Flexible Display Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 20.52 Billion |

| Market Size (2030) | USD 75.14 Billion |

| Growth Rate (2025 - 2030) | 29.64% CAGR |

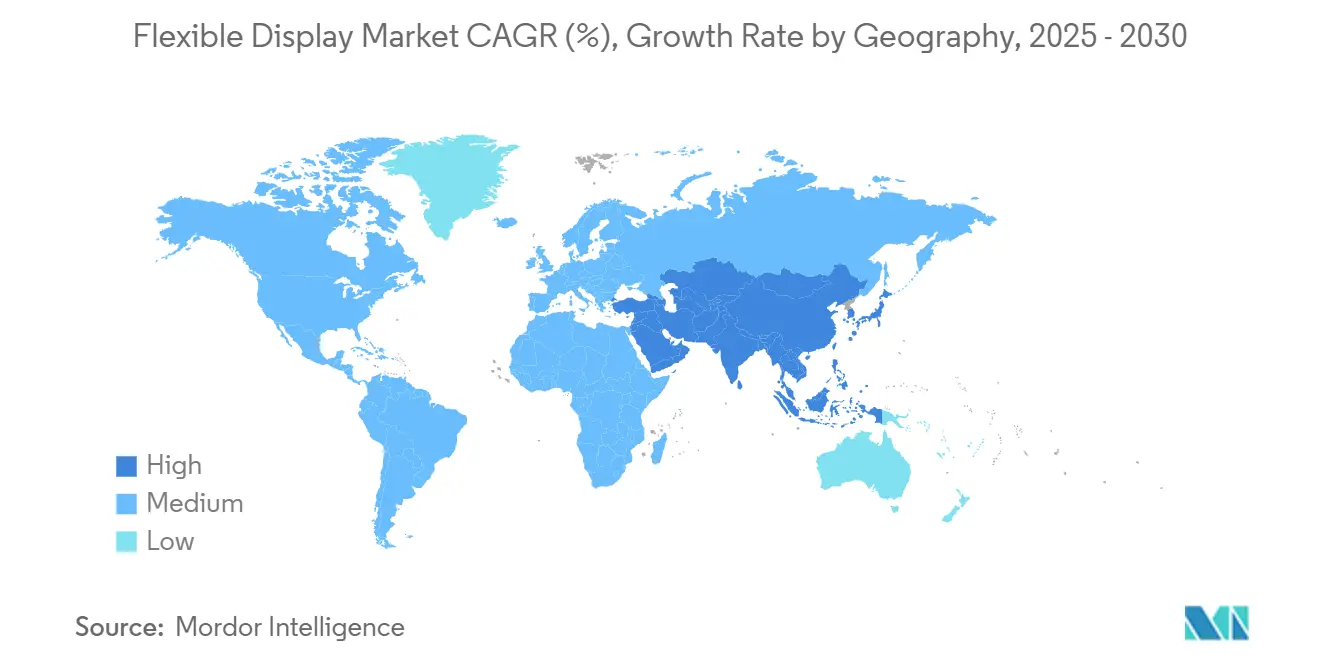

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

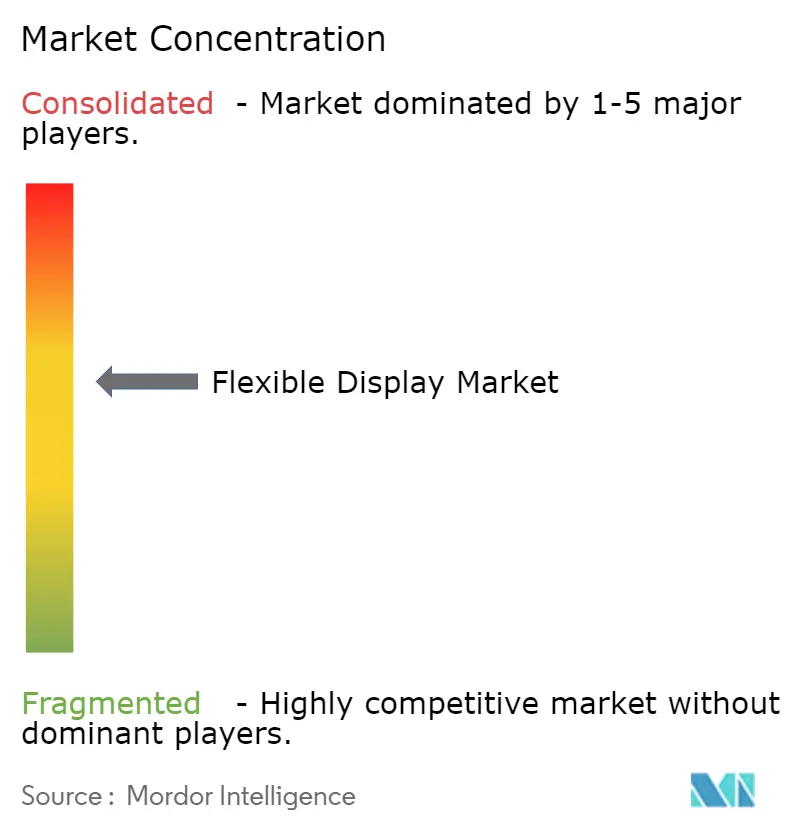

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

.webp)

Flexible Display Market Analysis by Mordor Intelligence

The flexible display market size stands at USD 20.52 billion in 2025 and is forecast to reach USD 75.14 billion by 2030, translating into a powerful 29.64% CAGR over the period. The valuation leap signals a turning point in which scale economies, material breakthroughs and product design freedom converge to shift flexible panels from niche concepts into mainstream interfaces across consumer electronics, mobility and industrial environments. Production investments in Gen-8.6 OLED fabs, rapid rollable innovation and the migration of micro-LED into wearables are widening the addressable base, while regulatory pushes for glass-free modules spur fresh applications in Europe. Competitive intensity is rising as Chinese manufacturers expand capacity faster than Korean incumbents, challenging established cost structures and accelerating price declines. Simultaneously, integrated players that secure polyimide, encapsulation and hinge know-how are insulating themselves from supply shocks and litigation risk.

Key Report Takeaways

- By display type, OLED captured 85% of the flexible display market share in 2024; micro-LED is projected to grow at a 36% CAGR to 2030.

- By form factor, foldables held 71% of the flexible display market size in 2024; rollables are advancing at a 39% CAGR between 2025-2030.

- By substrate, plastic-polyimide accounted for 62% of the flexible display market share in 2024; metal foil substrates are forecast to climb at a 33% CAGR to 2030.

- By application, smartphones and tablets commanded 66% of the flexible display market size in 2024; automotive cockpits are growing at a 31% CAGR through 2030.

- By geography, Asia Pacific led with 57% revenue share in 2024, while the Middle East & Africa region is projected to expand at a 32% CAGR through 2030.

Global Flexible Display Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rollable & Foldable Smartphone Launch Momentum in China and Korea | +7.2% | East Asia, with global spillover effects | Medium term (2-4 years) |

| Premium-EV Curved OLED Cockpit Adoption Across Europe | +5.8% | Europe, North America, premium segments in Asia | Medium term (2-4 years) |

| Demand Spike for Lightweight AR/VR Micro-OLED Panels in North America | +4.3% | North America, with expansion to Europe and East Asia | Long term (≥ 4 years) |

| Cost Reduction from Gen-8.6 Flexible OLED Fabs in China | +6.5% | Global, with primary impact in Asia Pacific | Short term (≤ 2 years) |

| EU Circular-Economy Push for Glass-Free Modules | +3.1% | European Union, with regulatory spillover to global supply chains | Medium term (2-4 years) |

| Growth in Flexible Medical Wearables in Japan & South Korea | +2.4% | East Asia, with expansion to North America and Europe | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rollable and foldable smartphone launch momentum in China and Korea

Shipments of flexible OLED smartphone panels climbed 26% in 2024 to 784 million units, underscoring how fresh form factors stimulate replacement demand.[1]Shuangyuan Liu, Xiaofei Xu and Jie Jiang, “Flexible Transparent ITO Thin Film with High Conductivity and High-Temperature Resistance,” Ceramics International, ceramicsinternational.comNew tri-fold designs slated for late 2025 bring 360-degree rotation and ultra-thin glass that lowers crease visibility, intensifying brand differentiation. Chinese entrants scale quickly by matching hinge durability targets and shortening design-to-launch cycles, pressuring incumbents on price and innovation tempo. Component ecosystems around hinges, temperature-resistant polyimide and transparent cover films benefit directly. The upturn also spills into accessory and repair markets, creating incremental service revenue streams.

Premium-EV curved OLED cockpit adoption across Europe

Luxury electric vehicles elevate interior experience through expansive curved dashboards such as the EQS SUV Hyper-screen, which merges multiple displays under a continuous glass cover.[2]Mercedes-Benz AG, “The EQS SUV Full Press Pack,” mercedes-benz-media.co.ukAutomotive OEMs prefer flexible OLED for its thin profile, uniform luminance and design latitude, leading to a surge in display-area per vehicle. Tier-1 suppliers deepen partnerships with panel makers to co-develop cockpit platforms, while software-defined vehicle strategies demand displays that support continuous over-the-air upgrades. As autonomous functionality matures, multi-modal interaction and stretchable pillar-to-pillar screens are set to multiply display square-meter consumption per car.

Lightweight AR/VR micro-OLED demand in North America

Shipments of XR displays are set to rise 6% in 2025, with AR glasses surging 42% on the back of thinner micro-OLED engines that cut headset weight and power draw. Brightness gains beyond 10,000 nits and side-wiring deposition that trims cost by three-fold remove hurdles to outdoor and enterprise adoption. Silicon backplane advances boost pixel density, enabling bi-focal designs that blend physical and digital layers seamlessly. Component suppliers reposition from mobile OLED to micro-OLED, opening fresh revenue pools.

Cost reduction from Gen-8.6 flexible OLED fabs in China

A USD 8.72 billion Gen-8.6 line now under construction is designed for cost-efficient tablet, notebook and automotive panels, allowing simultaneous processing of six 14-inch displays per mother-glass. Maskless lithography, inkjet-printed RGB stacks and oxide-TFT backplanes together shave material waste and cycle time. Lower panel ASPs accelerate penetration into mid-range devices, flattening price elasticity curves. Allied equipment makers in evaporation and encapsulation win larger tool orders, while domestic PI and barrier-film suppliers scale with guaranteed offtake.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gen-8+ polyimide yield losses | −2.8% | Global manufacturing hubs, mainly East Asia | Short term (≤ 2 years) |

| Encapsulation material supply crunch | −2.1% | Global with higher risk in Asia fabs | Medium term (2-4 years) |

| US-centric patent litigation on foldable hinges | −1.5% | North America with global spillovers | Medium term (2-4 years) |

| Cold-climate reliability issues of plastic-LCD signage | −1.1% | Northern Europe, North America, Northern Asia | Short term (≤ 2 years) |

Source: Mordor Intelligence

Gen-8+ polyimide yield losses elevating scrap costs

Scaling to larger mother-glass intensifies thermal stress on flexible PI substrates, driving defect-induced yield drops that inflate per-unit cost. Research on aerogel-reinforced PI fibers shows promise in lifting thermal stability yet industrial adoption remains nascent, leaving fabs exposed to expensive scrap during ramp-up.[3]Yonggang Min et al., “Pressure-Constrained Sonication Activation of Flexible Printed Metal Patterns for Multifunctional Electronics,” Nature Communications, nature.comYield recovery programmes now focus on real-time in-line metrology and AI-based predictive maintenance to shave defect density before mass output begins.

Encapsulation material supply crunch

Ultra-thin multi-layer barriers that fend off moisture and oxygen still come from a few qualified suppliers. Strong demand from smartphone and automotive lines strains coating capacity, extending lead times and raising spot pricing. Government-sponsored projects such as KONFECT seek to scale flexible OLED glass encapsulation via roll-to-roll systems, but commercial volumes remain limited. Panel makers with in-house barrier film or ALD capability gain schedule certainty and margin protection.

Segment Analysis

By Display Type: OLED still rules while micro-LED gains pace

OLED held an 85% share of the flexible display market in 2024, leveraging emissive pixels that enable thinner, curve-friendly modules without backlights. Cost erosion from Chinese fabs and evaporator throughput gains have kept OLED the panel of choice for smartphones, watches and curved infotainment clusters. At the same time, micro-LED shipments are scaling from pilot to early mass production, posting a 36% forecast CAGR as quantum-dot colour converters, mass-transfer accuracy and repair yields improve. Automotive head-up displays and rugged wearables benefit first because micro-LED pushes brightness to 10,000 nits and delivers long lifetimes even under high thermal load, as evidenced by Tianma’s 8-inch prototype. E-paper holds a niche in low-power signage and logistics tags, while quantum-dot LCD hybrids continue bridging price and colour-gamut gaps for mid-range devices.

OLED dominance faces three pressure points. First, inorganic micro-LED material longevity dilutes OLED’s burn-in risk narrative. Second, Gen-8.6 cost advantages narrow the ASP gap between rigid and flexible OLED, nudging budget segments toward flexible form factors. Third, quantum-dot on-chip approaches are now compatible with roll-to-roll plastic substrates, seeding future competition in ultra-large transparent windows. Even so, ecosystem maturity, equipment depreciation and abundant supply keep OLED firmly in charge through the mid-term.

Note: Segment shares of all individual segments available upon report purchase

By Form Factor: Rollable gains traction beyond foldables

Foldable devices captured 71% of the flexible display market in 2024 and remain the volume engine as smartphone vendors race to iterate bi-fold, tri-fold and wrap-around formats. Patent barricades on hinge geometry and UTG lamination reinforce the lead of first movers yet do not preclude rivals that licence or innovate alternative kinematic stacks. Rollable screens, forecast to expand at a 39% CAGR, unlock spatial efficiency by retracting into compact housings, aligning with consumer demand for pocket-friendly yet expansive displays. Early notebook and tablet rollables demonstrate that motorised spools and stretch-limiting lamination can achieve repeatability over 30,000 actuations.

Bendable and conformable displays remain staples in curved edge phones, fitness bands and automotive radars thanks to their simpler mechanical loads. A nascent “form-factor free” class, enabled by stretchable substrate meshes and serpentine circuit patterns, is under active exploration for skin-adhesive health patches and soft robots. Academic output on stretchable displays jumped from 17 papers in 2014 to 197 in 2023, mirroring heightened R&D investment. While commercialisation lags, the progress sets the stage for ubiquitous ambient display surfaces later in the decade.

By Substrate Material: Metal foil narrows the gap

Plastic-polyimide ruled with 62% share in 2024 owing to its proven thermal endurance, chemical stability and process familiarity. However, dimensional stability challenges at Gen-8+ scale and recyclability limitations give metal foil an opening. Aluminium and stainless-steel foils coupled with oxide TFT layers dissipate heat faster and block water better, pushing their CAGR to 33% through 2030. A recent sonication-activation technique raises the conductivity of printed metal traces, letting engineers craft origami-style fold nets with minimal resistance gain after repeated bending.[4]OLED-Info. "Flexible OLEDs: introduction and market status." , "April 2025 - OLED-Info." oled-info.com

Ultra-thin glass remains indispensable where optical clarity and touch rigidity dominate, notably in foldable cover windows below 30 µm. PET, PEN and polycarbonate serve cost-sensitive segments that accept lower thermal thresholds. Fluorinated-mica substrates with indium-tin-oxide coatings now reach 85% transparency and survive 800 °C anneals, setting new records for high-temperature tolerant flexible conductors.

Note: Segment shares of all individual segments available upon report purchase

By Application: Automotive cockpit pulls ahead

Smartphones and tablets together represented 66% of the flexible display market in 2024 and remain the primary showcase for high-refresh-rate OLED. Yet automotive cockpits are surging with a 31% forecast CAGR as premium EV brands deploy pillar-to-pillar curved dashboards, rear-seat entertainment strips and exterior welcome panels. BOE’s 17-inch electric cockpit prototype illustrates how flexible displays merge gauges, infotainment and passenger controls into a unified surface, reducing mechanical part count and enhancing upgradeability.

Wearables enjoy robust momentum, fuelled by health tracking, bi-directional communication and fashion appeal. Rollable TV concepts plus transparent retail signage continue to draw marketing buzz, though cost hurdles keep volumes modest for now. AR/VR headsets rely increasingly on micro-OLED micro-displays to meet ergonomic targets, linking back into the substrate and encapsulation advances noted earlier. Industrial control panels, rail information systems and rugged defence screens round out the expanding tapestry of use cases.

Geography Analysis

Asia Pacific dominated with 57% revenue in 2024, propelled by dense manufacturing ecosystems in Korea, China and Taiwan that span PI resin synthesis to module assembly. China alone is adding 8% annual flexible OLED capacity through 2028 against Korea’s 2% run-rate, lifting its share of global panel output from 68% to 74%. Regional policy incentives grant favourable land, tax and power terms to local champions, while domestic smartphone OEMs provide ready demand. This virtuous cycle cements supply-chain self-sufficiency and accelerates time-to-yield for new lines.

North America commands technology pull on account of its leadership in AR/VR, high-performance computing and premium notebook segments. US brands source OLED MacBook-class panels for 2026, compelling suppliers to qualify oxide TFT and tandem stack architectures that lengthen lifetime under static UI loads. Legal exposure arising from hinge patents remains a watch-item; however, players often settle or cross-licence to safeguard launch windows. Government grants for microelectronic reshoring may redirect portions of the ecosystem stateside, particularly in backplane and glass-free encapsulation tooling.

Europe exerts regulatory influence through the Ecodesign Regulation and the upcoming Digital Product Passport, pushing the industry toward recyclable structures and full material disclosure. Automotive clusters in Germany, Sweden and the United Kingdom adopt curved OLED clusters at a brisk pace, stimulating local integration, bonding and test partners. The continent’s circular material use target of 24% by 2030 drives R&D into solvent-reduced PI, biodegradable adhesives and mechanical fasteners that enable easy separation.

The Middle East and Africa, while comparatively small, records the fastest growth at a 32% CAGR off expanding digital signage in transport hubs, sports arenas and leisure venues. Flexible LED film screens that conform to glass facades exemplify the architectural appetite for novel form factors. Government-backed smart-city projects and high ambient-light conditions make high-brightness micro-LED an attractive option. South America follows with rising smartphone penetration and automotive assembly plants beginning to specify flexible clusters for export models.

Competitive Landscape

Incumbents Samsung Display and LG Display leverage broad IP portfolios covering flexible OLED stacks, encapsulation, foldable hinges and UTG lamination, securing design wins with global device brands. Yet their combined share is projected to erode as BOE, Visionox and CSOT unlock successive Gen-6 and Gen-8.6 lines that undercut cost while approaching uniformity targets. BOE’s USD 8.72 billion Chengdu fab is emblematic, aiming for full mass production by 2027 and positioning the firm to overtake Samsung Display in foldable smartphone panel output by 2028. Visionox meanwhile invests USD 690 million in an R&D campus focusing on AR/VR micro-OLED, signalling intent to diversify beyond handset panels.

Strategic moves revolve around vertical control. Samsung Display purchased mask-less OLED deposition IP from Orthogonal, seeking to eliminate costly fine-metal masks and leapfrog in pattern-resolution capability. LG Display unveiled a stretchable panel that extends 50% without distortion, targeting fashion and mobility sectors. BOE actively co-develops automotive cockpit platforms with leading OEMs, embedding its panels deeply into vehicle E/E architectures. Start-ups such as SmartKem commercialise low-temperature organic TFT inks compatible with roll-to-roll printing, offering incumbents optional paths to lower CapEx expansions.

Patent filings on fold mechanics stay elevated. While high-profile lawsuits in US courts can delay individual launches, settlements typically follow, allowing royalty-bearing models to proceed. Materials suppliers-Dow, Sumitomo, Kolon-also consolidate through targeted acquisitions to secure PI varnish and barrier-film formulations, further raising entry hurdles. Overall, the market tilts toward an oligopoly with room for specialised disruptors in micro-LED, metal-foil and stretchable niches.

Flexible Display Industry Leaders

-

LG Display Co., Ltd

-

Samsung Electronics Co. Ltd

-

ROYOLE Corporation

-

BOE Technology Group Co. Ltd

-

Microtips Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BOE began construction of an 8.6-Gen AMOLED line in Chengdu at USD 8.72 billion, the largest industrial project in Sichuan’s history, boosting premium flexible capacity.

- April 2025: LG Display reported OLED TVs accounting for 78.3% of China’s premium TV segment, guiding the company back to profit territory.

- April 2025: Visionox committed USD 690 million to a flexible AMOLED R&D complex in Kunshan with emphasis on AR/VR applications.

- March 2025: Samsung Display secured a multi-year order for OLED MacBook Pro panels beginning 2026 with initial annual volume of 3-5 million units.

- January 2025: Samsung confirmed an October 2025 launch window for a tri-fold smartphone employing 360-degree ultra-thin glass.

Global Flexible Display Market Report Scope

Flexible displays are rollable and flexible, unlike the traditional flat-screen displays used in most devices. These displays are built upon a flexible substrate which can be either plastic, metal, or flexible glass.

The scope of the study covers market dynamics and trends in Display Type (OLED, LCD, EPD (Electronic Paper Display), Other Display Types (LED)), Substrate Material (Glass, Plastic, Other Substrate Materials), Application (Smartphones and Tablets, Smart Wearables, Televisions, and Digital Signage, Personal Computers and Laptops, Other Applications), and Geography. The study also tracks the trends, opportunities, and COVID-19 impact on the flexible display market. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Display Type | OLED | |||

| LCD | ||||

| E-Paper Display (EPD) | ||||

| Micro-LED | ||||

| Quantum-Dot and Other Emerging Types | ||||

| By Form Factor | Foldable | |||

| Rollable | ||||

| Bendable | ||||

| Conformable (Curved/Wrap-around) | ||||

| By Substrate Material | Glass | |||

| Plastic - Polyimide (PI) | ||||

| Plastic - PET/PEN | ||||

| Metal Foil | ||||

| Others (Polycarbonate, Ultra-thin Glass) | ||||

| By Application | Smartphones and Tablets | |||

| Smart Wearables (Watches, Patches) | ||||

| Televisions and Digital Signage | ||||

| Personal Computers and Laptops | ||||

| Automotive Cockpit and Infotainment | ||||

| AR/VR Head-Mounted Displays | ||||

| Industrial and Public Transport Displays | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| South Korea | ||||

| India | ||||

| South East Asia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| OLED |

| LCD |

| E-Paper Display (EPD) |

| Micro-LED |

| Quantum-Dot and Other Emerging Types |

| Foldable |

| Rollable |

| Bendable |

| Conformable (Curved/Wrap-around) |

| Glass |

| Plastic - Polyimide (PI) |

| Plastic - PET/PEN |

| Metal Foil |

| Others (Polycarbonate, Ultra-thin Glass) |

| Smartphones and Tablets |

| Smart Wearables (Watches, Patches) |

| Televisions and Digital Signage |

| Personal Computers and Laptops |

| Automotive Cockpit and Infotainment |

| AR/VR Head-Mounted Displays |

| Industrial and Public Transport Displays |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| South East Asia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the flexible display market size in 2025 and how fast will it grow by 2030?

The market stands at USD 20.52 billion in 2025 and is projected to reach USD 75.14 billion by 2030, posting a 29.64% CAGR.

Which region currently leads the flexible display market and which region is expanding the fastest?

Asia Pacific holds the largest share at 57% in 2024, while the Middle East and Africa region is forecast to grow at a 32% CAGR from 2025-2030.

How quickly are rollable displays growing compared with foldable formats?

Foldables own 71% of 2024 volume, yet rollable displays are the growth engine with a 39% CAGR expected between 2025-2030.

Why are automotive cockpits emerging as a key application for flexible displays?

Premium EV makers integrate curved OLED dashboards to enhance user experience, driving a 31% CAGR for automotive cockpit displays through 2030.

What material-related challenges could slow flexible display adoption?

Yield losses in Gen-8+ polyimide substrates and tight supply of high-performance encapsulation materials are reducing output and raising costs.

Who are the main players and how is competition evolving?

Samsung Display and LG Display lead today, but BOE and Visionox are rapidly gaining share as new Gen-8.6 fabs in China cut costs and boost capacity.