PCR Molecular Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.26 Billion |

| Market Size (2031) | USD 13.31 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

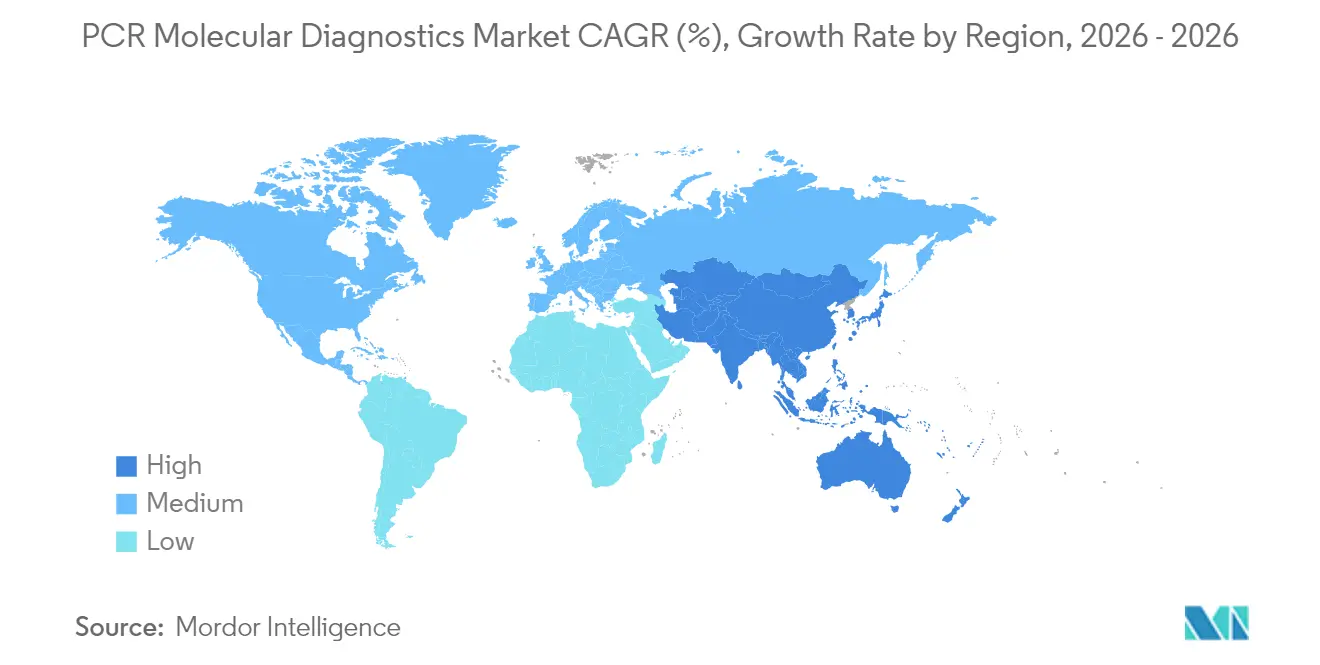

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

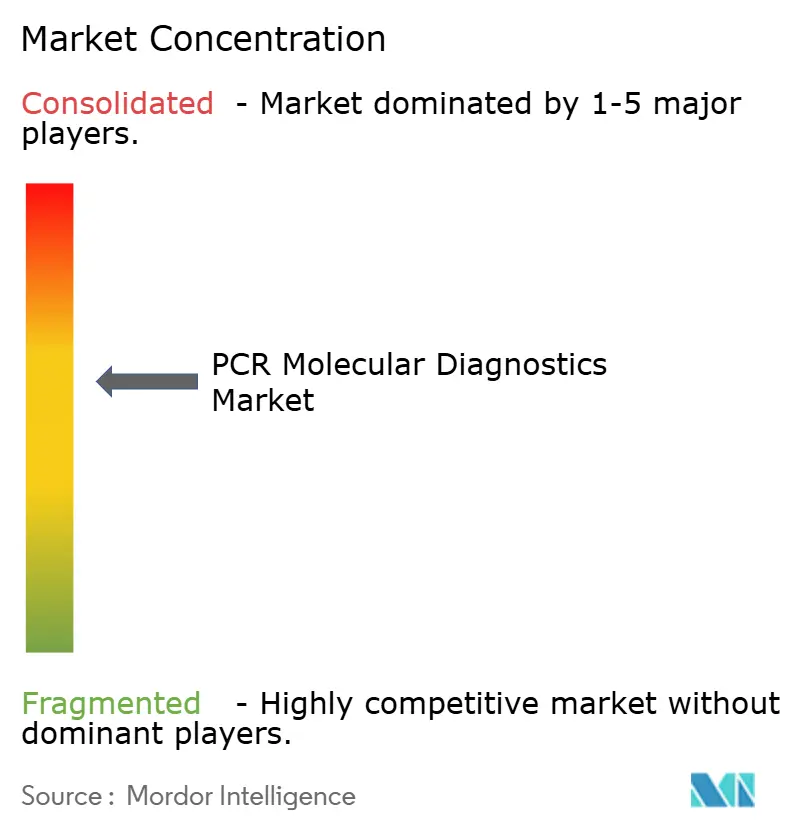

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PCR Molecular Diagnostics Market Analysis by Mordor Intelligence

The PCR Molecular Diagnostics Market size was valued at USD 9.74 billion in 2025 and estimated to grow from USD 10.26 billion in 2026 to reach USD 13.31 billion by 2031, at a CAGR of 5.36% during the forecast period (2026-2031).

Reagents and consumables underpin revenue expansion because every amplification run requires fresh chemistry, while demand for digital PCR systems is accelerating thanks to their 0.01% variant-allele detection thresholds that unlock liquid-biopsy and minimal-residual-disease use cases. Hospitals and reference laboratories continue to dominate test volumes, yet miniaturised platforms are pushing sophisticated assays into emergency departments, oncology clinics and community health centres. North America still captures the largest share at 42% on the strength of well-funded laboratories and supportive reimbursement, but Asia-Pacific represents the fastest-growing geography at a 6.54% CAGR as governments scale precision-medicine budgets. Competitive intensity is rising as incumbents such as F. Hoffmann-La Roche and Thermo Fisher Scientific refresh instrument portfolios, while specialist firms turn to AI-guided assay design and cloud-linked workflows to differentiate. Meanwhile, the United States Food and Drug Administration (FDA) is ending decades of enforcement discretion for laboratory-developed tests, adding compliance costs that will catalyse consolidation across the PCR molecular diagnostics market[1]Food and Drug Administration, “Medical Devices; Laboratory Developed Tests – Federal Register,” Federalregister.gov.

Key Report Takeaways

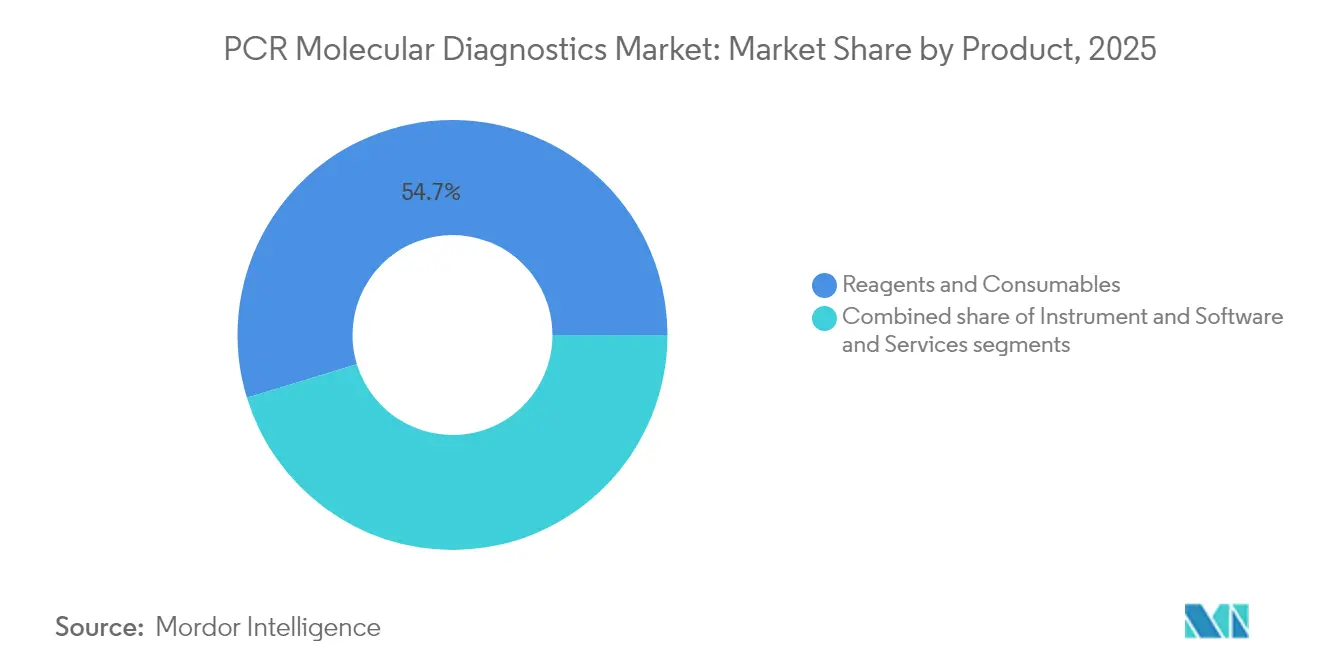

- By product type, reagents and consumables held 54.72% of the PCR molecular diagnostics market share in 2025, whereas digital PCR instruments are on track for the highest 2026-2031 CAGR at 6.86%.

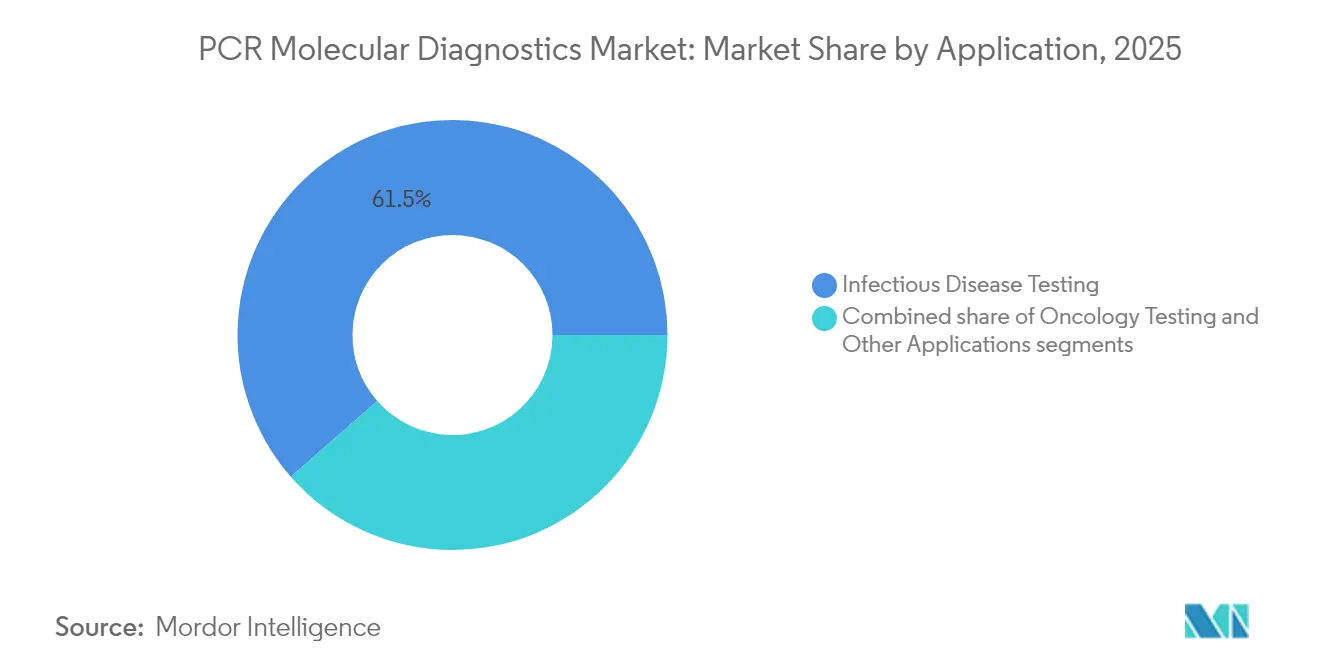

- By application, infectious disease assays led with 61.45% revenue share in 2025; oncology testing is projected to grow at an 7.33% CAGR to 2031.

- By end user, hospitals and reference laboratories contributed 47.35% of the PCR molecular diagnostics market size in 2025, while decentralised point-of-care settings are forecast to post the fastest 7.74% CAGR through 2031.

- By geography, North America commanded 41.62% of 2025 revenue; Asia-Pacific is projected to post the quickest 6.27% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global PCR Molecular Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising infectious-disease and cancer incidence | +1.8% | Global, stronger in North America & Asia-Pacific | Medium term (2-4 years) |

| Technological innovation in PCR chemistry & instrumentation | +1.2% | Global, earliest in North America & Europe | Medium term (2-4 years) |

| Adoption of syndromic & multiplex panels | +0.8% | North America & Europe, growing Asia-Pacific uptake | Short term (≤2 years) |

| Decentralised and point-of-care molecular testing | +0.7% | Rural & underserved regions worldwide | Medium term (2-4 years) |

| Government screening programs & public-health funding | +0.6% | North America, Europe, developed Asia-Pacific | Short term (≤2 years) |

| Rising demand for precision medicine & companion diagnostics | +1.1% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Infectious-Disease and Cancer Incidence

Escalating global disease burdens anchor demand for molecular assays across the PCR molecular diagnostics market. The American Cancer Society anticipates 2,041,910 new cancer diagnoses and 618,000 deaths in the United States during 2025, heightening the urgency for early detection strategies[2]American Cancer Society, “Cancer Facts & Figures 2025,” Cancer.org. Concurrently, paediatric hospitalisations linked to human metapneumovirus rose 17% versus 2023 across the United States and China, underscoring the need for rapid respiratory-virus differentiation. PCR offers attomolar sensitivity, enabling clinicians to guide antivirals, isolate patients more precisely and monitor minimal residual disease after therapy. Because 40% of new cancer cases are considered preventable through earlier detection, payers and policymakers increasingly treat molecular diagnostics as cost-saving rather than discretionary. The result is sustained throughput growth across centralised and near-patient laboratories within the PCR molecular diagnostics market.

Technological Innovation in PCR Chemistry & Instrumentation

Rapid-cycle enzymes, microfluidics and digitisation are rewriting performance benchmarks within the PCR molecular diagnostics market. Extreme-PCR protocols now compress complete thermocycles into 15 seconds, raising hourly sample capacity without raising instrument footprints. Digital PCR partitions reaction volumes into thousands of nanodroplets, reaching 0.01% variant calls that were once the sole province of next-generation sequencing. AI is becoming integral to quality control; Seegene is co-developing a Digitalized Development System with Microsoft that automates primer design and detects signal anomalies in real time. These advances collectively elevate sensitivity, shorten turn-around-time and lower operator variability, thereby expanding oncology monitoring, transplant surveillance and wastewater-based epidemiology within the PCR molecular diagnostics market.

Adoption of Syndromic and Multiplex Panels

Physicians are shifting from single-pathogen ordering to broad, symptom-centred panels that interrogate dozens of targets simultaneously. The BioFire FilmArray Pneumonia Panel demonstrates 96.3% sensitivity and 97.2% specificity while reducing time-to-result from ≥48 hours for culture down to about one hour. Fast, comprehensive data underpin antibiotic-stewardship programmes because clinicians can de-escalate broad-spectrum therapy once the causative organism is known. Laboratories also trim hands-on-time because multiplex cartridges consolidate extraction, amplification and detection. Point-of-care iterations such as BIOFIRE SPOTFIRE deliver answers in 15 minutes, further integrating syndromic testing into emergency and paediatric settings. As antibiotic resistance intensifies, hospitals use multiplex data to update local antibiograms, strengthening the long-run competitive position of the PCR molecular diagnostics market.

Decentralised and Point-of-Care Molecular Testing

Technological miniaturisation is unbundling diagnostics from core laboratories within the PCR molecular diagnostics market. The First Nations Molecular Point-of-Care Testing Program now reaches 100 remote Australian communities, running SARS-CoV-2, HIV and sexually transmitted infection panels directly in rural clinics. Systems such as GeneXpert and SPOTFIRE integrate sample preparation, thermal cycling and result interpretation inside sealed disposable cartridges, limiting biohazard exposure and training requirements. Policymakers increasingly subsidise such deployments to close healthcare-access gaps and strengthen outbreak surveillance. Cloud connectivity further allows real-time result aggregation for regional situational awareness, an advantage that creates continuous reagent demand across the PCR molecular diagnostics market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & consumable costs | –1.0% | Global, strongest in emerging economies | Short term (≤2 years) |

| Regulatory complexity & reimbursement uncertainty | –0.9% | Primarily North America; ripple effects worldwide | Short term (≤2 years) |

| Limited availability of skilled workforce | –0.7% | Global, higher impact in rural & underserved regions | Medium term (2-4 years) |

| Competition from isothermal amplification & CRISPR-based diagnostics | –0.6% | Global, higher impact in point-of-care settings | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs

Cutting-edge digital PCR instruments can exceed USD 250,000 per unit, a barrier for district hospitals that operate under tight capital budgets. Ongoing reagent outlays compound the burden because chemistry often represents 55-65% of lifetime testing expenses. Liquid-biopsy panels cost USD 500–3,000 each, limiting routine oncology follow-up outside high-income markets. Although manufacturing scale and open-channel chemistries are nudging prices downward, the near-term reality is a two-tier diagnostic ecosystem where sophisticated assays cluster in major medical centres. Smaller laboratories therefore outsource samples, extending turn-around-times and tempering volume growth in parts of the PCR molecular diagnostics market.

Regulatory Complexity and Reimbursement Uncertainty

The FDA’s July 2024 final rule ends enforcement discretion for laboratory-developed tests, sequencing compliance deadlines over four years. Each assay must now clear quality-system, adverse-event and pre-market review requirements akin to commercial kits, raising time-to-launch for hospital laboratories. Simultaneously, the Protecting Access to Medicare Act continues to ratchet fee-schedule reductions, complicating cost-recovery for innovative assays. Europe is tightening in-vitro diagnostic regulations under IVDR, while divergent policies across Asia create additional harmonisation headaches. The cumulative burden favours well-capitalised firms and accelerates mergers as smaller players seek regulatory expertise, consolidating power within the PCR molecular diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Digital PCR Drives Next-Generation Precision

Reagents and consumables produced the largest slice of 2025 revenue at 54.72% because every test run mandates fresh primers, probes and buffers, creating a predictable annuity business model inside the PCR molecular diagnostics market. Digital PCR instruments, though currently a minority in installed base, logged the quickest adoption pace due to absolute quantification and orders-of-magnitude gains in analytical sensitivity. For example, Bio-Rad’s droplet partitioning routinely detects rare alleles down to 0.01%, enabling detection of circulating tumour DNA in a standard blood draw. Standard thermocyclers still populate many regional hospitals thanks to lower acquisition costs, whereas real-time systems occupy a middle tier by offering quantitation without the capital intensity of digital.

Software and analytical services are emerging revenue streams as laboratories wrestle with data lakes generated by high-throughput systems. Roche’s LightCycler PRO integrates automatic calibration and robotics to lift walk-away time, and QIAGEN plans more than 100 new QIAcuity assays by 2028 after obtaining CE mark for its syndromic respiratory menu in late 2024. These developments highlight how engineering and bioinformatics advances continue to extend the value proposition of each instrument generation within the PCR molecular diagnostics market.

By Application: Infectious Disease Testing Maintains Dominance

Infectious-disease assays constituted 61.45% of 2025 turnover because clinicians rely on PCR to differentiate pathogens that share overlapping symptoms yet require distinct therapies. Tuberculosis remains a headline example; rapid molecular detection compresses diagnostic timeframes from weeks on solid culture to hours, informing targeted treatment and limiting transmission. Syndromic respiratory panels have become routine during influenza-like-illness seasons, especially where antimicrobial-resistance surveillance is a public-health priority.

Oncology testing is the fastest-growing application, reflecting expanding use of cell-free DNA assays and minimal-residual-disease monitoring. The Shield liquid-biopsy test, for instance, showed an 83.1% sensitivity for colorectal-cancer detection in peer-reviewed evaluation. As targeted therapies and immuno-oncology regimens proliferate, companion diagnostics based on PCR mutation panels are being co-developed with drugs to identify responders earlier. The move toward tumour-agnostic drug approvals further elevates the role of genomic profiling in directing treatment, sustaining double-digit growth for oncology sub-segments of the PCR molecular diagnostics market size through 2031.

By End User: Diverse Settings Expand Testing Access

Hospitals and reference labs generated 47.35% of 2025 revenue. Their economies of scale allow multishift operation of high-throughput thermocyclers and aligned clinical interpretation teams. Reference lab order volumes climbed alongside outreach testing; NeoGenomics, for example, reported 34% clinical next-generation-sequencing revenue growth in its 2024 filing, signalling appetite for complex molecular work-ups.

Academic and research institutes represent the most rapidly increasing user group because translational projects increasingly spin out as laboratory-developed tests. Meanwhile, decentralised environments—urgent-care centres, oncology infusion suites and mobile clinics—are adopting cartridge-based platforms that preserve analytical rigor yet eliminate complex pipetting. The First Nations program in Australia exemplifies how remote site testing can integrate into electronic health records, shrinking diagnostic deserts and growing sample throughput for all vendors operating within the PCR molecular diagnostics industry.

Geography Analysis

North America generated 41.62% of global revenue in 2025. Federal funding streams reinforce this leadership position; the U.S. Defense Health Program’s FY 2025 budget allocates substantial outlays for precision-medicine and genomic-surveillance projects. Large hospital networks frequently run dual platforms—high-throughput core-lab thermocyclers for routine testing and mobile units for operating rooms—creating layered demand across the PCR molecular diagnostics market size. FDA regulatory tightening is expected to spur lab consolidation but also encourage standardisation, possibly elevating U.S. export competitiveness for cleared kits.

Asia-Pacific is forecast to record a 6.27% CAGR through 2031, the fastest worldwide. Governments in China, India and South Korea earmark expanding precision-medicine budgets, while private laboratories race to meet oncology-panel demand. Japan currently leads regional adoption in oncology-focused testing, holding roughly 41% share of that application niche during 2023. Public-health authorities in Southeast Asia embrace point-of-care PCR for dengue and respiratory outbreaks to compensate for central-lab shortages. This multifaceted growth portfolio positions the region as the most dynamic frontier for the PCR molecular diagnostics market.

Europe maintains robust share on the back of universal-health-coverage frameworks and strong academic-industry R&D consortia. Implementation of the In Vitro Diagnostic Regulation is prompting earlier engagement between manufacturers and notified bodies, lengthening approval timelines yet raising device quality and post-market surveillance. In contrast, Latin America, Middle East and Africa constitute nascent but high-potential territories where decentralised platforms circumvent infrastructural deficits. Pilots deploying GeneXpert units in remote clinics illustrate the impact of real-time tuberculosis confirmation on treatment initiation and antibiotic stewardship, gradually stitching these regions into the global PCR molecular diagnostics market value chain.

Regulatory Landscape

In the United States, the Food and Drug Administration (FDA) issued a final rule published May 6, 2024 to phase out general enforcement discretion for laboratory-developed tests (LDTs) over a four-year period, shifting many PCR-based LDT workflows toward medical-device style requirements. This includes quality system, adverse event reporting, and premarket oversight. Under the staged approach, FDA has indicated that labeling requirements for most IVDs offered as LDTs will apply by May 6, 2026, which can increase compliance and documentation workload for providers and feed into decisions on menu rationalization, outsourcing, and consolidation.

In Europe, market access and lifecycle compliance for PCR IVDs continue to be shaped by Regulation (EU) 2017/746 (IVDR) and associated implementing acts that affect how notified bodies run conformity assessments. The European Commission adopted Implementing Regulation (EU) 2026/977 on May 4, 2026 to set more uniform quality-management and procedural requirements for notified body conformity assessment activities under IVDR, with application from February 25, 2027. In parallel, the Commission updated the IVDR harmonised standards list via Implementing Decision (EU) 2026/1313 dated June 15, 2026, reinforcing the role of standards-aligned technical documentation and post-market systems for PCR assay and instrument manufacturers selling in the EU.

Competitive Landscape

Competition blends global scale with niche specialisation. F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific, Inc., and Abbott Laboratories command extensive instrument and reagent portfolios that ensure lock-in across clinical chemistry, immunoassay and molecular disciplines, reinforcing cross-selling synergies. F. Hoffmann-La Roche Ltd. announced a USD 50 billion, five-year U.S. investment programme in April 2025 to enlarge domestic manufacturing, an explicit hedge against supply-chain disruptions.

Mid-sized innovators concentrate on technical differentiation. QIAGEN’s QIAcuity digital PCR platform partitions 96 wells into 26,000 nanoplates, boosting throughput for oncology liquid biopsies, and the firm secured CE mark for its QIAstat-Dx respiratory menu in September 2024. Bio-Rad advances droplet-emulsification IP, while bioMérieux leverages syndromic cartridge know-how to launch SPOTFIRE, a 15-minute respiratory test system targeting urgent-care clinics.

Strategic alliances and acquisitions continue apace. Hologic paid USD 795.0 million for Mobidiag to gain rapid gastrointestinal and sepsis panels, reinforcing its acute-care footprint. Myriad Genetics teamed with PathomIQ in February 2025 to co-develop oncology-focused PCR panels that marry Myriad’s lab network with PathomIQ’s AI analytics. Funding flows into start-ups remain healthy; Deepull Diagnostics raised EUR 50 million in April 2025 to commercialise its UllCore rapid pathogen platform. Those moves illustrate how intellectual-property depth and menu breadth drive bargaining power across the PCR molecular diagnostics market.

PCR Molecular Diagnostics Industry Leaders

Danaher Corp. (Cepheid)

QIAGEN N.V.

Abbott Laboratories

Thermo Fisher Scientific Inc.

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Oncology and infectious disease workflows are creating demand for higher-throughput and more automated PCR operations, particularly where minimal residual disease (MRD) and multiplex panels increase repeat testing and tighten turnaround times. Integrated DNA Technologies (Danaher) is a supply-side example: in April 2026, it expanded its Coralville, Iowa footprint with a greater than threefold increase in oligonucleotide synthesis capacity. That scale-up can support shorter lead times and broader menu expansion for reagent-heavy testing models, where reagents and consumables already represent the largest revenue component of the market.

Decentralization and near-patient adoption are also opening deployment opportunities in settings that cannot support full molecular laboratory infrastructure. In July 2026, QIAGEN opened a demonstration laboratory (QIAGEN Experience Lab) in the Philippines with Hamburg Trading Corporation to support local uptake of molecular technologies, reflecting how vendor-led enablement can extend demand beyond established hospital and reference lab hubs. On the manufacturing side, bioMérieux announced an investment of over EUR 250 million in May 2026 for a new La Balme-les-Grottes, France facility dedicated to BIOFIRE PCR test ranges, pointing to long-cycle commitment to cartridge-based syndromic testing supply under IVDR-driven quality and documentation requirements for the European market.

Recent Industry Developments

- June 2026: Cepheid and the Fleming Initiative launched the TRACE-CPE research study focused on rapid testing for drug-resistant infections. The multi-year evidence-generation effort supports the clinical and health-system case for diagnostics-led antimicrobial stewardship, backing wider adoption of rapid PCR testing protocols in hospitals.

- May 2026: Cepheid received CE marking under the EU IVDR for the Xpert GI Panel, a multiplex PCR test for gastrointestinal pathogens. The clearance broadens the company’s compliant syndromic menu in Europe as IVDR requirements continue to shape portfolio prioritization and documentation depth across manufacturers.

- April 2026: Cepheid and Oxford Nanopore expanded their collaboration to advance a research-use-only workflow for rapid bacterial and fungal pathogen identification. The partnership pairs PCR ecosystem leaders with complementary sequencing capabilities, reinforcing integration of workflows that compress time-to-answer for complex infection identification.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues earned from PCR-based molecular diagnostic testing used to detect and quantify human nucleic acid targets for clinical decision-making, including related instruments, reagents, consumables, and enabling software across routine and near-patient workflows.

Scope exclusions: Research-use-only PCR, veterinary diagnostics, and food testing applications are excluded from this market sizing.

Segmentation Overview

- By Product

- Instrument

- Standard PCR Systems

- Real-time PCR Systems

- Digital PCR Systems

- Reagents & Consumables

- Software & Services

- Instrument

- By Application

- Infectious Disease Testing

- Oncology Testing

- Other Applications

- By End User

- Hospitals

- Diagnostic & Reference Laboratories

- Academic & Research Institutes

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning definitions and demand signals around clinical PCR testing, and then mapping how volumes translate into revenue through product mix and pricing. We relied on public sources such as the World Health Organization, the US CDC, FDA public databases, and similar national health agencies for testing guidance, disease surveillance, and regulatory context that shapes assay adoption.

We also used sources such as OECD health statistics, World Bank indicators, peer-reviewed journals covering molecular diagnostics utilization, and trade and customs statistics to track import trends for instruments and key reagents in major regions. Company filings, investor presentations, press releases, and reputable industry association websites helped validate launch timelines and installed base direction, and also supported review of broad pricing movement. A paid subscription for company financials and a patent database were then used selectively to fill gaps. These examples are not exhaustive, and other sources were reviewed to collect data, cross-check assumptions, and clarify unclear points during the research process.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with lab leaders, procurement stakeholders, and operational managers across hospitals and diagnostic or reference labs, followed by distributors and service partners who see ordering patterns. We used these inputs to confirm test mix shifts (standard vs real-time vs digital PCR), typical reagent attachment to instruments, and realistic ASP ranges by region. When early model totals did not align with field reality, we re-contacted sources to correct mix and pull-through assumptions and then re-ran the model outputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 49% |

| Mid tier: 45% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 17% | Managers: 49% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built by starting from a top-down demand pool, where testing activity, lab throughput, and clinical adoption signals are used to reconstruct addressable PCR diagnostic spend by geography. The totals were then corroborated with selective bottom-up checks using sampled ASP times volume for key consumables, channel feedback on instrument placements, and a limited roll-up of reported diagnostics revenue where PCR exposure is clearly discussed.

The model uses market fingerprints that can be defended on a client call, such as the split between routine and outbreak-driven testing, utilization rates in hospital and reference labs, reagent pull-through per active instrument, service and software attachment behavior, and regional pricing spreads tied to procurement norms and currency timing. For forecasting, scenario analysis was applied so that different paths for infectious disease testing intensity, oncology and genetic test adoption, and replacement cycles for installed instruments could be reflected without forcing one aggressive curve. Where bottom-up data was incomplete for smaller geographies, gaps were handled through proxy assumptions anchored to comparable markets, followed by adjustments after interview validation.

Data Validation & Update Cycle

Outputs were checked against independent signals, including known testing guideline changes, public health surveillance direction, and the implied spend per test after applying realistic reagent usage and pricing. We ran variance checks by region and by major cost component, then escalated outliers for review so one-off events did not distort the base case.

Before sign-off, the model and assumptions go through multiple analyst review steps, and sources are re-contacted when a key input moves outside expected bounds. Reports refresh annually, with interim updates when material events occur, and we complete a final pre-delivery pass so clients receive the most current view available at the time.

Mordor Intelligence's Pcr Molecular Diagnostics Market Estimate Compared With Other Published Estimates

Published market values for PCR molecular diagnostics can vary because groups do not always count the same revenue streams, and they also pick different base years and currency timing. Differences can also show up when one estimate leans more on shipment proxies, while another leans on testing demand indicators, which can move in different directions.

The table points to a wide spread that is mainly explained by scope and what is treated as clinical PCR revenue versus adjacent molecular tools, and then by how fast pricing is assumed to normalize after surge periods. Under Mordor Intelligence's scope, the total is anchored to clinical PCR workflows and includes instruments, reagents and consumables, and enabling software, while excluding research-only and non-human uses, which avoids inflating the spend pool with nearby but non-clinical demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.26 B (2026) | |

| Trade Journal B | USD 8.80 B (2026) | Uses a narrower bill-of-materials view that undercounts software and recurring service revenue, and it appears to apply conservative ASP erosion without validating reagent pull-through with lab-side interviews. |

| Regional Consultancy A | USD 25.55 B (2024) | Blends broader PCR-related categories and adjacent molecular testing revenues into one figure, and it also compares an earlier-year value without clearly normalizing for post-surge testing volumes or consistent currency conversion timing. |

Reading the three figures together, the gap is not just about growth expectations, it is mostly about what is counted and how pricing and utilization are normalized to a clinical testing reality. Our approach stays traceable to practical inputs like test mix, utilization, and consumable attachment, which makes the estimate easier to repeat and stress-test when assumptions change.

Key Questions Answered in the Report

How large is the PCR molecular diagnostics market today?

The market generated USD 10.26 billion in 2026 and is set to climb to USD 13.31 billion by 2031, reflecting a 5.36% CAGR.

Which product category generates the highest revenue?

Reagents and consumables account for 54.72% of total revenue because every amplification run consumes fresh primers, probes and buffers.

Why are digital PCR systems gaining popularity?

Digital platforms detect variant alleles down to 0.01%, enabling liquid-biopsy and minimal-residual-disease monitoring that traditional real-time PCR cannot support.

Which region is growing the fastest?

Asia-Pacific is projected to expand at a 6.27% CAGR through 2031, driven by healthcare-infrastructure upgrades and rising precision-medicine budgets.

How will new FDA regulations affect the market?

The FDA will phase out enforcement discretion for laboratory-developed tests, increasing compliance costs and prompting consolidation among smaller laboratories.

What is the main barrier to wider adoption in emerging markets?

High capital investment for instruments and ongoing consumable costs remain the primary hurdles for laboratories operating under constrained budgets.

Page last updated on: