Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2020 - 2024 |

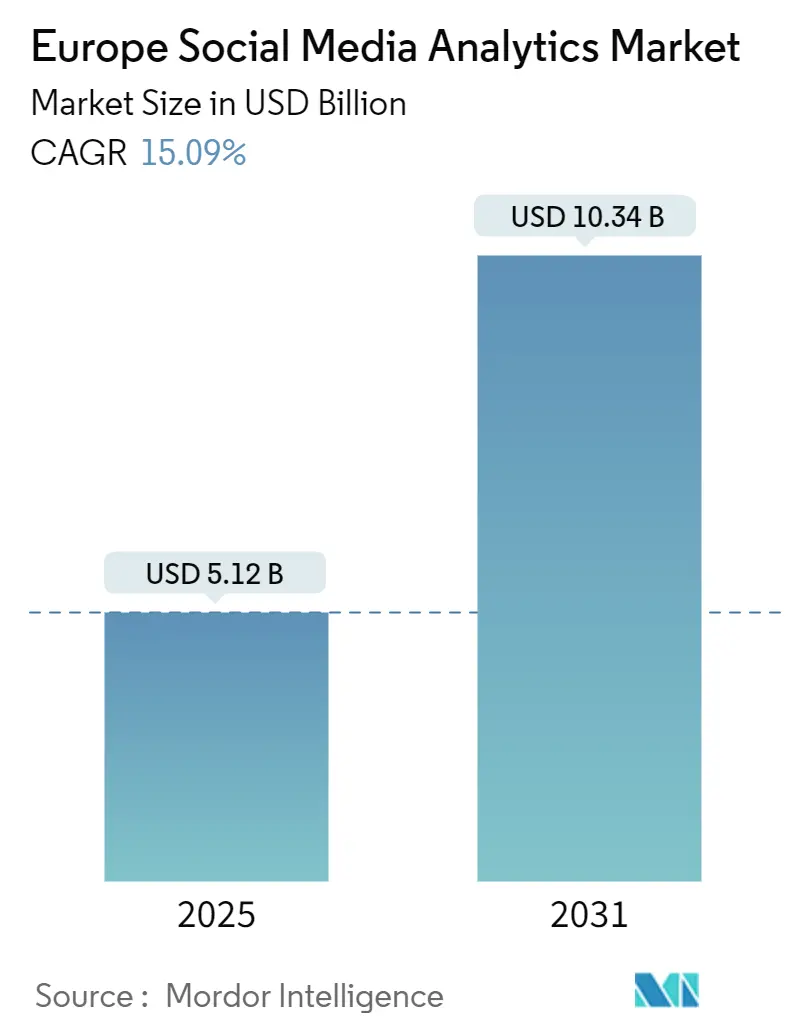

| Market Size (2026) | USD 5.12 Billion |

| Market Size (2031) | USD 10.34 Billion |

| Growth Rate (2025 - 2031) | 15.09% CAGR |

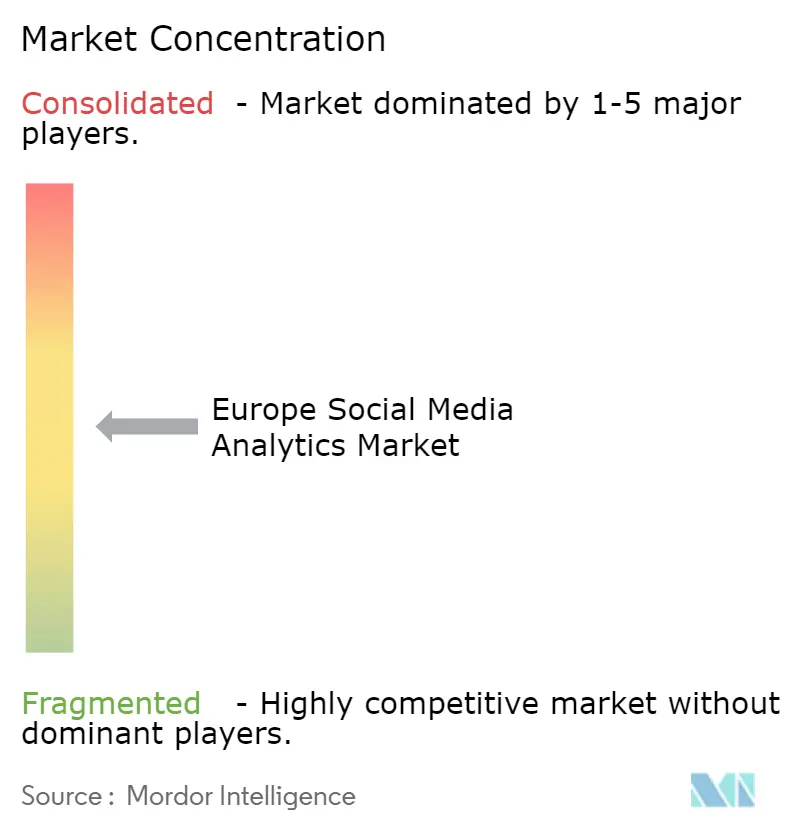

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Social Media Analytics Market Analysis by Mordor Intelligence

The Europe social media analytics market size reached USD 5.12 billion in 2026 and is projected to climb to USD 10.34 billion by 2031, advancing at a 15.09% CAGR through the forecast period. This growth reflects a structural shift from basic metric tracking to predictive sentiment modeling, as European enterprises seek real-time intelligence that aligns with regulatory disclosure requirements under the Digital Services Act. Surging digital advertising budgets - with social spend hitting EUR 15.394 billion (USD 16.89 billion) in 2024, up 32.8% year-on-year - have intensified demand for tools that link impressions to conversions. Cloud delivery dominates because multilingual natural-language models require elastic compute that small and medium enterprises cannot host on-premise. Competitive intensity is rising as incumbents embed large language models, while data-access constraints at X and Meta push vendors toward alternative sources.

Key Report Takeaways

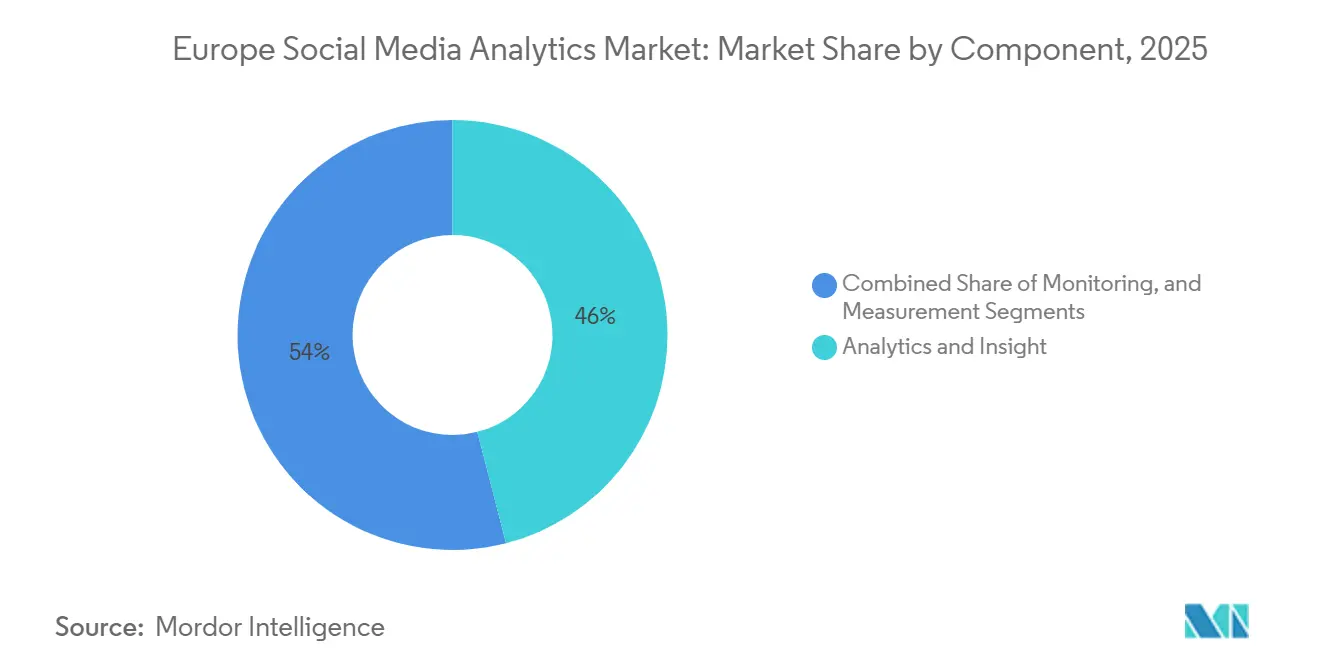

- By component, Analytics and Insight captured 46% of 2025 revenue and is forecast to expand at a 15.87% CAGR through 2031, the highest pace in its segmentation.

- By mode of deployment, cloud accounted for 71% of the 2025 value and will grow at a 16.12% CAGR through 2031.

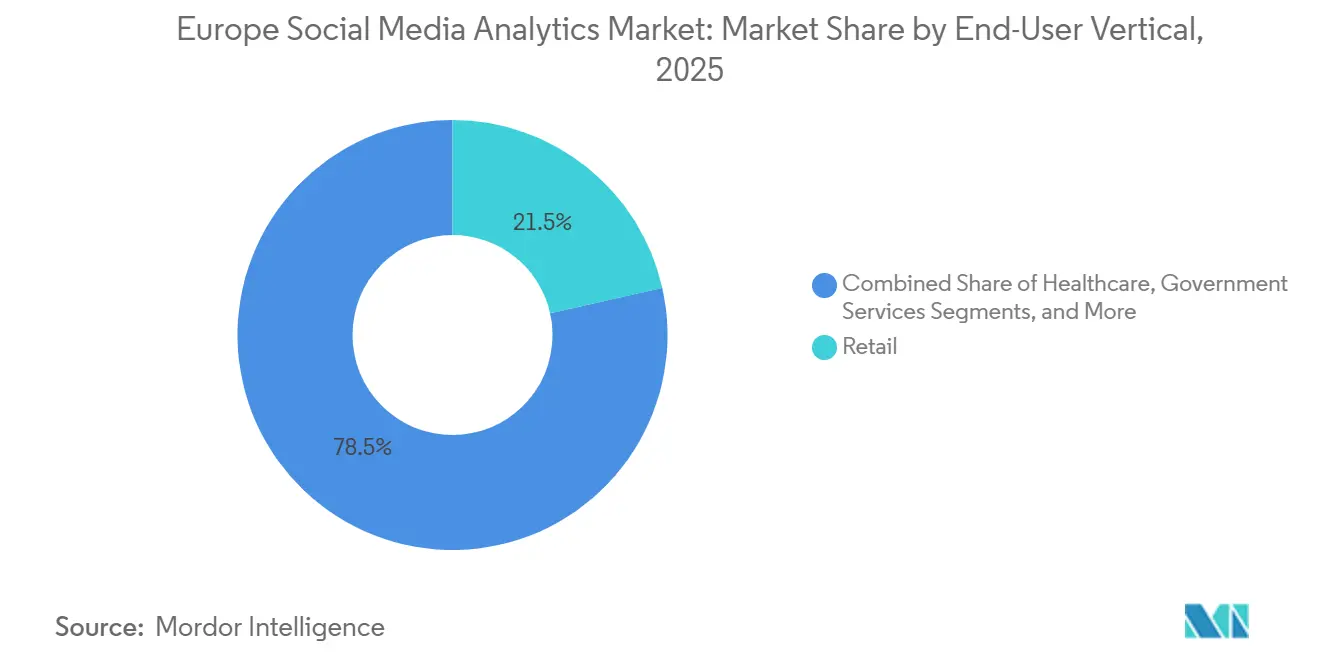

- By end-user vertical, retail held a 21.5% share in 2025, whereas healthcare is projected to grow at a 15.98% CAGR to 2031.

- By organization size, large enterprises commanded 62% of the revenue in 2025, while small and medium enterprises are projected to post the fastest growth rate of a 16.32% CAGR through 2031.

- By country, the United Kingdom led with 28.3% share in 2025; Spain is poised for the quickest 16.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Social Media Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of social-media users across Europe | +2.8% | Pan-European, highest in the United Kingdom, Germany, France | Medium term (2-4 years) |

| Rising adoption of AI-powered customer-insights platforms | +3.2% | United Kingdom, Germany, Netherlands | Short term (≤2 years) |

| Increasing digital ad spending by European enterprises | +2.5% | United Kingdom, Germany, France, Spain | Medium term (2-4 years) |

| Growing demand for real-time consumer-sentiment analysis | +2.1% | Retail and BFSI in United Kingdom, Germany | Short term (≤2 years) |

| Emergence of regulatory mandates for algorithmic transparency | +1.9% | Driven by the Digital Services Act and AI Act | Long term (≥4 years) |

| Localization needs for multilingual sentiment models | +1.6% | Spain, Italy, Belgium, Switzerland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of AI-Powered Customer Insights Platforms

Adobe’s March 2025 integration of IBM watsonx into Adobe Experience Platform let marketers query sentiment in plain language rather than SQL, accelerating insight cycles from weeks to hours.[1]Adobe, “Adobe and IBM Announce watsonx Integration,” adobe.com Salesforce matched the move the same month, launching Marketing Intelligence with 13 prebuilt connectors that fuse paid-social metrics and organic sentiment in a single view. Such releases reposition artificial intelligence from bolt-on feature to system backbone. Vendors now compete on corpus breadth and multilingual accuracy because sentiment classifiers trained largely on English misread nuance in Romance and Germanic languages, a gap underscored by the European Language Equality project.

Increasing Digital Ad Spending by European Enterprises

The AdEx Benchmark Study logged EUR 15.394 billion (USD 16.89 billion) in 2024 social-media ad spend, a 32.8% jump that eclipsed display and search growth. Social video represented 56% of that outlay, reflecting platform algorithms that elevate short-form clips. As a result, brands insist on attribution engines that align impression delivery with downstream sales, while simultaneously meeting Digital Services Act disclosure requirements. Analytics suites that automate compliance reporting therefore shift from optional to mandatory.

Growing Demand for Real-Time Consumer Sentiment Analysis

Retail and banking teams now track live dashboards to contain brand crises within minutes rather than days. Pulsar’s August 2025 report showed a 106% spike in TikTok conversations around “de-influencing,” compelling fast-moving consumer-goods labels to restructure influencer deals mid-campaign. Banks feed sentiment signals into liquidity and fraud models, while pharmaceutical firms parse patient forums for emerging adverse-event signals, a practice validated when 43% of respondents in a June 2025 European Medicines Agency survey said agency social channels aided drug-safety awareness.

Emergence of Regulatory Mandates for Algorithmic Transparency Driving Analytics Demand

The Digital Services Act obliges very large platforms to publish algorithmic-recommendation reports, forcing advertisers to document campaign interactions. The Artificial Intelligence Act classifies certain sentiment applications used in credit or hiring decisions as high-risk, requiring conformity assessments. Analytics vendors now embed audit trails that track each data transformation, turning compliance capability into a product differentiator and raising entry barriers for resource-constrained startups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent GDPR compliance constraints | -1.8% | Germany, France, Belgium | Long term (≥4 years) |

| High implementation costs for advanced analytics tools | -1.5% | SMEs in Southern and Eastern Europe | Medium term (2-4 years) |

| Consumer pushback against perceived surveillance | -0.9% | Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Fragmented data access from platform API restrictions | -1.3% | All markets reliant on X and Meta data | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent GDPR Compliance Constraints

National regulators in Germany, France, and Belgium have issued cumulative fines exceeding EUR 1 billion (USD 1.1 billion) for unlawful profiling since 2018. Platforms must secure explicit consent before processing personal data, yet sentiment analysis often infers demographics from public posts, a practice regulators scrutinize. Cloud providers also face residency mandates that compel local data centers, inflating costs that vendors must pass to customers.

Fragmented Data Access Due to Platform API Restrictions

X set a Basic tier price of USD 100 a month for 10,000 posts and an Enterprise tier at USD 42,000 in February 2024, ending free academic access. Meta shuttered CrowdTangle in August 2024, replacing it with a gated Content Library.[2]Meta, “CrowdTangle Shutdown,” facebook.com These shifts split the market: well-funded firms purchase enterprise licenses, while cash-strapped small and medium-sized enterprises downgrade data depth, slowing adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Insight Modules Outpace Data Collection

Analytics and Insight claimed 46% of 2025 revenue, the top component share of the Europe social media analytics market, and is predicted to post a 15.87% CAGR through 2031. The segment’s momentum stems from enterprises that favor prescriptive outputs over raw dashboards, illustrated by Adobe’s Agent Orchestrator, which automates audience segmentation and testing. Monitoring and Measurement still capture essential feeds, yet open-source stacks like Kafka shrink their value, shifting budgets toward predictive utilities that flag sentiment inflection points in advance.

General Data Protection Regulation pressure reinforces the tilt toward Insight modules because aggregated outputs carry lower legal exposure than user-level logs. Vendors bake anonymization directly into pipelines to satisfy German and French regulators, thereby combining compliance and decision support in a single workflow.

By Mode of Deployment: Cloud Dominates Through Elastic Compute

Cloud deployment generated 71% of 2025 revenue and will expand at a 16.12% CAGR through 2031, eclipsing on-premise alternatives in the Europe social media analytics market. Multilingual natural-language processing models scale compute during campaign surges then idle once traffic recedes, a pattern that favors utility pricing. Small and medium enterprises, the fastest-growing customer group, gravitate toward operating-expense subscriptions that avoid hardware acquisition.

On-premise installations persist in banking and government due to residency mandates. Financial institutions follow European Central Bank outsourcing guidelines that hold boards liable for data-security lapses even in cloud contracts. Hybrid patterns emerge: raw data remain behind corporate firewalls, while sanitized aggregates move to public clouds for model training.

By End-User Vertical: Healthcare Surges on Patient Sentiment Mining

Retail held 21.5% of 2025 spending, yet healthcare is forecast to be the quickest climber with a 15.98% CAGR through 2031. Pharmaceutical teams combine social listening with adverse-event tracking software to enrich pharmacovigilance, a workflow validated when the European Medicines Agency found a 10-percentage-point rise in YouTube engagement during 2025 drug-safety campaigns. Banking, financial services, and insurance integrate sentiment alerts into credit-risk and fraud systems, sharpening early warnings.

Media and entertainment companies analyze series premieres against audience reaction to time marketing bursts. Government bodies examine public sentiment around policy launches, while utilities monitor outage perceptions to triage service tickets. Emerging users in education, hospitality, and real estate lag in digital maturity but will accelerate as cloud vendors lower entry costs.

By Organization Size: SMEs Accelerate Through Digital Hubs

Large enterprises controlled 62% of 2025 revenue, leveraging dedicated analytics teams and multi-year contracts. Yet small and medium enterprises will log the swiftest 16.32% CAGR, propelled by 228 Digital Innovation Hubs that provide subsidized pilots and training. A Eurofound October 2025 survey showed 73% of European SMEs reached basic digital intensity, marking fertile ground for bundled social-listening and business-intelligence suites.

Software-as-a-service plans with monthly billing resonate with cash-conscious firms, dovetailing with the 71% cloud share. Vendors embed consent management, cutting legal workload for firms that lack privacy officers and bringing advanced capabilities within reach of non-technical teams.

Geography Analysis

The United Kingdom delivered 28.3% of 2025 value, driven by London’s financial-services and media clusters. Spain, however, is set to pace the field with a 16.23% CAGR to 2031, stimulated by the Spain Digital 2026 program that aims for 75% SME digitalization by 2030. Germany and France contribute sizable volumes but face stringent data-protection regimes that shape vendor roadmaps. Italy accelerates under national recovery-and-resilience funds that finance broadband and digital-skills training, expanding the Europe social media analytics market’s addressable base.

Smaller states like Belgium and Switzerland require sentiment engines tuned for multiple official languages, while Nordic countries support English-first deployments but still demand local-language inference for customer care. The European Language Equality strategy to close digital gaps by 2030 will keep localization a central buying criterion.

Regulatory Landscape

The Europe social media analytics market operates under a tightening set of EU-wide rules focused on transparency, lawful processing, and auditable controls over targeting and automated decision-making. The Digital Services Act (Regulation (EU) 2022/2065) sets platform obligations around advertising transparency and recommender-system disclosures for Very Large Online Platforms, which increases documentation requirements for advertisers and analytics vendors that support campaign reporting and verification workflows.

On privacy, GDPR enforcement against unlawful profiling continues to shape how vendors collect, store, and process personal data, pushing the market toward aggregation, anonymization, and consent management features. The European Data Protection Board reinforced these constraints with guidance on targeting social media users and, in July 2026, adopted Guidelines 03/2026 on web scraping in the context of generative AI, emphasizing precise filtering to avoid processing special-category data. That requirement directly constrains social listening pipelines that rely on large-scale public data collection.

Value Chain Analysis

The value chain begins with data origination on social platforms and adjacent public sources (forums, reviews, and messaging communities where permissible), followed by data acquisition through official APIs, licensed feeds, and compliant web collection. In Europe, data acquisition and governance act as gating steps, since vendors must align collection with GDPR requirements (lawful basis, transparency, data minimization, and cross-border transfer mechanisms) and with evolving platform access policies that affect coverage, cost, and continuity.

Downstream, analytics providers transform multilingual content through ingestion, normalization, identity resolution (where permitted), and natural language processing to produce monitoring, measurement, and higher-value analytics and insight outputs. These outputs integrate into customer experience, marketing automation, and risk workflows. Distribution is primarily SaaS and cloud marketplaces, with enterprise deployments adding legal, security, and procurement layers (data processing agreements, residency controls, and auditability). A notable Europe-specific linkage is the DSA Transparency Database (operational since September 2023), which supplies structured signals on moderation actions via Statements of Reasons, while DSA Article 40 creates a regulated path for vetted researcher data access that influences how platforms and analytics stakeholders operationalize data-sharing and compliance processes.

Competitive Landscape

The Europe social media analytics market shows moderate fragmentation. Global suites from Adobe, Oracle, Salesforce, SAP, and IBM compete with European specialists such as Talkwalker, Brandwatch, Meltwater, and Hootsuite. Sprinklr’s February 2024 acquisition of Talkwalker illustrates horizontal consolidation driven by the high cost of training multilingual models across 24 official European Union languages.[3]Sprinklr, “Talkwalker Acquisition Announcement,” sprinklr.com

Three strategic tracks dominate. First, platform vendors integrate sentiment into full customer-experience clouds, cross-selling analytics to marketing-automation users. Second, niche providers specialize in regulated verticals, offering granular audit trails for industries such as pharmaceuticals or banking. Third, regional startups differentiate themselves through native-language coverage and home-region compliance expertise, targeting small and medium-sized enterprises that are often overlooked by global giants.

Data-access friction alters the playing field. X’s steep application-programming-interface fees and Meta’s retirement of CrowdTangle raise entry costs, favoring firms with pre-existing platform contracts. New entrants counter by harvesting alternative data, such as forums, review sites, and messaging apps, and by leveraging generative artificial intelligence for automated insight generation, which reduces customer staffing needs.

Europe Social Media Analytics Industry Leaders

IBM Corporation

SAS Institute Inc.

Clarabridge Inc.

Adobe Systems Incorporated

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven analytics and reporting is a key whitespace area as the Digital Services Act moves transparency from voluntary disclosure to structured obligations. That shift increases demand for tools that map paid and organic activity to ad transparency records, content moderation signals, and audit-ready documentation. A concrete pull-through is the Commission Delegated Regulation (EU) 2025/2050 (July 2025), which sets technical conditions and procedures for VLOPs and VLOSEs to share data with vetted researchers under DSA Article 40, expanding standardized, governed data access. It also creates room for analytics vendors to provide data packaging, governance controls, and reproducible analysis environments that support formal oversight.

A second opportunity is privacy-preserving, multilingual insight generation that reduces reliance on user-level profiling while still meeting enterprise needs for real-time sentiment and attribution. The market is already shifting toward higher-value insight modules (Analytics and Insight held 46% of 2025 revenue) and cloud delivery (71% of 2025 value), leaving space for offerings that combine LLM-assisted querying and automated narratives with data minimization, audit trails, and residency options demanded by regulated buyers. Platform API restrictions and the retirement of legacy transparency tools, including Meta ending CrowdTangle in 2024, also create room for diversified data strategies that blend first-party inputs, public-interest datasets, and compliant third-party sources, reducing single-platform dependence while maintaining European governance standards.

Recent Industry Developments

- July 2026: The European Data Protection Board adopted Guidelines 03/2026 on web scraping in the context of generative AI, emphasizing precise filtering and safeguards to avoid processing special-category personal data. This elevates compliance requirements for social listening pipelines that collect large volumes of public posts and pushes vendors to harden data minimization, redaction, and audit trail capabilities across European deployments.

- September 2025: Adobe launched Experience Platform Agent Orchestrator, adding autonomous agents for audience segmentation and experimentation. The release reinforces the shift from dashboard-centric listening to action-oriented insight automation, raising competitive pressure on analytics suites to deliver faster, explainable outputs aligned with enterprise governance expectations.

- February 2024: X introduced paid API access tiers, including a Basic plan priced at USD 100 per month for 10,000 posts and an Enterprise tier priced at USD 42,000 per month, tightening access conditions for large-scale data collection. Higher data costs and stricter access terms increased the advantage of vendors with existing platform contracts and accelerated diversification toward alternative sources and hybrid data acquisition strategies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software and related services used by organizations in Europe to collect, monitor, measure, and analyze social media data so they can generate insights such as sentiment, trends, campaign performance, and brand health.

Scope exclusions: This sizing excludes social media advertising spend, standalone social media management tools that do not provide analytics, and pure data-reselling without an analytics layer.

Segmentation Overview

- By Component

- Monitoring

- Measurement

- Analytics and Insight

- By Mode of Deployment

- On-Premise

- Cloud

- By End-user Vertical

- Banking, Financial Services and Insurance (BFSI)

- Information Technology and Telecommunication

- Retail

- Healthcare

- Government Services

- Media and Entertainment

- Utilities

- Transportation and Logistics

- Other End-user Verticals

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what gets counted, and to anchor the model with public signals that can be checked country by country. We referred to sources such as Eurostat for digital economy indicators, the European Commission for regulatory context (including Digital Services Act related items), and OECD datasets to understand enterprise digital adoption patterns across Europe.

To keep demand logic realistic, we also reviewed non-paywalled references such as IAB Europe publications on digital marketing activity, ITU and national telecom regulator releases for connectivity and usage context, and peer-reviewed journals covering social listening and NLP adoption. Company filings, investor presentations, product documentation, and reputable press were used to understand packaging, pricing logic, and common deployment patterns. Select paid database subscriptions were used only for company financials, news checks, and patent trend scans linked to analytics and language processing. These desk sources are illustrative, and other references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary interviews focused on validating what is actually purchased in Europe and how budgets are split between software subscriptions, services, and adjacent tools. We spoke with a mix of solution providers, implementation partners, and enterprise users across major European economies, then used follow-up outreach to confirm key assumptions such as cloud adoption, typical contract sizes, and usage intensity by vertical.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 21% | |

| Mid tier: 50% | Functional/Unit leaders: 26% | |

| Smaller Players: 22% | Managers: 53% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where Europe enterprise demand pools are reconstructed through digital adoption indicators, industry-level marketing and customer experience spending intent, and the practical penetration of social listening and analytics use cases. Those totals were then corroborated with selective bottom-up approximations, using sampled vendor revenue splits where available, channel checks with partners, and price-per-seat or price-per-contract patterns applied to expected user volumes.

Key inputs used in the model included cloud versus on-premise deployment mix, the share of demand coming from regulated industries (such as BFSI and public sector), multilingual coverage requirements across European languages, renewal cycles and seat expansion behavior, and the proportion of analytics bundled inside broader customer experience or marketing suites. When bottom-up signals were incomplete for smaller countries, we used proxy scaling based on comparable digital maturity and enterprise density metrics, then followed with a manual check against interview feedback.

For forecasting, we relied on scenario analysis supported by simple multivariate regression checks, where growth is linked to cloud migration pace, social commerce and digital engagement intensity, and compliance-driven monitoring needs. Assumptions were reviewed with primary respondents so the forecast reflects how budgets are typically planned, rather than only extending historical trends.

Data Validation & Update Cycle

Validation is done in layers so that no single data point dominates the final number. Model outputs are checked against independent signals such as vendor revenue direction, reported enterprise software spending conditions, and observable shifts in cloud deployment preference, and any large variance is investigated before sign-off.

If unusual jumps appear at the country level, we re-check currency timing, deployment mix, and the implied spend per customer, then we re-contact select respondents to confirm what changed. Reports are refreshed annually, with interim updates when material events occur, and a final analyst pass is completed close to delivery so clients receive the latest updated view.

Mordor Intelligence's Europe Social Media Analytics Market Estimate Compared With Other Published Estimates

Published market sizes for Europe social media analytics can look different because the scope line is not drawn the same way, and because firms do not always treat services, bundled suites, and deployment models consistently. Timing also matters since refresh cycles and currency conversion choices can shift the apparent current-year value.

Cloud subscription pricing patterns, renewal behavior in large enterprises, and cross-checks against country-level digital adoption signals are the evidence we used to keep Mordor Intelligence's estimate tied to what organizations in Europe typically buy for monitoring, measurement, and analytics capabilities. Differences usually come from whether adjacent categories are added (like social media management without analytics), whether aggressive adoption scenarios are assumed, and whether multi-country weighting is validated with on-the-ground checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.12 B (2026) | |

| Global Consultancy A | USD 3.66 B (2025) | This estimate appears to use an earlier base year and a shorter forecast window, and it may apply narrower inclusion for services and suite-bundled analytics, which can reduce the counted spend in the current year. |

| Regional Consultancy B | USD 4.89 B (2025) | This figure leans on a broader platform definition that can blend analytics with related social tooling, and it also uses a different pricing and growth assumption set through 2034, which changes the implied current-year run rate. |

The spread across sources is mainly explained by base-year choice, what is counted as analytics versus adjacent tools, and how bundled pricing and services are treated. By keeping inclusions explicit and validating assumptions with repeatable demand signals, the sizing stays easier to trace and update when market conditions shift.

Key Questions Answered in the Report

How fast is the Europe social media analytics market projected to grow?

It is expected to post a 15.09% CAGR, scaling from USD 5.12 billion in 2026 to USD 10.34 billion by 2031.

Which component leads spending in Europe?

Analytics and Insight held 46% of 2025 revenue and is expanding faster than monitoring or measurement modules.

How important is cloud deployment to European buyers?

Cloud commanded 71% of 2025 revenue and benefits from elastic compute that supports multilingual models, driving a 16.12% CAGR through 2031.

Which end-user vertical is the fastest riser?

Healthcare is forecast to grow at 15.98% through 2031 as pharmaceutical firms mine patient sentiment for pharmacovigilance.

What challenges restrain adoption among small firms?

High tool costs and fragmented data-access rules limit uptake, although Digital Innovation Hubs and SaaS pricing are easing barriers.

Page last updated on: