Fiber Reinforced Concrete Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

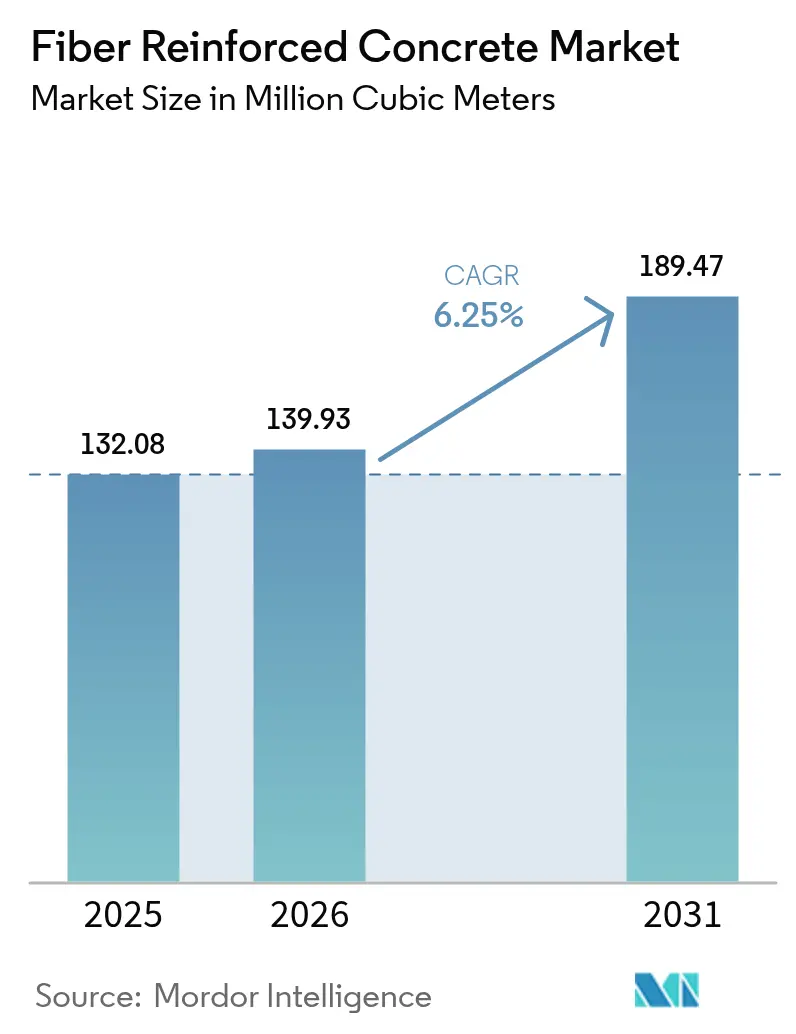

| Market Volume (2026) | 139.93 Million cubic meters |

| Market Volume (2031) | 189.47 Million cubic meters |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Reinforced Concrete Market Analysis by Mordor Intelligence

The Fiber Reinforced Concrete Market size is projected to expand from 132.08 Million cubic meters in 2025 and 139.93 Million cubic meters in 2026 to 189.47 Million cubic meters by 2031, registering a CAGR of 6.25% between 2026 to 2031. Demand stems from infrastructure stimulus packages, stricter embodied-carbon codes, and hyperscaler preference for precast solutions that fast-track data-center delivery. Steel fiber currently dominates heavy-duty pavements and tunnels, yet glass and macro-synthetic grades are gaining share as architects seek corrosion immunity, lighter panels, and labor savings. Rebar price volatility across emerging markets accelerates the shift toward macro-synthetic fibers, while 3D-printed concrete pilots open specialty niches for short, dispersible strands that prevent nozzle clogging. As regulatory bodies embed whole-life-carbon accounting, suppliers that publish facility-specific EPDs and co-optimize admixtures with fibers carve out a competitive edge.

Key Report Takeaways

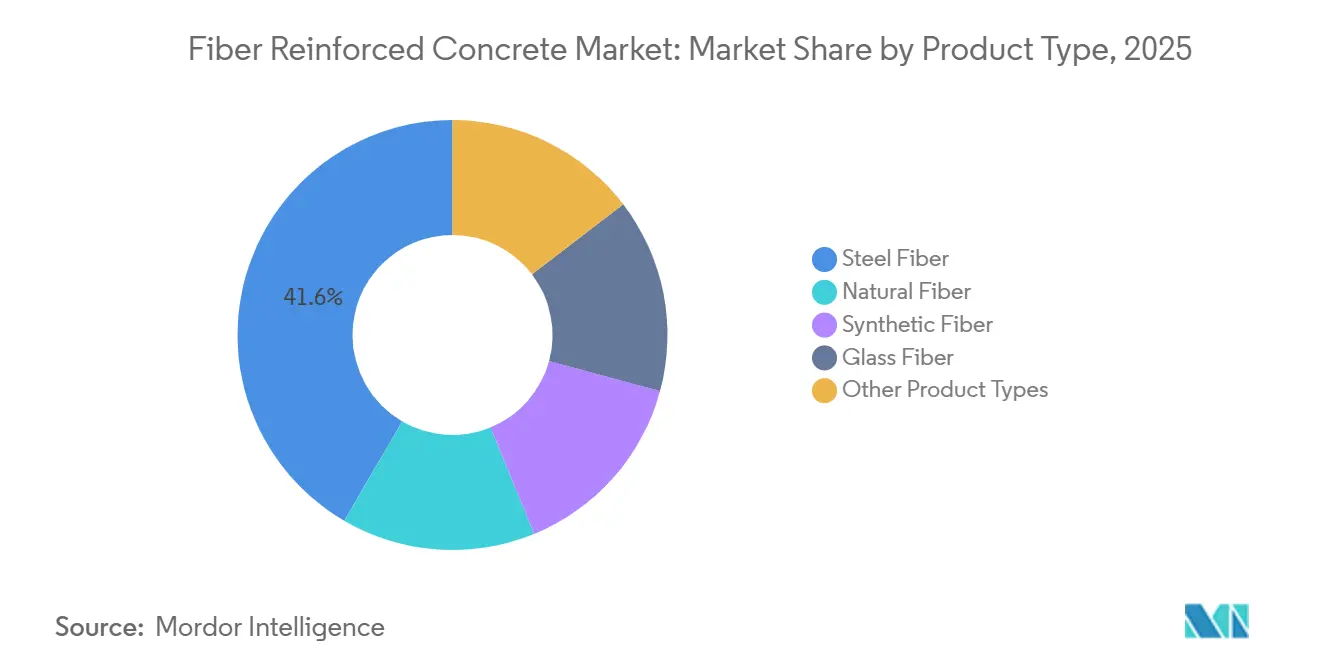

- By product type, steel fiber captured 41.60% of fiber reinforced concrete market share in 2025, while glass fiber is advancing at a 7.34% CAGR through 2031.

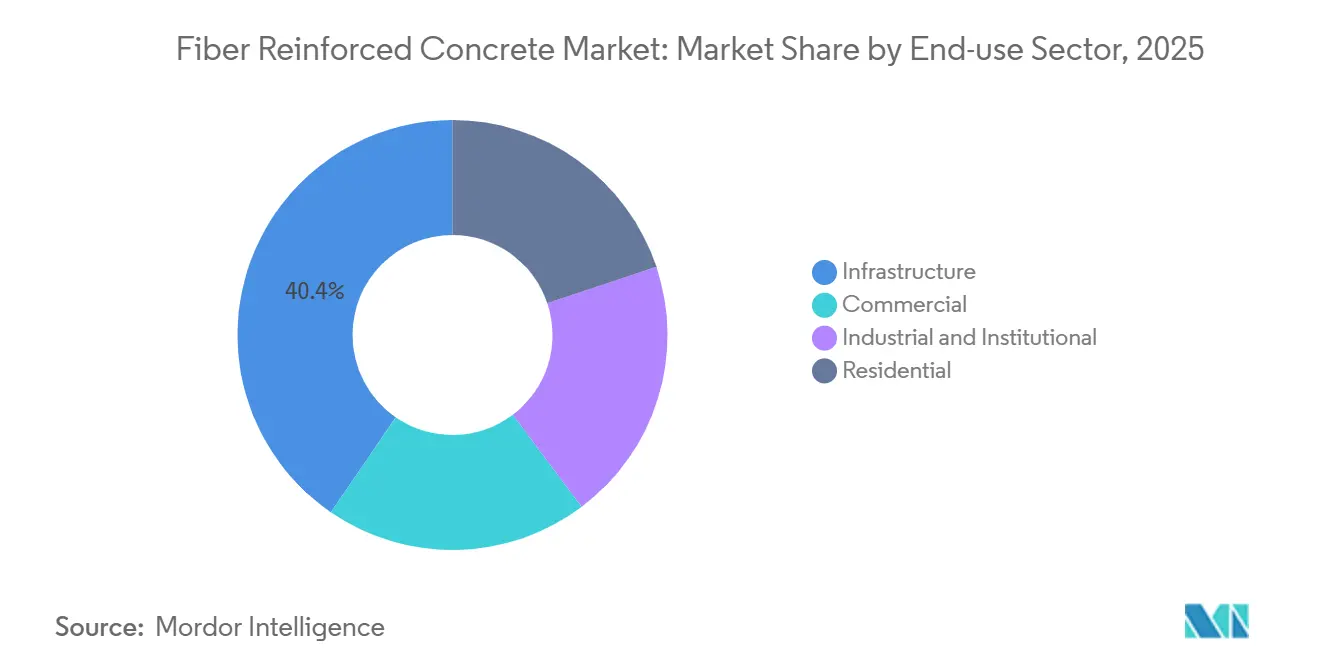

- By end-use sector, Infrastructure accounted for 40.41% fiber reinforced concrete market share, but the commercial segment is set to grow fastest at 6.97% CAGR through 2031.

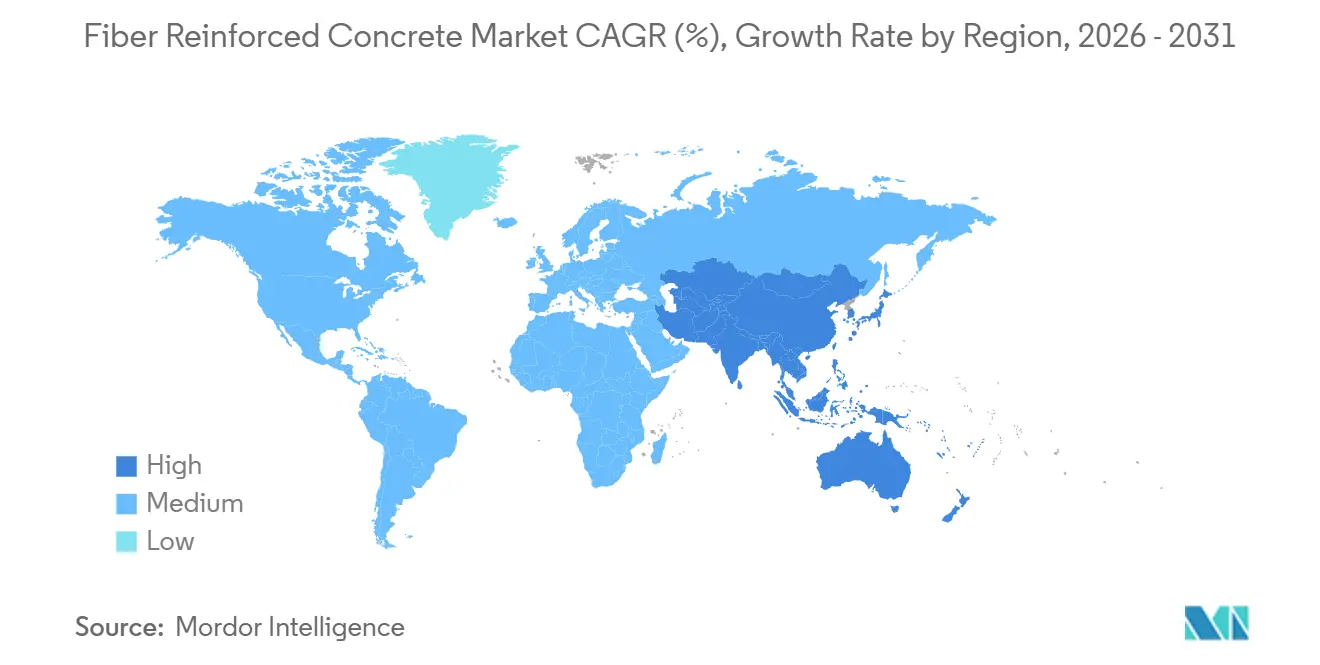

- By geography, Asia-Pacific captured 46.22% of fiber reinforced concrete market share in 2025 and the region is advancing at a 6.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fiber Reinforced Concrete Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega-infrastructure stimulus pipelines | +1.8% | Global, concentrated in APAC (China, India, Vietnam, Indonesia), Middle-East (Saudi Arabia, UAE), spill-over to Africa | Long term (≥ 4 years) |

| Green-building codes mandating low-embodied-carbon mixes | +1.2% | North America (California, Oregon, Massachusetts) and EU, early adoption in Australia | Medium term (2-4 years) |

| Precast-modular data-center build-outs | +0.9% | North America and EU core, APAC expansion (Singapore, India) | Short term (≤ 2 years) |

| Rebar price volatility hedging in emerging markets | +0.7% | APAC (India, Southeast Asia), South America (Brazil), MEA | Medium term (2-4 years) |

| 3D-printed concrete parts adoption | +0.4% | North America, EU pilot markets, select APAC innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mega-Infrastructure Stimulus Pipelines

Infrastructure programs such as China’s Belt and Road Initiative continue to absorb hundreds of millions of cubic meters of concrete every year, with tunnels, ports, and rail corridors adopting steel or macro-synthetic fibers to cut on-site rebar work and accelerate schedules. Saudi Vision 2030 mega-projects, India’s USD 1.4 trillion National Infrastructure Pipeline, and new expressways in Vietnam and Indonesia follow a similar pattern, specifying fiber reinforcement to withstand extreme climates and seismic zones. Government funding flows favor precast components that minimize skilled labor bottlenecks, lifting the fiber reinforced concrete market across APAC and the Middle-East. As shovel-ready projects proliferate, suppliers capable of delivering high-volume, field-proven fiber mixes win preferred-vendor status. The multiplier effect on downstream cement and admixture demand underpins a stable, long-duration growth runway for the fiber reinforced concrete market.

Green-Building Codes Mandating Low-Embodied-Carbon Mixes

California’s 2024 CALGreen amendments, Oregon and Massachusetts ordinances, and the EU Taxonomy set explicit embodied-carbon ceilings that penalize clinker-heavy concrete and reward high-SCM blends stabilized with fibers. Builders now pair fly-ash, slag, or LC3 binders with glass and recycled-polypropylene fibers to recover early-age strength without adding steel. Berkeley’s rule requiring facility-specific EPDs further advantages vertically integrated suppliers that control emissions data across the value chain. FORTA-branded recycled fibers give contractors dual credits for low carbon and recycled content under LEED v5 and BREEAM[1]FORTA Corporation, “FERRO-GREEN Technical Sheet,” fortacorp.com . The outcome is a structural shift in specifications, driving sustained penetration of alternative fibers and cement chemistries into the fiber reinforced concrete market.

Precast-Modular Data-Center Build-Outs

Hyperscalers plan dozens of gigawatt-scale campuses, with Google alone earmarking USD 40 billion for U.S. facilities and EUR 5.5 billion for German expansions. The Open Compute Project’s 2024 trials proved that fiber-reinforced, high-SCM concrete can trim embodied carbon by over 50% without sacrificing load capacity. Precast panels infused with macro-synthetic or glass fibers eliminate on-site welding, reduce dust, and shorten erection times by up to 30%, benefits that resonate with data-center schedules measured in weeks. Procurement teams screen suppliers through the EC3 tool, favoring those offering ISO 14025 EPDs, which cements the fiber reinforced concrete market as the default structural solution for digital-infrastructure projects.

Rebar Price Volatility Hedging in Emerging Markets

Energy-driven scrap-price swings lifted rebar costs through 2025, pushing contractors in India, Brazil, and Southeast Asia to replace welded-wire fabric with macro-synthetic fibers dosed at 3-7 lb/yd³. Local cement majors rolled out turnkey fiber-concrete products to capture this substitution wave, stressing theft mitigation and faster placement. Florida DEP test data show synthetic fibers delivering equivalent residual strength at a fraction of the weight of steel fibers[2]Florida Department of Environmental Protection, “Approved Fiber List for Concrete Receptacles,” floridadep.gov . Emerging-market builders now incorporate fiber price-adjustment clauses tied to scrap indices, but synthetic alternatives remain inherently more price-stable, supporting continuous uptake in the fiber reinforced concrete market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel-fiber cost premium amid scrap-price swings | -0.6% | Global, acute in APAC and South America where scrap volatility highest | Short term (≤ 2 years) |

| Limited seismic field-data for natural fibers | -0.3% | APAC (India, Indonesia, Philippines), South America (Peru, Chile) | Medium term (2-4 years) |

| Micro-plastic regulations threatening PP/PE fibers | -0.2% | EU primary, potential spill-over to North America and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel-Fiber Cost Premium Amid Scrap-Price Swings

Steel fiber prices track scrap indices with 60-90 day lags, complicating fixed-price bids. On high-volume pavement or apron projects, the material premium can reach USD 15 per m³ over synthetic alternatives, prompting value engineering in cost-sensitive markets. While steel retains superior post-crack capacity, contractors often prioritize budget certainty and reduced logistics complexity, especially where currency depreciation inflates import costs. To preserve share, suppliers are negotiating dynamic-pricing clauses, but the administrative burden dims appeal for small- to mid-scale jobs, tempering growth in the fiber reinforced concrete market.

Limited Seismic Field Data for Natural Fibers

Jute, sisal, and bamboo fibers appeal in tropical economies for cost and carbon reasons, yet cyclic-loading datasets remain thin. Building-code bodies in Indonesia, the Philippines, and the Andean region require validated shake-table results before approving structural use, keeping natural fibers in non-structural partitions and low-rise slabs. Joint industry–academia programs are underway, but code revisions will not materialize until late in the forecast, capping near-term contribution to the fiber reinforced concrete market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Glass Fiber Extends Gains on Corrosion Immunity

Steel fiber held 41.60% of 2025 volume, securing the largest fiber reinforced concrete market share, but glass fiber is projected to post the fastest 7.34% CAGR to 2031. Alkali-resistant zirconia coatings let designers specify 10-15 mm precast façade panels that trim weight and shipping costs while avoiding rust streaks. Macro-synthetic polypropylene and polyethylene lines occupy mid-price niches in residential slabs and sprayed concrete, buoyed by recycled-content variants that meet circular-economy criteria. Natural fibers—mainly jute and sisal—remain niche due to inconsistent tensile properties, while basalt and carbon experiments surface in ultra-high-performance mixes for bridge decks and blast-resistant shells.

Continued R&D focuses on enhancing dispersion and bond of glass and synthetic fibers to maximize residual strength at lower dosages, making them economical replacements for temperature-and-shrinkage rebar. FORTA’s alkali-resistant glass products recorded 37% fewer pavement cracks in an 8-year MnRoad study, driving adoption among U.S. DOTs. As rebar volatility persists, contractors in India and Brazil are shifting incremental volume toward macro-synthetics, a migration that slowly erodes steel share but expands overall fiber reinforced concrete market size through virgin applications like thin-shell architectural cladding.

By End-use Sector: Commercial Segment Accelerates on Data-Center Pipeline

Infrastructure consumed 40.41% of 2025 output, yet the commercial is on track for a sector-leading 6.97% CAGR through 2031. Data-center operators, retail-logistics developers, and mixed-use high-rises specify precast fiber panels to shave weeks off schedules and satisfy corporate carbon budgets. Industrial floors and institutional projects follow, favoring joint-free slabs that cut forklift maintenance and hospital downtime. Residential demand is more price sensitive but grows where builders market crack-free foundations and longer warranties.

Open Compute Project guidelines, now standard in hyperscaler RFQs, explicitly call for fiber reinforcement in high-SCM mixes, embedding the technology in the procurement DNA of a fast-growing asset class. The shift reinforces the fiber reinforced concrete market size trajectory, even as public-works volume moderates after stimulus peaks. Over the forecast horizon, natural-fiber certification could unlock economical reinforcement for low-rise housing in South Asia and Latin America, providing an incremental growth lever once seismic data gaps close.

Geography Analysis

Asia-Pacific controlled 46.22% of 2025 volume and is forecast to climb at a 6.75% CAGR, driven by Belt and Road exports, India’s rail and metro expansion, and Southeast Asian expressways that demand crack-resistant, humidity-tolerant mixes. Chinese contractors increasingly deploy steel and macro-synthetic fibers in overseas projects where remote sites make rebar logistics burdensome. India’s cement majors now bundle fibers with high-SCM binders for pavement overlays and railway sleepers, positioning the fiber reinforced concrete market as a cost-competitive alternative to welded-wire fabric. Mature economies like Japan and South Korea focus on seismic retrofit shotcrete and architectural precast, while Australia tracks more than 8,500 pipeline projects through 2030 that will strain traditional rebar supply chains.

North America and Europe favor low-carbon formulations under CALGreen, the EU Taxonomy, and similar provincial bylaws. Google’s Texas and German campuses showcase fiber-reinforced precast as the go-to solution for embodied-carbon compliance, accelerating technology diffusion into logistics, healthcare, and education builds. REACH Entry 78’s derogation maintains polypropylene fiber viability across Europe, while EC3 screening tools elevate only suppliers with ISO 14025 EPDs, intensifying documentation requirements but reinforcing demand for compliant products.

South America benefits from rebar volatility and local synthetic-fiber capacity in Brazil and Argentina, which hedge currency risk and stabilize construction budgets. The Middle-East gains momentum from Saudi Vision 2030 and UAE smart-city programs that specify steel and glass fibers to handle thermal cycling and saline soils. Sub-Saharan Africa remains nascent but poised for uptake via Chinese EPC contractors importing fiber technology through BRI infrastructure corridors. Together, these dynamics support steady diversification of the global fiber reinforced concrete market.

Competitive Landscape

The fiber reinforced concrete market remains fragmented. Global cement groups such as BASF, Sika, and Holcim package superplasticizers with fibers and digital EPD dashboards, giving them an end-to-end value proposition. Bekaert leads steel fiber volume but faces margin pressure as synthetic alternatives gain traction in cost-sensitive markets. FORTA completed a capacity expansion in Franklin, Pennsylvania in May 2025, citing North American infrastructure momentum. Independent specialists differentiate through alkali-resistant coatings, recycled content, or high-strain products for 3D printing.

M&A chatter centers on cement majors eyeing specialty fiber producers to internalize margins and secure supply. Regional challengers in India and Turkey leverage local markets and flexible pricing to outflank imports, though they lack the EPD libraries demanded by hyperscalers. Start-ups focus on AI-driven mix-design software that optimizes fiber dosage for strength and carbon, compressing development cycles from weeks to hours. As codes tighten documentation and performance thresholds, suppliers with in-house labs, IoT-enabled batch plants, and regulatory teams are best placed to capture share in the fiber reinforced concrete market.

Fiber Reinforced Concrete Industry Leaders

Bekaert

BASF

HOLCIM

Heidelberg Materials

Forta Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bekaert launched Dramix Loop, a sustainable steel fiber designed for concrete reinforcement, produced using recycled end-of-life tire cords. This 100% circular product offered a near-zero carbon footprint and delivered high tensile strength, making it suitable for industrial flooring and precast applications.

- February 2025: Owens Corning signed a definitive agreement to sell its global glass fiber reinforcements business to the India-based Praana Group for USD 755 million in cash. The transaction allowed Owens Corning to focus on its building products operations in North America and Europe.

Global Fiber Reinforced Concrete Market Report Scope

Fiber reinforced concrete is a composite material composed of cement, aggregate, and short, randomly oriented fibers (steel, synthetic, glass, or natural). These fibers enhance tensile strength, ductility, and crack control. Fiber reinforced concrete reduces shrinkage, improves impact resistance, and provides post-crack durability. It is commonly used in pavements, shotcrete, and structural applications, either to complement or replace traditional rebar.

The fiber reinforced concrete market is segmented by product type, end-use sector, and geography. By product type, the market is segmented into steel fiber, natural fiber, synthetic fiber, glass fiber, and other product types. By end-use sector, the market is segmented into infrastructure, commercial, industrial and institutional, and residential. The report also covers the market size and forecasts for fiber reinforced concrete in 20 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (cubic meters).

| Steel Fiber |

| Natural Fiber |

| Synthetic Fiber |

| Glass Fiber |

| Other Product Types |

| Infrastructure |

| Commercial |

| Industrial and Institutional |

| Residential |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Product Type | Steel Fiber | |

| Natural Fiber | ||

| Synthetic Fiber | ||

| Glass Fiber | ||

| Other Product Types | ||

| By End-use Sector | Infrastructure | |

| Commercial | ||

| Industrial and Institutional | ||

| Residential | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Market Definition

- End-use Sector - Fiber reinforced concrete consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- Product/Application - Under the scope of the study, the consumption of fiber-reinforced concrete based on natural fiber, synthetic fiber, glass fiber, steel fiber, and other types are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms