China Video Surveillance Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

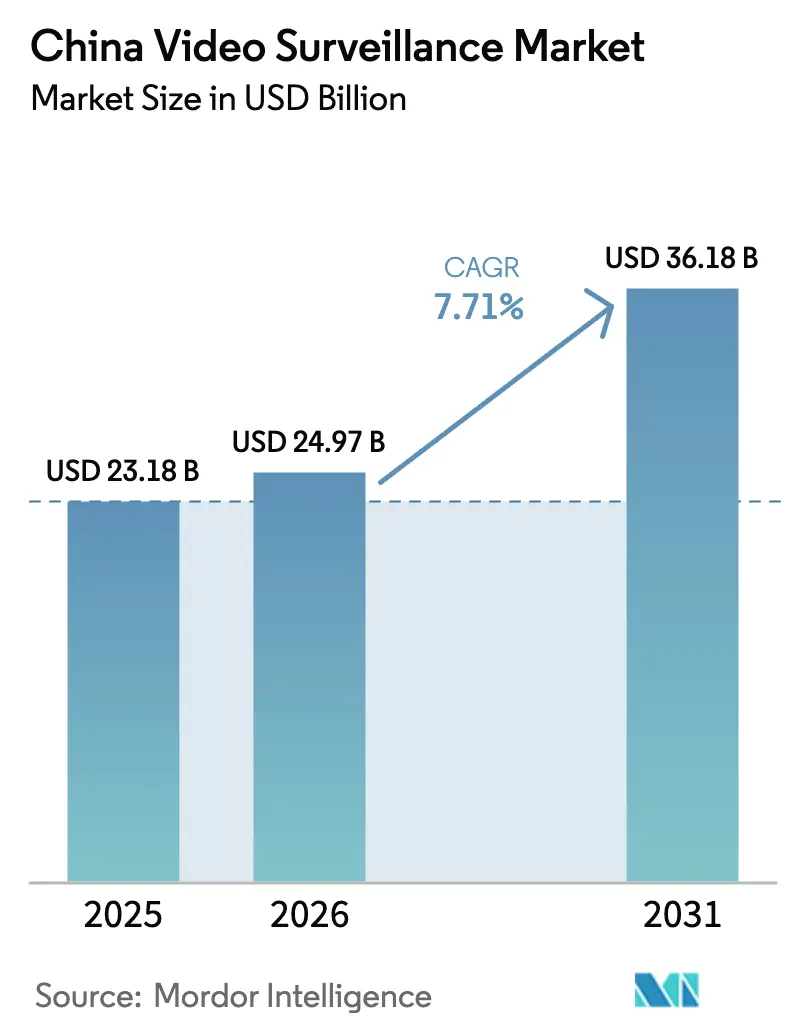

| Base Year Market Size (2025) | USD 23.18 Billion |

| Market Size (2026) | USD 24.97 Billion |

| Market Size (2031) | USD 36.18 Billion |

| Growth Rate (2026 - 2031) | 7.71% CAGR |

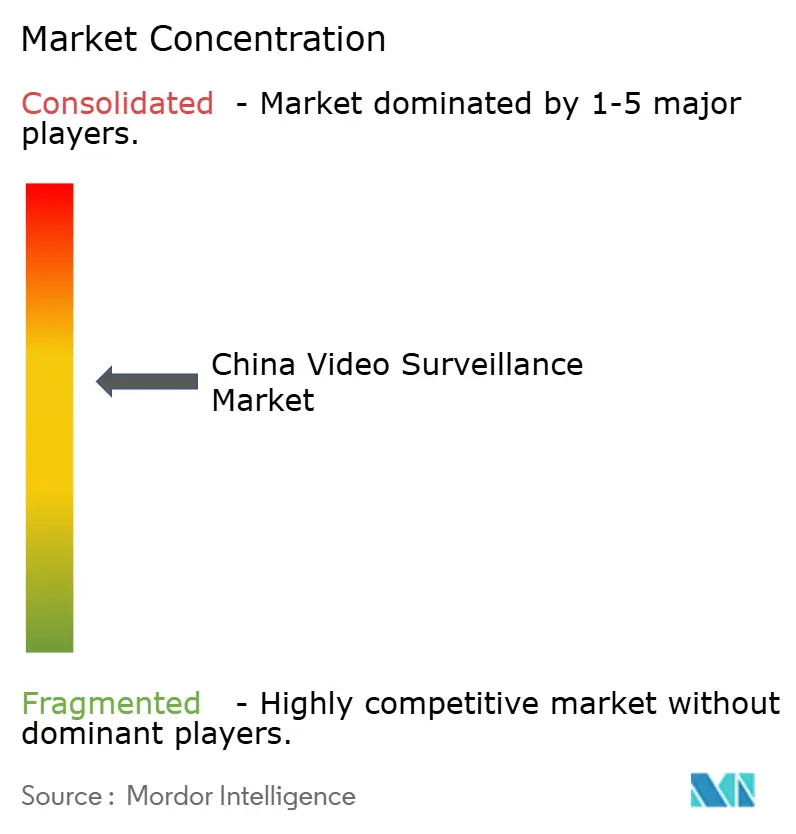

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Video Surveillance Market Analysis by Mordor Intelligence

The China video surveillance market size was valued at USD 23.18 billion in 2025 and estimated to grow from USD 24.97 billion in 2026 to reach USD 36.18 billion by 2031, at a CAGR of 7.71% during the forecast period (2026-2031). Robust government funding for safe-city programs, steady upgrades to higher-resolution cameras, and continued AIoT integration are keeping demand resilient even as hardware price competition intensifies.[1]Hangzhou Hikvision Digital Technology Co., Ltd., “2024 Annual Report,” cninfo.com.cn Domestic vendors are widening revenue streams through cloud-based VSaaS, smart retail analytics, and intelligent transportation systems, while rapid 5G roll-outs support wider use of wireless deployments. Stricter facial-recognition rules effective June 2025 are nudging suppliers toward privacy-enhancing technologies that comply with the new consent and data-protection mandates. At the same time, U.S. export controls on advanced chips are accelerating domestic semiconductor substitution, tempering near-term margins yet reinforcing long-term supply-chain resilience.

Key Report Takeaways

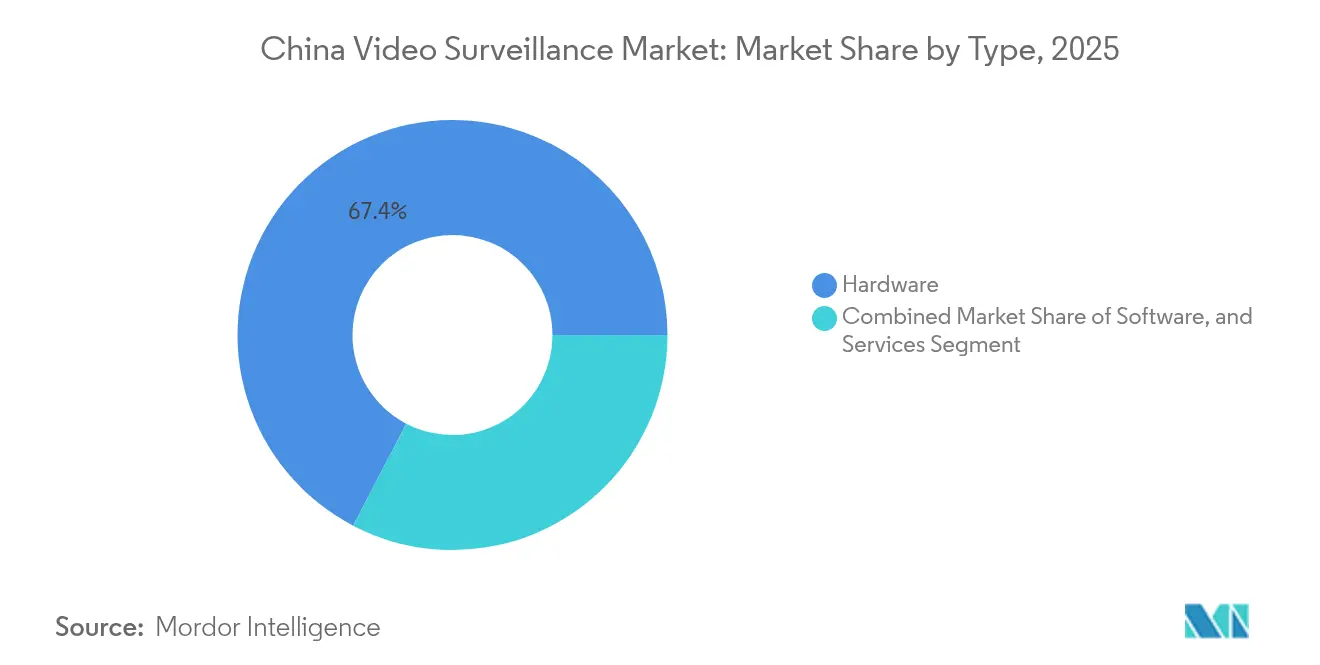

- By type, hardware led with 67.35% of China video surveillance market share in 2025, while VSaaS is projected to expand at a 9.35% CAGR to 2031.

- By application, city surveillance & public safety accounted for 43.55% of the China video surveillance market in 2025; residential deployments are advancing at an 8.38% CAGR through 2031.

- By camera resolution, Full HD devices commanded 35.45% share of the China video surveillance market size in 2025, whereas ≥4K cameras are growing at a 8.74% CAGR.

- By connectivity, wired systems retained an 83.25% share in 2025, yet wireless solutions are registering an 8.46% CAGR to 2031.

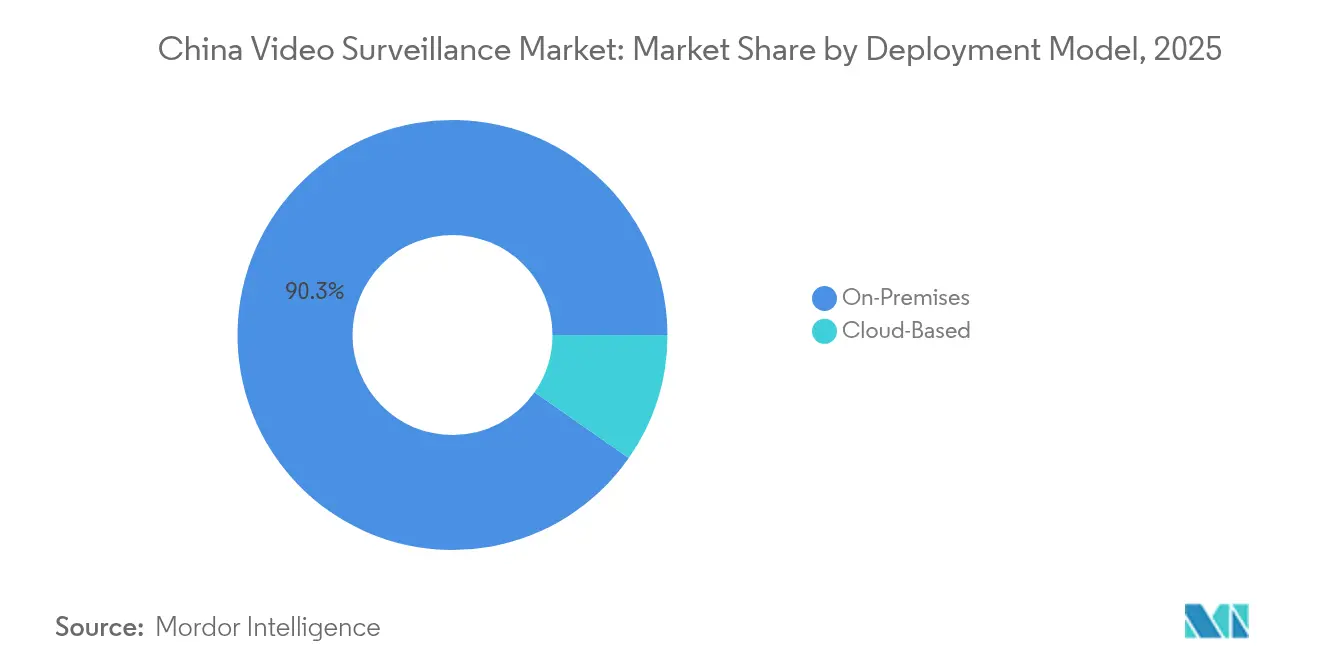

- By deployment model, on-premises architectures held 90.30% of the China video surveillance market in 2025, while cloud deployments are rising at a 9.12% CAGR.

- Hikvision, Dahua, and Uniview together controlled close to 58.85% of China video surveillance market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Video Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing urban safe-city initiatives backed by government funding | +2.1% | Nationwide, strongest in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Expansion of AI-powered smart cameras for real-time public surveillance | +1.8% | Nationwide, early adoption in eastern coastal provinces | Medium term (2-4 years) |

| Integration of video surveillance with city-wide IoT platforms | +1.5% | Major metros with advanced smart-city infrastructure | Long term (≥ 4 years) |

| Falling price per megapixel in domestic CMOS sensor production | +1.2% | Nationwide, production hubs in Shenzhen and Shanghai | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Urban Safe-City Initiatives Backed by Government Funding

Large-scale public-safety programs such as the Xueliang (Sharp Eyes) Project continue to anchor demand for the China video surveillance market. Nearly 800 smart-city pilots position the country as the single largest investor in video security infrastructure, with a cumulative spend topping USD 38.92 billion in 2023. Provincial roll-outs prioritize interlinking urban and rural camera networks, boosting coverage, and enabling unified command centers. Suppliers benefit from multi-year procurement frameworks that stabilize volume forecasts and de-risk R&D investments. The safe-city agenda increasingly spans traffic optimization and environmental monitoring, embedding cameras as core IoT sensors rather than stand-alone security devices. Such breadth broadens revenue pools beyond classical surveillance to data-driven civic operations services.

Expansion of AI-Powered Smart Cameras for Real-Time Public Surveillance

AI-enabled cameras are forecast to reach 63% of network-camera shipments by 2024, accelerating behavioral analytics and proactive incident response. Algorithms supplied by firms such as SenseTime and Megvii support facial, gait, and crowd-density analytics that shorten threat-identification cycles. Provincial police bureaus now budget for edge AI as a standard specification, raising the baseline ASP despite hardware commoditization. The formation of the China AI Safety & Development Association in 2025 is institutionalizing guardrails for responsible deployment, which should reinforce long-term adoption confidence among municipal buyers.[2]Concordia AI, "AI Safety in China #19", aisafetychina.substack.com

Integration of Video Surveillance with City-Wide IoT Platforms (e.g., OneNET)

China Mobile’s OneNET platform integrates more than 670 million IoT endpoints, including surveillance cameras, into a unified data layer. Seamless connectivity allows video feeds to inform traffic-signal algorithms, environmental sensors, and emergency-response systems. Cross-domain analytics unlock additional budget from city-management departments beyond public security, raising total addressable spend per city. Vendors embedding MQTT and LwM2M support into cameras accelerate plug-and-play onboarding to these municipal platforms.

Falling Price per Megapixel in Domestic CMOS Sensor Production

Local sensor makers such as SmartSens shipped 146 million CIS units for security cameras in 2020 and have since expanded capacity, pushing average camera prices down an estimated 15% in 2025.[3]EEWORLD, “SmartSens Lands on Sci-Tech Innovation Board,” eeworld.com.cnLower sensor cost enables ≥4K adoption in mid-tier segments and frees budgets for AI chipsets and analytics software. The price decline also supports the residential market, where consumers are highly price-sensitive yet increasingly favor higher definition for smart-home integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened public scrutiny over data privacy & facial recognition | –0.8% | Nationwide, stronger in tier-1 cities | Medium term (2-4 years) |

| U.S. Entity-List export controls restricting advanced chip supply | –0.6% | Nationwide, concentrated on high-end lines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Public Scrutiny over Data Privacy & Facial Recognition

The Security Management Measures for Facial Recognition Technology, effective June 2025, require explicit consent, alternative verification methods, and impact assessments, raising compliance complexity for commercial operators. Shanghai’s late-2024 enforcement campaign against unauthorized biometric capture illustrates stricter local oversight.[4]Biometric Update, “Shanghai Cracks Down on Facial Recognition Use by Businesses,” biometricupdate.com Vendors are responding with anonymization functions, on-device processing options, and privacy-masking algorithms to maintain project viability. Nevertheless, installation timetables for some retail and residential deployments are lengthening as legal reviews expand.

U.S. Entity-List Export Controls Restricting Advanced Chip Supply

Bans on advanced U.S. semiconductor technology constrain AI accelerators vital for real-time analytics in the China video surveillance market. Hikvision and Dahua have shifted design roadmaps toward domestic chipsets while pre-booking foundry capacity to mitigate supply risk. Short-term R&D expense and inventory buffers weigh on margins; however, the forced localization is fostering a domestic ecosystem of AI SoC suppliers, which could restore hardware autonomy over the long run.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Outpace Traditional Hardware

The hardware segment generated 67.35% of China video surveillance market revenue in 2025, reflecting enduring demand for cameras, NVRs, and specialized servers. Yet the services category, particularly VSaaS, is projected to grow 9.35% annually as enterprises favor subscription models that convert capex into opex and accelerate feature refresh cycles. Hanwha Vision’s May 2025 launch of the OnCloud platform exemplifies competitive intent to capture higher-margin recurring revenue.

Major incumbents are rebranding around “intelligent IoT” to signal strategic migration beyond commodity hardware. Innovative business lines overtook Hikvision’s core domestic sales for the first time in 2024, underscoring shifting profit pools. China video surveillance market size for services is forecast to narrow the revenue gap with hardware as AI analytics, device-health monitoring, and cybersecurity add-ons broaden VSaaS value propositions. Hardware vendors are countering commoditization by embedding edge AI modules and secure-boot chips that raise switching costs.

By Connectivity: Wireless Growth Challenges Wired Dominance

Wired solutions retained 83.25% share of the China video surveillance market in 2025 because reliability and bandwidth remain critical for public-safety grids and industrial facilities. Fiber backbones support lossless 4K transport and centralized storage architectures that many municipalities still prefer.

Wireless deployments, however, are expanding at an 8.46% CAGR, propelled by nationwide 5G coverage exceeding 800 million connections by end-2023 and poised to cross 1 billion in 2024. China video surveillance market size for wireless solutions is expected to accelerate as 5G-Advanced lowers latency and enhances uplink throughput, enabling camera installations in locations previously cost-prohibitive for trenching. Retail chains, rural townships, and temporary event venues favor LTE Cat.1 bis routers for cost-effective backhaul, proving wireless as an agile alternative during construction moratoriums or terrain constraints.

By Camera Resolution: 4K and Beyond Drives Premium Growth

Full HD cameras held 35.45% of the China video surveillance market in 2025, providing an optimal price-performance blend for mainstream deployments. The ≥4K segment, recording a 8.74% CAGR, is moving quickly into transportation hubs and casinos where analytics accuracy depends on pixel density. China video surveillance market size for ≥4K cameras benefits from domestic CIS price declines and HDR innovations that extend operational range under complex lighting.

Legacy ≤720p devices persist in legacy analog infrastructures, yet even cost-sensitive municipalities are planning phased upgrades tied to multiyear procurement cycles. Storage vendors are launching high-capacity, AI-ready arrays that blend NVMe tiers with cold archives to contain total cost of ownership as video data volume rises to zettabyte scale.

By Deployment Model: Cloud Adoption Accelerates Despite On-Premises Dominance

On-premises architectures accounted for 90.30% of China video surveillance market installations in 2025, driven by data-sovereignty mandates and stringent latency requirements for law-enforcement use cases. However, cloud models are growing 9.12% annually as telecom operators bundle compute, storage, and AI analytics into municipal smart-city projects. Hybrid topologies that offload inference to edge devices while archiving footage in regional data centers are gaining traction, meeting both responsiveness and compliance targets.

Subscription economics particularly resonate with SMEs seeking enterprise-grade analytics without capital-intensive server rooms. China video surveillance market share for cloud services is expected to rise as certification frameworks such as ETSI EN 303 645 reassure end users about cyber-hardening levels.

By Application: Residential Growth Complements Public-Safety Core

City surveillance & public safety projects represented 43.55% of China video surveillance market value in 2025 and remain the anchor segment under the Tianwang and Xueliang programs. Municipal deployments integrate cameras with license-plate recognition and traffic-signal control to optimize urban mobility while safeguarding public areas.

The residential category is the fastest-growing application with an 8.38% CAGR, fueled by bundled smart-home offerings from telecom operators and e-commerce platforms. Affordable 2K doorbells and battery-powered Wi-Fi cameras appeal to emerging middle-class homeowners seeking convenience and peace of mind. Commercial retail chains and logistics parks leverage analytics for queue management, heat-mapping, and inventory shrinkage reduction, broadening the use cases that underpin China video surveillance market demand beyond safety into operational intelligence.

Geography Analysis

Eastern coastal provinces—including Shanghai, Guangdong, and Jiangsu—constitute the epicenter of advanced deployments, supported by higher fiscal capacity and dense urbanization. Pilot adoption of ≥4K AI cameras and edge-cloud hybrid systems is most pronounced here, often setting reference standards later replicated nationwide. Local governments integrate police-cloud analytics with transportation and environmental datasets, yielding multi-department funding opportunities for suppliers.

Central and western provinces are narrowing the technology gap via the Xueliang Project’s mandate for unified urban-rural coverage, expanding surveillance grids into county seats and village committees. Funding packages tied to smart-city aspirations accelerate greenfield roll-outs that leapfrog legacy analog infrastructure, boosting incremental camera density and network-equipment orders.

Hong Kong, operating under a distinct regulatory regime, plans to add 2,000 new AI-ready cameras in 2024, raising deployment sophistication toward mainland standards while keeping privacy oversight mechanisms in place. Suppliers with proven experience in both jurisdictions enjoy a competitive edge in meeting nuanced procurement and compliance specifications.

Competitive Landscape

Market structure remains concentrated: Hikvision, Dahua, and Uniview collectively held almost 60% of China video surveillance market share in 2024. Hikvision reported RMB 92.5 billion (USD 12.85 billion) revenue but a 15.10% net-profit decline, intensifying its diversification into robotics and automotive electronics to regain margin headroom. Dahua’s RMB 717 million (USD 99.6 million) divestiture of its smart-home subsidiary re-focuses capital on core AIoT competencies, signaling portfolio rationalization in response to competitive saturation.

R&D intensity is the primary differentiator: Hikvision invested RMB 11.864 billion (USD 1.65 billion) in 2024, amassing over 10,580 patents that fortify barriers to entry and support premium positioning in AI chips and deep-learning frameworks. Emerging disruptors include niche AI-software vendors offering anonymization and cross-camera reidentification analytics that retrofit onto installed bases, eroding hardware lock-in. Strategic alliances between telecom carriers and platform vendors further alter channel dynamics, with integrated connectivity-plus-VSaaS bundles threatening traditional distributor margins.

China Video Surveillance Industry Leaders

-

Hangzhou Hikvision Digital Technology Co., Ltd.

-

Uniview Technologies Co., Ltd.

-

Sunell Technology Corporation

-

The Infinova Group

-

Zhejiang Dahua Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hanwha Vision launched OnCloud, a direct-to-cloud VSaaS platform that leverages AI search, mobile support, and multi-vendor camera compatibility, aligning with the market’s pivot toward service-centric revenue models

- April 2025: Hikvision’s Q1 revenue rose 4.01% year-over-year to RMB 18.532 billion, while net profit increased 6.41%, reflecting early gains from international diversification

- March 2025: China’s new facial-recognition rules took effect, prompting vendors to expedite privacy-enhancing features and tighten data-governance workflows

- March 2025: Dahua sold a 32.73% stake in Hangzhou Huacheng Network Technology for RMB 717 million, redeploying capital toward core AI R&D and enterprise verticals

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China video surveillance market as all revenue earned within mainland China from the sale, leasing, or subscription of security-focused cameras, recorders, video management software, analytics modules, and video-surveillance-as-a-service (VSaaS) solutions that feed live or recorded footage for safety, loss prevention, or operational monitoring. According to Mordor Intelligence, the base year is 2024, and the model tracks installed hardware, recurring cloud fees, and software licenses tied to those devices.

Scope Exclusions: Consumer webcams, dash-cams sold through retail, and broadcast television cameras are left out because they target personal entertainment or media creation rather than security.

Segmentation Overview

-

By Type

-

Hardware

-

Camera

- Analog

- IP Camera

- Hybrid

- Storage

-

Camera

-

Software

- Video Analytics

- Video Management Software

- Services (VSaaS)

-

Hardware

-

By Connectivity

- Wired

- Wireless

-

By Camera Resolution

- Standard Definition (≤720p)

- High Definition (720p-1080p)

- Full HD (1080p-2K)

- Ultra HD / 4K

- Above 4K

-

By Deployment Model

- On-Premises

- Cloud-Based

-

By Application

- City Surveillance and Public Safety

- Transportation and Traffic Management

- Commercial and Retail

- Industrial Facilities

- Institutional (Education and Healthcare)

- Residential

- Defense and Border Security

Detailed Research Methodology and Data Validation

Primary Research

Multiple in-depth interviews with municipal safe-city project managers, system integrators, component suppliers, and property-security directors across coastal, central, and western provinces allow us to test price bands, replacement cycles, and cloud adoption intent. These conversations let our team close data gaps found in desk work and fine-tune assumptions before final modeling.

Desk Research

We start by mining open data from tier-one agencies such as the National Bureau of Statistics of China, the Ministry of Public Security's procurement bulletins, China Customs shipment records, and provincial smart-city tenders, which together signal volumes and average selling prices. Trade associations like the China Security & Protection Industry Association, white papers from the Shanghai Municipal Security Technology Group, and peer-reviewed journals on computer vision provide insight into technology adoption curves.

Company filings, stock exchange disclosures, and reputable press archives gathered through D&B Hoovers and Dow Jones Factiva help Mordor analysts link financial performance with shipment trends, while patent alerts give early cues on pipeline innovation. The sources listed illustrate the breadth of material used; analysts review many additional publications for validation and context.

Market-Sizing & Forecasting

A top-down reconstruction begins with installed camera counts by setting, which are then aligned with government spending on public safety, urbanization ratios, and commercial floor-space completions. Select bottom-up checks, OEM shipment roll-ups, channel checks, and sampled ASP × unit math anchor the totals. Key variables include safe-city budget outlays, IP camera penetration, domestic CMOS price per megapixel, privacy-rule compliance costs, and export-control impacts. Forecasts use multivariate regression blended with ARIMA smoothing to project demand, while scenario analysis frames upside and downside around policy or technology shocks.

Data Validation & Update Cycle

Model outputs pass three levels of anomaly screening, variance checks against independent indicators, and peer review before sign-off. Reports refresh each year, and analysts trigger interim updates when material events, such as policy shifts, major tenders, or price shocks arise; a final validation sweep occurs immediately prior to client delivery.

Why Mordor's China Video Surveillance Baseline Inspires Confidence

Published estimates often diverge because firms pick different product baskets, price ladders, or refresh cadences, and because they convert yuan to dollars at varied rates.

Key gap drivers include differing treatment of VSaaS fees, whether smart-analytics modules are booked as software or hardware, and how aggressively each publisher rolls forward post-COVID replacement demand. Mordor's disciplined scope selection and annual refresh lower those variances.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.18 B (2025) | Mordor Intelligence | |

| USD 7.08 B (2024) | Global Consultancy A | Hardware-only scope and older base year exclude VSaaS and analytics revenues |

| USD 41.21 B (2024) | Industry Association B | Counts broadcast cameras and assumes aggressive pricing escalation with limited primary validation |

The comparison shows that while others skew low by omitting service income or skew high by folding in adjacent devices, Mordor's balanced view stays traceable to clear variables, refreshed data, and repeatable steps, giving decision-makers a steadier baseline.

Key Questions Answered in the Report

What is the current size of the China video surveillance market?

The market stands at USD 24.97 billion in 2026 and is projected to reach USD 36.18 billion by 2031.

Which segment is expanding fastest in the China video surveillance market?

Cloud-based Video Surveillance as a Service is growing at a 9.35% CAGR as organizations favor subscription models with embedded analytics.

How are new facial-recognition regulations influencing suppliers?

Vendors are enhancing privacy-masking, on-device processing, and consent-management workflows to comply with rules effective June 2025.

Why are ≥4K cameras gaining momentum?

Falling domestic sensor costs and the need for higher-resolution data to power AI analytics are driving a 8.74% CAGR in this premium segment

What competitive strategies are leading firms adopting?

Market leaders are diversifying into AIoT services, robotics, and automotive electronics while ramping R&D spending to protect technological advantage.

How will U.S. export controls impact China’s video surveillance supply chain?

The restrictions are squeezing near-term margins but catalyzing accelerated investment in local AI chip design and alternative component sourcing.

Page last updated on: