Aerobatic Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

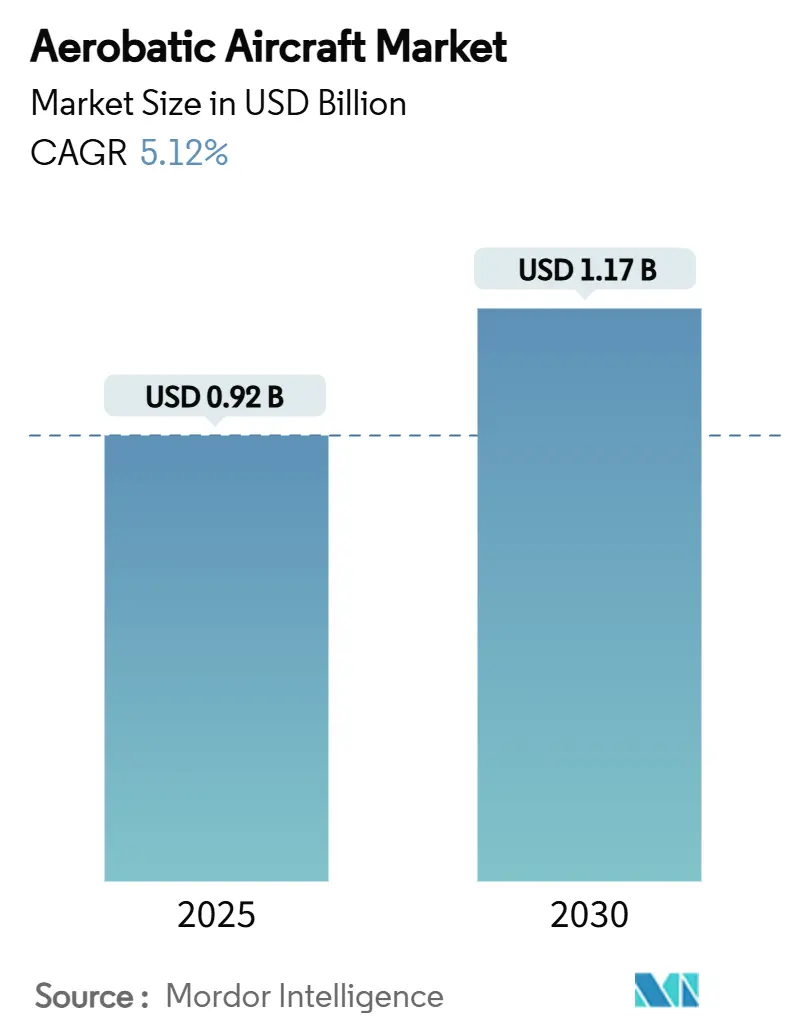

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.17 Billion |

| Growth Rate (2025 - 2030) | 5.12% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerobatic Aircraft Market Analysis by Mordor Intelligence

The aerobatic aircraft market size reached USD 915.06 million in 2025 and will advance to USD 1,174.36 million by 2030 at a 5.12% CAGR. The pivotal growth themes shaping the Aerobatic aircraft market worldwide are rising demand for military trainers, expanding flight-school networks, and shifting toward electric propulsion. Asia-Pacific keeps its lead through large trainer procurements, North America records the quickest regional gain, and twin-engine and electric platforms outpace legacy designs. Supply-chain strain in piston engines and steep insurance costs temper near-term momentum. Yet, regulatory liberalization, trainer replacement cycles, and new propulsion technologies reinforce a steady, long-term outlook for the aerobatic aircraft market.

Key Report Takeaways

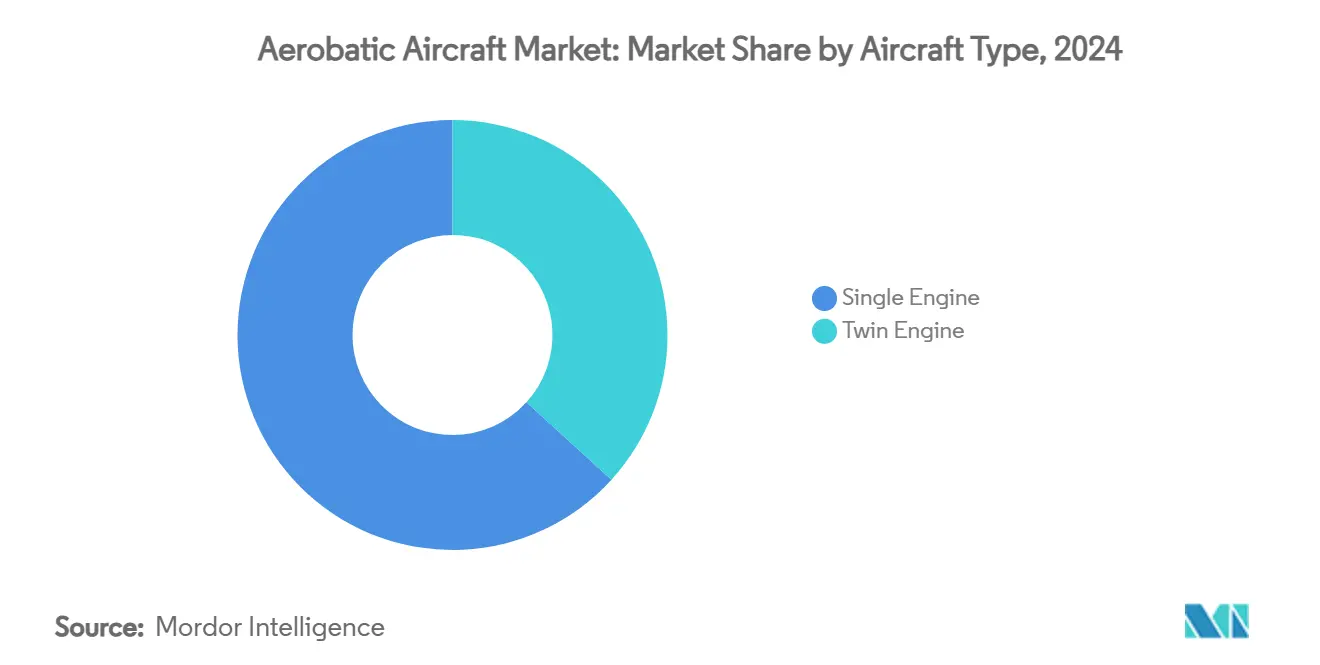

- By aircraft type, single-engine platforms led with 63.25% revenue share in 2024, while twin-engine aircraft are projected to expand at a 6.75% CAGR through 2030.

- By powerplant, turboprops held 35.65% of the Aerobatic aircraft market share in 2024; electric/hybrid systems are set to rise at a 9.73% CAGR to 2030.

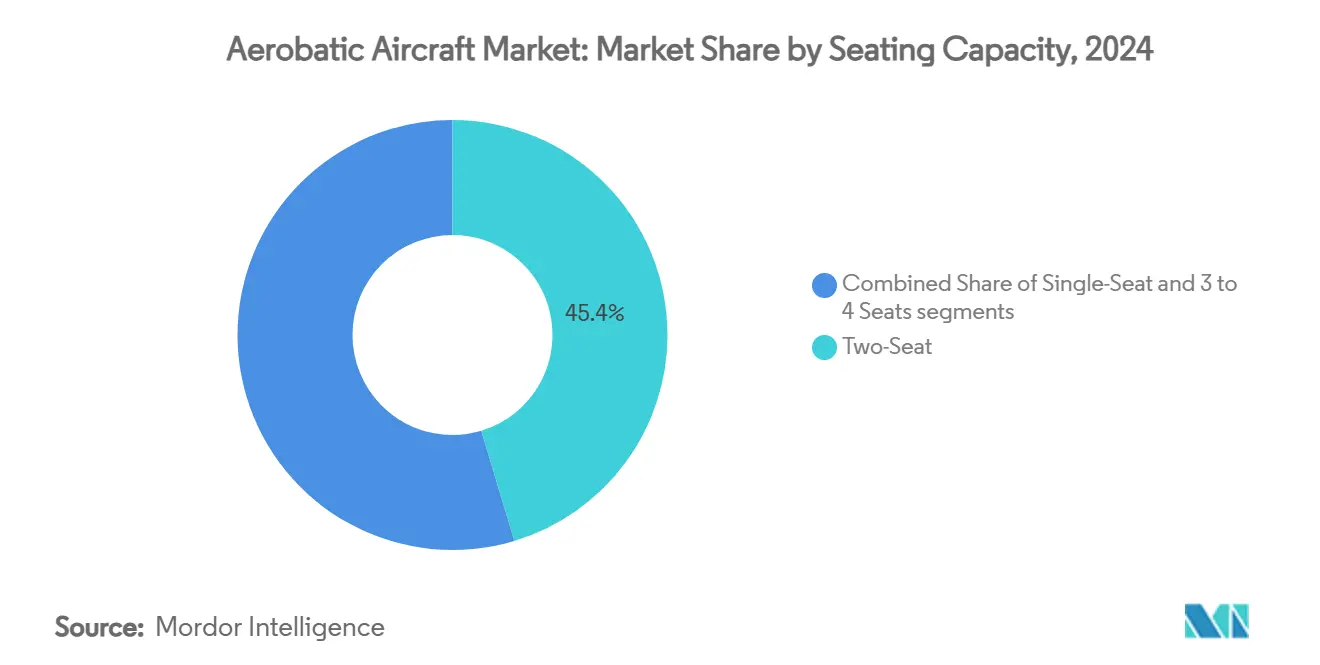

- By seating capacity, two-seat configurations accounted for 45.35% of the Aerobatic aircraft market size in 2024; three-to-four-seat models will grow fastest at 7.23% CAGR.

- By end user, leisure and sport flying dominated with a 53.45% share in 2024, whereas competitive air shows will climb at an 8.65% CAGR.

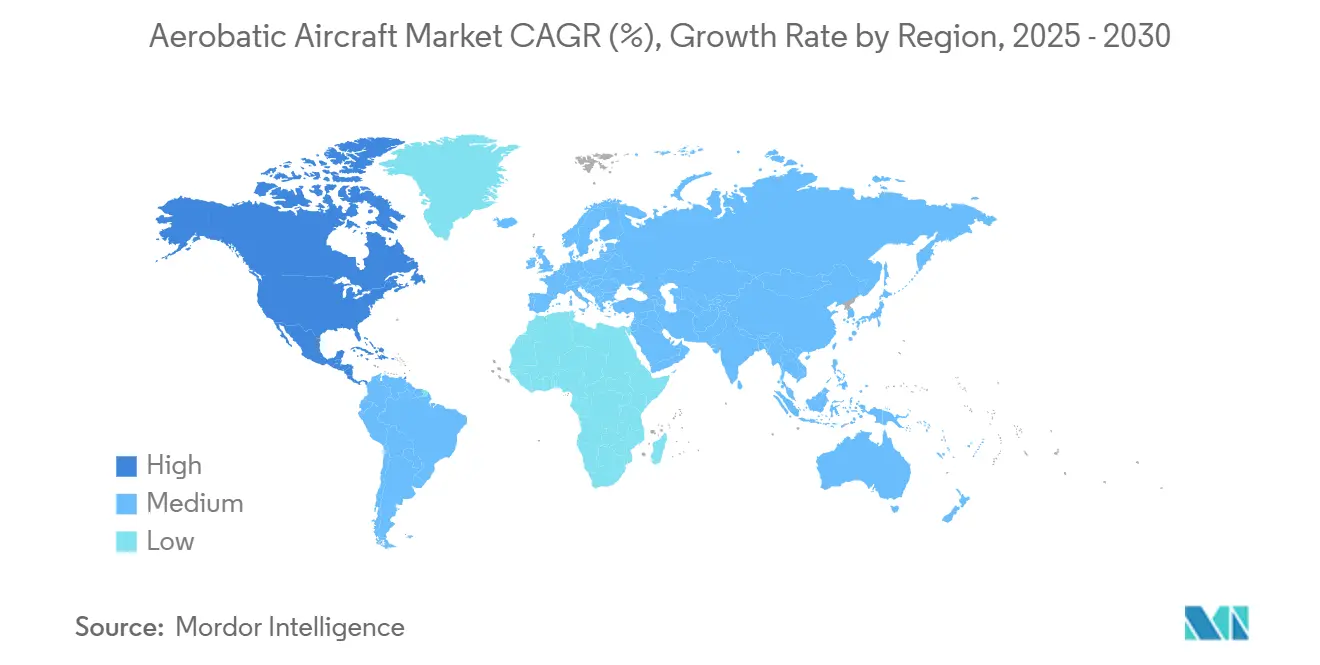

- By geography, Asia-Pacific commanded a 41.23% share in 2024; North America will post the highest 5.85% CAGR.

Global Aerobatic Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for leisure and sport flying among HNWIs | +0.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Growth in LSA and kit-built aircraft registrations | +0.6% | North America and Europe primarily | Short term (≤ 2 years) |

| Expansion of flight-training schools for upset-recovery courses | +0.9% | Global, with emphasis on commercial aviation hubs | Medium term (2-4 years) |

| Military basic-trainer replacement cycles | +1.2% | Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Electric-propulsion retrofits lowering operating costs | +0.7% | Europe leading, North America following | Long term (≥ 4 years) |

| AR/VR-based air-show experiences boosting audience size | +0.3% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for leisure and sport flying among HNWIs

High-net-worth individuals increasingly view aerobatic flying as a signature leisure pursuit that blends exclusivity, skill, and community. The BasicMed expansion that now covers aircraft up to 12,500 pounds eliminates the cost and time burden of periodic medical examinations, making ownership more convenient for busy executives. Attendance at EAA AirVenture and similar fly-ins keeps climbing, exposing newcomers to advanced routines and fueling aspirational purchases.[1]“UPRT Insurance Incentives,” ainonline.com Manufacturers answer with cleaner glass cockpits, noise-attenuating headsets, and ergonomic seating, as shown in the Extra 330 SX, marries pilot comfort with ±10 G performance margins. The result is a virtuous cycle in which rising discretionary income, easier licensing, and better product design reinforce demand for premium single- and twin-engine aerobatic aircraft.

Growth in LSA and Kit-Built Aircraft Registrations

Light-sport and kit-built categories expand as hobbyists exploit accessible regulations and crowdsourced expertise. Online build forums shorten learning curves, and digital tooling lets owners fabricate precision parts at home. The MOSAIC rule, expected to raise weight and speed limits, will allow many current aerobatic designs to qualify for simpler LSA oversight, encouraging additional registrations once finalized. Airparks in Florida, Texas, and Bavaria report longer waitlists for hangar space, signaling real growth at the grassroots end of the market. Flight schools also integrate kit models into syllabi to teach maintenance literacy alongside stick-and-rudder skills, giving the segment a formal training role beyond personal recreation.

Expansion of Flight-Training Schools for Upset-Recovery Courses

As a core safety element, airlines, business-jet operators, and insurers now require upset-prevention and recovery training. Flight academies purchase purpose-built aerobatic aircraft that tolerate repeated high-stress maneuvers without excessive maintenance downtime. Swiss Re and QBE offer insurance credits to operators that send pilots through approved syllabi, creating a direct financial incentive. The FAA’s 2024 instructor-privilege update clarifies legal boundaries for teaching high-G maneuvers, giving schools confidence to invest in new fleets.[2]“Velis Electro Delivery Milestone,” aopa.org The International Aerobatic Club now lists more than 150 approved practice areas in the United States, ensuring congestion-free airspace for syllabus completion. These factors combine to lift near-term aircraft sales and boost utilization rates of existing fleets.

Military Basic-Trainer Replacement Cycles

Several air forces are retiring 1980s-era trainers that lack digital avionics and sustainment support. Japan’s order for 36 Beechcraft T-6 Texan II aircraft under a JPY 133.65 billion (USD 882.09 million) contract illustrates the scale of modern programs. France’s choice of 22 Pilatus PC-7 MKX units and Canada’s CAD 11.2 billion (USD 8.19 billion) Future Aircrew Training package, featuring the PC-21, underline Europe’s and North America’s commitment to next-generation pilot pipelines. These fleets typically remain in service for 15-20 years, guaranteeing long-run parts, simulator, and upgrade revenue. Specifications now demand open-architecture avionics, embedded training aids, and airframe stress limits well above legacy standards, pushing manufacturers to integrate high-fidelity systems from the outset.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited pilot insurance availability and soaring premiums | -0.9% | Global, acute in North America | Short term (≤ 2 years) |

| Shortage of certified aerobatic instructors | -0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Stringent noise and emission regulations near air-show venues | -0.4% | Europe and North America primarily | Medium term (2-4 years) |

| Aging global piston-engine supply chain | -0.7% | Global manufacturing impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited pilot insurance availability and soaring premiums

General-aviation insurers raised rates as loss severity climbed with aircraft values and litigation costs. Direct written premiums reached USD 2.9 billion in 2024, yet underwriting profit remained only USD 343 million, prompting stricter risk selection.[3]“General Aviation Insurance Market Report,” milliman.com Aerobatic operators, classified as high-risk due to intentional envelope excursions, face even higher hurdles. Underwriters often demand 500 hours of recent aerobatic time plus annual UPRT refreshers before quoting, sidelining new entrants. Some pilots self-insure small hull values, but show organizers and airfield landlords still require liability certificates, limiting the practicality of that workaround. Although fresh capital is entering the sector, meaningful rate relief is unlikely before 2026, constraining short-term fleet expansion.

Shortage of certified aerobatic instructors

Retirements, airline hiring booms, and the specialized nature of aerobatic teaching have produced an instructor gap. Earning an unlimited-category waiver entails thousands of practice hours and recurrent evaluations, a path that discourages many candidates. As a result, academy waitlists now stretch six to eight months in major US hubs, slowing student throughput. Some schools import talent from Eastern Europe and South Africa, yet visa processing times and insurance endorsements add complexity. The shortage also inflates wage rates, raising hourly aircraft rental fees and potentially discouraging cost-sensitive trainees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Single-Engine Dominance Amid Twin-Engine Acceleration

Single-engine designs generated 63.25% of 2024 revenue, anchored by their primary training and recreational flying roles. Basic instructors prefer the responsive handling and simpler maintenance these platforms deliver, keeping the aerobatic aircraft market grounded on single-engine economics. The twin-engine share is smaller but records a 6.75% CAGR through 2030 as advanced syllabi and redundancy requirements favor two-engine configurations. Canada’s Future Aircrew Training project illustrates this shift, with multiengine trainers for later flight phases.

Manufacturers refine both paths. Extra’s 330SX focuses on lighter weight and higher roll rate for competition pilots, reinforcing single-engine appeal. Conversely, Tecnam’s newly certified P2006T brings twin-engine efficiency and modern avionics to the training arena.[4]“Velis Electro Delivery Milestone,” aopa.org Choice now hinges on mission profile rather than technology maturity, broadening the aerobatic aircraft market.

By Powerplant: Turboprop Leadership Challenged by Electric Innovation

Turboprops held 35.65% revenue in 2024, cherished for high altitude performance and rugged durability. They remain the workhorse of military basic-trainer contracts such as Japan’s T-6 Texan II order. Electric and hybrid systems lead growth at 9.73% CAGR as operators chase lower fuel spend and environmental compliance. Each Pipistrel’s Velis Electro delivery signals cost parity inching closer for the aerobatic aircraft industry.

Hybrid development narrows the gap: Ampaire’s Eco Caravan shows 50-70% fuel savings through a diesel-electric blend. Piston engines still underpin legacy fleets but face supply strain that could accelerate electric adoption. The aerobatic aircraft market size for electric platforms will expand sharply once battery endurance clears the current 90-minute barrier.

By Seating Capacity: Two-Seat Training Focus Drives Market Leadership

Two-seat models held a 45.35% share in 2024, an outcome of instructor-student pedagogy that dominates flight school procurement. Twin-seat cabins enable real-time coaching, keeping accident rates low during high-G lessons. Three-to-four-seat aircraft post the fastest 7.23% CAGR, appealing to owners who want cross-country versatility plus aerobatic flair. Sling Aircraft’s High Wing model illustrates the trend with more than 200.

Single-seat designs stay relevant for competition pilots, yet limited insurance options and narrow resale markets restrict volume. Kit-built single-seat units from Van’s Aircraft face scheduling delays during restructuring, further pivoting attention toward dual-occupancy trainers. The aerobatic aircraft market share for two-seaters will thus remain resilient even as larger cabins grow faster.

By End-User: Leisure Flying Leadership Amid Competitive Aerobatics Acceleration

Leisure and sport flying captured 53.45% revenue during 2024 as affluent buyers seek experiential recreation. Their purchases typically include factory-built or kit-built aircraft outfitted with glass cockpits and comfort upgrades. Competitive display teams, however, register 8.65% CAGR as air-show circuits expand and virtual streams monetize global audiences.

Flight schools and UPRT programs keep a dependable order cadence, yet confront instructor shortages that slightly suppress delivery rates. Military contracts, though episodic, inject large dollar swings; Japan’s USD 882.09 million buy single-handedly moved regional tallies in 2025. Together, these segments diversify the aerobatic aircraft market, buffering cyclical swings.

Geography Analysis

Asia-Pacific held 41.23% of 2024 sales, chiefly due to defense spending in Japan, India, and Australia. The Beechcraft T-6 Texan II contract secured long-run assembly lines and after-sales revenue. China’s general aviation growth remains potent yet controlled by airspace management reform timelines. Southeast Asian hubs add incremental demand as training franchises open in Thailand and Malaysia.

North America logs the strongest 5.85% CAGR to 2030. The United States sustains a robust pilot pipeline through 100+ Aerobatic Practice Areas and thriving EAA chapters.[5]“EAA AirVenture Attendance Report,” eaa.org Canada’s CAD 11.2 billion Future Aircrew Training investment further advances the aerobatic aircraft market size in the region. Regulatory flexibility under BasicMed and MOSAIC encourages private ownership, while a dense parts ecosystem keeps maintenance downtime low.

Europe occupies a steady middle ground. France, Germany, and the Netherlands buy new trainers but also face stricter environmental statutes that limit show calendars. Electric propulsion adoption in Switzerland and Slovenia helps mitigate noise restrictions, yet the broader shift hinges on cross-border certification acceptance. Eastern Europe presents niche growth tied to tourism flights over heritage cities.

Competitive Landscape

The market features moderate fragmentation. American Champion Aircraft and Extra Aircraft dominate certified production niches, while Van’s Aircraft remains a kit-built powerhouse despite restructuring. New entrants leverage propulsion innovation: Textron’s takeover of Pipistrel grants it a first-mover edge in electric trainers, evidenced by over 100 Velis Electro units in service.

Strategic emphasis converges on propulsion, avionics, and integrated training packages. Pilatus bundles simulators with PC-21 deliveries to offer turnkey military solutions. Tecnam pairs twin-engine designs with low operating costs, courting schools and back-country operators. Ampaire partners with maintenance providers to retrofit hybrid systems into existing fleets, creating an aftermarket revenue channel.

Regulatory headwinds and supply-chain gaps favor agile firms. Companies integrating additive manufacturing for spare parts shorten lead times and sidestep piston casting delays. Partnerships with insurance underwriters that certify in-house UPRT programs also become brand differentiators. The competitive landscape of the aerobatic aircraft market will likely see further mergers as electrification demands fresh capital and certification expertise.

Aerobatic Aircraft Industry Leaders

Van’s Aircraft,Inc.

Aviat Aircraft, Inc

Diamond Aircraft Industries GmbH

EXTRA Flugzeugproduktions – und Vertriebs – GmbH

American Champion Aircraft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Royal Canadian Air Force unveiled liveries for 71 new aircraft under the CAD 11.2 billion (USD 8.22 billion) Future Aircrew Training program, featuring Pilatus PC-21 and Grob G120TP.

- April 2025: France’s DGA ordered 22 Pilatus PC-7 MKX trainers under the Mentor 2 modernization with deliveries from 2027.

- March 2025: EAA AirVenture Oshkosh confirmed headline aerobatic performers for a seven-day July event.

- February 2025: Tecnam secured EASA certification for its next-generation P2006T twin.

Global Aerobatic Aircraft Market Report Scope

An aerobatic aircraft is an airplane heavier than an aircraft. These are used in aerobatics competitions and fight exhibitions. These aircraft are mainly used for practicing flying maneuvers that are not used for general flight. It is performed in gliders and airplanes for training, sport, recreation, and entertainment.

The aerobatic aircraft market is segmented based on type, application, and geography. By type, the market is segmented into single engine and kit. By application, the market is segmented into leisure activities and instructional. The market sizing and forecasts have been provided for all the above segments in value (USD million).

| Single Engine |

| Twin Engine |

| Piston |

| Turboprop |

| Electric/Hybrid |

| Single-Seat |

| Two-Seat |

| 3 to 4 Seats |

| Leisure and Sport Flying |

| Flight School/Instructional |

| Competitive Air-shows and Display Teams |

| Military Basic Training |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| South Africa | ||

| Rest of Africa | ||

| By Aircraft Type | Single Engine | ||

| Twin Engine | |||

| By Powerplant | Piston | ||

| Turboprop | |||

| Electric/Hybrid | |||

| By Seating Capacity | Single-Seat | ||

| Two-Seat | |||

| 3 to 4 Seats | |||

| By End-User | Leisure and Sport Flying | ||

| Flight School/Instructional | |||

| Competitive Air-shows and Display Teams | |||

| Military Basic Training | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | Egypt | ||

| South Africa | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Aerobatic aircraft market?

The aerobatic aircraft market stands at USD 915.06 million in 2025 and is set to reach USD 1,174.36 million by 2030.

Which region grows fastest?

North America registers the highest 5.85% CAGR through 2030 due to a strong general aviation base and sizable defense training budgets.

Which aircraft type dominates sales?

Single-engine platforms lead with 63.25% share because they suit fundamental training and recreational budgets.

How significant is electric propulsion?

Electric and hybrid systems grow at 9.73% CAGR, reflecting cost savings of up to 40% versus piston engines and compliance with noise rules.

Why are insurance premiums a restraint?

Aerobatic risk profiles and higher aircraft valuations pushed general aviation premiums to USD 2.9 billion in 2024, tightening underwriting criteria.

What new regulations affect the market?

The FAA BasicMed update now permits operations up to 12,500 pounds, widening access for pilots and lifting the addressable market for manufacturers.

Page last updated on: