Market Overview

| Study Period | 2020 - 2031 |

|---|---|

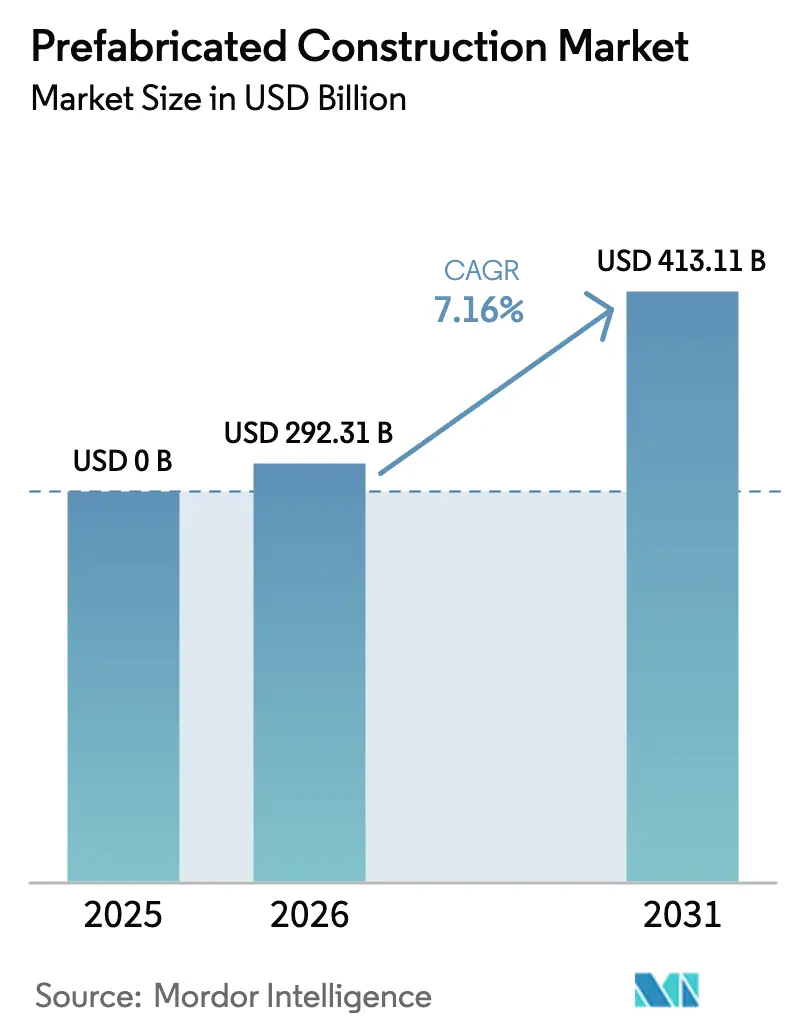

| Market Size (2026) | USD 292.31 Billion |

| Market Size (2031) | USD 413.11 Billion |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

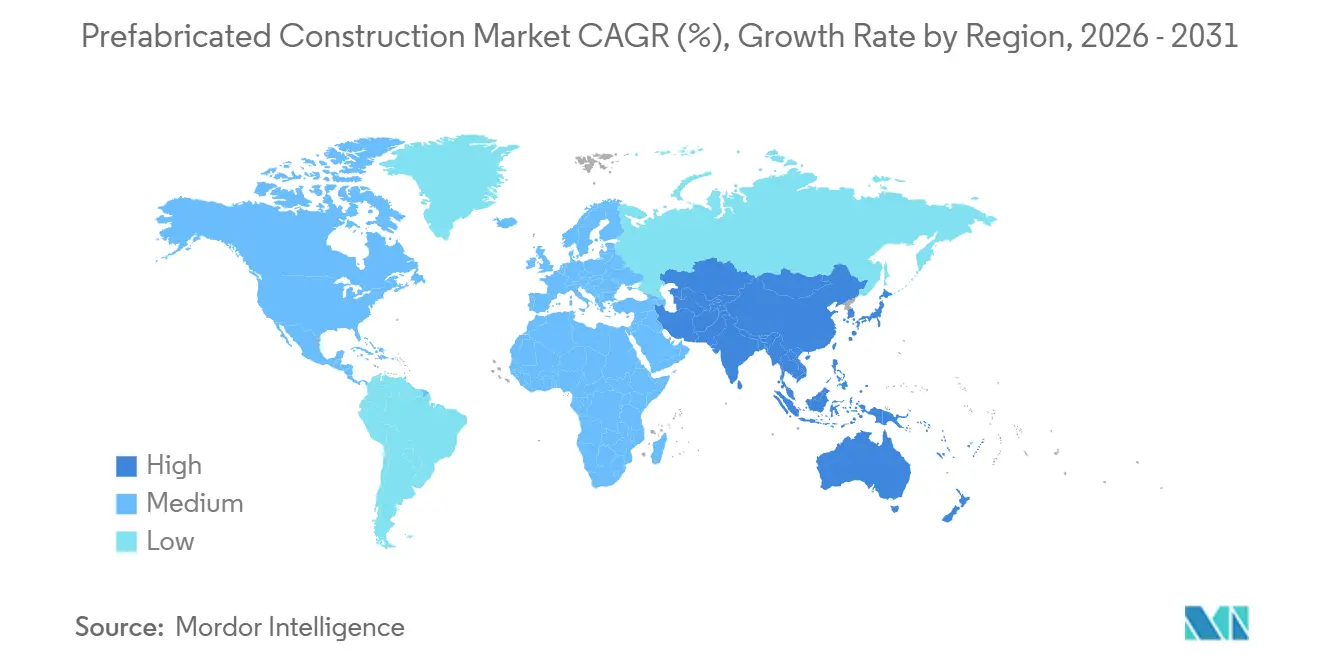

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prefabricated Construction Market Analysis by Mordor Intelligence

The Prefabricated Construction Market size was valued at USD 0 billion in 2025 and is estimated to grow from USD 292.31 billion in 2026 to reach USD 413.11 billion by 2031, at a CAGR of 7.16% during the forecast period (2026-2031).

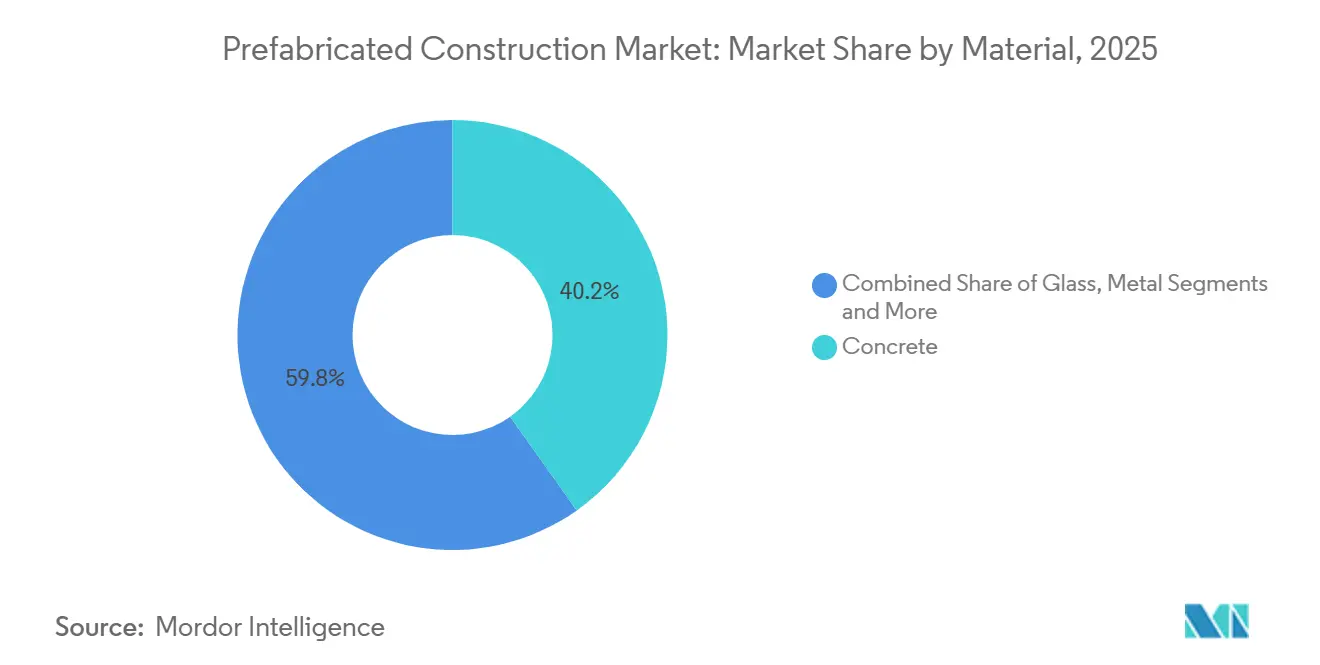

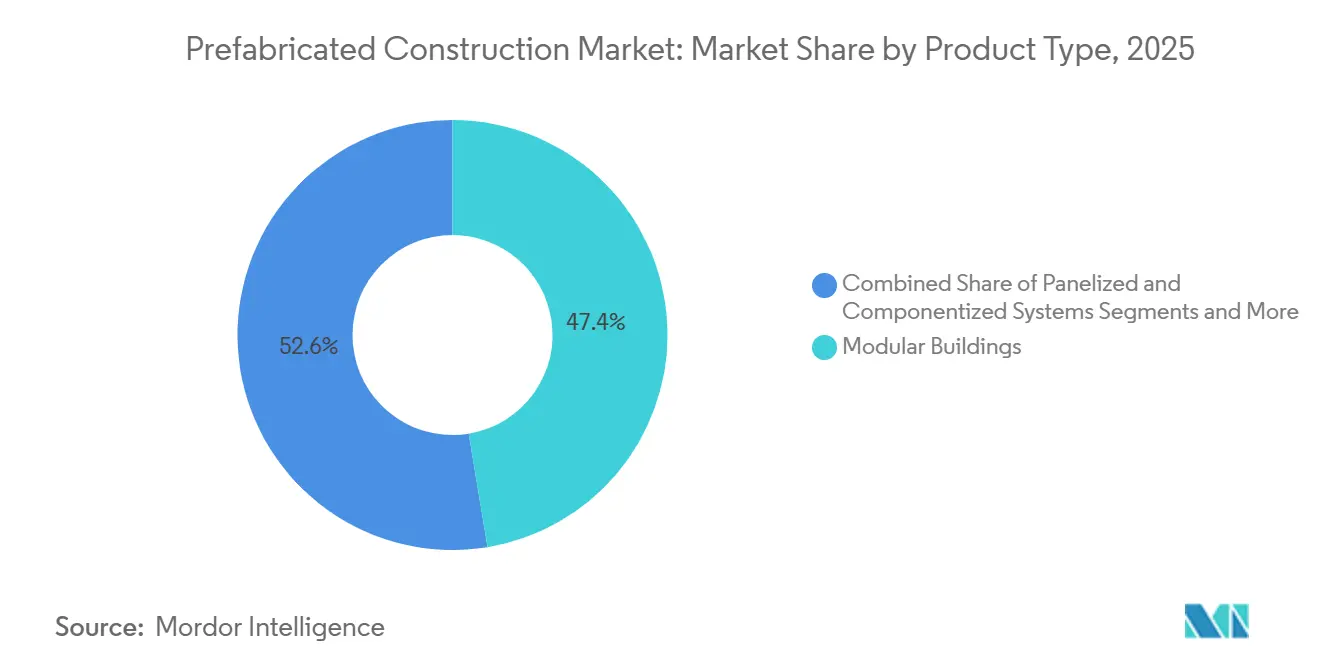

Escalating labor shortages, rising site‐productivity gaps, and tighter project schedules are steering investors toward factory-built delivery models that trim design-to-handover cycles by up to 40%. Concrete modules captured 40.2% of 2025 material revenue, yet cross-laminated timber is growing quickest as carbon accounting gains executive-level urgency. Residential work generated 57.1% of global demand in 2025, but data-center and logistics developers are now fueling the fastest gains in commercial pipeline starts. Volumetric modular buildings led product adoption with 47.4% share in 2025 and continue to outpace panelized systems, signaling broad acceptance rather than pilot-scale experimentation in the prefabricated construction market. Regional patterns diverge: North America benefits from zoning reforms that favor factory-built infill, while Asia-Pacific’s urbanization and public subsidies propel the highest regional CAGR.

Key Report Takeaways

- By material, in the prefabricated construction market, concrete held the largest share at 40.2% of 2025 revenue, whereas timber is forecast to register the fastest 7.89% CAGR through 2031.

- By application, residential projects commanded 57.1% of 2025 demand, while commercial developments are expected to accelerate at an 8.01% CAGR to 2031.

- By product type, modular buildings led with 47.4% of 2025 turnover and are also projected to advance at the quickest 8.31% CAGR over the forecast period.

- By geography, in the prefabricated construction market, North America accounted for 33.2% of 2025 sales, yet Asia-Pacific is on track for the swiftest regional growth at an 8.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing shortages and rapid urbanization | +1.8% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2–4 years) |

| Labor scarcity and site-productivity gaps | +1.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Stricter energy / carbon codes (ESG) | +1.2% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Public-sector programs favoring speed and certainty | +1.0% | Europe, Asia-Pacific, selective North America | Medium term (2–4 years) |

| Standardization and BIM-to-factory workflows | +0.9% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Housing Shortages and Rapid Urbanization Favor Fast, Scalable Offsite Delivery

Cities are welcoming 1.5 million new residents each week, and municipal agencies face mounting pressure to deliver housing within electoral cycles. Factory-built systems can cut project durations by half, making them indispensable for Indian and Chinese authorities that must commission thousands of units on fixed budgets. India’s PMAY program earmarked USD 20 billion for affordable housing through 2024, directing states to deploy offsite solutions on projects above 500 units to meet 2025 targets[1]Government of India, “Pradhan Mantri Awas Yojana – Housing for All,” pmaymis.gov.in. China’s dual-carbon policy adds a climate dimension by rewarding industrialized methods that slash embodied emissions. This momentum bifurcates urban demand: mega-cities lean on high-rise volumetric towers, while secondary cities in Africa and Latin America adopt single-story panelized kits. The upshot is a widening global template library that allows the prefabricated construction market to respond to distinct densification models.

Labor Scarcity and Site Productivity Pressures Tilt Economics Toward Factory-Built Solutions

Construction headcount in the United States fell by 400,000 between 2020 and 2024, while median worker age rose to 43. Factories shift up to 70% of labor hours under one roof and leverage robotic welding and CNC framing to blunt the skills gap. Skanska’s U.K. plant triples shift coverage and turns out bathroom pods at labor densities impossible on congested sites. In Japan, Sekisui House and Daiwa House invested more than USD 500 million combined in automated lines after workforce projections signaled a 30% decline by 2030[2]Sekisui House Ltd., “Integrated Report 2024,” sekisuihouse.co.jp. These moves confirm that labor scarcity is structural, setting a sturdy demand floor for the prefabricated construction market across at least the next decade.

Stricter Energy / Carbon Codes Boost Demand for High-Performance Modular Envelopes

The European Union’s 2024 revision to the Energy Performance of Buildings Directive mandates near-zero-energy standards by 2028 and fines non-compliance at up to 10% of project value. Factory-assembled wall panels routinely achieve U-values below 0.15 W/m²K, a performance level harder to reproduce on weather-exposed job sites. California updated Title 24 in 2025, compelling whole-building energy modeling on multifamily work; modular builders report 20% lower predicted energy use versus stick-built analogs. Demand is also tilting toward carbon-sequestering materials such as CLT, which captures about 1 ton of CO₂ per cubic meter. Lendlease demonstrated a 30% embodied-carbon drop on its Barangaroo South tower after adopting mass timber. As public buyers bake lifecycle assessments into bid scoring, carbon-optimized prefabrication secures a durable policy tailwind.

Public-Sector Programs Prioritize Speed and Cost Certainty

Government sponsors now treat schedule discipline as non-negotiable. The U.K. Department for Education ordered 50 modular schools in 2024, locking cost at GBP 2,500 per square meter (USD 3,200) and guaranteeing delivery within 12 months. The National Health Service followed by procuring 10 modular diagnostic hubs in 2025, each commissioned in under nine months. Spain reserved EUR 1 billion (USD 1.1 billion) in 2025 for modular social housing that must attain an energy rating of A or better. These initiatives underscore a stable funnel of public contracts that will reinforce annual order visibility for the prefabricated construction market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented permitting and municipal variability | −0.8% | Global, acute in North America and Southern Europe | Medium term (2–4 years) |

| Perceived cost premium and cultural bias toward masonry | −0.6% | Southern Europe, Latin America, Middle East | Long term (≥ 4 years) |

| Logistics and craneage constraints in dense cities | −0.5% | Urban cores in Europe, Asia-Pacific, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Permitting and Municipal Variability Slow Approvals and Scale

A module certified in Texas can face up to a year of re-approval if shipped to California, neutralizing speed advantages. Europe’s Construction Products Regulation standardizes product tests yet leaves structural and fire reviews to national codes, compounding paperwork on cross-border deals. The United States lacks a federal type-approval regime, so factory operators must maintain diverse compliance teams. Japan’s 2025 Building Standard Law revision introduced a fast-track path that cuts permitting from nine to three months, offering a template that other regulators are monitoring[3]Ministry of Land, Infrastructure, Transport and Tourism, Japan, “Building Standard Law Revisions 2025,” mlit.go.jp. Until similar harmonization spreads, permitting risk will temper growth in several pockets of the prefabricated construction market.

Perceived Cost Premium, Cultural Bias, and Limited Reference Cases Hinder Adoption

Developers often compare modular bids against the lowest on-site prices without factoring in shorter lease-up or reduced financing carry, showing a nominal 5-10% premium. A 2024 survey found 60% of Spanish builders citing “limited proven examples” as their top barrier. Mediterranean buyers also equate masonry with permanence, a cultural preference that delays specification shifts. Supply chains add another wrinkle: small regional fabricators lack capital for robotics, and large global players hesitate where pipeline visibility is thin. Demonstration projects in Lisbon and Rome are helping, but diffusion remains gradual, limiting penetration rates in the prefabricated construction market across Southern Europe and Latin America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Timber’s Rise Amid Carbon Accounting

Concrete secured 40.2% of 2025 revenue, reflecting its entrenched role in load-bearing panels, parking decks, and institutional assets that demand high fire and acoustic ratings. Precast concrete also benefits from ultra-high-performance mixes exceeding 150 MPa, which enable thinner panels and lighter freight weights. Timber occupies a smaller base but commands the highest growth, expanding at a 7.89% CAGR through 2031. Building codes in British Columbia, Oregon, and Austria now sanction CLT structures up to 18 stories, and the 2024 ICC update extended mass-timber provisions to similar heights in the United States. Developers in Scandinavia and the Pacific Northwest pay 5-8% more for CLT because carbon disclosures are weighted heavily in tenant and lender scorecards. As securities regulators tighten Scope 3 reporting, the prefabricated construction market sees timber shifting from niche to mainstream specification.

The metal segment—largely cold-formed steel—serves data centers and hospitals that cannot accept combustible materials, while glass panels dominate commercial curtain-walls. Fiber-reinforced polymers and hybrid sandwich panels round out the portfolio for temporary sites where weight is critical. Material substitution decisions increasingly hinge on carbon metrics and circularity rather than upfront cost alone, a pivot that widens procurement pathways for bio-based and recycled inputs. This dynamic strengthens supplier incentives to certify environmental product declarations, embedding sustainability credentials deep into the prefabricated construction market supply chain.

By Application: Commercial Projects Accelerate

In the Prefabricated Construction Market, Residential construction delivered 57.1% of total value in 2025, underpinned by North American manufactured housing shipments of 105,000 units and by social-housing rollouts across Europe and Asia-Pacific. Volume builders like Sekisui House cut delivery times by half in dense urban sub-markets, enabling quicker tenant occupancy and faster lender payoff. Commercial work, however, is the fastest-expanding application, set to grow at 8.01% per year to 2031 as data-center and cold-storage operators adopt repeatable modules that can be commissioned in weeks, not quarters. Alphabet and Amazon now deploy containerized server halls that plug directly into power and cooling backbones, shrinking revenue lag and excising rework.

Education and healthcare remain reliable contributors, with the U.K. Department for Education and NHS using repeatable designs that meet cost caps and stringent air-quality norms. Modular retrofit of existing structures is an emerging opportunity: facade-cladding panels can be fitted while occupants remain in place, circumventing relocation costs. This adaptability lowers lifetime disruption and increases building utilization, widening the addressable base for the prefabricated construction market.

By Product Type: Volumetric Modules Take the Lead

Volumetric buildings accounted for 47.4% of 2025 turnover and are scaling at an 8.31% CAGR to 2031, securing both the largest slice and the swiftest pace among product types. Sekisui House’s newest plant rolls out 30 fully fitted modules daily, each scanned by lasers to guarantee millimeter tolerances. Logistics limits remain: specialized trailers cap economical service radii at roughly 500 kilometers, driving a distributed plant network rather than megafactories. Platform designs mitigate the haul challenge by consolidating multiple layouts onto common chassis dimensions, thereby protecting yield rates while serving varied site geometries.

Panelized systems—walls, floors, roof cassettes—fill niches where modular craneage costs erode advantage or where international shipping is necessary. Bathroom pods illustrate a hybrid solution: Marriott’s London hotels adopted 400 factory-built units that slotted into concrete superstructures, slicing MEP installation times in half. Structural-insulated panels and hybrid timber-steel kits sit at the perimeter of the prefabricated construction market, yet R&D investment is rising because they offer lighter transport loads and higher thermal efficiency. As ISO 19650 modeling protocols penetrate procurement, fully modeled volumetric modules are simpler to coordinate, giving them a digital accelerant over stick-built alternatives.

Geography Analysis

In the Prefabricated Construction Market, North America generated 33.2% of 2025 sales thanks to a mix of manufactured housing in the United States, modular multifamily towers in Canada, and early-stage commercial adoption in Mexico. HUD’s 2024 rule changes permitted higher ceiling lines and larger window areas, enhancing curb appeal and easing lender approval. British Columbia and Ontario channeled USD 3 billion from Canada’s National Housing Strategy into modular builds to accelerate occupancy for low-income residents. In the United States, labor availability is forecast to remain 10% below pre-pandemic thresholds through 2027, encouraging local authorities in California and Oregon to legalize accessory dwelling units and modular infill.

In the Prefabricated Construction Market, Asia-Pacific is on track for the fastest expansion, advancing at 8.65% annually through 2031. China’s housing ministry targets 30% prefabrication penetration by 2026 and backs the objective with tax incentives and accelerated permits for factories that meet the quota. India, traditionally reliant on cast-in-place concrete, pivoted when Tata Steel and Larsen & Toubro launched modular divisions to overcome rising labor costs. Japan and South Korea push the automation frontier; Daiwa House’s Nara facility produces steel modules with zero manual welding, lowering per-unit cost by 18%. In Southeast Asia, Singapore’s BCA runs a certification scheme that assigns higher bid scores to modular bids, while Indonesia’s provincial approvals remain segmented.

Europe grows at a steadier clip yet leads on regulatory alignment and deep sustainability mandates that push the prefabricated construction market toward offsite envelopes. The Renovation Wave initiative seeks 35 million building upgrades by 2030, and prefabricated facade kits are central to tenant-in-situ retrofits. Nordic countries exhibit the highest global penetration above 40%, driven by timber supply chains and consumer acceptance of factory quality. Germany’s Kleusberg delivered 500 student units in 2025 across three cities inside 12 months, testifying to rising institutional confidence. Southern Europe still clings to masonry traditions, but Madrid’s modular social-housing pilots are nudging sentiment. In the Middle East and Africa, mega-projects like Saudi Arabia’s NEOM rely on Red Sea Housing’s large-scale worker camps, highlighting how extreme-climate and remote-site conditions unlock prefabricated demand.

Competitive Landscape

Competition is moderately fragmented globally, with the top suppliers collectively accounting for only a limited share of the market. Sekisui House and Daiwa House together account for close to 40% of Japan’s modular housing volume by leveraging proprietary steel frames and earthquake-resistant designs. In Europe, PEAB and Skanska maintain integrated supply chains that cover design, fabrication, and assembly, letting them hedge raw-material volatility and secure long-term framework agreements with public buyers. North American players are split between manufactured-housing giants such as Clayton Homes and emergent multifamily specialists, creating a two-tier ecosystem inside the prefabricated construction market.

Strategic maneuvers center on vertical integration and automation. Lendlease bought a Melbourne precast plant in December 2025 to internalize facade and pod production, echoing Skanska’s rollout of dedicated modular lines in the U.K. and Nordics. Sekisui House’s 2025 partnership with a robotics company targets a 40% labor reduction by 2028, aiming for sub-millimeter precision that unlocks healthcare and semiconductor-cleanroom projects. Smaller innovators like Element5 target CLT panels, while Forta PRO develops modular cleanrooms for pharmaceutical clients, leveraging niche know-how to sidestep direct showdowns with volume leaders.

Technology adoption is becoming the sorting mechanism between scale winners and followers. Plants that run end-to-end BIM integration report up to 20% lower unit costs thanks to scrap reduction and punch-list avoidance. Compliance with ISO 19650 and ISO 14040 is now a prerequisite for public tenders in Europe and parts of the Asia-Pacific region, raising the investment bar for entrants. Venture-funded disruptors such as ILKE Homes show that capital intensity can derail operations without a robust backlog, highlighting execution risk even amid strong structural tailwinds in the prefabricated construction market.

Prefabricated Construction Industry Leaders

Clayton Homes

Sekisui Homes

China Saite Group Company Limited

PEAB

Barratt Developments PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Skanska formed a joint venture with a Swedish pension fund to develop 2,000 modular apartments across three cities by 2028, targeting 20% below-market rents.

- December 2025: Lendlease acquired a Melbourne precast facility for AUD 85 million (USD 57 million) to bolster in-house module supply.

- November 2025: Lendlease acquired a Melbourne precast facility for AUD 85 million (USD 57 million) to bolster in-house module supply.

- October 2025: PEAB opened a Gothenburg modular line with robotic welding that cuts module build time to five days.

- September 2025: Sekisui House partnered with a robotics firm to introduce AI-guided assembly targeting sub-millimeter tolerances.

Global Prefabricated Construction Market Report Scope

A prefabricated building is a building or part of a building that has been manufactured in advance and can be easily transported and assembled.

The prefabricated buildings market is segmented by material type (concrete, glass, metal, timber, and other material types), application (residential, commercial, and industrial), and geography (North America, Europe, Asia-Pacific, and the Rest of the World).

The report offers market size and forecast in (USD) for the segments mentioned above.

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Material | Concrete | |

| Glass | ||

| Metal | ||

| Timber | ||

| Other Materials | ||

| By Application | Residential | |

| Commercial | ||

| Others | ||

| By Product Type | Modular Buildings | |

| Panelized & Componentized Systems | ||

| Other Prefab Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the prefabricated construction market in 2026?

The prefabricated construction market size reached USD 292.31 billion in 2026 and is forecast to keep expanding at a 7.16% CAGR.

Which material dominates revenue today?

Precast concrete modules lead with 40.2% of 2025 revenue because of their structural reliability and acoustic performance.

Which application segment is growing fastest?

Commercial projects—especially data centers and logistics hubs—are projected to grow at an 8.01% CAGR through 2031 as developers value faster lease-up.

Which region delivers the highest growth rate?

Asia-Pacific is expected to post an 8.65% CAGR to 2031, driven by rapid urbanization, supportive policy, and rising labor costs.

What restrains wider adoption of modular methods?

Fragmented permitting, cultural preference for masonry, and last-mile logistics costs in dense cities remain the primary barriers.

Who are the leading players?

Sekisui House, Daiwa House, Skanska, PEAB, and Red Sea Housing headline the competitive field, yet none exceeds a 10% individual share.

Page last updated on: