Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

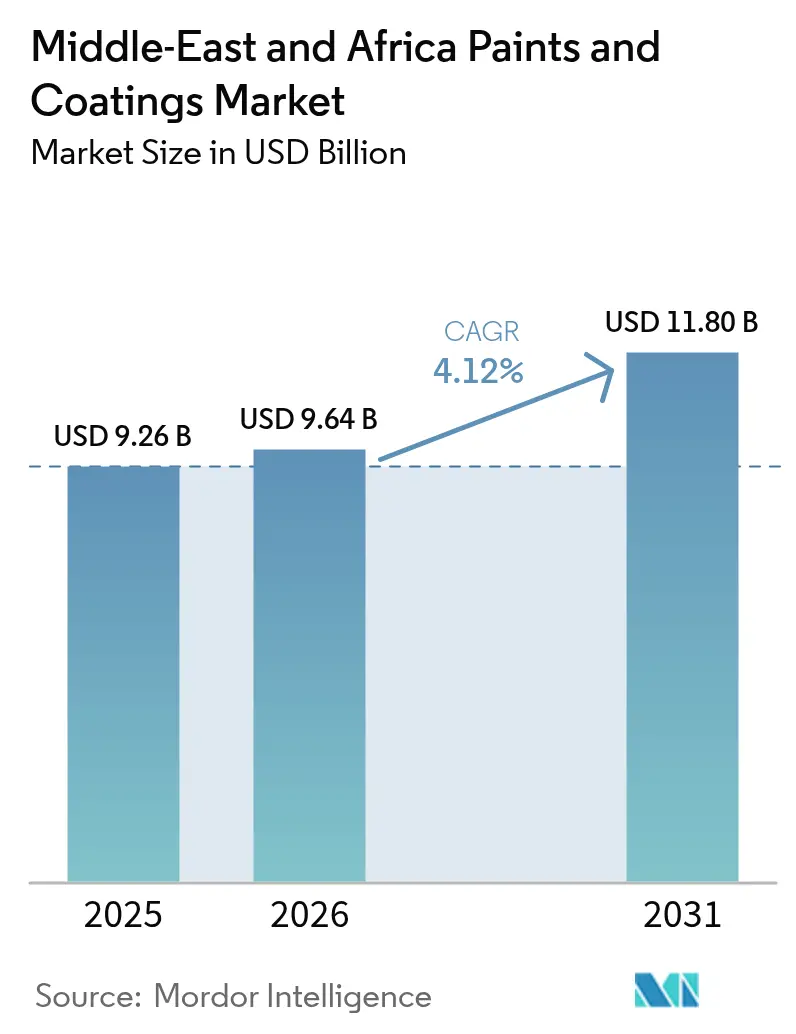

| Base Year Market Size (2025) | USD 9.26 Billion |

| Market Size (2026) | USD 9.64 Billion |

| Market Size (2031) | USD 11.80 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

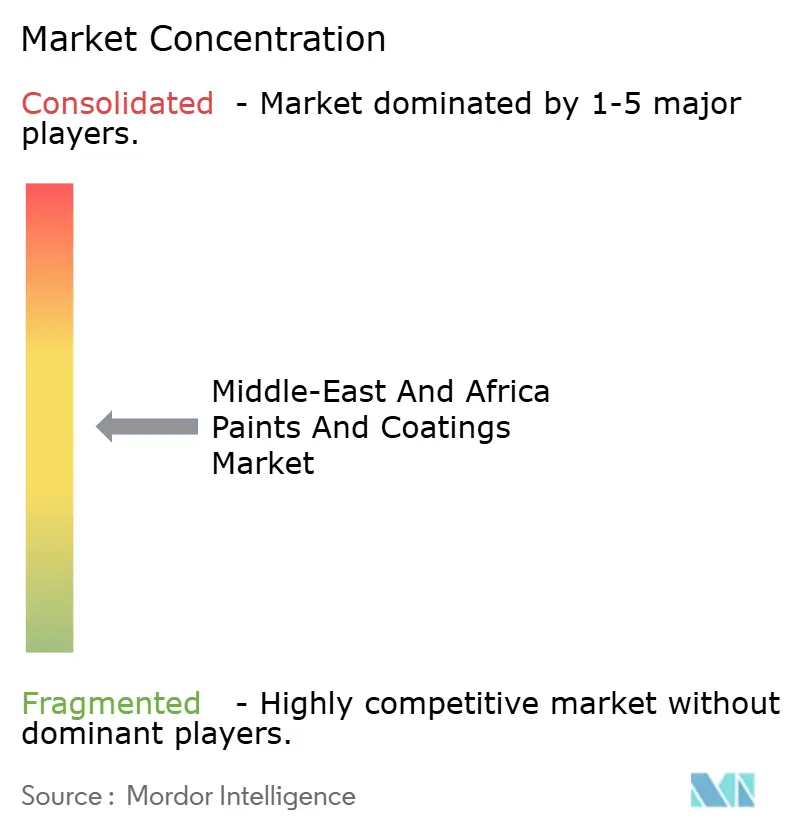

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Paints And Coatings Market Analysis by Mordor Intelligence

The Middle-East and Africa Paints and Coatings Market size is projected to be USD 9.26 billion in 2025, USD 9.64 billion in 2026, and reach USD 11.80 billion by 2031, growing at a CAGR of 4.12% from 2026 to 2031. Governments in the Gulf Cooperation Council (GCC) are linking their Vision 2030 goals to incentives for local manufacturing. This move is spurring the establishment of new facilities, reducing lead times, and setting up research and development centers within free zones. Concurrently, a resurgence in housing across North and East Africa is boosting architectural activities that had previously stalled due to the oil downturn from 2020 to 2022. New regulations, specifically GSO 2764:2024, are tightening ceilings on volatile organic compounds (VOCs), further pushing the industry towards water-based solutions. While fluctuations in Brent crude prices and new carbon accounting rules are squeezing margins for solvent-based products, suppliers offering high-performance waterborne, powder, and low-carbon solutions are enjoying premium pricing. These shifts in the resin market are being driven by a combination of mega-projects, mandates for localized industries, and a regional move towards eco-friendlier formulations.

Key Report Takeaways

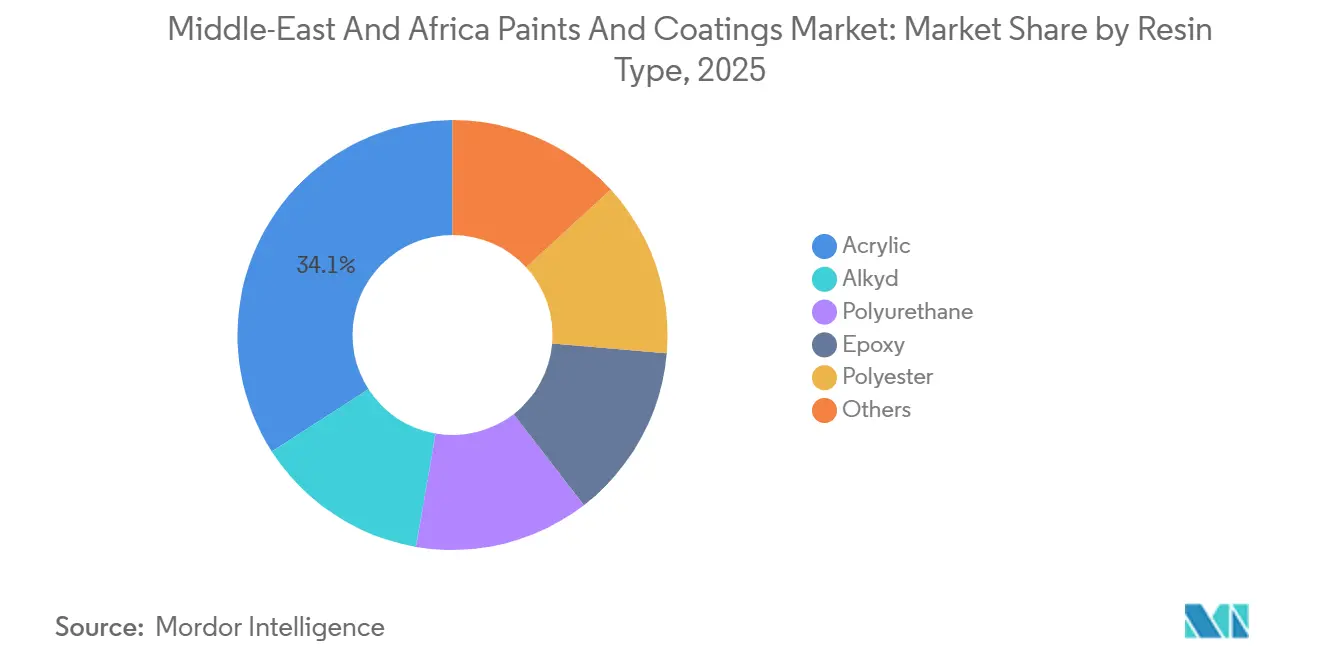

- By resin type, acrylic held 34.11% of the Middle-East and Africa paints and coatings market share in 2025, while polyurethane posted the fastest 4.31% CAGR through 2031.

- By technology, solvent-borne systems retained 48.05% share of the Middle-East, and Africa paints and coatings market size in 2025, yet water-based formulations are expanding at a 4.38% CAGR to 2031.

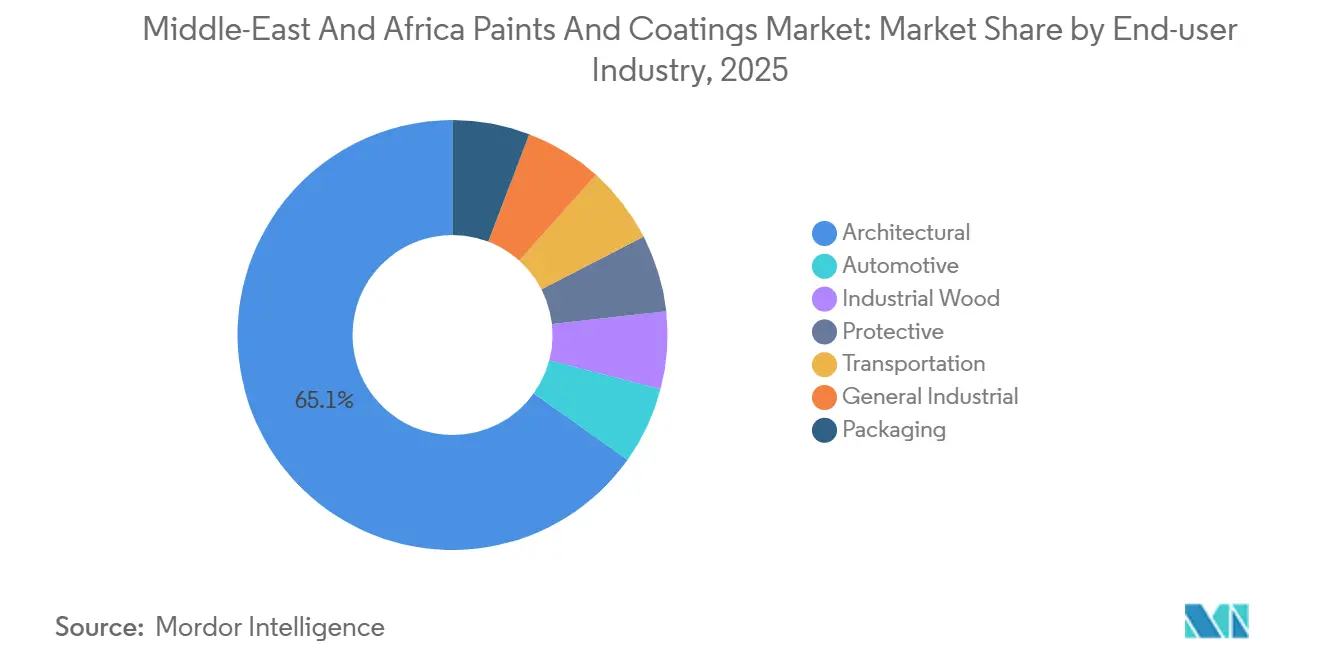

- By end-user industry, architectural applications captured 65.12% of the revenue in 2025 and presented the strongest growth outlook of 4.21% from 2026 to 2031.

- By geography, Turkey led with 25.61% revenue share in 2025; Egypt is projected to compound at a 4.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East And Africa Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public mega-project pipelines (NEOM, Lusail, Expo City) | +1.2% | Saudi Arabia, Qatar, UAE | Medium term (2-4 years) |

| Industrial localisation policies lifting OEM coatings demand | +0.9% | Saudi Arabia, UAE, Morocco, Turkey | Long term (≥ 4 years) |

| Urban housing rebound in key African economies | +0.8% | Egypt, Nigeria, South Africa, Kenya | Short term (≤ 2 years) |

| VOC-compliance push for low-solvent and waterborne systems | +0.6% | GCC (Saudi Arabia, UAE, Qatar, Kuwait), Turkey | Medium term (2-4 years) |

| Heritage-site restoration funding for breathable mineral paints | +0.2% | Egypt, Morocco, Saudi Arabia (Diriyah, Jeddah) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Public Mega-Project Pipelines (NEOM, Lusail, Expo City)

NEOM, Lusail, and Expo City are attracting substantial investments, driving a consistent demand for sophisticated architectural and protective systems. These systems are designed to withstand harsh conditions, such as intense heat and saline winds. With warranties stretching up to 15 years, contractors are placing a premium on suppliers certified under ISO 12944. This trend is steering them towards high-end materials, especially acrylic-silicone and polyurethane hybrids. Furthermore, the Public Investment Fund's focus on local content underscores the importance of R&D conducted within the Kingdom, making it as vital as the bid price. Consequently, many multinational corporations are forming joint ventures in Saudi Arabia to align with these qualification standards.

Industrial Localization Policies Lifting OEM Coatings Demand

Under the Vision 2030 initiative and concurrent agendas from the UAE, Morocco, and Turkey, automakers and appliance OEMs are increasingly being urged to source more domestically. Stellantis has responded decisively, enhancing its Kenitra facility's capacity. This upgrade introduces a RoDip cathodic electrocoat and energy-efficient ovens, signaling a transition to on-site waterborne adoption. Saudi Arabia’s CEER-Dürr plant, set to begin operations this year, is preparing to manufacture electric vehicles on an annual basis. This move not only strategically positions the Kingdom but also guarantees a consistent supply of waterborne basecoats compliant with SASO VOC standards. These localization efforts are not just fortifying long-term offtake agreements but are also integrating coatings engineers into the OEM design processes.

Urban Housing Rebound in Key African Economies

Egypt's social-housing initiative and Nigeria's urgent housing deficit are fueling a rising demand for affordable bulk emulsions and factory-applied powder coatings, particularly on modular steel frames. In South Africa, municipalities are advocating for reflective roof systems to reduce HVAC loads. As a result, suppliers are focusing on diversifying their offerings - emphasizing high-volume, low-margin emulsions for public projects while reserving specialty formulations for the expanding private modular construction market.

VOC-Compliance Push for Low-Solvent and Waterborne Systems

GSO 2764:2024 has set stringent limits on interior VOCs, prompting a swift shift from solvent-borne alkyds to waterborne acrylics and hybrids across the GCC region. Hempel's strategic decision to dedicate its Jeddah plant solely to waterborne lines highlights this industry pivot[1]Hempel, “Saudi Arabia Capacity Expansion,” hempel.com. Distributors who maintain legacy solvent inventories risk significant write-downs unless they transition to protective niches, where higher occupational-exposure limits remain.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-linked raw-material prices | -0.7% | Global, with acute impact on GCC and North Africa | Short term (≤ 2 years) |

| Trade sanctions restricting raw-material inflows into Iran | -0.3% | Iran, Iraq (spillover), Turkey (transit routes) | Medium term (2-4 years) |

| Embodied-carbon reduction shifting budgets to alternative materials | -0.4% | Saudi Arabia, UAE, Qatar (Green Building Code adopters) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Linked Raw-Material Prices

In 2025, spot values for MEK saw a decline. Meanwhile, disruptions in logistics at Jubail led to a tightening of butadiene supplies, which forced formulators to renegotiate prices more frequently. While major regional players are entering into resin joint ventures with SABIC and QAPCO to counter feedstock risks, this strategic move is not accessible to smaller entities.

Trade Sanctions Restricting Raw-Material Inflows into Iran

In July 2025, United States sanctions on Indian traders increased lead times for Iranian additives and raised costs. While Iraqi coaters face challenges in securing financing, Iranian OEMs are constrained by outdated spray booth technology that does not comply with European Union Volatile Organic Compound (VOC) standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Performance Tilt Toward Polyurethane

In 2025, acrylics, lauded for their UV stability and cost-effectiveness in large-scale housing, captured 34.11% of the paints and coatings market across the Middle-East and Africa. While polyurethane claimed a smaller market share, it emerged as the fastest-growing segment, with a 4.31% CAGR extending through the forecast period of 2026–2031. This growth is largely fueled by a surge in demand for protective and automotive clearcoats, especially within Saudi Arabia's petrochemical industry and Morocco's export-driven OEM lines. Alkyds remain the preferred choice for decorative wood applications, though they face regulatory hurdles. In contrast, epoxies are establishing a stronghold in anti-corrosion and tank-lining projects.

BASF's cutting-edge overspray-free OFLA process is a key driver behind the projected growth of the polyurethane segment in the Middle-East and Africa's paints and coatings market[2]BASF, “Overspray-Free Coating Technology,” basf.com. This innovative approach not only boosts material-utilization efficiency but also significantly reduces CO₂ emissions on OEM lines. On another front, silicone and fluoropolymer systems, though representing a smaller share, are tapping into premium markets. Their applications, such as high-temperature pipeline cladding, yield impressive margins for suppliers with specialized expertise.

By Technology: Waterborne Gains Momentum

In 2025, solvent-borne platforms commanded a 48.05% share, highlighting their resilience in arid climates. Waterborne systems, however, are becoming increasingly competitive and are advancing at 4.38% through 2031. This progress is attributed to improved coalescents that address open-time challenges in environments with less than 10% relative humidity. Powder coatings, recognized for their zero VOCs and exceptional corrosion resistance, are gaining applications in EV battery housings, appliance chassis, and architectural extrusions.

As AkzoNobel secures Interpon approvals from major automotive players, the paints and coatings market in the Middle-East is simultaneously experiencing a rise in the adoption of powder technology. This trend underscores the growing confidence of OEMs in electrostatic-spray platforms. Furthermore, UV-cured shares, though still in their early stages, are gaining prominence in the furniture sectors of Egypt and Turkey due to their rapid curing capabilities and reduced energy requirements.

By End-User Industry: Architectural Dominance and Industrial Diversification

In 2025, architectural shares accounted for 65.12% of the market and are growing at a 4.21% CAGR through 2031, driven by Saudi Arabia's ambitious giga-projects and Egypt's focus on social housing. Multi-year maintenance contracts are ensuring stable margins for protective coatings across LNG terminals, marine docks, and onshore pipelines. In a significant industry shift, automotive OEMs in Morocco and Saudi Arabia are transitioning from European-imported coatings to locally formulated waterborne basecoats, which enhances regional value addition.

As Jotun increases its passive fire protection production in Oman annually, the market share for protective applications within the Middle-East and Africa's paints and coatings sector is expected to grow during the forecast period of 2026–2031. In Nigeria, the growing preference for factory-applied powder systems in modular housing is prompting industrial suppliers to expand their offerings beyond decorative portfolios.

Geography Analysis

In 2025, buoyed by robust vehicle exports and substantial investments in post-earthquake reconstruction, Turkey's revenue share surged to 25.61%. Local producers, such as Betek Boya, and multinational formulation centers fuel the market; however, they face pressures from titanium dioxide (TiO₂) costs, predominantly influenced by Chinese imports.

Egypt, with a 4.63% CAGR through 2031, is rapidly rising, propelled by its ambitious housing projects and the towering New Administrative Capital. From 2026 to 2031, these initiatives are set to demand a significant amount of architectural coatings. Jotun’s plant in 10th of Ramadan City, showcasing notable growth in 2024, underscores Egypt's dual role as a primary consumer and a pivotal export hub for East Africa.

The GCC states - Saudi Arabia, UAE, Qatar, and Kuwait - occupy the premium tier, where stringent VOC compliance and mega-project demands inflate per-liter prices. This robust demand is further validated by new facility establishments and regional expansions. In contrast, Iran and Iraq grapple with the fallout of sanctions, contending with additive shortages, prolonged lead times, and an over-reliance on outdated spray-line technology - challenges that dampen their export competitiveness.

Competitive Landscape

The Middle-East and Africa paints and coatings market is moderately fragmented. Jazeera Paints received the Local Content Excellence Award in February 2026, highlighting the increasing significance of in-Kingdom research and development (R&D) and workforce development in Saudi tender evaluations. Opportunities for expansion exist in areas such as renewable-energy infrastructure, cool-roof technologies for cities in Sub-Saharan Africa, and the restoration of heritage sites requiring breathable mineral systems. Additionally, process innovations, such as BASF's OFLA technology, create switching costs and generate environmental credits, further strengthening partnerships with original equipment manufacturers (OEMs).

Middle-East And Africa Paints And Coatings Industry Leaders

Jotun

Akzo Nobel N.V.

PPG Industries Inc.

The Sherwin-Williams Company

National Paints Factories Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BASF SE inaugurated a dispersion production line in Dilovası, Türkiye, which boosts the supply of low-VOC binders to architectural and construction customers across the Middle East and Northwest Africa.

- December 2024: Qemtex commissioned a powder coatings plant in the UAE’s Umm Al Quwain Free Trade Zone with an initial 5,000 t/y capacity, to double to 10,000 t/y in phase two, alongside a EUR 15.2 million research and development center targeting advanced polyester-TGIC grades.

Middle-East And Africa Paints And Coatings Market Report Scope

Paints and coatings are materials, available in liquid or powder form, that are applied to surfaces to form a protective or decorative solid film. They are composed of binders (film-formers), pigments (for color and opacity), solvents (to adjust viscosity), and additives. "Paints" are primarily designed for aesthetic purposes with pigmentation, while "coatings" are formulated for performance, providing features such as corrosion resistance, durability, and specialized functional properties like electrical conductivity.

The coatings market is segmented by resin type, technology, end-user industry, and geography. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and others (including silicone, vinyl, and fluoropolymer). By technology, the market is segmented into water-borne, solvent-borne, powder coating, and UV-cured coating. By end-user industry, the market is segmented into architectural, automotive, industrial wood, protective, transportation, general industrial, and packaging. The report also covers the market size and forecasts for the market in 14 countries across the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Others (Silicone, Vinyl, Fluoropolymer) |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coating |

| UV-cured Coating |

By End-user Industry

| Architectural |

| Automotive |

| Industrial Wood |

| Protective |

| Transportation |

| General Industrial |

| Packaging |

By Geography

| Saudi Arabia |

| Qatar |

| Kuwait |

| United Arab Emirates |

| Iran |

| Iraq |

| Nigeria |

| South Africa |

| Turkey |

| Tanzania |

| Kenya |

| Algeria |

| Morocco |

| Egypt |

| Rest of Middle-East and Africa |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Others (Silicone, Vinyl, Fluoropolymer) | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coating | |

| UV-cured Coating | |

| By End-user Industry | Architectural |

| Automotive | |

| Industrial Wood | |

| Protective | |

| Transportation | |

| General Industrial | |

| Packaging | |

| By Geography | Saudi Arabia |

| Qatar | |

| Kuwait | |

| United Arab Emirates | |

| Iran | |

| Iraq | |

| Nigeria | |

| South Africa | |

| Turkey | |

| Tanzania | |

| Kenya | |

| Algeria | |

| Morocco | |

| Egypt | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

What is the projected value of the Middle-East and Africa paints and coatings market by 2031?

The Middle-East and Africa Paints and Coatings Market size is projected to be USD 9.26 billion in 2025, USD 9.64 billion in 2026, and reach USD 11.80 billion by 2031, growing at a CAGR of 4.12% from 2026 to 2031.

Which segment currently holds the largest market share?

Architectural coatings lead with a 65.12% share in 2025, fueled by giga-projects and social-housing programs.

Which resin category is expanding the fastest?

Polyurethane is growing at a 4.31% CAGR through 2031, driven by protective and automotive clearcoat demand.

How are VOC regulations influencing technology adoption?

GSO 2764:2024 caps VOCs at 50 g/L for interiors, accelerating the shift from solvent-borne to waterborne and powder systems across GCC markets.

Which country is expected to grow the quickest?

Egypt is set to record the fastest 4.63% CAGR through 2031, supported by large-scale housing and commercial projects.

Page last updated on: