Fiber Optic Gyroscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

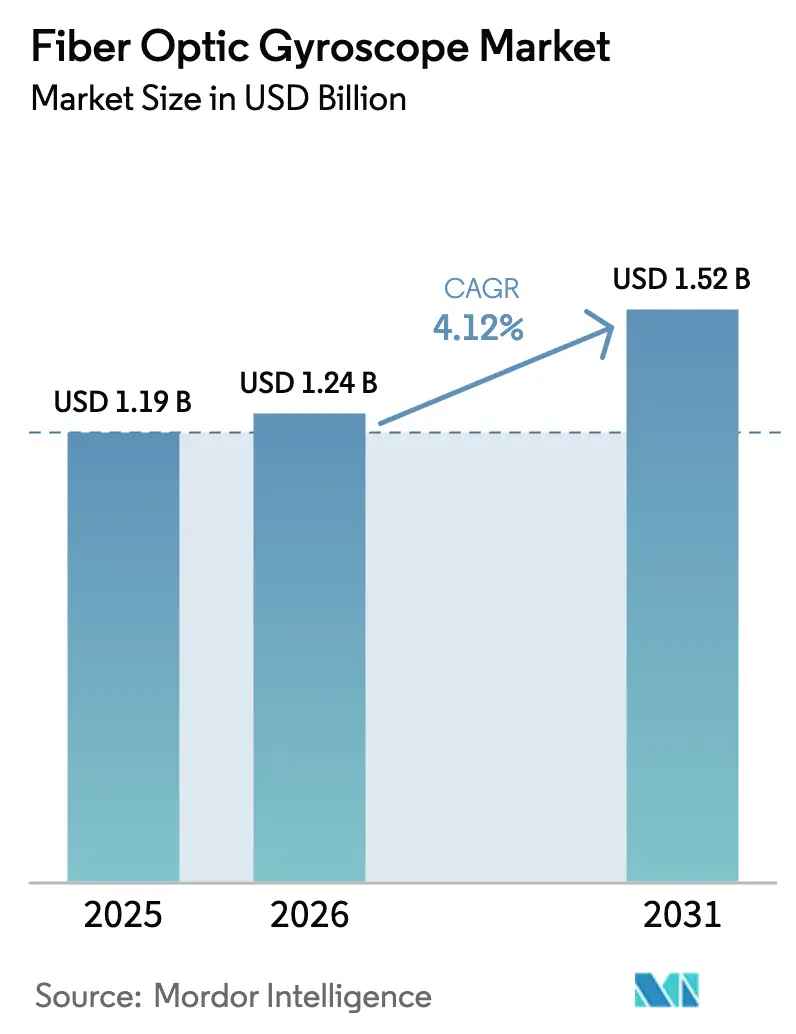

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

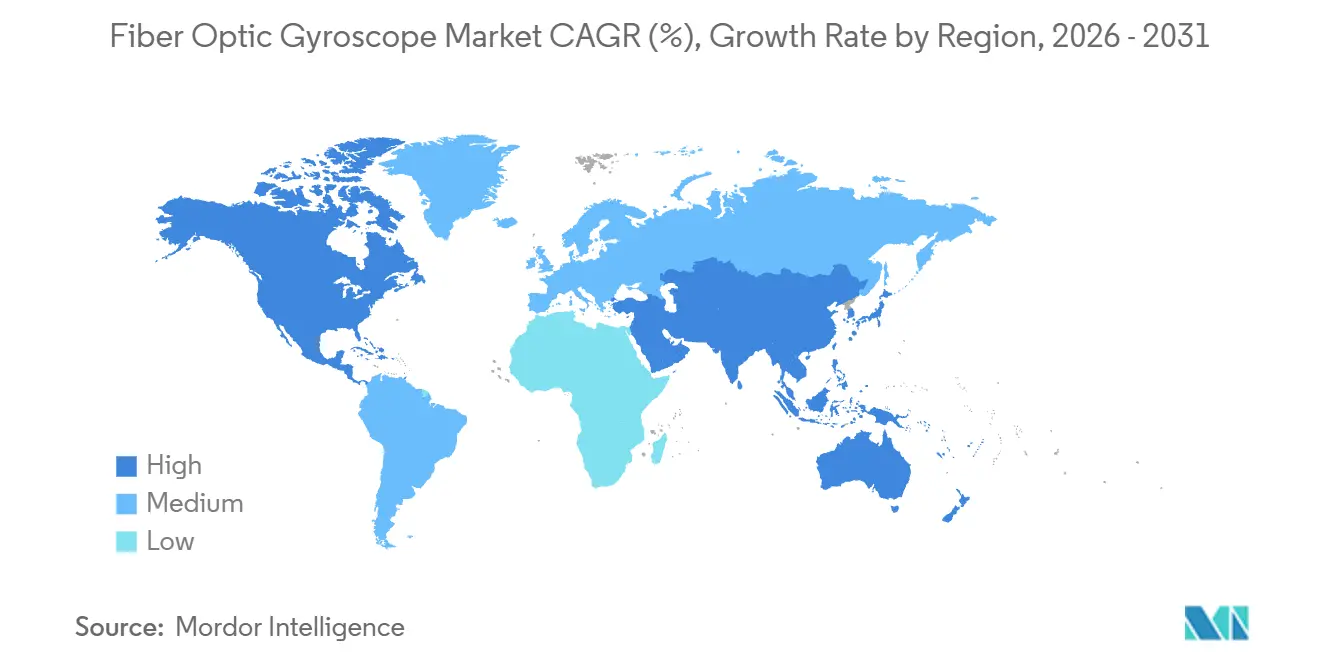

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

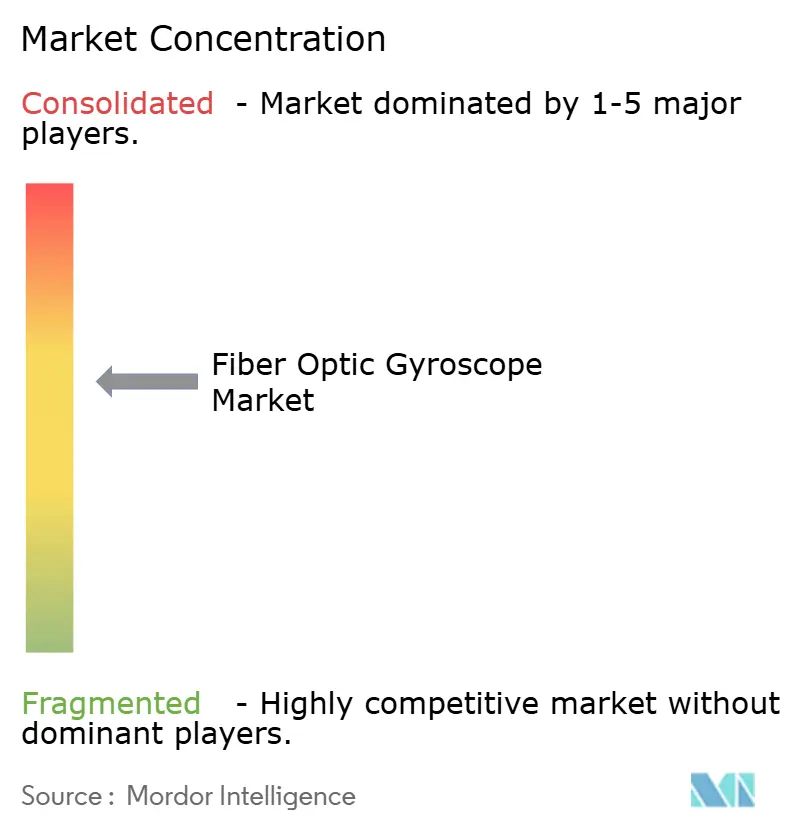

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Optic Gyroscope Market Analysis by Mordor Intelligence

The Fiber Optic Gyroscope Market size was valued at USD 1.19 billion in 2025 and is estimated to grow from USD 1.24 billion in 2026 to reach USD 1.52 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). Steady defense spending, e-navigation mandates in Europe, and high-temperature drilling projects in the Middle East anchor demand even as lower-cost MEMS gyros squeeze entry-level designs. Procurement of autonomous NATO platforms sustains baseline volume, while silicon-photonics FOGs priced up to 70% below legacy units open new commercial niches. Supply risk around lithium-niobate modulators and polarization-maintaining fiber continues to influence purchasing decisions, and ongoing yield volatility in fiber-coil winding drives price swings that favor vertically integrated vendors. Despite cost pressure, customers that operate in GPS-denied environments or extreme temperatures continue to choose closed-loop FOGs for their unrivaled bias stability.

Key Report Takeaways

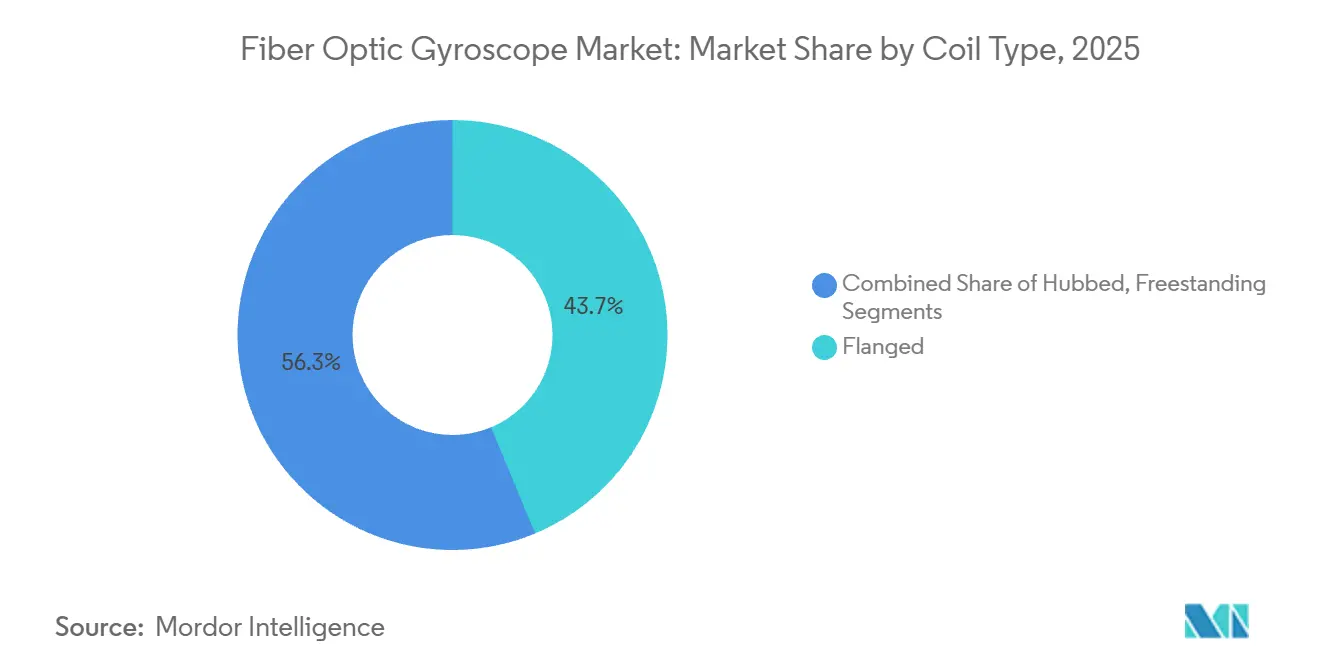

- By coil type, flanged coil designs led with 43.72% revenue share in 2025, while freestanding coils are projected to expand at a 5.72% CAGR to 2031.

- By sensing axis, three-axis systems commanded 51.63% share in 2025 and two-axis units are forecast to grow at 6.13% CAGR through 2031.

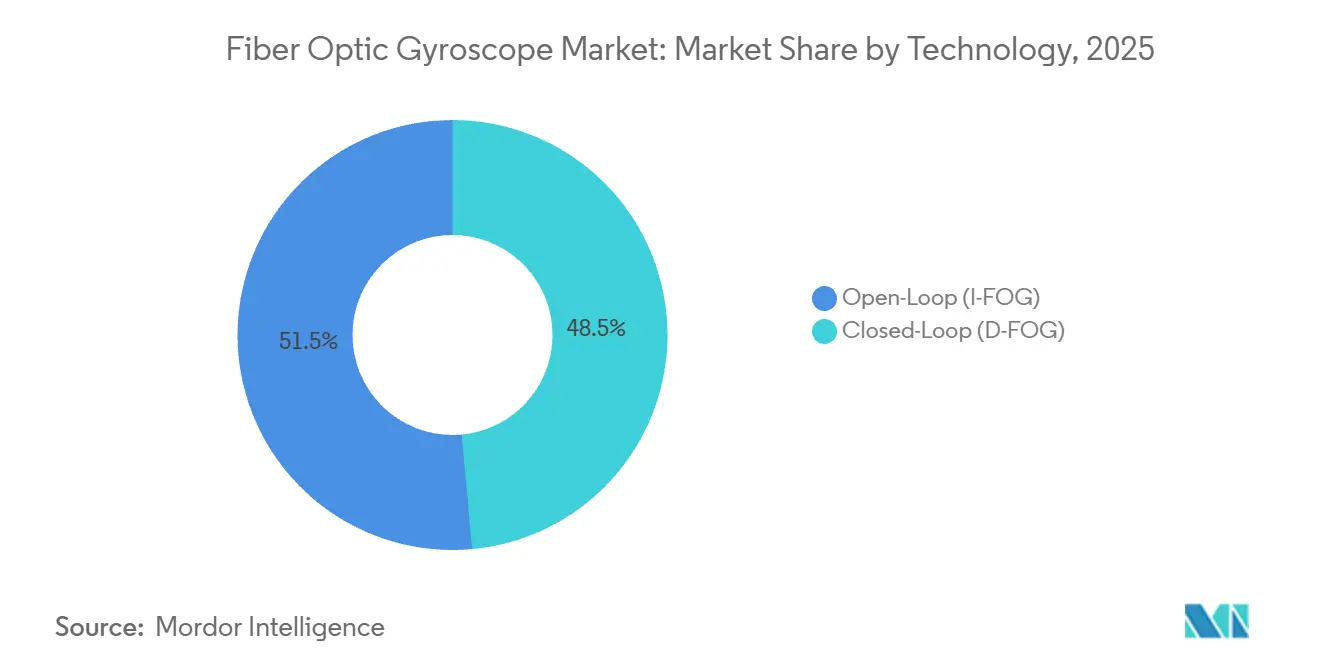

- By technology, closed-loop architectures captured 48.54% share in 2025; open-loop variants are expected to advance at 5.31% CAGR to 2031.

- By device, IMUs accounted for 37.51% share in 2025, whereas AHRS is set to grow at 6.14% CAGR over the same horizon.

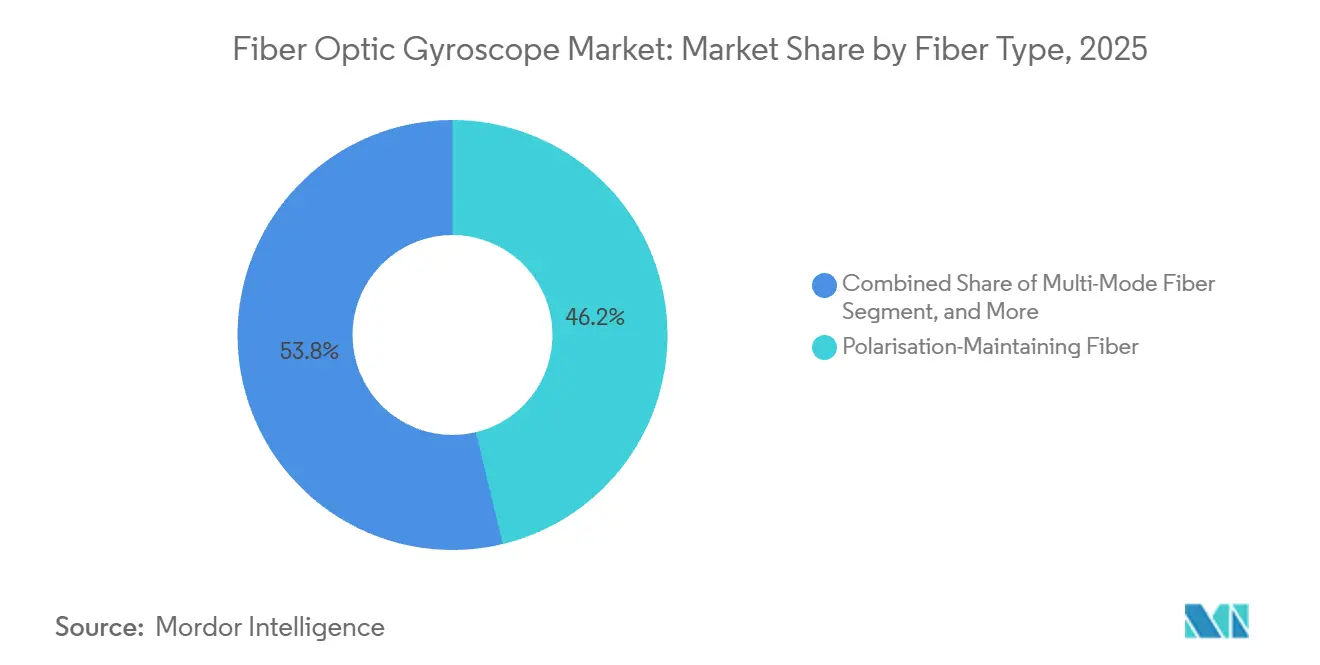

- By fiber type, polarization-maintaining fiber held 46.24% share in 2025, with multi-mode fiber poised for 5.91% CAGR through 2031.

- By end-user, defense applications represented 54.12% share in 2025, while robotics and industrial automation are projected to climb at a 6.02% CAGR toward 2031.

- By geography, North America held 32.19% share in 2025; Asia Pacific is projected to post a 6.17% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fiber Optic Gyroscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Procurement of Autonomous UAVs and UGVs by NATO Allies | +0.8% | North America and Europe, spillover to NATO partner states | Medium term (2-4 years) |

| Mandatory INS-Grade Navigation for IMO E-Navigation Compliance in Europe | +0.6% | Europe, with adoption spreading to Asia Pacific and Middle East maritime hubs | Medium term (2-4 years) |

| Oil-and-Gas Downhole Drilling Efficiency Gains in Middle East, Demanding High-Temp FOGs | +0.5% | Middle East core, expansion to North America shale and offshore Africa | Short term (≤ 2 years) |

| Electrification of Rail Signalling in Asia Driving Track Geometry Cars with FOG IMUs | +0.4% | Asia Pacific, particularly China, India, Japan, South Korea | Medium term (2-4 years) |

| Surge in Space-Launch Constellations Requiring Radiation-Hard FOGs | +0.3% | Global, led by United States, China, Europe | Long term (≥ 4 years) |

| Robotics Fulfilment Centres Growth in Developed Economies | +0.3% | North America and Europe, early adoption in Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Procurement of Autonomous UAVs and UGVs by NATO Allies

Defense ministries across NATO have placed unmanned systems at the center of modernization strategies, and each tender now specifies INS-grade navigation with bias stability below 0.01 °/hr. The United States Embedded GPS/INS program, valued at USD 3.5 billion, is a bellwether that locks fiber optic gyroscope market vendors into multi-year delivery schedules. In Europe, a GBP 20.5 million (USD 27.39 Million) award to Northrop Grumman for Royal Navy minehunters underscores similar requirements. These contracts exclude consumer-grade MEMS sensors and sustain high-margin closed-loop FOG demand. Beyond headline orders, joint exercises reveal that ground robots operating in tunnels lose MEMS heading within minutes, whereas FOGs maintain accuracy for hours, reinforcing adoption momentum.

Mandatory INS-Grade Navigation for IMO E-Navigation Compliance in Europe

MSC.467(101) obliges vessels above 500 GT to carry navigation-grade INS by 2027, and about

12,000 European hulls still need upgrades.[1] Exail Group, “MARINS and PHINS Inertial Navigation Systems,” exail.com Commercial shipping operators now retrofit the same MARINS and PHINS FOG systems already proven on naval fleets, curbing certification risk. Singapore’s intent to mirror the regulation broadens the addressable fleet, pushing the fiber optic gyroscope market into Asia Pacific maritime hubs. Retrofit windows are tight, so integrators pre-order coils and modulators, creating a near-term spike in component lead times that favors vertically integrated European suppliers.

Oil-and-Gas Downhole Drilling Efficiency Gains in the Middle East

Extended-reach drilling across Saudi and Emirati reservoirs now exceeds bottom-hole temperatures of 165 °C, well beyond MEMS gyro limits. Field trials with Schlumberger Omega and GyroSphere assemblies cut sidetrack costs by 18% and improved azimuth to 0.1 °, metrics that operators now use as procurement thresholds. Similar performance expectations migrate to North American shale pads, raising global demand for high-temperature coils. As a result, the fiber optic gyroscope market enjoys insulation from crude-price volatility because precision steering directly lifts recovery rates.

Electrification of Rail Signaling in Asia Driving Track-Geometry Cars with FOG IMUs

China’s USD 16.5 billion rail-electrification push mandates millimeter-level track profiling, and FOG IMUs outperform MEMS gyros above 50 Hz vibration bands critical for corrugation detection. Japan, India, and South Korea enforce similar geometry audits for high-speed corridors, locking in multi-axis FOG demand through 2030. Suppliers leverage volume contracts for 200-plus geometry cars to stabilize coil-production runs, lowering unit cost enough to fend off lower-grade MEMS alternatives in this niche.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short-Cycle Design Wins of MEMS Gyros in Mini Drones (Less than 5 kg) | -0.5% | Global, particularly Asia Pacific and North America consumer UAV markets | Short term (≤ 2 years) |

| Fiber Coil Winding Yield Loss Above 8% Raising ASP Volatility | -0.4% | Global, affecting all FOG manufacturers | Medium term (2-4 years) |

| Export-Control Lead-Times for Polarization-Maintaining Fiber (More than 90 days) | -0.3% | Emerging markets in Southeast Asia, Latin America, Africa | Medium term (2-4 years) |

| Limited Indigenous Lithium-Niobate Modulator Supply in Emerging Economies | -0.3% | Asia Pacific (excluding Japan), Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short-Cycle Design Wins of MEMS Gyros in Mini Drones

Sub-5 kg drones ship within 12-week design cycles, and MEMS gyros priced below USD 50 meet their looser bias targets. DJI’s 2025 product line owns three-quarters of the consumer-drone segment without a single FOG channel, and its scale anchors the supply chain around MEMS. Because mini drones represent the highest unit volumes in aerial robotics, FOG suppliers accept that this tranche remains out of reach for the fiber optic gyroscope market through the forecast window.

Fiber Coil Winding Yield Loss Above 8% Raising ASP Volatility

Manual coil winding introduces splice loss, epoxy contamination, and breakage during thermal cycling, driving scrap rates above 8% at many plants. KVH Industries reported a three-point margin swing tied solely to incremental yield gains. Price-sensitive customers feel volatility when vendors roll scrap costs into quarterly ASPs, disrupting long-term budgeting. Automation programs such as Advanced Navigation’s photonic-chip pathway promise 95% yields, yet equipment capital outlays delay broad deployment, keeping yield risk on the table for most mid-tier firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coil Type: Flanged Designs Maintain the Lead but Weight-Sensitive Platforms Eye Freestanding Alternatives

Flanged coils held an undisputed 43.72% share in 2025, testifying to their ruggedness in missile and naval environments that impose shocks above 20 g RMS. Bias stability consistently remains inside 0.01 °/hr during launch events, a benchmark no freestanding design has replicated at scale. Defense primes therefore keep flanged units on legacy qualified parts lists, and replacement cycles alone safeguard a sizable slice of the fiber optic gyroscope market. Nevertheless, rocket-launch providers and small-sat builders weigh every gram, and freestanding coils shave up to 30% of assembly mass, an advantage that translates directly into payload margin. As a result, freestanding coils are projected to outpace the overall market with a 5.72% CAGR to 2031, particularly inside satellite ADCS modules and long-endurance UAVs.

In space, Redwire Space specifies freestanding FOGs below 500 g per axis for CubeSat buses, while in defense aviation the Eurofighter Typhoon retains its flanged Northrop Grumman LCR-100 for qualification ease. Hubbed coils sit between the two extremes, offering moderate vibration tolerance at competitive price points, which resonates with Asian rail integrators. Should hollow-core fiber coils prove manufacturable, weight and thermal advantages might redefine design choices, yet commercial readiness sits beyond the current forecast horizon.

By Sensing Axis: Three-Axis Units Dominate, Dual-Axis Configurations Gain Momentum in Cost-Sensitive Marine Projects

The three-axis architecture captured 51.63% of 2025 revenue thanks to 6-DOF navigation requirements in autonomous vehicles, guided missiles, and warehouse robots. Folding all axes into one enclosure slashes cabling, simplifies thermal management, and enables Kalman filtering on a shared processor, lowering total system error. Two-axis FOGs, while behind on share, benefit from segment needs where heave or vertical rate carries less weight, such as in hull-mounted sonar stabilization. With a 6.13% CAGR projection, dual-axis models will see the fastest pickup through 2031, especially on offshore support vessels adopting remote operation. Single-axis gyros linger in retrofit headings where compartment space is tight, yet their limited scope means secular decline across the fiber optic gyroscope market.

Automotive pilot fleets in Munich and Phoenix already embed three-axis FOGs alongside lidar and radar stacks, reporting drift under 10 cm across two-hour autonomy loops. Conversely, navies often keep standalone azimuth gyros as backup in case integrated INS units suffer electronic compromise. This redundancy explains why niche single-axis demand endures even though unit cost remains high relative to dual-axis alternatives.

By Technology: Closed-Loop (D-FOG) Retains the Premium Segment while Open-Loop (I-FOG) Expands Commercial Footprint

Closed-loop systems held 48.54% share in 2025 on the back of sub-0.01 °/hr bias stability that missile, submarine, and high-orbit satellite customers can monetize. The closing feedback nulls Sagnac phase shifts in real time, flattening scale-factor nonlinearities and extending calibration intervals. Yet each closed-loop channel needs a lithium-niobate phase modulator and higher bandwidth digital signal processor, pushing bill-of-materials two-to-three times above open-loop counterparts. Consequently, price-constrained buyers, especially in autonomous delivery robots, now accept 0.1–1 °/hr drift in exchange for sub-USD 1 500 hardware. Open-loop designs are therefore forecast to compound at 5.31% through 2031, chipping away at the total fiber optic gyroscope market but leaving the high-reliability core intact.

Defense platforms like the F-35 keep closed-loop HG1120 IMUs that demonstrate 0.003 °/hr bias over 10 000 flight hours. At the other end, Guangdong Ausno’s silicon-photonics FOG family delivers open-loop performance under 0.5 °/hr at USD 500, enough for last-mile delivery vehicles in dense Chinese cities. Volume from such commercial orders allows vendors to amortize coil-winding automation, a step that paradoxically will also benefit higher-grade closed-loop lines by lowering shared overhead.

By Device: IMUs Remain Center-Stage as AHRS and INS Carve Specific Growth Paths

IMUs aggregated 37.51% of 2025 sales because six-degree-of-freedom data is non-negotiable for GPS-denied autonomy in air, sea, land, and space. Integrated accelerometers and gyros support full navigation solutions when fused with GNSS, odometry, or visual landmarks. Fiber optic gyroscope market size projections show IMUs maintaining leadership but ceding incremental share to AHRS in commercial aviation, where pilots need attitude and heading rather than full dead-reckoning. With retrofit timelines linked to 2028 airworthiness directives on aging ring-laser gyros, AHRS demand posts a 6.14% CAGR.

INS units stay relevant in submarine patrols where vessels must keep 100 m position accuracy after 30 days submerged. Gyrocompasses, although eclipsed technologically, endure in merchant shipping because international rules require a dedicated heading reference that can operate independently of power-hungry IMUs. As multipurpose FOG modules shrink to cigarette-pack form factors, OEMs begin to embed upgrade hooks that unlock INS-grade processing through software licenses, a strategy that simultaneously extends product life and elevates average selling price.

By Fiber Type: Polarization-Maintaining Fiber Tops Navigation-Grade Builds, Multi-Mode Gains in Cost-Driven Sectors

Navigation-grade FOGs need PM fiber to suppress polarization-induced bias drift to below 0.001 °/hr, and therefore PM coils owned 46.24% of 2025 volume. Robust demand from nuclear submarines, ballistic missiles, and satellite payloads guarantees base-load production. However, PM fiber sits on ITAR lists, and orders outside allied countries endure 90-day clearance, a delay that pushes emerging-market buyers toward single-mode or multi-mode alternatives. As a result, multi-mode coils track a 5.91% CAGR through 2031, especially in Asia’s low-altitude economy, where open-loop silicon-photonics FOGs balance performance and cost. Single-mode fiber offers a compromise and continues to equip offshore survey vessels where magnetic interference remains modest.

Corning supplies 60% of global PM fiber, a concentration that triggered allocation rationing during the 2024 semiconductor crunch. Vendors responded by dual-qualifying Japanese sources to limit downtime. Meanwhile, research on hollow-core photonic-crystal fiber hints at bias floors comparable with PM coils without the export licenses, setting a possible inflection point later in the decade.[2]Nature Communications, “Navigation-Grade Hollow-Core Fiber Optic Gyroscope,” nature.com

By End-User Industry: Defense Holds Majority Share, Robotics Emerges as the Fastest Riser

Defense applications absorbed 54.12% of 2025 revenue as autonomous minehunters, hypersonic missiles, and deep-space probes all specify FOG-based inertial navigation for GPS-denied missions. Even incremental purchases such as the Royal Navy retrofit ripple across the fiber optic gyroscope market share among specialized suppliers. Looking forward, robotics and industrial automation exhibit a 6.02% CAGR as e-commerce warehouses deploy tens of thousands of autonomous mobile robots requiring centimeter-level indoor positioning. Furniture-friendly form factors and steady unit pricing below USD 3 000 remove the last barriers to mass adoption in this vertical.

Aerospace remains steady, buoyed by AHRS retrofits on legacy fleets. Oilfield service firms invest when crude prices support complex deviated wells, keeping that sector cyclical yet lucrative. Rail electrification, maritime hydrography, and automotive autonomy each claim unique niches where MEMS drift proves unacceptable, preserving diverse growth corridors within the broader fiber optic gyroscope industry.

Geography Analysis

North America retained the largest fiber optic gyroscope market share at 32.19% in 2025, underpinned by multi-year United States Department of Defense production awards for Embedded GPS-INS units and satellite-constellation payloads. Early adoption of autonomous ground vehicles for logistics missions and a steady flow of retrofit contracts for legacy aircraft further anchor demand, while Canada’s Arctic-focused naval modernization and Mexico’s growing aerospace cluster add incremental volume. Recent quantum-sensor research grants awarded to Honeywell’s Arizona plant hint at a long-term shift toward next-generation gyros, yet commercial deployment remains outside the current forecast window. Together, these factors keep the North American fiber optic gyroscope market size on a stable growth path through 2031.

Europe followed with roughly 28% of 2025 revenue, buoyed by International Maritime Organization e-navigation rules that force 12,000 commercial vessels to install INS-grade sensors by 2027. Rail modernization programs in Germany, France, and Spain rely on track-geometry cars equipped with FOG-based IMUs to maintain 250 km/h service, creating recurring coil orders for regional suppliers. Defense spending also supports volume; the United Kingdom’s GBP 20.5 million (USD 27.39 Million) contract for Royal Navy minehunters locks in closed-loop units through 2027. Export restrictions limit Russian participation, but Safran and Exail capture regional share by leveraging ITAR-free supply chains.

Asia Pacific is forecast to post the fastest expansion at a 6.17% CAGR from 2026 to 2031, driven by China’s silicon-photonics vendors that price FOGs up to 70% below Western equivalents. Japan’s Cabinet Office Space Technology Strategy accelerates satellite builds that need radiation-hardened FOGs, while India’s Defense Research and Development Organisation funds domestic programs for fighter aircraft and submarines. Electrification of 15 000 km of Chinese regional rail lines and large track-monitoring orders in India and South Korea broaden industrial uptake. Elsewhere, Saudi Aramco’s high-temperature drilling campaigns and emerging UAV procurements in the United Arab Emirates lift Middle East volumes, whereas Brazil’s aerospace and offshore sectors provide a foothold in South America. Collectively, these developments diversify the regional demand base and temper supply-chain risk for global vendors.

Regulatory Landscape

Export controls and qualification standards remain the primary regulatory anchors for navigation-grade fiber optic gyroscopes (FOGs). In the United States, high-precision inertial sensors for defense and space programs are shaped by ITAR/EAR pathways, and the U.S. Department of State issued a final rule updating ITAR and targeted USML revisions in August 2025, effective September 15, 2025. This affects licensing lead times and product configurations for global deliveries.

In China, civil and military standardization frameworks define test and performance requirements for domestic aerospace and defense adoption. GB/T 45570-2025 (effective August 1, 2025) sets general technical requirements for optical gyroscopes, while military standards such as GJB 8898-2017 and GJB 10100-2021 specify aerospace-oriented requirements including EMC and vibration testing. China also issued GB/T 47121-2026 for optical gyro angle sensor (goniometer) technical requirements. Alongside these frameworks, vendor positioning around exportability continues to matter, including EMCOREs non-ITAR classification for its TAC-450-340/360 Photonic IMU (released in March 2026).

Value Chain Analysis

The fiber optic gyroscope value chain starts with specialty materials and photonic components, notably polarization-maintaining (PM) fiber, lithium niobate (LiNbO3) integrated optical circuits (IOCs) or phase modulators, broadband light sources, photodetectors, and precision analog and digital electronics. These inputs feed coil winding, optical assembly and packaging (including splicing, epoxy processes, and thermal management), followed by calibration and environmental qualification (particularly for aerospace and defense programs with 18-36 month cycles). The end product is shipped either as stand-alone gyros or embedded into IMUs, INS, gyrocompasses, and AHRS units sold through OEMs and prime contractors.

Bottlenecks cluster around PM fiber availability, concentrated among a limited set of suppliers across the United States, Japan, and Europe, along with LiNbO3 IOC yield and repeatability in high-volume coil winding and cure processes. To address this, the chain is shifting toward automation and semiconductor-style manufacturing approaches, including silicon photonics and heterogeneous integration to reduce splicing and improve manufacturability. YOEC highlighted ongoing work on fully automatic coil winding machines (March 2026) aimed at scaling integrated FOG production and reducing manual-intervention constraints. These moves align with broader industry efforts toward vertical integration and dual-sourcing to reduce exposure to export controls and single-source photonic component risk.

Competitive Landscape

The global market remains moderately concentrated, with the top five players, Honeywell, Safran, Northrop Grumman LITEF, Exail, and KVH, collectively controlling about 70% of navigation-grade revenue through vertically integrated fiber-winding, modulator fabrication, and in-house calibration facilities. Their long histories of qualification for defense and space platforms create high switching costs for prime contractors, preserving premium pricing even during semiconductor shortages.

Second-tier challengers are expanding aggressively. Guangdong Ausno and Zhuzhou Fisrock now ship silicon-photonics FOGs at unit prices under USD 500, targeting autonomous delivery vehicles and low-altitude urban air mobility, segments where strict ITAR rules limit Western vendor reach. Advanced Navigation’s October 2025 acquisition of VAI Photonics brings photonic-chip design in-house and aims to raise coil yields to 95%, a move expected to lower manufacturing cost by 30% and strengthen its position in the commercial robotics channel. VIAVI’s January 2025 purchase of Inertial Labs for USD 150 million folds FOG and MEMS sensors into a 5G test-equipment portfolio, signaling that optical-network specialists see inertial technology as a strategic adjacency.

Innovation pipelines continue to widen the moat. Honeywell demonstrated a hybrid quantum-enhanced FOG with drift below 0.1 m per hour during a 24-hour mission in 2025, setting a new performance bar for space vehicles that operate in deep-space radiation belts.[3]Honeywell Aerospace, “HG1120 IMU and EGI Navigation Systems,” honeywell.com Concurrently, Jinan University showed a hollow-core fiber optic gyroscope that cuts Kerr-effect nonlinearity and delivers 0.0017 °/hr bias, 30 times better than conventional solid-core coils, although commercialization lies beyond 2030. These R&D trajectories suggest that while price competition intensifies at the low end, breakthrough performance at the top end reinforces the incumbents’ grip on the high-reliability slice of the fiber optic gyroscope market.

Fiber Optic Gyroscope Industry Leaders

Honeywell International Inc.

Safran S.A.

KVH Industries Inc.

EMCORE Corporation

Exail Group (iXblue SAS)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Maritime compliance and GNSS-denied operations create a clear whitespace for inertial upgrades where certification and operational risk favor proven FOG-based navigation. Europe is working through IMO e-navigation compliance timelines, with MSC.467(101) obliging vessels above 500 GT to carry navigation-grade INS by 2027 and about 12,000 European hulls still needing upgrades. This concentrates near-term retrofit activity around integrated INS/gyrocompass solutions that rely on FOG performance and supplier qualification history.

A second opportunity track is cost and size reduction through photonic integration, which extends adoption beyond traditional defense and space programs into commercial robotics, marine autonomy, and industrial platforms that cannot tolerate MEMS drift but remain price sensitive. In 2026, multiple navigation-relevant demonstrations highlighted this integration direction, including a silicon photonic integrated circuit based FOG (MDPI Photonics, June 2026) and an FPGA-based gain-controlled closed-loop interferometric FOG using a silicon multi-function integrated optical circuit (Optics Letters, July 2026). On the supply side, demand for high-purity PM fiber and high-yield LiNbO3 photonic components remains a gating factor, reinforcing opportunities for suppliers and vertically integrated manufacturers that can stabilize coil yield, component access, and exportability, including non-ITAR positioned product lines.

Recent Industry Developments

- July 2026: Thales Group announced the acquisition of a 35.51% controlling stake in Exail Technologies, valuing Exail at about USD 4.45 billion. The acquisition strengthens Thales presence in inertial navigation and maritime drone systems where FOG-based solutions are a key enabling subsystem. It also tightens a European supply chain around a major FOG and INS provider, influencing competitive dynamics for naval and autonomous platform programs.

- June 2026: Exail introduced Advans Vega SL, an inertial navigation system using FOG technology designed for GNSS-denied amphibious operations. The system extends Exails portfolio toward rapidly deployable and harsh-environment use cases where users prioritize self-contained navigation over GNSS dependence. It also reinforces the shift of FOG deployments from fixed platforms into agile fielded systems and multi-domain operations.

- October 2025: EMCORE Corporation launched the TAC-DSP-1750, a re-engineered tactical-grade fiber optic gyroscope built around photonic integrated chip technology. By refreshing a tactical FOG platform with a modernized architecture, EMCORE targeted performance, manufacturability, and program continuity for defense and inertial integrator customers. The product also supports broader positioning around exportability and supply chain control in tactical navigation builds.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the fiber optic gyroscope market covers the revenue generated from fiber optic gyros sold as standalone units or embedded inside inertial navigation related devices used for positioning, stabilization, and guidance across civil and defense use cases.

Scope exclusions: We exclude non-FOG gyro technologies (such as MEMS and ring laser gyros), lab-only prototypes, and aftermarket repair-only services.

Segmentation Overview

- By Coil Type

- Flanged

- Hubbed

- Freestanding

- By Sensing Axis

- 1-Axis

- 2-Axis

- 3-Axis

- By Technology (Interferometric)

- Open-Loop (I-FOG)

- Closed-Loop (D-FOG)

- By Device

- Gyrocompass

- Inertial Measurement Unit (IMU)

- Inertial Navigation System (INS)

- Attitude and Heading Reference System (AHRS)

- By Fiber Type

- Single-Mode Fiber

- Multi-Mode Fiber

- Polarisation-Maintaining Fiber

- By End-User Industry

- Defense, Land/Naval/Air, Missile and Space

- Aerospace and Commercial Aviation

- Automotive and Transportation, ADAS and Autonomous, Rail

- Robotics and Industrial Automation

- Oil and Gas Exploration/Downhole

- Marine Surveying and Hydrography

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by collecting public signals to map where demand is coming from and how deployments are changing by platform and end use. For fiber optic gyros, this commonly includes aerospace and defense procurement disclosures, navigation and sensor standards references, and trade or manufacturing updates tied to optical components.

Typical non-paywalled sources include government procurement and budget portals, customs and trade statistics, standards bodies publications (such as IEEE), and technical papers from journals and conference proceedings. We also review company annual reports, investor decks, credible press coverage, and association websites that discuss inertial navigation adoption and platform upgrades. Where helpful, our analysts use paid subscriptions for company financials and intelligence, patent databases, and global contracts and tenders to cross-check timelines and keep assumptions consistent. These examples are not exhaustive, and many other sources were also reviewed for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to pressure-test the desk research assumptions, particularly where public sources do not clearly separate FOG demand from broader inertial systems. We spoke with component level experts, system integrators, and downstream users across APAC, EMEA, and the Americas. We then re-contacted select participants when responses suggested different pricing, lead-time, or qualification patterns that affect unit sales timing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 42% |

| Mid tier: 56% | Functional/Unit leaders: 31% | EMEA: 33% |

| Smaller Players: 15% | Managers: 56% | Americas: 25% |

Market-Sizing & Forecasting

The sizing model is built by first reconstructing the addressable demand pool from platform and deployment indicators, and then applying adoption and replacement rates to estimate annual unit needs that are converted to value using typical selling prices. For fiber optic gyros, the demand pool logic is informed by variables such as defense and aerospace navigation upgrades, marine navigation installs, the mix of single-axis versus multi-axis requirements, open-loop versus closed-loop adoption, and expected qualification cycles that affect shipment timing.

Once the demand pool is formed, we corroborate it with selective bottom-up approximations. This includes sampled supplier and integrator revenue checks, a few price band validations by performance class, and channel level confirmation of volume direction. When gaps appear in bottom-up inputs, for example limited disclosure on embedded FOG content inside an INS or IMU, the model uses conservative attachment-rate ranges that are validated through interviews and then tightened through cross-checks against platform build rates.

For forecasting, we typically apply scenario analysis supported by a light regression-style check, where the growth path is tested against leading drivers such as defense spending trends, aircraft and naval platform deliveries, and automation activity that can pull demand into industrial and robotics use cases. Final forecast assumptions are adjusted only after interview feedback aligns with observed lead-time, capacity, and pricing behavior.

Data Validation & Update Cycle

We validate outputs by checking consistency across multiple layers, including comparing implied unit volumes, average prices, and regional splits against independent signals and what respondents describe as feasible shipment ranges. Outliers are investigated, and when a number looks directionally right but too large or too small, the driver assumptions are revisited before sign-off.

A second analyst review is done to confirm that scope and exclusions were applied consistently across regions and end uses. Reports are refreshed annually, with interim updates when material events occur that can change demand or pricing. Before delivery, an analyst performs a fresh pass through the model and key inputs so clients receive the latest updated view.

Mordor Intelligence's Fiber Optic Gyroscope Market Estimate Compared With Other Published Estimates

Published market sizes for fiber optic gyroscopes often do not match because the scope is not identical, and the build logic behind volumes and pricing is not always visible. Differences usually come from what gets counted as a FOG sale, the treatment of embedded content inside navigation systems, and how fast pricing is assumed to move over the forecast period.

The spread also reflects choices on end-use coverage and timing. Some estimates lean heavily toward defense and aerospace demand and apply aggressive growth based on autonomy narratives, while others undercount industrial and marine installs where adoption is steadier but more fragmented. The year used, currency timing, and refresh cadence can also shift the published value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.19 B (2025) | |

| Industry Newswire A | USD 1.90 B (2025) | Uses a high-growth outlook and appears to include a broader share of inertial navigation system value as FOG-related revenue, which can inflate totals versus counting only FOG hardware content. |

| Press Release B | USD 1.10 B (2024) | Uses an earlier base year and can miss embedded FOG content inside IMUs and INS, and it may apply slower price progression across performance classes. |

Across the three figures, the main driver is whether embedded FOG content is isolated inside IMUs and INS and then priced by performance class, which keeps the total closer to shipped FOG hardware value in the market sizing approach used by Mordor Intelligence.

Key Questions Answered in the Report

How big will the fiber optic gyroscope market be by 2031?

The fiber optic gyroscope market size is projected to reach USD 1.52 billion by 2031, up from USD 1.24 billion in 2026.

Which segment leads the fiber optic gyroscope market in 2025?

Defense platforms, including land, naval, air, missile, and space applications, hold the largest slice at 54.12% of 2025 revenue and remain the dominant segment through 2026.

What is driving growth in Asia Pacific?

Indigenous silicon-photonics programs in China, Japan’s satellite constellations, and India’s localization of defense electronics push Asia Pacific to a 6.17% CAGR through 2031.

Why choose a closed-loop FOG over a MEMS gyro?

Closed-loop FOGs deliver bias stability under 0.01 °/hr, which is essential for GPS-denied operations, high-temperature drilling, and high-velocity missile maneuvers, whereas MEMS gyros drift faster and cannot survive extreme environments.

Which companies dominate high-reliability FOG supply?

Honeywell, Safran, Northrop Grumman LITEF, Exail, and KVH control about 70% of navigation-grade revenue through vertically integrated production and decades of qualification heritage.

What technology could disrupt FOGs after 2030?

Research into hollow-core fiber and quantum-enhanced gyroscopes shows potential for bias stability improvements of 10- to 100-fold, but large-scale production is unlikely before the next decade.

Page last updated on: