Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

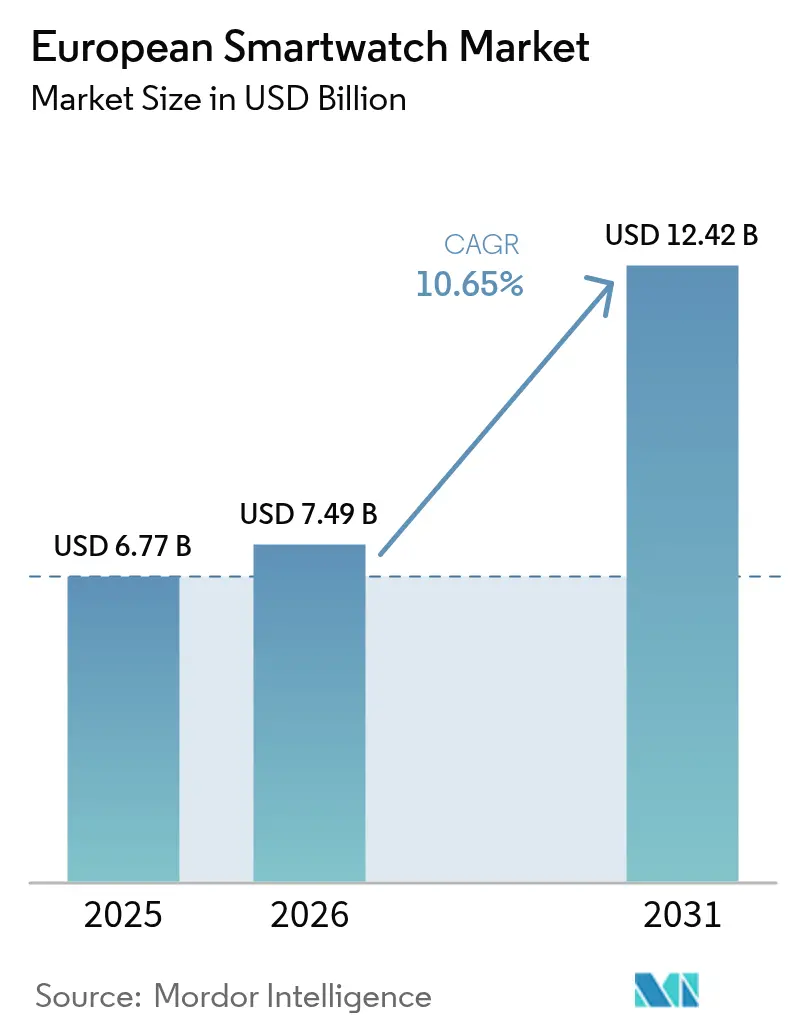

| Base Year Market Size (2025) | USD 6.77 Billion |

| Market Size (2026) | USD 7.49 Billion |

| Market Size (2031) | USD 12.42 Billion |

| Growth Rate (2026 - 2031) | 10.65% CAGR |

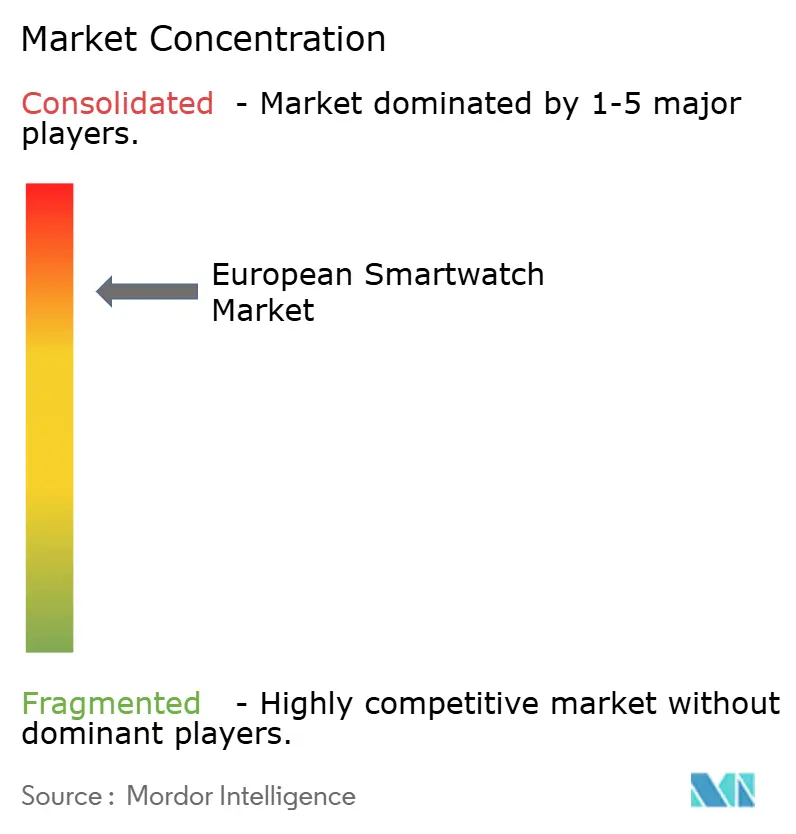

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

European Smartwatch Market Analysis by Mordor Intelligence

The European smartwatche market size in 2026 is estimated at USD 7.49 billion, growing from 2025 value of USD 6.77 billion with 2031 projections showing USD 12.42 billion, growing at 10.65% CAGR over 2026-2031. Growth is propelled by demand for clinical-grade health monitoring, steady LTE/5G roll-outs, and rapid uptake of NFC-based payments. Regulatory clarity on device safety and data privacy underpins consumer confidence, while circular-economy rules encourage premium-segment replacement cycles. Platform providers tighten ecosystem integration to lock in users, and carriers bundle smartwatch connectivity to lift average revenue per user. Manufacturing advances in high-brightness displays and low-power chipsets enlarge the addressable base of seniors, outdoor enthusiasts, and enterprise users.

Key Report Takeaways

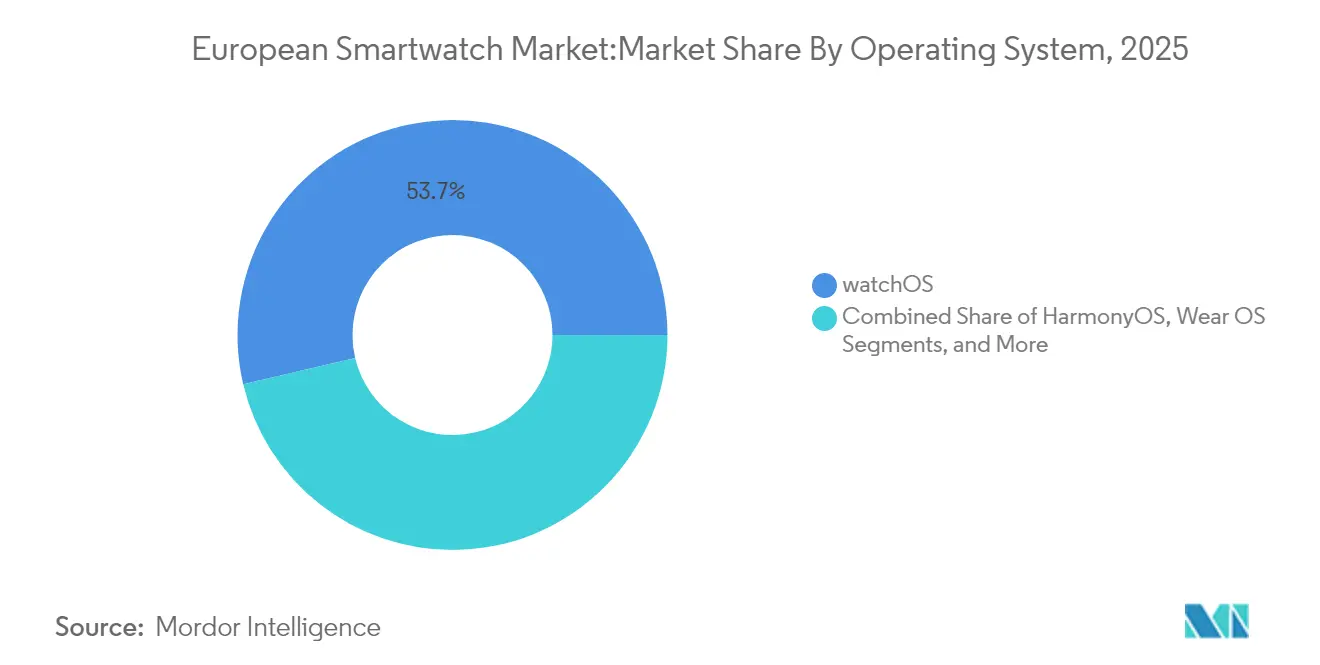

- By operating system, watchOS led with 53.68 of % European smart watches market share in 2025; HarmonyOS is projected to expand at a 17.25% CAGR through 2031.

- By display technology, AMOLED commanded 70.38% of the European smart watches market size in 2025, while Micro-LED displays are forecast to grow at 20.55% CAGR between 2026-2031.

- By application, Fitness and Sports accounted for 36.08% of the European smart watches market size in 2025, whereas Health and Medical is set to advance at 15.62% CAGR to 2031.

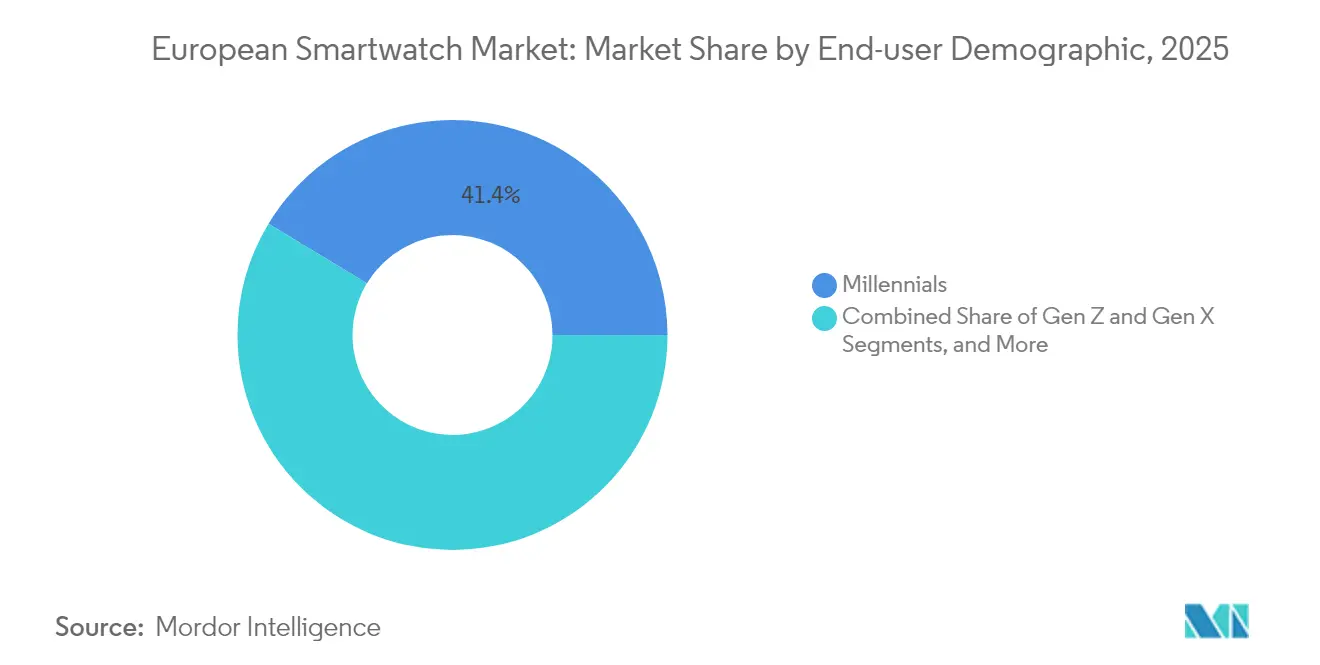

- By end-user demographic, Millennials represented 41.35 of % European smart watches market share in 2025, yet the Seniors segment is poised for 13.02% CAGR through 2031.

- By distribution channel, online sales held 47.62% of the European smart watches market size in 2025; Telco carriers are projected to register an 11.62% CAGR up to 2031.

- By geography, the United Kingdom led with 23.05 of % European smart watches market share in 2025, while Spain is expected to grow at a 10.79% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

European Smartwatch Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of health and fitness monitoring | +3.2% | Nordic countries and Germany | Medium term (2-4 years) |

| Expansion of LTE/5G-enabled standalone watches | +2.8% | UK, Germany, France | Short term (≤ 2 years) |

| Rise of contactless payments via NFC-enabled watches | +2.1% | Western Europe | Medium term (2-4 years) |

| Corporate wellness subsidies for smartwatches | +1.7% | Northern Europe and UK | Long term (≥ 4 years) |

| EU digital-product-passport push for circular electronics | +1.2% | EU-wide implementation, with early adoption in Netherlands and Denmark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Health and Fitness Monitoring

European consumers increasingly view smartwatches as clinical tools, not lifestyle add-ons. The Pixel Watch 3 gained FDA clearance for Loss-of-Pulse detection, setting a precedent for on-wrist medical diagnostics.[1]U.S. Food & Drug Administration, “FDA Permits Marketing of First Watch for Pulse Stoppage Detection,” fda.govSamsung’s BioActive Sensor now includes advanced glycation measurements that flag metabolic risk.[2]Samsung Electronics, “Samsung BioActive Sensor Adds AGEs Index,” news.samsung.com Withings’ ScanWatch Nova extends battery life to 30 days while adding ECG, SpO₂, and temperature sensors. Insurers use these readings to refine risk scoring and reimbursement models, strengthening demand. Hospitals pilot remote-patient-monitoring programs that feed continuous vitals into electronic health records, lowering follow-up visits.

Expansion of LTE/5G-Enabled Standalone Watches

Carrier eSIM activation removes the smartphone tether and positions smartwatches as safety devices for children, seniors, and outdoor athletes. Vodafone’s OneNumber plan at GBP 7.50 per month allows a single data allowance across wrist and phone, driving penetration in the UK and Italy.[3]Vodafone Group, “OneNumber eSIM Service Overview,” vodafone.co.ukManufacturers re-engineer antennas and battery housings to maintain sub-13 mm thickness while meeting 24-hour endurance targets. Independent connectivity underpins fall detection, SOS messaging, and over-the-air diagnostics, widening addressable segments. Carriers benefit from incremental service revenue and lower churn, prompting cross-selling into family plans.

Rise of Contactless Payments via NFC-Enabled Watches

Post-pandemic hygiene concerns and mandatory PIN caps have accelerated wearable payments. Huawei introduced a virtual prepaid Mastercard on its GT-5 series supported by the EU-funded Quicko Wallet, broadening acceptance beyond Apple Pay and Google Wallet.[4]Huawei Technologies, “HarmonyOS Next-Generation Wearable Roadmap,” developer.huawei.com Transparent NFC antennas patented by Meta maintain bezel aesthetics while boosting read ranges, encouraging fashion brands to integrate payments without design compromise. Retailers roll out wrist-optimized POS flows, cutting queue times and boosting average ticket size. Fintech partnerships allow instant issuance of tokenized cards inside watch apps, eliminating plastic and supporting EU sustainability targets.

Corporate Wellness Subsidies for Smartwatches

Enterprises across Denmark, Sweden, and the UK reimburse staff up to EUR 200 on connected wearables that sync with occupational-health dashboards. Peer-benchmark leaderboards increase daily step counts, while continuous HRV tracking pre-empts burnout. Peer-reviewed studies show 15% reductions in musculoskeletal claims when employees hit moderate-intensity-activity goals. Employers negotiate volume discounts with OEMs, helping vendors clear inventory while achieving sticky enterprise contracts. Integrators embed watch data into HR software, automating benefit verification and ROI reporting.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-driven data-privacy concerns | −2.3% | EU-wide, stricter in Germany and France | Short term (≤ 2 years) |

| Margin pressure from mid-/low-tier ASP erosion | −1.8% | Eastern Europe and price-sensitive segments | Medium term (2-4 years) |

| Micro-LED display supply constraints | -1.4% | Global impact, affecting premium segment launches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Data-Privacy Concerns

Smartwatch vendors must appoint EU representatives, conduct algorithm risk assessments, and store sensitive biometric data inside the EEA. Germany’s regulator fined several fitness-app operators in 2025 for inadequate consent workflows, raising awareness among consumers. The forthcoming AI Act classifies on-device predictive health scoring as high risk and mandates human-override options. Compliance raises firmware and legal costs, slowing releases from smaller Asian brands lacking local counsel. Some firms offset by adding on-device processing, reducing cloud uploads, and offering paid data-sovereignty tiers for enterprise clients.

Margin Pressure from Mid-/Low-Tier ASP Erosion

Xiaomi’s sub-EUR 100 models expanded 44% in shipments during Q1 2025, prompting price comparisons that compress margins for incumbents mi.com. Features such as GPS and SpO₂ are now table stakes, eroding once-premium differentiators. Established brands hold volumes through loyalty programs and trade-in credits, but discounting shrinks gross margin pools needed for Micro-LED and glucose-monitoring R&D. Component suppliers consolidate to maintain pricing power, passing cost volatility to OEMs. Western vendors respond by emphasizing longevity, upgrade-able software, and premium materials to justify price gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: HarmonyOS Chips Away at Incumbency

The European smartwatch market logged 53.68% share for watchOS in 2025, translating into the largest installed base of apps and accessories. HarmonyOS, pre-loaded across all new Huawei wearables from 2025, is projected to record a 17.25% CAGR as Chinese expatriate communities and value-seekers migrate to the ecosystem. Wear OS maintains relevance through Samsung’s Galaxy Watch6 and Google’s Pixel Watch 3, anchoring Android phone users who value Google Assistant and access to the Play Store. Sustained competition now hinges on cross-device continuity. Apple syncs medication reminders across watch, phone, and Mac, while Huawei pairs smartwatches with Harmony-powered cars for keyless entry. The European smartwatch market is increasingly rewarding platforms that can localize apps, such as Monese banking or Deezer music, for each language. Compliance updates for GDPR appear to be implemented fastest on watchOS, giving Apple an enterprise edge; however, Huawei offsets this by open-sourcing compliance libraries to local developers.

By Display Technology: Micro-LED Signals the Next Premium Leap

AMOLED held 70.38% of the European smartwatch market size in 2025, owing to mature supply chains and thin form factors. Micro-LED promises double the nits brightness and 30% power savings, supporting sunlight readability at ski resorts and Mediterranean beaches. The technology is forecast to grow at a 20.55% CAGR once backend yields rise and wafer-level mass transfer costs fall.Luxury makers such as TAG Heuer and Montblanc have reserved early Micro-LED batches for USD 1,500-plus SKUs, banking on early-adopter willingness to pay. TFT-LCD survives in sub-EUR 80 price bands and kids’ trackers where battery longevity trumps color depth. The European smartwatch industry may adopt dual-sourcing models, where mid-range lines utilize hybrid OLED backplanes while testing Micro-LED pilots in 2027.

By Application: Health and Medical Rises Toward Parity

Fitness and Sports still delivered 36.08% of the European smartwatch market size in 2025, led by running, cycling, and swimming modes. Health and Medical logs a faster 15.62% CAGR, driven by the clinical validation of ECG, blood pressure trends, and arrhythmia alerts. Hospitals in the Netherlands now prescribe smartwatches for hypertension management, reimbursing patients who transmit fortnightly readings to cardiologists.Payments and Commerce is the dark horse as wrist-based checkout gains trust. NFC readers on public transit in Paris and Berlin recognize tokenized watch wallets, slashing queue times during rush hour. Personal Assistance and Notifications remain steady, but vendors refocus their UX on contextual suggestions, such as inhaler reminders tied to pollen counts, thereby cementing daily utility.

By End-User Demographic: Seniors Accelerate Adoption

Millennials secured 41.35% European smartwatch market share in 2025 by combining health, productivity, and fashion requirements. Seniors, however, deliver the fastest 13.02% CAGR as Europe’s aging population values fall detection and medication reminders through 2031. Battery-life-first designs, such as Withings’ 30-day analog-hybrid dial, address dexterity challenges and charging fatigue.Gen Z prefers bold colors, sustainability stories, and creator collabs. Gen X seeks sleep-apnea screening and calendar glanceability between meetings. Corporate wellness schemes increasingly subsidize senior employees’ devices to curb chronic-care payouts, making employers pivotal channel partners.

By Distribution Channel: Carriers Turn Connectivity Into Retail Muscle

Online pure-play stores captured 47.62 of % European smartwatch market size in 2025 as consumers compared specs and prices at a click. Telco carriers now outpace other channels with an 11.62% CAGR, driven by LTE/5G bundles. Zero-interest financing allows buyers to amortize devices over 24 months, reducing upfront costs.Carrier shops demo on-wrist video calls and remote SIM provisioning, driving attach rates. Consumer-electronics retailers remain strong in Germany thanks to expansive showroom footprints where shoppers test display brightness and strap comfort. Luxury watch and jewelry stores focus on limited editions that align digital functions with Swiss-made craftsmanship.

Geography Analysis

The United Kingdom retained a 23.05% share of the European smartwatch market in 2025, as disposable income and advanced mobile coverage supported the adoption of premium models. Post-Brexit product-safety rules mostly mirror EU norms, avoiding disruption and favoring incumbents with UK warehouses and service centers.Spain leads the growth chart with a 10.79% CAGR through 2031. Aggressive marketing of G-SHOCK and other fashion labels in Madrid and Barcelona pairs streetwear aesthetics with robust water resistance. Germany and France grow steadily on the back of corporate wellness tax incentives, while Italy leans into luxury heritage, blending stainless steel cases with Napa leather straps.Nordic countries collectively showcase near-saturation penetration, yet they sustain replacement cycles through outdoor-specific features, such as ski mode and storm alerts. Eastern Europe absorbs cost-efficient devices, with local e-commerce events such as Poland’s “Hot 12.12” boosting volumes for sub-EUR 60 trackers.

Regulatory Landscape

Smartwatches in Europe sit at the intersection of horizontal product safety, wireless compliance, and data protection, with elevated scrutiny when biometric sensing is marketed as clinical-grade. For connected devices, manufacturers must align with EU cybersecurity and product requirements as the regulatory emphasis shifts from legacy delegated rules under the Radio Equipment Directive toward the Cyber Resilience Act (Regulation (EU) 2024/2847), including vulnerability-handling expectations that start to bite from September 2026 in the CRA framework. Alongside GDPR, this places technical documentation, security-by-design, and EU market-access processes at the center of product roadmaps, particularly for LTE/5G models and health-monitoring features.

Circular-economy rules also shape industrial design choices. The EU Batteries Regulation (Regulation (EU) 2023/1542) introduces expectations on removability and replaceability for portable batteries, and the European Commission clarified in July 2026 (C(2026) 5032 final) that wearable devices such as smartwatches can qualify for derogations where miniaturization or water-ingress protection requirements apply. In parallel, smartwatches and wearable mobile phones are excluded from the ecodesign requirements defined in Regulation (EU) 2023/1670 for smartphones and tablets, which reduces near-term ecodesign-driven redesign risk versus adjacent consumer electronics categories, while keeping pressure on sustainability disclosures and repairability expectations as EU rules evolve.

Value Chain Analysis

The European smartwatch value chain is import-led for finished devices, with most high-volume assembly concentrated in Asia, while European value add is strongest in design and IP, selected specialty components, and premium or niche assembly in countries with established watchmaking and electronics capabilities. Key upstream inputs include application processors and wireless chipsets (Bluetooth, GNSS, LTE/5G), AMOLED and emerging Micro-LED displays, custom lithium-polymer batteries, enclosures and straps, and multi-sensor stacks (optical PPG modules, ECG electrodes, IMUs, microphones, and haptics). Bottlenecks typically center on high-spec optical sensor modules, round AMOLED panels, energy-dense batteries, and combo chipsets, which can extend lead times and constrain premium launches.

Midstream activities cover OS integration (watchOS, Wear OS, HarmonyOS, and proprietary platforms), firmware and companion apps, and compliance engineering across overlapping EU regimes (wireless conformity, cybersecurity expectations, and safety requirements). Partnerships illustrate how component and platform ecosystems pull through to final products. For example, Masimo and Google collaborate on a Wear OS reference platform for device manufacturers, while STMicroelectronics works with Pison and Timex to integrate neural-sensing and gesture-control capabilities on a smartwatch platform. Downstream, distribution spans brand e-commerce, consumer electronics retailers, carrier bundles that monetize eSIM connectivity, and watch and jewelry channels for luxury smartwatches, with aftersales service, warranty handling, and software and security updates increasingly shaping lifecycle cost and brand trust.

Competitive Landscape

Apple’s vertically integrated hardware, software, and services stack anchors a loyal UK and German base, though the vendor trimmed Apple Watch pricing in 2025 to soften share leakage. Huawei positions HarmonyOS as the alternative that spans phones, TVs, and EV dashboards, seeding a self-contained Chinese ecosystem within Europe amid geopolitical tensions.

Samsung leverages its BioActive Sensor and regional telco alliances to sustain Wear OS relevance. Xiaomi scales volume through sub-EUR 100 devices while inching into USD 220 tiers with sapphire glass and LTE. Garmin strengthens its core of endurance athletes by expanding ECG apps across Europe, complementing its reputation for high-accuracy GNSS.

Patent intensity rises. Meta filed transparent antenna designs for thinner bezels, and Citizen embeds solar-charging Eco-Drive modules for months-long autonomy. Supply-chain control differentiates winners: brands able to secure Micro-LED pilot capacity and comply with Digital Product Passport rules will outpace assemblers dependent on third-party compliance audits.

European Smartwatch Industry Leaders

TAG Heuer S.A.

Apple Inc.

Fitbit Inc.

Garmin Ltd

Samsung Electronics Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clinical-grade health monitoring and regulated wellness-to-medical pathways create whitespace for European smartwatch vendors that can substantiate claims and navigate EU conformity requirements. Under the EU Medical Device Regulation (MDR 2017/745), devices that claim diagnosis, monitoring, or treatment of disease can move into medical-device classification, which raises the bar for clinical evaluation and notified-body engagement but can enable deeper integration into care pathways. A visible commercial signal is the market pull for on-wrist medical capabilities reflected in major OEM feature roadmaps, along with the sector precedent of regulated health features, for example Pixel Watch 3 receiving loss-of-pulse detection clearance. This continues to reinforce demand for validated sensing, high-quality algorithms, and robust post-market processes.

Interoperability and secure data exchange with healthcare systems stands out as a differentiator as the European Health Data Space (EHDS) agenda advances. Product strategies that structure patient-generated data using standardized formats such as FHIR, and that document interoperability and compatibility for software and device components, align with emerging expectations for connected health ecosystems. Circular-economy compliance also opens product-design and services opportunities. The July 2026 European Commission clarification on battery-design derogations for wearables reduces forced redesign risk for waterproof and miniaturized watches, while still leaving room for premium trade-in, repair, and refurbished programs that fit EU sustainability direction and carrier financing models.

Recent Industry Developments

- July 2026: The European Commission adopted C(2026) 5032 final, clarifying that wearable devices such as smartwatches may qualify for derogations from end-user portable-battery removability and replaceability requirements where miniaturization or waterproof design constraints apply. This reduces redesign pressure for thin, sealed architectures and helps premium models preserve water-ingress protection while staying aligned with the EU Batteries Regulation compliance track.

- October 2025: TAG Heuer launched the Connected Calibre E5 series and highlighted a shift to a proprietary TAG Heuer OS with Made for iPhone (MFi) positioning. The change emphasizes ecosystem differentiation in the luxury segment and creates a distinct software layer for brands seeking tighter control over performance, UX, and integration with iOS-centric users in Europe.

- April 2024: Masimo and Google announced a partnership to develop a reference platform aimed at helping device manufacturers bring high-performing Wear OS smartwatches to market. The collaboration strengthens the midstream platform and sensor ecosystem, giving OEMs a faster path to integrate advanced health features and shortening development cycles for differentiated Wear OS devices sold across European channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenues from smartwatches sold across Europe, covering wrist-worn devices that run an independent operating system, connect through wireless options, and support app-based functions such as notifications and health tracking.

Scope exclusions: We exclude basic fitness bands and hybrid analog watches that do not run an independent smartwatch operating system.

Segmentation Overview

- By Operating System

- watchOS

- Wear OS (Android)

- HarmonyOS

- Proprietary / Other OS

- By Display Technology

- AMOLED

- Micro-LED

- TFT-LCD / MIP

- By Application

- Personal Assistance and Notifications

- Health and Medical Monitoring

- Fitness and Sports

- Payments and Commerce

- By End-user Demographic

- Gen Z (18-24)

- Millennials (25-40)

- Gen X (41-56)

- Seniors (57+)

- By Distribution Channel

- Online (E-commerce and Brand.com)

- Offline - CE Retail

- Offline - Watch and Jewellery

- Telco Carriers

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Nordics (Sweden, Norway, Denmark, Finland)

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and build the first data spine for the model, especially around device shipments, price positioning, and consumer adoption patterns in Europe. We referenced public sources such as Eurostat for population and income indicators, the European Commission and national telecom regulators for connectivity direction, and UN Comtrade-style trade statistics for import and export signals linked to wearable electronics.

On top of these, we reviewed company annual reports, investor presentations, and official press releases to understand product refresh cycles and reported regional performance comments that can be tied back to demand. A paid subscription covering company financials and news was used selectively to standardize historical disclosures, and a patent database was checked to sense feature focus (for example health and sensor-related filings) that can shift average selling prices over time. The desk sources mentioned here are illustrative only, and we also reviewed other public documents to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work was used to pressure-test shipment and pricing assumptions, and to confirm how demand is behaving by country clusters and key sales routes. We spoke with a mix of brand-side teams, distribution partners, retailers, and industry specialists across Europe, so gaps left by public sources could be filled and key ratios cross-checked before the model was finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 50% | Functional/Unit leaders: 31% | |

| Smaller Players: 17% | Managers: 55% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that reconstructs Europe smartwatch value by linking regional smartwatch shipment direction to an average selling price curve, and then filtering the totals using replacement cycles and attach rates seen in key European countries. To keep the model grounded, we corroborate the outcome with selective bottom-up checks, such as sampling channel pricing, mapping supplier and distributor revenue signals, and using volume and ASP combinations to test whether totals stay realistic.

Inputs that mattered in this market include the smartphone installed base as the practical addressable pool, LTE and eSIM readiness as a proxy for standalone smartwatch demand, replacement cycle behavior, average selling price progression by tier, and the timing of annual product refresh windows that typically shift mix. For forecasting, scenario analysis is used so the base case reflects consensus views from primary respondents on adoption and pricing, and then conservative and aggressive cases are tested around unit growth and ASP drift. Where direct country inputs are thinner, we bridge gaps using cluster-level indicators (income bands and connectivity readiness) and then re-check shares so the final Europe total remains coherent.

Data Validation & Update Cycle

Validation is done in layers so one data point does not dominate the story. We compare model outputs with independent signals such as shipment trend direction, price tier mix movement, and public financial commentary for Europe, and then investigate unusual jumps before sign-off.

A second analyst review is completed to check definitions, currency handling, and the logic behind growth drivers, followed by targeted re-contacts if a key assumption moves outside expected ranges. Reports are refreshed annually, and interim updates are made when a material event changes demand, pricing, or supply outlook. Before delivery, a fresh pass is done so clients receive the latest updated view.

Mordor Intelligence's Europe Smart Watches Market Size Compared Against Other Published Estimates

Published market sizes for Europe smartwatches often do not match because teams use different base years, product boundaries, and price logic, and those choices quickly change the final value number. We keep the estimate tied to observable demand signals and then confirm the logic through interviews, which reduces the risk of counting adjacent device categories.

Key gaps usually come from whether a study counts fitness bands and hybrid watches, whether revenue is treated as factory-gate or retail value, and how average selling prices are moved over time when new models launch. Shipment direction and price tier mix checks, followed by interview confirmation across retail and distribution, are the evidence trail that keeps Mordor Intelligence aligned to smartwatch-only factory-gate revenues rather than a broader wearable total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.77 B (2025) | |

| Global Databook A | USD 9.78 B (2022) | Uses an older base year, and the published cut is strongly organized around price bands, which can leave readers unclear on how factory-gate pricing versus retail pricing was handled across countries and channels. |

| Industry Brief B | USD 8.00 B (2024) | Reported as a rounded value with limited scope notes, so inclusion rules (such as excluding fitness bands and hybrids) and currency timing assumptions are not fully transparent, which can shift the total. |

Across the three figures, the spread is mainly explained by different base years and how clearly smartwatch-only scope and pricing layers are defined. By anchoring the model to shipment and ASP signals and validating the assumptions through primary checks, the final number stays traceable to inputs that can be revisited and repeated each year.

Key Questions Answered in the Report

What is the current value of the Europe smart watches market?

The European smartwatch market is valued at USD 7.49 billion in 2026.

How fast is the market expected to grow?

It is projected to expand at a 10.65% CAGR, reaching USD 12.42 billion by 2031.

Which operating system leads the market?

Apple’s watchOS holds the largest share at 53.68% in 2025.

Which country is the fastest-growing European market?

Spain is forecast to rise at a 10.79% CAGR through 2031.

What feature is driving senior adoption?

Clinical-grade health monitoring, including ECG and fall detection, is the main draw for seniors.

Why are carriers important to future growth?

LTE/5G bundles offered by carriers lower upfront costs and enable standalone connectivity, boosting adoption.

Page last updated on: