Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

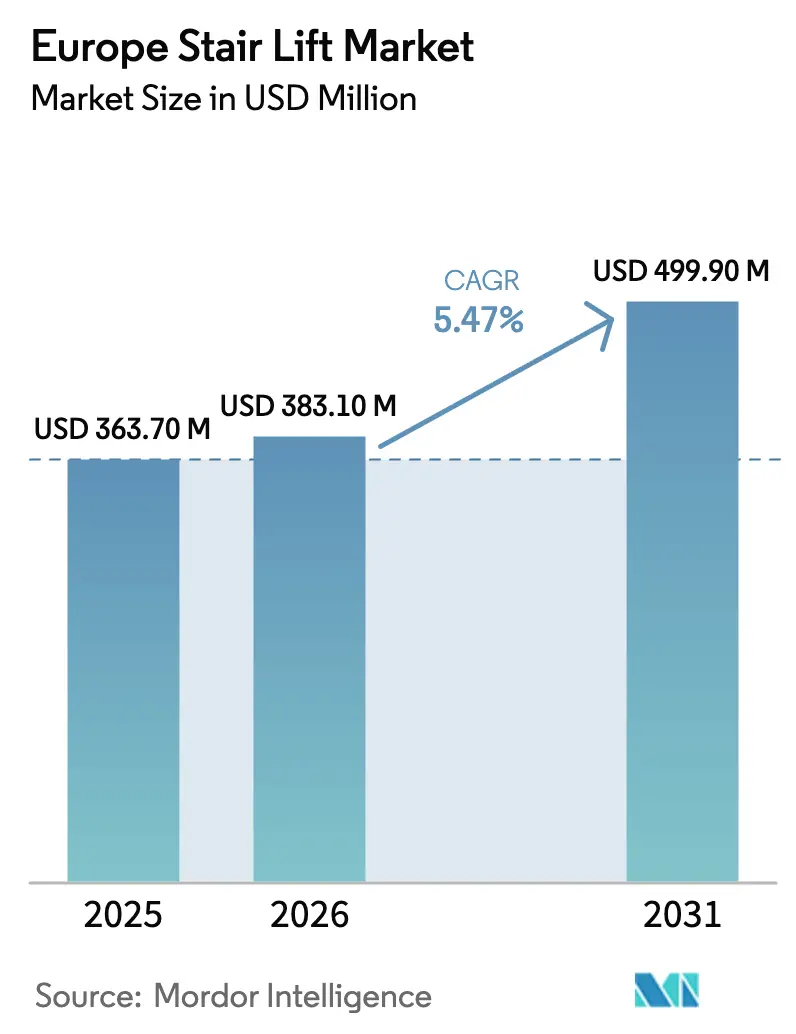

| Base Year Market Size (2025) | USD 363.70 Million |

| Market Size (2026) | USD 383.10 Million |

| Market Size (2031) | USD 499.90 Million |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Stair Lift Market Analysis by Mordor Intelligence

The Europe Stair Lift Market size was valued at USD 363.70 million in 2025 and is estimated to grow from USD 383.10 million in 2026 to reach USD 499.90 million by 2031, at a CAGR of 5.47% during the forecast period (2026-2031). A steadily widening base of residents aged 65 and above, already above one-fifth of the region’s population, is steadily enlarging addressable demand.[1]Eurostat, “Population Structure and Ageing,” EUROSTAT Rising disability prevalence, coupled with a strong preference for aging at home, keeps conversion activity brisk, especially in owner-occupied dwellings that can support retrofit spending. Fiscal incentives ranging from the United Kingdom’s VAT-relief scheme to Germany’s Pflegekasse grants soften upfront costs and broaden access. Manufacturers are sharpening their focus on modular rail systems and factory-standardized components, trimming installation time and helping curved models gain traction. Competitive attention is shifting toward rental subscriptions, smart-home interoperability, and IoT-driven remote diagnostics that cut downtime and strengthen after-sales economics, while the European Accessibility Act solidifies technical compliance norms that favour well-capitalized providers.

Key Report Takeaways

- By rail orientation, straight models captured 67.10% of the Europe stair lift market share in 2025, while curved variants are forecast to grow at a 10.72% CAGR through 2031.

- By user orientation, seated configurations held 71.80% share of the Europe stair lift market size in 2025, whereas standing units are projected to expand at a 9.42% CAGR to 2031.

- By installation site, indoor systems accounted for 80.60% of the Europe stair lift market share in 2025, with outdoor models poised for a 10.28% CAGR over the same period.

- By application, residential settings represented 68.05% share of the Europe stair lift market size in 2025, and healthcare facilities are set to register a 9.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Stair Lift Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising proportion of aged people and disability prevalence | +2.80% | Europe-wide, highest in Italy, Portugal, Bulgaria | Long term (≥ 4 years) |

| Growing home-care preference to avoid institutionalisation | +2.10% | UK, Germany, Netherlands, France | Medium term (2-4 years) |

| Advancements in modular rail manufacturing and retrofit kits | +1.50% | Germany, UK, Czech Republic manufacturing hubs | Short term (≤ 2 years) |

| Subsidies and VAT-exempt schemes for mobility aids | +1.20% | UK, Germany, Austria, Netherlands | Medium term (2-4 years) |

| Emergence of rental and subscription models | +0.90% | UK, Germany, France | Short term (≤ 2 years) |

| Smart-home integration and IoT remote diagnostics | +0.50% | Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Proportion of Aged People and Disability Prevalence

Europe’s age structure is shifting toward older cohorts as the baby-boomer generation enters advanced years, lifting the potential customer pool for accessibility products. The population aged 65 and above climbed from 90.5 million in 2019 to 97.8 million in 2024 and is projected to top 129.8 million by 2050. Mobility limitations intensify with age, creating sustained demand for stair lifts that enable safe vertical movement inside multi-story homes. Elderly women experience higher mobility constraints than men, a dynamic that influences product marketing and feature emphasis. Rural regions, where older residents are more concentrated and elevator-equipped housing is scarce, represent fertile ground for retrofit activity. Countries such as Italy, Portugal, and Bulgaria, which post the largest elderly shares, carry particularly strong long-term potential for the Europe stair lift market.

Growing Home-Care Preference to Avoid Institutionalization

Households across Europe increasingly opt for community-based or domiciliary care rather than nursing-home placement. Uptake of home-care services among people aged 75 and over climbed sharply during the pandemic and remains elevated as public health authorities promote independent living. Financial prudence underpins this choice; average daily nursing-home charges often exceed the cost of installing a stair lift within two years of residency. Disabled homeowners also display a higher incidence of income strain, making one-time retrofits supplemented by grants or VAT exemptions more attractive than recurring institutional fees. Policy instruments such as the United Kingdom’s Disabled Facilities Grant and Germany’s adaptation allowances strengthen this preference by lowering capital outlays. As a result, conversion rates in owner-occupied dwellings continue to advance, particularly in markets with streamlined grant-application processes.

Advancements in Modular Rail Manufacturing and Retrofit Kits

Suppliers are redesigning rails into modular, prefabricated segments that can be cut, adjusted, and joined on-site, transforming the economics of curved installations. Production lines in the Czech Republic and the United Kingdom now employ laser-guided welding and automated quality control to shorten lead times, reduce material waste, and raise throughput.[2]Stannah Group, “The Stannah Report 2024,” STANNAH GROUP Installers benefit from lighter components that navigate narrow or winding staircases without structural changes, extending addressable demand in heritage properties common across Europe. Modular designs also minimize downtime between measurement and commissioning, shrinking project cycles from weeks to days in many cases. Lower fabrication cost per unit allows dealers to defend margins while offering more competitive pricing, a combination that accelerates replacement cycles for aging equipment. Continued investment in additive manufacturing, especially for bespoke brackets and gear housings, is projected to sustain this positive cost trajectory.

Subsidies and VAT-Exempt Schemes for Mobility Aids

Many governments recognize accessibility as a social imperative and deploy fiscal instruments that lower consumer out-of-pocket expense. The United Kingdom exempts qualifying stair-lift purchases from the 20% value-added tax, easing the price shock for retirees living on fixed incomes. Germany reimburses a portion of adaptation expenses through statutory care insurance, while Austria and the Netherlands run mobility-budget programs that top up household contributions. Local authorities often bundle direct cash grants with low-interest loans, expanding eligibility beyond the poorest quintiles. Public sector support is especially influential in outer-urban and rural districts where median disposable income lags national averages. As policymakers face the fiscal realities of long-term care, maintaining elderly independence at home through co-financed stair lifts remains a fiscally efficient alternative to institutional subsidies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront purchase and installation cost | -1.80% | Eastern and Southern Europe, rural areas | Medium term (2-4 years) |

| Complex staircase geometries inflating customisation prices | -1.20% | Historic city centers, older housing stock | Long term (≥ 4 years) |

| Perceived stigma associated with assistive devices | -0.80% | Southern Europe, traditional communities | Medium term (2-4 years) |

| Limited reimbursement coverage outside medical indication | -0.60% | Eastern Europe, private healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Purchase and Installation Cost

Despite supportive grant mechanisms, the sticker price of a new stair lift remains a hurdle for households in lower-income regions. Indoor straight models commonly start around GBP 2,500 (USD 3,175) when purchased without subsidies, and price escalates sharply for outdoor units requiring weatherproofing. Electrical upgrades, structural reinforcements, and certified installation services can add several hundred dollars to the final invoice. Buyers in Eastern and Southern Europe, where disposable income trails the EU average, often defer purchase or seek second-hand units, slowing penetration in these territories. Rental programs and manufacturer-backed financing mitigate the burden but do not fully offset the perception of high cost, especially where awareness of grant eligibility is limited. Continued pressure on public budgets could temper future subsidy growth, keeping affordability at the center of competitive strategy within the Europe stair lift market.

Complex Staircase Geometries Inflating Customization Prices

Europe’s architectural heritage delivers visual charm yet often complicates accessibility retrofits. Spiral stairs, narrow treads, and multi-landing layouts force dealers to commission custom rails that double fabrication time and inflate material usage. Historic-preservation rules in city cores restrict structural alterations, further elevating engineering complexity. Narrow staircases under 850 mm wide, which are common in pre-1970 properties, require space-saving designs or partial wall removal, adding cost and professional services fees. Limited resale value of bespoke curved rails constrains the secondary market, depriving budget-conscious buyers of lower-cost options. Manufacturers are introducing slimmer carriages and reduced-radius turn systems, but until these innovations scale, architectural challenges will cap installation volumes in the hardest-to-fit dwellings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rail Orientation: Straight Dominates Volume While Curved Rises Quickly

Straight units maintained 67.10% of the Europe stair lift market share in 2025, reflecting their compatibility with most single-flight staircases and lower installed cost. The Europe stair lift market size for curved installations is projected to expand at a 10.72% CAGR through 2031 as modular manufacturing trims lead times and reduces per-unit expense. Straight models continue to benefit from bulk procurement by public housing authorities and large care-home chains, where standardized footprints simplify fleet maintenance. Curved systems attract homeowners in historic districts and urban row houses that feature tight landings or 90-degree turns. Vendors are expanding factory capacity in Central Europe to handle rising curved demand, combating the perception that customization equals prohibitively long waits. As production ramps and rental fleets accumulate, price differentials between straight and curved products should narrow, unlocking additional addressable households for the Europe stair lift market.

Installation crews report that modular rail segments now shave multiple hours off onsite assembly, reducing occupant disruption and decreasing labour cost per project. Manufacturers also incorporate lighter alloys and updated drive trains that improve ride smoothness on longer or more complex curves. The shift toward predictive maintenance is expected to resonate with curved owners, who often occupy older properties susceptible to humidity and temperature swings that can accelerate component wear. Accordingly, dealers highlight remote-diagnostic packages when pitching premium curved options, reinforcing total cost-of-ownership advantages across the equipment’s service life.

By User Orientation: Seated Leads, Standing Builds Momentum

Seated lifts constituted 71.80% of shipments in 2025 and remain the default choice for multi-user households due to universal appeal and enhanced comfort. Standing units are forecast to log a 9.42% CAGR to 2031, appealing to users with knee stiffness, partial weight-bearing capacity, or highly constrained stair widths. The Europe stair lift market size for standing variants is further buoyed by condominiums and terraced homes where stair treads are shallow and headroom is limited. Seated models are gaining refinements such as swivel-away footplates, multi-point harnesses, and antimicrobial seat covers that reflect lessons from healthcare facility procurement. Standing lifts now incorporate fold-down perches, integrated grab rails, and sensor-locked doors that add stability and confidence during ascent, addressing safety concerns that once limited uptake.

Integration of both modes in hybrid platforms provides futureproofing for households anticipating progressive mobility decline. Dealers often recommend hybrid models to families expecting multiple generations to use a single installation, promoting longevity and resale flexibility. As software features standardize across orientations, functional differences dwindle to physical footprint and posture preference, enabling higher gross margin on standing sales without major incremental R&D expense. This trend supports greater product-line diversification inside the Europe stair lift market, assisting smaller dealers in catering to niche requirements without bloating inventory.

By Installation: Indoor Commands the Base, Outdoor Accelerates

Indoor placements represented 80.60% of 2025 installations, mirroring Europe’s predominance of multi-floor housing that lacks private elevators. Outdoor units are projected to post a 10.28% CAGR through 2031, aided by improved ingress protection and corrosion-resistant materials that extend operating life in wet climates. Installation of an outdoor system typically adds GBP 500–1,000 (USD 635–1,270) over an indoor equivalent due to weatherproof wiring, foundation anchoring, and drainage mitigation. Yet the upside is significant for bungalows with raised entries, terraced gardens, and split-level patios, all of which can isolate mobility-impaired residents. Manufacturers newly offer heated seats, UV-stable upholstery, and lithium-ion batteries rated for sub-zero environments that are common in Nordic territories.

Indoor adoption shows no signs of saturation, as loft conversions and basement living areas remain widespread across Western Europe. Many property owners schedule indoor installs in tandem with kitchen or bath renovations to streamline financing and minimize total renovation downtime. IoT capabilities are rolling out first in indoor models where Wi-Fi coverage is stronger, but outdoor variants will likely follow as 5G, and mesh networks proliferate. As climate-change resilience gains policy priority, local codes may soon demand exterior barrier-free access points in new construction, reinforcing the outdoor opportunity in the Europe stair lift market.

By Application: Residential Base Sustains, Healthcare Facilities Surge

Residential use accounted for 68.05% of 2025-unit placements, underscoring homeowners’ determination to age in familiar surroundings. Healthcare facilities ranging from outpatient centers to rehabilitation clinics are set to record a 9.88% CAGR through 2031, spurred by stricter clinical safety standards and rising patient throughput. Many clinics favour platform lifts for stretcher transport, yet stair lifts remain popular in staff areas and narrow fire-escape routes where elevators do not fit. Commercial buildings, including retail and office properties, integrate stair lifts to meet European Accessibility Act compliance milestones, though their share of the Europe stair lift market remains comparatively modest.

Residential growth remains anchored in retrofit grants and the willingness of adult children to co-finance installations for aging parents. Long-term mortgage tenures in several European countries make it practical to roll stair-lift upgrades into home-equity lines, trading upfront cash outflow for manageable instalments. Healthcare facilities increasingly specify antimicrobial finishes, sealed drive housings, and quick-swap battery packs to reduce downtime between patient transfers. These requirements spill over into premium residential models, illustrating technology transfer from institutional to domestic segments and bolstering functional convergence across applications in the Europe stair lift market.

Geography Analysis

The United Kingdom continues to hold the leading national position, underpinned by VAT relief, Disabled Facilities Grants worth up to GBP 30,000 (USD 38,100), and a dense dealer network capable of 24-hour callouts. Penetration is further aided by building-code provisions that require new homes to maintain stair widths suitable for future stair-lift retrofits, anchoring long-term pipeline visibility. Rental programs originated here and have attained significant scale, widening access among temporary users awaiting surgery or limited rehabilitation periods.

Germany is the fastest-growing major market, propelled by statutory long-term care insurance that reimburses a portion of residential adaptations. Dealer networks benefit from an engineering-centric culture that values quality certification, driving willingness to pay for IoT connectivity, automatic swivel technology, and proactive maintenance alerts. Czech-based rail manufacturing supports just-in-time deliveries into southern Germany, tightening lead times despite elevated demand. Federal subsidies for energy-efficient home retrofits can be layered onto accessibility works, encouraging homeowners to combine thermal-envelope upgrades with stair-lift installations.

France, Italy, and Spain cluster in a middle-growth band but offer considerable headroom due to high percentages of multi-story dwellings and rapidly aging populations. Tax-credit frameworks and municipal co-financing schemes are proliferating, although administrative complexity can slow execution. Southern European climates also boost outdoor unit demand for garden and veranda access. The broader Rest of Europe segment includes Nordic countries where smart-home integration rates are the highest and emerging Eastern markets where affordability remains the key bottleneck. Harmonized accessibility standards are gradually levelling requirements, allowing manufacturers to replicate product platforms across sub-regions and elevate volumes across the Europe stair lift market.

Competitive Landscape

The Europe stair lift market displays moderate concentration, with a handful of multinational manufacturers controlling most branded shipments. Stannah leverages dual-plant capacity in the United Kingdom and Czech Republic to serve both straight and curved niches, coupling rapid production with a field force that maintains over 90,000 units under service contract. Companies are intensifying R&D into lithium-ion powertrains, wireless call stations, and self-diagnostic firmware to differentiate value beyond basic lift function.

Rental and subscription programs are expanding dealer annuity streams, lowering entry costs, and creating secondary fleets that can be refurbished for price-sensitive geographies. Manufacturers collaborate with finance houses to bundle equipment and service on multi-year operating leases, shifting procurement from capex to opex. Partnerships between stair-lift firms and smart-home platforms aim to embed voice control, geofencing, and caregiver alerts, elevating product relevance to tech-savvy seniors.

The European Accessibility Act raises documentation and testing thresholds, which larger incumbents meet through accredited labs and full-time regulatory teams, erecting barriers for smaller assemblers. However, niche players excel in portable and trackless lifts that cater to temporary events or rental properties. White-space opportunities persist in multi-language user interfaces, low-rise home lifts that complement stair lifts, and subscription-based monitoring services that share anonymized usage statistics with insurers. Consolidation remains likely as strategic buyers pursue geographic fill-ins and technology tuck-ins to boost share in the Europe stair lift market.[4]Otolift, “Commitment to Sustainability,” OTOLIFT

Europe Stair Lift Industry Leaders

Handicare Group AB

Stannah Lifts Holdings Ltd

Acorn Mobility Services Ltd

Thyssenkrupp Elevator AG

Candor Care Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Full applicability of the European Accessibility Act imposed harmonized product and service rules across all EU member states, raising compliance obligations for stair-lift vendors.

- April 2025: Several U.K. dealers widened rental offers with flexible monthly terms that bundle installation, removal, and service, targeting customers with short-term mobility loss.

- March 2025: Stannah launched Uplifts, a residential home lift line with through-floor travel in two cabin sizes, broadening the company’s accessibility portfolio.

- March 2025: Lehner Lifttechnik reported 95% export share across 80 countries, underscoring its focus on international expansion and TÜV-certified quality standards.

Europe Stair Lift Market Report Scope

A stair lift is commonly deployed to lift people down the staircases, and a stair lift is a chair, a mechanical lifting device that glides up and down a staircase on a motorized rail. It is typically used by persons with restricted mobility or disabilities who cannot navigate stairs without needing assistance in outdoor and indoor environments. The study considers the revenue generated from the sale of Stairlifts by various vendors in the region.

The European stair lift market is segmented by rail orientation (straight, curved), user orientation (seated, standing, integrated), installation (indoor, outdoor), application (residential, healthcare), and country (United Kingdom, France, Germany, Rest of Europe).

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Rail Orientation

| Straight |

| Curved |

By User Orientation

| Seated |

| Standing |

| Integrated |

By Installation

| Indoor |

| Outdoor |

By Application

| Residential |

| Healthcare Facilities |

| Commercial |

| Other Applications |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Rail Orientation | Straight |

| Curved | |

| By User Orientation | Seated |

| Standing | |

| Integrated | |

| By Installation | Indoor |

| Outdoor | |

| By Application | Residential |

| Healthcare Facilities | |

| Commercial | |

| Other Applications | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe stair lift market?

The Europe stair lift market size stands at USD 383.1 million in 2026 and is on track to reach USD 499.9 million by 2031.

How fast is the Europe stair lift market expected to grow?

The market is projected to post an 5.47% CAGR between 2026 and 2031, driven by demographic aging and supportive subsidy frameworks.

Which product type leads sales across Europe?

Straight-rail stair lifts hold the largest share at 67.10%, thanks to simpler design and lower installed cost.

What is the main growth area inside healthcare settings?

Hospital and clinic adoption is forecast to climb at a 9.88% CAGR as facilities upgrade to comply with the European Accessibility Act and rising patient flow.

How are rental models influencing adoption?

Weekly or monthly subscription packages are lowering upfront cost, widening access for short-term users, and creating a profitable recurring-revenue stream.

Which technology trends are reshaping stair-lift offerings?

IoT-enabled remote diagnostics, smart-home voice control integration, and modular manufacturing that shortens lead time are quickly becoming standard features.

Page last updated on: