Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

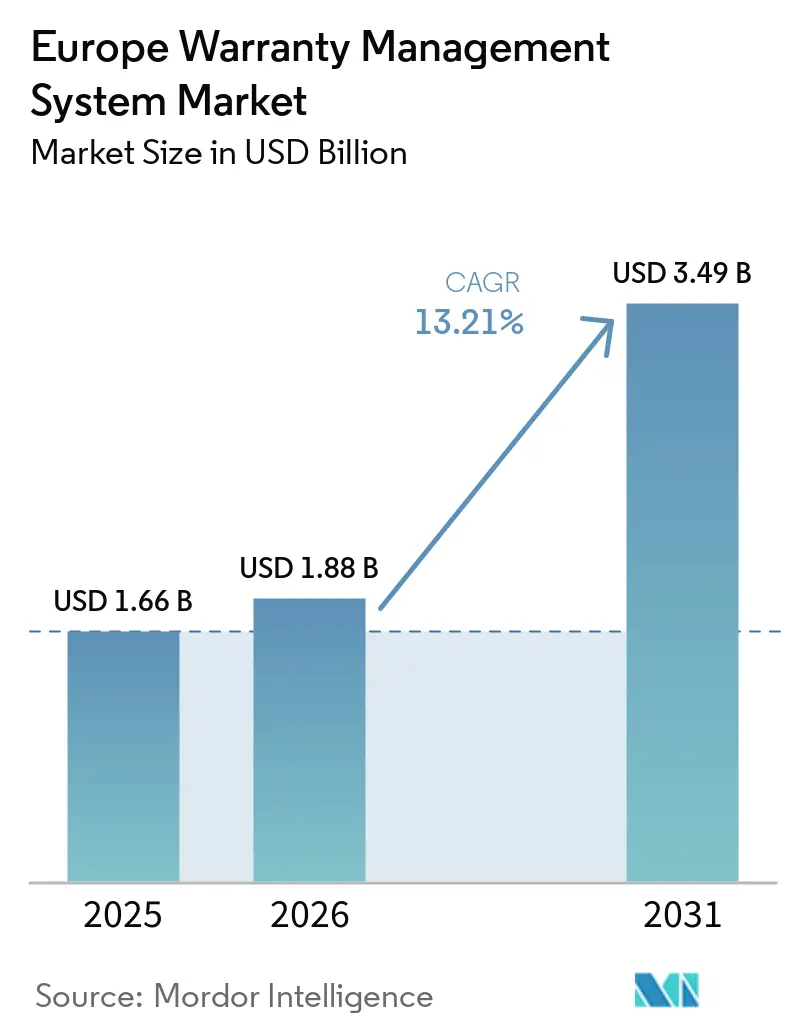

| Base Year Market Size (2025) | USD 1.66 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 3.49 Billion |

| Growth Rate (2026 - 2031) | 13.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Warranty Management System Market Analysis by Mordor Intelligence

The Europe warranty management system market size is expected to increase from USD 1.66 billion in 2025 to USD 1.88 billion in 2026 and reach USD 3.49 billion by 2031, growing at a CAGR of 13.21% over 2026-2031. Expanding cloud-native deployments, tighter EU data-sharing mandates, and rising automotive recall costs continue to redirect spending from legacy on-premise platforms to elastic architectures that support real-time analytics. Manufacturers are prioritizing application programming interface (API) layers and granular consent controls to enable supplier recovery, dealer portals, and third-party repairers to exchange warranty data securely under the EU Data Act. At the same time, predictive failure models that leverage Internet of Things (IoT) telemetry and machine learning are demonstrating 25%-35% cost reductions, prompting enterprises to embed intelligence modules alongside traditional claim processing. Competitive intensity is increasing as Oracle, SAP, and PTC defend enterprise accounts against regional software-as-a-service (SaaS) challengers such as iWarranty and Garanteasy, which package ready-to-run workflows for small- and mid-sized manufacturers and consumer-durable brands.

Key Report Takeaways

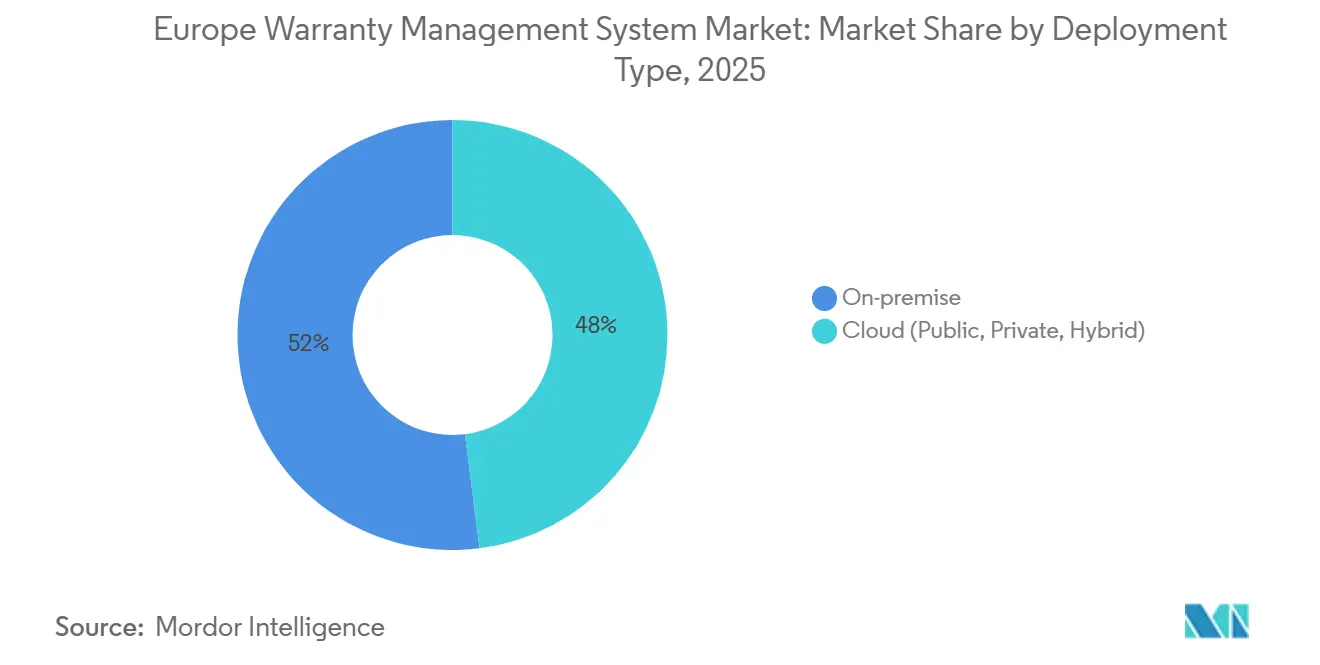

- By deployment type, on-premise installations commanded 52.18% of the Europe warranty management system market share in 2025, while cloud solutions are projected to advance at a 14.12% CAGR through 2031 and capture the fastest growth.

- By software type, claim management led with 41.56% of the Europe warranty management system market share in 2025, whereas warranty intelligence and analytics modules present the highest forecast CAGR at 14.58% to 2031.

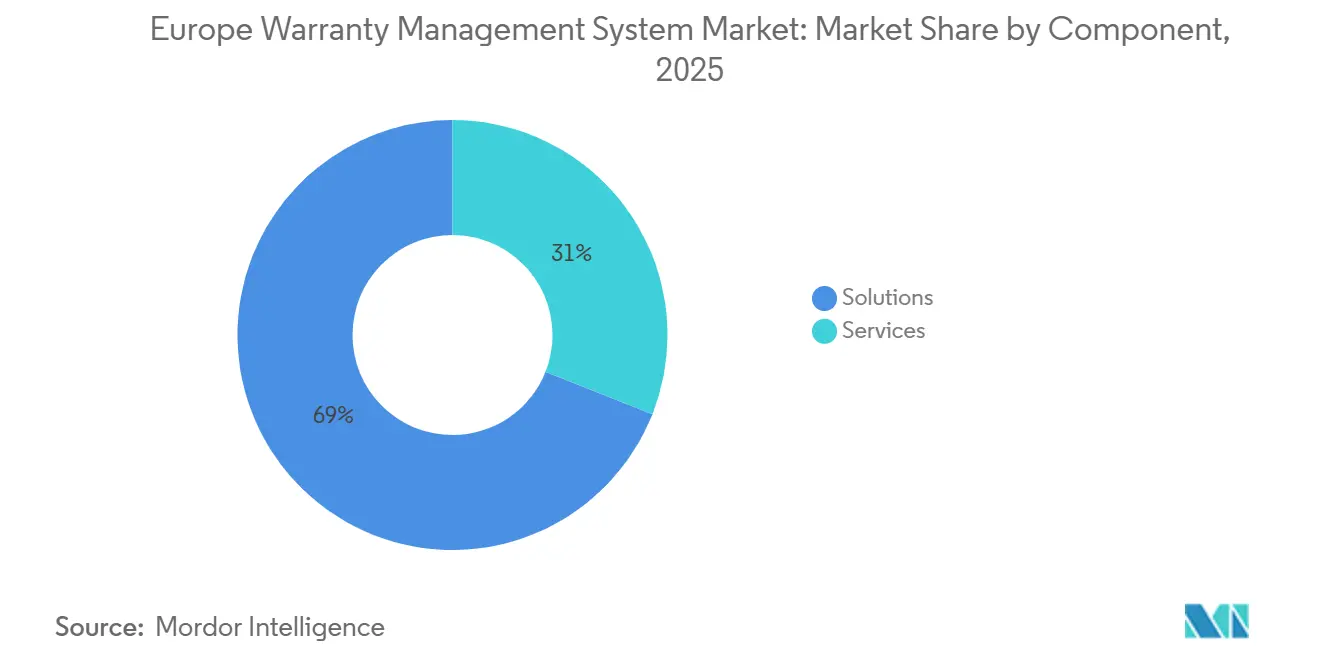

- By component, solutions represented 69.11% of the Europe warranty management system market share in 2025, while services post the fastest expected growth at a 13.55% CAGR through 2031.

- By organization size, large enterprises retained 68.23% of the Europe warranty management system market share in 2025, but small and mid-sized enterprises are expanding at a 14.18% CAGR on the back of subscription-based SaaS pricing.

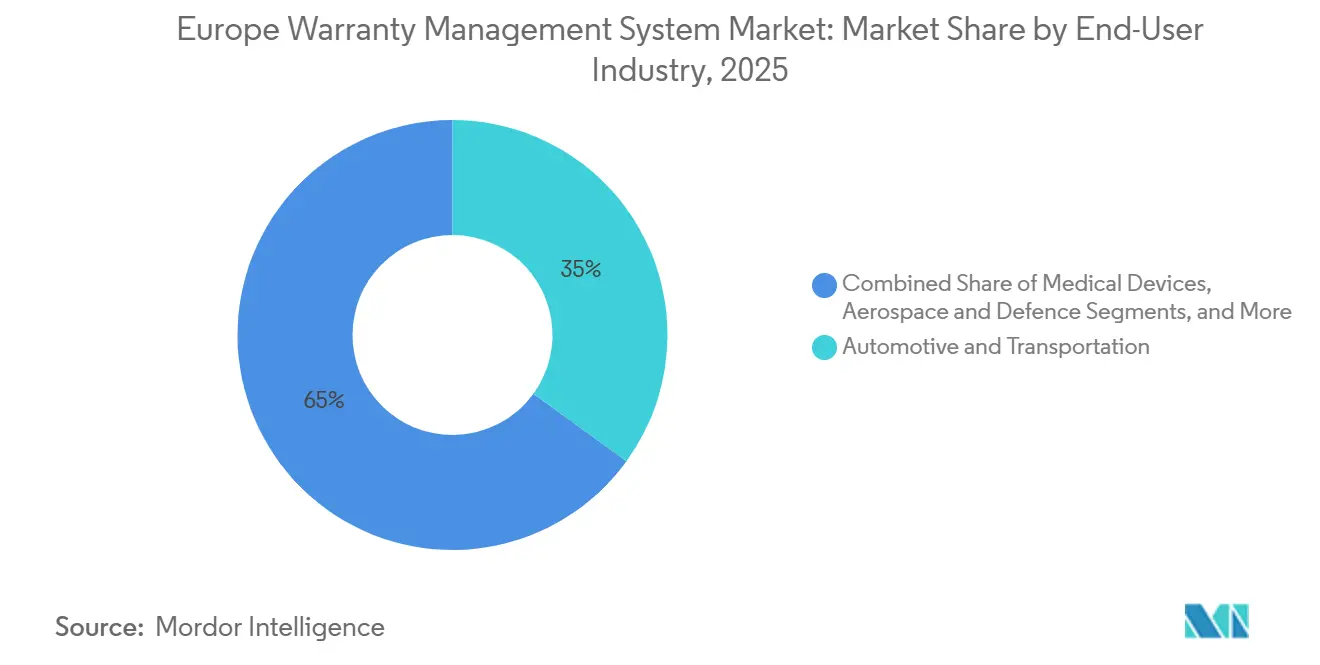

- By end-user industry, automotive and transportation generated 35.17% of the Europe warranty management system market share in 2025, while medical devices post the fastest expected growth at a 13.98% CAGR through 2031.

- By geography, Germany accounted for 22.52% of the Europe warranty management system market share in 2025, and Spain is forecast to post the highest national CAGR at 14.44% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Warranty Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cloud-native deployments in after-sales operations | +2.8% | Germany, France, UK, Benelux, Nordics | Medium term (2-4 years) |

| Increasing European automotive recalls and associated warranty costs | +3.1% | Germany, France, Italy, Spain | Short term (≤ 2 years) |

| Digital transformation mandates under EU Data Act compliance | +2.5% | Pan-European | Medium term (2-4 years) |

| Shift toward predictive analytics for proactive warranty cost reduction | +2.2% | Germany, UK, France | Long term (≥ 4 years) |

| Growing adoption of embedded warranty offerings by OEMs | +1.6% | Germany, UK, Italy | Medium term (2-4 years) |

| ESG-linked pressure to extend product lifecycles and reduce e-waste | +1.3% | Nordics, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cloud-Native Deployments In After-Sales Operations

Manufacturers are migrating from monolithic warranty environments to microservices because elastic compute absorbs telemetry spikes from connected products, shortening rollout cycles from more than a year to under 3 months. Automotive OEMs in Germany and France are already funneling assembly-plant, dealer, and supplier data into unified cloud repositories so that external repairers can retrieve compliant records once the EU Data Act enters force in September 2025.[1]European Commission, “Commission Welcomes Political Agreement on Data Act,” ec.europa.eu Subscription-based SaaS packages priced below EUR 500 (USD 565) per month are attracting Spanish and Italian SMEs seeking to avoid server capital expenditures. This rapid adoption cycle keeps the total cost of ownership low and accelerates the adoption of predictive analytics pilots.

Increasing European Automotive Recalls And Associated Warranty Costs

Automakers paid EUR 26.163 billion (USD 29.57 billion) in 2024 warranty claims, and a single BMW recall required EUR 1 billion (USD 1.13 billion) in provisions. Such pressure drives investment in automated rules engines that reject fraudulent claims and orchestrate supplier chargebacks in hours rather than weeks. The forthcoming Right to Repair directive, which extends warranty periods when customers choose independent repairers, amplifies administrative complexity and favors configurable policy engines. By unifying claim histories with supply-chain quality data, early-warning dashboards can trigger field actions before mass campaigns become inevitable.

Digital Transformation Mandates Under EU Data Act Compliance

The Data Act obligates manufacturers to provide structured warranty and repair data to third parties, forcing API-first architectures that expose claim events, parts usage, and diagnostics without breaching General Data Protection Regulation (GDPR) safeguards. France’s digital-product-passport pilots show how warranty data is converging with circular-economy labeling to demonstrate repairability and carbon footprints. Vendors that ship open connectors to customer-relationship-management (CRM), enterprise-resource-planning (ERP), and field-service systems enjoy a head start as enterprises re-platform ahead of the September 2025 deadline.

Shift Toward Predictive Analytics For Proactive Warranty Cost Reduction

Machine-learning models built on historical claims, IoT feeds, and supplier quality metrics are cutting costs by 25%-35%. European equipment makers that previously paid for no-fault-found returns now filter out up to half of such requests using computer-vision triage. German and UK OEMs with robust data pipelines are leading deployments, but Southern European manufacturers still face skills shortages, reinforcing demand for low-code analytic tooling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented legacy IT landscapes in traditional manufacturing firms | -1.9% | Italy, Spain, Eastern Europe | Medium term (2-4 years) |

| Shortage of skilled warranty data scientists | -1.4% | Southern and Eastern Europe | Long term (≥ 4 years) |

| High initial integration costs for SMEs | -1.1% | Spain, Italy, Portugal | Short term (≤ 2 years) |

| Cybersecurity and GDPR-related concerns over warranty data sharing | -0.8% | Germany, France, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy IT Landscapes In Traditional Manufacturing Firms

Mid-tier suppliers run decades-old ERP and spreadsheet workflows that lack common data schemas, adding 18-36 months of cleansing and interface work before cloud migration can start.[2]Tata Consultancy Services, “Intelligent Automation for Warranty Claims Management,” tcs.com Italian and Spanish plants that still rely on SAP R/3 or Oracle E-Business Suite often face EUR 500,000 (USD 565,000) integration tabs, discouraging adoption until warranty costs exceed 3% of revenue. Parallel domestic and export databases compound the challenge because each set follows different regulatory taxonomies, inflating reconciliation overhead.

Shortage Of Skilled Warranty Data Scientists

45% of European SMEs report a cloud-skills gap, and the share rises in Spain, Portugal, and Poland. Warranty analytics demands cross-disciplinary talent spanning engineering, supply chain, and actuarial science, a mix that rarely exists in a single profile. Consulting firms offer pre-trained models, yet mid-tier firms often outsource analytics to managed service providers, which can introduce latency and limit customization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Adoption Accelerates Under Data-Sharing Mandates

On-premises installation held 52.18% market share, as many organizations, particularly in the manufacturing, automotive, and industrial sectors, prioritize stringent control over their data and IT environments. Cloud solutions are advancing at 14.21% CAGR. In Germany and France, automotive OEMs use cloud (hybrid) architectures, retaining sensitive design data in private clouds while routing dealer claims through public endpoints during recall spikes, ensuring performance remains stable across distributed dealer networks. Southern European SMEs demonstrate a different pattern, skipping hybrid stages altogether and subscribing directly to fully managed SaaS, driven by pay-per-use economics and the ability to roll out in eight weeks. While defense contractors in the United Kingdom still hedge toward private cloud to satisfy security protocols, their share of overall spending is small.

Looking ahead, the European warranty management system market will see on-premises budgets shrink after 2028, when extended support terms for many client-server platforms end. Vendors prepare by packaging lift-and-shift accelerators that migrate rule libraries, claim histories, and supplier contracts into cloud schemas with minimal downtime. As an added incentive, public cloud providers bundle compliance documentation and automated encryption, enabling smaller manufacturers to pass regulatory audits without hiring additional security architects.

By Software Type: Intelligence Modules Emerge As Growth Catalyst

Claim management engines will remain the mandatory backbone for capturing submissions, yet investment momentum is shifting toward intelligence overlays that detect anomalies, predict failures, and orchestrate supplier recovery. The Europe warranty management system market share for claim management stood at 41.56% in 2025, but analytics portfolios, growing at 14.58% CAGR, are becoming a pivotal buying criterion. OEMs now evaluate platforms on the accuracy of predictive maintenance scores, not just the number of configurable claim fields. In Germany, early adopters benchmark cost-avoidance savings, recording 25% reductions within a year of model deployment.

Extended service-contract modules gain traction because automakers and appliance brands embed multi-year coverage into upfront pricing, adding complex renewal and revenue-recognition logic. Parts returns and supplier recovery tools, although niche, generate outsized value by reallocating repair liability back to component makers. Solution providers that furnish visual fault classification, real-time return merchandise authorization (RMA), and automatic debit note creation gain favor with procurement teams that measure performance on recovery yield rather than throughput.[3]Tech Mahindra, “Strengthening Warranty With Supplier Recovery Programs,” techmahindra.com

By Component: Solutions Lead While Services Fill The Skills Vacuum

Solutions accounted for 69.11% of Europe's warranty management system market revenue in 2025, as enterprises still prefer to license configurable software and retain system control. However, services are growing faster with 13.55% as manufacturers confront chronic shortages of warranty data scientists and integration engineers. Global system integrators bundle ticket-based processing, anomaly detection, and supplier outreach under outcome-based pricing models, transferring talent risk to the vendor. Professional-services margins remain robust because large enterprises undertake multi-year re-platforming, absorbing twelve-month data-harmonization exercises that streamline disparate regional workflows into a single European template.

The skills gap ensures that services stay integral to every major rollout. When a Fortune 500 heavy-equipment maker contracted with Infosys BPM, the provider reduced claim-closure time from 15 to under 10 days by redesigning approval hierarchies and introducing optical character recognition capture at dealer portals. Similar engagements across Southern Europe show how blended teams of domain consultants and data scientists expedite returns on analytics investments.

By Organization Size: SMEs Embrace SaaS Despite Budget Friction

Large enterprises retain 68.23% of spending because they shoulder the region’s largest warranty reserves, yet experimentation among small- and mid-sized manufacturers is reshaping vendor roadmaps. SMEs advancing at 14.18% growth gravitate toward subscription bundles that embed best-practice rules and low-code workflow builders, allowing business analysts to tweak coverage parameters without writing Python. Cloud infrastructure credits from hyperscalers cushion early-stage budgets, but funding friction persists; 31% of SMEs still cite capital constraints, reinforcing the popularity of flat-rate packages below EUR 1,000 (USD 1,130) per month.

Market leaders target SMEs by releasing starter editions that cap monthly claim volume while maintaining upgrade paths to enterprise tiers. Community portals share configuration recipes for appliance makers, tool manufacturers, and refurbished-goods resellers, reducing reliance on scarce consultants. As skills marketplaces mature, the European warranty management system market will see an influx of certified administrators offering remote configuration, further lowering entry thresholds for the long-tail customer base.

By End-User Industry: Medical Devices Close The Gap With Automotive

The automotive sector accounted for 35.17% of 2025 spending, due to its vast scale and the significant volume of warranty claims. Medical devices are advancing at a 13.98% CAGR. The manufacturers, incentivized by the EU Medical Device Regulation’s post-market surveillance rules, are investing heavily in traceable, audit-ready warranty workflows. Field evidence capture, adverse-event flagging, and clinical follow-up now funnel through unified portals, linking serial numbers to patient outcomes and supplier batch records.

Industrial equipment, consumer durables, and construction machinery round out substantial opportunity pools. Programs such as Wacker Neuson’s EquipCare tie telematics activation to longer warranty periods, blending predictive maintenance with customer-value propositions. Aerospace remains a niche but strategic sector, as defense ministries demand comprehensive data threads linking design to in-service performance for airworthiness decisions. As vendors tailor blueprints for each vertical, cross-industry feature reuse reduces development cycles and accelerates time-to-value across segments.

Geography Analysis

Germany anchors the European warranty management system market with a 22.52% share in 2025, buoyed by automotive titans whose combined warranty reserves eclipsed EUR 28 billion (USD 32 billion) that year. Early adoption of IoT sensors in factories and vehicles equips German OEMs with ample data to drive predictive analytics and automate supplier recovery automation.[4]European Parliament, “Right to Repair: Parliament Adopts New EU Rules,” europarl.europa.eu The United Kingdom and France form the second tier, propelled by aerospace, defense, and high-tech medical device ecosystems that demand traceable audit trails. France’s investment in digital product passports showcases how warranty modules dovetail with national circular-economy initiatives.

Southern Europe is transitioning rapidly. Spain, forecast to log a 14.44% CAGR through 2031, benefits from vigorous SME adoption of SaaS platforms that comply with both the EU Data Act and the Right to Repair directive. Italian suppliers follow a similar curve but remain constrained by legacy IT and funding limitations. The Netherlands acts as a logistics conduit for pan-European parts returns, amplifying demand for supplier recovery dashboards among electronics importers and refurbishers. Central and Eastern European manufacturers integrate into German supply chains, prompting upgrades to warranty systems that harmonize data exchange formats and accelerate chargeback settlement.

Nordic markets, though smaller, influence sustainability-driven features that prioritize lifecycle extension and e-waste reduction mandates. These countries champion real-time transparency, spurring platform vendors to expose environmental impact metrics alongside conventional claim data. Overall, geographic concentration will persist around Germany, the UK, and France, yet momentum from Spain and integrated Central-European plants will diversify revenue streams and spur localized SaaS innovation.

Competitive Landscape

Top Companies in Europe Warranty Management System Market

The European warranty management system market exhibits moderate concentration, with the top five vendors collectively holding a significant share, leaving substantial room for niche disruptors. Oracle, SAP, PTC, Pegasystems, and Syncron dominate large-enterprise contracts owing to deep ERP and service-lifecycle hooks. PTC’s elevation to Leader status in the 2024 IDC MarketScape validated its IoT-driven approach, positioning warranty as a growth lever rather than a cost sink. Syncron’s 2025 Partner Network rollout illustrates how ecosystem alliances accelerate mid-market penetration and mitigate skills gaps by tapping integrator headcount.[5]PTC, “PTC Named Leader in IDC MarketScape Warranty Assessment,” ptc.com

Regional SaaS specialists intensify price-performance competition. Spain’s iWarranty and the Netherlands-based Garanteasy pre-bundle compliance workflows for Data-Act reporting and multilingual dealer portals. ServiceNow and Salesforce are converting existing CRM clients by adding warranty modules that share customer master records and field-service entitlements, thereby lowering integration hurdles. IBM-Siemens collaborations extend asset-management lineage into heavy equipment, integrating serialized bill-of-materials data with repair histories to improve correct-first-time metrics.

Technology roadmaps concentrate on three axes: predictive analytics, supplier recovery automation, and open APIs. Vendors that deliver low-code model training workbenches, digital twin visualizations, and document intelligence for parts returns gain differentiation. Cybersecurity incidents, such as the 2024 MSI breach that exposed 600,000 records, elevate encryption, zero-trust access, and audit logging from optional to mandatory, further benefiting cloud-first vendors with certified compliance frameworks.

Europe Warranty Management System Industry Leaders

Oracle Corporation

SAP SE

PTC Inc.

Pegasystems Inc.

Syncron AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mercedes-Benz started bundling a 6-year Integrated Service Package within the VLE electric lineup, covering maintenance and high-voltage inspections up to 120,000 km and priced into the EUR 82,260 (USD 93,000) entry variant, reinforcing the shift toward embedded, data-driven warranty offerings.

- January 2026: Alexander Dennis launched a digital warranty management system via its AD24 service portal, aiming to streamline the warranty process for bus operators. The AD24 digital warranty management system went live for UK customers, with plans to roll it out in international markets in the coming months.

- May 2025: Syncron launched its Partner Network to enable systems integrators to implement Syncron Warranty, Analytics, and Supplier Recovery modules, addressing deployment speed challenges in mid-tier manufacturing accounts.

- January 2025: IFS was named the sole Customer’s Choice in the 2025 Gartner Voice of the Customer for Enterprise Asset Management, bolstering its credibility in warranty-heavy asset sectors.

Europe Warranty Management System Market Report Scope

The Europe Warranty Management System Market Report is Segmented by Deployment Type (On-premise, and Cloud), Software Type (Warranty Intelligence and Analytics, Claim Management, Service Contract Administration, and Parts Returns and Supplier Recovery), Component (Solutions, and Services (Professional Services, and Managed Services)), Organization Size (Large Enterprises, and Small and Mid-sized Enterprises), End-user Industry (Automotive and Transportation, Industrial Equipment and Heavy Machinery, Consumer Durables and Home Appliances, Construction and Building Materials, Medical Devices, Aerospace and Defence, and Other End-user Industries), and Country (Germany, United Kingdom, France, Italy, Spain, Netherlands, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Deployment Type

| On-premise |

| Cloud (Public, Private, Hybrid) |

By Software Type

| Warranty Intelligence and Analytics |

| Claim Management |

| Service Contract Administration |

| Parts Returns and Supplier Recovery |

By Component

| Solutions | |

| Services | Professional Services |

| Managed Services |

By Organization Size

| Large Enterprises |

| Small and Mid-sized Enterprises (SMEs) |

By End-user Industry

| Automotive and Transportation |

| Industrial Equipment and Heavy Machinery |

| Consumer Durables and Home Appliances |

| Construction and Building Materials |

| Medical Devices |

| Aerospace and Defence |

| Other End-user Industries |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Deployment Type | On-premise | |

| Cloud (Public, Private, Hybrid) | ||

| By Software Type | Warranty Intelligence and Analytics | |

| Claim Management | ||

| Service Contract Administration | ||

| Parts Returns and Supplier Recovery | ||

| By Component | Solutions | |

| Services | Professional Services | |

| Managed Services | ||

| By Organization Size | Large Enterprises | |

| Small and Mid-sized Enterprises (SMEs) | ||

| By End-user Industry | Automotive and Transportation | |

| Industrial Equipment and Heavy Machinery | ||

| Consumer Durables and Home Appliances | ||

| Construction and Building Materials | ||

| Medical Devices | ||

| Aerospace and Defence | ||

| Other End-user Industries | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current and projected value of the Europe warranty management system market?

The Europe warranty management system market size is forecast to rise from USD 1.66 billion in 2025 to USD 1.88 billion in 2026 and reach USD 3.49 billion by 2031.

Which deployment model is growing fastest in Europe?

Cloud deployments are expanding at a 14.12% CAGR to 2031 because they simplify EU Data Act compliance and shorten rollout cycles.

Why are medical-device firms increasing spending on warranty software?

EU Medical Device Regulation demands continuous post-market surveillance, so device makers integrate warranty claims with clinical follow-up data, driving a 13.98% CAGR for the segment.

How does predictive analytics lower warranty costs?

Machine-learning models that flag high-risk serial numbers before failure have demonstrated 25%-35% reductions in claim payouts among early adopters.

What impact will the Right to Repair directive have on manufacturers?

From Jul 31 2026, warranty periods must extend when consumers choose independent repairers, adding administrative load that favors configurable policy engines over manual processing.

Who are the main vendors in the market?

Oracle, SAP, PTC, Pegasystems, and Syncron lead enterprise accounts, while ServiceNow, Salesforce, and regional SaaS firms such as iWarranty compete for mid-size and SME users.

Page last updated on: