Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

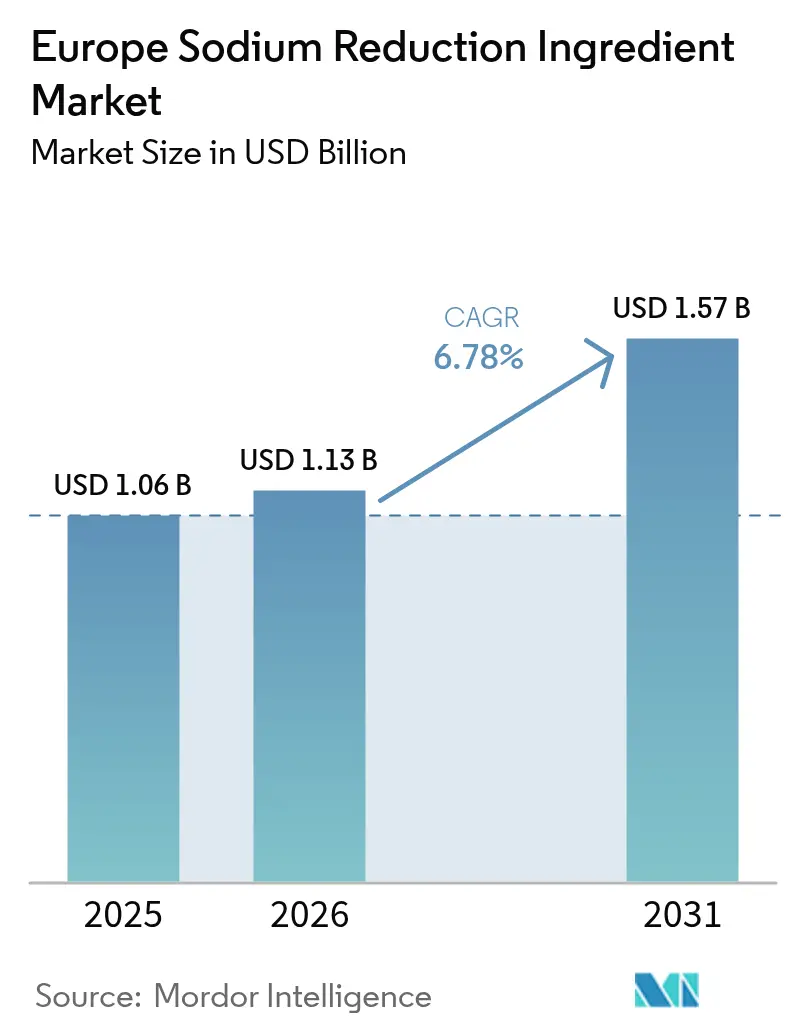

| Base Year Market Size (2025) | USD 1.06 Billion |

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Sodium Reduction Ingredient Market Analysis by Mordor Intelligence

The Europe sodium reduction ingredients market size was valued at USD 1.06 billion in 2025 and estimated to grow from USD 1.13 billion in 2026 to reach USD 1.57 billion by 2031, at a CAGR of 6.78% during the forecast period (2026-2031). Stricter regional nutrition policies, rapid clean-label reformulation, and advancing salt-replacement technologies are driving food manufacturers to achieve significant sodium reductions without sacrificing flavor, texture, or shelf-life. Key innovations, such as mineral-salt solutions, potassium lactate blends, and a diverse range of umami-rich yeast extracts, are propelling this shift across categories like bakery, meat, sauces, and snacks. The United Kingdom is at the forefront, largely due to its High Fat, Sugar and Salt (HFSS) regulations. Meanwhile, Germany, France, Italy, and Spain are adopting similar measures through Nutri-Score labeling, which penalizes high-sodium recipes. In Eastern Europe, as convenience products see volume growth, there's a notable reliance on cost-effective potassium-chloride blends. This trend highlights a growing divide: premium demand in the West versus price sensitivity in the East. On the supply side, innovations like AI-driven taste design, systems that enhance both shelf-life and flavor, and microcrystal salt advancements are not only differentiating competitors but also speeding up reformulation processes.

Key Report Takeaways

- By product type, mineral salts held 65.72% of Europe sodium reduction ingredients market share in 2025 and will expand at a 5.76% CAGR through 2031.

- By product type, yeast extracts are set to post the fastest 9.04% CAGR between 2026-2031 across Europe.

- By form, powders and granules commanded a 61.60% share of the Europe sodium reduction ingredients market size in 2025, while liquids are projected to grow at 6.98% CAGR.

- By application, meat products captured 38.10% share of the Europe sodium reduction ingredients market in 2025; sauces and seasonings are forecast to rise at 8.33% CAGR.

- By geography, the United Kingdom controlled 24.20% of Europe sodium reduction ingredients market share in 2025 and is on track for a 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Sodium Reduction Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU salt-reduction frameworks, United Kingdom HFSS, and Nutri-Score adoption intensify reformulation | 1.8% | United Kingdom, France, Germany, Belgium, Netherlands | Short term (≤ 2 years) |

| Clean-label umami and yeast-extract systems enabling deeper sodium cuts without taste loss | 1.5% | Western Europe (United Kingdom, Germany, France, Italy, Spain) | Medium term (2-4 years) |

| Rising processed and convenience food penetration in Eastern Europe | 1.2% | Poland, Russia, Rest of Eastern Europe | Medium term (2-4 years) |

| Supplier portfolios bundling shelf-life (lactates/acetates) with taste to de-risk reformulation | 0.9% | Global, with concentration in Germany, United Kingdom, Netherlands | Medium term (2-4 years) |

| AI-driven taste design and predictive formulation accelerating time-to-compliance | 0.7% | Western Europe (United Kingdom, Germany, Netherlands) | Long term (≥ 4 years) |

| Microcrystal/microsphere salt technologies enabling non-KCl paths to high reductions | 0.6% | United Kingdom, Germany, France, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU salt-reduction frameworks, UK HFSS, and Nutri-Score adoption intensify reformulation

In the UK, mandatory HFSS regulations, coupled with a unified Nutri-Score labeling system in France, Germany, Belgium, the Netherlands, and Spain, have significantly narrowed the window for product reformulation[1]Source: European Commission, " Food information to consumers - legislation", food.ec.europa.eu. These regulations aim to promote healthier food choices by encouraging manufacturers to improve the nutritional profiles of their products. Retail incentives now prioritize low-sodium SKUs, driving both private-label and branded companies to accelerate their compliance projects to align with these evolving standards. This shift not only ensures regulatory adherence but also enhances their market positioning by catering to the increasing consumer demand for healthier options. Notably, Germany’s Ministry of Food and Agriculture reported that 60% of reformulated products achieved a one-grade improvement in their Nutri-Score, primarily by eliminating sodium. This underscores the critical role of sodium reduction as a key strategy for meeting regulatory requirements and addressing public health concerns.

Clean-label umami and yeast-extract systems enabling deeper sodium cuts without taste loss

Yeast extracts, abundant in glutamate and nucleotide enhancers, elevate the perception of savoriness. This enhancement enables a sodium reduction of 30-40% without introducing metallic undertones, making them a preferred choice for health-conscious consumers and food manufacturers aiming to meet regulatory sodium limits. Ohly-K and Biospringer have recently unveiled products that sidestep "E-number" labels, a feature that aligns with the growing demand for clean-label ingredients and has garnered approval from Western European consumers. Meanwhile, Angel Yeast has positioned its non-GMO capabilities at its Hungarian facility, bringing it nearer to Central Europe and streamlining supply chains, which is expected to improve delivery efficiency and reduce logistical complexities for regional manufacturers.

Rising processed and convenience food penetration in Eastern Europe

In 2024, Poland's packaged food market reached a significant milestone, driven by robust annual growth. This surge is largely attributed to urbanization and the rise of dual-income households, which have significantly increased the demand for convenient food options such as ready meals, processed meats, and shelf-stable sauces. However, the price-sensitive nature of Eastern Europe continues to limit the adoption of premium yeast extracts, as consumers prioritize affordability over premium offerings. Notably, KCl-based mineral blends dominate the sodium-reduction ingredient sales, claiming 75% in Poland and Russia, a stark contrast to the 55% share in Western Europe. Suppliers are addressing this disparity by adopting tiered portfolios: Kerry Group's "Essential" line rolls out cost-optimized KCl blends specifically designed for Eastern markets, catering to the demand for affordable solutions. Meanwhile, its "Taste & Nutrition" premium range targets the clean-label segments of Western Europe, where consumers are more inclined to pay a premium for high-quality, health-focused products. This strategic segmentation effectively aligns product offerings with varying consumer preferences and willingness to pay across regions.

Supplier portfolios bundling shelf-life (lactates/acetates) with taste to de-risk reformulation

Plant trials in 2024 reveal that mid-tier processors have halved their time-to-market by adopting Corbion's Verdad N-series and Jungbunzlauer's SaltWise. These innovations blend potassium lactate, calcium lactate, and yeast extracts, offering a solution that not only achieves a 40% reduction in sodium but also ensures product quality and safety by maintaining a 21-day refrigerated shelf life. This development addresses growing consumer demand for healthier food options without compromising shelf stability, production efficiency, or taste. Furthermore, the use of these advanced ingredient combinations supports manufacturers in optimizing their production processes, reducing formulation complexities, and aligning with evolving regulatory standards and market trends focused on sodium reduction and clean-label solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| KCl off-notes and consumer acceptance hurdles at >25-30% sodium cuts | -1.2% | Global, with higher sensitivity in Southern Europe (Italy, Spain) | Short term (≤ 2 years) |

| Functional trade-offs in bread/meat (structure, water activity, microbiology) | -0.9% | Western Europe (Germany, UK, France, Netherlands) | Medium term (2-4 years) |

| KCl supply-price volatility and logistics constraints post-Belarus/Russia sanctions | -0.7% | EU-wide, with acute impact in Eastern Europe | Short term (≤ 2 years) |

| Potassium-label sensitivity for CKD populations limiting KCl-based solutions | -0.5% | Northern Europe (Germany, Netherlands, Sweden) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

KCl off-notes and consumer acceptance hurdles at >25–30% sodium cuts

Across 15 European nations, sensory panels conducted extensive evaluations to determine the bitterness onset associated with potassium chloride (KCl) substitution in food products. The findings revealed that bitterness became noticeable when KCl substitution reached 25-30%. Among the participants, Italian and Spanish tasters demonstrated the lowest tolerance levels for the bitterness, indicating significant regional differences in taste preferences. Furthermore, the retail performance of high-KCl stock-keeping units (SKUs) reflected these sensory challenges. Within six months of their market launch, sales for these products experienced a decline of up to 18%, highlighting the potential impact of consumer taste perception on product acceptance and market performance.

Functional trade-offs in bread/meat (structure, water activity, microbiology)

German bakery trials observed a significant impact on product quality when sodium content was reduced by 35% without the addition of compensatory hydrocolloids[2]Source: German Baker's Confederation, "Positive Trendwende bestätigt: Zahl der Auszubildenden steigt", baeckerhandwerk.de. Specifically, the trials recorded a 20% reduction in loaf volume, highlighting the critical role sodium plays in maintaining gluten network strength, dough elasticity, and overall product structure. Sodium reduction weakens the gluten network and lowers the ionic strength, which directly affects the bread's ability to retain gas during baking, leading to reduced loaf volume. Similarly, UK ham processors faced challenges in maintaining product integrity when sodium reductions exceeded 35%. To address the resulting purge loss, they had to incorporate phosphates, which helped retain moisture, improve water-binding capacity, and stabilize the product. These findings underscore the importance of carefully managing sodium reductions in food formulations to avoid compromising product quality, texture, and performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mineral Salts Anchor Cost-Efficiency, Yeast Extracts Lead Innovation

In 2025, mineral salts dominated the European sodium reduction ingredients market, capturing 65.72% of total revenues. This stronghold is largely attributed to the prevalent use of potassium chloride, bolstered by EU-wide endorsements and a competitive price range of EUR 1.20–1.50 per kilogram. Mid-tier manufacturers in Germany and France are increasingly adopting blends of calcium chloride and magnesium sulphate. This shift aims to optimize taste while minimizing potassium disclosures, catering to consumers sensitive to chronic kidney disease (CKD). Furthermore, hybrid microcrystal systems are emerging as a holistic solution, seamlessly integrating taste, texture, and regulatory adherence into a singular ingredient platform.

Yeast extracts are the segment witnessing the most rapid expansion, boasting a robust 9.04% CAGR projected through 2031. This surge is largely driven by Western European food processors' growing inclination towards clean-label solutions that naturally enhance umami and flavor. With revenues anticipated to eclipse USD 320 million by 2031, yeast extracts are swiftly carving out a significant market presence, despite their modest starting point. The segment's innovation is largely propelled by patents emphasizing in-situ fermentation and microencapsulation technologies. These advancements not only elevate functionality beyond mere sodium replacement but also bolster the product's standing in the realm of natural formulations.

By Form: Powder Dominance Meets Liquid Precision

In 2025, powder and granule formats dominated the European sodium reduction ingredients market, seizing 61.60% of the total demand. Their stronghold is bolstered by widespread use in bakery, snack, and dry application segments, all of which benefit from the properties of free-flowing salts and spray-dried yeast extracts. These formats are favored by processors due to their stability in low-moisture environments and compatibility with standard mixing systems, which streamline production processes and ensure consistent product quality. Projections indicate that by 2031, the market size for the powder segment could approach nearly USD 995 million, underscoring its enduring commercial significance and its critical role in meeting the growing demand for sodium reduction solutions across various industries.

Liquid formats, while constituting about a quarter of market revenues, are emerging as the fastest-growing segment, boasting a 6.98% CAGR. Their rising adoption in meat, sauce, and gravy production is attributed to in-line dosing, which effectively reduces dust generation and mitigates cross-contamination risks. Liquid yeast extracts offer efficient dispersion in high-moisture formulations, ensuring uniform flavor distribution, while potassium lactate blends not only enhance flavor but also provide antimicrobial benefits, extending product shelf life. Moreover, advancements in dosing technologies, particularly AI-assisted injection systems, are propelling their adoption by guaranteeing accurate sodium reduction, improving operational efficiency, and maintaining process consistency. These innovations are expected to further drive the growth of liquid formats in the coming years.

By Application: Meat’s Structural Challenge versus Sauces’ Flavor Flexibility

In 2025, meat and its products dominated the European sodium reduction ingredients market, accounting for 38.10% of total revenues. This segment's leading position is attributed to its high processing volumes and the stringent microbial safety standards it upholds, underscoring the need for dependable sodium reduction solutions. The meat industry faces unique challenges, such as maintaining flavor profiles and ensuring food safety, which makes sodium reduction a critical focus area. While functional limitations restrict deeper sodium reductions, the meat sector remains a focal point for ingredient suppliers aiming for high-volume reformulations. Here, potassium lactate blends and mineral salt mixes are widely adopted, striking a balance between taste preservation and pathogen control. These solutions not only address regulatory requirements but also cater to evolving consumer preferences for healthier processed meat products.

Sauces, seasonings, and condiments are set to experience the most rapid growth, projected at an 8.33% CAGR through 2031. This surge is largely fueled by yeast extracts, which provide a pronounced umami boost, adeptly masking the off-notes of potassium chloride in tomato and soy formulations. The segment's growth is further supported by its adaptability to various culinary applications, ranging from ready-to-eat meals to packaged condiments. By 2031, the segment's market share is anticipated to surpass 25.40%, bolstered by increasing clean-label demands and their seamless integration with liquid dosing systems. This swift ascent positions sauces as a pivotal growth driver in the overarching trend of processed food reformulation, as manufacturers increasingly prioritize healthier and more natural ingredient profiles to meet consumer expectations.

Geography Analysis

In 2025, the United Kingdom led the pack with a 24.20% market share, projecting a robust 7.18% CAGR. This growth is fueled by stringent HFSS promotion restrictions and private-label sodium ceilings that surpass official targets. These measures aim to address public health concerns by reducing high-fat, salt, and sugar content in food products, thereby driving demand for healthier alternatives. Germany, holding an approximate 18.70% share, is set to expand at a 6.62% CAGR. This is driven by Nutri-Score labels now gracing over 70% of grocery shelves, which influence consumer purchasing decisions by providing clear nutritional information. Additionally, federal mandates for a 20% salt reduction in bakery, meat, and cheese products by 2028 are pushing manufacturers to reformulate their products. France, with a roughly 14.80% market share, is on a 6.32% growth trajectory, bolstered by mandatory Nutri-Score labels and adherence to PNNS benchmarks, which are part of the country’s broader public health strategy to improve dietary habits.

Italy and Spain command a combined 16-18% market share, but their growth lags at a 6.02% CAGR. This slowdown is attributed to PDO regulations limiting KCl usage in their renowned cured meats and cheeses, which are integral to their culinary heritage. These restrictions pose challenges for manufacturers attempting to reduce sodium content while maintaining traditional flavors. Meanwhile, Eastern European nations like Russia, Poland, the Czech Republic, and Hungary are witnessing a surge in supply volumes. Russia, boasting a share of up to 10%, faces a constrained CAGR of 5.37% due to rising KCl costs from Belarus potash sanctions, which have disrupted supply chains and increased production costs. Poland's 6.78% growth is buoyed by a 5.2% annual uptick in packaged foods, reflecting growing consumer demand for convenience products. Its advantageous proximity to Angel Yeast’s hub in Hungary further supports growth by streamlining yeast-extract logistics and reducing transportation costs. Not to be overlooked, Sweden and the Netherlands, though smaller markets, are outpacing with growth rates exceeding 7% CAGR. This is driven by heightened procurement standards from retailers and institutions, which prioritize low-sodium and health-conscious products to meet evolving consumer preferences.

Even with EU Regulation 1169/2011 standardizing nutrition labeling, regional taste preferences diverge. Northern consumers are amenable to a 30% KCl replacement, as they are more accustomed to reduced-sodium products. In contrast, those in the Mediterranean region detect bitterness beyond the 20-25% threshold, making it challenging to implement higher KCl levels without compromising taste. The post-Brexit landscape necessitates dual-compliance strategies, as manufacturers must adhere to both UK and EU regulations. However, many UK-compliant low-sodium recipes transition effortlessly to EU markets, given the more stringent thresholds set by the UK. This alignment allows manufacturers to streamline product development while catering to both markets effectively.

Competitive Landscape

In the European sodium reduction ingredients market, a moderate concentration is evident. The top five suppliers - Cargill, Kerry Group, Tate & Lyle, dsm-firmenich, and Corbion - collectively account for about 50% of the market's revenue. These industry leaders are actively pursuing vertical integration, aiming to bolster their fermentation capacities and enhance their flavor-masking expertise. Between 2022 and 2024, Kerry Group expanded its footprint by acquiring three yeast plants. In a strategic move, dsm-firmenich merged in 2023, consolidating enzymes and taste modulation capabilities. Meanwhile, Tate & Lyle is intensifying its focus on microencapsulation patents, allowing for enhanced saltiness perception with reduced dosages.

The market also boasts a dynamic second tier. Players like Ohly, Biospringer, and Angel Yeast are making strides in the yeast-extract domain, while K+S Minerals and Brenntag are key players in mineral-salt distribution. Disruptors such as MicroSalt and Salt of the Earth are capitalizing on their proprietary microcrystal intellectual property, achieving price premiums of 40-50% in the premium snack segment. The competitive landscape is increasingly influenced by AI-driven data assets. Notably, companies like Symrise and Givaudan are investing between EUR 10-20 million annually into machine-learning platforms, honing in on forecasting sensory acceptance tailored to regional taste preferences. Furthermore, certifications like ISO 22000 and FSSC 22000 have become essential, serving as baseline requirements for securing supply contracts with multinational corporations.

Recent patent filings highlight a trend towards hybrid mineral-yeast systems and innovative controlled-release salt particles. To expand their market reach without incurring capital expenditures on sales infrastructure, tier-two firms are forging partnerships with logistics experts like Brenntag. As processors in Western Europe increasingly emphasize turnkey compliance, suppliers offering bundled services encompassing sodium reduction, shelf-life extension, and labeling support are finding themselves with a tighter grip on customer loyalty.

Europe Sodium Reduction Ingredient Industry Leaders

-

Cargill Incorporated

-

Kerry Group

-

Tate & Lyle PLC

-

dsm-firmenich

-

K+S Minerals and Agriculture GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kerry Group unveiled a EUR 35 million (USD 37.6 million) expansion at its yeast-extract production facility in the Netherlands. This expansion boosts capacity by 40%, addressing the surging demand for clean-label sodium-reduction ingredients in meat and sauce applications throughout Western Europe.

- November 2024: Tate & Lyle introduced SODA-LO Prime, a microencapsulated sodium chloride platform. This innovation facilitates a 50% sodium reduction in bakery products, sidestepping KCl substitution. The focus is on the premium bread and cracker markets in the UK and Germany.

- October 2024: Corbion forged a partnership with a prominent European meat processor. Together, they implemented Corbion's Verdad N-series, a blend of potassium lactate and yeast extract. This collaboration achieved a 40% sodium reduction in cooked ham, all while preserving a 21-day refrigerated shelf-life.

Europe Sodium Reduction Ingredient Market Report Scope

The Europe sodium reduction ingredients market is segmented by product type,application and by geography. Based on product type, the market is segmented into amino acids and glutamates, mineral salts, yeast extracts, and other product types. Based on application, the market is segmented into bakery and confectionery, condiments, seasonings and sauces, dairy and frozen foods, meat and meat products, snacks, and other applications. By Geography, the market is studied for the following countries i.e. Spain, Italy, United Kingdom, Germany, Russia, France and Rest of Europe

By Product Type

| Amino Acids and Glutamates | |

| Mineral Salts | Potassium Chloride |

| Magnesium Sulphate | |

| Potassium Lactate | |

| Calcium Chloride | |

| Yeast Extracts | |

| Others |

By Form

| Powder/Granules |

| Liquid |

By Application

| Bakery and Confectionery |

| Condiments, Seasonings and Sauces |

| Dairy and Frozen Foods |

| Meat and Meat Products |

| Snacks |

| Others |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Amino Acids and Glutamates | |

| Mineral Salts | Potassium Chloride | |

| Magnesium Sulphate | ||

| Potassium Lactate | ||

| Calcium Chloride | ||

| Yeast Extracts | ||

| Others | ||

| By Form | Powder/Granules | |

| Liquid | ||

| By Application | Bakery and Confectionery | |

| Condiments, Seasonings and Sauces | ||

| Dairy and Frozen Foods | ||

| Meat and Meat Products | ||

| Snacks | ||

| Others | ||

| Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of the Europe sodium reduction ingredients market by 2031?

The market is forecast to reach USD 1.57 billion by 2031, growing at a 6.78% CAGR.

Which country leads adoption of sodium reduction ingredients in Europe?

The United Kingdom holds the largest 24.20% share thanks to HFSS legislation and retailer mandates.

Which product type is growing fastest?

Yeast extracts post the highest 9.04% CAGR as clean-label umami systems gain traction.

How do microcrystal salts differ from potassium chloride solutions?

Microcrystal salts deliver 50% sodium cuts without KCl, avoiding bitter off-notes that appear above 25-30% KCl substitution.

Page last updated on: