Viscosupplementation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.73 Billion |

| Market Size (2031) | USD 7.31 Billion |

| Growth Rate (2026 - 2031) | 9.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

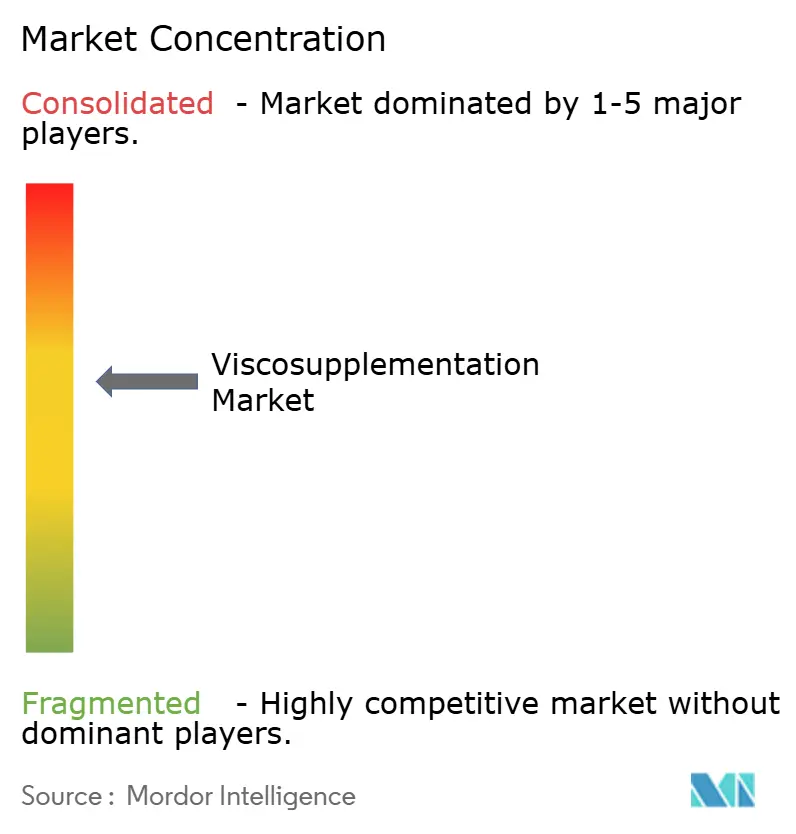

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Viscosupplementation Market Analysis by Mordor Intelligence

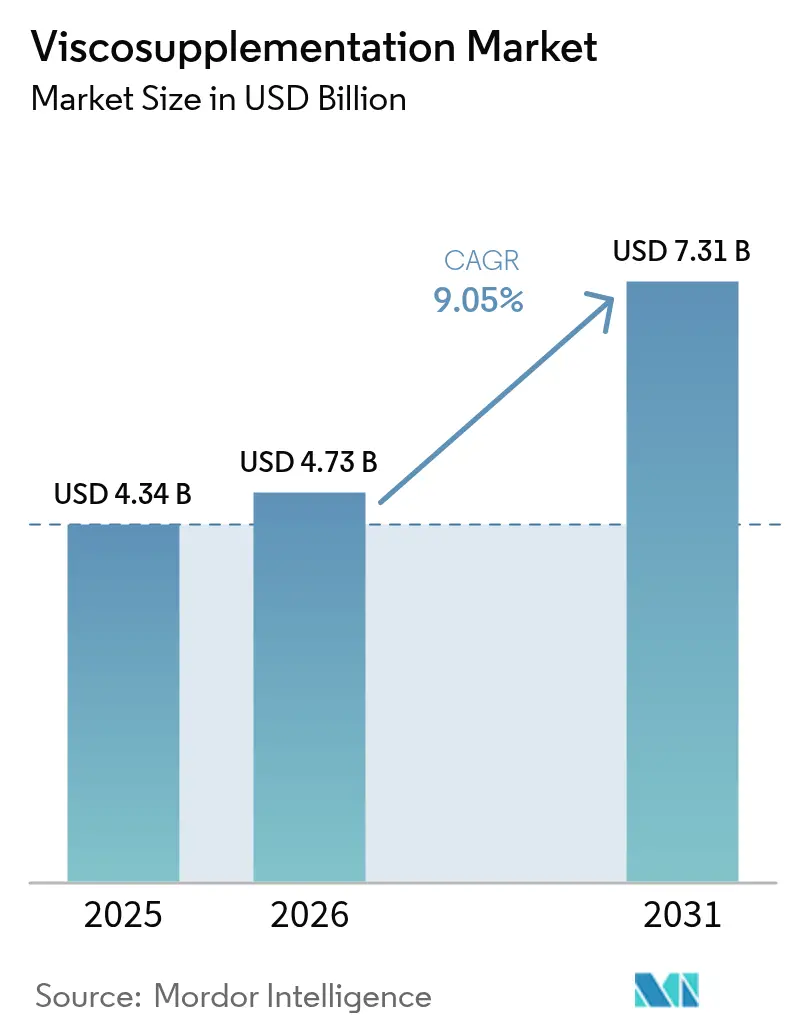

The viscosupplementation market size is expected to grow from USD 4.34 billion in 2025 to USD 4.73 billion in 2026 and is forecast to reach USD 7.31 billion by 2031 at 9.05% CAGR over 2026-2031. Growth rests on three pillars: population ageing that lifts osteoarthritis incidence, manufacturing advances that allow high-purity hyaluronic acid at scale, and clinical guidelines that increasingly recommend single-injection protocols over multi-dose regimens. In practice, viscosupplementation postpones total knee replacement by a mean of 2.6 years, trimming episode-of-care costs while sustaining mobility for millions of patients. Regionally, Asia-Pacific sets the fastest pace at a 10.02% CAGR as reimbursement coverage widens and ambulatory centers proliferate, whereas North America commands the largest revenue share at 42.07% underpinned by broad HCPCS code usage. The competitive field remains moderately concentrated; leading producers differentiate through molecular-weight tailoring, while regulatory uncertainty tied to potential FDA device-to-drug reclassification injects risk but also raises entry barriers.

Key Report Takeaways

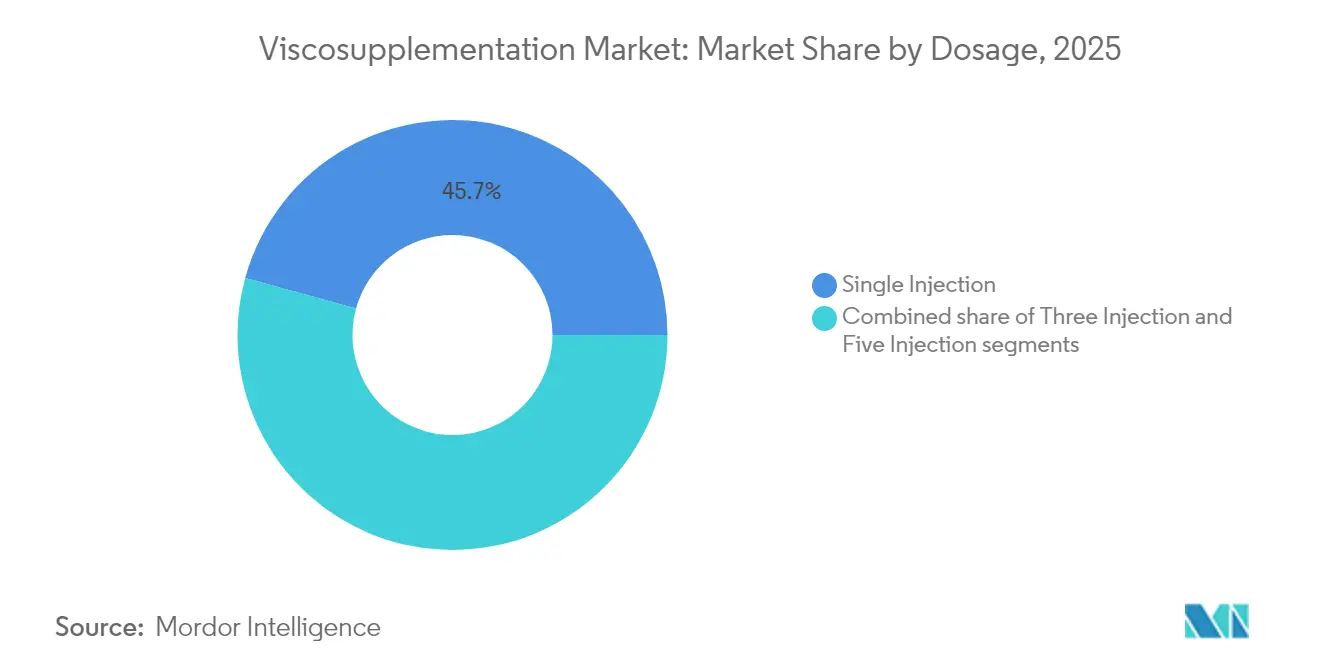

- By dosage, single-injection products held 45.72% of the viscosupplementation market share in 2025 and are expanding at the segment-leading 9.41% CAGR to 2031.

- By product source, avian-derived hyaluronic acid led with 53.65% revenue share in 2025, while fermentation-based alternatives are growing at 9.32% CAGR.

- By application site, knee injections accounted for 73.88% of the viscosupplementation market size in 2025; the Others segment is expected to register the fastest 10.12% CAGR.

- By end-user, hospitals retained 41.74% revenue in 2025, whereas ambulatory surgical centers post a 9.69% CAGR through 2031.

- By geography, Asia-Pacific records the highest 9.58% CAGR; North America remains the largest regional market with 41.45% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Viscosupplementation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-Linked OA Prevalence Surge | +2.1% | Global, with peak impact in North America & Europe | Long term (≥ 4 years) |

| Shift to Single-Injection HA Regimens | +1.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Product Approvals & Reimbursement Expansions | +1.4% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Fermentation-Based Vegan HA Supply Scalability | +1.2% | Global, with manufacturing concentrated in Asia-Pacific | Long term (≥ 4 years) |

| Ultrasound-Guided Injections in ASC Networks | +1.0% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Regenerative Combo Injectables | +0.8% | Global, with early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-Linked OA Prevalence Surge

Worldwide osteoarthritis cases climbed to 607 million in 2021, with knee disease making up more than 56% of the burden. The age-standardized prevalence rate[1]Zihao Wang, “Global, regional and national burden of osteoarthritis in 1990–2021: a systematic analysis of the global burden of disease study 2021,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com rose from 6,393.1 to 6,967.3 per 100,000. Obesity contributes approximately 4.43 million disability-adjusted life years, amplifying joint degeneration severity. Health-economic analyses show viscosupplementation delays knee arthroplasty and lowers lifetime treatment expense, positioning the therapy as a fiscal lever for payers coping with an ageing base.

Shift to Single-Injection HA Regimens

Randomized trials confirm that single-injection hyaluronic acid provides pain relief comparable to multi-dose courses while reducing clinic visits. FDA clearance of Monovisc, the first single-injection, non-animal product, accelerated adoption. Yet head-to-head studies[2]Selim Safali, “Evaluation of single and multiple hyaluronic acid injections at different concentrations with high molecular weight in the treatment of knee osteoarthritis,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com show three low-dose injections can yield better functional scores than one high-dose shot. Manufacturers are therefore raising molecular weight to prolong residence time, aiming to reconcile convenience with peak efficacy.

Product Approvals & Reimbursement Expansions

Recent FDA clearances, such as Hymovis, underscore regulators’ focus on demonstrable clinical outcomes over bioequivalence alone. U.S. payers now reimburse distinct HA codes J7318-J7329, although prior-authorization rules have tightened. The 2025 Physician Fee Schedule[3]Centers for Medicare & Medicaid Services, “Medicare and Medicaid Programs; CY 2025 Payment Policies Under the Physician Fee Schedule and Other Changes to Part B Payment and Coverage Policies; Medicare Shared Savings Program Requirements; Medicare Prescription Drug Inflation Rebate Program; and Medicare Overpayments,” federalregister.gov revises practice-expense RVUs, influencing provider margins. Companies with robust evidence portfolios enjoy smoother market entry, whereas products lacking comparative data face formulary pushback.

Fermentation-Based Vegan HA Supply Scalability

Engineered Streptococcus zooepidemicus fermentation now yields up to 4.38 g/L hyaluronic acid through refined precursor balance and gene-expression control. This route avoids animal-derived raw materials and reduces exposure to H5N1 supply shocks. It also lets producers tailor ultra-high molecular weight grades[4]Filippo Migliorini, “Comparison of Different Molecular Weights of Intra-Articular Hyaluronic Acid Injections for Knee Osteoarthritis: A Level I Bayesian Network Meta-Analysis,” Biomedicines, mdpi.com that clinical meta-analyses associate with superior pain relief. Marine by-products, such as mussel wastewater substrates, present additional feedstock options, deepening supply resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical-Efficacy Debate & Payer Push-Back | -1.9% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| FDA Device-to-Drug Re-Classification Risk | -1.1% | North America, with potential spillover to other regions | Short term (≤ 2 years) |

| Avian-Supply Shocks from H5N1 Outbreaks | -0.9% | Global, with highest impact on avian-derived HA supply | Short term (≤ 2 years) |

| Growing Adoption of PRP/MSCs as Substitutes | -0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clinical-Efficacy Debate & Payer Push-Back

The American College of Rheumatology and the American Academy of Orthopaedic Surgeons classify viscosupplementation evidence as limited, fueling insurer caution. Meta-analyses show high study heterogeneity, allowing payers to impose step-therapy criteria that favor NSAIDs or corticosteroids first. Platelet-rich plasma now records stronger long-term results in several trials, prompting coverage committees to revisit HA reimbursement. Providers must compile detailed conservative-treatment histories to secure payment, elevating the administrative load.

FDA Device-to-Drug Reclassification Risk

Following the Genus court ruling, FDA signaled plans to re-evaluate hyaluronic acid’s device status, which could trigger costlier, drug-style trials and longer review clocks. The prospect complicates R&D budgeting and may advantage larger pharma players able to fund phase III programs. Firms thus maintain dual dossier strategies to hedge against final classification outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage: Single-Injection Convenience Drives Adoption

Single-injection products captured 45.72% of the viscosupplementation market share in 2025 and command a 9.41% CAGR to 2031. The Viscosupplementation market size tied to single-dose regimens is forecast at USD 3.38 billion in 2031. The popularity stems from reduced clinic time and lower procedural fees. Three-injection courses retain relevance for patients needing incremental symptom control, while five-shot regimens serve severe bilateral disease.

Clinical data show concentrated cross-linked preparations sustain symptom relief over 60 days. Ongoing formulation work seeks to match the functional gains of multi-dose protocols by boosting viscoelasticity and residence time of single shots. Manufacturers exploit this clinical tension to position premium high-molecular-weight brands at the intersection of convenience and efficacy.

By Product Source: Fermentation Gains Ground Despite Avian Dominance

Avian sources held 53.65% of the viscosupplementation market size in 2025, thanks to decades of clinical familiarity. However, fermentation products grow 9.32% annually as the Viscosupplementation market prioritizes supply security and vegan labelling. The Viscosupplementation market size for non-avian HA is projected to reach USD 3.42 billion by 2031.

Process innovation allows bespoke molecular-weight spectra without the viral-contamination risks linked to rooster comb extract. Companies hedge by running parallel avian and fermentation lines, but long-range capex tilts toward fermenters located in China and South Korea, where feedstock and utilities cost less.

By Application Site: Knee Dominance Masks Emerging Opportunities

Knee injections delivered 73.88% revenue in 2025, representing the largest slice of the viscosupplementation market share. Others segment pace the field at a 10.12% CAGR.

Ultrasound guidance now enables accurate hip access under local anesthetic, improving patient tolerance and expanding referral volumes. In the shoulders, viscosupplementation eases glenohumeral stiffness in seniors unable to undergo arthroplasty. As device makers roll out narrow-gauge needles and portable imaging, orthopedists broaden HA use beyond knees, seeding new revenue layers.

By End-User: ASCs Capitalize on Efficiency Trends

Hospitals held 41.74% of the viscosupplementation market share in 2025, yet ambulatory surgical centers (ASCs) record a 9.69% CAGR through 2031, the fastest among care settings.

ASC growth rides on bundled-payment models that reward lower facility fees and same-day discharge. Portable ultrasound lowers setup cost, letting clinics perform injections in procedure rooms rather than fluoroscopy suites. Orthopedic and sports medicine offices occupy a middle ground, retaining loyal athlete populations while referring complex geriatric cases back to hospital groups.

Geography Analysis

North America contributed 41.45% of the viscosupplementation market share in 2025 and is forecast to grow at 8.98% CAGR until 2031. HCPCS codes J7318-J7329 assure reimbursement continuity, but payers are tightening prior-authorisation rules that lengthen approval cycles. FDA product clearances sustain pipeline momentum, yet looming device-to-drug reclassification could inflate compliance spending, particularly for smaller entrants. Distribution partnerships, such as the renewal between Anika Therapeutics and Pendopharm that extends to 2030, reinforce market depth.

Asia-Pacific registers the top 9.58% CAGR, driven by urban hospitals adopting minimally invasive pain procedures and by domestic HA producers scaling fermentation capacity. Government import-substitution policies in China and India nudge buyers toward local brands, trimming landed cost. Rising life expectancy and joint-disease prevalence in Japan and South Korea sustain demand even in mature payer environments.

Europe advances at 8.66% CAGR under the strict EU Medical Devices Regulation that mandates post-market performance studies. The paperwork burden weeds out small labelers, handing advantage to well-capitalised suppliers. Middle East & Africa follow at 8.51% CAGR on the back of hospital expansion in Gulf Cooperation Council states, whereas South America trails at 8.07% due to fiscal austerity and uneven insurance penetration. Collectively, emerging regions form the next frontier once regulatory clarity and payer frameworks solidify.

Mordor Intelligence provides coverage of the viscosupplementation market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Viscosupplementation products for intra-articular injection are mainly regulated as high-risk medical devices. In the United States, FDA oversight runs through Premarket Approval (PMA) pathways, while Europe is governed by Regulation (EU) 2017/745 (EU MDR) and related conformity assessment through notified bodies. In the United States, lifecycle changes often proceed via PMA supplements, including FDA approvals in May 2025 for Euflexxa manufacturing-capacity expansion (PMA supplement) and for Channel-Markers Medical to add an alternate bulk sodium hyaluronate supplier for TriVisc and GenVisc 850 (PMA supplement), which keeps manufacturing controls and raw-material change documentation central.

Quality and clinical-evidence expectations are also moving tighter through system-level updates and MDR implementation. The FDA implemented the Quality Management System Regulation (QMSR) in February 2026, bringing device quality systems closer to ISO 13485:2016 and raising compliance expectations across design controls, supplier management, and post-market processes. In Europe, MDR-related updates continued as the European Commission adopted Delegated Regulation (EU) 2026/1451, while EMA and EU expert-panel processes maintain scrutiny of clinical evaluation for higher-risk device categories. That combination keeps barriers elevated for smaller labelers and sustains the importance of post-market performance data.

Value Chain Analysis

The value chain starts with pharmaceutical-grade sodium hyaluronate production, sourced from avian tissue extraction or, increasingly, from bacterial fermentation, commonly Streptococcus zooepidemicus, to reduce exposure to avian biosecurity shocks and protein or viral impurity risks. Upstream steps include purification, molecular-weight control, and, for longer-acting products, chemical modification or cross-linking using specialized reagents. Midstream manufacturers then execute aseptic formulation, prefilled syringe filling, terminal sterilization or sterility assurance, and quality release under medical device quality systems aligned with ISO 13485, reinforced by the FDA QMSR shift implemented in February 2026.

Downstream, products reach customers through direct sales forces, specialty distributors, and centralized procurement by hospital groups and ambulatory surgical centers that manage inventory and reimbursement workflows. Cold-chain handling (commonly 2-8 degrees Celsius) and shelf-life constraints favor established distribution networks, while reimbursement administration and prior authorization create friction at the point of care. Regulatory maintenance and manufacturing continuity also remain part of the operational chain, as reflected in recent FDA PMA supplements for manufacturing changes and raw-material supplier additions, such as the May 2025 approvals tied to Euflexxa capacity and Channel-Markers Medical supplier flexibility.

Competitive Landscape

The viscosupplementation market shows moderate concentration: the top five suppliers account for a large chunk of global sales. Anika Therapeutics leads with Orthovisc and Monovisc portfolios, yet its Q3 2024 revenue slipped 7% year on year to USD 38.8 million, reflecting U.S. procedure softness. Bioventus posted Q1 2024 revenue of USD 129 million, up 9%, fuelled by DUROLANE rollouts in new hospital accounts.

Players differentiate on molecular weight, cross-linking chemistry, and injection schedule. Pipeline assets combine hyaluronic acid with platelet-rich plasma to extend symptom relief; early randomized data indicate greater WOMAC score reduction than monotherapy. Firms also invest in handheld ultrasound systems and fine-gauge needle sets that reduce procedure pain, bundling disposables with HA syringes to deepen account loyalty.

Strategic focus remains sharp: Anika divested Parcus Medical in March 2025 to channel resources into core HA technology. Bioventus sold its Advanced Rehabilitation unit for USD 45 million to trim debt and fund viscosupplementation R&D. Midsize peers pursue licensing deals rather than full acquisitions, betting that post-market surveillance costs under EU MDR will drive smaller brands to seek shelter under larger commercial umbrellas.

Viscosupplementation Industry Leaders

Anika Therapeutics, Inc.

Bioventus Inc.

Fidia Farmaceutici S.p.A.

Seikagaku Corporation

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Single-injection regimens continue to represent a key commercial whitespace, since they reduce clinic visits while the evidence debate persists around comparative outcomes versus multi-injection courses. Evidence generation remains a direct input into product positioning and protocol standardization, including a clinical trial initiated in January 2026 at University of Erlangen-Nurnberg Medical School (NCT07352540) that compares single-shot versus triple-shot hyaluronic acid protocols. Guideline and consensus work is also shaping uptake, with ESCEO convening a working group in January 2025 to update evidence on intra-articular hyaluronic acid, which gives a near-term lever to manufacturers that can support stronger comparative data packages.

Portfolio expansion is also being pursued through chemistry and combination strategies that differentiate beyond molecular weight alone, including linear versus cross-linked (chemically modified) constructs and co-formulations or co-injection approaches with non-HA agents. Recent actions provide concrete entry points, including FDA PMA for HYMOVIS ONE in April 2025, followed by its US commercial launch in January 2026 and visibility at AAOS in 2026, which supports a path for new premium single-injection offerings. On the supply side, FDA acceptance of manufacturing and sourcing changes, such as the May 2025 approvals tied to capacity expansion and alternate bulk sodium hyaluronate suppliers, supports resilience initiatives and widens the addressable scope for non-avian and multi-sourced HA supply strategies.

Recent Industry Developments

- March 2026: Seikagaku Corporation announced the resubmission of its application to the US FDA seeking approval for SI-6603, an injectable therapeutic for lumbar disc herniation. The step reinforces the companys US regulatory engagement in injectable pain-management categories adjacent to osteoarthritis care pathways. This can influence competitive focus and partnering attention across non-opioid, procedure-based musculoskeletal interventions.

- November 2025: Anika Therapeutics filed the third and final module of its PMA application with the US FDA for the Hyalofast cartilage repair scaffold. The filing advances Anikas regulatory roadmap in orthopedic regenerative products that sit upstream of end-stage osteoarthritis management. It also complements the companys HA franchise strategy by broadening its musculoskeletal portfolio beyond viscosupplementation alone.

- October 2024: Bioventus divested its Advanced Rehabilitation segment to Accelmed Partners for USD 45 million with contingent earn-outs. The transaction simplified Bioventus operating focus and released capital for priority growth platforms, including its osteoarthritis and pain-related franchises. The move also tightened the companys emphasis on higher-margin product lines where sales coverage overlaps with orthopedic accounts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues from viscosupplementation injections used to manage osteoarthritis related joint pain, including the product and procedure value captured through common care settings across major geographies.

Scope exclusions: We exclude oral pain drugs, physical therapy services, orthopedic implants, and surgical joint replacement procedures that are not part of viscosupplementation injection revenue.

Segmentation Overview

- By Dosage

- Single Injection

- Three Injection

- Five Injection

- By Product Source

- Avian-derived HA

- Non-Avian

- By Application Site

- Knee

- Hip

- Shoulder

- Others

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Orthopedic & Sports Clinics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the osteoarthritis and treatment context, then mapping it to how injections move through real care pathways. We typically rely on public sources such as the CDC and NIH for osteoarthritis burden, CMS for reimbursement and site of care signals, and FDA databases for product approvals and labeling updates.

To keep the market tied to observable activity, we also refer to sources such as OECD health statistics and WHO population aging indicators, along with peer reviewed journals that discuss hyaluronic acid injection patterns and outcomes. Company filings, investor presentations, and reputable press coverage are used to understand portfolio focus and broad pricing direction, and then a paid subscription focused on company financials and patent databases is used selectively to reduce guesswork on product coverage and innovation cadence. This list is not exhaustive, and many other public and paid references were used for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm how utilization is changing across hospitals, ambulatory surgical centers, and orthopedic or sports clinics, and to sanity check price points for different injection regimens. We also validate drivers such as single injection adoption, patient affordability, and payer coverage logic by speaking with clinicians, distributors, and operational leaders across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 41% |

| Mid tier: 54% | Functional/Unit leaders: 40% | EMEA: 36% |

| Smaller Players: 16% | Managers: 46% | Americas: 23% |

Market-Sizing & Forecasting

We begin with a top-down build where the treated osteoarthritis pool is translated into procedure volumes by site of care, then converted to value using typical regimen mix and average selling price ranges. To keep the totals realistic, the outputs are corroborated with selective bottom-up approximations such as sampled price checks, distributor channel feedback, and supplier level revenue sanity checks, with gaps handled using conservative ranges when coverage is thin.

Key inputs that shape the model include osteoarthritis prevalence trends, aging population growth, the share of injections performed in hospitals versus ambulatory surgical centers, the mix of single, three, and five injection regimens, and the shift between avian derived and non avian (fermentation) hyaluronic acid sources. Forecasts are developed using scenario analysis, where adoption and pricing are stress tested under different payer coverage and guideline environments, and then adjusted based on expert consensus on what is most likely to hold through the forecast window.

Data Validation & Update Cycle

Validation is done through triangulation across model outputs, interview feedback, and independent signals such as reimbursement direction, approval timelines, and visible shifts in site of care. When a value or growth rate looks unusual, the assumptions are reopened and the related steps are recalculated before the numbers move forward for review.

A multi step analyst review is followed, where inputs, formulas, and intermediate outputs are checked for variance and logical consistency, and then outliers are challenged with additional callbacks when needed. Reports are refreshed annually, with interim updates triggered by material events such as major regulatory actions or sharp pricing changes, and a final pre delivery pass is completed so clients receive the latest view.

Mordor Intelligence's Viscosupplementation Market Size Measured Against Other Published Estimates

Published market values for viscosupplementation can look far apart because the scope and counting rules are not the same, even when the topic name matches. Differences usually come from what gets treated as revenue, which care settings are included, and whether adjacent joint injections are mixed into the total.

Some estimates blend viscosupplementation with broader joint pain injection baskets, or they assume aggressive price uplift without reconciling it to payer behavior and regimen mix shifts. In our case, the total is tied to procedure volume logic by regimen and site of care, and it keeps knee led demand as the dominant driver without automatically inflating smaller joints, which is the main reason the 2025 value lands where it does for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.34 B (2025) | |

| Trade Journal A | USD 4.55 B (2025) | This figure appears to lean on a faster near term ramp in pricing and utilization, and it may not separate regimen mix changes (single versus multi injection) across sites of care before valuing the market. |

| Industry Brief B | USD 3.25 B (2024) | The estimate is anchored to a narrower product interpretation that emphasizes hyaluronic acid injections, and it can undercount value where procedure setting mix and paid price differences are material. |

The spread in values is mainly explained by what is counted as viscosupplementation revenue, how regimen mix is priced, and how quickly assumptions are refreshed when payer policies change. By keeping the volume build and the pricing logic traceable to care settings and regimen patterns, the final number stays easier to reproduce and update when new signals arrive.

Key Questions Answered in the Report

What clinical trend is reshaping viscosupplementation protocols?

Single-injection hyaluronic acid regimens are becoming the preferred option because they cut clinic visits and improve patient adherence without compromising pain-relief outcomes.

How are manufacturers securing long-term raw-material supply for hyaluronic acid?

They are scaling fermentation-based, non-animal production methods that deliver consistent molecular-weight profiles and sidestep risks tied to avian-derived sources.

Why are ambulatory surgical centers gaining importance in this market?

Cost-conscious payers favor outpatient facilities, and advances in handheld ultrasound now let clinicians perform guided injections accurately in ASC procedure rooms.

What regulatory shift could alter product development strategies?

A potential FDA move to reclassify hyaluronic acid products from devices to drugs would require more extensive clinical trials, raising both timelines and investment thresholds.

Which combination therapy is emerging as a promising alternative to monotherapy?

Co-injection of hyaluronic acid with platelet-rich plasma is showing superior improvements in pain relief and joint function compared with hyaluronic acid alone.

How are payers influencing viscosupplementation adoption?

Insurers are tightening prior-authorization rules and demanding documented failure of conservative treatments, nudging clinicians toward evidence-rich products and competitive pricing.

Page last updated on: