Acousto Optic Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

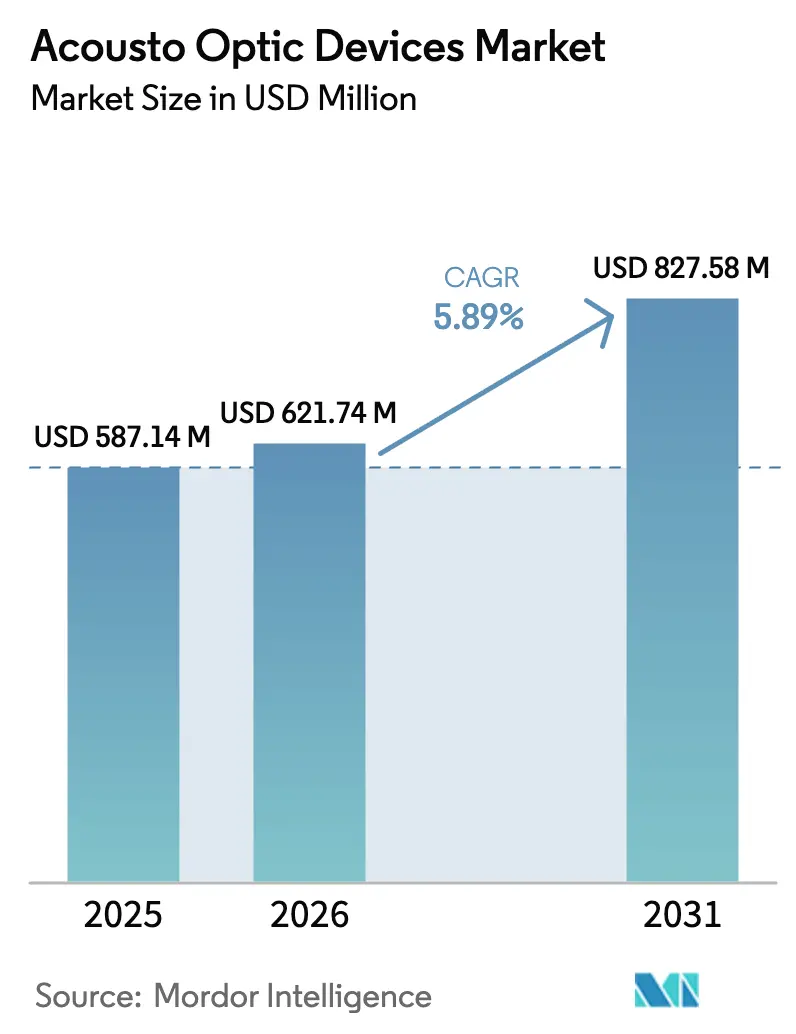

| Market Size (2026) | USD 621.74 Million |

| Market Size (2031) | USD 827.58 Million |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acousto Optic Devices Market Analysis by Mordor Intelligence

The Acousto optic devices market size was valued at USD 587.14 million in 2025 and estimated to grow from USD 621.74 million in 2026 to reach USD 827.58 million by 2031, at a CAGR of 5.89% during the forecast period (2026-2031). Growth stems from widening use of high-precision optical control inside 5G network nodes, semiconductor lithography lines, and next-generation laser systems.[1]Yajun Pang, “Intracavity Frequency Doubling Acousto-Optic Q-Switched…,” Applied Optics, osa.org Manufacturers are leveraging vertical integration to guard against material shortages and shorten lead times, while sustained RandD in tunable filters is unlocking new revenue in hyperspectral imaging and quantum photonics. Sub-micron laser machining needs, rising adoption of TeO₂-based Q-switches in medical devices, and demand for compact beam-steering solutions in aerospace are shaping competitive strategy. The acousto optic devices market is also benefiting from public-sector spending on defense-grade LiDAR and satellite-borne spectroscopy, creating fertile ground for specialized suppliers with radiation-hardened designs.

Key Report Takeaways

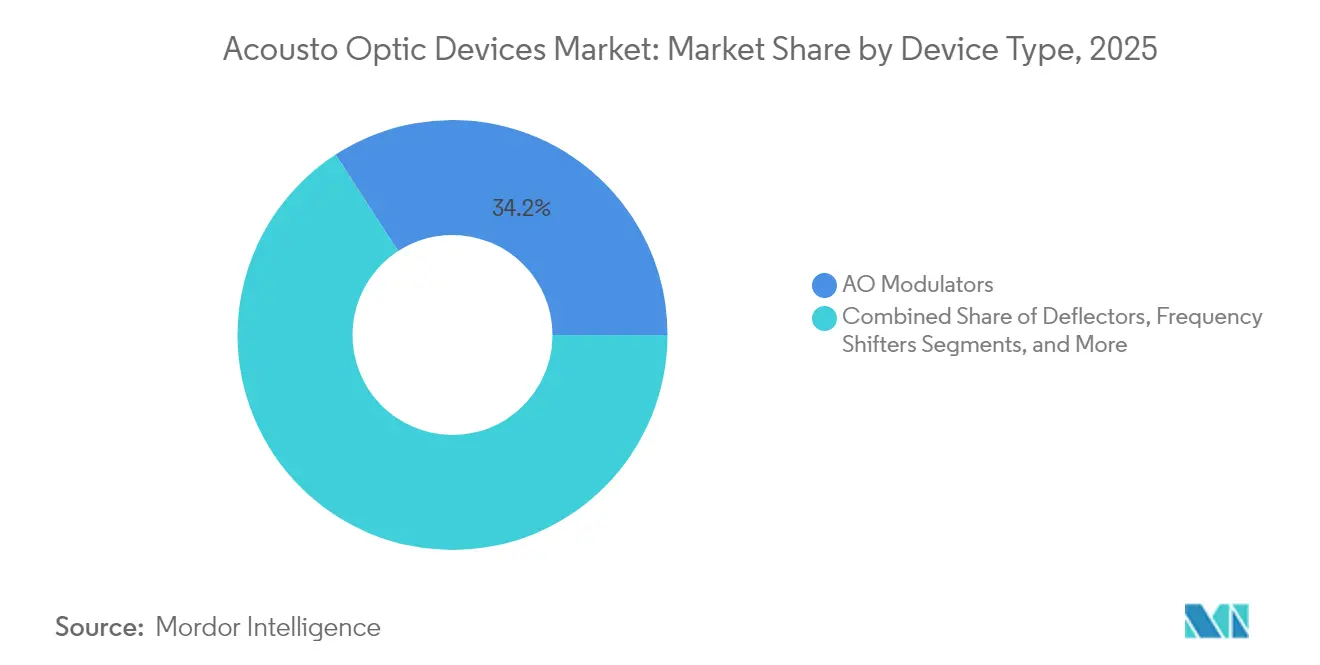

- By device type, acousto-optic modulators led with 34.15% of the acousto optic devices market share in 2025; tunable filters are advancing at the fastest 6.09% CAGR through 2031.

- By material, TeO₂ accounted for 47.92% share of the acousto optic devices market size in 2025, while lithium niobate is projected to expand at 6.57% CAGR to 2031.

- By wavelength, near-infrared devices held 39.68% of revenue in 2025; ultraviolet products are expected to grow at 6.98% CAGR.

- By reconfiguration speed, the medium-speed class (1-10 kHz) controlled 51.63% of the acousto optic devices market size in 2025, whereas >10 kHz products register the highest 6.29% CAGR.

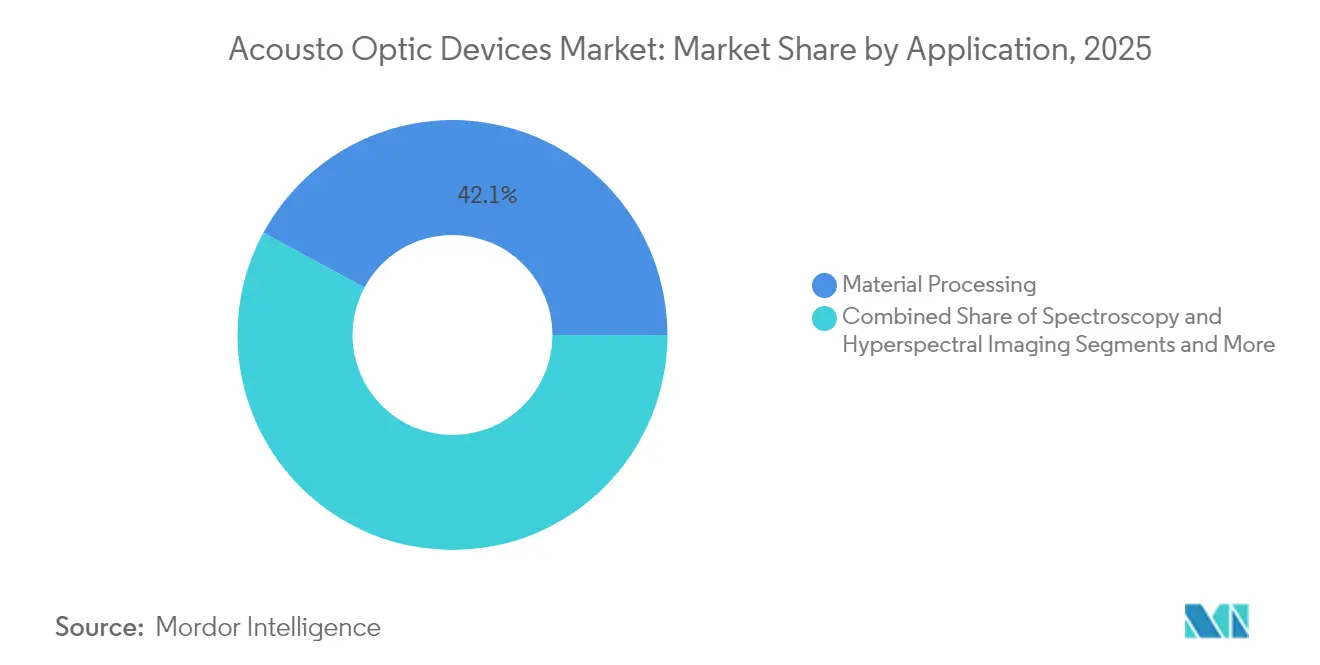

- By application, laser material processing retained 42.12% share in 2025, yet biomedical imaging posts a leading 6.48% CAGR through 2031.

- By vertical, industrial manufacturing kept 27.55% share in 2025, underpinned by heavy investment in precision machining. the acousto optic devices industry finds its fastest vertical expansion in life sciences at 6.74% CAGR through 2031.

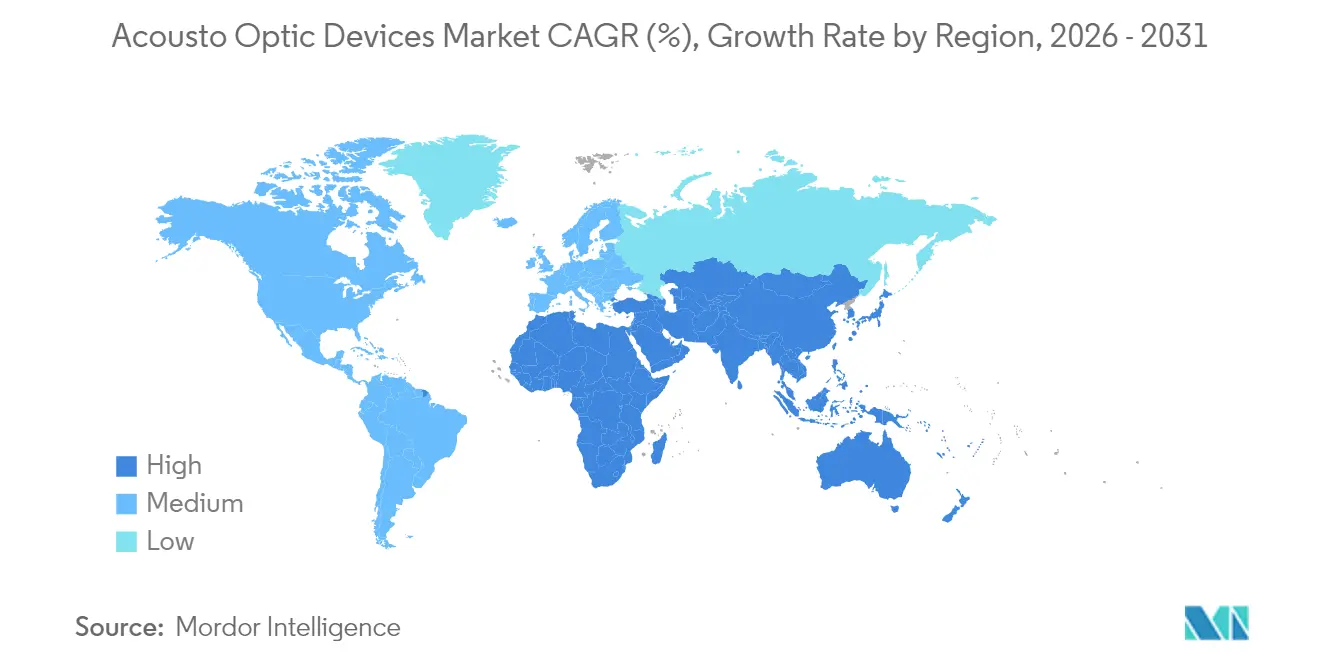

- By geography, Asia Pacific commanded 35.94% of 2025 revenue; the Middle East and Africa region is set to log the fastest 5.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acousto Optic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultrafast-laser micro-machining capacity growth in Asian fabs | +1.2% | China, South Korea, Taiwan | Medium term (2-4 years) |

| 5G/400G optical network roll-outs boosting AO modulators | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Defense-grade LiDAR for hypersonic detection | +0.7% | Germany, France, UK | Medium term (2-4 years) |

| Hyperspectral cubesats lifting space-qualified AOTFs | +0.8% | Global | Medium term (2-4 years) |

| TeO₂ Q-switch uptake in high-energy medical lasers | +0.6% | North America, Europe | Short term (≤ 2 years) |

| AO-enabled tunable sources for quantum photonics RandD | +0.5% | North America, Europe, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Ultrafast-Laser Micro-Machining Capacity in Asian Semiconductor Fabs

Surging adoption of ultrafast-laser workstations across leading Asian foundries is feeding demand for modulators and Q-switches that supply nanosecond-scale pulse gating. Chinese tool builders reported a 27% rise in TeO₂ modulator shipments during 2024 as advanced packaging lines shifted to finer redistribution layers. Sub-micron beam control delivered by acousto-optic devices enables higher yield in through-silicon-via drilling and wafer dicing, positioning the acousto optic devices market for sustained pull-through across the region.

Rapid 5G/400G Optical Network Roll-outs Driving AO Modulator Demand

North American carriers are replacing legacy 100 G links with 400 G coherent optics, a migration that requires modulators capable of high extinctions at multi-gigahertz symbol rates. Acousto-optic phase modulators offer low chirp and reliable thermal performance, making them the component of choice for new metro and long-haul builds. Data-center interconnect providers also favor AO technology to maintain signal integrity as traffic density rises, supporting incremental growth for the acousto optic devices market through 2027.

Defense-Grade LiDAR Adoption for Hypersonic Threat Detection

European integrators are field-testing solid-state LiDAR that relies on TeO₂ acousto-optic deflectors for sub-millisecond beam steering. These devices achieve scanning rates beyond 100 kHz, outperforming mechanical gimbals while trimming weight on airborne platforms.[4] G&H, “Ultimate Control of the Laser – Acousto-Optic Beam Deflectors,” gandh.com Recent crystal-growth advances have lifted TeO₂ damage thresholds, permitting higher-power operation critical for long-range target recognition.

Growth of Hyperspectral Imaging Cubesats Fueling Space-Qualified AOTF Sales

Miniaturized satellites need filter systems that can survive launch vibration yet deliver selectable narrowband imaging once on-orbit. Radiation-hardened acousto-optic tunable filters satisfy both constraints, squeezing programmable dispersion control into packages weighing under 200 g.[2]HÜBNER Photonics, “Tunable Light Speeds Up the Search for the Perfect Qubit,” hubner-photonics.com Environmental monitoring missions now specify AO filters as standard, bolstering high-reliability revenue inside the acousto optic devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Optical-grade TeO₂ crystal shortage | -0.8% | Global, acute in Asia Pacific | Medium term (2-4 years) |

| Complex RF-driver integration above 10 kHz | -0.5% | North America, Europe | Short term (≤ 2 years) |

| Narrow thermal-management window in high-power mid-IR devices | -0.6% | Global | Medium term (2-4 years) |

| Fragmented export-control regimes for dual-use optics | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Optical-Grade Tellurium Dioxide Crystals

TeO₂ is grown as a by-product of copper smelting, linking availability to mining cycles rather than photonics demand. Slow ramp-ups in purification capacity and yield losses during crystal pull keep lead times extended and prices volatile. Device makers hedge by pursuing lithium niobate or chalcogenide glass alternatives, but such shifts often require redesigns that dilute near-term margins within the acousto optic devices market.

Complex RF-Driver Integration in Above 10 kHz Beam-Steering Systems

Fast-axis AO deflectors need synchronized RF channels with phase errors held below one degree. Building drivers that maintain sub-nanosecond timing across multi-element arrays raises bill-of-materials cost and demands scarce microwave engineering talent. Smaller OEMs face steep entry barriers, curbing supplier diversity for the highest-speed segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Modulators Anchor Revenue, Filters Accelerate

The acousto optic devices market recorded 34.15% revenue from modulators in 2025, reflecting their ubiquity in laser processing tools and optical switches. Recent designs reach 83% diffraction efficiency, boosting throughput in laser micromachining and fiber communication hubs.

AOTFs, advancing at 6.09% CAGR, benefit from the rise of hyperspectral payloads and in-vitro diagnostics where motionless wavelength selection minimizes maintenance. Deflectors, frequency shifters, and Q-switches contribute resilient demand, with Q-switches favored for medical pulses where fluence uniformity is mandatory.

By Material: TeO₂ Remains Dominant While Alternatives Gain Pace

TeO₂ delivered 47.92% of 2025 sales thanks to its superior figure-of-merit and broad transmission window, yet constrained supply pushes integrators toward substitutes. The acousto optic devices market size for lithium niobate solutions is projected to expand swiftly as thin-film deposition methods produce low-loss waveguides suitable for on-chip AO modulators.

Fused silica keeps a foothold in UV photolithography, and interest in Ge-Sb-Se chalcogenide glass is stirring after lab data showed a 270-fold gain over quartz in acousto-optic response.

By Wavelength Range: Near-Infrared Leads, Ultraviolet Surges

Near-infrared hardware captured 39.68% of 2025 revenue due to telecom fiber deployment and 1 µm fiber-laser machining. Ultraviolet modules, growing fastest at 6.98% CAGR, address semiconductor patterning and biophotonics where shorter wavelengths enable finer resolution.

The acousto optic devices market share for mid-infrared cells is stable, aided by industrial gas spectroscopy, while far-infrared devices remain niche yet promising for security imaging.

By Reconfiguration Speed: Medium Class Dominates, High-Speed Climbs

Devices switching between 1 kHz and 10 kHz controlled 51.63% of spending in 2025 by balancing cost with adequate agility for coding, marking, and telecom add-drop functions.

The acousto optic devices market size attributable to >10 kHz products is poised for a 6.29% CAGR as researchers integrate 7 GHz on-chip modulators into quantum photonic circuits. Low-speed options persist in metrology setups where stability outranks rapidity.

By Application: Laser Processing Holds Top Slot, Imaging Accelerates

Laser material processing comprised 42.12% of 2025 revenue, leveraging AO modulators for tight pulse shaping in cutting, welding, and texturing lines. Biomedical imaging follows a brisk 6.48% CAGR because AO tunable filters enable multi-spectral scans inside confocal microscopes.

Optical signal processing and LiDAR represent sizable adjacent fields, while quantum photonics remains an emerging but strategically significant buyer for customized AO modules.

By Vertical: Industrial Manufacturing Leads, Life Sciences Race Ahead

Industrial manufacturing kept 27.55% share in 2025, underpinned by heavy investment in precision machining. Aerospace and defense persist as a core vertical driven by laser targeting and free-space communication.

The acousto optic devices industry finds its fastest vertical expansion in life sciences at 6.74% CAGR, tied to diagnostics advancements. Telecommunications maintains durable demand, and medical OEMs adopt AO Q-switches to refine therapeutic laser pulses.

Geography Analysis

Asia Pacific generated 35.94% of global revenue in 2025, reflecting dominant electronics production and expanded wafer-fab capacity. Policymakers channel subsidies toward domestic photonics supply chains, lifting consumption of AO components in cutting, drilling, and inspection tools. Near-term expansion of 5G backhaul links and research into quantum secure communication further cements regional leadership in the acousto optic devices market.

North America ranks second as telecom carriers densify fiber and cloud providers upgrade long-haul bandwidth. Defense contracts for directed-energy and LiDAR systems add dependable volume, while federal funding accelerates quantum photonics projects that depend on tunable AO elements. The acousto optic devices market size is reinforced by the presence of vertically integrated suppliers and university research clusters.

Europe commands a solid share built on high-precision manufacturing and medical technology adoption. Germany, the UK, and France spearhead R&D into high-speed AO deflectors for hypersonic surveillance. Regulatory support for space-based Earth-observation missions keeps demand flowing for radiation-hardened AOTFs, enriching the acousto optic devices market with specialized high-margin orders.

The Middle East and Africa hold a smaller base today yet post a leading 5.98% CAGR through 2031. National initiatives to diversify economies into photonics fabrication and 5G infrastructure create steady pipelines for AO modulators and Q-switches. Emerging research hubs in Israel and South Africa explore AO-driven spectroscopy for water and soil monitoring, adding scientific demand layers.

Value Chain Analysis

The value chain starts with upstream sourcing of optical-grade acousto-optic media (notably TeO2 and LiNbO3), RF-grade piezoelectric transducers, precision optics/coatings, and electronic components for RF drivers. A key bottleneck sits at crystal growth and finishing, where limited global suppliers and long pull and qualification cycles for high-spec material (especially UV-grade TeO2) constrain availability and extend lead times. This has reinforced vertical integration strategies by suppliers such as Gooch and Housego, Isomet, and AA Opto-Electronic to control crystal, coating, and packaging steps.

Midstream activities cover device design (acoustic wave management and thermal control), precision assembly and alignment, environmental screening, and system-level validation with laser, telecom, and aerospace and defense OEM requirements. For high-reliability applications, distribution skews toward direct-to-OEM programs and engineered-to-order deliveries rather than broadline channels, due to performance verification and traceability needs. Buyer discovery and low-volume procurement still uses specialist catalogs and directories (for example, RP Photonics buyer guides and industrial directories), but mission-critical builds typically move to direct supply agreements. Downstream demand concentrates in laser material processing tools, optical network nodes, spectroscopy and hyperspectral payloads, and defense-grade LiDAR, where co-development with system integrators increasingly bundles discrete AO devices with matched RF drivers and optical subassemblies to shorten integration cycles.

Competitive Landscape

The top five suppliers controlled roughly 60% of 2024 revenue, confirming a moderate-concentration structure. Gooch and Housego leverages vertically integrated crystal growth, coating, and packaging to secure premium contracts in aerospace and semiconductor metrology. Its US manufacturing footprint insulates customers from cross-border supply risks, an edge magnified by TeO₂ shortages.

Coherent strengthens scale economies by merging legacy II-VI crystal operations with laser subsystem expertise. Recent upgrades in TeO₂ furnace throughput help mitigate raw-material bottlenecks, ensuring sustained deliveries to high-power laser OEMs. Brimrose focuses on AOTF innovation for spectroscopy, rolling out radiation-hardened versions aimed at cubesat integrators.

Chinese challengers such as Lightcomm undercut incumbents on price for standard modulators, yet established firms keep an advantage in diffraction-efficiency consistency and low-scatter coatings. Collaboration between device vendors and quantum labs is rising, with custom chip-scale modulators co-designed to satisfy cryogenic compatibility. White-space opportunities center on integrated photonic platforms that replace discrete bulk optics; early proof-of-concepts on thin-film lithium niobate suggest new form-factor possibilities for the acousto optic devices market.

Acousto Optic Devices Industry Leaders

Gooch and Housego PLC

Brimrose Corporation of America

Isomet Corporation

Coherent Corp.

L3Harris Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is forming around integrated acousto-optics, where bulk AO components are re-implemented on platform-integrated photonic stacks to achieve smaller form factors and higher channel density. Academic demonstrations in 2026 highlighted CMOS-fabricated integrated acousto-optic phase modulation and formalized integrated acousto-optic frequency beamsplitter concepts for quantum information processing. This reinforces a pathway from discrete modulators and deflectors toward chip-scale frequency control and microwave-to-optical conversion on ferroelectric platforms such as lithium tantalate on insulator (LTOI). Integration also aligns with the report’s observed shift toward lithium-niobate-family alternatives as TeO2 supply volatility persists, supporting suppliers that can package integrated devices with RF drivers and deliver repeatable, manufacturable performance.

On the application side, hyperspectral imaging continues to provide pull-through for acousto-optic tunable filters (AOTFs) because they already deliver microsecond-scale spectral control and remove moving parts, which is useful in compact payloads and laboratory imaging. The opportunity set expands where customers need ruggedization and qualification, including radiation-hardening for space payloads, thermal management for high-power mid-IR, and high-speed synchronization above 10 kHz. These barriers constrain fast followers and favor vendors that can supply complete, validated subassemblies. With 2025 as the base year, vendors that combine material strategy (TeO2 where performance is essential and integrated ferroelectric platforms where supply chain and miniaturization matter) with co-designed RF driver ecosystems are positioned to capture spend shifting from component purchases to engineered optical control modules.

Recent Industry Developments

- June 2026: Gooch and Housego released new in-line optical modulation devices, including acousto-optic tunable filters and deflectors, aimed at precision applications such as LiDAR and quantum computing. The launches broaden its catalog beyond discrete components toward application-tailored modules, tightening its fit with OEM design-in cycles that demand validated performance and packaging.

- February 2026: Gooch and Housego announced domestic US production of thin-film lithium niobate (TFLN) wafers in Cleveland, Ohio, in collaboration with Raytheon following a US Air Force Research Laboratory contract. Establishing a local TFLN supply capability supports secure sourcing for defense-linked photonics and underpins chip-scale acousto-optic integration efforts that rely on lithium-niobate-family platforms.

- October 2024: Gooch and Housego completed the acquisition of Phoenix Optical Technologies Ltd. to strengthen its optical systems capabilities and extend its reach in aerospace and defense-oriented photonics. The move reinforced vertical integration in optics and assembly, which is strategically relevant as AO device makers work to mitigate crystal and component bottlenecks while offering higher-value subassemblies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from acousto-optic devices used to modulate, deflect, shift, or filter light using an acoustic wave, mainly inside laser and photonics setups across end users and regions.

Scope exclusions: We exclude passive optical parts that do not use acousto-optic interaction, such as standard lenses, mirrors, and beam splitters.

Segmentation Overview

- By Device Type

- Acousto-Optic Modulators

- Deflectors

- Frequency Shifters

- Q-Switches

- Tunable Filters (AOTF)

- Mode Lockers

- Pulse Pickers/Cavity Dumpers

- RF Drivers

- Other Device Types

- By Material

- Tellurium Dioxide (TeO?)

- Lithium Niobate (LiNbO?)

- Fused Silica

- Crystal Quartz

- Calcium Molybdate and Others

- By Wavelength Range

- Ultraviolet (200-400 nm)

- Visible (400-700 nm)

- Near-Infrared (700-1500 nm)

- Mid-Infrared (1500-3000 nm)

- Far-Infrared (Above 3000 nm)

- By Reconfiguration Speed

- Low (Less than 1 kHz)

- Medium (1-10 kHz)

- High (Above 10 kHz)

- By Application

- Material Processing

- Laser Macro-Processing

- Laser Micro-Processing

- Spectroscopy and Hyperspectral Imaging

- Optical Signal Processing

- Biomedical Imaging and Diagnostics

- Other Emerging (LiDAR, Quantum Photonics)

- Material Processing

- By Vertical

- Aerospace and Defense

- Telecommunications

- Semiconductor and Electronics Manufacturing

- Industrial Manufacturing

- Life Sciences and Scientific Research

- Medical

- Oil and Gas

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics (Denmark, Sweden, Norway, Finland)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Australia

- Rest of Asia-Pacific-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping where these devices are used and what typically drives demand, before we build the model. For this, we relied on public references such as trade statistics from UN Comtrade, tariff and HS classification guidance from the World Customs Organization, and macro and industry indicators from sources like the World Bank and OECD.

We also reviewed technical context and adoption signals from sources such as IEEE and SPIE conference and journal materials, plus patents from USPTO and WIPO to understand material shifts and device-function trends (for example, modulation and beam steering usage in laser tools). To ground the supplier landscape, we used company filings, investor presentations, and reputable press coverage, and we supplemented this with a paid subscription used for company financials and news tracking, plus a paid patent database for faster claim and assignee screening. These desk sources are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the sizing logic and fill gaps that desk sources do not fully explain, including how RF driver bundling is priced and how written specifications translate into shipped demand. We spoke with participants across the value chain, including component makers, photonics system integrators, distributors, and end users in laser processing, telecom and datacom labs, medical and research environments, and defense-focused programs, with coverage across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 49% |

| Mid tier: 45% | Functional/Unit leaders: 27% | EMEA: 31% |

| Smaller Players: 17% | Managers: 59% | Americas: 20% |

Market-Sizing & Forecasting

For sizing, we used top-down and bottom-up logic in a practical way. The top-down build reconstructs the demand pool from photonics and laser equipment activity, and then applies acousto-optic attach rates by use case, before revenue is derived using realistic price bands by device class.

To keep the totals anchored, selective bottom-up checks were run using sampled supplier and channel signals, along with sanity checks of typical price per unit times unit volumes for common items like modulators, deflectors, and tunable filters (including cases where RF drivers are sold as part of a kit). Where direct volume visibility was limited, gaps were handled using proxy indicators such as laser tool shipments, industrial laser installed base growth, telecom and lab instrument refresh cycles, and defense and research procurement momentum, which were then reviewed with interview feedback.

Forecasts were produced using scenario analysis supported by short-term exponential smoothing on the most stable inputs. The main drivers that were varied include industrial laser processing activity, average selling price progression by material and performance tier, adoption of beam steering in micro-processing, and regional manufacturing expansion. The results were then rechecked to ensure the implied units and pricing still look realistic.

Data Validation & Update Cycle

Outputs are validated by triangulating the model results against independent signals, and then checking whether growth patterns match what the supply chain and end users are reporting. When outliers appear, assumptions are revisited, and re-contact is triggered to confirm whether the issue is pricing, mix, or a scope interpretation.

A multi-step review is followed so that inputs, calculations, and outputs are examined by more than one analyst before sign-off. The report is refreshed annually, and interim updates are made when material events occur, such as sharp changes in photonics demand, trade restrictions, or noticeable pricing shifts. Before delivery, a fresh pass is completed to ensure clients receive the latest updated view.

Mordor Intelligence's Acousto Optic Devices Market Estimate Compared With Other Published Estimates

Published market values for acousto-optic devices can vary because each publisher draws the boundary of what counts as a device sale, and then uses different base years, pricing logic, and refresh timings. Differences also show up when one study leans more on shipment proxies, while another leans more on broad photonics revenue shares.

The table points to a clear spread in the 2024 to 2026 range, and in Mordor Intelligence's model the sizing is tied to acousto-optic device revenue and associated RF drivers only when they are sold as part of the acousto-optic device setup, rather than counting broader passive optics or unrelated photonics components. Beyond scope, the other gaps are usually caused by using aggressive CAGRs, mixing constant and current USD without clarity, and not re-validating attach rates and ASP bands with supply-side and end-user interviews when the demand cycle changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 621.74 M (2026) | |

| Global Consultancy A | USD 720.00 M (2024) | Uses an earlier base year and applies a higher growth trajectory, and the public summary does not clarify how RF drivers and adjacent photonics parts are treated in the revenue boundary. |

| Industry Publisher B | USD 523.12 M (2024) | Reports a lower 2024 value with limited disclosure on ASP construction and currency timing, and the approach appears to rely on broad segment splits without showing attach-rate checks by use case. |

Taken together, the comparison suggests that scope handling and pricing and attach-rate assumptions are the biggest reasons for differences, more than any single demand driver. By keeping the model traceable to device-level use cases, realistic price bands, and repeatable validation checks, we can explain the market total in a way that is easier to audit and update year to year.

Key Questions Answered in the Report

What is the current size of the acousto optic devices market?

The acousto optic devices market is valued at USD 621.74 million in 2026 and is projected to grow to USD 827.58 million by 2031.

Which device type holds the largest share?

Acousto-optic modulators lead with 34.15% of 2025 revenue, thanks to widespread use in laser machining and optical switching.

Why is tellurium dioxide crucial for AO components?

TeO₂ offers a high acousto-optic figure of merit and broad optical transparency, making it the preferred crystal for modulators, deflectors, and Q-switches.

Which geographic region is growing fastest?

The Middle East & Africa region shows the highest forecast CAGR at 5.98% through 2031, driven by 5G infrastructure roll-outs and emerging photonics research hubs.

How are AO devices used in quantum photonics?

Laboratories employ AO-controlled tunable lasers for rapid wavelength shifts during qubit interrogation, enabling precise manipulation of quantum states.

What is the main challenge facing high-power mid-IR AO devices?

Effective thermal management is difficult because slight temperature rises can alter beam angle and reduce diffraction efficiency, requiring complex cooling solutions.

Page last updated on: