Europe Viscosupplementation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

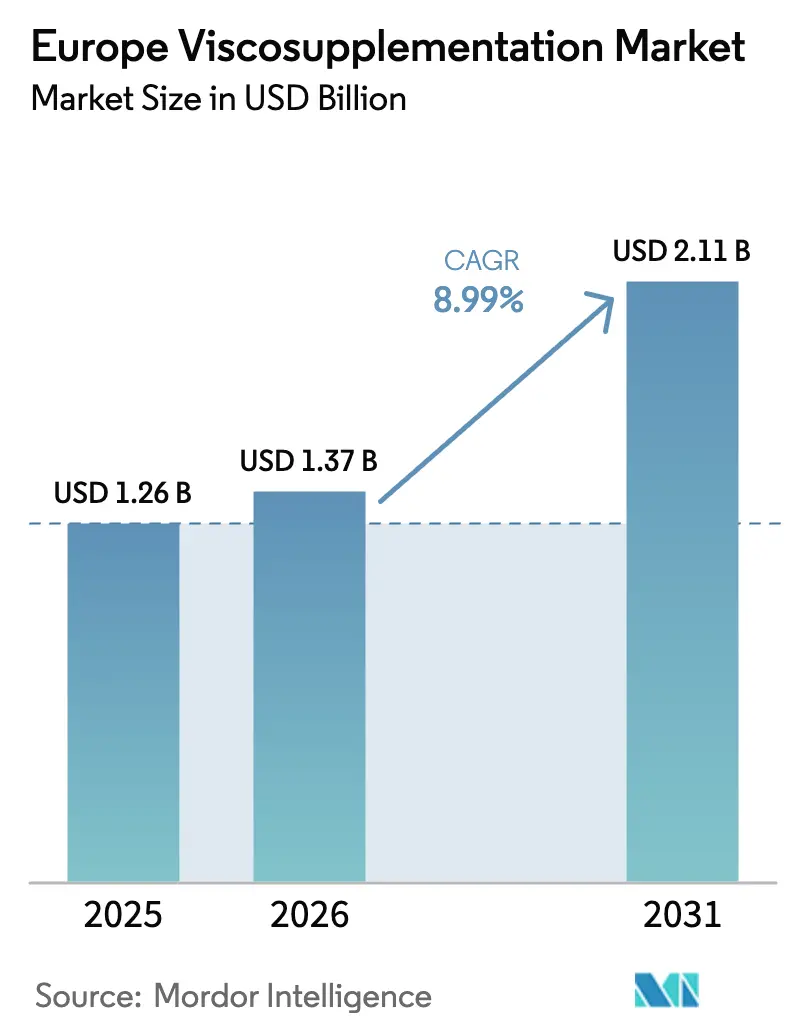

| Base Year Market Size (2025) | USD 1.26 Billion |

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 8.99% CAGR |

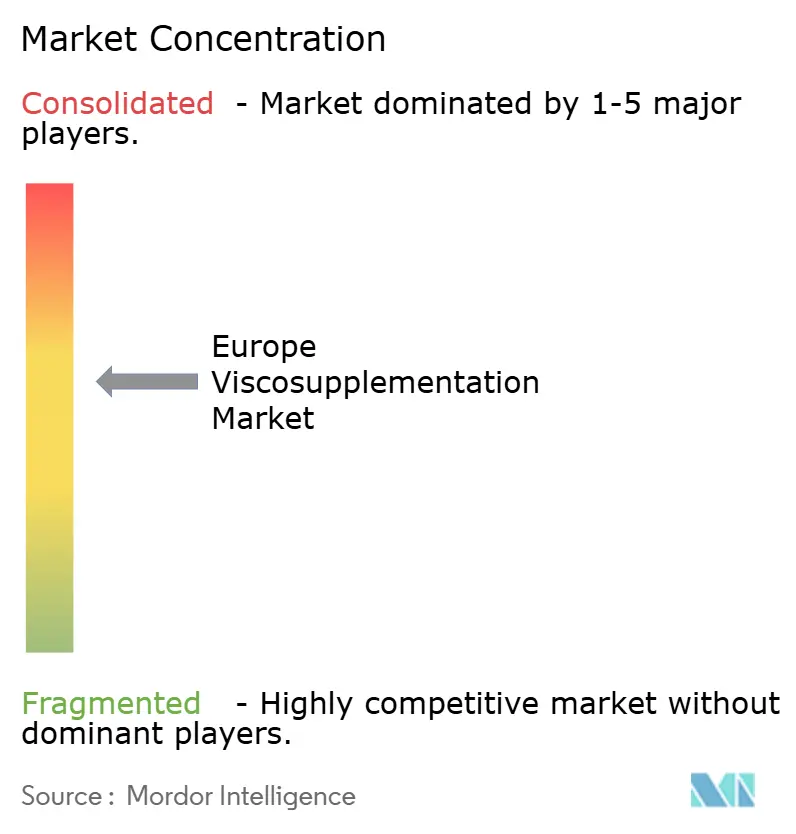

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Viscosupplementation Market Analysis by Mordor Intelligence

Europe viscosupplementation market size in 2026 is estimated at USD 1.37 billion, growing from 2025 value of USD 1.26 billion with 2031 projections showing USD 2.11 billion, growing at 8.99% CAGR over 2026-2031. In the short term, the growth reflects aging demographics, obesity‐related joint degeneration, and steady reimbursement expansion across the EU-5. Mid-term momentum stems from rapid adoption of single-injection hyaluronic acid (HA) products that cut clinic visits and align with outpatient care models. Long-term prospects are bolstered by regulators harmonizing Class III device pathways under EU-MDR 2021, encouraging larger manufacturers to invest in post-market evidence while smaller firms seek partnerships. Rising ambulatory surgical center (ASC) capacity widens access to cost-effective procedures, positioning viscosupplementation as a financially attractive bridge between conservative therapy and total knee replacement.

Key Report Takeaways

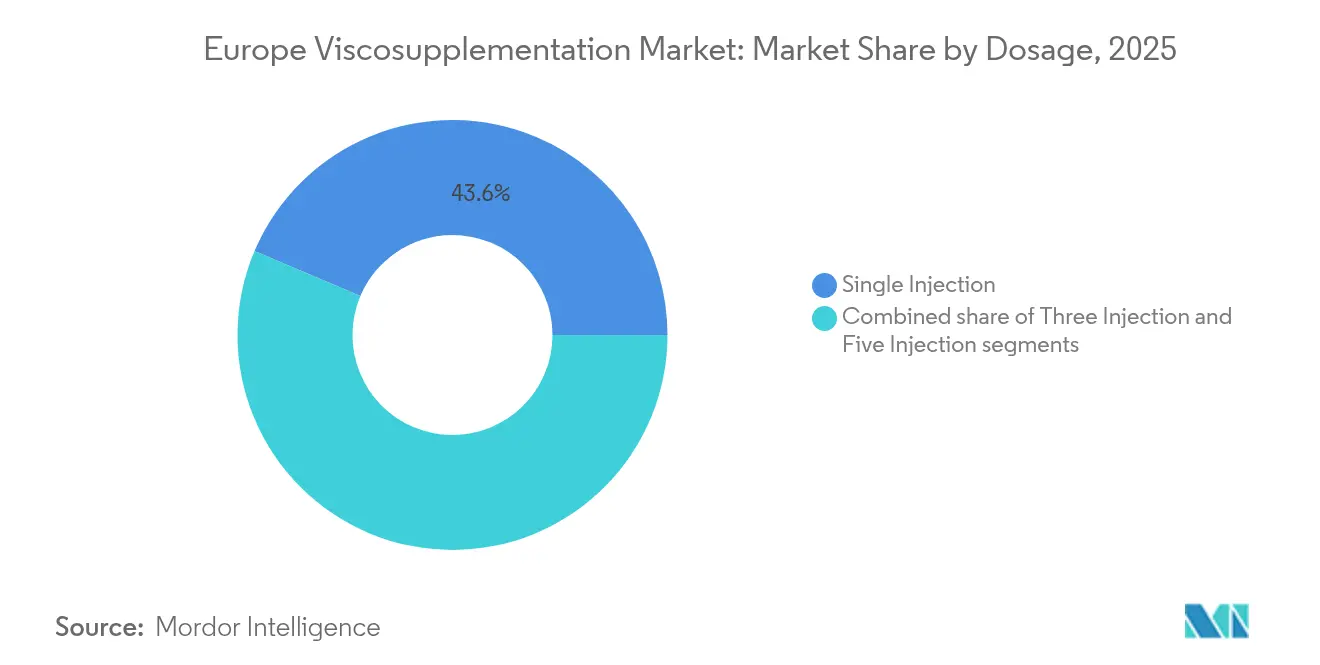

- By dosage – The single-injection format led with 43.62% of the Europe viscosupplementation market share in 2025 and is on track for a 9.44% CAGR through 2031.

- By product source – Avian-derived HA retained 52.63% revenue share in 2025, while non-avian alternatives are expected to post a 9.25% CAGR to 2031.

- By application site – Knee injections accounted for 71.85% of the Europe viscosupplementation market size in 2025; the “Others” category, covering hip and shoulder joints is set to expand at 10.05% CAGR to 2031.

- By end-user – Hospitals captured 40.74% of segment revenue in 2025, whereas ASCs are projected to grow fastest at 9.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on viscosupplementation market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Viscosupplementation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising osteoarthritis prevalence & ageing population | +2.8% | EU-5 core, expanding to CEE markets | Long term (≥ 4 years) |

| Rapid uptake of single-injection HA formats | +1.9% | Germany, France, UK | Medium term (2-4 years) |

| Expansion of reimbursement across EU-5 | +1.4% | Germany, France, Italy | Medium term (2-4 years) |

| Viscosupplementation as TKR-deferral strategy | +1.2% | EU-5 with ageing populations | Long term (≥ 4 years) |

| ASC Capacity Boost Enabling Outpatient Injections | +0.9% | Germany, Netherlands, UK | Short term (≤ 2 years) |

| Combination Biologics Widen Pool | +0.7% | Western Europe, selective CEE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Osteoarthritis Prevalence & Ageing Population

Europe hosts an expanding senior demographic that is highly susceptible to knee osteoarthritis, now affecting more than 5 million Germans alone[1]Erliang Li, “Global burden and socioeconomic impact of knee osteoarthritis: a comprehensive analysis,” Frontiers in Medicine, frontiersin.org. As life expectancy rises and sedentary lifestyles become more common, cartilage wear accelerates. This trend boosts the demand for intra-articular HA injections, which help maintain mobility and delay expensive arthroplasty procedures. Clinical studies reveal that combining PRP with HA[2]Journal of Orthopaedic Surgery and Research, “A meta-analysis and systematic review of the clinical efficacy and safety of platelet-rich plasma combined with hyaluronic acid (PRP + HA) versus PRP monotherapy for knee osteoarthritis (KOA),” josr-online.biomedcentral.com yields better results than using either alone. Meta-analyses back this, highlighting significant pain reduction and improved functionality. Healthcare payers note that delaying a total knee replacement by two to three years not only eases budget pressures but also maintains the patient's quality of life. Given this pressing clinical need, HA therapies continue to see widespread adoption across national insurance schemes, signaling robust growth for the Europe viscosupplementation market.

Rapid Uptake of Single-Injection HA Formats

Products such as Monovisc and Durolane replace multi-visit regimens[3]Selim Safali, “Evaluation of single and multiple hyaluronic acid injections at different concentrations with high molecular weight in the treatment of knee osteoarthritis,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com with a single procedure, improving adherence and freeing clinical resources. Real-world studies show pain-relief durability beyond 15 months, supporting premium pricing that offsets higher per-dose costs. EUROVISCO guidance favors patient preference, spurring surgeons across Germany and France to integrate single-shot HA into standard pathways. The format also expands reach to younger working-age individuals who seek minimal disruption, fortifying the near-term trajectory for the Europe viscosupplementation market.

Expansion of Reimbursement Across EU-5

France maintains comprehensive coverage, and Germany now reimburses HA for patients who have exhausted conservative care. Italian economic evaluations cite incremental cost-effectiveness ratios around EUR 3,161 per QALY, validating payer support. While NHS England remains conservative, private UK insurers discreetly reimburse injections, sustaining demand outside public channels. These shifts lower out-of-pocket expense, enlarging the treated population and encouraging manufacturer investment in real-world evidence, reinforcing growth in the Europe viscosupplementation market.

Viscosupplementation as TKR-Deferral Strategy

Clinical data indicate that repeat HA injections can postpone total knee replacement by more than three years, trimming per-patient expenditure relative to immediate arthroplasty averaging EUR 15,000–20,000. This bridge therapy appeals to active adults in their fifties who wish to delay irreversible surgery. Hospitals under surgical backlog pressure endorse the protocol to reduce waiting lists, further embedding HA in orthopedic treatment algorithms and deepening penetration of the Europe viscosupplementation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Divergent clinical-practice guidelines on HA efficacy | −1.8% | UK, Netherlands, Nordic states | Medium term (2-4 years) |

| EU-MDR 2021 compliance burden for HA Class III | −1.2% | EU-wide, small manufacturers | Short term (≤ 2 years) |

| High Out-of-Pocket Costs in CEE Markets | -0.9% | Poland, Czech Republic, Hungary | Long term (≥ 4 years) |

| Avian-Source Supply-Chain Bio-Risk | -0.6% | Global supply chains affecting EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Divergent Clinical-Practice Guidelines on HA Efficacy

NICE in the UK and AAOS in the USA express reservations about routine HA injections, prompting hesitation among evidence-driven clinicians. Contrastingly, EUROVISCO’s supportive stance creates a patchwork of recommendations across Europe, complicating payer decisions and slowing adoption in guideline-sensitive markets. The uncertainty trims momentum for the Europe viscosupplementation market until harmonized consensus emerges.

EU-MDR 2021 Compliance Burden for HA Class III

The MDR upgrade classifies injectable HA as a high-risk device, demanding robust clinical evidence and comprehensive post-market surveillance. Smaller European firms must secure millions in compliance outlays, pushing some toward mergers or exits. Certification delays can stall product launches, tempering short-term supply growth within the Europe viscosupplementation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage: Single Injection Convenience Drives Adoption

The single-injection segment controlled 43.62% of the Europe viscosupplementation market share in 2025 and is predicted to climb at 9.44% CAGR to 2031. This commanding position is grounded in streamlined clinic scheduling, enhanced patient satisfaction, and health-system cost avoidance tied to multiple appointments. Three-injection regimens retain relevance among long-practicing surgeons who value incremental dosing, whereas five-shot protocols remain niche.

Advances in cross-linking chemistry lengthen HA residence time, enabling therapeutic benefit from a single shot that lasts more than 15 months. As ASCs proliferate, their efficiency ethos dovetails with single-injection workflows, thereby reinforcing segment dominance. These factors combine to secure sustained double-digit revenue contribution to the Europe viscosupplementation market.

By Product Source: Avian Dominance Faces Non-Avian Challenge

Avian-derived HA represented 52.63% of the Europe viscosupplementation market size in 2025, fueled by decades of clinician familiarity and well-established rooster-comb extraction methods. Nevertheless, biosafety concerns and supply continuity issues stimulate a 9.25% CAGR in non-avian, bacterial-fermentation alternatives through 2031.

Large producers invest in microbial fermentation that yields high-molecular-weight HA and eliminates animal-protein residues. Kewpie reports equivalence in viscoelasticity and clinical efficacy between avian and bacterial products. Policy makers keen on minimizing zoonotic risk increasingly favor synthetic supply chains, while manufacturers diversify sourcing to hedge against avian influenza-related disruption. This gradual migration bolsters resilience in the Europe viscosupplementation market.

By Application Site: Knee Dominance with Emerging Opportunities

Knee injections captured 71.85% of the Europe viscosupplementation market in 2025, reflecting the joint’s central role in mobility and its higher osteoarthritis incidence. Yet the “Others” category, encompassing hip and shoulder joints, is projected for a 10.05% CAGR to 2031 as ultrasound-guided techniques lift physician confidence.

Hip viscosupplementation trials note significant pain reduction at one-year follow-up. Shoulder applications target rotator cuff pathology in athletic cohorts seeking nonsurgical relief. The broadening clinical scope lessens reliance on knee volume and diversifies revenue streams, reinforcing expansion of the Europe viscosupplementation market.

By End-User: ASC Growth Transforms Delivery Models

Hospitals maintained 40.74% revenue in 2025, but ambulatory surgical centers are growing at 9.6% CAGR amid Europe-wide shifts toward outpatient orthopedics. ASCs deliver 30–50% procedure-cost savings with infection rates below inpatient benchmarks.

Orthopedic specialty clinics remain vital, servicing sports-medicine and early-OA patients who pursue fast recovery. The ASC trajectory aligns with payer incentives for cost containment, ensuring that outpatient infrastructure becomes integral to the Europe viscosupplementation market.

Geography Analysis

Germany spearheads adoption through statutory insurance coverage that reimburses HA once conservative therapy fails. A robust ASC network, advanced ultrasound utilization, and manufacturer presence create a self-reinforcing ecosystem. The Europe viscosupplementation market gains additional German tailwinds from demographic aging and a 20% obesity prevalence that elevates knee OA risk.

The United Kingdom offers contrasting dynamics. Limited NHS coverage restrains volumes, yet a thriving private sector and short surgical wait avoidance drive demand among self-pay patients. Brexit-related supply chain adjustments introduce complexity but established distributor relationships continue to ensure product availability. Premium single-injection formats appeal to time-sensitive consumers and help sustain growth.

France enjoys mature reimbursement and clinician acceptance. Cost-effectiveness assessments validate HA’s budget impact, and local firms conduct combination-therapy trials to expand indications. Regulatory reforms mandating prescriptions for injectable HA, effective July 2024, ensure professional oversight without restricting access and thus stabilize growth for the Europe viscosupplementation market.

Italy and Spain show divergent regional pathways. Italian cost-utility analyses support nationwide coverage, whereas Spain’s autonomous communities present variable reimbursement that producers navigate via localized market access teams. Central and Eastern Europe remains underpenetrated but exhibits high growth potential as reimbursement evolves and GDP per capita rises, extending the long-term footprint of the Europe viscosupplementation market.

Competitive Landscape

The Europe viscosupplementation industry is moderately consolidated. Anika Therapeutics, Sanofi, and Fidia dominate single-injection portfolios, leveraging broad distribution and strong regulatory infrastructure. Anika’s strategic divestiture of its sports-medicine unit in March 2025 refocused capital on HA innovation, including next-generation cross-linked formulations.

Mid-tier European players such as Contura Orthopaedics widen portfolios with polymer hydrogel alternatives, supported by 10-year safety datasets. Smaller firms pivot to bacterial-fermentation sourcing to differentiate on purity and supply stability, while outsourcing MDR compliance activities to notified bodies with HA expertise. Supply-chain partnerships mitigate avian-origin risk and enable uninterrupted service to the Europe viscosupplementation market.

Strategic alliances with ASC groups surface as a competitive lever, embedding product education and ultrasound training within outpatient networks. Companies invest in digital platforms that schedule repeat injections, collect patient-reported outcomes, and feed post-market registries demanded by MDR rules. These integrated solutions raise switching costs and reinforce brand loyalty, sustaining competitive advantage across the Europe viscosupplementation market.

Europe Viscosupplementation Industry Leaders

Anika Therapeutics, Inc.

Bioventus Inc.

Fidia Farmaceutici S.p.A.

Sanofi S.A.

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Anika Therapeutics completed the divestiture of Parcus Medical to Medacta Group SA to intensify focus on HA technologies for osteoarthritis pain management.

- October 2024: Contura Orthopaedics presented 10-year safety and 5-year efficacy data for Arthrosamid polyacrylamide hydrogel at WCO 2025 Rome, substantiating long-term benefits for knee OA therapy.

- July 2024: French authorities mandated medical prescriptions for injectable HA products effective 1 July 2024, ensuring administration by licensed professionals while maintaining access.

- September 2023: Enovis Corp agreed to acquire Limacorporate S.p.A. for EUR 800 million to broaden its joint-preservation device portfolio in Europe.

Europe Viscosupplementation Market Report Scope

Viscosupplements are injections of hyaluronic acid for diarthrodial joints, intending to restore the rheological properties of the synovial fluid, thereby producing analgesia, mechanical, chondroprotective, and anti-inflammatory effects. Viscosupplements are usually preferred by healthcare providers to treat osteoarthritis. They may also benefit patients with certain other kinds of arthritis, such as rheumatoid arthritis.

Europe's viscosupplementation market is segmented by dosage, end user, and geography. By dosage, the market is segmented into single injections, three injections, and five injections. By end user, the market is segmented into hospitals, ambulatory surgical centers, and others. Other end users include specialty clinics, and rehabilitation centers, among others. By geography, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and Rest of Europe. The report offers the value (USD) for all the above segments.

| Single Injection |

| Three Injection |

| Five Injection |

| Avian-derived HA |

| Non-Avian |

| Knee |

| Hip |

| Shoulder |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Orthopedic & Sports Clinics |

| Others |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Dosage | Single Injection |

| Three Injection | |

| Five Injection | |

| By Product Source | Avian-derived HA |

| Non-Avian | |

| By Application Site | Knee |

| Hip | |

| Shoulder | |

| Others | |

| By End-User | Hospitals |

| Ambulatory Surgical Centers | |

| Orthopedic & Sports Clinics | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

Why are single-injection hyaluronic acid products gaining traction in Europe?

They simplify treatment by eliminating multiple clinic visits, which improves patient adherence and frees up clinical resources, making them attractive to both patients and providers.

How is EU-MDR 2021 influencing competition among viscosupplement manufacturers?

Stricter Class III device requirements raise compliance costs, favoring well-capitalized firms and encouraging smaller players to seek partnerships or exit the market.

What role do ambulatory surgical centers (ASCs) play in viscosupplement delivery?

ASCs offer lower procedure costs and faster scheduling than hospitals, supporting greater access to intra-articular injections and accelerating outpatient adoption.

Why is non-avian hyaluronic acid production becoming more prominent?

Bacterial-fermentation methods reduce biosafety risks linked to animal-derived material, provide supply-chain stability, and meet growing regulatory expectations for risk mitigation.

How do divergent clinical guidelines impact viscosupplement uptake across Europe?

Conflicting recommendations from organizations such as NICE and EUROVISCO create prescriber uncertainty, resulting in uneven adoption rates between countries and healthcare settings.

What strategic importance do combination biologics hold for market participants?

Pairing platelet-rich plasma with hyaluronic acid shows superior pain and function outcomes, offering manufacturers a pathway to differentiate products and command premium pricing.

Page last updated on: