Fiducial Markers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

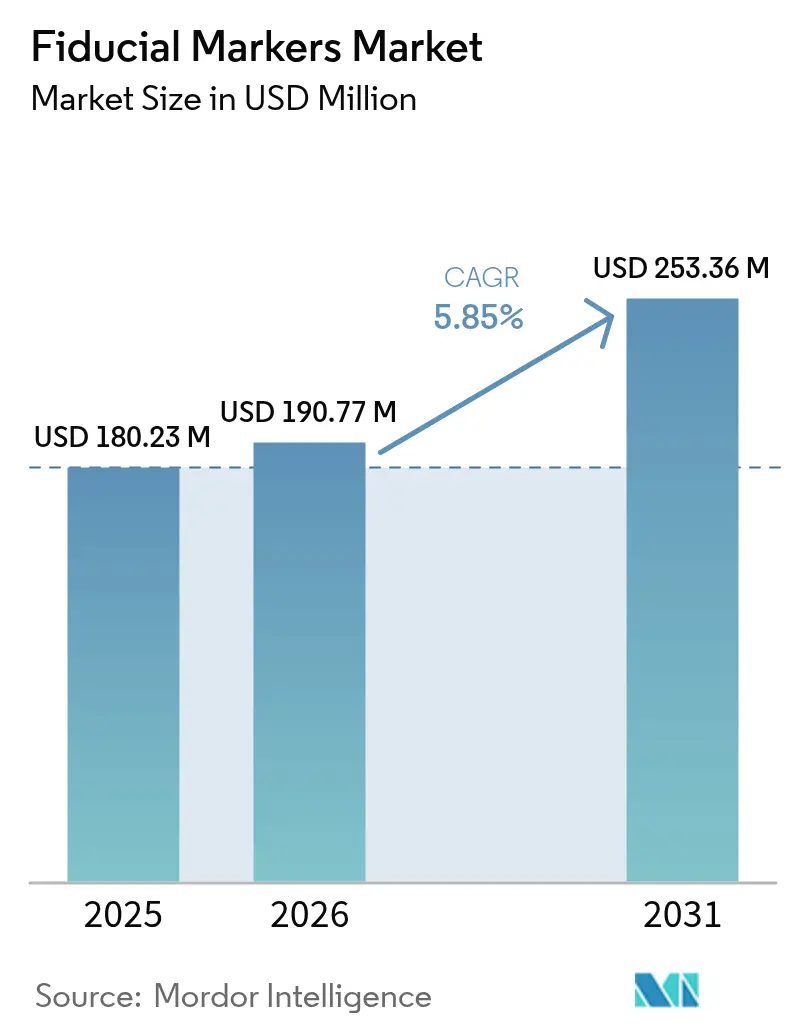

| Market Size (2026) | USD 190.77 Million |

| Market Size (2031) | USD 253.36 Million |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

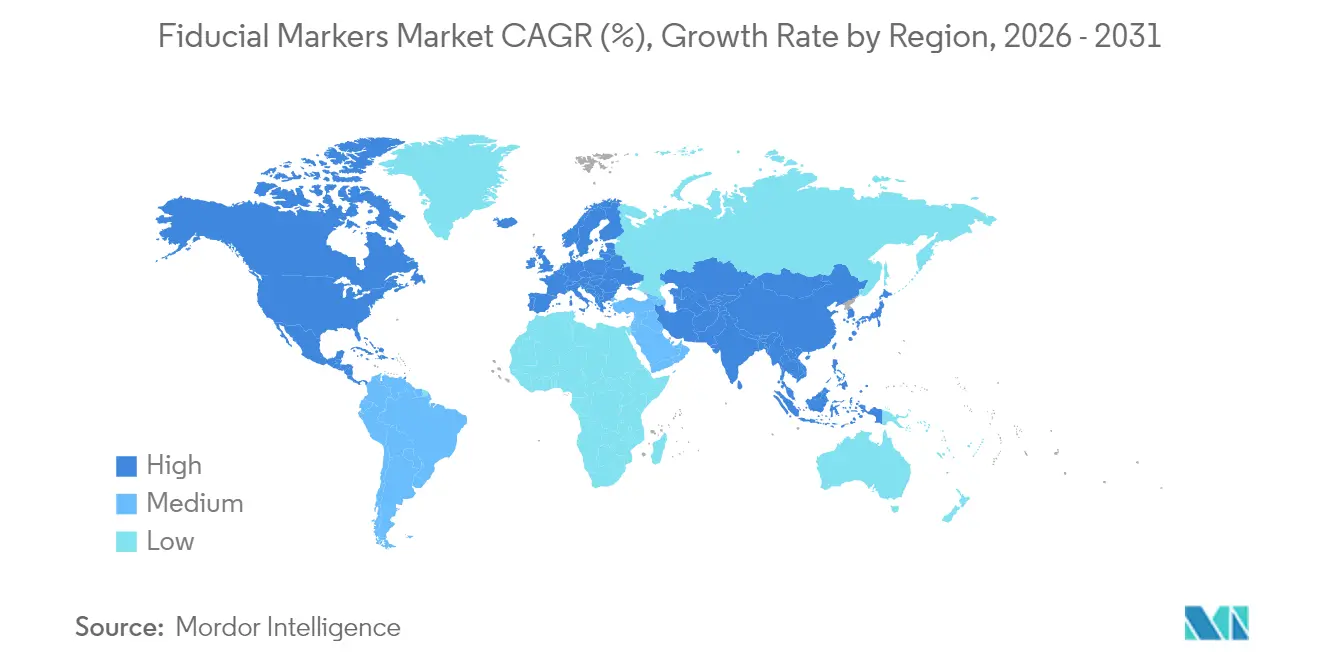

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiducial Markers Market Analysis by Mordor Intelligence

The fiducial markers market size was valued at USD 180.23 million in 2025 and estimated to grow from USD 190.77 million in 2026 to reach USD 253.36 million by 2031, at a CAGR of 5.85% during the forecast period (2026-2031). Growth is anchored in the need for sub-millimeter localization accuracy as image-guided radiotherapy (IGRT) becomes the standard of care across oncology centers. A steady rise in global cancer diagnoses, with over 20 million new cases reported in 2023, continues to expand the patient pool requiring radiation treatment. At the same time, hospital investments in CT/CBCT, MRI-linac, and proton therapy equipment upgrade workflows that depend on implanted or injectable reference points. Payer policies in North America and parts of Europe now reimburse fiducial placement when clinically justified, encouraging providers to adopt value-adding marker innovations. Competitive intensity remains moderate, but recent strategic acquisitions, such as Lantheus Holdings’ January 2025 purchase of Evergreen Theragnostics and Life Molecular Imaging, illustrate a shift toward bundled imaging therapeutic solutions that enhance differentiation.

Key Report Takeaways

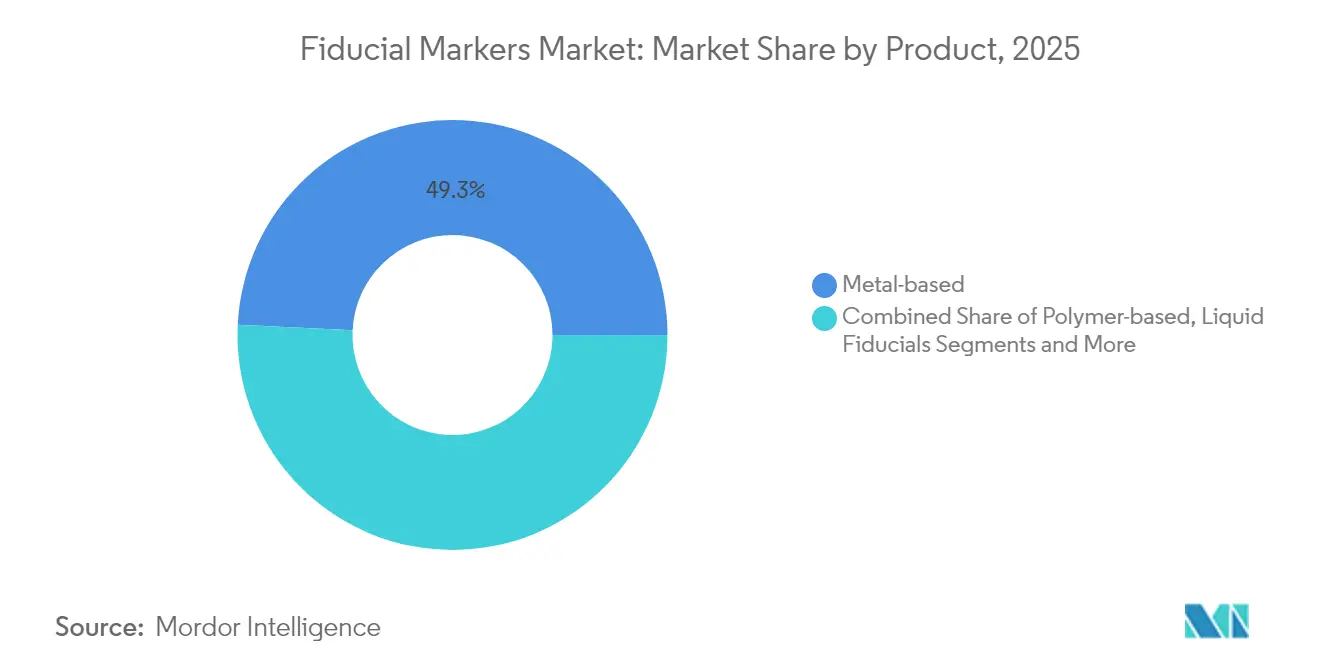

- By product, gold-based fiducials held 49.25% of 2025 revenue; liquid hydrogel markers are projected to grow at a 9.12% CAGR to 2031.

- By modality, CT/CBCT systems commanded 57.05% of the fiducial markers market share in 2025, while MRI-guided systems exhibit the fastest expansion at 7.88% through 2031.

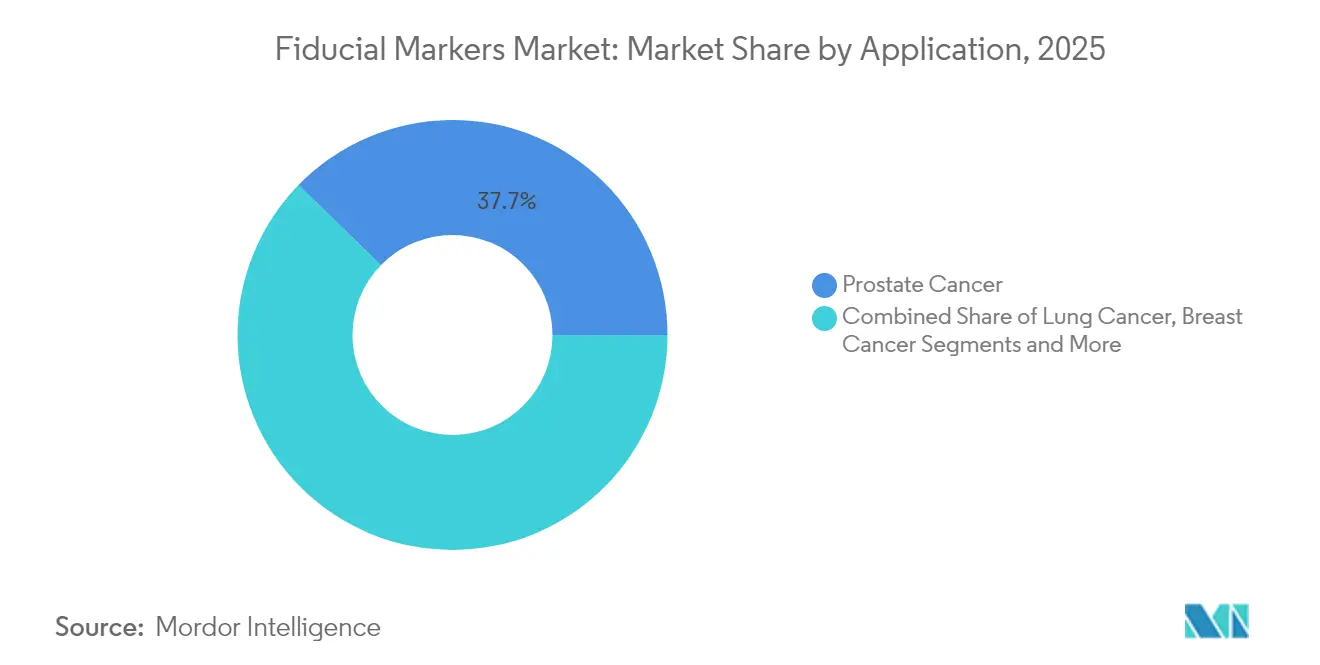

- By application, prostate cancer accounted for 37.70% of 2025 demand; pancreatic and liver use cases are advancing at a 9.06% CAGR.

- By end user, hospitals represented 62.80% of 2025 sales, yet ambulatory radiotherapy clinics are growing at 7.55% as outpatient care scales.

- geographically, North America led with 38.05% revenue share in 2025, while Asia-Pacific is projected to grow at a 6.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fiducial Markers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Incidence Of Cancer | 1.80% | Global | Long term (≥ 4 years) |

| Rising Adoption Of Image-Guided Radiotherapy | 1.50% | North America & EU, APAC core | Medium term (2-4 years) |

| Increasing Reimbursement Coverage For IGRT Procedures | 1.20% | North America & EU | Medium term (2-4 years) |

| Emergence Of Liquid Hydrogel Fiducials For MRI-Guided Adaptive RT | 0.90% | Global, with early gains in North America, Germany | Short term (≤ 2 years) |

| AI-Driven Real-Time Tumor-Tracking Systems Boosting Fiducial Demand | 0.60% | North America, EU, Japan | Short term (≤ 2 years) |

| Expansion Of Proton Therapy Centers Globally | 0.40% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Cancer

Global cancer diagnoses climbed to more than 20 million in 2023, and epidemiologists project roughly 35 million annual cases by 2050, expanding radiotherapy utilization and, consequently, fiducial marker demand.[1]International Agency for Research on Cancer, “GLOBOCAN 2022,” iarc.who.int Half of all cancer patients eventually receive radiation, and tumors such as prostate and lung malignancies, which together dominate fiducial placement, are highly correlated with aging demographics in high-income nations. Asia-Pacific now absorbs a rising portion of this burden, and the region’s capital spending on linear accelerators and particle therapy rooms is accelerating to keep pace. Hospitals in urban China and India increasingly mandate IGRT workflows, positioning the fiducial markers market for sustained long-term growth.

Rising Adoption of Image-Guided Radiotherapy

Cone-beam CT has become a routine adjunct on modern linacs, explaining CT/CBCT’s 57.6% 2024 share of the fiducial markers market. Newer MRI-linac installations deliver superior soft-tissue contrast but require fiducials that do not distort magnetic images; liquid hydrogels, therefore, gain ground at an 8.2% CAGR. The February 2024 FDA clearance for Varian’s HyperSight upgraded CBCT workflow and halved image acquisition time, improving throughput and marker visualization. Even “markerless” tracking research cements the importance of high-contrast reference objects because algorithm training relies on fiducial benchmarks that underpin accuracy ratings.

Increasing Reimbursement Coverage for IGRT Procedures

Since 2024, the US Centers for Medicare & Medicaid Services has clarified billing rules for IGRT, allowing separate payment for fiducial placement when medically necessary.[2]Centers for Medicare & Medicaid Services, “Transmittal 12052: IGRT Billing Guidance,” cms.govSeveral EU payers have followed, assigning bundled Diagnosis-Related Group add-ons once practitioners document outcome advantages. The resulting revenue certainty is persuading outpatient oncology chains to install marker-friendly imaging suites, a dynamic that helps ambulatory clinics outpace hospital growth rates. Payers also view fewer treatment fractions and lower toxicity as downstream savings, reinforcing a pro-fiducial coverage stance.

Emergence of Liquid Hydrogel Fiducials for MRI-Guided Adaptive RT

Hydrogel formulations such as BioXmark improve multimodal visibility and create negligible CT artifacts while offering conspicuous MRI contrast, attributes that reduce replanning events and shorten simulation sessions. The clinical series on EUS-guided pancreatic placement reports technical success of 85–100%, with adverse events under 7.6%, giving physicians confidence in treating anatomically challenging sites.[3PubMed, “Fiducial Migration Meta-analysis,” pubmed.ncbi.nlm.nih.gov ] As proton-MRI prototypes move from research to clinical pilots, for instance, Dresden launched the first in January 2024, demand for artifact-free, absorbable markers is set to surge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit Cost Of Gold-Based Markers | -0.80% | Global, particularly cost-sensitive markets | Medium term (2-4 years) |

| Risk Of Marker Migration Causing Re-Planning | -0.60% | Global | Short term (≤ 2 years) |

| MRI Artefacts Interfering With Auto-Segmentation Workflows | -0.40% | Global, concentrated in MRI-guided RT centers | Short term (≤ 2 years) |

| Stringent Regulatory Approval Timelines For Novel Fiducials | -0.30% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost of Gold-Based Markers

A single gold marker can cost multiples of polymer alternatives, and patients often need three per lesion, straining budgets in capitated systems. While clinical familiarity upholds gold’s 49.9% share, buyers in Brazil, India, and parts of Eastern Europe now trial polymer or hydrogel substitutes that offer lower acquisition and placement costs without compromising visibility. Hospitals using activity-based costing find that total episodic spend falls when market price declines, particularly once imaging verification and replanning overheads are included.

Risk of Marker Migration Causing Re-Planning

Migration rates of 1.7–7.6% interrupt treatment schedules, trigger added CT scans, and divert physicist time toward recontouring. In prostate and liver cases, even a 2 mm shift forces dose redistribution to protect surrounding structures, delaying therapy initiation. Manufacturers now add helical grooves and deployable wings to improve tissue anchorage, yet smaller ambulatory centers may lack the resources to buy newer designs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diversifying Beyond Gold

Gold-based devices comprised 49.25% of the fiducial markers market share in 2025, reflecting decades of decision-maker confidence in their radiopacity and inertness. Yet polymer, platinum, and hydrogel formats are steadily chipping away at that dominance as MRI-compatible workflows expand. The fiducial markers market size attributed to liquid hydrogels is rising at a 9.12% CAGR, aided by their artifact-free profile and eventual bio-absorption, a preference shared by clinicians and patients who seek temporary implants.

Clinical trials now demonstrate that polymer markers paired with CBCT achieve equivalent localization accuracy in prostate and lung stereotactic body radiotherapy. Cost differentials, sometimes exceeding 30% per lesion, are relevant in lower-middle-income countries where public insurance must stretch procurement budgets. Premium gold configurations, such as coiled designs that resist migration, retain utility in highly mobile organs, though their unit price limits uptake outside tertiary referral centers.

By Modality: CT/CBCT Remains the Workhorse

CT/CBCT systems generated 57.05% of fiducial markers market revenue in 2025 because nearly every linac fleet includes cone-beam hardware, ensuring consistent marker visibility. The fiducial markers market size linked to MRI-guided systems is, however, expanding at an 7.88% CAGR, signaling that soft-tissue contrast superiority is gaining fiscal endorsement among capital-rich centers.

Upgrades such as HyperSight elevate CBCT quality enough to reduce artifacts from metallic markers, prolonging CT relevance. Simultaneously, hybrid MRI-proton prototypes in Europe demonstrate early-stage promise but will need fiducial materials that do not upset magnetic homogeneity or proton range. Ultrasound continues as a placement modality in hepatobiliary lesions, although its real-time tracking role is dwarfed by X-ray or MRI.

By Application: Urology Leads, Gastrointestinal Oncology Accelerates

Prostate protocols dominated usage with 37.70% of 2025 because the gland’s motion relative to the bladder and rectum necessitates implanted references; gold coils remain the most commonly used design. Fiducial markers market size devoted to pancreatic and liver tumors is expanding, as EUS-guided injections mitigate the anatomical inaccessibility that previously limited high-dose SBRT in these organs.

Pancreatic fiducial placement can now be completed in less than 20 minutes under moderate sedation, contributing to the observed 9.06% CAGR in that sub-segment. Meanwhile, bronchoscopic marker deposition coupled with respiratory gating improves lung SBRT conformity. Breast surgery teams are adopting bio-absorbable clips visible on ultrasound and MRI for lumpectomy cavity localization, preferring temporary devices that do not alter mammographic follow-up.

By End User: Inpatient Strength, Outpatient Momentum

Hospital centers captured 62.80% of 2025 purchases due to integrated oncology departments that place markers during diagnostic imaging or surgery under one roof. Large teaching hospitals often bundle fiducial spend into broader capital budgets that include linac and imaging upgrades.

Conversely, ambulatory clinics, growing at 7.55%, capitalize on payer incentives that favor shorter care cycles and convenient access. These facilities frequently outsource marker placement to interventional radiologists, yet have begun training in-house teams to cut referral delays, boosting throughput. Cancer specialty centers leverage advanced modalities and AI-enhanced tracking to command premium reimbursements, making them early adopters of polymer and hydrogel innovations.

Geography Analysis

North America led the fiducial markers market in 2025, backed by high per-capita health expenditure and clear reimbursement for IGRT procedures. Regulatory certainty under the FDA’s 510(k) process encourages continuous product iteration, while academic centers such as Penn Medicine drive early clinical validation for emerging designs.

Europe follows, supported by structured healthcare financing and the EU MDR framework, which, though demanding, facilitates continent-wide market entry once clearance is earned. Dresden’s MRI-guided proton program showcases European leadership in adaptive technologies reliant on non-metallic fiducials. National authorities, particularly in Germany and the Nordics, reward cost-effective innovations, spurring polymer uptake.

Asia-Pacific is the fastest-growing region, buoyed by national cancer plans in China, Japan, and South Korea that fund proton rooms and high-end MRI-linacs. China’s 77 active proton or heavy-ion projects highlight scale, while local firms develop cost-optimized polymer markers tailored to domestic price points. In Southeast Asia, private hospital chains import hydrogel devices for liver and pancreatic programs catering to medical tourism.

Regulatory Landscape

In the United States, fiducial markers used for radiation therapy are generally regulated as Class II medical devices under FDA oversight, most commonly via the 510(k) pathway for substantial equivalence. Product classification commonly falls under product code IYE for implantable radiology markers and QUV for phase-changing fiducial markers for radiation therapy, where special controls emphasize evidence around visualization, migration, and interference or artifact behavior. FDA classification activity remained visible in 2026, including an April 2026 Federal Register rulemaking on radiation therapy marking device classification.

In Europe, fiducial markers are governed under the EU Medical Device Regulation (MDR, Regulation (EU) 2017/745), requiring conformity assessment prior to CE marking based on intended use and risk. Interoperability requirements also shape compliance and procurement. Radiotherapy-relevant DICOM standards, for example NEMA DICOM CID 7112 for radiotherapy fiducials, support consistent identification and registration of fiducials across imaging and radiotherapy planning systems.

Value Chain Analysis

The fiducial markers value chain begins with specialized raw materials, for example gold or platinum, and engineered polymers or ceramics such as zirconium oxide. This is followed by precision fabrication, including machining, coiling, or molding depending on the design, plus finishing and validated sterilization, frequently using ethylene oxide. Downstream steps include packaging and labeling aligned to device regulatory requirements, distribution through medical device channels, and clinical deployment through interventional radiology, gastroenterology (EUS-guided placement), urology, and radiation oncology workflows where markers are implanted or injected and then visualized on CT/CBCT or MRI for planning and IGRT delivery.

Quality and compliance requirements act as a gate across the value chain. In the United States, the FDA Quality Management System Regulation (QMSR) became effective on February 2, 2026, incorporating ISO 13485:2016 into 21 CFR Part 820 and raising the bar on documentation and supplier controls across the chain. Operational risk tends to concentrate around continuity of specialty materials, sterilization capacity constraints, and supplier qualification, particularly as demand shifts toward MRI-compatible and injectable fiducials that require tighter controls on biocompatibility testing (commonly aligned to ISO 10993) and on performance consistency for migration and imaging artifacts.

Competitive Landscape

Competition is moderate, featuring specialized firms and diversified med-tech conglomerates. IZI Medical Products, CIVCO Radiotherapy, and Gold Anchor hold strong brand equity on the strength of long-term clinical data, while enterprises such as Medtronic and Boston Scientific enter through adjacent interventional portfolios. Strategic alliances trend upward: Lantheus Holdings’ early-2025 dual acquisition strengthens its diagnostic-theranostic bundling capability, foreshadowing integrated care models.

Technological differentiation surrounds material science and AI. Hydrogel developers emphasize MRI clarity and absorption profiles, whereas polymer innovators stress cost control. Siemens-Varian’s HyperSight release demonstrates hardware–marker co-development as a route to lock-in, integrating imaging protocols pre-tuned for specific fiducials. Patent filings covering coiled shapes and AI detection algorithms remain brisk at the USPTO, signaling ongoing innovation cycles.

Financial resilience is an emerging separator. ViewRay’s April 2025 Chapter 11 filing shows that even clinically lauded systems can falter without scale. In contrast, integrators with broad oncology software stacks enjoy recurring revenue that cushions R&D risk. M&A activity is therefore expected to tighten market concentration moderately over the forecast horizon.

Fiducial Markers Industry Leaders

IZI Medical Products

CIVCO Radiotherapy

Boston Scientific Corp.

Gold Anchor (Naslund Med.)

Nanovi A/S

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace centers on fiducials that maintain high visibility while minimizing MRI susceptibility artifacts and supporting adaptive workflows, aligning with the market shift toward MRI-guided radiotherapy and multimodality image fusion. The FDA has established a distinct Class II category for phase-changing fiducial markers (product code QUV), with special controls that focus on migration and visualization performance. This provides manufacturers a clearer route to differentiate injectable or novel-material designs when paired with clinical data.

Non-invasive or less invasive approaches also create incremental adoption room, including accessory or patient-specific devices that embed markers for tracking without permanent implantation, such as 3D-printed intravaginal devices reported in clinical research settings. Another opportunity sits at the photon-to-proton interface, where universal marker designs that reduce beam perturbation and remain reliably trackable across CT/CBCT and MRI can simplify protocols for centers expanding IGRT and proton programs. This complements ongoing hardware and workflow upgrades in radiotherapy that depend on consistent fiducial detectability during planning and treatment verification.

Recent Industry Developments

- July 2026: IZI Medical announced the acquisition of Naslund Medical, the Sweden-based developer of Gold Anchor fiducial markers. The deal brings Gold Anchor into IZI Medicals fiducial portfolio alongside Visicoil offerings and strengthens its position in radiotherapy localization workflows. The move also reflects consolidation around established fiducial brands as providers standardize on fewer, better-validated SKUs.

- May 2026: CQ Medical announced the acquisition of .decimal, a manufacturer of patient-specific beam shaping devices used in radiation therapy. The transaction broadens CQ Medicals footprint across radiotherapy hardware and workflow components that are procured alongside localization and planning tools. A wider portfolio can support bundling strategies with adjacent products used in IGRT-enabled treatment pathways.

- July 2024: CIVCO Radiotherapy and Qfix formally transitioned into a combined brand, CQ Medical, and highlighted an expanded radiation therapy portfolio that includes BioXmark liquid fiducial markers (manufactured by Nanovi A/S). The rebrand unified product lines under one commercial platform and improved portfolio visibility for departments sourcing immobilization, QA, and localization tools together. It also reinforced availability of liquid fiducials in mainstream radiotherapy procurement channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the fiducial markers market covers medical markers that are placed in or near a target anatomy to support localization during imaging and radiation therapy planning and delivery.

Scope exclusions: We exclude non-medical fiducial concepts like printed alignment marks used in electronics, packaging, and general machine-vision registration tasks.

Segmentation Overview

- By Product

- Metal-based

- Polymer-based

- Liquid / Hydrogel Fiducials

- Bio-absorbable Markers

- By Modality

- CT / CBCT

- MRI

- Ultrasound

- X-Ray / Fluoroscopy

- Hybrid MRI-LINAC systems

- By Application

- Prostate Cancer

- Lung Cancer

- Breast Cancer

- Liver and Pancreatic Cancers

- Others

- By End-User

- Hospitals

- Cancer Specialty Centers

- Ambulatory Radiotherapy Clinics

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the clinical and procedural context, then translate that context into measurable demand signals. We referenced public sources such as the World Health Organization for cancer burden, the International Agency for Research on Cancer for incidence trends, and sources like the US FDA device databases for product clearances and labeling notes.

To ground procedure and modality assumptions, we also used government and health-system publications, including the US Centers for Medicare and Medicaid Services for reimbursement and coding signals, and peer reviewed journals indexed on PubMed for placement practices and modality visibility (CT/CBCT, MRI, ultrasound, and fluoroscopy). Company filings, investor presentations, association websites, and reputed healthcare press were used to understand rollout pace and portfolio focus. Where available, paid subscriptions for company financials, news and financials, and patent databases helped cross-check timelines and product pipelines. These desk sources are not exhaustive, and we also used other public references for clarification and validation during the work.

Primary Interviews and Surveys

Primary work focused on validating what gets bought, how often it is replaced, and what drives pricing in different care settings. We interviewed manufacturers, distributors, clinicians involved in placement, and radiation therapy decision-makers across APAC, EMEA, and the Americas, so the model assumptions could be adjusted when desk signals looked inconsistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 39% |

| Mid tier: 55% | Functional/Unit leaders: 38% | EMEA: 37% |

| Smaller Players: 15% | Managers: 47% | Americas: 24% |

Market-Sizing & Forecasting

The core model uses a top-down demand pool build that starts from addressable radiotherapy and image-guided workflows, which are then filtered through where fiducial placement is clinically common. From there, value is built by combining expected procedures with typical markers used per case and an average selling price that is normalized by modality and material type.

Inputs that materially shape the totals include cancer incidence and treatment patterns, the mix of indications where markers are routinely used (such as prostate and lung), the adoption level of IGRT and advanced systems (including CT/CBCT and MRI guided workflows), and reimbursement and coding signals that influence placement volume. We also tracked practical buying factors like hospital versus ambulatory center usage, replacement frequency, and price differences between metal, polymer, and liquid or bio-absorbable options. Select bottom-up checks are then used to keep totals realistic, such as sampling a set of supplier revenues, validating distributor flow, and using ASP times volume sanity checks in priority countries, with gaps handled through conservative ranges agreed during interviews.

For forecasting, scenario analysis is applied so slower and faster adoption paths can be expressed clearly, followed by expert-reviewed assumptions for procedure growth and modality mix shift. Where historic patterns were stable, light time-series smoothing was used to avoid overreacting to one-off events, and the final curve was adjusted only when the drivers were supported by interview consensus.

Data Validation & Update Cycle

Validation is done through multiple passes so the numbers stay tied to real-world clinical activity and procurement behavior. We compare outputs against independent signals such as procedure volumes, installed base cues for imaging guided radiotherapy, and observed pricing bands, then investigate any outliers before sign-off.

If a variance cannot be explained by geography mix, modality mix, or a timing effect, we re-contact the relevant respondents and revisit the assumption that caused the swing. Reports are refreshed annually, with interim updates when major regulatory changes, reimbursement shifts, or notable technology adoption events materially affect demand. Before delivery, an analyst performs a fresh check so clients receive the most current view available at the time of release.

Mordor Intelligence's Fiducial Markers Market Size Compared With Other Published Estimates

Published market values for fiducial markers can differ for the same year because the scope is not always aligned, and the pricing logic can be treated differently. Differences typically come from what is counted as a fiducial marker, which clinical settings are included, and how modality shifts are translated into average selling prices.

Some external estimates bundle adjacent radiotherapy accessories or broader oncology device spend into the same total, which raises the overall figure even if unit usage is unchanged. In contrast, Mordor Intelligence limits the count to medical fiducial markers used in image-guided radiotherapy and related localization workflows, and then ties value to procedure-based demand signals and modality-specific ASP checks refreshed during updates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 190.77 M (2026) | |

| Global Consultancy A | USD 0.23 B (2026) | Uses a broader oncology adjuncts scope and applies blended pricing without separating CT/CBCT versus MRI visibility driven product mix, which can lift the modeled ASP and inflate value. |

| Trade Journal B | USD 165.00 M (2026) | Leans on a narrower hospital-only purchasing view and omits part of the ambulatory radiotherapy clinic demand, and it also carries forward older price points with limited refresh for new liquid or bio-absorbable introductions. |

Across the three figures, most of the spread can be traced to scope choices and how pricing is updated as modality and material mix change. When the market is tied back to procedure volume, markers-per-case, and realistic price bands by setting, the resulting number is easier to reconcile and re-create year to year.

Key Questions Answered in the Report

What is the current value of the fiducial markers market?

The market is valued at USD 190.77 million in 2026 and is projected to hit USD 253.36 million by 2031.

Which product type leads the fiducial markers market in 2025?

Gold-based markers remain dominant, holding 49.25% of 2025 revenue because of proven radiopacity and physician familiarity.

How quickly is the MRI-guided segment growing?

MRI-compatible fiducial solutions are expanding at an 7.88% CAGR through 2031, the fastest among imaging modalities.

Why are liquid hydrogel fiducials gaining attention?

They exhibit high MRI visibility, create minimal CT artifacts, and absorb over time, driving a 9.12% CAGR in their segment.

Page last updated on: