Zero-emission Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 8.29 Billion |

| Market Size (2031) | USD 10.25 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zero-emission Aircraft Market Analysis by Mordor Intelligence

The zero-emission aircraft market size is expected to grow from USD 7.54 billion in 2025 to USD 8.29 billion in 2026 and is forecasted to reach USD 10.25 billion by 2031 at a 4.34% CAGR over 2026-2031. Momentum is shifting from demonstrations to scalable production as hydrogen-electric propulsion nears type certification pathways and battery-electric platforms gain range and turnaround capabilities. However, high fuel cell power density, cryogenic storage certification, and airport refueling infrastructure remain gating items for large-scale deployment. Airframe OEMs are still sequencing capital between SAF-readiness and hydrogen or electric architecture. Yet, the program's intent remains visible, as Airbus highlights a fuel-cell concept with four 2 MW electric propulsion engines and targets service in the second half of the 2030s.

Key Report Takeaways

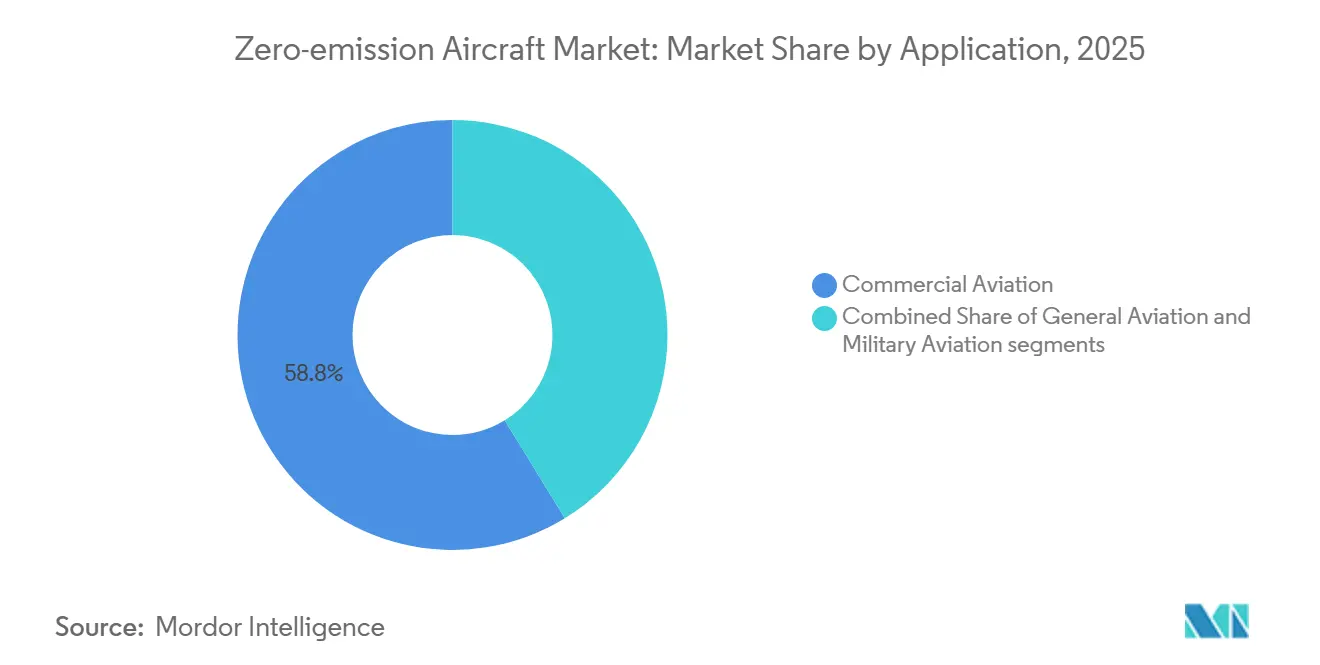

- By application, commercial aviation led the zero-emission aircraft market with a 58.75% revenue share in 2025, and general aviation is projected to grow at a 6.54% CAGR through 2031.

- By propulsion technology, hybrid electric held 46.21% share of the zero-emission aircraft market in 2025, while hydrogen is forecasted to expand at a 9.34% CAGR through 2031.

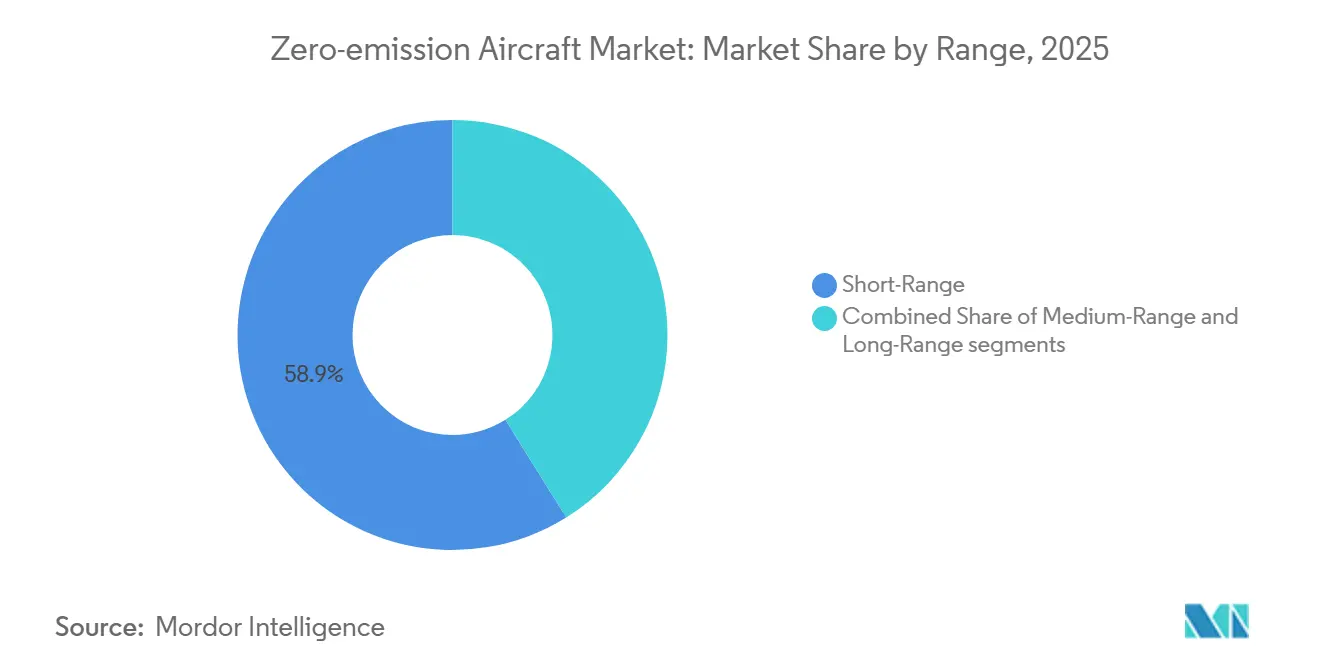

- By range, short-range accounted for a 58.87% share of the zero-emission aircraft market in 2025, while medium-range is advancing at a 6.21% CAGR through 2031.

- By aircraft type, fixed-wing represented a 43.22% share of the zero-emission aircraft market in 2025, while unmanned aerial systems are growing at a 7.95% CAGR through 2031.

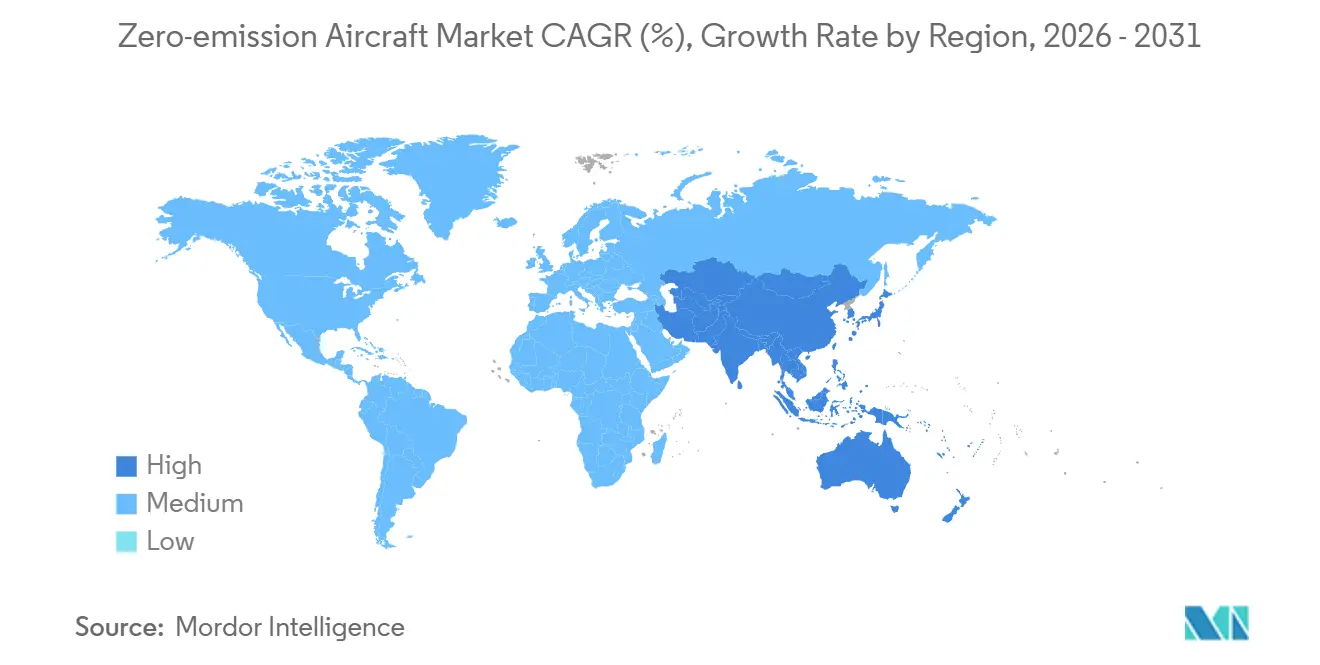

- By geography, North America commanded a 31.54% share of the zero-emission aircraft market in 2025, while the Asia-Pacific is the fastest-growing region at a 6.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Zero-emission Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in hydrogen fuel cell power systems for aviation | +1.2% | Global, with early gains in North America, Europe, and Japan | Medium term (2-4 years) |

| Global policy momentum behind green hydrogen aviation infrastructure | +1.0% | Europe, North America, and Asia-Pacific | Short term (≤ 2 years) |

| Breakthroughs in next-generation high-energy-density aviation batteries | +1.1% | Global with supply chain nodes in US, Europe, and Asia | Medium term (2-4 years) |

| Sustainable aviation fuel mandates accelerating zero-emission aircraft development | +0.8% | Europe, UK, Asia-Pacific, South America | Short term (≤ 2 years) |

| Rising public-private investments in airport-based hydrogen production facilities | +0.7% | Europe, North America, Middle East | Medium term (2-4 years) |

| Regulatory and economic incentives favoring low-noise electric propulsion technologies | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements in Hydrogen Fuel Cell Power Systems for Aviation

Airbus validated a 1.2 MW integrated hydrogen propulsion system and showcased a notional configuration with two liquid hydrogen tanks feeding four 2 MW electric propulsion engines, clarifying a system architecture targeting entry in the second half of the 2030s.[1]Airbus Communications, “Airbus Showcases Hydrogen Aircraft Technologies During Its 2025 Summit,” Airbus, airbus.com The FAA’s Hydrogen-Fueled Aircraft Roadmap outlines hazard analysis focus through 2028 and policy readiness by 2028-2032 for fuel cells and hydrogen-burning turbines, anchoring the regulatory arc for type certification of hydrogen-electric powertrains. ZeroAvia secured the FAA’s first G‑1 issue paper for a 600 kW hydrogen-electric system and targets initial service on 10-20 seat aircraft, signaling a practical near-term route for commuter retrofits within the zero-emission aircraft market.[2]ZeroAvia Team, “Advancing Hydrogen Aviation in 2025 – The 4 Pillars of Success,” ZeroAvia, zeroavia.com Europe’s Clean Aviation Joint Undertaking has embedded hydrogen-electric thrust into multi-year programs that support scalable stacks, thermal management, and integration methods compatible with retrofit and clean-sheet designs. These developments consolidate fuel cells as the priority pathway for medium-range missions where battery weight limits are binding, given hydrogen’s higher gravimetric energy density.

Global Policy Momentum Behind Green Hydrogen Aviation Infrastructure

The FAA’s hydrogen roadmap sets a staged plan for safety assessments through 2028 and policy readiness by 2028-2032 across fuel cells, hydrogen-burning turbines, and hybrid architectures, offering a structured path for technology adoption. EASA’s corresponding roadmap anticipates regional aircraft entry for hydrogen concepts between 2030 and 2040 and broader commercial deployment in the 2040-2050 window, which helps align transatlantic standards. The EU has earmarked significant capital to scale the hydrogen economy, including a hydrogen auction under the European Hydrogen Bank, with earmarked off-take categories for aviation and maritime. The US regional funding initiatives, such as the ARCHES hydrogen hub, are mobilizing airport-adjacent production, logistics, and refueling pilots that link federal support to state-led buildouts. Airport-side initiatives continue to expand through OEM-led partnerships that scope fueling concepts and operational procedures in advance of aircraft entry into service in the zero-emission aircraft market. This policy, along with the momentum in infrastructure, reduces program risk premiums for fuel-cell and hydrogen-turbine programs by clarifying the design and operational envelopes.

Breakthroughs in Next-Generation High-Energy-Density Aviation Batteries

Cell-level energy density of 400 Wh/kg has reached flight programs, as demonstrated by MagniX’s Samson Battery, which offers a doubled range potential compared with many prior-generation electric aircraft systems. These advancements enhance operational capabilities for battery-electric trainers, air taxis, and regional feeders, emphasizing quick turnaround times and consistent duty cycles in zero-emission aviation. Product architectures that blend electric propulsion and range extenders are maturing in parallel, enabling operators to deploy electric for short legs and hybrid modes for longer stages. Airframers continue to emphasize systems integration, thermal management, and charging protocols that standardize ground operations across varied airfields and vertiports.

Sustainable Aviation Fuel Mandates Accelerating Zero-Emission Aircraft Development

ReFuelEU Aviation requires SAF blending that rises from an initial target to steep long-term thresholds by 2050, which anchors operator compliance planning and accelerates parallel investments in both SAF and zero-emission platforms. The UK has set a formal SAF mandate with clear milestones for 2030 and 2040, nudging airlines and airports to allocate capital for fuel logistics and offtake agreements. Engine OEMs have responded by certifying fleets to operate on 100% SAF blends, which supports near-term decarbonization while longer-term hydrogen and electric architectures mature. Recent analysis by industry partners indicates that targeted hydrogen infrastructure in a limited set of major EU hubs could yield substantial emissions reductions relative to a business-as-usual trajectory, further strengthening the case for fuel-cell platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited availability of certified aerospace-grade liquid hydrogen cryotanks | -0.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| High volatility in raw material prices for advanced battery chemistries | -0.5% | Global with concentration risks in Asia-Pacific | Short term (≤ 2 years) |

| Lengthy certification timelines for novel electric and hydrogen propulsion systems | -0.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Widespread use of drop-in sustainable aviation fuels delaying zero-emission investments | -0.4% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Certified Aerospace-Grade Liquid Hydrogen Cryotanks

Liquid hydrogen must be stored at near minus 253 degrees Celsius and requires more than four times the volume of conventional jet fuel for the same energy content, which forces dedicated tank designs and new aircraft layouts rather than traditional wet wings. Materials and structural performance requirements are stringent because tanks must endure repeated pressure and temperature cycles across years of service without microcracking or unacceptable boil-off losses. EASA’s staged hydrogen roadmap reflects the complexity of end-to-end systems integration, with regional entry projected between 2030 and 2040 and broad deployment in later decades. These gaps increase capital requirements for test articles, ground tanks, and operational prototypes, slowing platform certification and airport approvals for the zero-emission aircraft market. As cryotank standards converge, retrofit kits and clean-sheet designs can scale with lighter, longer-life tanks that preserve payload and turnaround economics.

High Volatility in Raw Material Prices for Advanced Battery Chemistries

Lithium demand grew sharply in 2024, while refining capacity remained concentrated in a small number of countries, increasing exposure to policy and trade disruptions that can quickly alter cost curves. The top refining hubs expanded their share of global processing, and supply chain concentration raised the risk of price swings that complicate aircraft program business cases. Export controls and short-term supply suspensions in critical minerals underscore how procurement shocks can ripple into pack prices and delivery schedules. Aviation-grade cells require higher energy density and tighter quality controls than typical EV packs, which limits the ability to offset spikes with commodity-grade substitutions. Developers in the zero-emission aircraft market often rely on bespoke formats and chemistries to meet certification and performance targets, which dampens economies of scale compared with those in the automotive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Fleet Renewal Cycles Propel Commercial Adoption

Commercial aviation accounted for the largest portion of the zero-emission aircraft market in 2025, with a 58.75% share, reflecting airline fleet renewal cycles and decarbonization plans that prioritize certified platforms in the late 2020s and early 2030s. Regional carriers have anchored early adoption through commitments to 30-seat hybrid-electric aircraft, with electric for short-haul segments and hybrid for extended stages to sustain dispatch reliability. Airbus continues to refine a fuel-cell architecture with four 2 MW electric propulsion engines and a two-tank liquid hydrogen layout as a pathway for later deployment, creating an option set for airlines that need long-term line-fit solutions.

General aviation is forecast to grow at a 6.54% CAGR through 2031, supported by flight schools, charter, and owner-operators that value low operating costs and noise reduction for frequent short missions. Battery-electric models have demonstrated passenger operations and flight endurance suited to typical training sorties, and these use cases help validate maintenance cycles, charging routines, and airfield logistics. The zero-emission aircraft industry will witness sustained demand from public services, including emergency response and medical flights, prioritizing quiet operations and shorter stage lengths for efficient functionality. Over time, the adoption of general aviation will feed data back into regional platforms on battery performance, thermal stability, and charging throughput.

By Propulsion Technology: Hybrid Electric Bridges Near-Term Gaps, Hydrogen Targets Longer Ranges

Hybrid electric held 46.21% of the zero-emission Aircraft market share in 2025, reflecting near-term retrofits and conversions that use electric motors for takeoff and climb while maintaining extended range through turbine-based generation. Clean aviation programs continue to support hybrid demonstrators that de-risk the integration of propellers, electric machines, power electronics, and thermal management for regional aircraft. Applications where runway length, noise, and local air quality drive airport constraints favor hybrids in the near term, as they offer strong takeoff performance and lower noise without relying on hydrogen infrastructure. FAA type certification pathways for Part 23 commuter-class aircraft progress from hybrid demonstrations to commercial deployment, guiding supplier and operator strategies.

Hydrogen propulsion is projected to expand at a 9.34% CAGR through 2031, supported by its higher gravimetric energy density compared to batteries and rapid refueling cycles that help preserve aircraft utilization on medium-range routes. ZeroAvia’s program milestones, including the first FAA G‑1 issue paper for a 600 kW hydrogen-electric system and a growing engine order pipeline, position fuel cells for 10-20 seat aircraft first, with larger stacks targeting the 40-80 seat class next. Airbus has validated a megawatt-class fuel cell system and outlined a concept featuring four 2 MW electric propulsion engines powered by liquid hydrogen tanks, establishing precise performance benchmarks to guide suppliers in meeting technical specifications. Fully electric propulsion will remain central in urban and short-range regional networks where energy density and ground charging throughput can support high-frequency mission cycles.

By Range: Short-Range Dominates, Medium-Range Accelerates

Short-range flights accounted for 58.87% of the zero-emission aircraft market in 2025, matching the performance envelope of current battery and hydrogen systems for regional aviation and urban air mobility. Thirty-seat hybrid-electric designs, such as the ES‑30, combine a pure-electric mode for shorter legs and a hybrid mode for extended stages to preserve dispatch flexibility across varied airports. Demonstrations of passenger-carrying electric flights at major airports reinforce realistic turnaround times, ground procedures, and safety case development for short sectors. Air taxi architectures emphasize short lanes and quick cycles, which magnify the operational benefits of lower noise and fewer moving parts inherent in electric propulsion within the zero-emission aircraft market.

Medium-range aircraft are expected to advance at a 6.21% CAGR through 2031 as liquid hydrogen validation supports regional turboprop displacement and eventually single-aisle missions. Fuel-cell propulsion’s higher gravimetric energy density and rapid refueling align with turnaround economics on regional networks that cannot accept long charging times. Developers of multi-megawatt stacks and cryogenic storage are prioritizing integration steps that enable engines in the 2 MW class to support 40-80 seat platforms. Advancements in tanks, stacks, and thermal systems are driving larger cabins and extended ranges in the zero-emission aircraft market. Hydrogen combustion or SAF will support long-range missions until energy density improvements and optimized aircraft configurations enable scalable zero-emission propulsion for intercontinental operations.

By Aircraft Type: UAS Growth Outpaces Fixed-Wing Leadership

Fixed-wing platforms held 43.22% of the zero-emission aircraft market in 2025, led by commuter and regional programs that can incorporate hybrid or hydrogen-electric propulsion with defined certification paths. FAA roadmaps and industry demonstrations target commuter-class aircraft to validate the reliability of megawatt-class systems and optimize thermal management for daily operational cycles. As energy storage and fuel cell performance improve, fixed-wing platforms can scale in cabin size while preserving payload and range against operational targets. The zero-emission aircraft industry is also leveraging crossover components from general aviation, where proof points in charging throughput and cycle life reduce system risks. These elements make fixed-wing a natural anchor for early adoption while infrastructure scales.

Unmanned aerial systems (UAS) are projected to grow at a 7.95% CAGR through 2031, propelled by missions that value long endurance, low acoustic signatures, and reduced thermal emissions. Hydrogen fuel cells can extend small drone endurance by multiple times that of batteries, expanding their roles in surveillance, inspection, and emergency response. Electric architectures simplify maintenance and system health monitoring, advantages that translate into higher availability for high-tempo missions. As regulatory frameworks evolve for beyond-visual-line-of-sight operations, UAS platforms will benefit from safety cases developed in crewed commuter programs.

Geography Analysis

North America held 31.54% of the zero-emission aircraft market in 2025, supported by clear certification roadmaps and active demonstrations that align technology readiness with commuter-class deployments. FAA guidance on hydrogen-fueled aircraft frames hazard analysis and risk mitigation through the decade, which helps align OEM and operator test campaigns. Demonstrations of passenger electric flights at major US airports show the operational feasibility of near-term services for training, charter, and short regional missions. Boeing’s sustainability disclosures confirm a heavy focus on SAF use across operations, which complements rather than replaces zero-emission propulsion R&D. Integrating SAF and zero-emission pilots enables carriers and airports to ensure compliance while strategically planning mid-term hydrogen and hybrid transitions for priority routes in the zero-emission aircraft market.

Asia-Pacific is the fastest-growing region, with a projected 6.82% CAGR through 2031, driven by investments in hydrogen programs and electrified aircraft initiatives alongside high-growth air traffic markets. Regional carriers and airports are testing electric operations in urban and island networks where shorter legs and frequent cycles align with the strengths of electric propulsion. Over the forecast period, Asia-Pacific’s buildout of hydrogen and charging ecosystems will drive a steady ramp from pilot services to early commercial missions in the zero-emission aircraft market.

Europe continues to make consistent contributions to adoption through ambitious climate targets and public funding under EU programs that prioritize hydrogen and hybrid demonstrators for regional fleets.[3]Clean Aviation Programme Office, “Work Programme and Budget 2024–2025,” Clean Aviation Joint Undertaking, clean-aviation.eu ReFuelEU Aviation sets a rising SAF baseline that aligns near-term decarbonization with medium-term zero-emission entry, while member states and airports explore hub-based hydrogen deployment. Airbus’s hydrogen concept work and airport partner initiatives indicate that scalable deployment will follow standards convergence and infrastructure readiness. European industry initiatives are also shaping component supply chains for tanks, stacks, and power electronics that feed into aircraft programs across the zero-emission aircraft market.

Competitive Landscape

Industry incumbents and specialists are advancing along different paths as SAF adoption ramps while hydrogen-electric and hybrid-electric programs move through certification. Airbus reported increased R&D in 2025 and continues to fund hydrogen concepts integrating megawatt-class fuel cell stacks, reinforcing its intent to bring a fuel-cell-powered aircraft into service in the second half of the 2030s. The Boeing Company emphasized the use of SAF across its operations. It sustained R&D as shown in its annual filings and sustainability disclosures, signaling a dual-track approach that supports near-term decarbonization while tracking zero-emission propulsion.

Specialists are concentrating on modular propulsion architectures that scale across commuter and regional classes. ZeroAvia achieved the FAA’s first G‑1 issue paper for a 600 kW hydrogen-electric powertrain, continued to build an engine order pipeline, and expanded manufacturing capability for fuel cell systems and stacks, which together support initial 10-20 seat entries.

Technology partnerships are capturing key building blocks, such as cell-level energy density, power electronics, and thermal systems. MagniX’s 400 Wh/kg cell-level battery announcement highlights how propulsion integrators can extend electric stage lengths for commuter routes. As airframers and system providers align on certification evidence, they are building de facto standards for operations, charging, and refueling that new entrants must match to compete in the zero-emission aircraft market.

Zero-emission Aircraft Industry Leaders

The Boeing Company

ZeroAvia, Inc.

Heart Aerospace AB

Airbus SE

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Surf Air Mobility Inc., a prominent player in the air mobility sector, announced an Aircraft Purchase Agreement with BETA Technologies, an innovator in electric aerospace. This strategic alliance aims to fast-track the rollout of advanced air mobility solutions that prioritize safety, reliability, and profitability. As per the agreement, Surf Air Mobility has placed a firm order for 25 all-electric ALIA CTOL aircraft, with an option to expand the order by an additional 75 aircraft. These aircraft are set to bolster Surf Air Mobility's regional operations.

- June 2025: ZeroAvia received a Small Business Innovation Research (SBIR) grant from AFWERX to study the integration of hydrogen propulsion and advanced automation technology in Cessna Caravan aircraft, as part of AFWERX's program to address research priorities related to critical challenges within the Department of the Air Force (DAF).

- March 2025: ZeroAvia received a Small Business Innovation Research (SBIR) grant from AFWERX to study the integration of hydrogen propulsion and advanced automation technology in Cessna Caravan aircraft, as part of AFWERX's program to address research priorities related to critical challenges within the Department of the Air Force (DAF).

Global Zero-emission Aircraft Market Report Scope

The aviation sector is investing in green technology. A global effort is underway, with international airlines pouring millions into innovations being developed by green tech pioneers. Zero-emission aircraft is one such concept that has gained popularity recently.

The zero-emission aircraft market is segmented by application, propulsion technology, range, aircraft type, and geography. By application, the report is segmented into commercial aviation, general aviation, and military aviation. By propulsion technology, the market is segmented into hydrogen, hybrid electric, and fully electric. By range, the market is segmented into short-range, medium-range, and long-range. By aircraft type, the market is segmented into fixed-wing, rotorcraft, unmanned aerial systems, and regional turboprop/turbofan. The report also covers the market sizes and forecasts in major regions. For each segment, the market size is provided in terms of value (USD).

| Commercial Aviation |

| General Aviation |

| Military Aviation |

| Hydrogen |

| Hybrid Electric |

| Fully Electric |

| Short-Range |

| Medium-Range |

| Long-Range |

| Fixed-Wing |

| Rotorcraft |

| Unmanned Aerial Systems |

| Regional Turboprop/Turbofan |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| Rest of Europe | ||

| France | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Commercial Aviation | ||

| General Aviation | |||

| Military Aviation | |||

| By Propulsion Technology | Hydrogen | ||

| Hybrid Electric | |||

| Fully Electric | |||

| By Range | Short-Range | ||

| Medium-Range | |||

| Long-Range | |||

| By Aircraft Type | Fixed-Wing | ||

| Rotorcraft | |||

| Unmanned Aerial Systems | |||

| Regional Turboprop/Turbofan | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| Rest of Europe | |||

| France | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the Zero Emission Aircraft market?

The zero-emission aircraft market size was USD 7.54 billion in 2025 and is projected to reach USD 10.25 billion by 2031 at a 4.34% CAGR, reflecting a shift from demonstrations to early commercial deployment.

Which propulsion approach is growing the fastest in zero-emission aviation?

Hydrogen propulsion is projected to expand at a 9.34% CAGR through 2031 due to high gravimetric energy density and rapid refueling that fits regional and medium-range missions.

Which applications lead adoption today?

Commercial aviation led with 58.75% share in 2025, while general aviation is growing at 6.54% CAGR as training and charter missions validate electric and hybrid operations.

What ranges are most viable for near-term deployment?

Short-range flights account for 58.87% of 2025 demand, supported by battery and hybrid systems, while medium-range is advancing at a 6.21% CAGR as hydrogen-electric systems mature.

Which regions are leading and which are accelerating fastest?

North America held 31.54% share in 2025 due to certification clarity and demonstrations, while Asia-Pacific is the fastest growing region at a 6.82% CAGR through 2031.

What policy factors are shaping the pace of zero-emission aircraft deployment?

FAA and EASA hydrogen roadmaps, EU SAF mandates under ReFuelEU, and targeted airport hydrogen pilots are defining certification, operations, and infrastructure paths that reduce program risk.

Page last updated on: