Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

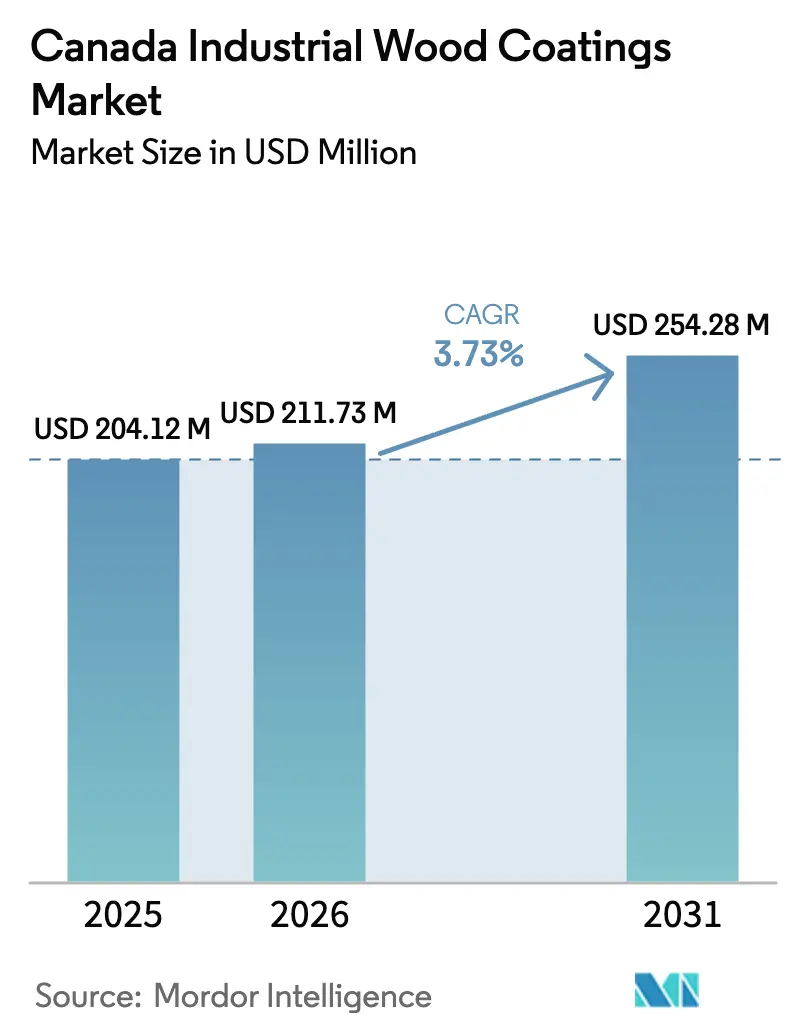

| Base Year Market Size (2025) | USD 204.12 Million |

| Market Size (2026) | USD 211.73 Million |

| Market Size (2031) | USD 254.28 Million |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

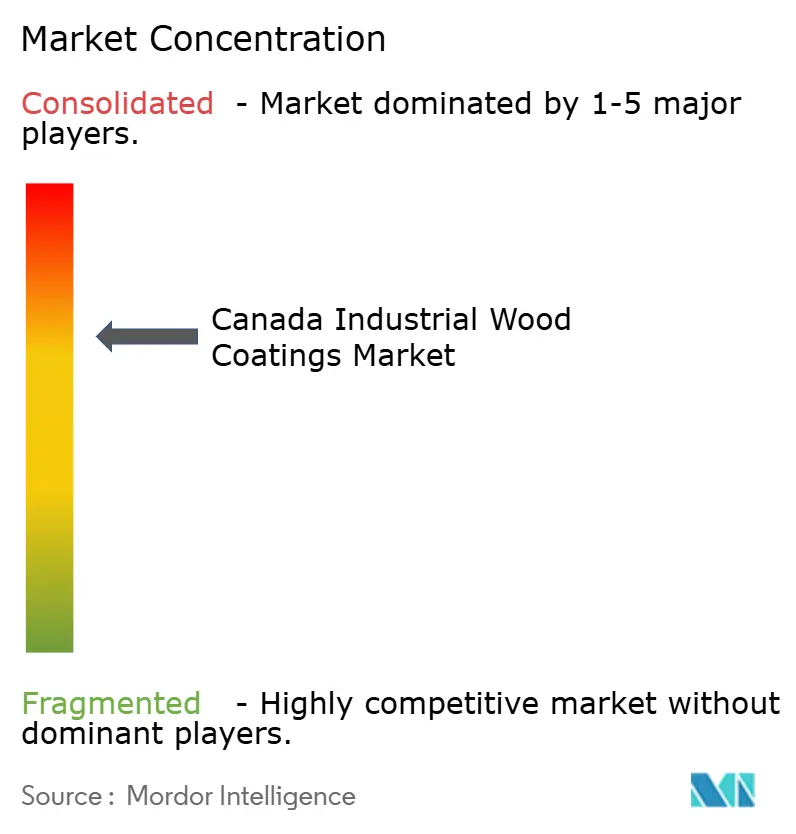

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Industrial Wood Coatings Market Analysis by Mordor Intelligence

The Canada Industrial Wood Coatings Market size is projected to be USD 204.12 million in 2025, USD 211.73 million in 2026, and reach USD 254.28 million by 2031, growing at a CAGR of 3.73% from 2026 to 2031. As federal loan guarantees support modular offsite timber factories, there is a growing demand for low-VOC, rapid-cure products. Concurrently, Environment and Climate Change Canada (ECCC) has proposed a VOC ceiling, aiming to phase out legacy nitrocellulose and high-solvent polyurethanes. Polyurethane resin systems dominate the market, offering a combination of durability, aesthetic appeal, and compliance with upcoming bans on PFAS and formaldehyde. Waterborne technologies are expanding rapidly as furniture manufacturers, cabinet shops, and mass timber panel plants pursue GREENGUARD Gold or LEED-eligible finishes, aiming to match the performance of traditional solvent-borne products. However, challenges remain: United States lumber tariffs have caused a decline in Canadian wood-product sales since 2025. Additionally, imports of prefinished ready-to-assemble (RTA) cabinets from China increased significantly in December 2025, impacting domestic coating volumes.

Key Report Takeaways

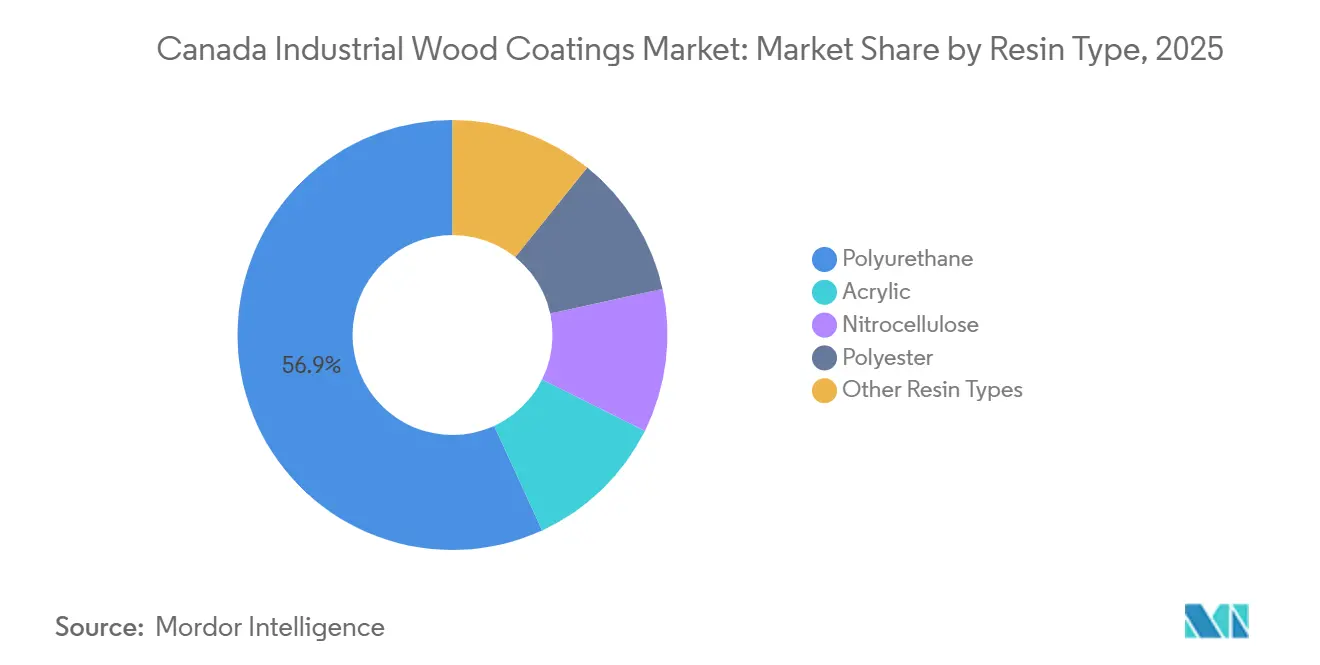

- By resin type, polyurethane led with 56.85% of the Canada industrial wood coatings market share in 2025 and is forecast to expand at a 4.03% CAGR through 2031.

- By technology, waterborne coatings are the fastest-growing segment, advancing at a 4.48% CAGR from 2026-2031 even though solvent-borne systems retained 52.48% share in 2025.

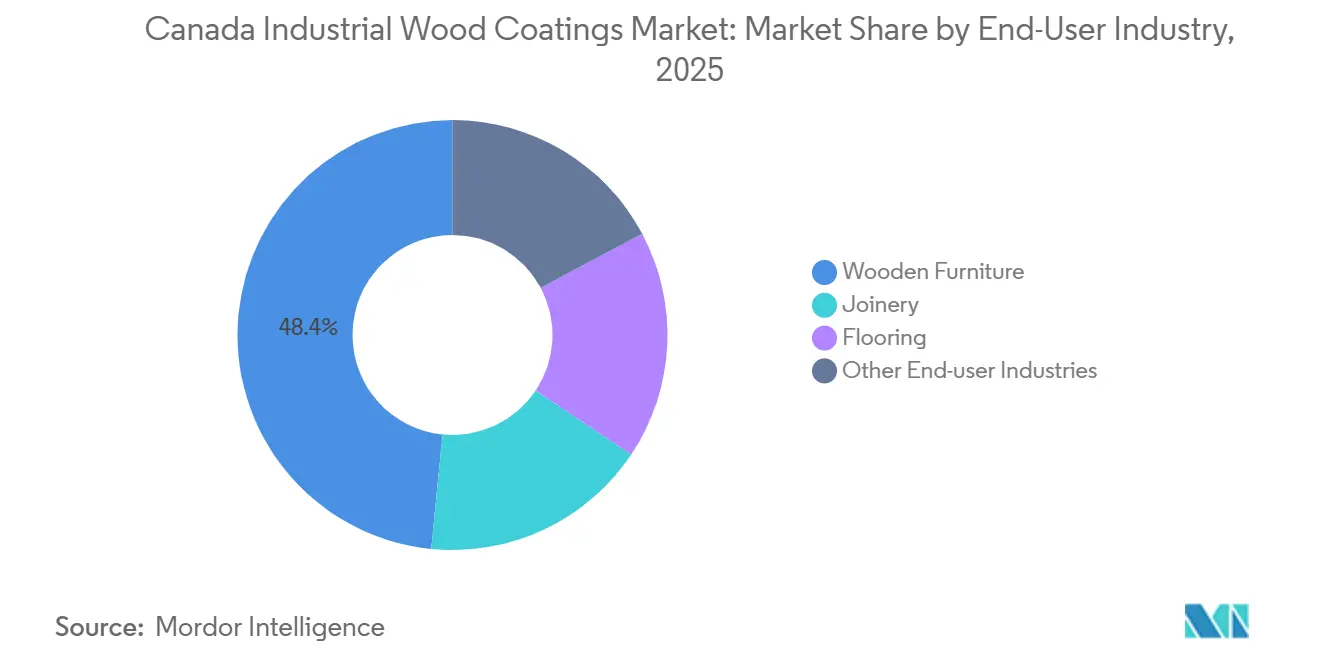

- By end-user industry, wooden furniture absorbed 48.42% of the Canada industrial wood coatings market size in 2025 and is projected to grow at a 4.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Industrial Wood Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Wooden Furniture | +0.90% | Ontario and Quebec furniture corridors | Medium term (2-4 years) |

| Increasing Construction and Renovation | +0.70% | National; strongest in Montreal | Short term (≤ 2 years) |

| Adoption of Low-VOC and Water-borne Systems | +1.10% | National; driven by federal VOC cap | Medium term (2-4 years) |

| Investment in Modular and Prefab Timber Builds | +0.80% | British Columbia and Atlantic provinces | Long term (≥ 4 years) |

| Federal Loan Guarantees for Off-site Plants | +0.60% | Regions with forestry infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Wooden Furniture

In March 2025, furniture sales increased as households updated their inventories from the pandemic era. This growth also boosted demand for coatings used in casegoods and kitchen cabinets. In a strategic move, Haworth acquired Tayco's expansive plant in Toronto in February 2026, positioning itself in a market that prioritizes low-VOC finishes compliant with WELL and LEED standards. A notable majority of small and mid-sized furniture shops are turning to local suppliers for their quick color-matching needs, which is proving beneficial for regional formulators. By December 2025, inventories climbed, signaling a restocking momentum that temporarily boosted coating demand. However, a surge in imports of pre-finished ready-to-assemble (RTA) cabinets from China has increased price pressures. This development has prompted domestic finishers to shift toward customization niches as a strategy to maintain their market share.

Increasing Construction and Renovation Activities

In May 2025, housing starts were approximately 243,000 units, but there were significant regional disparities: Montreal experienced an increase, while Toronto and Vancouver recorded declines. Mid-rise "missing-middle" housing is increasingly relying on factory-applied components. This shift is driving faster adoption of UV and waterborne chemistries that cure in minutes. The Build Canada Homes initiative is expected to boost timber demand. However, due to delayed disbursements, forecasting volumes has become a challenge. A softwood tariff has reduced sawmill output, limiting substrate availability for joinery shops. Renovation spending, which constitutes a significant portion of residential construction, is highly sensitive to interest rates. The Bank of Canada's policies in 2026 will play a crucial role in determining whether homeowners proceed with floor and cabinet renovations or choose to postpone them.

Adoption of Low-VOC and Water-borne Formulations

Canada's ECCC has proposed a new cap for wood coatings, significantly reducing current solvent-borne levels. Additionally, formaldehyde thresholds have been established, and with a PFAS ban now in effect, suppliers are increasingly turning to alternatives. These include polyurethane dispersions, acrylic emulsions, and UV-cured oligomers. Notably, AkzoNobel’s RUBBOL WF 3350 and Sherwin-Williams’ SHER-WOOD EA Hydroplus are emerging as drop-in alternatives, boasting solvent-like hardness without the drawback of pot-life waste. However, research from the University of Waterloo indicates that challenges with clear-coat flow are hindering the broader adoption of these premium-grade products. On a different note, Cloverdale Paint has partnered in carbon-capture resin initiatives, underscoring that significant CO₂ reductions from cradle to gate are becoming a key market differentiator.

Investment in Modular and Prefabricated Timber Buildings

In the 2025 budget, funding was allocated for transforming the forest sector. The first installment was disbursed in February 2026, benefiting seven Atlantic projects that focus on mass-timber elements[1]Natural Resources Canada, “Forest Sector Transformation,” NRCAN.GC.CA . Additionally, loan guarantees have been introduced to mitigate underwriting risks. These guarantees specifically cater to robotic lines that utilize zero-solvent coatings, which are cured in mere seconds. In New Brunswick and Nova Scotia, demonstration plants are working on valorizing by-products from regional sawmills. However, there is a pressing need to expand training programs to produce operators proficient in UV conveyor systems. Federal "Buy Canadian" policies have established a preference for mass timber in public building tenders. This move generates significant anchor demand, contingent on provinces aligning with this standard. Yet, while GCWood is currently emphasizing mid-rise constructions, this focus moderates the immediate growth potential for participants in Canada's industrial wood coatings market, especially those linked to low-rise housing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC Emission Regulations | -0.5% | Ontario and British Columbia enforcement hot-spots | Short term (≤ 2 years) |

| Availability of Alternative Non-wood Materials | -0.3% | Commercial builds and multi-family corridors | Medium term (2-4 years) |

| Rising Imports of Pre-finished RTA Cabinets | -0.4% | Ontario and Quebec cabinetry clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent VOC Emission Regulations

Canada's ECCC sets a limit, signaling the end for nitrocellulose lacquers, especially in touch-up and musical instrument markets. Starting June 2026, bans on PFAS, PBDE, and HBCD will challenge formulators, stripping them of wetting agents and flame retardants, both highly valued in yacht interiors and commercial kitchens. While multinationals can spread research and development costs across their global portfolios, smaller Canadian batch plants grapple with steep reformulation expenses for each SKU. Although permit trading exists, its administrative weight poses a challenge, especially for family-owned varnish shops. Additionally, resin bottlenecks from select global suppliers introduce price volatility, tightening margins further.

Availability of Alternative Non-wood Materials

Quartz and engineered stone worktops, metal-clad façades, and luxury vinyl tiles are increasingly diverting demand from traditional wood finishing channels. In multi-family towers, powder-coated aluminum window systems are surpassing varnished timber in fire compliance, which is prompting a shift in orders toward metal paint lines. Mass-timber structural panels are prioritizing intumescent fire coatings over decorative lacquers, leading to a decline in demand for standard clearcoats. Furthermore, prefabricated bath pods made from fiberglass are entirely bypassing wood joinery, redirecting chemical spending toward FRP gelcoats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Dominance Driven by Durability and Regulatory Alignment

Polyurethanes held 56.85% of Canada industrial wood coatings market share in 2025 and are on track for a 4.03% CAGR through the forecast period of 2026-2031. Two-component systems, achieving König hardness exceeding 160 seconds and passing KCMA's chemical-spot tests, have become the preferred choice for kitchen cabinets and flooring. Due to lignin-based polyols, the bio-content in Canada's polyurethane wood coatings market is increasing, while achieving a commendable reduction in cradle-to-gate CO₂ emissions. Acrylics dominate exterior windows, leveraging their ultraviolet (UV) retention capabilities, although their one-component formulation falls short on indoor scratch resistance. While nitrocellulose boasts a rapid rub-down feature, it faces challenges with the impending volatile organic compound (VOC) regulations. Polyester finds its niche in high-end applications, catering to mirror-gloss pianos and super-yachts, where price sensitivity is minimal.

AkzoNobel’s RUBBOL line, featuring a 100% ultraviolet-polyurethane formulation, exemplifies the industry's shift as resin families merge with ultraviolet oligomers, achieving a notable reduction in drying time. Meanwhile, Covestro’s Bayhydrol UV 2901 dispersion combines waterborne handling with a swift ultraviolet snap-cure, addressing the clear-coat flow challenge that has hindered widespread adoption.

By Technology: Waterborne Systems Gain Share Despite Solvent-borne Incumbency

Solvent-borne systems still accounted for 52.48% of total demand in 2025, thanks to legacy spray booths and quick stack time in high-throughput shops. However, waterborne platforms are expected to achieve a 4.48% CAGR through the forecast period of 2026-2031, driven by an impending VOC rule mandate. In Canada, the industrial wood coatings market, leaning towards waterborne finishes, is poised to eclipse its solvent-based counterparts. This shift is anticipated as end-users transition to HVLP guns and booth de-humidifiers. Meanwhile, UV-cured liquids and powders are witnessing robust growth in factories crafting RTA cabinets, MDF panels, and flooring planks. Here, three-minute cure cycles are paving the way for single-shift production economics. On the other hand, powder coatings for wood are still in their infancy. The reason is that conveyorized infrared lines are expensive, which present a significant barrier for smaller operators.

By End-user Industry: Wooden Furniture Leads Amid Import Pressure and Capacity Investments

Wooden furniture accounted for 48.42% of 2025 consumption, and despite headwinds from Asian imports, it is expected to climb at a CAGR of 4.08% during the forecast period of 2026-2031, driven by persistent office refits and home-office expansions. In Canada, the market share for industrial wood coatings, primarily linked to furniture, surpasses that of joinery or flooring. This dominance is largely attributed to consistent repeat orders placed by thousands of small and medium-sized enterprises (SMEs), which prefer quarts and gallons over drums. This preference, in turn, bolsters distributor volumes. While joinery and architectural millwork cater to commercial construction, their demand is influenced by fluctuations in public-sector building policies. The flooring segment has been evolving; luxury vinyl tile has secured a significant share of residential installations in North America, leading to a decline in traditional sand-and-refinish cycles. Meanwhile, specialty niches, such as guitars and hockey sticks, prioritize solvent clarity and hand-rubbed depth, ensuring the continued use of nitrocellulose, even amidst stricter regulations.

Geography Analysis

Ontario and Quebec, home to the bustling furniture corridors from Toronto through Kitchener-Waterloo and from Montreal down the Chaudière Valley, account for approximately two-thirds of the nation's coating turnover. While Toronto experienced a drop in housing starts in early 2025, curbing millwork volumes, Quebec's increase provided a counterbalance. In 2025, Laurentide Paint introduced "Splendi," a brand proudly marketed as 100% Quebec-made, tapping into the province's strong buy-local sentiment.

In late 2025, British Columbia's forest-product sales declined due to sawmill curtailments linked to tariffs. In mid-2025, Cloverdale Paint expanded its Surrey plant capacity twofold, anticipating that the province's push for mass timber would drive demand for low-emission primers and clears. Meanwhile, Atlantic Canada, spurred by mass-timber grants, is emerging as a potential hub. Here, smaller CLT plants might boost coating demand, even if the region's population is relatively modest.

The Prairie provinces, accounting for a significant portion of consumption primarily driven by single-family construction and agricultural buildings, are witnessing increased attention. In late 2025, Sherwin-Williams inaugurated a new hub in Saskatoon, underscoring the optimism of multinationals despite the region's lower density. While national loan guarantees aim to channel plant investments toward areas with stranded timber, the timelines for this remain uncertain. However, suppliers with the agility to shift distribution and technical teams across provinces stand poised to reap early benefits.

Competitive Landscape

The Canada industrial wood coatings market is moderately consolidated. Major players such as AkzoNobel, Sherwin-Williams, Axalta, PPG, and RPM command a significant share of the market, leaving room for regional specialists such as Cloverdale Paint, Canlak Coatings, and Laurentide Paint. However, the landscape has shifted with the merger between AkzoNobel and Axalta, announced in December 2025. If regulators identify too much overlap in the industrial wood segment, divestitures could be required. Meanwhile, PPG's strategic move in late 2024, selling its architectural unit, not only freed up capital for ventures in the lucrative mobility and aerospace sectors but also created opportunities for local players to engage with previously untapped dealers[2]PPG Industries, “Sale of Architectural Coatings Business,” PPG.COM .

Private equity's interest is evident with SK Capital's Canlak platform, which in 2023 acquired Ceramic Industrial Coatings, bringing four North American plants into its fold, specializing in UV, waterborne, and 2-K polyurethane chemistries. Cloverdale, on the other hand, is carving a niche by emphasizing its regional identity, pioneering carbon-capture resins, and adopting just-in-time mixing, especially as larger players step back from smaller batch services. RPM made headlines with its June 2025 acquisition of Ready Seal, bolstering its presence in the outdoor wood segment. Technology is emerging as the focal point of competition.

AkzoNobel is championing UV-cured polyurethanes that eliminate mix ratios; Sherwin-Williams is highlighting its GREENGUARD Gold certifications; and Canlak is making waves with drop-in clears that seamlessly integrate with traditional gun settings. Distributors that provide color-match software, viscosity troubleshooting, and LEED documentation are securing loyalty from the diverse cabinet shops in the market.

Canada Industrial Wood Coatings Industry Leaders

The Sherwin Williams

Akzo Nobel N.V.

PPG Industries Inc.

Axalta Coating Systems

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: AkzoNobel launched RUBBOL WF 3350, a sprayable water-borne coating with 20% bio-based content that meets sub-50 g/L VOC requirements, targeting LEED-specified furniture and joinery projects.

- January 2025: AkzoNobel rolled out the Selva Pro polyurethane–acrylic system for kitchens, bathrooms, and millwork through the Chemcraft distributor network, focusing on renovation demand in aging housing stock.

Canada Industrial Wood Coatings Market Report Scope

Industrial wood coatings are high-performance finishes designed to enhance durability, aesthetics, and resistance to environmental factors such as moisture, UV rays, and chemicals. Commonly used on furniture, cabinetry, and flooring, these coatings offer various finishes, utilizing waterborne, solvent-borne, or UV-curing technologies.

The Canada Industrial Wood Coatings Market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into acrylic, nitrocellulose, polyester, polyurethane, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, UV coatings, and powder coatings. By end-user industry, the market is segmented into wooden furniture, joinery, flooring and others end-user industries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylic |

| Nitrocellulose |

| Polyester |

| Polyurethane |

| Other Resin Types |

By Technology

| Water-Borne |

| Solvent-Borne |

| UV Coatings |

| Powder Coatings |

By End-user Industry

| Wooden Furniture |

| Joinery |

| Flooring |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Nitrocellulose | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By Technology | Water-Borne |

| Solvent-Borne | |

| UV Coatings | |

| Powder Coatings | |

| By End-user Industry | Wooden Furniture |

| Joinery | |

| Flooring | |

| Other End-user Industries |

Key Questions Answered in the Report

How large will Canada’s industrial wood coatings demand be in 2031?

The Canada industrial wood coatings market size stands at USD 211.73 million in 2026, and it is projected to reach USD 254.28 million by 2031 at a 3.73% CAGR.

Which resin dominates orders from Canadian furniture makers?

Polyurethane claims a 56.85% share thanks to abrasion resistance and compliance with the upcoming 275 g/L VOC cap.

What technology is growing fastest with Canadian cabinet shops?

Waterborne formulations are projected to rise at a 4.48% CAGR as shops pivot to low-VOC systems that match solvent performance.

How will the AkzoNobel-Axalta merger influence Canadian buyers?

Potential divestitures could shift supply to mid-tier players, but expanded R&D scale may speed innovation in low-emission products.

What federal policy most affects long-term growth?

CAD 700 million in loan guarantees for modular off-site timber factories underpins future factory-applied coating demand.

Page last updated on: