Family Floater Health Insurance Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

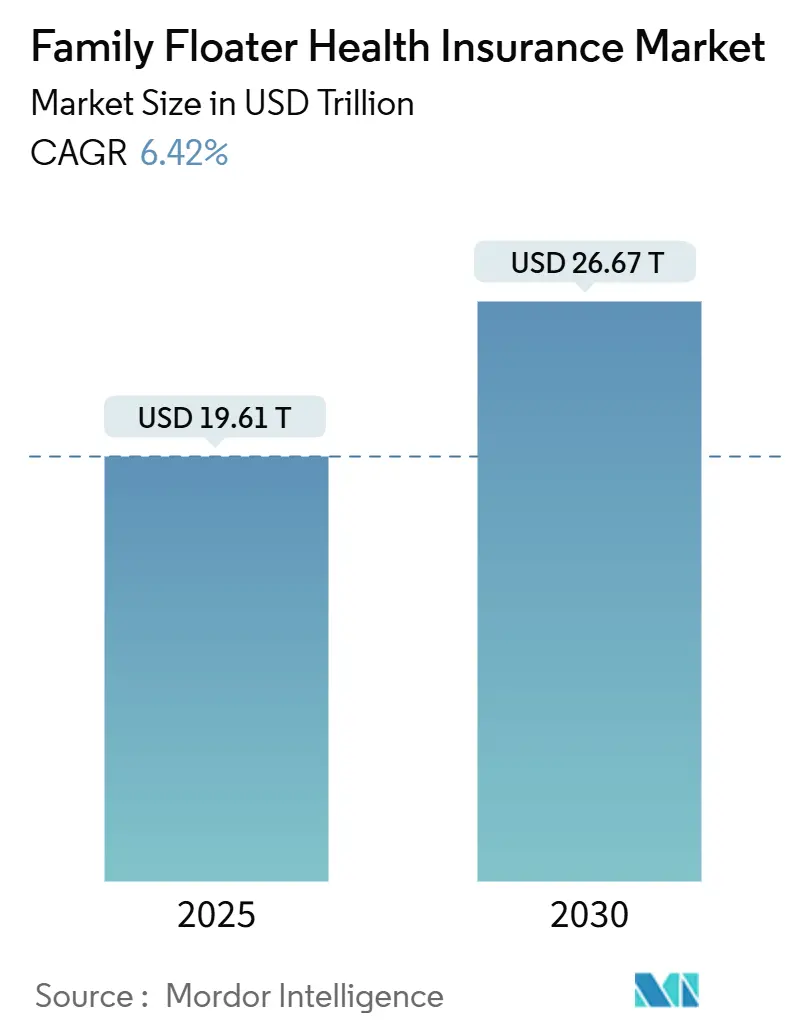

| Market Size (2025) | USD 19.61 Trillion |

| Market Size (2030) | USD 26.67 Trillion |

| Growth Rate (2025 - 2030) | 6.42% CAGR |

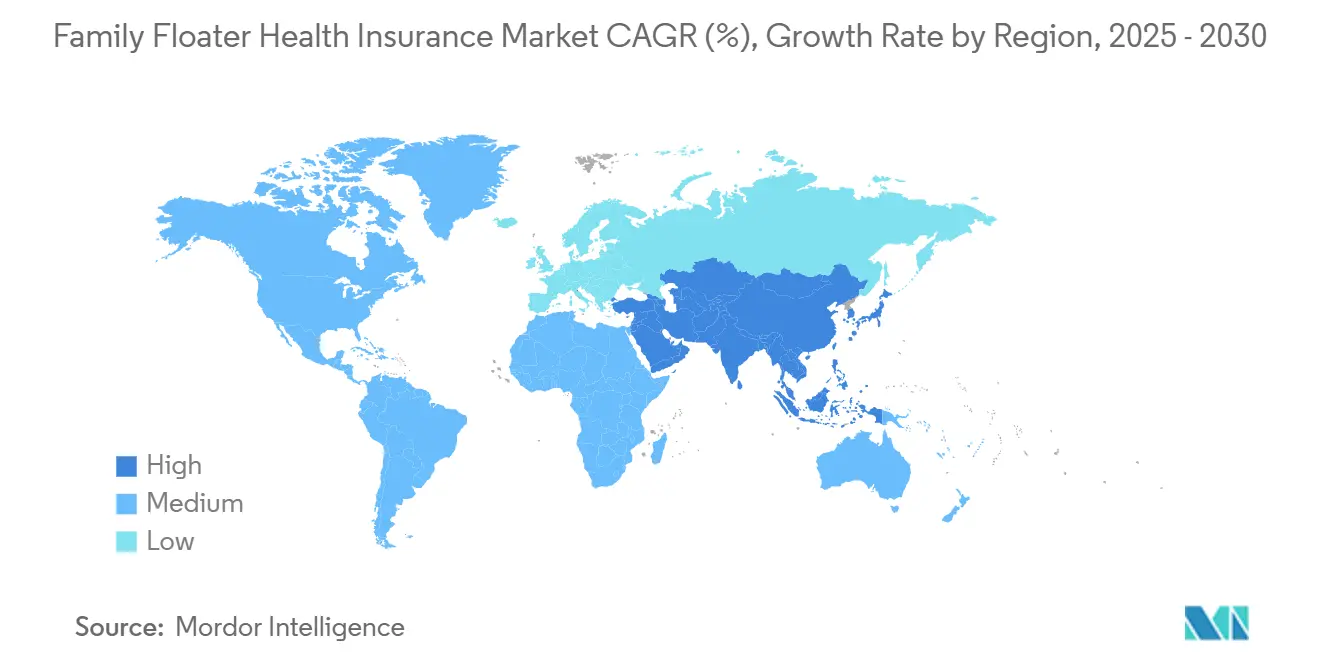

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Family Floater Health Insurance Market Analysis by Mordor Intelligence

The family floater health insurance market size was USD 19.61 trillion in 2025 and is forecast to reach USD 26.67 trillion by 2030, advancing at a 6.42% CAGR. North America led in 2024 with a 36.89% family floater health insurance market share while Asia-Pacific delivered the fastest growth at an 8.36% CAGR. Comprehensive plans continued to dominate because households value broad protection, and carriers stimulated take-up with telehealth, preventive-care perks, and digital self-service enrollment. Regulatory support for tax deductions and the removal of foreign-ownership caps kept premiums affordable and encouraged cross-border investment. Intensifying climate risk pushed insurers to attach parametric micro-health riders, and big-tech partnerships embedded cover inside health, banking, and mobility apps, expanding reach and lowering acquisition cost.

Key Report Takeaways

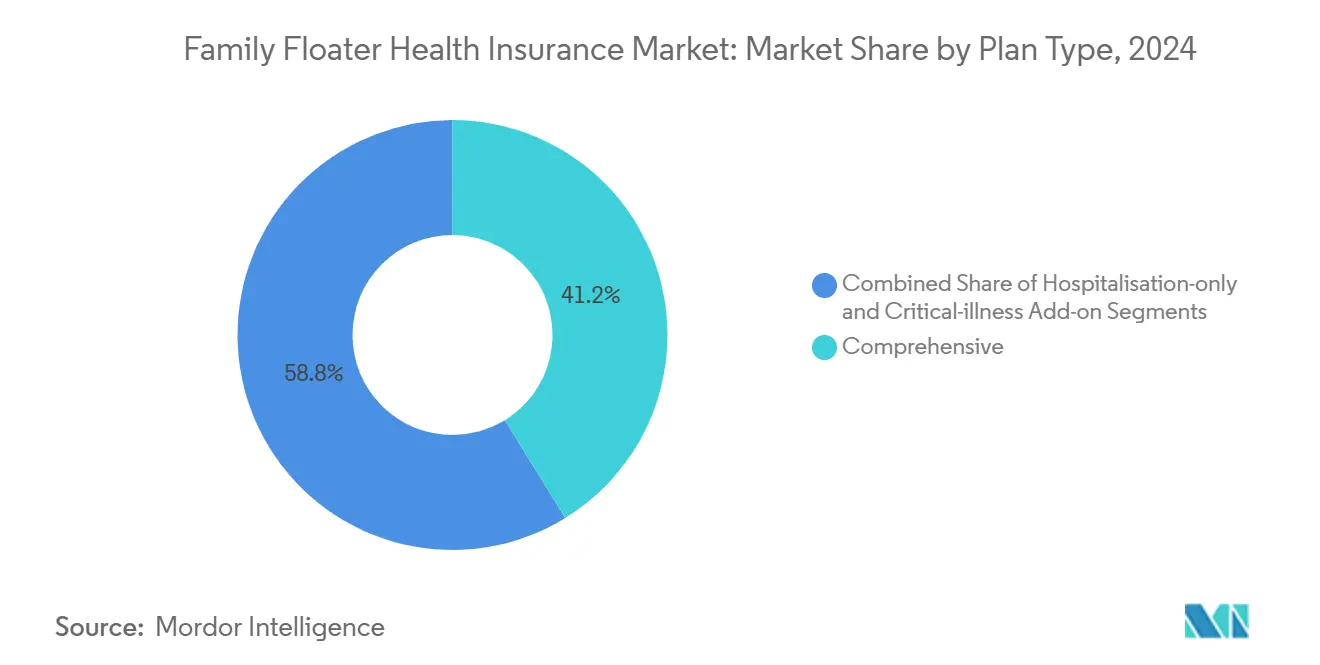

- By plan type, comprehensive plans held 41.22% of the family floater health insurance market share in 2024, whereas critical-illness add-ons are growing at a 10.23% CAGR through 2030.

- By sum-insured band, policies below USD 25,000 accounted for 46.37% of the family floater health insurance market size in 2024; sums above USD 100,000 are projected to post a 9.58% CAGR during 2025-2030.

- By distribution channel, the agency & broker model retained 44.68% share of the family floater health insurance market size in 2024 and digital direct-to-consumer sales are expanding at a 9.63% CAGR to 2030.

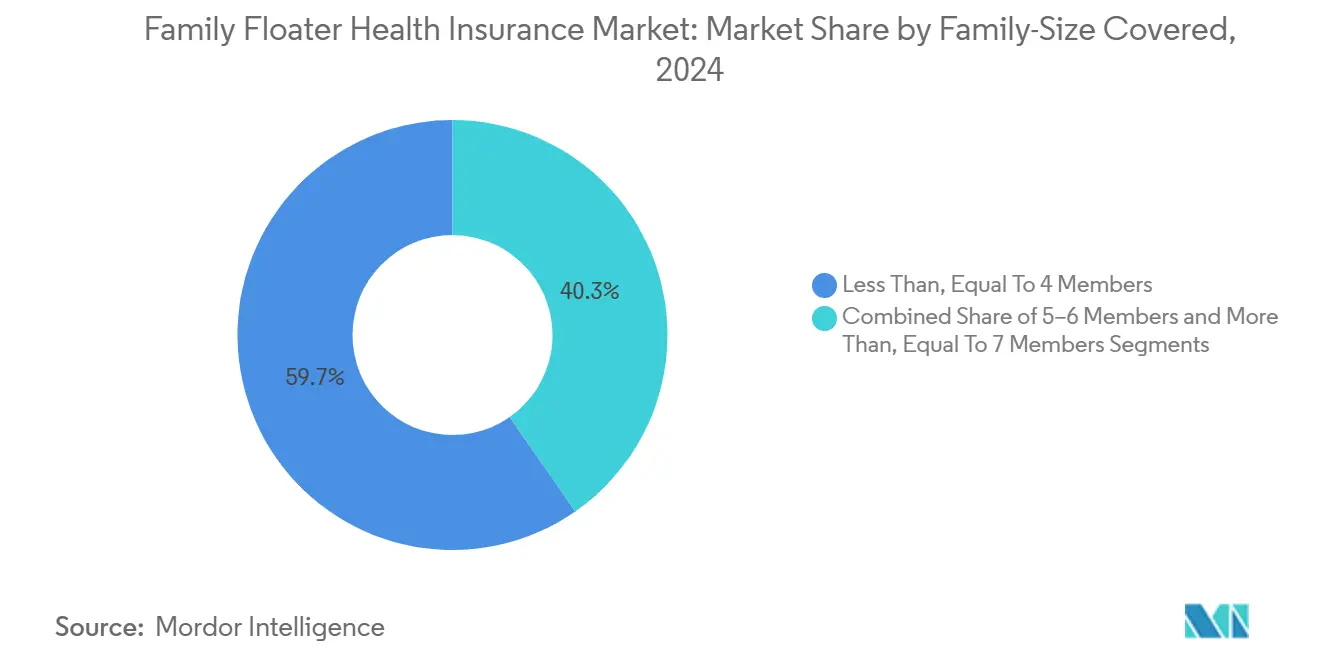

- By family size, policies covering up to four people contributed 59.68% of 2024 revenues, while plans for seven or more members are advancing at a 9.91% CAGR through 2030.

- By eldest-member age, the 36-50-year bracket captured 37.89% share of the family floater health insurance market size in 2024; policies where the eldest person is ≤35 years are rising at 9.47% CAGR to 2030.

- By region, North America commanded 36.89% of global revenue in 2024, yet Asia-Pacific is forecast to add the most absolute dollars with an 8.36% CAGR to 2030.

Global Family Floater Health Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global healthcare costs & out-of-pocket burden | +1.8% | Global, especially North America & Europe | Medium term (2-4 years) |

| Expansion of digital-first distribution platforms | +1.2% | Asia-Pacific core, spill-over to North America | Short term (≤2 years) |

| Tax incentives on health-insurance premiums | +0.9% | North America & EU, selective APAC markets | Long term (≥4 years) |

| Entry of big-tech embedded-insurance models | +1.1% | Global, led by North America & China | Medium term (2-4 years) |

| Preventive-care & tele-consult benefits bundled with policies | +0.7% | Global, accelerated in developed markets | Short term (≤2 years) |

| Parametric micro-health riders for climate-linked outbreaks | +0.3% | APAC & MEA, emerging Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Healthcare Costs & Out-of-Pocket Burden

Medical inflation outpaces general consumer prices worldwide; U.S. health-insurance premium inflation rose faster than overall medical care costs because hospital services dominate the weight of the index.[1]Brett Matsumoto, “Measuring Total-Premium Inflation for Health Insurance in the CPI,” U.S. Bureau of Labor Statistics, bls.govChinese payers expect medical costs to climb 11% in 2025, widening the protection gap for middle-income families. Family floater products mitigate that gap by pooling risks across household members under a single sum insured. Shared deductibles enhance efficiency, and predictable premiums safeguard cash flow against surprise hospitalization bills. Demand strengthens as post-pandemic health-care utilization normalizes while prices keep rising. Insurers further promote adoption by layering wellness programs that reduce long-term claim frequency.

Expansion of Digital-First Distribution Platforms

Large carriers and insurtechs embed family floater offerings in e-commerce and banking journeys, lifting conversion. Cover Genius secured USD 80 million to scale its API-driven distribution engine that transacts policies at checkout for global merchants.[2]Lucinda Shen, “Embedded Insurance Company Cover Genius Nabs USD 80 Million,” Axios, axios.com UnitedHealthcare released “UHC Hub,” consolidating benefits for employers and employees on a single portal. Asian incumbents such as Star Health digitized underwriting workflows, shrinking issuance time to minutes. Consumers welcome anytime purchase, transparent pricing, and instant e-policy delivery, pushing the family floater health insurance market toward direct and embedded channels.

Tax Incentives on Health-Insurance Premiums

Governments employ deductions and credits to improve affordability. The IRS raised long-term-care deduction limits for 2025, cutting effective premiums for policyholders who itemize. Premium-tax-credit enhancements under the Inflation Reduction Act saved marketplace enrollees USD 705 on average in 2024.[3]Gideon Lukens, “Premium Tax Credit Improvements Must Be Extended,” Center on Budget and Policy Priorities, cbpp.org India’s Section 80D deduction and fresh 100% FDI allowance continue to spur health-cover uptake. These measures reduce price sensitivity, encourage multi-member enrollment, and support sustained growth even as medical inflation accelerates.

Entry of Big-Tech Embedded-Insurance Models

Digital ecosystems with massive user bases integrate plug-and-play insurance components. Chubb’s global embedded platform supports partnerships from fintech to mobility players. A survey of industry executives ranks embedded distribution as the leading model for future personal lines growth. Big-tech firms harness transactional data to personalize pricing and deliver at-point-of-need offers, expanding the family floater health insurance market without extensive agent networks. Regulatory bodies, however, are advancing privacy and AI fairness rules that carriers must observe to sustain momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Age-weighted premium inflation for elder-inclusive families | -1.4% | Global, acute in aging societies (Japan, Europe) | Medium term (2-4 years) |

| Regulatory caps on broker/agent commissions | -0.8% | India, selective European markets | Short term (≤2 years) |

| Algorithmic-underwriting bias triggering tighter oversight | -0.6% | North America & EU, emerging APAC | Long term (≥4 years) |

| Data-privacy backlash against wearable-linked discounts | -0.9% | Global, led by privacy-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Age-Weighted Premium Inflation for Elder-Inclusive Families

Premiums tied to the oldest insured person escalate quickly in aging societies, stretching budgets for multigenerational households. Rate filings indicate double-digit increases in several supplemental covers for seniors, fueled by rising hospital charges and workforce shortages. Younger earners sometimes split coverage to avoid surcharges, shrinking the pooled risk base. Insurers experiment with flat-family pricing and wellness credits to soften sticker shock, yet actuarial margins must remain intact to absorb high-severity claims.

Regulatory Caps on Broker/Agent Commissions

India’s expense-management framework limits total outgo to 30% of premiums by FY26, tightening room for commission-heavy selling. Similar ceilings appear across Europe, curbing incentives for agents who often explain complex family floater designs. Carriers pivot toward online self-service and bancassurance to offset lost field capacity, but high-touch consultative sales remain vital for large households or elder-inclusive plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plan Type: Critical-Illness Coverage Drives Premium Growth

Comprehensive plans captured 41.22% of 2024 revenue. The family floater health insurance market size for critical-illness add-ons is projected to expand at a 10.23% CAGR as households recognize gaps in standard hospitalization covers. Carriers enhance engagement with mental-health sessions and virtual specialists accessible through mobile apps. AXA’s all-in-one digital suite illustrates the trend toward bundling risk cover with self-care tools.

Aging populations and increased incidence of lifestyle diseases push families to seek lump-sum payouts that fund expensive treatments and post-care rehabilitation. Despite higher premiums, critical-illness riders offer peace of mind against catastrophic expenses and reinforce customer loyalty, enlarging the family floater health insurance market.

By Sum-Insured Band: Premium Segments Accelerate Despite Lower Volume Base

Coverage below USD 25,000 holds 46.37% share thanks to affordability in emerging economies. Yet the family floater health insurance market size for policies above USD 100,000 is poised for a 9.58% CAGR as affluent customers hedge against dollar-denominated medical bills at private centers. India’s regulator removed entry-age caps, freeing carriers to issue high-limit covers to senior citizens and chronic-condition patients, expanding demand for premium tiers.

Greater disposable income and medical tourism spur purchases of big-ticket policies. Insurers invest in concierge support and international provider networks, further justifying higher sums insured and placing upward pressure on overall market value.

By Distribution Channel: Digital Transformation Reshapes Sales Dynamics

Agencies and brokers still delivered 44.68% of 2024 gross written premiums. However, direct-to-consumer portals will record a 9.63% CAGR to 2030 as millennials favor self-service. Sure’s rails demonstrate how white-label APIs can embed offers in automotive and retail platforms. Bancassurance thrives where universal bank apps push cross-sell alerts, while embedded models piggyback on ride-sharing, pharmacy, or telco ecosystems.

The hybrid model prevails: human agents handle complex family configurations, whereas chatbots confirm routine endorsements. Insurers that orchestrate omnichannel journeys will gain share in the family floater health insurance market.

By Family Size Covered: Extended Families Drive Growth Despite Complexity

Families of ≤4 people generated 59.68% of revenue in 2024, aligned with nuclear norms in developed regions. Plans for ≥7 members, though smaller in count, will outpace at 9.91% CAGR as multigenerational living remains common in Asia and parts of Africa. Larger households appreciate shared deductibles and unified renewal dates, yet underwriting several risk profiles in one policy strains actuarial modeling. Digital proposal forms and automated health-declaration scoring reduce cycle time.

Carriers may introduce step-pricing that increments sum insured with household size while capping per-capita loading, balancing profitability and accessibility.

By Eldest-Member Age Bracket: Youth Segments Outpace Aging Demographics

Policies where the eldest person is 36-50 years commanded 37.89% of premiums. Younger families, with the eldest ≤35 years, are set to grow 9.47% annually as employers promote voluntary benefits and digital influencers spotlight the cost of untreated illness. Start-ups bundle tele-consult, fitness coaching, and mental-wellness to resonate with Gen-Z parents.

Conversely, premiums escalate sharply once the eldest turns 51, challenging adoption among fixed-income seniors. Some carriers trial flat-premium pools financed by wellness participation points, aiming to retain multigenerational groups inside the family floater health insurance market.

Geography Analysis

North America retained 36.89% of global premiums in 2024 owing to high per-capita spend, mature private insurance penetration, and robust tax credits. Stringent disclosure laws around AI underwriting and health-data privacy shape product design, yet integrated payer-provider models such as UnitedHealth Group demonstrate economies of scale in claims control.

Europe sustains steady growth as households supplement state systems with private covers that fast-track elective procedures. Cross-border labor mobility drives demand for portable family plans, and EU data-protection norms influence global product standards. Commission ceilings in select markets pressure intermediated sales, accelerating migration to bancassurance and digital channels.

Asia-Pacific delivers the highest incremental premium volume, clocking an 8.36% CAGR. Liberalized FDI rules in India and rapid digitalization in China raise competitive intensity and innovation speed. Japan’s My Number health card supports seamless e-claims, encouraging integrated wellness-insurance ecosystems. Middle East & Africa and Latin America exhibit low penetration but healthy upside as governments push universal-health reforms and mobile adoption climbs, positioning the family floater health insurance market for long-term expansion.

Competitive Landscape

The market remains moderately concentrated. In the United States, 95% of metropolitan areas are classified as highly concentrated, with UnitedHealth Group the largest carrier by commercial and Medicare Advantage membership. Europe sees a mix of pan-regional giants such as Allianz and AXA alongside mutual insurers. Asia continues to fragment, though foreign acquisitions like Bupa’s majority stake in Niva Bupa signal consolidation.

Strategic focus revolves around vertical integration: Health Care Service Corporation bought Cigna’s Medicare lines for USD 3.7 billion, adding 4.3 million seniors to its base. Carriers deploy venture capital to accelerate insurtech partnerships, favoring telehealth, AI underwriting, and embedded-distribution capabilities. Allianz Partners allied with Chery to package mobility insurance and roadside services across Europe.

Regulators monitor algorithmic fairness, prompting investments in explainable AI and inclusive product design. Climate risk opens whitespace for parametric riders, and demographic shifts create niches around gig-worker and multi-elder covers. Sustained technology spend, data governance discipline, and multi-channel reach differentiate winners in the family floater health insurance market.

Family Floater Health Insurance Industry Leaders

UnitedHealth Group

Allianz SE

AXA SA

Ping An Health

Bupa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Health Care Service Corporation completed the USD 3.7 billion acquisition of Cigna’s Medicare and CareAllies businesses, adding 4.3 million members and broadening national reach.

- March 2025: Allianz Partners and Chery International signed a mobility-insurance partnership covering MTPL, own-damage, and usage-based products across Europe to 2027.

- February 2025: DXC Technology enabled Allianz PNB Life to slash policy-issuance time to five minutes through its cloud-based DXC Assure Integral platform.

Global Family Floater Health Insurance Market Report Scope

| Comprehensive (All-risk) |

| Hospitalisation-only |

| Critical-illness Add-on |

| Less Than US$25 k |

| US$25 k-100 k |

| More Than US$100 k |

| Agency & Brokers |

| Bancassurance |

| Direct-to-Consumer (Online & Mobile Apps) |

| Embedded / Affinity Partnerships |

| Less than, Equal To 4 Members |

| 5-6 Members |

| More Than, Equal To 7 Members (Joint / Extended) |

| Less Than, Equal To 35 Years |

| 36-50 Years |

| 51-65 Years |

| More Than 65 Years |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Plan Type | Comprehensive (All-risk) | |

| Hospitalisation-only | ||

| Critical-illness Add-on | ||

| By Sum-Insured Band | Less Than US$25 k | |

| US$25 k-100 k | ||

| More Than US$100 k | ||

| By Distribution Channel | Agency & Brokers | |

| Bancassurance | ||

| Direct-to-Consumer (Online & Mobile Apps) | ||

| Embedded / Affinity Partnerships | ||

| By Family Size Covered | Less than, Equal To 4 Members | |

| 5-6 Members | ||

| More Than, Equal To 7 Members (Joint / Extended) | ||

| By Eldest-Member Age Bracket | Less Than, Equal To 35 Years | |

| 36-50 Years | ||

| 51-65 Years | ||

| More Than 65 Years | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the family floater health insurance market by 2030?

It is forecast to reach USD 26.67 trillion, rising at a 6.42% CAGR.

Which region is growing fastest in family floater policies?

Asia-Pacific is on track for an 8.36% CAGR through 2030 because of economic growth and digital-first distribution.

Which plan type is expanding most rapidly?

Critical-illness add-on covers, with a 10.23% CAGR as families seek protection against catastrophic events.

How are digital channels impacting sales?

Direct-to-consumer and embedded platforms are expected to grow 9.63% annually, eroding the dominance of traditional intermediaries.

Why are parametric riders gaining interest?

They provide instant payouts based on climate-related triggers, offering families quick financial relief during health crises.

What challenges limit uptake among elder-inclusive households?

Age-weighted premium inflation can make comprehensive coverage unaffordable for multigenerational families, prompting product redesign.

Page last updated on: