Europe Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

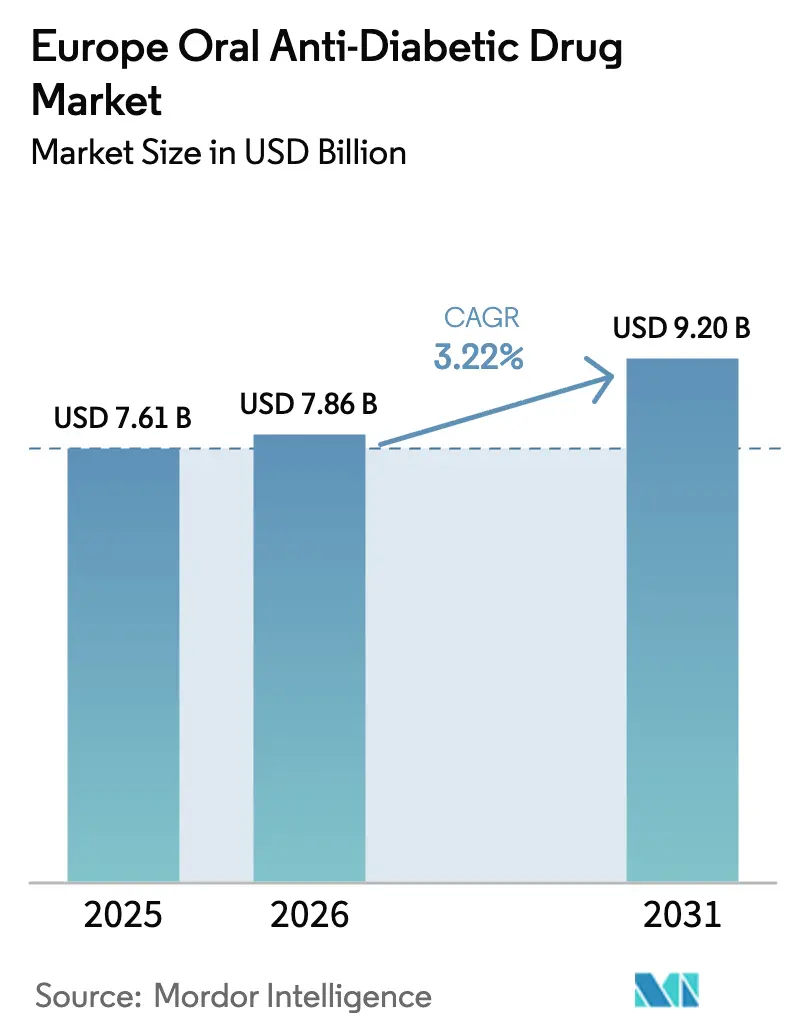

| Base Year Market Size (2025) | USD 7.61 Billion |

| Market Size (2026) | USD 7.86 Billion |

| Market Size (2031) | USD 9.2 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

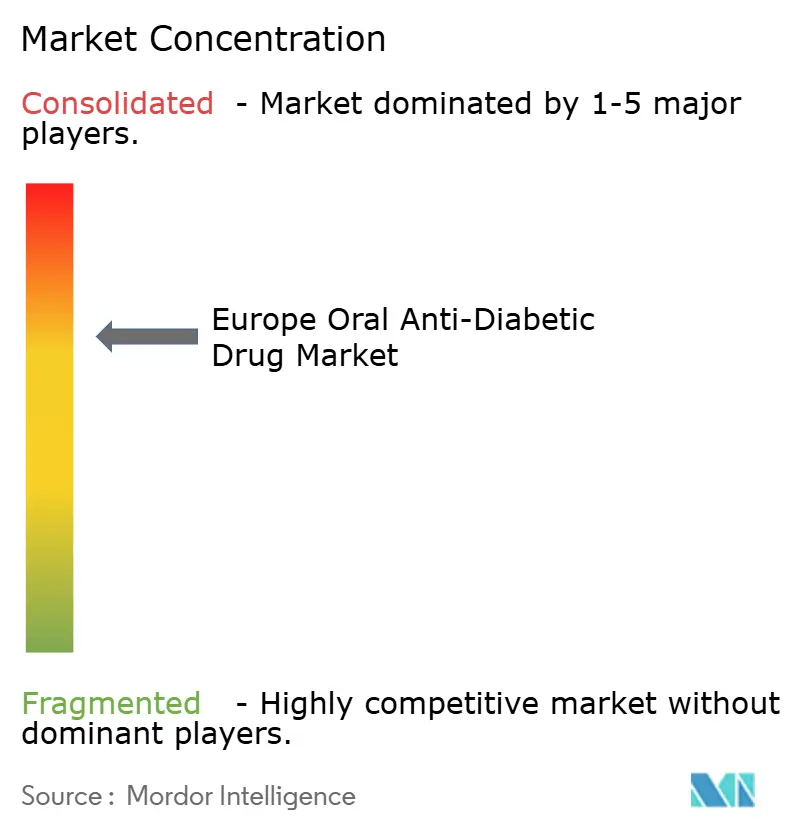

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

The Europe oral anti-diabetic drug market size was valued at USD 7.61 billion in 2025 and estimated to grow from USD 7.86 billion in 2026 to reach USD 9.2 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031). Sustained demand is shaped by the widening prevalence of obesity-linked type 2 diabetes, rapid uptake of oral GLP-1 and SGLT-2 classes, and broader cardio-renal indications that now influence prescribing decisions. Intensifying competition among incumbents and newcomers keeps prices under pressure even as patent cliffs unlock low-cost generics. Digital health mandates, especially e-prescriptions, accelerate the migration toward online dispensing, while artificial-intelligence-enabled treatment optimisation begins to influence primary-care choices. Collectively, these trends underpin the resilient expansion of the Europe oral anti-diabetic drug market despite mounting cost-containment headwinds.

Key Report Takeaways

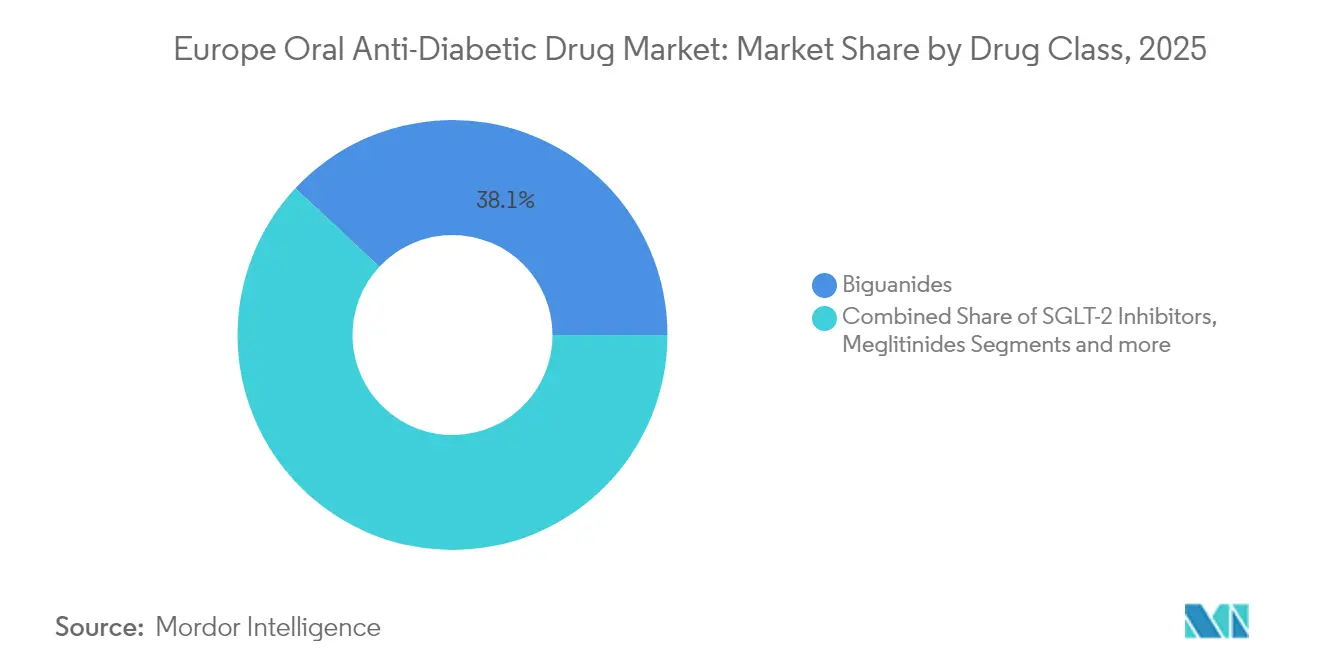

- By drug class, biguanides led with 38.05% of the Europe oral anti-diabetic drug market share in 2025, while SGLT-2 inhibitors post the fastest 3.72% CAGR through 2031.

- By age group, adults accounted for 66.35% of 2025 sales; the geriatric cohort is projected to grow at a 3.86% CAGR.

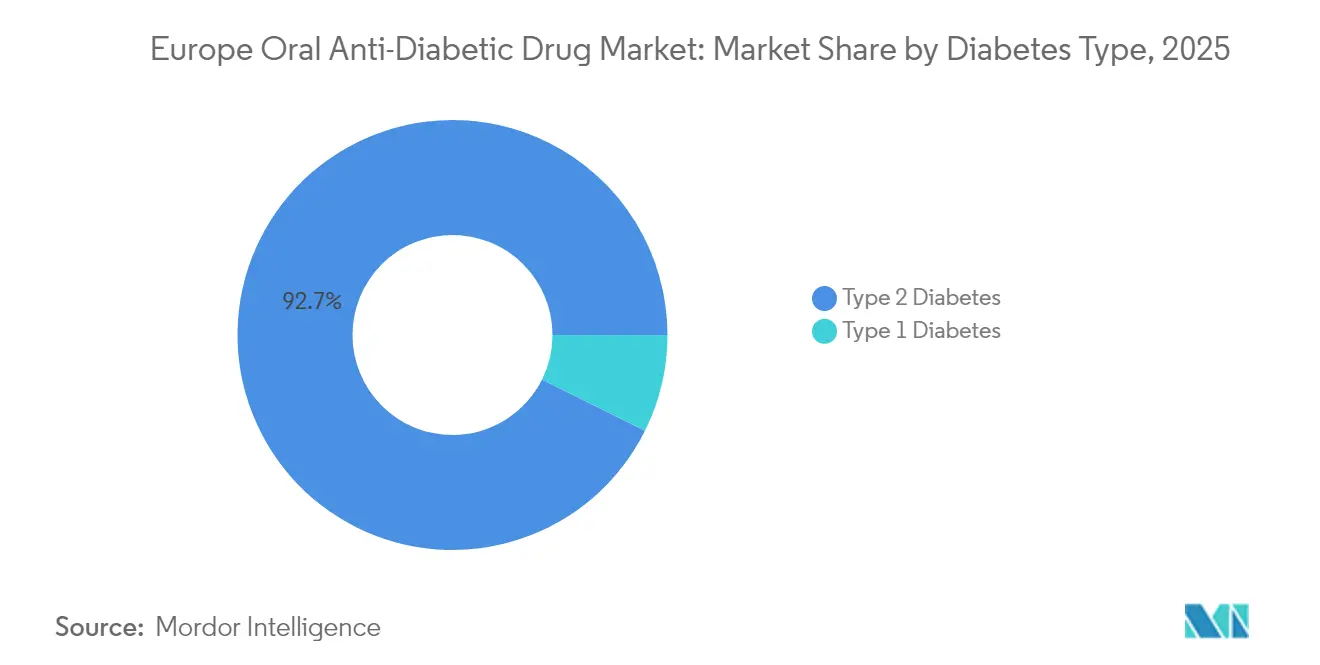

- By diabetes type, type 2 diabetes held 92.65% share of the Europe oral anti-diabetic drug market size in 2025 and is expected to expand at a 3.78% CAGR.

- By distribution channel, hospital pharmacies commanded 64.92% share in 2025, whereas online pharmacies are set to grow at a 4.05% CAGR.

- By geography, Germany captured 27.08% revenue share in 2025; France is projected to grow at the highest 3.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple regions, with Europe contributing to the overall trajectory. The outlook on worldwide oral anti-diabetic drugs market reflects how these are expected to evolve collectively.

Europe Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Prevalence of Type-2 Diabetes & Obesity | +1.2% | Global, with early gains in Germany, France, UK | Long term (≥ 4 years) |

| EU-Wide Cardio-Renal Label Expansions For SGLT-2 Class | +0.8% | EU-27 core, spill-over to Switzerland, Norway | Medium term (2-4 years) |

| Uptake Of Oral GLP-1 (Semaglutide/Rybelsus) | +0.6% | Germany & UK leading, expanding to Southern Europe | Medium term (2-4 years) |

| E-Prescription Mandates Accelerating E-Pharmacy Channels | +0.4% | Germany, France, Netherlands, expanding EU-wide | Short term (≤ 2 years) |

| Upcoming Patent Cliffs Unlocking Low-Cost Generics | +0.3% | Global impact, concentrated in major EU markets | Short term (≤ 2 years) |

| AI-Driven Poly-Pharmacy Optimisation in Primary Care | +0.2% | UK, Germany, Denmark pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Type-2 Diabetes & Obesity

Population ageing and lifestyle changes keep the absolute number of diabetic adults climbing despite public-health efforts. The International Diabetes Federation projects 784 million global cases by 2045, a figure that underpins long-run volume growth for every therapeutic class [1]Novo Nordisk, "Diabetes care," novonordisk.com. Recent Italian market data showed annual GLP-1 spending of EUR 26 billion in 2024, with private out-of-pocket purchases doubling as patients pursue advanced options. Similar momentum appeared in Portugal where sales neared EUR 20 million in early 2025 even without reimbursement. Spain’s weight-management segment rose 65% to EUR 484 million in 2024, underscoring unmet demand that transcends traditional payer funding. Collectively, these country snapshots illustrate how obesity trends directly expand the Europe oral anti-diabetic drug market.

EU-Wide Cardio-Renal Label Expansions for the SGLT-2 Class

The European Commission’s 2024 approval of empagliflozin (Jardiance) for chronic kidney disease reframed SGLT-2 inhibitors as cardio-metabolic agents rather than glucose-lowering drugs alone [2]Boehringer Ingelheim, "Boehringer Ingelheim reports strong growth in 2023 and accelerates late-stage pipeline," boehringer-ingelheim.com. With an estimated 47 million Europeans living with CKD, the addressable pool widened materially. Jardiance generated EUR 7.4 billion in 2023 revenue, reflecting 31% annual growth. Meta-analyses confirm superior reductions in HbA1c, BMI and systolic blood pressure relative to DPP-4 inhibitors, while also cutting hospitalisation for heart failure. These multidimensional benefits strengthen clinician confidence and elevate the Europe oral anti-diabetic drug market growth path.

Uptake of Oral GLP-1 (Semaglutide/Rybelsus)

The availability of a once-daily oral GLP-1 receptor agonist removes injection-related barriers that previously limited incretin adoption. Rybelsus captured 27% share of modern oral therapies in selected EMEA markets within its first commercial year. Head-to-head data show weight loss and HbA1c reductions comparable to injectable semaglutide, supporting broader guideline inclusion. Demand spikes have strained manufacturing capacity, prompting Novo Nordisk to invest USD 2.3 billion in additional filling lines. As supply stabilises, oral incretins are expected to penetrate first-line regimens, adding incremental value to the Europe oral anti-diabetic drug market.

E-Prescription Mandates Accelerating E-Pharmacy Channels

Compulsory digital prescription systems introduced across major countries during 2024 speeded the migration of chronic-care refills online. Patients appreciate doorstep delivery, automatic refills and integrated adherence reminders. Large hospital chains now transmit discharge prescriptions electronically, enabling seamless procurement through certified platforms. Regulatory bodies support the trend by mandating serialisation and tamper-proof e-vouchers, reducing counterfeit risk. These structural changes create durable tailwinds for online channels within the Europe oral anti-diabetic drug market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High List Prices of Novel Incretin & SGLT-2 Therapies | -0.9% | EU-wide, particularly Germany, France | Medium term (2-4 years) |

| Safety Signals: SGLT-2-Induced Euglycaemic DKA Cases | -0.5% | Global regulatory concern, EU implementation | Short term (≤ 2 years) |

| API Supply-Chain Fragility Within Europe & India | -0.3% | EU manufacturing hubs, India dependencies | Medium term (2-4 years) |

| Therapeutic Inertia Among General Practitioners | -0.4% | Croatia, Southern Europe, rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High List Prices of Novel Incretin & SGLT-2 Therapies

Annual acquisition costs for GLP-1 agents can exceed USD 16,000, challenging public budgets already stretched by multiple sclerosis, oncology and rare-disease drugs. Germany excludes weight-loss indications from statutory reimbursement, while France removed Wegovy from its positive list in late 2023 following incremental-benefit review. The United Kingdom limits access to specialist obesity clinics pending full NICE roll-out. Although cardiovascular-outcomes evidence continues to accumulate, payer hesitancy persists. Roughly 76 million obese but non-diabetic adults across the EU-5 therefore remain priced out of therapy, constraining upside for the Europe oral anti-diabetic drug market.

Safety Signals: SGLT-2-Induced Euglycaemic DKA Cases

Meta-analysis indicates a 3.7-fold higher risk of diabetic ketoacidosis among SGLT-2 inhibitor users compared with other oral agents. The European Medicines Agency has issued peri-operative warnings and urged pre-surgical discontinuation to mitigate rare but serious events. Case reports describe presentations with near-normal glucose levels, complicating diagnosis and heightening the need for ketone testing equipment at point-of-care. Middle-aged women with long-standing type 2 diabetes appear disproportionately affected [3]European Medicines Agency, "Meeting highlights from the Pharmacovigilance Risk Assessment Committee," ema.europa.eu. These concerns moderate the otherwise robust expansion trajectory of the Europe oral anti-diabetic drug market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Expanding Role of SGLT-2 Inhibitors

Biguanides continued to command 38.05% of 2025 prescriptions, anchoring first-line therapy due to low cost and extensive familiarity. However, SGLT-2 inhibitors delivered the fastest 3.72% CAGR toward 2031 as multidimensional cardio-renal benefits drive physician preference. Sulfonylurea use declined sharply in parts of Southern Europe, mirroring global de-adoption trends linked to hypoglycaemia risk. DPP-4 inhibitors maintained a steady but unremarkable footprint, chiefly in patients unsuitable for SGLT-2 or GLP-1 agents.

The “others” bucket, including dual GIP/GLP-1 agonists such as tirzepatide, shows high clinical promise following network meta-analyses that reported a 2.24% HbA1c decline. Alpha-glucosidase inhibitors and thiazolidinediones now occupy niche roles, reserved for specific intolerance scenarios. Across this landscape, the Europe oral anti-diabetic drug market size allotted to innovation-driven classes keeps expanding, even as metformin retains volume leadership. Declining sulfonylurea demand exemplifies how guideline shifts and outcome data continuously reshape the Europe oral anti-diabetic drug market.

By Age Group: Geriatric Uptake Intensifies

Adults accounted for 66.35% of 2025 utilisation, reflecting the core working-age burden of type 2 diabetes. Yet the geriatric segment exhibited a 3.86% CAGR, powered by refined guidelines that advocate complication-oriented treatment regardless of chronological age. Swiss registry data highlight persistently sub-optimal control rates among seniors, underscoring the need for agents with low hypoglycaemia risk. SGLT-2 inhibitors and GLP-1 receptor agonists meet that requirement but necessitate vigilant renal-function monitoring.

Portuguese community studies revealed 97.7% adherence in older adults yet low achievement of blood-pressure and fasting-glucose targets, signalling unmet multidimensional needs. Digital therapeutics show promise: AI-driven “digital twin” models cut medication requirements by 74% while preserving glycaemia. These trends collectively elevate the Europe oral anti-diabetic drug market size associated with the geriatric cohort. Paediatric prescriptions remain modest, limited chiefly to metformin in adolescents experiencing insulin resistance.

By Diabetes Type: Type 2 Remains the Growth Engine

Type 2 diabetes held 92.65% of revenue in 2025 and is advancing at a 3.78% CAGR to 2031 as earlier diagnosis and broader therapy initiation widen the treated pool. Oral semaglutide has gained notable traction, often supplanting DPP-4 inhibitors because of superior weight and HbA1c outcomes.

Automated insulin-delivery trials show that adjunctive SGLT-2 therapy can improve time-in-range in selected type 1 patients, though risk–benefit assessment remains case specific. For the foreseeable horizon, clinicians anchoring decisions on renal and cardiovascular protection will keep the Europe oral anti-diabetic drug market weighted heavily toward type 2 disease. Type 1 utilisation will stay confined to specialist centres until regulators and payers expand approved indications.

By Distribution Channel: Digital Dispensing Gains Ground

Hospital pharmacies retained 64.92% share in 2025, reflecting their central role in complex case initiation and inpatient management. Online pharmacies, while still a minority channel, are projected to post a 4.05% CAGR as e-prescription rules remove logistical friction. Patients cite convenience, full-line availability and transparent pricing as key attractors. Retail community outlets maintain relevance for chronic refills of metformin and other generics.

Germany and the United Kingdom lead in digital uptake thanks to permissive regulations that allow prescription fulfilment via accredited platforms. Stringent serialisation rules guard against counterfeits, supporting trust in the channel. These structural changes ensure that the Europe oral anti-diabetic drug market continues to diversify away from traditional bricks-and-mortar outlets. Integration of medication-adherence reminders within e-pharmacy apps positions the channel to capture incremental value through improved outcomes.

Geography Analysis

Germany remained the largest national contributor with 27.08% share in 2025, anchored by a broad specialist network and early adoption of SGLT-2 inhibitors following positive reimbursement decisions. The country’s compulsory e-prescription rollout in early 2024 accelerated digital-dispensing penetration, easing access for chronic patients. Boehringer Ingelheim’s domestic leadership, underpinned by Jardiance, continues to influence prescribing norms throughout Central Europe.

France is poised for the fastest 3.98% CAGR, supported by evolving reimbursement frameworks that increasingly recognise cardiovascular-outcome benefits. The 2024 withdrawal of Wegovy reimbursement slowed GLP-1 uptake temporarily, but pathway revisions are under discussion to balance affordability and public-health objectives. National health-data platforms facilitate real-world-evidence collection, thereby hastening label and guideline updates that reinforce market momentum.

The United Kingdom exhibits sophisticated market dynamics driven by NICE’s incremental technology appraisal approach. While GLP-1 access still sits primarily within specialist obesity clinics, broader NHS integration is scheduled to commence in 2025. Italy demonstrates how high out-of-pocket willingness can bridge publicly funded gaps, as private GLP-1 expenditure doubled in 2024. Spain and Portugal, though smaller in absolute value, posted double-digit volume growth as unmet obesity and diabetes needs override funding limitations. Outside the EU-5, Switzerland’s 2024 approval of tirzepatide for weight management illustrates regulatory agility. Meanwhile, markets such as Croatia highlight therapeutic inertia, with utilisation of SGLT-2 and GLP-1 classes far below guideline recommendations, indicating education opportunities that can further expand the Europe oral anti-diabetic drug market.

Analysis of the oral anti-diabetic drugs market by Mordor Intelligence spans multiple other regional evaluations across North America, Asia, and Latin America, supported by country-level insights for Italy, France, Malaysia, South Korea, Vietnam, and Indonesia, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Competition is dominated by a concentrated group of global innovators. Novo Nordisk controlled 55.3% of the GLP-1 segment in 2024 and 34% of total diabetes revenue, but capacity constraints led to periodic shortages. The company responded with USD 2.3 billion in new filling-line investments and the acquisition of three Catalent sites to de-risk supply. Eli Lilly, leveraging tirzepatide’s dual-agonist profile, committed USD 5.3 billion to its Indiana complex, targeting both obesity and diabetes demand surges.

Boehringer Ingelheim leveraged Jardiance’s chronic-kidney-disease indication to solidify its regional standing and invested EUR 120 million to expand tablet output in Greece. Sanofi, pivoting from traditional basal-insulin dominance, partnered with Health2Sync to integrate its SoloSmart connected-device ecosystem, signalling a shift toward data-enabled value propositions. Roche, via its collaboration with Zealand Pharma on amylin analogue petrelintide, exemplifies diversification into novel hormonal pathways that may reshape the Europe oral anti-diabetic drug market over the next decade.

Generic manufacturers are positioning for the post-2026 wave of GLP-1 patent expirations. Sandoz publicly confirmed internal development programmes and aims to leverage its established insulin-biosimilar infrastructure. Merck’s USD 2 billion licence agreement with Hansoh Pharma grants rights to an emerging oral GLP-1 agonist, reflecting big-pharma appetite for fast-follow assets. Supply-chain resilience has become a core differentiator: firms with end-to-end European active-pharmaceutical-ingredient capability enjoy a strategic hedge against geopolitical or pandemic-driven disruptions.

Europe Oral Anti-Diabetic Drug Industry Leaders

-

Sanofi

-

Eli Lilly

-

Astrazeneca

-

Astellas

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: UK High Court revoked AstraZeneca’s supplementary protection certificate and core patent covering dapagliflozin.

- August 2024: Sanofi partnered with Health2Sync to roll out the SoloSmart digital solution, enriching real-time patient monitoring for over 1.3 million registered users.

- May 2024: Sanofi announced more than EUR 1 billion investment to expand biomanufacturing capacity in France and create 500 new positions.

Europe Oral Anti-Diabetic Drug Market Report Scope

Antihyperglycemic medications are taken orally to lower blood glucose levels. They are frequently employed in the management of type 2 diabetes. The Europe Oral Anti-Diabetic Drug Market is set to witness a CAGR of more than 3% during the forecast period. The Europe Oral Anti-Diabetic Drug Market is segmented into drugs (Biguanides, Alpha-glucosidase inhibitors, Dopamine-D2 receptor agonists, Sodium-glucose Cotransport-2 (SGLT-2) inhibitor, Dipeptidyl Peptidase-4 (DPP-4) Inhibitors, Sulfonylureas, and Meglitinides), and Geography. The report offers the value (in USD million) and volume (in Units million) for the above segments.

| Biguanides |

| Sulfonylureas |

| Meglitinides |

| Thiazolidinediones |

| Alpha-Glucosidase Inhibitors |

| DPP-4 Inhibitors |

| SGLT-2 Inhibitors |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| Type 1 Diabetes |

| Type 2 Diabetes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Drug Class | Biguanides |

| Sulfonylureas | |

| Meglitinides | |

| Thiazolidinediones | |

| Alpha-Glucosidase Inhibitors | |

| DPP-4 Inhibitors | |

| SGLT-2 Inhibitors | |

| Others | |

| By Age Group | Adults |

| Pediatric | |

| Geriatric | |

| By Diabetes Type | Type 1 Diabetes |

| Type 2 Diabetes | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe oral anti-diabetic drug market?

The market generated USD 7.86 billion in 2026 and is projected to reach USD 9.2 billion by 2031 at a 3.22% CAGR (2026-2031).

Which drug class is expanding fastest?

SGLT-2 inhibitors show the highest 3.72% CAGR through 2031, propelled by new cardio-renal indications.

How dominant is type 2 diabetes in market revenue?

Type 2 diabetes represents 92.65% of 2025 sales and is forecast to grow at 3.78% annually through 2031.

Why are online pharmacies gaining traction?

Mandatory e-prescription systems and patient preference for home delivery enable a 4.05% CAGR for online channels to 2031.

Which company leads the GLP-1 segment?

Novo Nordisk held 55.3% of global GLP-1 revenue in 2024, supported by strong demand for semaglutide products.

What main challenge could slow market growth?

High list prices for novel incretin and SGLT-2 therapies strain payer budgets, exerting a −0.9% drag on forecast CAGR.

Page last updated on: