Fake Image Detection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 7.43 Billion |

| Growth Rate (2026 - 2031) | 31.73% CAGR |

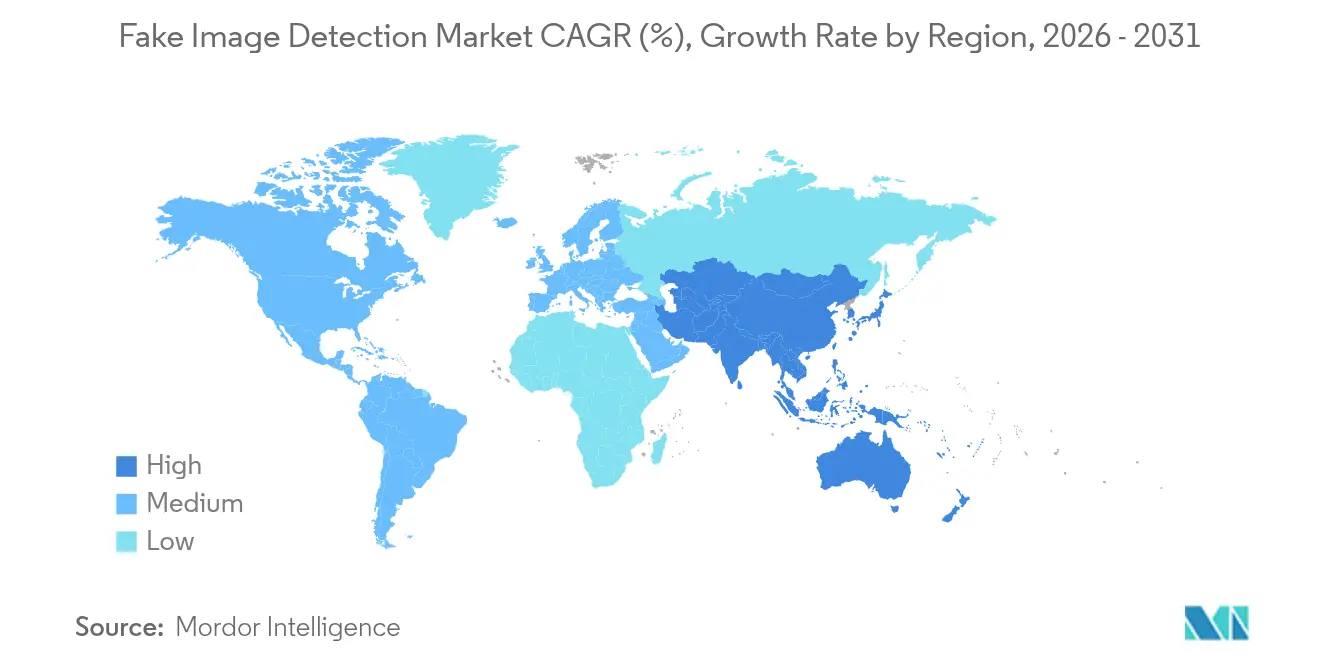

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fake Image Detection Market Analysis by Mordor Intelligence

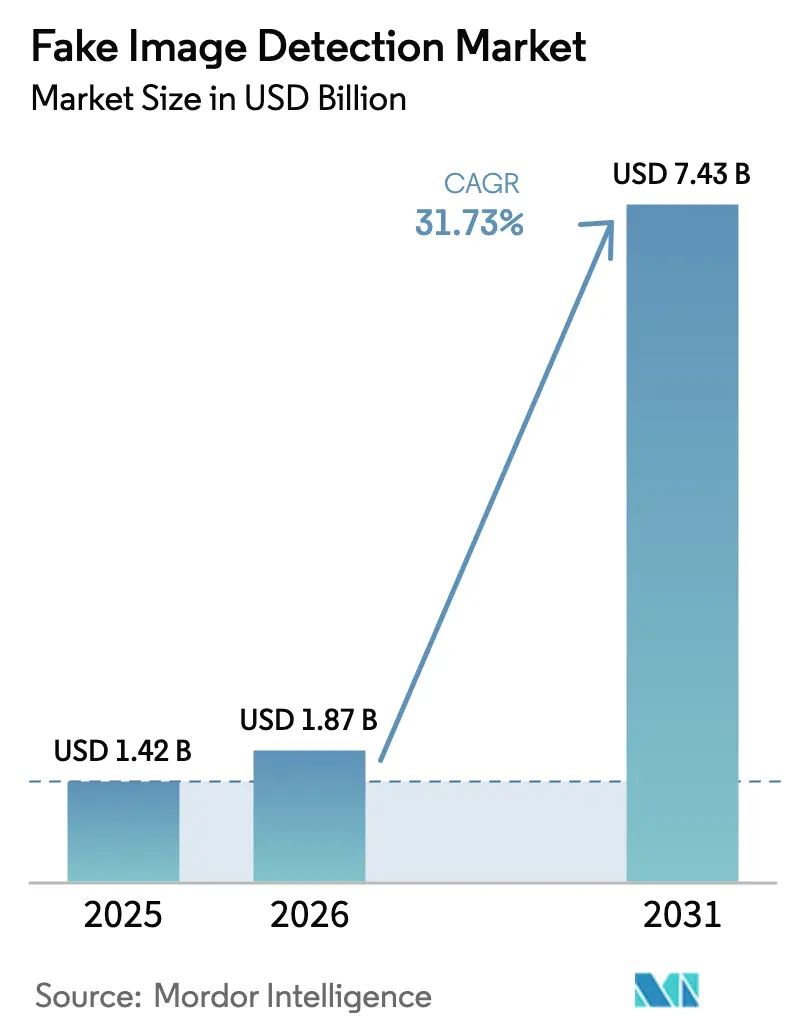

Fake image detection market size in 2026 is estimated at USD 1.87 billion, growing from 2025 value of USD 1.42 billion with 2031 projections showing USD 7.43 billion, growing at 31.73% CAGR over 2026-2031. Escalating synthetic-media abuse, tighter disclosure mandates under the EU AI Act, and expanding enterprise risk budgets jointly propel the fake image detection market. Rapid adoption of watermarking standards by camera makers, deepening cloud–edge synergies that cut inference latency, and rising integration of detector APIs into mainstream creative-tool chains compound demand. Financial institutions, newsrooms, and defense agencies continue to allocate larger compliance and security outlays as multi-modal deepfakes disrupt identity verification and information integrity. Heightened investor activity and patent filings signal an innovation race in detection algorithms, watermarking protocols, and edge accelerators poised to shape competitive positioning.

Key Report Takeaways

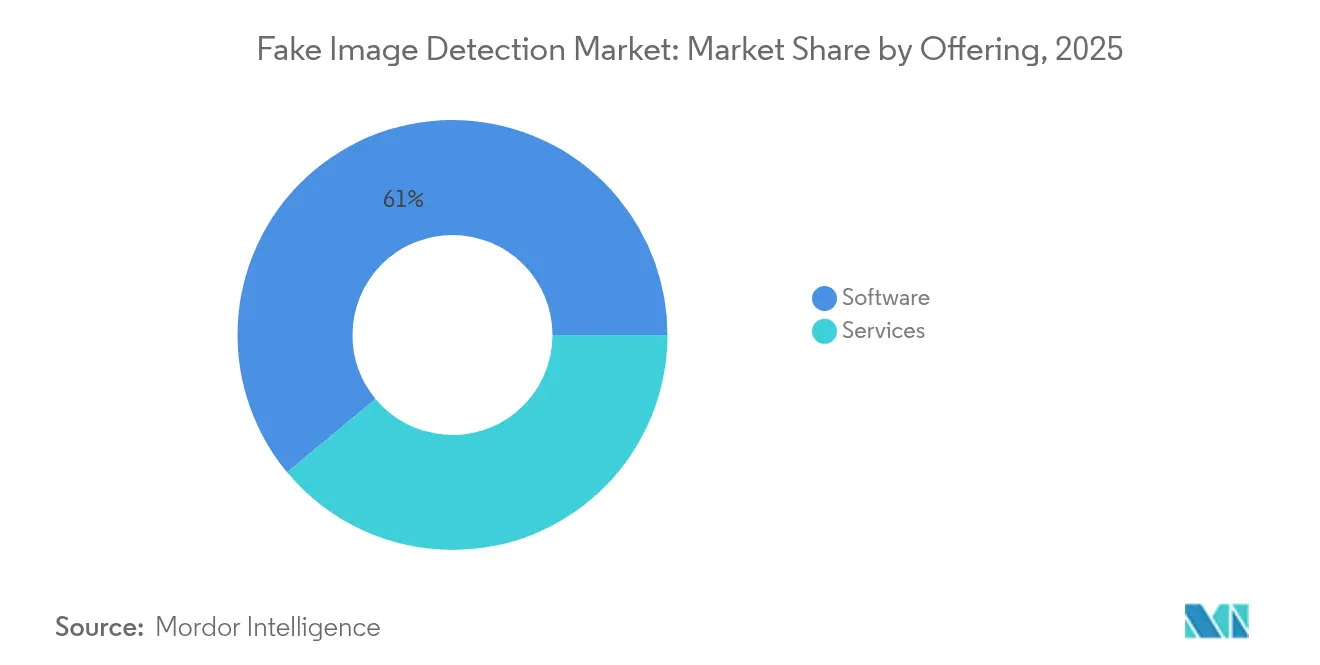

- By offering, software captured 61.03% of fake image detection market share in 2025; services are projected to advance at a 33.08% CAGR between 2026-2031.

- By solution, deepfake image detection accounted for 47.86% share of the fake image detection market size in 2025 and AI-generated image detection is growing at 35.12% CAGR to 2031.

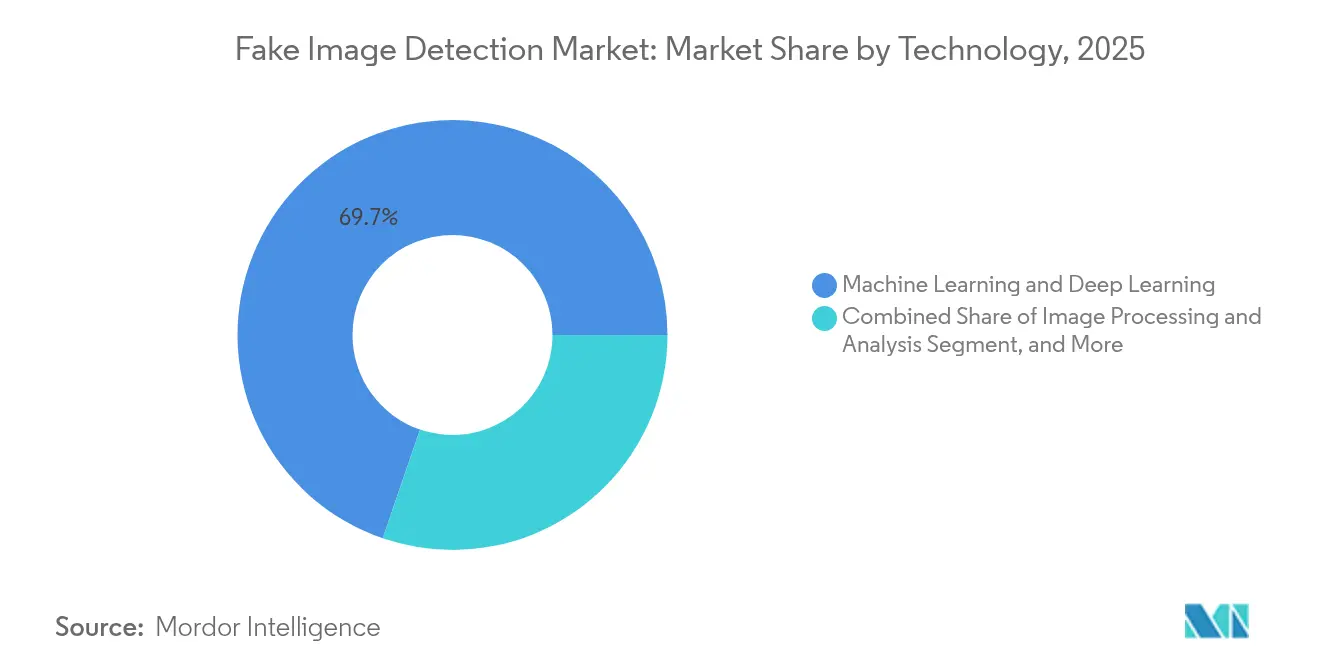

- By technology, machine learning and deep learning commanded 69.74% of the fake image detection market size in 2025, while blockchain and cryptographic hashing record the highest 34.88% CAGR through 2031.

- By deployment mode, cloud models maintained 66.92% share of fake image detection market size in 2025; edge/on-device deployment is set to climb at 32.96% CAGR to 2031.

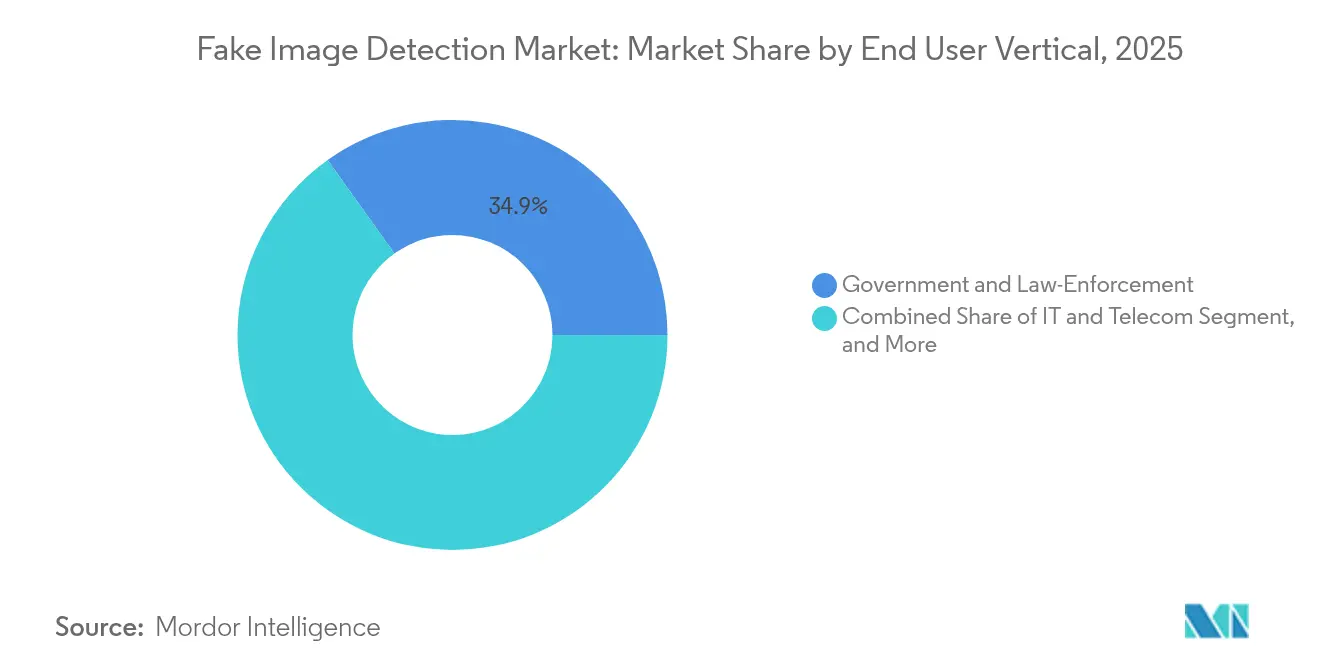

- By end-user vertical, government and law enforcement held 34.86% of fake image detection market share in 2025, whereas BFSI is witnessing the fastest 34.37% CAGR through 2031.

- By image type, static images led with 56.58% share in 2025; video/live-stream analysis is forecast to post a 33.52% CAGR during 2026-2031.

- By geography, North America led with 45.15% revenue share in 2025, while Asia Pacific is forecast to expand at a 32.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fake Image Detection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Compliance with EU AI Act's Synthetic Media Disclosure Clauses Raising Enterprise Spend in Europe | +8.2% | Europe, with spillover to North America and Asia-Pacific | Short term (≤ 2 years) |

| Spike in Identity-Theft Losses via Face-Swap Fraud Triggering KYC Upgrades in North-American BFSI | +6.8% | North America, expanding to global BFSI operations | Medium term (2-4 years) |

| Content Authenticity Initiative Adoption by Global News Agencies Creating Demand for Image-Forensics APIs | +4.5% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cloud-Native Vision-AI Accelerators Reducing Inference Latency for Real-Time Mobile Detection | +5.1% | Global, with early adoption in North America and Asia-Pacific | Long term (≥ 4 years) |

| Media and Entertainment Shift to Virtual Production Pipelines Driving On-Set Authenticity Water-Marking | +3.8% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Asia-Pacific Government Disinformation Taskforces Funding Open-Source Detector Development | +4.2% | Asia-Pacific core, with technology transfer to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory compliance with EU AI Act synthetic-media clauses raising enterprise spend in Europe

Starting February 2025, the EU AI Act compels visible and machine-readable labels on AI-generated imagery, imposing fines up to EUR 35 million (USD 38 million) for violations.[1]AI or Not, “Spain's AI Detection Requirement: $38 Million Fine for Unlabeled AI,” aiornot.com European firms now embed detectors at ingest and distribution layers to avoid penalties, driving the fake image detection market toward scalable, cloud-native platforms that can tag, score, and audit visual assets in real time. Multinationals extend EU-compliant workflows enterprise-wide, creating global network effects that accelerate adoption.

Surge in face-swap fraud losses triggering KYC upgrades in North-American BFSI

Deepfake-enabled identity-theft attempts rose 2,137% in three years, now representing 6.5% of all fraud incidents.[2]Signicat, “Fraud Attempts with Deepfakes Have Increased by 2137%,” signicat.com North-American banks retrofit liveness, micro-expression, and behavioral-analysis modules into onboarding funnels, fueling premium demand for managed detection services able to refresh models weekly. Limited internal AI expertise explains the pivot from perpetual software licenses to outcome-based service contracts.

Content Authenticity Initiative adoption by global news agencies creating demand for image-forensics APIs

AFP piloted C2PA-compliant watermarking during the 2024 US elections while the BBC rolled out content-credential features across news desks.[3]Agence France-Presse, “AFP Tests Photo Authenticity Tech,” afp.com These deployments stimulate API demand from wire services and CMS vendors seeking seamless integration of provenance checks into editorial pipelines. The momentum encourages hardware makers to ship cameras with embedded digital-signature firmware, tightening the end-to-end integrity chain.

Cloud-native vision-AI accelerators reduce inference latency for real-time mobile detection

The introduction of new GPU, TPU, and NPU instances has significantly reduced latency, bringing it down from several seconds to less than 200 milliseconds. This advancement enables real-time processing and analysis of live-stream data with remarkable efficiency. As a result, businesses can now perform live-stream analysis without any noticeable delay, enhancing operational capabilities and improving user experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Evolution of Diffusion Models Outpacing Detector Training Cycles, Increasing False Negatives | -7.3% | Global, with highest impact in regions with advanced AI research | Short term (≤ 2 years) |

| Privacy Regulations Restricting Access to Annotated Training Datasets | -4.8% | Europe and North America, expanding globally | Medium term (2-4 years) |

| High Computational Costs for Edge Deployment on Low-Power Devices in Developing Regions | -3.2% | Asia-Pacific, MEA, and Latin America | Long term (≥ 4 years) |

| Lack of Unified Benchmark Standards Leading to Buyer Uncertainty and Longer Sales Cycles | -2.9% | Global, with particular impact on enterprise adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid evolution of diffusion models outpacing detector training cycles

Single denoising steps already degrade current detectors, shrinking accuracy to 68% on complex artifacts. Vendors face escalating retraining costs and must deploy continual-learning pipelines to sustain efficacy, tempering near-term margins in the fake image detection market.

Privacy regulations restricting access to annotated training datasets

GDPR and CPRA obligations complicate collection of diverse facial datasets, prompting research into synthetic training records that match real-world performance. While synthetic data mitigates privacy risk, it adds engineering overhead and can widen bias gaps for under-represented demographics, prolonging validation cycles for enterprise deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum Despite Software Dominance

Software maintained 61.03% revenue in 2025, reflecting early demand for self-hosted SDKs and API toolkits. Nevertheless, services are accelerating at 33.08% CAGR, signalling a structural pivot toward managed detection as enterprises offload model maintenance to specialists. Continuous retraining to outpace diffusion-model advances renders the in-house route cost-intensive, steering procurement toward subscription agreements that bundle threat-intelligence feeds and SLA-backed accuracy guarantees. BFSI and media groups drive multiyear contracts that allow vendors to pool learning across clients, reinforcing scale advantages. This shift boosts recurring revenue predictability, tightening vendor lock-in and raising switching costs in the fake image detection market.

Simultaneously, cloud marketplace listings ease procurement friction, enabling mid-size enterprises to activate detectors via pay-as-you-go billing. Vendors respond with modular service tiers ranging from API-only to full-stack SOC integrations. The services trend elevates human-in-the-loop audit offerings, where skilled analysts validate edge-case outputs, enhancing trust among regulated customers. As this model matures, analysts expect services to approach parity with software by late 2028, reshaping revenue mix across the fake image detection industry.

By Solution: AI-Generated Detection Emerges as Growth Driver

Deepfake image detection still commands 47.86% segment share in 2025, anchoring the category. Yet AI-generated image detection is racing ahead at 35.12% CAGR as diffusion-based text-to-image tools democratize synthetic scene creation. Cross-domain detectors that inspect lighting, shadows, and object geometry now win RFPs from e-commerce and advertising clients confronted with manipulated product photos. Market momentum reflects a strategic pivot from reactive deepfake hunting toward holistic authenticity scoring covering all generative approaches.

Sony’s Camera Verify rollout with C2PA support underscores the forward integration of authenticity at capture. Watermark-integrated detectors jointly raise switching barriers, as downstream platforms must interpret proprietary signature schemes. Consequently, solution roadmaps converge around multi-signal architectures blending inference scores with cryptographic proofs, redefining competitive baselines inside the fake image detection market.

By Technology: Blockchain Emerges as Watermarking Alternative

Machine learning and deep learning engines hold 69.74% of 2025 revenues, providing probabilistic judgments that identify pixel or frequency-domain anomalies. However, blockchain-anchored watermarking rises at 34.88% CAGR, appealing to courts and regulators demanding cryptographic evidence. Digimarc’s C2PA 2.1-aligned release illustrates market readiness for immutable provenance tracing. Hybrid stacks now hash capture-device IDs on public ledgers, then feed inference modules for anomalies, delivering layered defenses that satisfy both legal admissibility and operational practicality.

Parallel innovation in computer-vision accelerators compresses transformer-based detectors without sacrificing AUC, making on-premise and edge inference affordable. Vendors wield proprietary silicon partnerships to differentiate latency profiles, a critical buying criterion for broadcast and surveillance clients. This dual-track strategy enlarges the fake image detection market size by opening budget-constrained use cases previously priced out of advanced detection.

By Deployment: Edge Computing Gains Traction Despite Cloud Dominance

Cloud deployment accounted for 66.92% share in 2025, leveraging elastic compute and unified model-management consoles. Yet edge/on-device roll-outs post a 32.96% CAGR as privacy mandates and real-time use cases proliferate. Qualcomm’s roadmap includes hardware root-of-trust for authenticity signals in future mobile chipsets. Edge inference eliminates round-trip latency and shields biometric data from cross-border transfer risk, widening adoption among healthcare and defense users.

To balance performance and cost, vendors employ federated-learning schemes that aggregate gradients rather than raw images, meeting sovereignty rules while enriching global models. Such architectures tighten ecosystem dependencies; device makers, cloud providers, and detector firms collaborate under revenue-sharing arrangements, adding multi-stakeholder complexity yet broadening the total addressable fake image detection market.

By End-User Vertical: BFSI Drives Fastest Growth Despite Government Leadership

Government and law-enforcement agencies captured 34.86% revenue in 2025, buoyed by digital-evidence admissibility requirements and funded national-security programs such as Hive’s USD 2.4 million DoD contract. The sector emphasizes deterministic proofs and chain-of-custody logging, steering R&D toward watermarking and hardware-rooted approaches.

BFSI, expanding at 34.37% CAGR, confronts tangible fraud losses and evolving KYC regulations. Institutions deploy multi-modal detectors that cross-check document authenticity, user liveness, and behavioral biometrics. Integration with core banking platforms drives high-margin services revenue and catalyzes vendor specialization in fraud-analytics consultative offerings. As regulators issue sector-specific deepfake advisories, BFSI share within the fake image detection market is expected to narrow the gap with government spend by 2029.

By Image Type: Video Processing Complexity Drives Growth

Static-image analysis held 56.58% share in 2025, underpinning social-media moderation and e-commerce listing scans. Video and live-stream detection now logs a 33.52% CAGR as misinformation threats pivot to dynamic content. Streaming platforms require per-frame authenticity scoring below 100 milliseconds, prompting vendors to blend temporal-coherence checks with optical-flow-based anomaly detection. The compute premium lifts average selling prices, expanding the fake image detection market size.

Sports broadcasters and video-conferencing providers emerge as early adopters, exploiting authenticity overlays to reassure viewers. Over time, content platforms intend to expose authenticity scores via public APIs, mirroring spam-filter transparency, which could reshape user trust metrics and create secondary analytics revenue streams.

Geography Analysis

North America continues to command 45.15% of 2025 revenues, anchored by a dense base of AI platform vendors, defense primes, and Tier-1 financial institutions. The region benefits from multi-stakeholder funding such as Microsoft and OpenAI’s USD 2 million election-integrity fund. Federal contracting pathways accelerate technology readiness levels, while state bills on synthetic-media disclosure nurture additional compliance spend, reinforcing leading-indicator status for the fake image detection market.

Asia Pacific records the fastest 32.47% CAGR to 2031, magnetized by explosive deepfake incident growth of 1,530%. Singapore’s USD 20 million Centre for Advanced Technologies in Online Safety demonstrates proactive public funding that seeds regional research clusters. Additionally, India’s 2024 election cycle showcased both surge and mitigation, sparking procurement among local broadcasters and fintechs. The region’s manufacturing prowess fosters cost-efficient edge hardware, amplifying growth in mid-tier segments.

Europe represents the most regulation-driven addressable pool as the EU AI Act mandates transparency and authenticity labelling. Spain’s EUR 35 million (USD 38 million) fine ceiling elevates compliance urgency, with enterprises integrating detectors across pan-EU digital-asset workflows. European vendors prioritize privacy-preserving techniques such as federated-learning detectors, differentiating on GDPR alignment and enhancing export appeal to jurisdictions with similar data-protection regimes, thereby expanding the fake image detection market.

Competitive Landscape

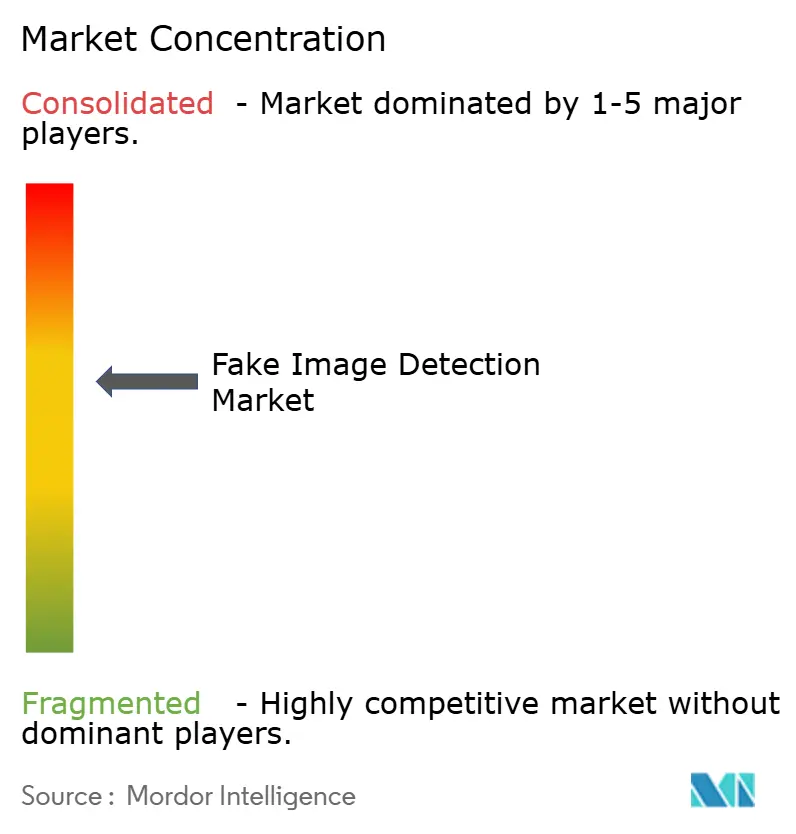

The fake image detection market shows moderate fragmentation, with scale advantages accruing to firms that can train on multi-modal datasets and deploy globally. Technology majors—Adobe, Microsoft, Google—leverage cloud footprints to bundle authenticity services with creative suites, while pure-plays such as Reality Defender and Sensity AI differentiate on algorithmic precision and responsive model updates. Patent activity around validation automation and video-deepfake detection systems is intensifying, signalling rising IP defensibility stakes.

Strategically, competitors cluster into inference-focused detector specialists and provenance-first watermarking providers. Alliances emerge between camera OEMs, chipset vendors, and software start-ups to offer end-to-end authenticity, evidenced by Sony’s in-camera signatures and Qualcomm’s processor-embedded roots of trust. Disruptors pursue edge AI, pairing model compression with hardware acceleration to challenge cloud incumbents on latency and privacy grounds.

Funding momentum remains strong: Daon joined AWS ISV Accelerate, widening distribution for biometric and deepfake detection solutions. Government contracts, exemplified by Hive’s Department of Defense award, validate technological maturity and provide revenue certainty that supports aggressive R&D roadmaps. Overall, convergence between content-creation and content-verification ecosystems intensifies, blurring category lines and setting up new coopetition dynamics inside the fake image detection industry.

Fake Image Detection Industry Leaders

Microsoft Corporation

Google LLC

Canon Inc.

Sony Group Corporation

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Daon joined AWS ISV Accelerate program to scale identity-verification and deepfake-detection products, signalling a channel-expansion strategy that leverages AWS co-selling incentives.

- December 2024: The US DoD awarded Hive a USD 2.4 million contract for multimodal deepfake detection, validating product capability and unlocking classified-data training opportunities.

- October 2024: Digimarc released C2PA 2.1-compliant watermarking, positioning for first-mover advantage in provenance-as-a-service.

Global Fake Image Detection Market Report Scope

Fake Image Detection identifies and verifies alterations, manipulations, or artificial generation of images. This task becomes paramount in the digital landscape, where tools like Photoshop and AI models can easily alter or create images. Fake image detection aims to ascertain an image's authenticity, ensuring it remains untampered and not crafted to deceive or mislead its viewers.

The study tracks the revenue accrued through the sale of fake image detection solutions by various players across the globe. The study also tracks the key market parameters, underlying growth influences, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

Fake Image Detection Market is Segmented by Offering (Software, and Services), Solution (Photoshopped Image Detection, Deepfake Image Detection, and More), Technology (Machine Learning and Deep Learning, and More), Deployment Mode (Cloud, On-Premise, and More), End-User Vertical (BFSI, and More), Image Type (Static Images, and Video Frames/Live Stream), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Photoshopped Image Detection |

| Deepfake Image Detection |

| AI-Generated Image Detection |

| Real-Time Verification |

| Blockchain/Watermark Integrity Check |

| Machine Learning and Deep Learning |

| Image Processing and Analysis |

| Blockchain and Cryptographic Hashing |

| Computer Vision Accelerators (GPU, TPU, NPU) |

| Cloud |

| On-Premise |

| Edge / On-Device |

| BFSI |

| Government and Law-Enforcement |

| Defense and Intelligence |

| IT and Telecom |

| Media and Entertainment |

| Healthcare and Life Sciences |

| E-commerce and Retail |

| Other End-User Vertical |

| Static Images |

| Video Frames / Live Stream |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Software | ||

| Services | |||

| By Solution | Photoshopped Image Detection | ||

| Deepfake Image Detection | |||

| AI-Generated Image Detection | |||

| Real-Time Verification | |||

| Blockchain/Watermark Integrity Check | |||

| By Technology | Machine Learning and Deep Learning | ||

| Image Processing and Analysis | |||

| Blockchain and Cryptographic Hashing | |||

| Computer Vision Accelerators (GPU, TPU, NPU) | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| Edge / On-Device | |||

| By End-User Vertical | BFSI | ||

| Government and Law-Enforcement | |||

| Defense and Intelligence | |||

| IT and Telecom | |||

| Media and Entertainment | |||

| Healthcare and Life Sciences | |||

| E-commerce and Retail | |||

| Other End-User Vertical | |||

| By Image Type | Static Images | ||

| Video Frames / Live Stream | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the fake image detection market?

The fake image detection market is valued at USD 1.87 billion in 2026.

Which region is growing the fastest for fake-image detection solutions?

Asia Pacific is forecast to grow at a 32.47% CAGR through 2031, the highest worldwide.

Why are financial institutions accelerating adoption of deepfake detectors?

Face-swap fraud attempts have soared 2,137% in three years, pushing BFSI firms to upgrade KYC workflows.

How does the EU AI Act influence market demand?

The Act mandates labeling of AI-generated imagery and imposes fines up to EUR 35 million (USD 38 million), compelling European companies to integrate authenticity checks.

Page last updated on: