Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.61 Billion |

| Market Size (2026) | USD 12.14 Billion |

| Market Size (2031) | USD 15.17 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

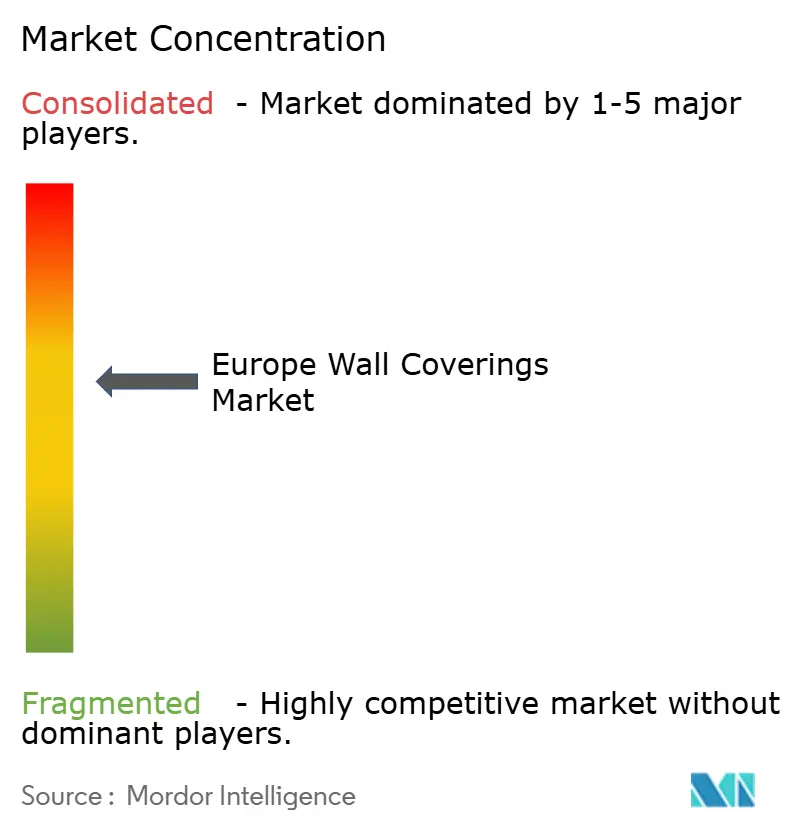

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wall Coverings Market Analysis by Mordor Intelligence

Europe wall coverings market size in 2026 is estimated at USD 12.14 billion, growing from 2025 value of USD 11.61 billion with 2031 projections showing USD 15.17 billion, growing at 4.56% CAGR over 2026-2031. The market’s resilience rests on renovation-led demand, heightened do-it-yourself activity, and strict environmental regulations that favor eco-certified products. Vinyl maintains dominance through durability and cost advantages, yet wood-based alternatives gain momentum as sustainability credentials strengthen. Wallpaper remains the largest product category, although wall panels accelerate on the back of modular construction adoption and 3-D printing customization. Hospitality renovations ahead of marquee international events continue to anchor commercial demand, while rising disposable incomes stimulate residential upgrades, particularly in Eastern Europe.

Key Report Takeaways

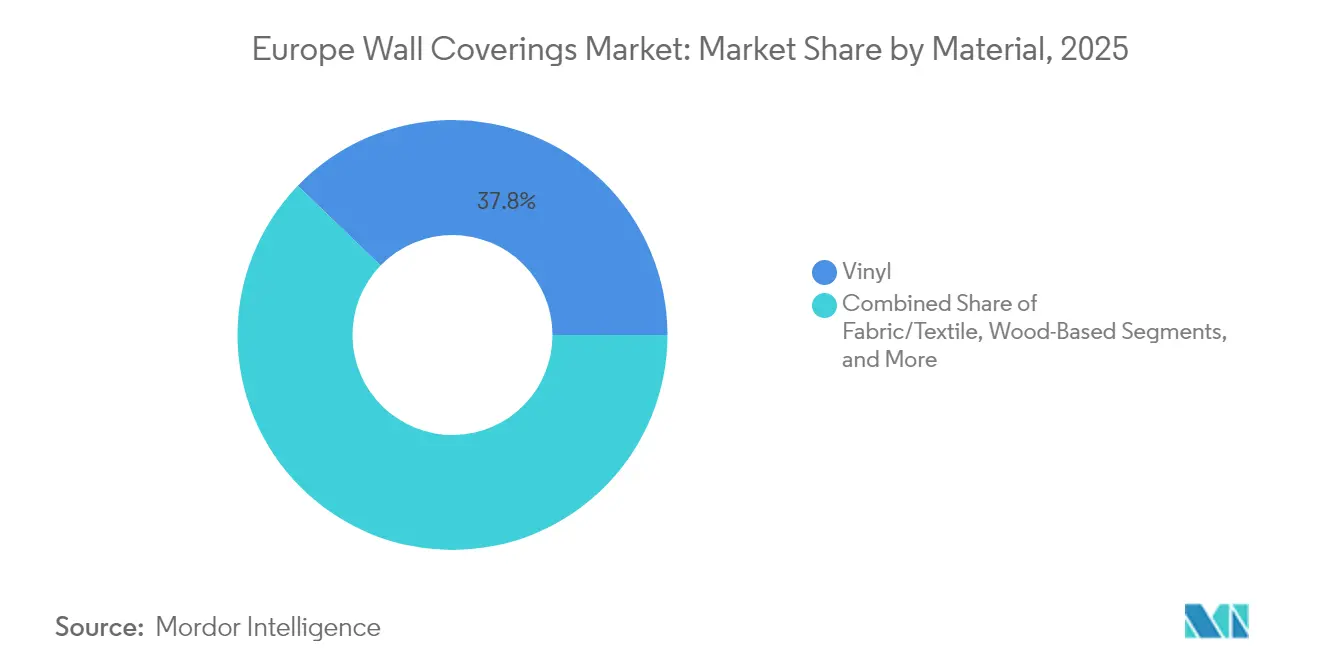

- By material, vinyl led with 37.78% Europe wall coverings market share in 2025, whereas wood-based materials posted the highest 5.21% CAGR through 2031.

- By product type, wallpaper accounted for 39.88% of the Europe wall coverings market size in 2025, while wall panels registered the fastest 5.55% CAGR to 2031.

- By end-use industry, hospitality captured 28.05% of the Europe wall coverings market size in 2025, and domestic housing expanded at a 6.41% CAGR over the forecast period.

- By country, the United Kingdom held 39.00% of the Europe wall coverings market share in 2025, while Poland exhibited the strongest 6.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Wall Coverings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing DIY home-improvement culture | +0.8% | UK, Germany, Scandinavia | Medium term (2-4 years) |

| Revival of heritage buildings and public-funded renovations | +0.6% | France, Italy, Central Europe | Long term (≥ 4 years) |

| Rapid e-commerce penetration in home-decor | +0.5% | Global Europe, strongest in Northern Europe | Short term (≤ 2 years) |

| Shift toward low-VOC and eco-certified coverings | +0.7% | Germany, Netherlands, Nordic countries | Medium term (2-4 years) |

| Hospitality refurbishment boom ahead of 2030 Olympics and EXPOs | +0.4% | France, Italy, Spain | Short term (≤ 2 years) |

| 3-D printed customised wall panels | +0.3% | Germany, Netherlands, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing DIY Home-Improvement Culture

European households increasingly adopt self-directed renovation to bypass costly labor, a tendency propelled by abundant online tutorials and retailer training sessions. Specialty stores captured 30.21% channel share in 2024 by offering in-store demonstrations and advisory services. Labor costs that exceed EUR 35 per m² in Northern Europe encourage wider uptake of peel-and-stick wallpaper and modular panels that novices can apply with limited tools. Fragmented contractor markets-81,000 painting companies in France alone-underscore the potential for substitution by user-friendly materials. Advanced adhesives and pre-finished surfaces preserve professional aesthetics while reducing installation time, deepening consumer confidence in do-it-yourself solutions.

Revival of Heritage Buildings and Public-Funded Renovations

Europe’s Renovation Wave earmarks EUR 500 billion for energy and aesthetic upgrades to historical structures, guaranteeing multi-year demand for compliant wall coverings.[1]European Commission, “Renovation Wave Strategy-Building Envelope Improvements,” europa.eu Conservation projects often stipulate fabric or paper-based finishes that replicate original textures, generating premium orders for artisanal suppliers. Fiscal incentives such as France’s heritage tax relief and Italy’s superbonus fuel owner participation. Custom reproduction and low-VOC mandates raise material complexity and favor local manufacturing that can meet tight specification windows. Central Europe’s dense catalog of heritage sites positions the region as a long-run demand hotspot.

Rapid E-Commerce Penetration in Home-Décor

Omnichannel retail surges as consumers research online, then verify texture and color in store. Franchise outlets combine brand consistency with neighborhood access, achieving 6.21% CAGR. Direct-to-consumer portals empower boutique producers to bypass wholesalers, enabling customized wallpaper runs with augmented-reality previews. Logistics improvements cut transit damage rates for fragile rolls, while instant-quote software simplifies cross-border shipping. Small manufacturers from Belgium and the Netherlands leverage digital platforms to enter the wider Europe wall coverings market without sizable capital outlays.

Shift Toward Low-VOC and Eco-Certified Coverings

Regulators tighten formaldehyde thresholds below 0.1 ppm under REACH, accelerating the shift from solvent-based vinyl to wood and non-woven substrates. Wood-based coverings log a 5.43% CAGR by integrating FSC-certified fibers and bio-adhesives. EMICODE labeling becomes a procurement prerequisite for healthcare and childcare facilities. German innovators pilot mycelium composites that meet durability standards while biodegrading at the end of life. Compliance costs heighten market entry barriers, nudging smaller import-reliant firms toward partnership or acquisition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive post-inflation consumer sentiment | -0.9% | Southern Europe, Eastern Europe | Short term (≤ 2 years) |

| Tightened building-fire codes limiting vinyl wallpaper share | -0.4% | UK, Germany, Scandinavia | Medium term (2-4 years) |

| Volatile titanium-dioxide prices pressuring margins | -0.6% | Global Europe, strongest impact in Germany, Netherlands | Short term (≤ 2 years) |

| Ageing labor force in skilled wall-covering installation | -0.5% | Western Europe, particularly Germany, France, Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Post-Inflation Consumer Sentiment

Persistently high living costs compress discretionary home-improvement budgets in price-conscious regions. Wall covering prices climbed 2.3% year-over-year in Q1 2025, outpacing broader CPI and curbing demand for premium designs. Hospitality operators in Southern Europe delay nonessential refurbishments, reallocating funds to energy upgrades. Polish façade refurbishments cost USD 37–62 per m², with materials composing up to 70% of the spend, magnifying the hit of raw-material inflation.[2]Polish Construction Statistics, “Renovation Cost Analysis 2025,” gus.gov.pl Manufacturers counter by streamlining SKUs and expanding value lines to protect volume without eroding brand equity.

Tightened Building-Fire Codes Limiting Vinyl Wallpaper Share

Post-Grenfell investigations catalyze stricter flame-spread and smoke-toxicity thresholds, curbing vinyl use in public and multi-family buildings. Alternative substrates such as fiberglass-reinforced paper gain approval despite higher cost. Extended testing and certification impose extra lead times and capital outlay for vinyl suppliers. Scandinavian hotel chains pivot toward non-woven solutions to ensure code compliance, eroding vinyl’s historical lead in commercial interiors. Producers invest in halogen-free additives and top coats, yet uptake remains cautious pending full-scale validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Vinyl Dominance Challenged by Wood-Based Innovation

Vinyl accounted for 37.78% of the Europe wall coverings market share in 2025, upheld by antimicrobial finishes and cleanability that suit healthcare corridors. Nevertheless, environmental pressure and fire-code revisions temper its long-term outlook. Wood-based coverings capitalize on sustainability and tactile warmth, registering a 5.21% CAGR through 2031 while attracting residential renovators and luxury hospitality brands. The Europe wall coverings market size contribution from recycled cellulose and mycelium composites is small today but rising as pilot programs scale. Vinyl producers deploy closed-loop recycling and bio-plasticizers to defend share, whereas paper and fabric makers leverage FSC supply chains and water-based inks to court eco-certified projects.

Demand polarization intensifies: high-traffic commercial venues favor robust vinyl, while premium boutiques and heritage sites opt for low-emission wood veneers. Fabric coverings extend into acoustic applications by laminating wool or hemp fibers onto mineral boards. Paper-based wallpaper enjoys a niche in conservation renovations, aided by digital heritage pattern archives that facilitate accurate reproductions. Metal and ceramic substrates satisfy laboratory and food-processing zones where hygiene and chemical resistance outrank aesthetics.

By Product Type: Wall Panels Accelerate Through Modular Construction

Wallpaper retained 39.88% of the Europe wall coverings market size in 2025 thanks to ubiquitous roll formats, diverse prints, and rising peel-and-stick variants. Yet wall panels increased 5.55% CAGR as prefabricated buildings and flexible offices demand quick, dry installation. Large architects specify panels with integrated cable channels and acoustic cores, reducing post-fit alterations. 3-D printed panel offerings enlarge design scope, while digital wallpaper printing tailors small-batch motifs for boutique hotels. Tile and metal products address hygiene-critical environments and contemporary commercial settings.

The Europe wall coverings market experiences cross-fertilization: wallpaper producers launch clip-on panel ranges, and panel specialists offer complementary trim and corner guards. Consumers appreciate wall panels’ ability to conceal uneven substrates without intensive surface prep, lowering overall project time. In multi-family retrofits, combination schemes emerge, pairing feature-wall panels with cost-effective wallpaper on secondary surfaces.

By End-Use Industry: Domestic Housing Momentum Drives Growth

Domestic housing delivers the fastest 6.41% CAGR as pandemic-induced home-centric lifestyles persist. Home offices and wellness areas spur the adoption of textured panels and nature-inspired wallpaper. The Europe wall coverings market benefits from mortgage-rate incentives in Western Europe and EU renovation subsidies in Central Europe. Hospitality keeps the volume crown, commanding 28.05% share in 2025 through cyclical refurbishments and strict branding guidelines. Healthcare maintains a steady pipeline, requiring antimicrobial, easy-clean surfaces. Retail layouts rotate rapidly to sustain customer engagement, reinforcing repeat orders for removable coverings.

Facility managers increasingly specify wall systems that couple visual refresh with resilience to disinfectants. Case studies such as the Metrodora Institute demonstrate the adoption of seamless medical-grade panels delivering infection-control compliance without sacrificing biophilic aesthetics. Corporate campuses favor demountable partitions to accommodate hybrid work patterns, combining writable surfaces with acoustic dampening.

By Distribution Channel: Franchise Expansion Transforms Retail Landscape

Specialty stores held a 29.90% share in 2025 by providing sample libraries and on-site color matching, anchoring consumer trust. Franchise networks grow 5.97% CAGR, driven by scalable branding and uniform service standards across regions. E-commerce accelerates as interactive visualization tools and live chat consultation replicate showroom experiences online. The Europe wall coverings market witnesses manufacturers investing in direct-to-consumer portals that offer curated design bundles, adhesives, and instructional videos.

Installation services evolve: retailers partner with vetted contractors, bundling product and labor warranties. Omnichannel approaches integrate click-and-collect options, enabling customers to inspect the texture before finalizing orders. For commercial clients, distributors deploy virtual mock-ups that overlay coverings onto CAD layouts, expediting specification cycles.

Geography Analysis

The United Kingdom accounted for 39.00% of the Europe wall coverings market in 2025, driven by vibrant renovation activity and robust DIY chains. Favorable mortgage refinancing and cultural emphasis on property investment motivate homeowners to refresh interiors regularly. Stricter post-Grenfell fire codes reshape material mix toward low-smoke-emitting substrates, opening space for non-woven and intumescent-coated panels. E-commerce growth accelerates via national courier networks that offer next-day delivery for wallpaper rolls and panel kits.

Germany and France illustrate mature yet distinct profiles. German firms intertwine advanced automation with circular-economy initiatives, yielding export-ready eco-certified offerings. Domestic demand softens amid demographic headwinds, but retrofit programs anchored in energy-saving mandates sustain baseline volumes. French consumers display affinity for high-design motifs and heritage-compliant fabrics. Inflation lifted wall covering prices by 2.3% in Q1 2025, though tax incentives for energy upgrades indirectly boost interior refurbishment budgets.

Poland spearheads growth with a 6.79% CAGR through 2031 as EU funds modernize aging housing stock and build public infrastructure. Rising wages stimulate private renovations, and local installers expand capacity to address demand surges. Spain and Italy rely on hospitality refurbishments as tourist arrivals normalize, funneling capital into boutique hotels and vacation rentals. Nordic countries maintain steady expansion by specifying zero-VOC and cradle-to-grave certified coverings in both residential and public buildings. The remainder of Eastern Europe records varied trajectories, contingent on macroeconomic resilience and EU convergence progress.

Competitive Landscape

The Europe wall coverings market exhibits moderate concentration: leading five brands command roughly 45% combined share, leaving room for regional specialists. Companies differentiate through technology, sustainability portfolios, and integrated distribution. 3-D printing lines from Dutch pioneers and German conglomerates enable bespoke panel production without tooling delays, shortening design-to-installation cycles. Patent filings in bio-based binders and recycled content surged during 2024-2025, underscoring R&D intensity.[3]European Patent Office, “Patent Activity in Bio-Based Materials,” epo.org

Strategic alliances emerge between material suppliers and installer networks to mitigate labor shortages and guarantee workmanship quality. Some manufacturers launch training academies that certify contractors on new panel systems, enhancing product reliability and brand loyalty. M&A activity targets complementary capabilities: large vinyl producers acquire wood-veneer startups to diversify material mix, while specialty wallpaper houses absorb digital print boutiques to expand custom offerings.

Titanium dioxide prices peaked at EUR 2,900 per ton (USD 3388.01 per ton) in 2025, compressing margins for producers reliant on pigmented coatings. Firms hedge through long-term supply contracts and formulation optimization. Sustainability commitments intensify; Akzo Nobel publicly tied executive compensation to carbon-footprint reduction, mirroring industry-wide governance trends. Forward-looking competitors pilot smart wall coverings with embedded sensors, positioning for future demand in health monitoring and workspace analytics.

Europe Wall Coverings Industry Leaders

Ahlstrom-Munksjö Oyj

Akzo Nobel N.V.

A.S. Création Tapeten AG

Arte International N.V.

Benjamin Moore & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MSI introduced Exotika large-format porcelain tiles with advanced texturing for luxury wall applications.

- February 2025: Grandeco WallFashion debuted a spring range featuring natural fibers and eco-certified coatings.

- January 2025: Benjamin Moore expanded digital color consultation services, enhancing specification accuracy for professional projects.

- January 2025: Armstrong World Industries reported architectural specialties revenue growth on strong healthcare and education demand for modular wall systems.

Europe Wall Coverings Market Report Scope

Wall coverings protect the wall surface from accidental marks or scratches, besides imparting an air of quality and grandeur to uncovered walls. Wall coverings further help in neutralizing interiors of a building and customizing it with the help of various colors and patterns. These coverings are also cost-effective. The European wallcoverings market report is segmented based on products, applications, and countries. Based on the type of product, the market is divided into wallpaper, wall panel, decorative tile, metal, and other products. Based on application, the market is largely divided into commercial and non-commercial segments. The commercial application segment includes, official, commercial, institutional, industrial, and other non-residential buildings.

By Material

| Paper-Based |

| Fabric/Textile |

| Wood-Based |

| Vinyl |

| Other Materials |

By Product Type

| Wall Panel | |

| Wallpaper | Vinyl Wallpaper |

| Non-woven Wallpaper | |

| Paper-based Wallpaper | |

| Fabric Wallpaper | |

| Other Wallpaper Types | |

| Tile | |

| Metal Wall Covering | |

| Other Product Types |

By End-use Industry

| Hospitality |

| Healthcare |

| Retail |

| Corporate Offices |

| Education |

| Domestic Housing |

| Industrial Facilities |

| Other End-use Industries |

By Distribution Channel

| Specialty Store |

| Franchise store |

| E-commerce |

| Other Distribution Channels |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Poland |

| Rest of Europe |

| By Material | Paper-Based | |

| Fabric/Textile | ||

| Wood-Based | ||

| Vinyl | ||

| Other Materials | ||

| By Product Type | Wall Panel | |

| Wallpaper | Vinyl Wallpaper | |

| Non-woven Wallpaper | ||

| Paper-based Wallpaper | ||

| Fabric Wallpaper | ||

| Other Wallpaper Types | ||

| Tile | ||

| Metal Wall Covering | ||

| Other Product Types | ||

| By End-use Industry | Hospitality | |

| Healthcare | ||

| Retail | ||

| Corporate Offices | ||

| Education | ||

| Domestic Housing | ||

| Industrial Facilities | ||

| Other End-use Industries | ||

| By Distribution Channel | Specialty Store | |

| Franchise store | ||

| E-commerce | ||

| Other Distribution Channels | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe wall coverings market?

The market is valued at USD 12.14 billion in 2026 and is projected to reach USD 15.17 billion by 2031.

Which material leads sales in Europe?

Vinyl remains the leading material, representing 37.78% of 2025 revenue because of durability and easy maintenance.

Which segment is expanding the fastest?

Wood-based wall coverings grow at 5.21% CAGR through 2031, driven by sustainability preferences and bio-adhesive innovations.

Which country offers the strongest growth potential?

Poland leads with a 6.79% CAGR, supported by EU funding and rising household incomes.

Why are wall panels gaining popularity?

Modular construction, quick installation, and 3-D printing customization spur a 5.55% CAGR for wall panels across Europe.

How strict are environmental regulations affecting the industry?

REACH and national indoor-air regulations cap formaldehyde at 0.1 ppm, pushing demand toward low-VOC and eco-certified products.

Page last updated on: