European Built-in Refrigerator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

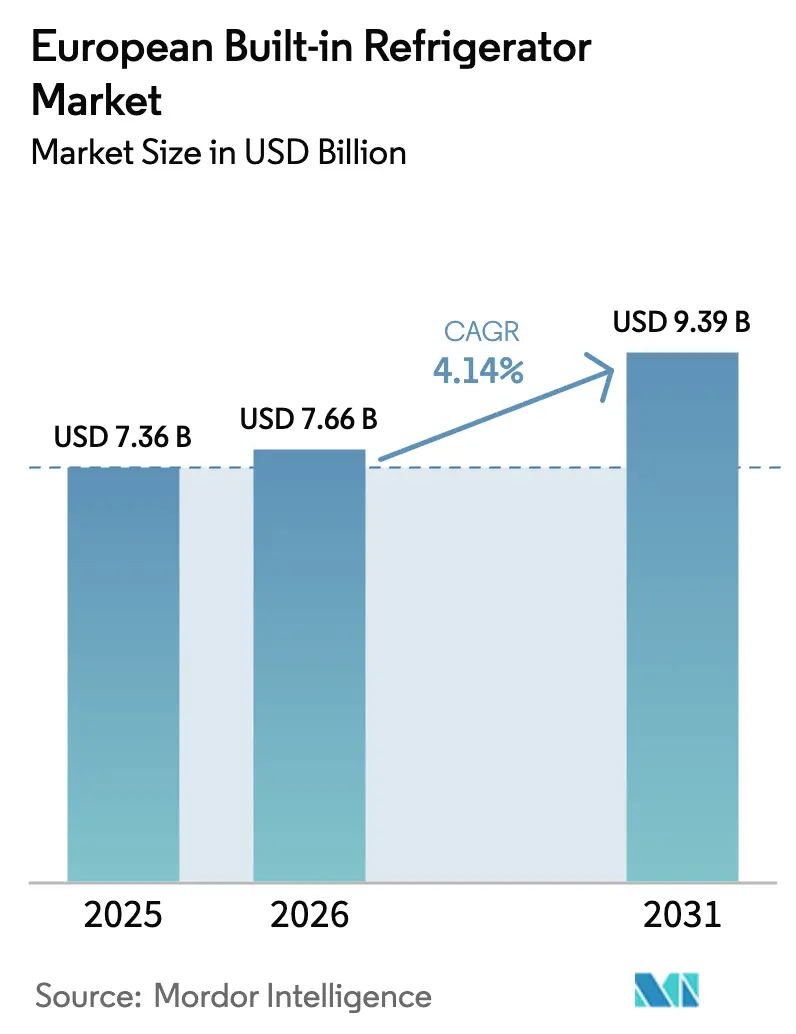

| Base Year Market Size (2025) | USD 7.36 Billion |

| Market Size (2026) | USD 7.66 Billion |

| Market Size (2031) | USD 9.39 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

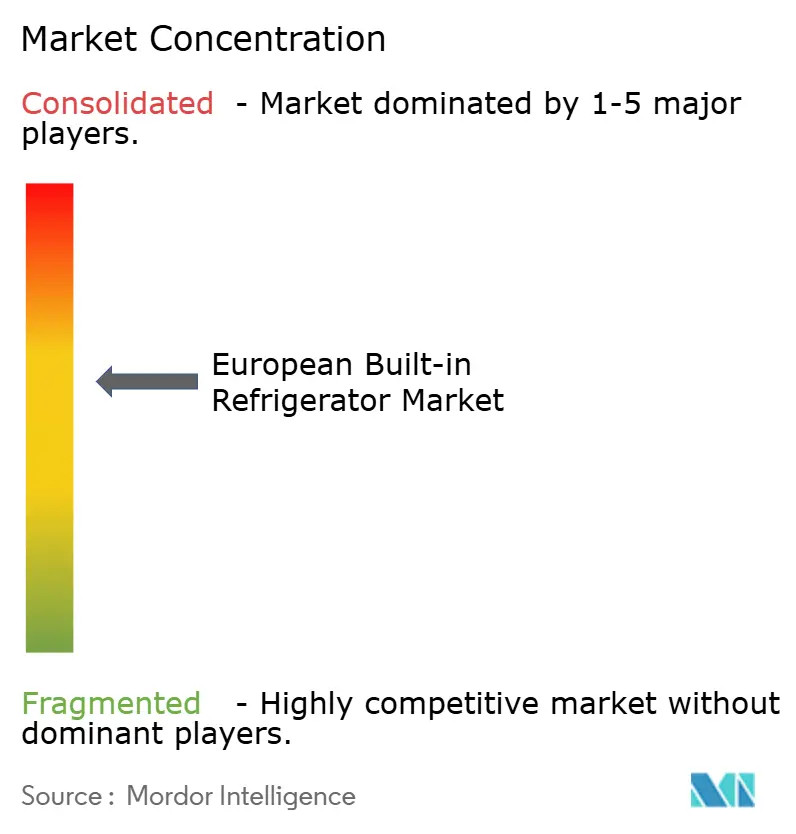

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

European Built-in Refrigerator Market Analysis by Mordor Intelligence

The European Built-in Refrigerator Market size is expected to grow from USD 7.36 billion in 2025 to USD 7.66 billion in 2026 and is forecast to reach USD 9.39 billion by 2031 at 4.14% CAGR over 2026-2031.

The Europe built-in refrigerator market reached USD 7.36 billion in 2025 and is forecast to register a 4.2% CAGR to USD 9.04 billion by 2030. Demand remains resilient because renovation spending holds firm even as new housebuilding slows, and because EU regulations encourage early replacement of older, less efficient models. Market participants also benefit from consumer preference for premium, space-saving kitchens, rising disposable income in core economies, and rapid uptake of large-appliance e-commerce. At the same time, manufacturers face higher input costs as copper exceeds USD 10,000 per metric ton and aluminum prices remain elevated, while a shortage of certified installers restrains rollout speed. Competitive dynamics are shifting as Whirlpool’s European unit merges with Arçelik, Samsung and LG broaden smart-home ecosystems, and German brands defend their reputation for engineering excellence through energy-efficient innovations.

Key Report Takeaways

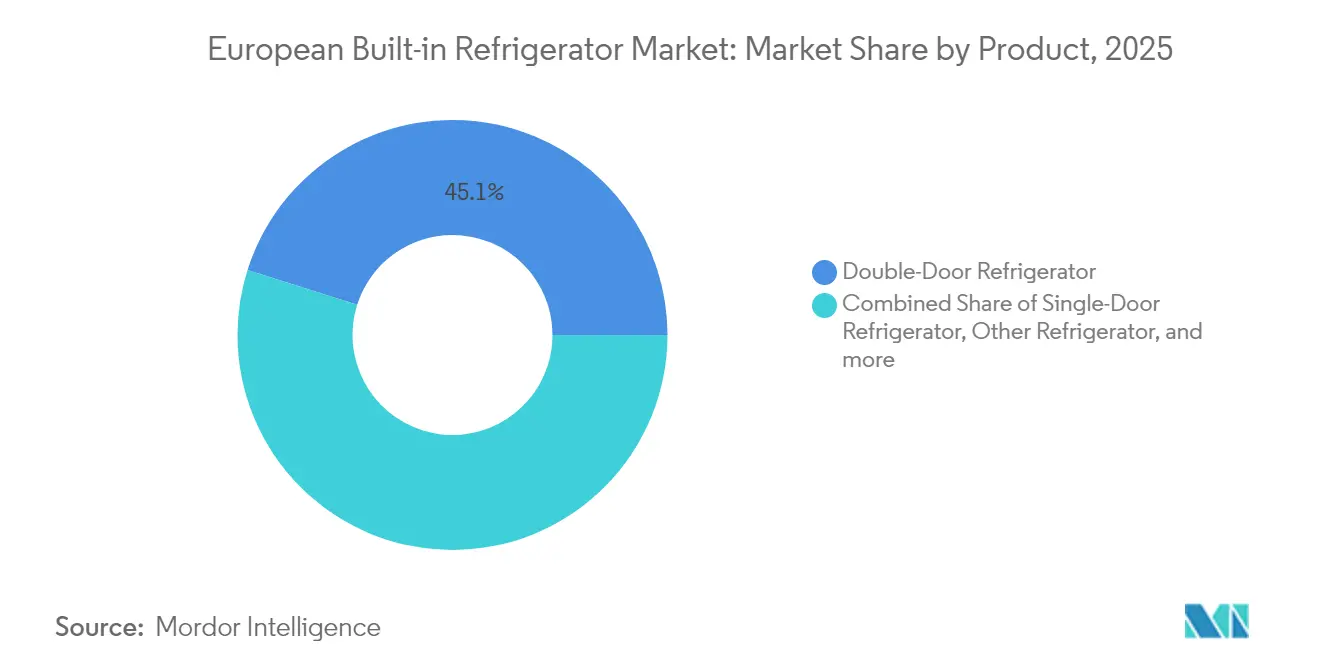

- By product, double-door refrigerators led with 45.12% revenue share in 2025; side-by-side configurations are projected to expand at a 5.34% CAGR through 2031.

- By capacity, models above 15 cubic feet accounted for 67.10% share of the Europe built-in refrigerator market size in 2025 and are advancing at a 4.66% CAGR through 2031.

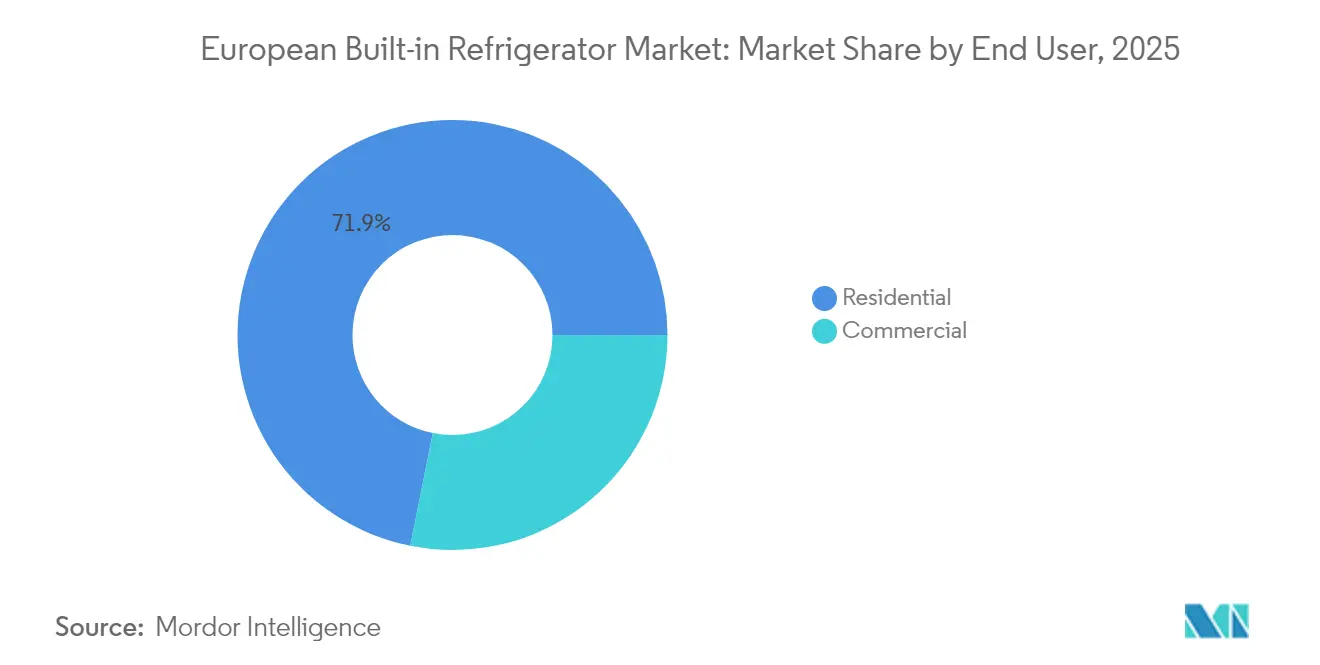

- By end user, residential applications held 71.85% of the Europe built-in refrigerator market share in 2025, while commercial demand is forecast to grow at 5.86% CAGR through 2031.

- By distribution channel, B2C retail controlled 75.70% revenue in 2025; online retail within B2C is projected to record a 6.28% CAGR to 2031.

- By geography, Germany captured a 17.30% share in 2025; the Nordic region is anticipated to expand at a 5.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

European Built-in Refrigerator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization-driven demand for space-saving kitchens | +0.8% | Western Europe, Nordic regions | Medium term (2-4 years) |

| Premiumization and rising disposable income | +0.6% | Germany, Nordic, BENELUX | Long term (≥ 4 years) |

| Stringent EU energy-efficiency regulations are accelerating replacements | +0.9% | EU-wide | Short term (≤ 2 years) |

| Rapid growth of e-commerce for large appliances | +0.7% | UK, Germany, France | Medium term (2-4 years) |

| Post-pandemic surge in modular kitchen renovations | +0.5% | Western Europe | Short term (≤ 2 years) |

| Luxury real-estate developers bundling smart built-ins | +0.3% | Germany, UK, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanization-Driven Demand For Space-Saving Kitchens

Apartment sizes continue to shrink in major European cities, and 48% of residents already live in flats, pushing architects and homeowners toward integrated appliances that conserve floor area. Overcrowding affects 16.8% of households, making full-height built-in models attractive because they nest seamlessly within cabinetry. Building permits for new dwellings fell 19.8% in 2023, yet renovation activity remains robust, directing spending toward kitchen upgrades that favor built-in formats. Rising monthly housing costs, averaging EUR 765 in early 2024, intensify the need to optimize usable space, and developers increasingly specify integrated refrigeration to justify premium rents [1]Eurostat, “Housing Statistics 2024,” ec.europa.eu.

Premiumization And Rising Disposable Income

Stabilizing consumer confidence supports willingness to pay extra for design, connectivity, and food-preservation features. Grocery sales grew faster than inflation in 2024, signalling discretionary spending capacity for large appliances. Brands such as Miele target affluent buyers with MasterCool units that include internal cameras and advanced freshness systems, while surveys show Northern Europeans rate energy efficiency and product longevity as core purchase criteria. The smart-appliance subsegment is expanding, and regional research confirms that consumers in the BENELUX and Nordic states willingly trade up to connected models that integrate with wider smart-home ecosystems.

Stringent EU Energy-Efficiency Regulations Accelerating Replacements

The Ecodesign for Sustainable Products Regulation obliges manufacturers to deliver longer-lasting, repairable, and more efficient refrigerators, while new labeling rules force retailers to display class ratings in advertisements. The F-Gas Regulation sets a 2050 phase-out of HFC refrigerants, driving redesigns toward natural alternatives and pushing replacement cycles forward. A January 2025 consumer survey of 5000 people found 80% of respondents were concerned about energy bills, steering demand toward A-class models, and the EPREL database makes efficiency data searchable at the point of sale. Collectively, these measures lift the near-term growth outlook for the Europe built-in refrigerator market.

Rapid Growth of E-Commerce For Large Appliances

Seventy-seven percent of EU internet users bought goods online in 2024, and furniture plus home accessories already account for 19% of purchases. Electrical-appliance sites in Germany convert at 2.4% with a USD 212 average order value, demonstrating consumer comfort with high-ticket digital transactions. Same-day and next-day delivery expectations compel retailers to upgrade logistics, and manufacturers partner with white-glove installers to mitigate complexity. Robust online adoption broadens reach into secondary cities and fuels omnichannel promotions that lift visibility of premium built-in models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price premium versus freestanding models | -0.4% | Eastern Europe, Southern Europe | Medium term (2-4 years) |

| Volatile raw materials and logistics costs | -0.6% | EU-wide | Short term (≤ 2 years) |

| Shortage of certified installers and service technicians | -0.5% | EU-wide, especially Nordic and BENELUX | Medium term (2-4 years) |

| Cabinet-depth constraints in micro-apartments | -0.3% | Western European urban centers, Nordic cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Premium Versus Freestanding Models

Built-in refrigerators can cost 30-70% more than comparable freestanding units, deterring price-sensitive buyers in Eastern and Southern Europe. A 35,000-member UK poll reported that one-quarter of shoppers place the lowest price above all, while housing cost ratios exceed 40% for renters, squeezing budgets for premium appliances. Installation charges and cabinetry modifications add further expense, reinforcing the gap and slowing penetration outside affluent regions [2]European Central Bank, “Consumer Expectations Survey January 2025,” ecb.europa.eu.

Volatile Raw Materials and Logistics Costs

Copper, aluminum, and steel price swings elevate bill-of-materials costs by as much as 4.2%, while ocean-freight disruption forces contingency inventory and raises working capital needs. The European Investment Bank finds that 37% of firms are hindered by raw-material access and 34% by logistics delays. Energy prices remain two to three times higher than in the United States, undercutting margins and pressuring manufacturers either to raise prices or relocate production [3]European Investment Bank, “EIB Investment Report 2024/2025,” eib.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Double-Door Dominance Amid Side-by-Side Acceleration

Double-door models commanded 45.12% of 2025 revenue because they balance storage capacity with familiar ergonomics. The segment benefits from widespread cabinet designs that accommodate standard heights and hinge positions. In contrast, side-by-side units, though holding a smaller base, are forecast to grow 5.34% CAGR through 2031 as consumers with larger floorplans seek quick access to fridge and freezer compartments. The Europe built-in refrigerator market size for side-by-side models is on track to widen materially, given rising adoption in Germany and the Nordics.

Premium brands differentiate through Wi-Fi connectivity, AI-driven energy modes, and internal cameras. Samsung’s 2024 EuroCucina lineup includes the BRB6500D with SmartThings optimization, while Miele’s MasterCool range enables remote monitoring via the Miele@Home app. These innovations reinforce premium positioning and justify higher price points, sustaining momentum within the Europe built-in refrigerator market.

By Capacity: Large-Format Units Drive Market Expansion

Refrigerators above 15 cubic feet represented 67.10% of sales in 2025 and will deliver the fastest 4.66% CAGR because households buy in bulk and cook at home more often. Higher capacity aligns with renovation projects that expand kitchens, and SlimTech insulation from Whirlpool boosts usable volume within existing footprints, appealing to space-constrained urban dwellers. The Europe built-in refrigerator market size for large-format units will therefore outpace smaller categories despite shrinking apartment dimensions.

Smaller than 15 cubic feet models retain a niche in studio flats and secondary pantries but face headwinds as consumers demand multifunctional storage. Urban developers look to integrate full-height columns that maximize cubic capacity while preserving aisle clearance. Manufacturers respond by slim-lining down wall thickness and adopting variable cooling zones to attract both groups, strengthening the versatility of offerings within the Europe built-in refrigerator market.

By End User: Residential Supremacy With Commercial Momentum

Residential buyers held 71.85% share in 2025, sustained by renovation projects that dipped only 0.9% despite a wider construction slump, and by owners upgrading kitchens to elevate property value. Energy-efficient built-ins reduce utility bills and satisfy the EU’s tightening standards, reinforcing replacement incentives. The Europe built-in refrigerator market share remains heavily residential, yet signals point to gentle erosion as hospitality recovers.

Commercial demand is projected to rise 5.86% CAGR as hotels, restaurants, and coworking offices invest in smart, durable refrigeration to control energy spend and meet ESG goals. Connected units allow operators to monitor temperature remotely and schedule predictive maintenance, cutting food waste and downtime. Growth in quick-service formats and premium coffee chains brings additional volume, improving scale economics across the Europe built-in refrigerator market.

By Distribution Channel: Retail Leadership Amid Online Acceleration

B2C retail captured 75.70% of sales in 2025, with multi-brand stores and exclusive showrooms providing a physical experience for high-consideration purchases. Omnichannel services such as click-and-collect and live video consultations extend reach beyond store footprints, underpinning the strength of the Europe built-in refrigerator market.

Online retail is the fastest-growing path at 6.28% CAGR as consumers overcome delivery and installation concerns. Specialist platforms offer bundled disposal, in-home setup, and financing, lowering adoption barriers. Manufacturers also employ direct-to-consumer web shops to display full specifications, configurators, and energy-cost calculators, fostering informed decisions and reinforcing the Europe built-in refrigerator industry’s shift to digitally enabled sales.

Geography Analysis

Germany led with 17.30% of 2025 revenue due to a large housing stock, strong brand loyalty toward domestic engineering, and willingness to pay for premium kitchen systems. High energy awareness also drives early replacement, keeping the Europe built-in refrigerator market vital in the country. France, Italy, and Spain follow, leveraging extensive renovation activity and style-driven consumers who favor seamless cabinet integration. The United Kingdom maintains a sizeable demand as city apartments require compact yet upscale solutions, even amid broader economic uncertainty.

The Nordic region posts the quickest 5.63% CAGR through 2031, propelled by high disposable incomes, early smart-home adoption, and sustainability values that reward A-class machines. Retailers in Sweden and Denmark report strong uptake of connected refrigerators that adjust cooling based on usage patterns, illustrating how technology aligns with cultural preferences. BENELUX markets likewise enjoy high urbanization and e-commerce penetration, enabling rapid diffusion of premium built-ins via online storefronts.

Eastern Europe contributes a smaller absolute volume but grows steadily as rising wages encourage gradual premiumization. Romania and Hungary showcase e-commerce growth of 43 and 37 percentage points, respectively, from 2014-2024, expanding access to imported brands. Construction trends diverge—building permits fell sharply in Austria and Finland, yet grew in Greece and Ireland—but renovation remains an avenue for built-in upgrades. Across Europe, a 48% house-price increase since 2010 challenges affordability, prompting owners to renovate existing kitchens rather than relocate, which in turn sustains the Europe built-in refrigerator market across diverse regions.

Competitive Landscape

The market is moderately concentrated. BSH Hausgeräte leads with brands such as Bosch, Siemens, Gaggenau, and Neff that emphasize reliability and energy leadership. Whirlpool’s sale of its European business to Arçelik birthed Beko Europe B.V. in April 2024, an entity with EUR 5.5 billion in combined revenue that reshapes the competitive hierarchy. This consolidation underscores a strategic pivot toward margin stability and regional focus.

Samsung enlarges its AI Home platform by embedding 9-inch screens and voice controls in built-in models, while LG adds Athom’s Dutch smart-home software to its ThinQ ecosystem to broaden interoperability. These moves reflect a race to lock consumers into proprietary ecosystems that span multiple appliances and services. Miele, Liebherr, and other German premium brands protect share through superior build quality and local after-sales networks, emphasizing longevity to comply with EU durability rules.

Price competition intensifies as Chinese manufacturers enter with feature-rich alternatives at lower cost, supported by growing European sales subsidiaries. Compliance with F-Gas and Ecodesign standards raises the barrier to entry, favoring incumbents with robust R&D budgets and certified service teams. Partners capable of installing and maintaining complex units gain importance, prompting appliance makers to launch training programs that widen the technician pool and support future volume within the Europe built-in refrigerator market.

European Built-in Refrigerator Industry Leaders

BSH Hausgeräte (Bosch, Siemens, Neff, Gaggenau)

Electrolux AB (incl. AEG)

Whirlpool Corp.

Haier Europe (Candy, Hoover)

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Miele launched its newest generation MasterCool line of built-in refrigerators featuring integrated cameras for remote viewing via the Miele@Home app and freshness systems that extend food preservation up to five times longer, with availability starting Oct 2025.

- December 2024: Samsung Electronics announced the launch of a new 9-inch AI Home screen for its Bespoke refrigerators, enhancing user experience with voice control via Bixby and Map View for monitoring connected appliances, showcased at CES 2025.

- September 2024: Samsung Electronics introduced Smart Forward updates for home appliances, including new functionalities for Family Hub on 4-Door French Door Refrigerators such as Quick Share, Buds Auto Switch, and Fridge Call, available for models produced since 2017.

- April 2024: Samsung Electronics showcased its new premium kitchen and built-in product lineup at EuroCucina 2024, including the Built-in Wide Bottom Mount Freezer (BRB6500D) with Wi-Fi compatibility and SmartThings AI Energy Mode.

European Built-in Refrigerator Market Report Scope

Built-In Refrigerators are one of the most widely demanded products as people adopt urbanization. A complete background analysis of the Europe Built-in Refrigerator Market includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles covered in the report. European Built-in Refrigerator Market is segmented based on By Product Type (Single Door, Double Door, Side by Side Door, French Door, and Other), By Application (Residential and Commercial), By Distribution Channel (Online Channel and Offline Channel), and by Country (United Kingdom, France, Germany, and Other European Countries).

| Single-Door Refrigerator | |

| Double-Door Refrigerator | Top Freezer |

| Bottom Freezer | |

| Side-By-Side Door Refrigerator | |

| French-Door Refrigerator | |

| Other Refrigerators |

| Less Than 15 cu. Feet |

| More Than 15 cu. Feet |

| Residential |

| Commercial |

| B2C / Retail | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly From The Manufacturers |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest Of Europe |

| By Product | Single-Door Refrigerator | |

| Double-Door Refrigerator | Top Freezer | |

| Bottom Freezer | ||

| Side-By-Side Door Refrigerator | ||

| French-Door Refrigerator | ||

| Other Refrigerators | ||

| By Capacity | Less Than 15 cu. Feet | |

| More Than 15 cu. Feet | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-Brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly From The Manufacturers | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest Of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe built-in refrigerator market?

The market stands at USD 7.66 billion in 2026 and is projected to reach USD 9.39 billion by 2031.

Which product type holds the largest share?

Double-door built-in refrigerators lead with 45.12% revenue share as of 2025.

How quickly are online sales growing?

Online retail of built-in refrigerators is advancing at a 6.28% CAGR through 2031, faster than any other channel.

Why are energy regulations important for this market?

EU Ecodesign and F-Gas rules mandate higher efficiency and low-GWP refrigerants, accelerating the replacement of older models and driving new sales.

Which region shows the fastest growth?

The Nordic region is expanding at a 5.63% CAGR to 2031 due to high incomes, sustainability priorities, and early smart-home adoption.

How will raw-material volatility influence pricing?

Continued swings in copper and aluminum prices add 3.5–4.2% to manufacturing costs, which may translate into higher consumer prices unless offset by efficiency gains.

Page last updated on: