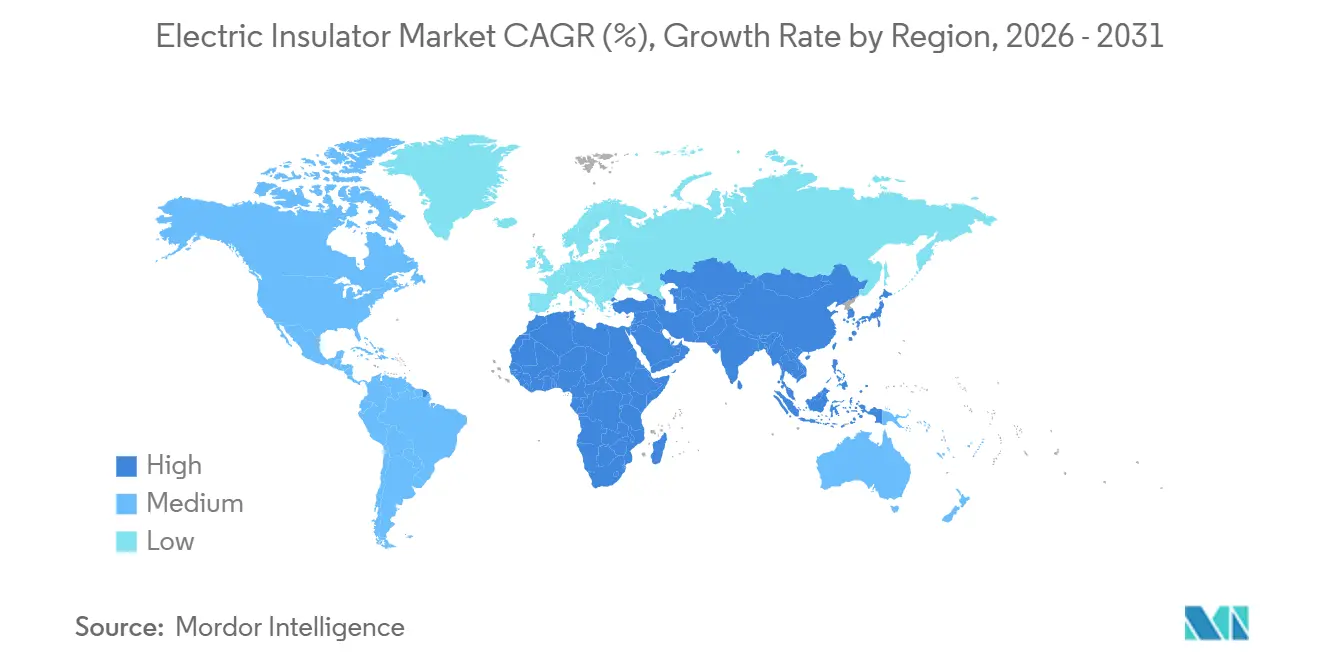

- By geography, Asia-Pacific held 54.7% of the market share in 2025, and the same is projected to grow at 7.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Insulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-hardening spend for climate-resilient T&D infrastructure | 1.8% | Global, with concentration in North America, Australia, Mediterranean Europe | Medium term (2-4 years) |

| Electrification of rail freight corridors in Asia & Europe | 0.7% | Asia-Pacific (India, China, ASEAN), Europe (Germany, France, Poland) | Long term (≥4 years) |

| Rapid build-out of >220 kV HVDC links in China & India | 2.1% | Asia-Pacific core, spillover to Middle East and South America | Long term (≥4 years) |

| Utilities' composite-insulator retrofits to cut wildfire risk | 1.3% | North America (California, Pacific Northwest), Australia, Southern Europe | Short term (≤2 years) |

| AI-enabled predictive maintenance boosting replacement demand | 0.9% | OECD markets initially, expanding to emerging Asia by 2028 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Hardening Spend for Climate-Resilient T&D Infrastructure

Wildfire- and hurricane-prone utilities are channeling 20-30% of capital budgets into hardening overhead assets, shifting investment from capacity additions to resilience. The U.S. Infrastructure Investment and Jobs Act earmarks USD 65 billion for modernization, including USD 5 billion dedicated to transmission resilience.[1]U.S. Department of Energy, “Grid Modernization Programs,” energy.gov California utilities intend to replace 600,000 ceramic units with composites by 2028, a USD 1.2 billion program mandated by state wildfire-mitigation rules.[2]California Public Utilities Commission, “Wildfire Mitigation Plans,” cpuc.ca.gov Australia’s Energy Security Board requires composite products on all new 132 kV-plus lines in bushfire zones.[3]Australian Energy Market Operator, “Bushfire Standards,” aemo.com.au Germany’s TSOs plan EUR 2.8 billion in weather-resilient upgrades covering 8,000 km of lines by 2030.[4]Bundesnetzagentur, “Transmission Investment Plans,” bundesnetzagentur.de Standards such as IEEE 1724 and ISO 9001 are embedded in procurement.

Rapid Build-Out of >220 kV HVDC Links in China & India

State Grid Corporation commissioned three ±800 kV corridors in 2025, together consuming more than 1.2 million insulators rated above 765 kV. India’s Power Grid awarded USD 3.1 billion for six HVDC bipoles totaling 18 GW, led by the 6 GW Raigarh-Pugalur line that alone requires 420,000 units. Brazil, Saudi Arabia, and other markets are adopting similar schemes, each demanding specialized composite designs resilient to humidity and sand. IEC 60071 and IEC 61109 guide insulation coordination and material choice in these ultra-high-stress corridors.

Utilities’ Composite-Insulator Retrofits to Cut Wildfire Risk

Hydrophobic silicone-rubber sheds deter conductive pollution layers that can arc and ignite vegetation, a failure mode blamed for the 2018 Camp Fire in California. PG&E replaced 87,000 porcelain devices across 2,400 circuit-miles in high-fire-threat districts during 2024, cutting fault-induced ignitions by 34%. Ausgrid and Essential Energy now specify composites on all new 132 kV and 330 kV assets in bushfire zones. Southern European utilities are following under pressure from insurers that tie coverage to certified fire-risk mitigation. ASTM D6815 and IEC 62217 testing are standard.

AI-Enabled Predictive Maintenance Boosting Replacement Demand

Machine-learning models trained on thermal imagery and weather data predict failures 12-18 months ahead, compressing 25-year life cycles but limiting unplanned outages. Duke Energy’s analytics platform cut forced outages by 22% in 2025 after screening 32,000 transmission structures. Siemens’ Sensformer suite links edge sensors embedded in insulator strings to real-time dashboards used by 14 European TSOs. TEPCO’s drone-based inspections flagged 18,000 units for early replacement in 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (alumina, epoxy, silicone rubber) | -0.7% | Global, with acute pressure in Asia-Pacific and Europe | Short term (≤2 years) |

| Counterfeit low-grade insulators causing safety recalls | -0.4% | Southeast Asia, Middle East, Africa; spillover risk to Latin America | Medium term (2-4 years) |

| Lengthy utility pre-qualification cycles in OECD grids | -0.5% | North America, Europe, Japan, Australia; limited impact in emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Alumina, Epoxy, Silicone Rubber)

Alumina surged 23% in 2024 after export curbs in Guinea and Indonesia, inflating costs for ceramic insulators whose bills of materials are up to 50% alumina. Epoxy resin prices climbed 18% in early 2025 amid Chinese supply redirection to wind and auto composites. Silicone rubber rose 15% after platinum-catalyst shortages following Gulf Coast hurricane damage. NGK Insulators reported a 320-basis-point gross-margin squeeze, and three European composite makers exited the market in 2025.

Counterfeit Low-Grade Insulators Causing Safety Recalls

Grid outages in Vietnam, Indonesia, and the Philippines since mid-2024 traced failures to counterfeit 110-230 kV products lacking IEC 61109 certification. EVN pulled 12,000 units from service and blocked seven suppliers. PLN discovered 8% of its Java-Bali upgrade stock degraded under UV in 18 months. The Thai regulator now mandates third-party batch testing, while Malaysia requires manufacturer registration with Suruhanjaya Tenaga. Audit cycles can now stretch to 24 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Material: Polymer Gains Ground on Wildfire Mandates

Ceramic and porcelain held 45.5% electric insulator market share in 2025 due to reliability in high-pollution zones. Glass serves niche self-cleaning roles at about 12%. Composite products captured 42.5% in 2025 and will post a 7.7% CAGR, buoyed by California and Australian mandates. The electric insulator market size for composites is projected to reach USD 13.4 billion by 2031. Ceramic remains entrenched above 800 kV where lifetime data outweigh polymer benefits.

Utilities value polymer’s 40% weight advantage and hydrophobicity that resists fire starts. ABB’s Exlim line integrates sensors for condition monitoring, and Chinese firms have halved landed cost versus Western peers, sparking IEC 62217 revisions. Glass is declining as vandal-resistant and low-maintenance priorities rise.

By Voltage Rating: Ultra-High Voltage Surges on HVDC Expansion

Medium-voltage products (70-220 kV) represented 40.2% electric insulator market size in 2025 and serve distribution feeders. Low-voltage devices below 70 kV account for 25%. Extra- and ultra-high voltage classes above 765 kV will log the fastest 7.8% CAGR, reflecting China’s ±800 kV corridors and India’s 18 GW HVDC awards.

Designs with creepage distances beyond 9,000 mm prevent flashovers under pollution and ice. NGK, Lapp, and Sediver dominate thanks to decades of field data. Medium-voltage growth links to bidirectional flows from rooftop solar and battery storage. Low-voltage margins are under Chinese price pressure.

By Installation Environment: Outdoor Dominates Amid Transmission Build-Out

Outdoor insulators captured 64.4% revenue in 2025 and will rise at 7.0% CAGR, driven by transmission-line hardening and new HVDC corridors in Asia-Pacific. Indoor products serve GIS and transformer bushings and face slower growth in mature OECD grids.

Outdoor devices must withstand UV, thermal cycling, and pollution over 30 years; composites are gaining because they weigh less and reduce maintenance. Indoor demand grows in dense cities adopting GIS, where land costs justify the premium. IEC 62271 and IEC 60137 govern specifications.

By Application: HVDC Lines Lead Transmission Growth

Transmission lines owned 41.8% of 2025 demand; HVDC projects inside this slice will grow at 7.5% CAGR. Substations and switchgear take 28%, transformers and bushings 20%, and surge protection 10%.

China’s Baihetan-Jiangsu line deployed 340,000 insulators, India’s Raigarh-Pugalur will need 420,000, and Brazil’s Manaus-Boa Vista interconnection boosts South American demand. Substation growth follows grid-edge automation, while bushing replacements track aging transformer fleets. Surge protection concentrates in high-lightning tropical belts.

By End User: Utilities Command Two-Thirds of Demand

Utilities held 62.6% share in 2025 and expanded at 7.2% CAGR on the back of USD 65 billion U.S. and EUR 584 billion EU network plans. Commercial and industrial end users occupy 27%, from data centers to electrified rail. Residential sits near 10%, constrained by undergrounding trends.

Utilities let multi-year framework contracts that specify stringent IEC and ANSI tests, creating barriers for newcomers. Data-center growth and rail electrification spur medium-voltage demand, while household segments pivot to polymer units that lower truck-roll costs.

Geography Analysis

Asia-Pacific owns 54.7% of the electric insulator market and grows at 7.3% CAGR through 2031. China commissioned three ±800 kV links in 2025 and targets 30,000 km of new capacity by 2026. India’s six bipoles total 18 GW. Japan’s TEPCO is replacing 18,000 aging units, and ASEAN members plan USD 42 billion in upgrades under the ASEAN Power Grid. Australia mandates composites in bushfire regions.

North America holds 22% share. U.S. wildfire programs will replace 600,000 units by 2028. AI-driven maintenance at Duke and Dominion accelerates turnover, and Hydro-Québec is building 2,400 km of 735 kV lines.

Europe commands 18%. Germany’s four TSOs are investing EUR 2.8 billion in upgrades, France’s RTE adds 2,100 km of 400 kV lines, and Southern Europe shifts to composites for wildfire risk. Sanctions push Russia toward domestic ceramics.

South America and the Middle East & Africa together hold 5% but are rising. Brazil’s 2,500 km Manaus-Boa Vista HVDC link needs 95,000 polymer units. Saudi Arabia’s 3 GW NEOM-Riyadh project underpins Gulf demand, while South Africa and Egypt pursue replacement despite fiscal headwinds.

Competitive Landscape

The electric insulator market is moderately concentrated. The top five, ABB, Siemens, NGK Insulators, General Electric, and Hubbell, control roughly 38%. Chinese entrants Dalian Insulator Group and Zhejiang TCI offer composites at half Western landed cost, forcing IEC tightening and extended utility audits. NGK’s nano-silica polymer claims 35-year hydrophobicity, ABB embeds load sensors in Exlim, and Siemens acquired a silicone-rubber compounder to secure feedstock.

M&A accelerates: Hubbell bought Victor Insulators for USD 340 million, Toshiba and BHEL formed a ±800 kV JV in India, and Lapp expanded extra-high-voltage ceramic capacity in Germany. Growth whitespaces include predictive-maintenance-as-a-service and graphene-enhanced polymers targeting 10× tracking resistance. IEC 62217, ISO 9001, and national certification cycles spanning 24 months remain high entry barriers.

Electric Insulator Industry Leaders

ABB Ltd

Siemens AG

General Electric Company

Hubbell Inc.

NGK Insulators Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ensto introduced a new range of pin insulators designed to meet the updated IEC 60383-1:2023 standard. These products offer increased creepage distance, enhanced insulation thickness, and semiconductive coatings to improve durability and minimize partial-discharge risks in overhead transmission lines.

- June 2025: Jotun introduced powder coating technologies aimed at improving electrical insulation, thermal management, fire protection, and corrosion resistance in battery packs for electric vehicles (EVs) and energy storage systems. These solvent-free coatings enhance the safety, durability, and efficiency of high-voltage battery components, which are critical for the reliability of electrical systems.

- June 2025: Armacell inaugurated a new aerogel insulation manufacturing facility in Pune, India, to produce its ArmaGel XG aerogel blankets. This expansion doubles the company’s production capacity for high-performance thermal insulation and supports the increasing demand for insulation solutions, particularly those contributing to thermal management in energy systems, which align with the electrical insulation market.

- February 2025: Insulation Technology Group (ITG) acquired porcelain insulator manufacturer Cerisol, increasing production capacity and enhancing global service capabilities in high-voltage electrical insulation for utility grids.

Global Electric Insulator Market Report Scope

The electric insulator market report includes:

| Ceramic/Porcelain |

| Glass |

| Composite/Polymer |

| Low (Below 70 kV) |

| Medium (70 to 220 kV) |

| High (221 to 765 kV) |

| Extra- and Ultra-High (Above 765 kV) |

| Outdoor |

| Indoor |

| Transmission Lines |

| Substations and Switchgear |

| Transformers and Bushings |

| Surge/Lightning Protection |

| Utilities |

| Commercial and Industrial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Dielectric Material | Ceramic/Porcelain | |

| Glass | ||

| Composite/Polymer | ||

| By Voltage Rating | Low (Below 70 kV) | |

| Medium (70 to 220 kV) | ||

| High (221 to 765 kV) | ||

| Extra- and Ultra-High (Above 765 kV) | ||

| By Installation Environment | Outdoor | |

| Indoor | ||

| By Application | Transmission Lines | |

| Substations and Switchgear | ||

| Transformers and Bushings | ||

| Surge/Lightning Protection | ||

| By End User | Utilities | |

| Commercial and Industrial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the electric insulator market by 2031?

The sector is forecast to reach USD 31.98 billion by 2031, rising at a 6.52% CAGR from 2026.

Which region contributes the largest demand for high-voltage insulators?

Asia-Pacific accounts for 54.7% of global revenue, led by China's and India's ultra-high-voltage build-outs.

Why are utilities shifting from ceramic to polymer insulators?

Polymer units are lighter, stay hydrophobic, and cut wildfire risk, which lowers maintenance costs and liability exposure.

How will HVDC expansion influence insulator demand?

±800 kV corridors in China, India, Brazil, and Saudi Arabia require millions of extra-high voltage insulators, driving the fastest growth slice of the market.

What is the main supply-chain risk facing manufacturers?

Volatile prices for alumina, epoxy, and silicone rubber can squeeze margins by more than 300 basis points during spikes.

How are AI tools changing replacement cycles?

Machine-learning surveillance flags failures a year ahead, prompting earlier but planned replacements that improve grid reliability.

Page last updated on: