Autonomous Aircraft Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.70 Billion |

| Market Size (2031) | USD 27.99 Billion |

| Growth Rate (2026 - 2031) | 21.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

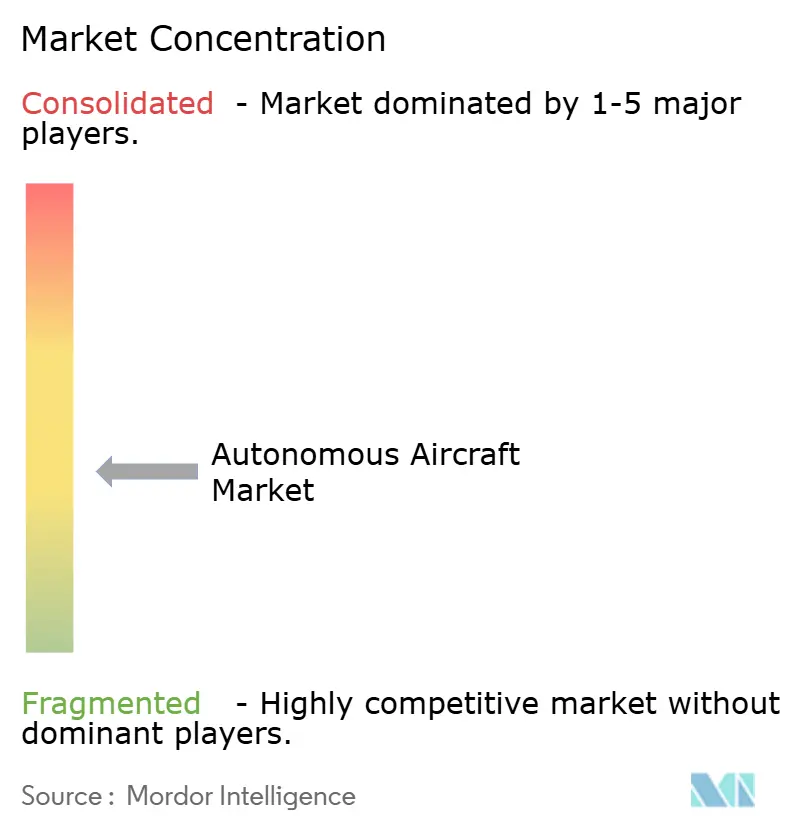

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Aircraft Market Analysis by Mordor Intelligence

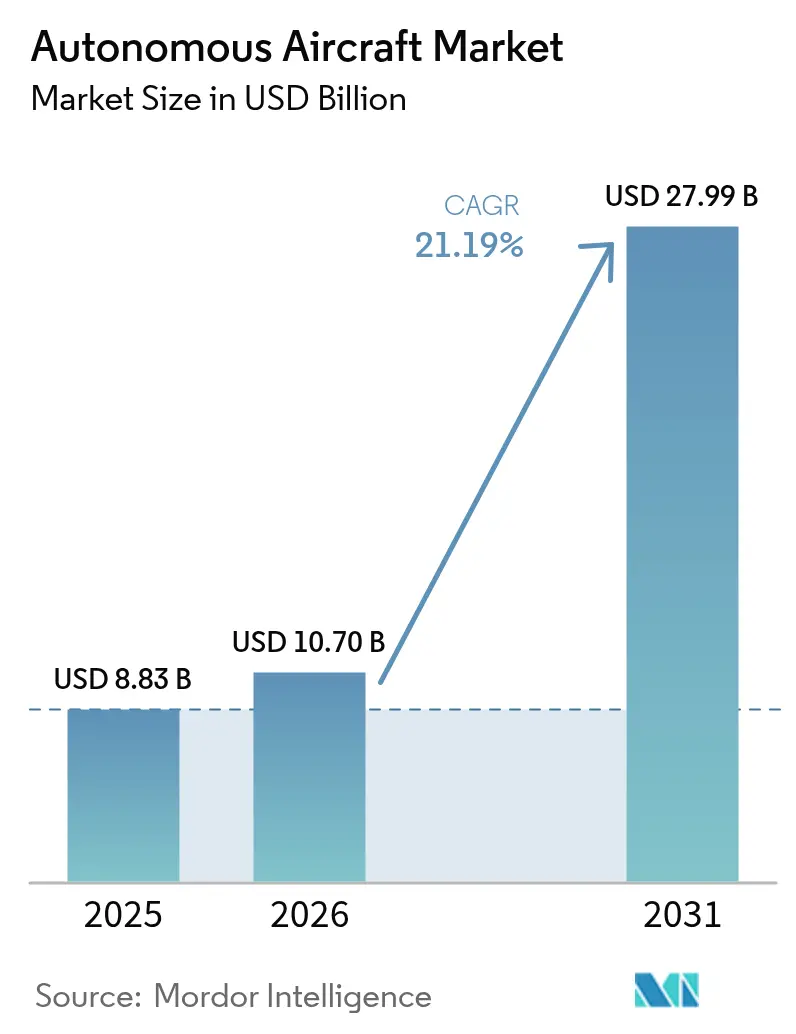

The autonomous aircraft market size was valued at USD 8.83 billion in 2025 and estimated to grow from USD 10.7 billion in 2026 to reach USD 27.99 billion by 2031, at a CAGR of 21.19% during the forecast period (2026-2031). A wave of defense modernization, urban mobility plans, and logistics automation is reshaping aviation economics and elevating demand for progressively self-directed platforms. Fixed-wing configurations command present dominance, yet hybrid fixed-wing VTOL aircraft lead the growth curve, reflecting airlines’ and militaries’ preference for versatile mid-range solutions. Rapid investments by defense agencies in collaborative combat aircraft and ISR drones accelerate technology readiness. At the same time, urban air mobility (UAM) programs foster beyond-visual-line-of-sight corridors and vertiport construction. Deepening AI integration helps unlock fully autonomous operations and widens the addressable envelope across cargo, passenger, and special-mission use cases. Conventional turbine engines remain the primary propulsion base, but hydrogen fuel-cell and advanced electric systems draw rising capital as sustainability mandates tighten.

Key Report Takeaways

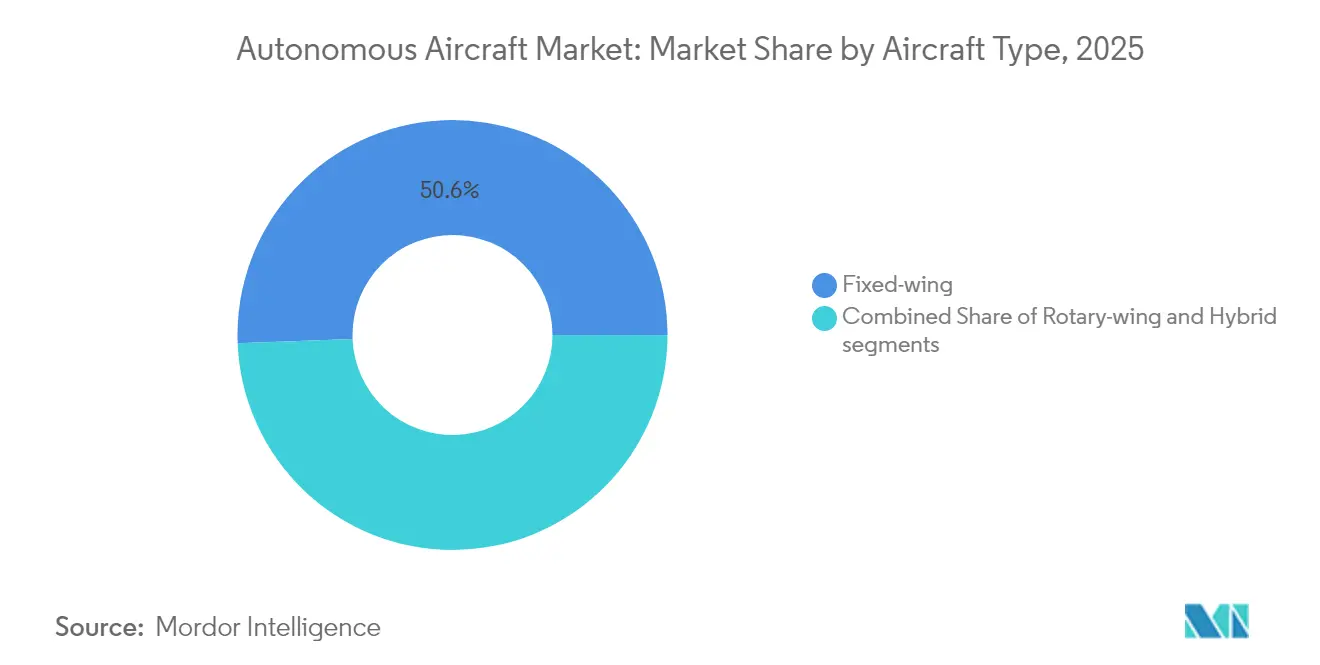

- By aircraft type, fixed-wing platforms led 50.62% of the autonomous aircraft market share in 2025, while hybrid fixed-wing VTOL systems are forecasted to expand at a 26.12% CAGR through 2031.

- By autonomy level, increasingly autonomous systems held 67.78% of the autonomous aircraft market size in 2025; fully autonomous platforms are advancing at a 26.96% CAGR to 2031.

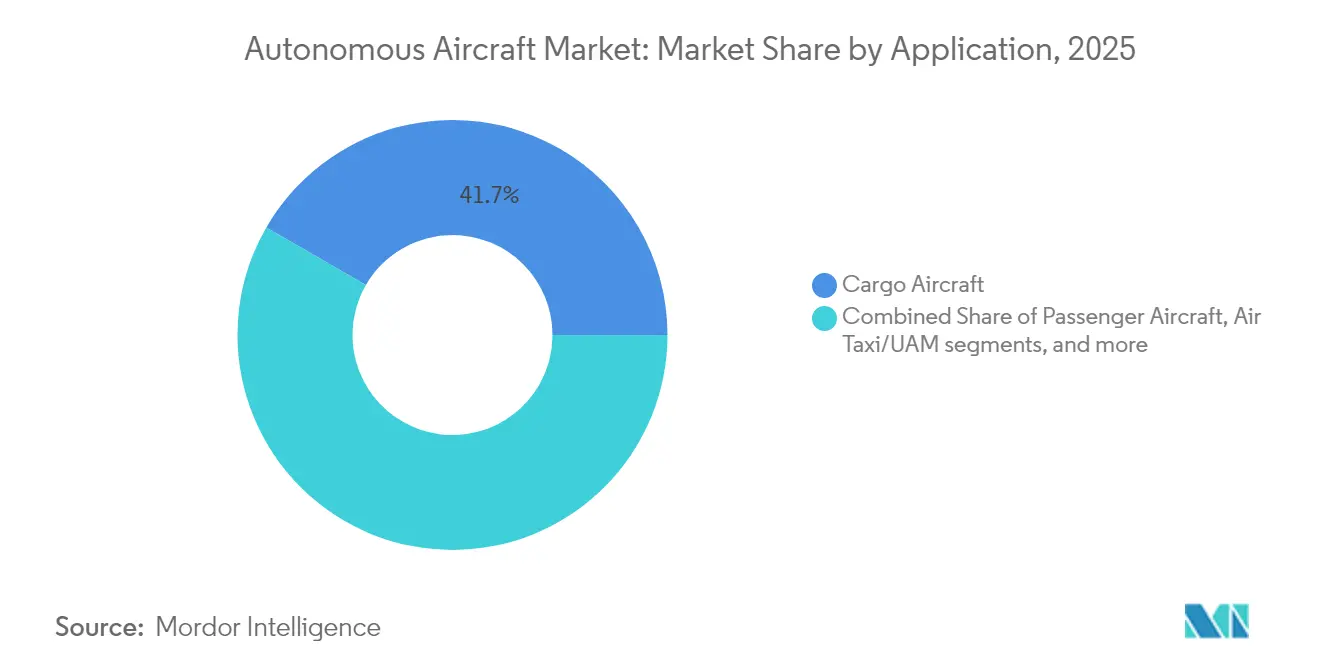

- By application, cargo aircraft accounted for a 41.67% share of the autonomous aircraft market size in 2025, yet air-taxi and UAM services record the highest projected CAGR at 28.45% during 2026-2031.

- By propulsion type, conventional turbines commanded 55.54% revenue share in 2025, whereas hydrogen fuel-cell systems are projected to grow at a 31.17% CAGR to 2031.

- By component, sensors and navigation suites led with a 27.74% share in 2025, while software and AI algorithms are growing at a 25.55% CAGR to 2031.

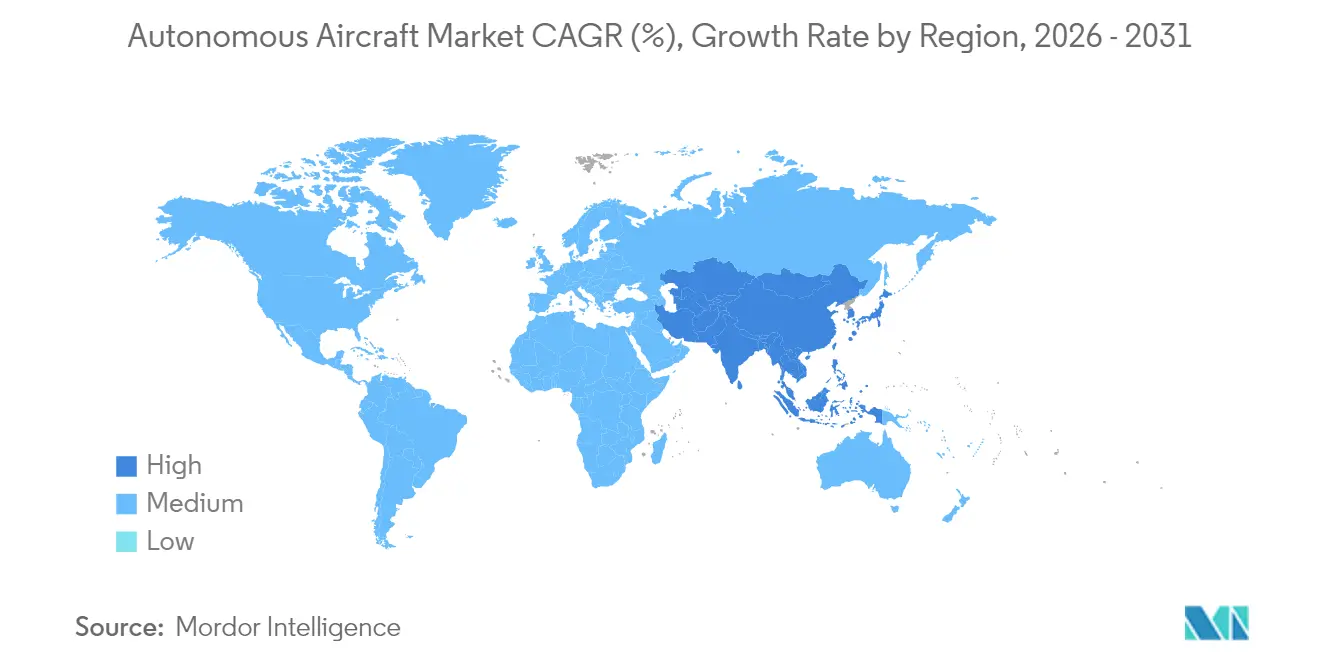

- By geography, North America held a 36.74% share in 2025; Asia-Pacific is forecasted to post a 23.92% CAGR, making it the fastest-growing regional cluster.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autonomous Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in AI-driven flight control systems | +4.2% | North America, China | Medium term (2-4 years) |

| Rapid growth in Urban Air Mobility (UAM) and eVTOL adoption | +3.8% | North America, Europe, accelerating in APAC | Medium term (2-4 years) |

| Cost reduction incentives for logistics via autonomous cargo drones | +3.1% | Global, early operations in North America and Europe | Short term (≤ 2 years) |

| Increased military investments in ISR and combat autonomy | +4.7% | North America, Europe, APAC defense corridors | Long term (≥ 4 years) |

| Deployment of BVLOS air corridors and Unmanned Traffic Management (UTM) | +2.9% | North America and Europe | Medium term (2-4 years) |

| Increased availability of flight-certified autonomous avionics and sensor suites | +3.1% | Global, supply chain concentrated in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advancements in AI-Driven Flight Control Systems

Real-time machine-learning algorithms guide tactical maneuvers, obstacle avoidance, and route optimization without pilot intervention. Saab’s autonomous Gripen E trials illustrate fighter-grade AI executing split-second decisions, validating moves from rule-based automation to adaptive cognition. The FAA’s AI Safety Assurance Roadmap, released in June 2024, outlines certification tiers for statically trained and continuously learning AI, clearing a progression path for civil fleets. Combat programs demanding millisecond decision loops, such as the US Air Force’s collaborative combat aircraft, spill proven architectures into commercial systems, enabling cargo operators and emerging air-taxi fleets to inherit hardened AI stacks for navigation, sense-and-avoid, and health-monitoring functions.

Rapid Growth in Urban Air Mobility and eVTOL Adoption

Metropolitan planners increasingly view three-dimensional mobility as a lever for congestion relief and regional connectivity. Vertical Aerospace committed USD 1 billion of Honeywell avionics orders to certify the VX4 by 2028, a signal of supply-chain confidence.[1]“VX4 Systems Agreement Expanded to USD 1 Billion,” Vertical Aerospace, vertical-aerospace.com Japan’s first eVTOL routes target the 2028 Osaka Expo, with SkyDrive capturing over 300 provisional orders, aligning national priorities for advanced air mobility. Network effects amplify as vertiport developers such as Urban-Air Port plan 200 sites that bundle energy, maintenance, and air-traffic services. Regulatory hurdles ease: EASA released its VTOL package, and the FAA’s powered-lift final rule clarifies pilot licensing, paving the runway-free aircraft toward scaled service. Improved batteries and certified autonomy underpin business cases for 20-100-mile urban hops where time savings justify premium fares.

Cost Reduction Incentives for Logistics via Autonomous Cargo Drones

Removing pilots unlocks continuous flight cycles and lowers labor overhead for parcel networks. Natilus booked USD 6.8 billion in orders for its blended-wing cargo drones, securing anchor operators such as Ameriflight.[2]Graham Warwick, “Natilus Books USD 6.8 Billion in Orders for Cargo Drones,” Aviation Week, aviationweek.com FAA-approved demonstration corridors allowed MightyFly to complete autonomous beyond-line-of-sight freight routes, reinforcing regulatory feasibility for middle-mile deployment. AI-driven route planning and predictive maintenance compress variable costs, while 24/7 utilization improves return on capital for operators serving remote communities, medical deliveries, and oil-and-gas installations.

Increased Military Investments in ISR and Combat Autonomy

Unmanned systems reduce pilot risk and extend reach in contested airspace. The US Air Force’s General Atomics’ YFQ-42A designation marks the first unmanned fighter nomenclature, underscoring budget priorities for autonomous wingmen programs. Boeing secured a USD 20 billion slot in the Next Generation Air Dominance portfolio, blending manned platforms with autonomous loyal wingmen. Allied initiatives include Saab’s swarm demonstrations under AUKUS, showing multinational alignment on networked autonomy. ISR drones like the MQ-4C Triton provide days-long persistence, supplying strategic intelligence without crew fatigue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity in certification and airspace integration | –2.8% | Global, intensity varies by regulator | Long term (≥ 4 years) |

| Limitations in battery technology and high capital costs | –2.1% | Global, cell supply tilted toward APAC | Medium term (2-4 years) |

| Heightened vulnerability to cyber threats and system hijacking | –1.7% | Global critical-infra nodes | Short term (≤ 2 years) |

| Semiconductor supply disruptions affecting AI processing units | –1.9% | Acute in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity in Certification and Airspace Integration

Legacy aviation rules struggle to fit aircraft with no onboard crew. The FAA aims to publish comprehensive BVLOS regulations by 2026, extending present waiver-based operations into routine commercial lanes. EASA’s certified category demands type certificates and air operator approvals similar to manned fleets, stretching autonomous programs to multi-year timelines. Cross-border routes magnify complexity because harmonization remains partial, pushing manufacturers to chase parallel approvals. Air-traffic integration further hinges on unmanned-traffic-management systems that must interface seamlessly with conventional ATC. Resource-constrained startups often struggle to fund long certification paths, tilting competitive advantage toward incumbent aerospace primes.

Limitations in Battery Technology and High Capital Costs

Lithium-ion packs around 300 Wh/kg fall short of the 800 Wh/kg energy density desirable for regional missions. As a result, eVTOL craft still cap commercial range in the 20-100-mile window, restricting versatility. Development expenses scale quickly: integrating AI flight computers, multi-modal sensor suites, and redundant actuation can surpass USD 100 million before first revenue. Chip shortages and export controls have elevated avionics bill-of-materials costs, weighing on early-stage builders. High capital barriers favor firms with existing cash flows or government backing. They may crowd out novel entrants that could otherwise push breakthroughs in solid-state batteries or high-temperature fuel cells.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Fixed-Wing Dominance Meets VTOL Innovation

Fixed-wing models accounted for 50.62% of the autonomous aircraft market 2025, underscoring their aerodynamic efficiency and range advantages for long-haul ISR and cargo missions. General Atomics’ MQ-20 Avenger upgrade proves that legacy airframes can be retrofitted with full autonomy, keeping lifecycle costs low while enhancing capability. Hybrid fixed-wing VTOL systems, however, register a 26.12% CAGR, indicating fleet planners’ appetite for runway-independent operations that preserve cruise performance. The autonomous aircraft market size attached to hybrid VTOL platforms will broaden sharply as urban networks demand aircraft that lift vertically yet sustain 200-knot cruise.

Hybrid VTOL growth also springs from defense refueling concepts such as Boeing’s MQ-25 Stingray, which proves carrier compatibility without deck-space penalties. Rotary-wing craft hold niche roles for hover-intensive tasks like medevac and firefighting, but tilt-rotor and tilt-wing architectures now offer similar vertical dexterity with extended reach. Combining designs bridges the gap between sprawling runways and tightly packed city cores, easing infrastructure constraints and expanding mission sets.

By Autonomy Level: Incremental Path to Full Autonomy

In 2025, platforms classed as increasingly autonomous made up 67.78% of active deliveries, reflecting regulators’ and operators’ preference for step-wise feature upgrades over radical leaps. Retrofittable kits such as AeroVironment’s ARK add advanced autonomy to existing fleets, enabling operators to harvest benefits without new-type certification. Fully autonomous systems—still a smaller slice—are growing at 26.96% CAGR as AI reliability, sensor fusion, and cloud connectivity converge.

The autonomous aircraft market size for fully autonomous craft will expand as regulatory confidence builds through supervised operations data. Military programs embracing optionally crewed designs provide real-world stress tests for perception stacks, accelerating tech maturity. On the civil side, Joby Aviation’s takeover of Xwing’s autonomy division highlights capital gravitating toward turnkey AI flight decks aimed at passenger services. Over the forecast period, human-on-the-loop governance will gradually yield to exception-only intervention, cutting operating costs and extending 24/7 utilization.

By Application: Cargo Leadership Yields to Air-Taxi Growth

Cargo held a 41.67% revenue share in 2025, leveraging autonomy to slash pilot overhead and hit rural endpoints that lack crew amenities. Operators such as Natilus and MightyFly are chartering autonomous freighters that handle middle-mile logistics at costs competitive with trucking on time-critical lanes. Yet the air-taxi segment posts a 28.45% CAGR as cities race to craft vertiport masterplans. The autonomous aircraft market share for air-taxis will increase sharply once powered-lift rules unlock routine services.Public-sector missions—wildfire suppression, border patrol, environmental monitoring—remain steady due to budgets favoring persistent, low-risk platforms. Passenger inter-city routes remain nascent, limited by range, but demonstrations such as Sikorsky’s crew-optional Black Hawk drops foreshadow future civilian deployments in hazardous response scenarios. Diverse use cases ensure that technology amortization spreads across military, cargo, and urban mobility channels.

By Propulsion Type: Conventional Base Enables Alternative Growth

Conventional turbines powered 55.54% of deliveries in 2025, buoyed by entrenched support networks and unmatched energy density for multi-day ISR sorties. The autonomous aircraft market size attributable to turbine craft, therefore, remains robust through mid-term forecasts. Nonetheless, hydrogen fuel-cell projects notch the fastest 31.17% CAGR as operators chase zero-carbon mandates and extended electric range. GA-ASI’s hybrid-electric testbed illustrates industry experiments with blended powertrains that marry turbine cruise efficiency with electric loiter.Pure-electric architectures dominate short-hop UAM prototypes: battery energy density suits sub-100-mile stage lengths, and acoustic profiles comply with city noise limits. Hybrid-electric systems bridge gaps, allowing conventional engines to handle climb and cruise while swappable battery modules power quiet arrival phases. Infrastructure roll-out—refuelling trucks, hydrogen pipelines, high-voltage chargers—will determine adoption pace; nonetheless, developmental pipelines suggest eventual aperture for multiple propulsion chemistries.

By Component: Sensors Led While Software Accelerates

Sensors and navigation arrays captured 27.74% of revenue in 2025, reflecting the indispensable role of LiDAR, radar, and multi-spectral cameras for perception in low-altitude airspace. Garmin’s certified Autoland retrofit package demonstrates retrofit demand for safety-critical autonomy in GA fleets. Software and AI algorithms record the fastest 25.55% CAGR because aircraft value increasingly resides in code that interprets sensor streams and makes split-second control calls. The autonomous aircraft market size associated with software stacks expands as edge-compute hardware shrinks and in-flight upgrades become routine.Flight-control computers integrate open-architecture standards that allow over-the-air patching, mirroring smartphone ecosystems. Secure communication links enable ground monitoring, real-time mission reroutes, and swarm coordination, while resilient cyber-layers mitigate spoofing risks. Structural and propulsion sub-systems adapt to house redundant electronics and cooling for AI accelerators, making airframes digitally native rather than purely mechanical shells.

Geography Analysis

North America accounted for 36.74% of global revenue in 2025. Pentagon funding for collaborative combat aircraft and high-altitude ISR drones underpins domestic demand, while the FAA’s regulatory leadership shapes global certification pathways. Major primes—Boeing, Lockheed Martin, Northrop Grumman—pair with AI start-ups to field pilotless fighters and delivery drones, enriching a talent pipeline spanning universities to Silicon Valley labs. Canada bolsters supply with avionics and composite manufacturing, and Mexico hosts cost-effective assembly lines that feed cross-border programs. The autonomous aircraft market size will continue to compound as defense appropriations and urban mobility pilots mature under clarified BVLOS frameworks.

Asia-Pacific is the fastest-growing arena at 23.92% CAGR through 2031. China’s low-altitude economy plan, which targets 1.5 trillion yuan aviation output by 2025, funnels subsidies into eVTOL production bases such as EHang’s Hefei plant. Japan aims for commercial air-taxi launches coinciding with the 2028 Osaka Expo, spotlighting public-private coordination on vertiport zoning and autonomous flight-testing. South Korea’s Incheon-centered vertiport grid and Australia’s electric air-taxi feasibility studies widen regional experimentation. India’s defense R&D incentives and increasing satellite connectivity open opportunities for autonomous ISR and cargo operations in remote terrain, while Southeast Asia eyes drones for medical resupply amid archipelagic geography.Europe maintains a strategic foothold, balancing a stringent safety culture with sustainability imperatives. EASA’s phased VTOL regulations define global benchmarks and anchor confidence for city planners across Germany, France, and the United Kingdom, each hosting eVTOL prototypes from Volocopter and Vertical Aerospace. Regional funds target hydrogen propulsion and recyclable structures, giving European OEMs an edge in eco-centric tenders. Italy’s plan for nationwide vertiport corridors and Sweden’s autonomous swarm trials echo the continent’s dual civilian-military thrust. Although the continent grows more slowly than APAC, its policy influence and carbon targets position it as a key reference market.

Competitive Landscape

The market remains moderately fragmented. Defense contracting niches exhibit higher concentration around incumbent primes, leveraging classified supply chains and decades-long program histories. Commercial eVTOL and cargo segments draw a mix of aerospace upstarts and consumer-electronics innovators, leading to a vibrant partnership matrix. Honeywell’s USD 1 billion avionics supply deal with Vertical Aerospace typifies stack integration alliances that knit established component makers to fresh airframe entrants. Joby Aviation’s acquisition of Xwing’s autonomy cadre merges eVTOL hardware with proven perception software, accelerating certification timetables.

White-space competition unfolds in retrofit autonomy kits that lengthen legacy fleet life, an arena in which AeroVironment moves to occupy with modular payloads. Sensor-algorithm co-design becomes a differentiator: firms optimizing AI to specific LiDAR configurations shave compute latency and power draw, appealing to endurance-minded cargo carriers. Meanwhile, open-architecture flight computers encourage third-party app ecosystems, allowing weather firms or telematics providers to rent algorithm slots mid-flight. Competitive chess will hinge on who controls update pipelines and data rights rather than solely on airframe patents.

Autonomous Aircraft Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Airbus SE

Joby Aviation, Inc.

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: General Atomics unveiled the first operational prototype of the YFQ-42A unmanned fighter jet, advancing the US Air Force's initiative to incorporate autonomous systems in its air operations.

- February 2025: EHang partnered with JAC Motors and Guoxian Holdings to build a dedicated eVTOL plant in Hefei, integrating automotive production methods with aerospace standards.

- February 2025: AeroVironment unveiled the JUMP 20-X modular Group-3 UAS, featuring 13-hour endurance and AI autonomy for maritime and land missions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the autonomous aircraft market as all newly built fixed-wing, rotary-wing, and hybrid-lift airframes that can complete gate-to-gate missions without real-time pilot input, together with the certified autonomy hardware and embedded software shipped on those platforms. We include civil cargo, passenger transport, special-mission, and defense programs that have reached at least technology-readiness level 6.

Scope Exclusions: Disposable loitering munitions, tethered drones, and aftermarket retrofit kits are outside the present scope.

Segmentation Overview

- By Aircraft Type

- Fixed-wing

- Rotary-wing

- Hybrid (Fixed-Wing VTOL)

- By Autonomy Level

- Increasingly Autonomous

- Fully Autonomous

- By Application

- Cargo Aircraft

- Passenger Aircraft

- Special Mission/ISR

- Air Taxi/UAM

- By Propulsion Type

- Conventional Turbine

- Electric

- Hybrid-Electric

- Hydrogen Fuel-cell

- By Component

- Flight Control Computers

- Sensors and Navigation

- Communication and Data Links

- Software and AI Algorithms

- Propulsion Systems

- Airframe and Structure

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed flight-test directors, propulsion engineers, venture investors, and regulators across North America, Europe, and Asia. The conversations tested database trends, refined price bands, and aligned adoption timelines voiced by early cargo-drone and urban-air-mobility operators.

Desk Research

We gathered core figures from open sources such as FAA and EASA aircraft registries, ICAO traffic statistics, NASA autonomy test logs, and national defense budget papers. We then traced trade flows with UN Comtrade records and IATA air-cargo tonnage. According to Mordor Intelligence analysts, these datasets map where autonomous fleets are already operating and where approvals are pending.

Company 10-Ks, investor presentations, and reputable aerospace press revealed prototype pipelines and average selling prices, while paid resources like D&B Hoovers for revenue splits and Questel for patent volumes flagged technology infusion rates. The sources listed are illustrative only; many additional databases and public documents inform every datapoint we accept.

Market-Sizing & Forecasting

A top-down build measured global fleet value from production, registration, and procurement outlays, followed by selective bottom-up checks using sampled OEM prices multiplied by disclosed deliveries. This is where Mordor Intelligence differentiates by cross-checking channel feedback before adjusting totals. Model drivers include defense UAV contract allocations, eVTOL certification milestones, battery-energy-density curves, sensor package ASP shifts, and regional BVLOS approval rates. Multivariate regression with scenario analysis extends these variables through 2030, and gaps in supplier counts are bridged with averaged bill-of-materials costs validated in interviews.

Data Validation & Update Cycle

Outputs move through a three-layer review that tests variance against quarterly OEM revenue, flight-test hours, and funded program awards. Before release, a senior analyst refreshes any figures affected by material events, and dashboards trigger interim checks when major orders or regulatory changes emerge, ensuring each annual update stays current.

Why Mordor's Autonomous Aircraft Baseline Earns Buyers' Trust

Published estimates often differ because firms choose disparate aircraft families, start years, and refresh cadences.

Key gap drivers include: some studies focus only on defense or rotary-wing craft, others add retrofit services that we exclude, and several freeze exchange rates at the research start, whereas we anchor every value to live 2025 currency averages and a clearly stated aircraft inclusion rule set.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.83 B (2025) | Mordor Intelligence | |

| USD 7.20 B (2023) | Regional Consultancy A | Older base year, defense and rotary scope only |

| USD 2.15 B (2024) | Industry Association B | Omits cargo UAV and urban-air-mobility platforms |

| USD 7.40 B (2024) | Global Consultancy A | Counts rotary-wing and eVTOL units but ignores fixed-wing |

The comparison shows that our disciplined scope, live currency treatment, and yearly refresh give decision-makers a balanced, transparent baseline that is traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the autonomous aircraft market?

The autonomous aircraft market stands at USD 10.7 billion in 2026 and is projected to grow to USD 27.99 billion by 2031, equating to a vigorous 21.19% CAGR.

Which aircraft type leads in market share today?

Fixed-wing platforms hold 50.62% of autonomous aircraft market share thanks to long-range efficiency and established manufacturing bases.

Which application segment is expanding the fastest?

Air-taxi and urban air mobility services exhibit the highest growth, with a forecasted 28.45% CAGR through 2031 as cities plan vertiports and BVLOS corridors.

How are regulators supporting autonomous flight adoption?

The FAA’s AI Safety Assurance Roadmap and powered-lift rule, alongside EASA’s VTOL frameworks, establish clear certification tiers and pilot licensing standards that enable wider commercial deployment.

What propulsion technologies are emerging beyond conventional turbines?

Hydrogen fuel-cell systems and hybrid-electric architectures are the fastest-growing alternatives, stimulated by environmental policies and advances in fuel-cell stacks.

Which regions will offer the strongest growth opportunities to 2031?

Asia-Pacific leads with a 23.92% CAGR forecast, powered by China’s low-altitude economy investments and Japan’s eVTOL route commitments, while North America remains the largest revenue base.

Page last updated on: