Optical Coordinate Measuring Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

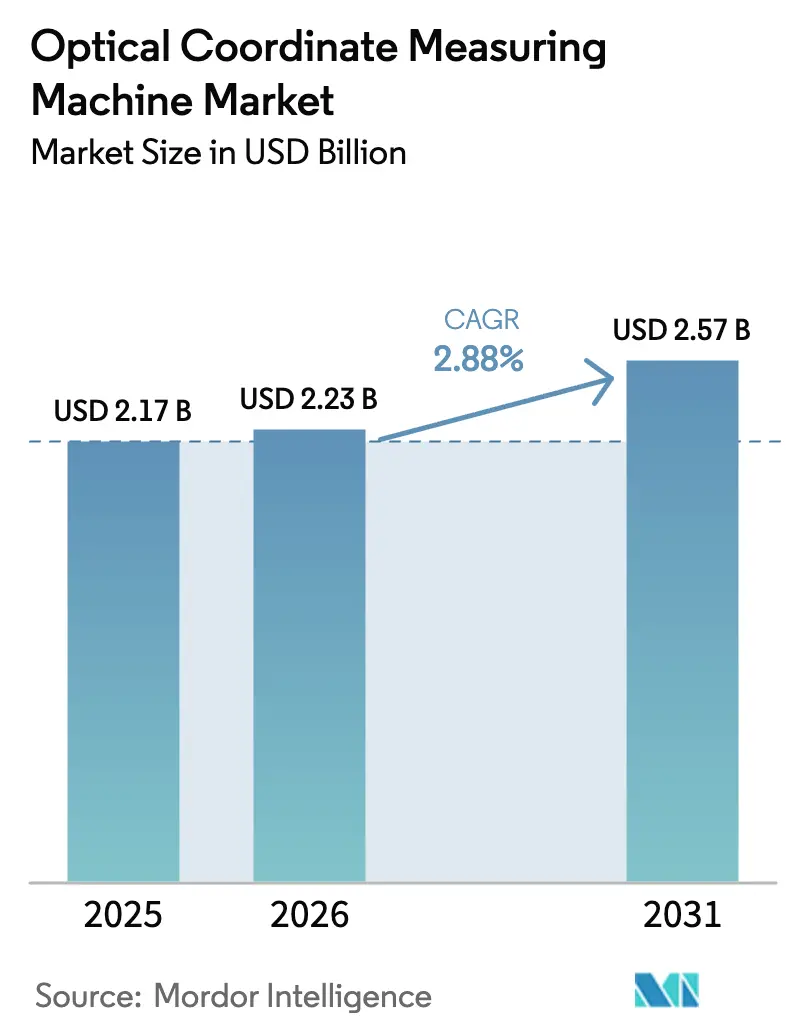

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

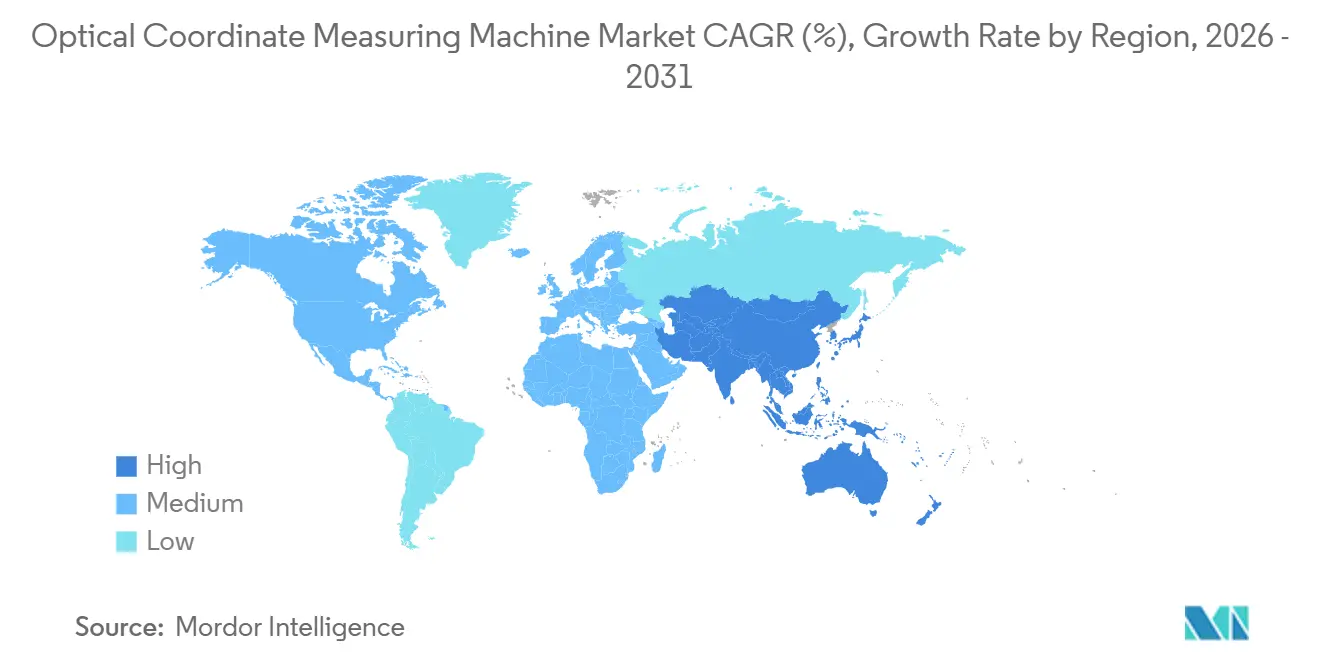

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

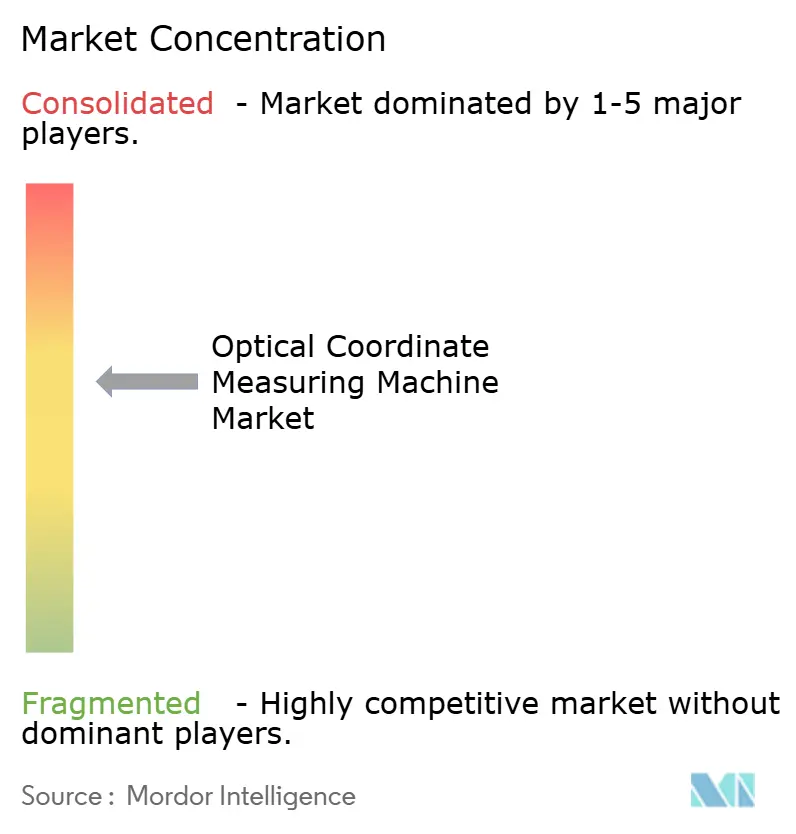

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Coordinate Measuring Machine Market Analysis by Mordor Intelligence

The optical coordinate measuring machine market size is projected to expand from USD 2.17 billion in 2025 and USD 2.23 billion in 2026 to USD 2.57 billion by 2031, registering a CAGR of 2.88% between 2026 to 2031. Continuous demand for non-contact inspection in automotive, aerospace, and semiconductor production supports this steady climb, even as capital budgets tighten in several mature manufacturing hubs. Structural shifts toward additive manufacturing, lightweight composites, and electronics miniaturization place optical systems at the center of shop-floor quality loops, because tactile probes risk surface damage or particulate contamination. Vendors are therefore emphasizing software-driven accuracy compensation and digital-twin connectivity over incremental gains in hardware rigidity, a pivot that is already visible in the rising share of subscription revenue inside the optical coordinate measuring machine market. In parallel, regional diversification is underway, Asia Pacific’s electronics boom offsets flatter conditions in North America and Europe, while small-volume benchtop systems pull new medical-device and contract-machining users into the customer base.

Key Report Takeaways

- By end-user industry, automotive applications led with 29.82% revenue share in 2025, whereas electronics and semiconductor demand is advancing at a 3.94% CAGR through 2031.

- By product type, laser-scanning platforms commanded 38.12% of the optical coordinate measuring machine market share in 2025, while structured-light systems are projected to expand at a 3.13% CAGR to 2031.

- By machine type, bridge configurations accounted for 41.53% of the optical coordinate measuring machine market size in 2025; portable benchtop units are growing the fastest at 3.47% CAGR to 2031.

- By geography, Asia Pacific captured 34.41% of 2025 revenue and is forecast to grow at 3.68% CAGR through 2031, the quickest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Optical Coordinate Measuring Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Changing Product Designs in Industry 4.0 | +0.7% | Germany, Japan, South Korea | Medium term (2–4 years) |

| Adoption of In-Line Inspection and Automation | +0.9% | North America, Europe, China | Short term (≤ 2 years) |

| Lightweight Composite Parts Require Optical Metrology | +0.5% | North America, Europe, Asia Pacific | Medium term (2–4 years) |

| High-Precision Additive Manufacturing Demand | +0.4% | Global, early aerospace and medical | Long term (≥ 4 years) |

| Regulatory Push for First-Article Inspection | +0.3% | North America, Europe | Short term (≤ 2 years) |

| AI-Driven Error-Compensation Algorithms | +0.6% | North America, Germany, Japan | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Changing Product Designs in Industry 4.0

Rapid adoption of lattice structures, multi-material castings, and stamped aluminum battery enclosures has made traditional gauges insufficient for dimensional confirmation. More than 60% of automotive tier-1 suppliers now apply optical systems to check weld-seam integrity in electric-vehicle packs, where deviations above 0.1 mm threaten IP-ratings. Aerospace primes specify non-contact scanning for composite fuselage sections, protecting delicate lamina from tool-tip deflection. Public funding echoes this shift. Horizon Europe earmarked EUR 120 million (USD 139.28 million) for advanced-metrology R&D in 2024-2025.[1]European Commission, “Horizon Europe Programme 2024-2025,” ec.europa.eu Medium-term momentum persists as serial EV production scales, although penetration slows once design iterations stabilize after 2028.

Adoption of In-Line Inspection and Automation

Manufacturers are relocating optical systems from climate-controlled labs to automated production cells, enabling 100% inspection without pausing throughput. German and Chinese body-shops now finish full body-in-white measurement in under 90 seconds, trimming rework by 40%. Collaborative-robot installations housing vision scanners jumped 18% in 2024.[2]International Federation of Robotics, “World Robotics Report 2024,” ifr.org The short-term impact is strongest where labor is expensive, but cost-optimized local solutions are accelerating adoption in Asia Pacific as well.

Lightweight Composite Parts Require Optical Metrology

Carbon-fiber and glass-fiber elements dominate new aircraft and EV battery housing designs, yet their non-isotropic surfaces deform under tactile contact. Optical systems preserve surface integrity while mapping ply orientation and thickness. In 2024, U.S. composite shipments climbed 9% to reach 1.2 million t, signaling durable demand for precision inspection. Growth should hold through mid-term horizons as aeronautics and electric mobility pursue higher structural performance.

High-Precision Additive Manufacturing Demand

Metal and polymer powder-bed fusion processes now target tolerances tighter than ±20 µm. Aerospace fuel nozzles and medical implants undergo optical checks to confirm lattice diameters and cooling channels. ASTM F42 standards revised in 2024 position optical coordinate measurement as a best practice for first-article validation. Adoption stays gradual until additive moves from prototyping toward serial runs post-2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure and TCO | -0.8% | Global SMEs | Short term (≤ 2 years) |

| Lack of Skilled Metrology Workforce | -0.5% | North America, Europe, Japan | Medium term (2–4 years) |

| Environmental Sensitivity on Shop Floor | -0.3% | Emerging markets | Short term (≤ 2 years) |

| Cyber-Security and IP-Leakage Concerns | -0.2% | Aerospace, defense, semiconductors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and TCO

Entry-level optical units start near USD 50 000, while high-end multi-sensor bridges exceed USD 500 000, and mandatory ISO 10360 reverification adds USD 5 000–15 000 per cycle.[3]National Institute of Standards and Technology, “Manufacturing Technology Survey 2024,” nist.gov Many small firms, therefore, favor tactile gauges, despite longer cycle times. Subscription bundles are emerging but remain largely confined to North America and Western Europe.

Lack of Skilled Metrology Workforce

The average U.S. quality engineer is now 52 years old and retirements outpace incoming talent. Similar gaps plague Germany and Japan. Although vendors ship AI-guided software, expert oversight is still required to interpret out-of-tolerance results, prolonging ROI for inexperienced buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Structured-Light Gains on Laser-Scanning Incumbency

Laser scanning platforms delivered 38.12% of 2025 revenue, favored for proven accuracy in body-in-white and turbine-blade checks. Conversely, structured-light systems will pace at 3.13% CAGR, prized for rapid full-field capture that compresses measurement cycles from minutes to seconds.[4]Institute of Electrical and Electronics Engineers, “Comparative Study 2024,” ieee.org Adoption is strongest in additive-manufactured components and EV battery trays, where users accept ±0.02 mm uncertainty in exchange for throughput. The optical coordinate measuring machine market responds by widening structured-light product lines, such as Nikon’s 5-MP system that achieves 0.01 mm accuracy for electronics casings.

Large-volume aerospace structures still rely on laser scanning to penetrate reflective composites and handle envelopes above 2 m. Multi-sensor hybrids now find traction in tier-1 automotive suppliers needing a single station to check aluminum castings and plastic fascias without relocating parts. Tight ISO 10360-8 conformance across technologies reassures quality managers, further propelling the optical coordinate measuring machine market toward hybrid architectures.

By Machine Type: Portable Benchtop Flexibility Challenges Bridge Stability

Bridge machines held 41.53% of 2025 takings thanks to granite-base rigidity and ±2 µm accuracy over 3 m volumes. Portable benchtop units, however, will expand 3.47% annually as factories pull measurement next to CNC centers, trimming handling time. FARO’s articulated arm revenue grew 11% in 2024 on aerospace maintenance demand. This shift underscores how the optical coordinate measuring machine market values agility over maximum precision in high-mix settings.

Bridge models remain indispensable for calibration labs and aerospace jigs that demand sub-micrometer repeatability under climate control. Yet benchtop units unlock new SME customers because floor-space needs shrink and list prices fall 40–60% below bridge equivalents. Gantry platforms stay relevant for fuselage, ship hull, and wind-blade tasks; Hexagon’s 18-m Leitz PMM-Xi line secures these outsize jobs.

By Component: Software Value-Add Outpaces Hardware Commoditization

Hardware still produced 64.43% of total receipts in 2025, yet software is growing 3.23% CAGR as measurement planning, thermal drift compensation, and cloud dashboards become primary differentiators. Keyence noted software and services contributed 38% of metrology revenue in 2024 versus 29% two years earlier. The optical coordinate measuring machine industry accordingly channels R&D toward AI algorithms that suggest probe paths and auto-classify defects, securing sticky subscription income.

Hardware margins compress where Chinese suppliers offer granite-bridge systems at steep discounts. Incumbents thus bundle proprietary software and ISO 10360 reverification into multi-year packages, smoothing revenue and defending share. Services revenue in calibration, training, and preventive maintenance further cushions hardware commoditization.

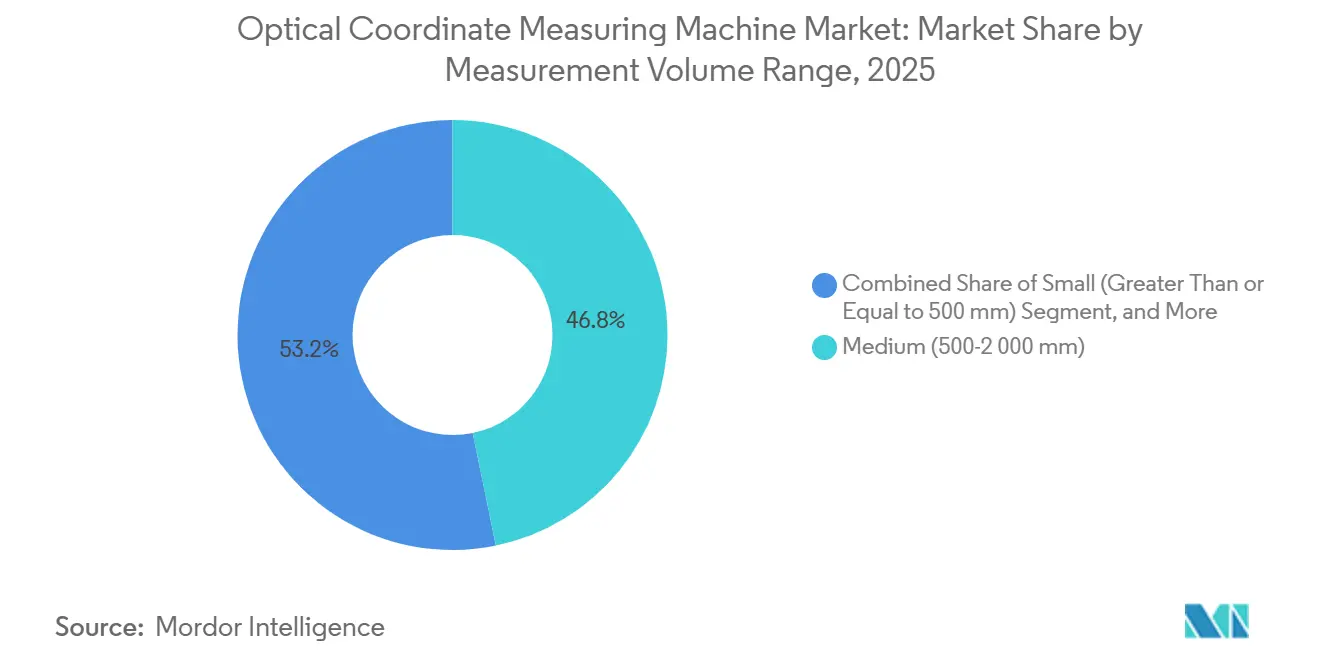

By Measurement Volume Range: Small-Part Precision Accelerates Amid Electronics Surge

Medium volumes of 500–2 000 mm took 46.77% in 2025, matching most automotive and aerospace sub-assemblies. Yet small-volume systems under 500 mm will outpace peers at 3.53% CAGR, carried by semiconductor substrates and medical implants demanding sub-10 µm accuracy. As electronics ups its share within the optical coordinate measuring machine market, benchtop form factors become entry tickets for contract-assembly lines where floor space is scarce.

Large-volume machines stay niche but indispensable for composite fuselage barrels and wind-turbine blades. Their six- or seven-figure prices restrict uptake to OEMs with specialized facilities, keeping unit volumes low even when revenue impact is high.

By End-User Industry: Electronics Outpaces Automotive Maturity

Automotive led 2025 demand at 29.82%, yet electronics will expand 3.94% per year as wafer-level optics and 3D stacking require tighter control. More than 70% of U.S. automotive suppliers still rely on pre-2020 installs, swapping systems primarily when software is no longer supported. By contrast, every semiconductor process migration resets metrology needs, propelling fresh hardware and software sales.

Aerospace and defense apply optical inspection for composite layups and stealth-panel fits, sustaining stable orders even while unit build rates fluctuate. Medical devices depend on surface-texture mapping for osseointegration, keeping this smaller vertical on a consistent upward slope within the optical coordinate measuring machine market.

Geography Analysis

Asia Pacific generated 34.41% of global sales in 2025 and will climb at 3.68% CAGR through 2031. China’s semiconductor equipment buy surged 22% in 2024 as fabs chased sub-3 nm yields that require wafer-level metrology. Japan exported 68% of domestic CMM output, leveraging elite optical know-how. South Korea’s battery and logic chip expansions pushed optical installs up 14% in 2024. India and ASEAN nations trail but rise steadily as contract-electronics manufacturing migrates from coastal China.

North America retains a stronghold in aerospace and defense. Boeing’s backlog above 14 000 jets protects baseline demand for fuselage and wing inspections. Battery-electric platforms fuel new installs in U.S. auto plants, amplified by EUR 8.2 billion EV cap-ex in Germany during 2024. Europe’s strict conformity to ISO 10360 and CE marking keeps prices high yet lock-step with premium quality requirements.

South America, the Middle East, and Africa collectively represent single-digit percentages of the optical coordinate measuring machine market. Brazil’s assembly operations adopt optical solutions inside multinational plants but domestic tier-2 firms hesitate. Gulf states fund aerospace MRO hubs, buying portable arms for on-wing turbine checks, yet volumes lag industrial peers. Africa’s 11% manufacturing share of GDP undercuts large-scale metrology investment.

Competitive Landscape

Twenty-two profiled suppliers compete, but the top three Hexagon AB, Carl Zeiss AG, and Mitutoyo Corp. hold major share of revenue through tight hardware-software coupling and multiyear service contracts. Strategy now hinges on software. Hexagon filed 17 AI error-compensation patents in 2024, and Zeiss embedded natural-language programming in CALYPSO 2025. Mitutoyo opened a 12 000 m² training center to shore up user competence and lock clients into its ecosystem.

Price pressure from Chinese bridge-CMM vendors pushes Western firms to accentuate application consulting and ISO 10360 reverification. Portable specialists like FARO grow via articulated arms suited to field service, while niche players Werth and OGP exploit multisensor fusion for aerospace first-article compliance. Consolidation remains light; the major move was Hexagon’s 2023 buy of Volume Graphics to overlay CT data onto optical scans, a step toward holistic 3D inspection.

Emerging challengers chase unmet SME needs with turnkey, subscription-priced benches that demand minimal operator skills. Yet entrenched industry validation requirements and proprietary calibration scripts keep switching costs high, preserving moderate concentration in the optical coordinate measuring machine market.

Optical Coordinate Measuring Machine Industry Leaders

Hexagon AB

Carl Zeiss AG

Mitutoyo Corp.

Nikon Metrology NV

Werth Messtechnik GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hexagon AB partnered with NVIDIA to integrate AI algorithms into optical CMM software, enhancing error correction and reducing programming time.

- February 2026: Carl Zeiss AG opened a EUR 45 million (USD 52.23 million) optical metrology facility in Germany, increasing CMM capacity by 35% for EV battery demand.

- January 2026: Mitutoyo Corp. launched the CRYSTA-Apex V HA series, a bridge-type optical CMM with ±1.2-micrometer accuracy, addressing aerospace composite-structure inspection challenges.

- December 2025: Keyence Corp. secured an USD 18 million contract with a Taiwanese semiconductor foundry for IM-Series vision systems.

Global Optical Coordinate Measuring Machine Market Report Scope

The Optical Coordinate Measuring Machine (CMM) market is witnessing significant growth due to advancements in measurement technologies and increasing demand across various industries. These machines are essential for ensuring precision and quality control in manufacturing processes, driving their adoption in sectors such as aerospace, automotive, and medical devices. The market's expansion is further supported by the integration of automation and Industry 4.0 technologies, enhancing operational efficiency and accuracy.

The Optical Coordinate Measuring Machine Market Report is Segmented by Product Type (Multi-Sensor, 2D Vision, 3D Vision, Laser Scanning, Structured-Light), Machine Type (Bridge, Gantry, Articulated Arm, Horizontal, Portable Benchtop), Component (Hardware, Software, Services), Measurement Volume Range (Small, Medium, Large), End-User Industry (Aerospace, Automotive, Medical Device, Heavy Machinery, Electronics, Energy, Other), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Multi-Sensor |

| 2D Vision Measurement Machine |

| 3D Vision Measurement Machine |

| Laser Scanning Optical CMM |

| Structured-Light Optical CMM |

| Bridge |

| Gantry |

| Articulated Arm |

| Horizontal |

| Portable Benchtop |

| Hardware |

| Software |

| Services |

| Small (? 500 mm) |

| Medium (500-2 000 mm) |

| Large (> 2 000 mm) |

| Aerospace and Defense |

| Automotive |

| Medical Device and Orthopedics |

| Heavy Machinery and Metal Fabrication |

| Electronics and Semiconductor |

| Energy and Power Generation |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Malaysia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Multi-Sensor | |

| 2D Vision Measurement Machine | ||

| 3D Vision Measurement Machine | ||

| Laser Scanning Optical CMM | ||

| Structured-Light Optical CMM | ||

| By Machine Type | Bridge | |

| Gantry | ||

| Articulated Arm | ||

| Horizontal | ||

| Portable Benchtop | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Measurement Volume Range | Small (? 500 mm) | |

| Medium (500-2 000 mm) | ||

| Large (> 2 000 mm) | ||

| By End-User Industry | Aerospace and Defense | |

| Automotive | ||

| Medical Device and Orthopedics | ||

| Heavy Machinery and Metal Fabrication | ||

| Electronics and Semiconductor | ||

| Energy and Power Generation | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is demand for optical coordinate measurement growing in Asia Pacific?

Asia Pacific revenue is forecast to rise at 3.68% CAGR from 2026-2031 as semiconductor self-sufficiency, precision machinery exports, and EV battery investments accelerate adoption.

Which product type is winning share against incumbents?

Structured-light systems are projected to grow 3.13% CAGR, edging into applications once owned by laser scanners by trimming inspection cycles from minutes to seconds.

What drives electronics and semiconductor users to upgrade metrology?

Advanced packaging and wafer-level optics now impose sub-10 µm tolerances, compelling fabs to deploy high-magnification optical CMMs that verify alignment without contaminating delicate surfaces.

Why are small and medium enterprises still hesitant to invest?

Up-front prices starting around USD 50 000 and recurring ISO 10360 reverification costs deter many SMEs, despite payback periods that often fall under two years.

Which three companies dominate global revenue?

Hexagon AB, Carl Zeiss AG, and Mitutoyo Corp. together control roughly 40–45% of sales through integrated hardware, proprietary software, and bundled service contracts.

Page last updated on: