Europe Smart Parking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

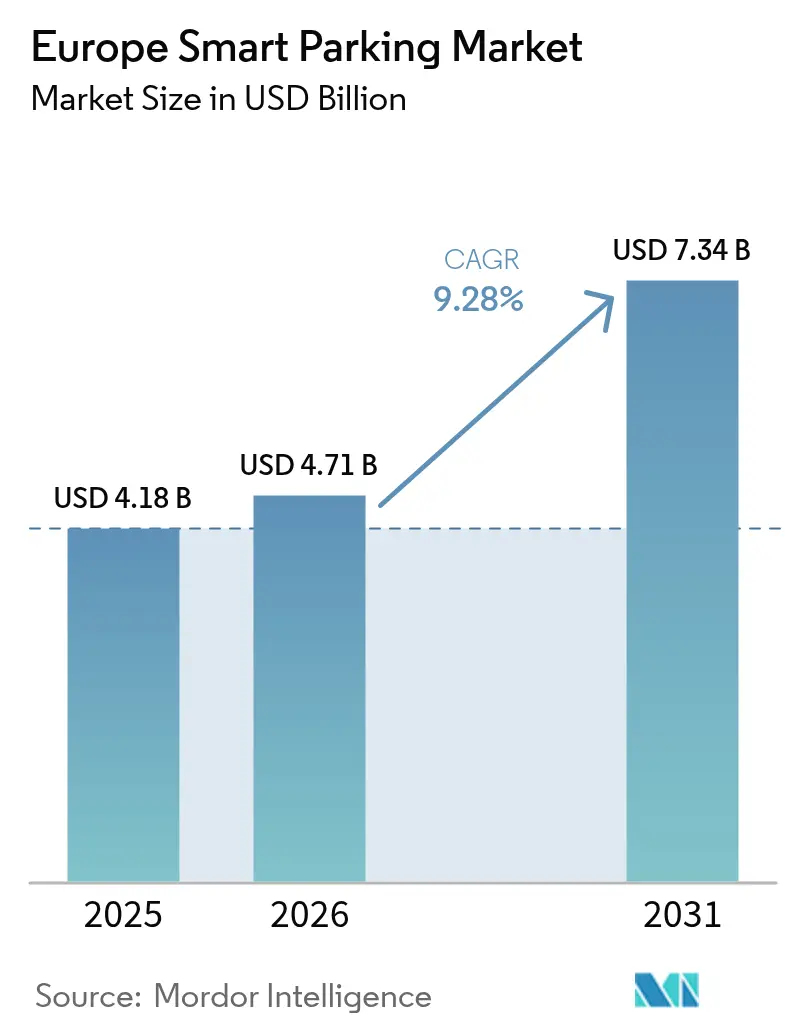

| Base Year Market Size (2025) | USD 4.18 Billion |

| Market Size (2026) | USD 4.71 Billion |

| Market Size (2031) | USD 7.34 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

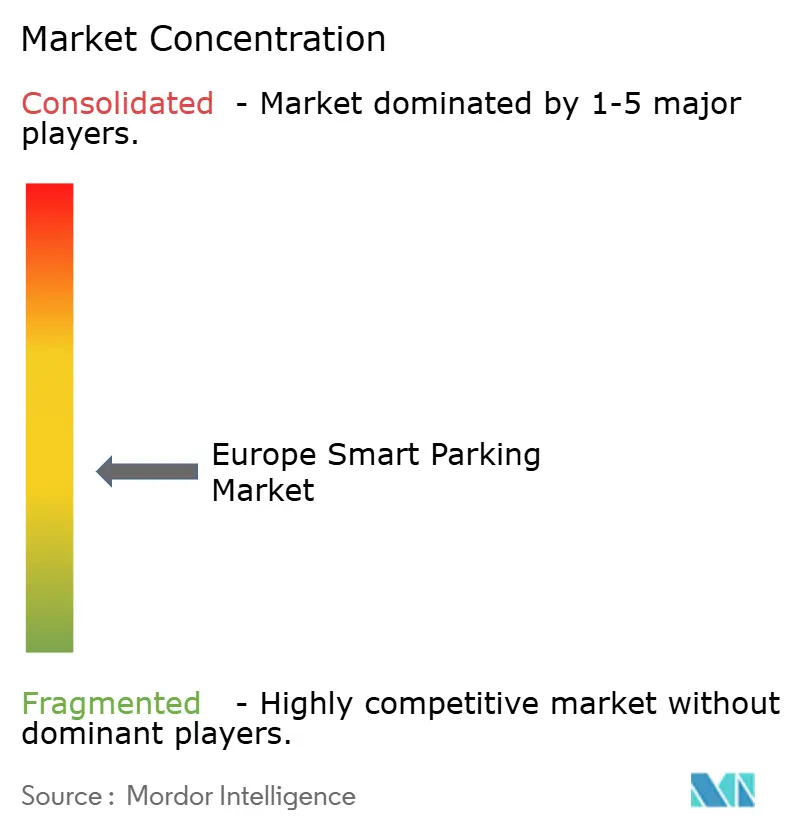

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Smart Parking Market Analysis by Mordor Intelligence

The Europe smart parking market size is projected to be USD 4.18 billion in 2025, USD 4.71 billion in 2026, and reach USD 7.34 billion by 2031, growing at a CAGR of 9.28% from 2026 to 2031. Cities are reframing curb management as a decarbonization and revenue lever, while the revised Intelligent Transport Systems Directive obliges open data sharing across the region. Electric-vehicle (EV) adoption is pushing operators to retrofit bays with charging hardware, and contactless payments have become the default interface for on-street transactions, cutting cash-handling costs. Municipal funding tied to Mobility-as-a-Service (MaaS) pilots is accelerating pilot projects, yet up-front sensor costs and fragmented procurement still slow rollouts in many mid-sized towns. Competitive intensity remains moderate because no firm controls more than 10% share, and software-only entrants are bypassing civil-works barriers to scale rapidly.

Key Report Takeaways

- By solution, software platforms led with 44.91% of Europe smart parking market share in 2025, while managed services are forecast to expand at a 10.14% CAGR to 2031.

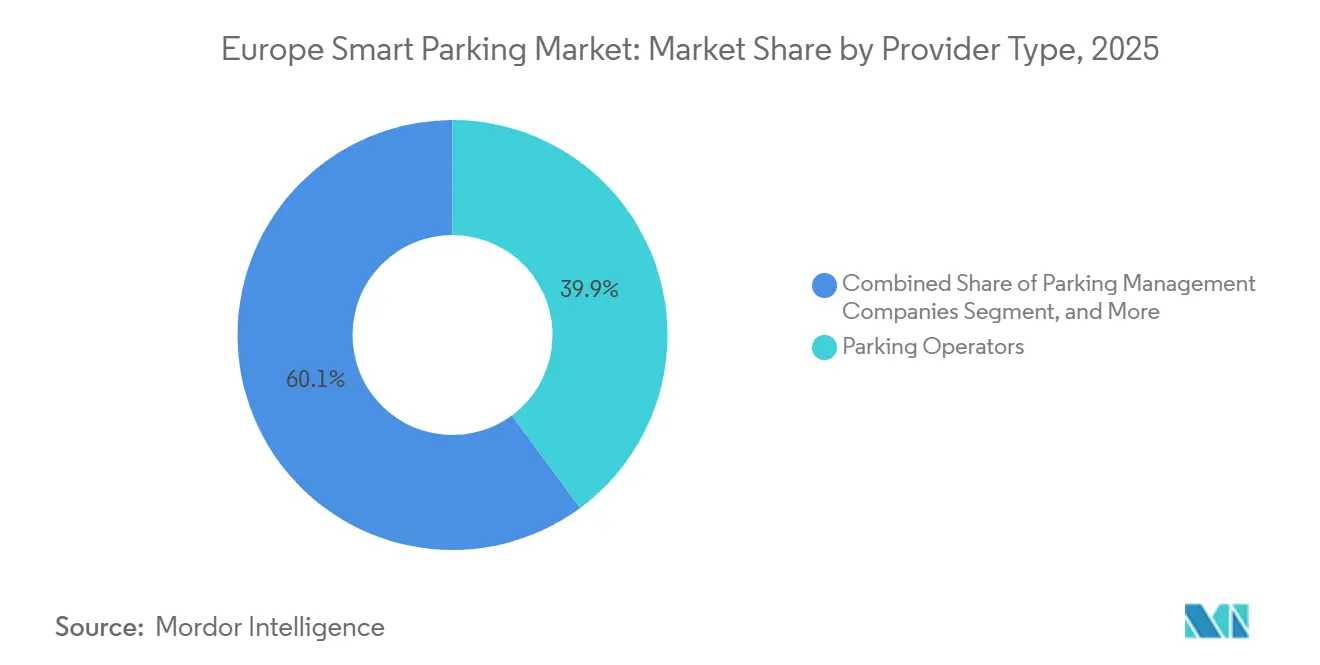

- By provider type, parking operators dominated with 39.87% share in 2025, whereas peer-to-peer platforms are projected to grow fastest at an 11.02% CAGR through 2031.

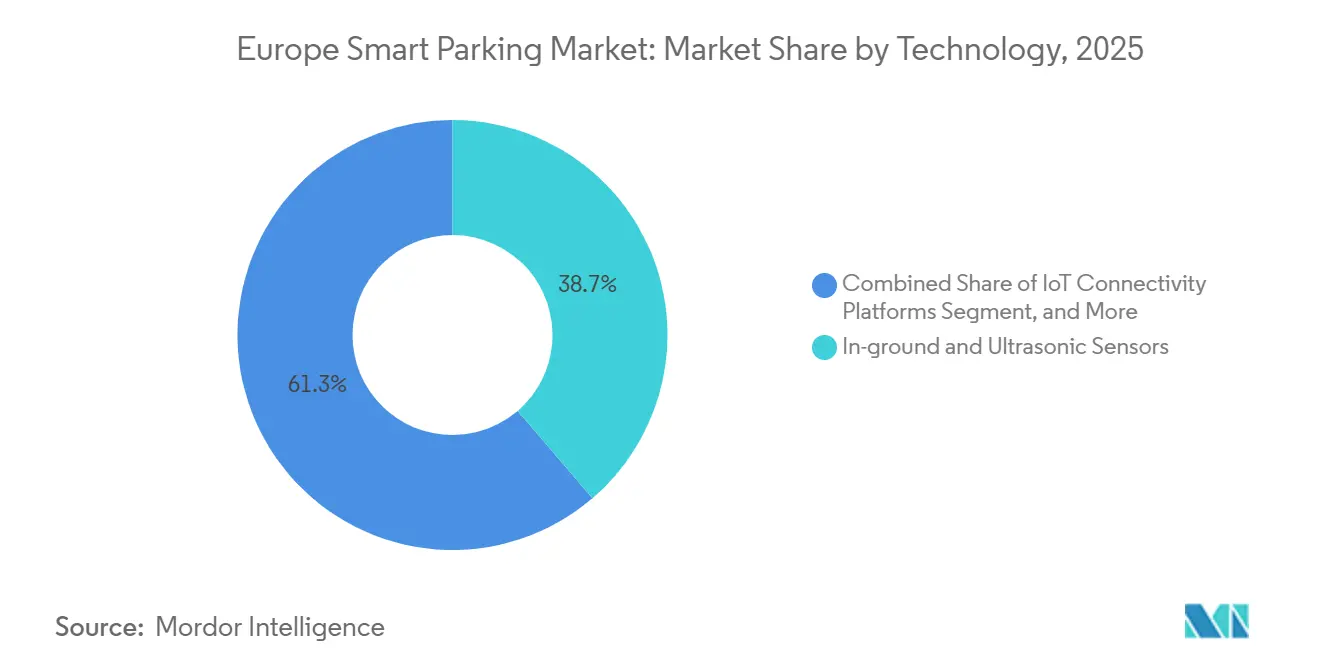

- By technology, in-ground and ultrasonic sensors accounted for 38.71% of Europe smart parking market size in 2025, but EV-charging-integrated parking is advancing at a 12.27% CAGR over 2026-2031.

- By end user, municipalities and government entities captured 41.74% spending in 2025, while corporate campuses are set to rise quickest at a 10.43% CAGR through 2031.

- By geography, Germany held 36.12% revenue share of the Europe smart parking market size in 2025, whereas Italy is expected to achieve the highest 11.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Smart Parking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Driven Parking Space Stress | +2.1% | Germany, Netherlands, Nordics, spillover to France and United Kingdom | Medium term (2-4 years) |

| Rise of Mobile Payments and Parking Apps | +1.8% | United Kingdom, Germany, France, Spain, Italy | Short term (≤ 2 years) |

| EU Smart-City Funding for MaaS Pilots | +1.5% | Italy, Spain, France, Central and Eastern Europe | Medium term (2-4 years) |

| Corporate Scope-3 Decarbonization Targets | +1.2% | Germany, United Kingdom, Netherlands, France | Long term (≥ 4 years) |

| EU Data-Sharing Mandates Under Revised ITS Directive | +0.9% | All EU member states | Medium term (2-4 years) |

| 15-Minute-City Zoning Accelerating Curb Reforms | +0.8% | France, Spain, Netherlands, pilot interest in Italy and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Driven Parking Space Stress

Battery-electric vehicle registrations passed 1 million public charging points in 2024, and analysts see that figure doubling by 2030, forcing operators to retrofit facilities with power upgrades, conduit, and payment integration. The Alternative Fuels Infrastructure Regulation compels every member state to provide one public charger for every 10 EVs by 2030, converting parking areas into distributed energy nodes.[1]European Commission, “Alternative Fuels Infrastructure Regulation,” ec.europa.eu Energy utilities such as E.ON have earmarked EUR 40 billion (USD 45.2 billion) for charging networks and are now piloting vehicle-to-grid services with automotive OEMs. These initiatives create fresh revenue streams but introduce operational complexity as parking managers must comply with metering rules and manage peak-tariff exposure. Municipalities that blend parking and charging data can unlock congestion-pricing synergies while meeting climate targets, positioning EV-ready bays as premium real estate.

Rise of Mobile Payments and Parking Apps

Contactless transactions became mainstream during the pandemic, and by 2025 the United Kingdom recorded 81% penetration for parking fees, with most users preferring in-car or smartphone payments. EasyPark processed more than 250 million parking sessions across 4,000 cities in 2025, highlighting the shift from coin-operated meters to digital sessions that capture granular occupancy data.[2]EasyPark Group, “250 Million Transactions Across 4,000 Cities in 2025,” easyparkgroup.com Interchange-fee caps, 0.2% for debit and 0.3% for credit, lowered the cost barrier for small municipalities to adopt card-based systems . Mobile apps also enable real-time push notifications, bundled mobility rewards, and dynamic pricing experiments that were impossible with static kiosks. As curb management becomes data-rich, operators leveraging digital payments gain insights to calibrate tariffs and reduce cruising time, improving air quality in dense urban cores

EU Smart-City Funding for MaaS Pilots

Horizon Europe earmarked EUR 101.5 million (USD 114.7 million) for MaaS research in 2024, and the European Institute of Innovation and Technology added EUR 60 million (USD 67.8 million) for integrated mobility pilots.[3]European Commission, “EUR 101.5 Million for Mobility-as-a-Service Research,” ec.europa.eu Italy alone set aside EUR 561 million (USD 633 million) for city-scale pilots in Milan, Rome, and Turin. The revised ITS Directive obliges member states to release static and dynamic parking data by 2027, cutting vendor lock-in and letting MaaS aggregators display real-time availability alongside transit options. Spain followed with EUR 150 million (USD 169.5 million) for smart-mobility infrastructure, prioritizing parking data as the backbone of congestion-pricing experiments. Funding conditions that mandate open APIs and KPI-based payouts are steering procurement toward cloud-native platforms with strong analytics layers

Corporate Scope-3 Decarbonization Targets

Large enterprises are embedding commuter emissions into ESG scorecards, creating demand for workplace parking systems that log vehicle type, dwell time, and energy source. DHL aims to cut Scope 3 emissions by 2.6 million metric tons annually by 2030, and its parking analytics feed employee commute dashboards. Maersk and Unilever have announced similar metrics, while IKEA plans to use 100% renewable electricity across sites by 2030, integrating EV charging into staff parking. Tech giants Amazon, Google, and Microsoft already run reservation-based parking that enforces allocation rules and auto-generates emissions reports. Vendors that can couple parking bookings with carbon calculations are tapping a fast-growing B2B niche where buying cycles are shorter than municipal tenders and budgets are less constrained.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-Front Sensor and Civil-Works Costs | -1.4% | All regions, acute in Southern and Eastern Europe | Short term (≤ 2 years) |

| Fragmented Municipal Procurement Cycles | -1.1% | Italy, Spain, France, Germany, United Kingdom | Medium term (2-4 years) |

| GDPR-Driven Restrictions on ANPR Analytics | -0.7% | All EU member states | Long term (≥ 4 years) |

| EV-First Kerb Allocation Shrinking Paid Bays | -0.5% | Germany, Netherlands, Nordics, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-Front Sensor and Civil-Works Costs

Municipalities spend USD 300-500 per bay to install in-ground sensors, covering excavation, cabling, and backhaul connectivity, a burden that deters smaller cities with modest parking revenues.[4]U.S. Department of Transportation, “Parking Sensor Installation Costs USD 300-500 per Space,” its.dot.gov A Czech pilot using 3,676 sensors showed an average lifespan of just over five years before battery replacement, adding a recurring outlay for cash-strapped councils. Heritage zones further inflate costs because trenching requires archaeological supervision and adherence to strict restoration codes. Camera-based systems lower civil-works outlays but carry higher licensing fees and data-privacy compliance costs. Without external grants or outcome-based financing, many towns choose incremental meter upgrades rather than full smart-parking rollouts, slowing overall penetration.

Fragmented Municipal Procurement Cycles

European local authorities often run 18-24-month tender processes, and revised Italian procurement rules now score bids on social and environmental criteria, lengthening evaluations. Barcelona and Madrid each work with multiple concessionaires managing more than 100,000 bays, complicating integration and delaying region-wide standards. United Kingdom councils grappled with 20% real-term budget cuts between 2010 and 2025, forcing parking projects to compete with essential services for scarce funds. Vendors face high bid-preparation expenses, and staggered awards make it hard to achieve scale economies, keeping hardware prices elevated and dampening smart-parking adoption rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Provider Type: Peer-to-Peer Platforms Challenge Incumbents

Peer-to-peer players recorded the fastest growth trajectory, with an 11.02% projected CAGR through 2031, as asset-light models monetize idle residential driveways and off-peak office lots. This surge is eating into the 39.87% share parking operators held in 2025, pressuring concessionaires that rely on fixed tariffs and long-term contracts. Marketplaces such as JustPark, ParkBee, and Parclick advertise real-time availability, transparent pricing, and loyalty perks, creating a seamless user journey that traditional cash or kiosk environments cannot match. The Europe smart parking market is therefore witnessing a power shift toward data-driven platforms that can scale across borders without laying concrete.

Parking operators retain strategic advantages in airports and city-center garages, yet they must modernize apps, embed dynamic pricing, and partner with EV-charging networks to defend margins. As municipalities mandate open data, operators that cling to proprietary systems risk being sidelined in MaaS aggregators. Peer-to-peer hosts still navigate zoning, insurance, and tax hurdles, but once these frameworks mature, their low capital intensity will keep them at the growth frontier of the Europe smart parking market.

By Solution: Services Segment Gains Traction

Managed services are forecast to expand at a 10.14% CAGR to 2031, reflecting municipal appetite for outcome-based contracts that shift uptime and data-accuracy risk to vendors. Bundled packages that include software licenses, sensor maintenance, and analytics dashboards help budget-constrained cities convert large capital outlays into predictable operating expenses. Software already held 44.91% of Europe smart parking market share in 2025, illustrating the sector’s pivot from hardware-centric deployments to cloud-native platforms that aggregate real-time occupancy feeds and support API connectivity.

Hardware remains critical but is inching toward commoditization as sensor prices fall and multi-vendor interoperability becomes the norm. Services firms differentiate through rapid deployment, KPI guarantees, and integration expertise, enabling city managers to meet regulatory timelines without hiring in-house data scientists. As more municipalities adopt performance-based tenders, vendors offering cradle-to-grave support are well positioned to capture recurring revenue in the Europe smart parking market.

By Technology: EV-Charging Integration Accelerates

In-ground and ultrasonic sensors captured 38.71% of technology revenue in 2025, valued for detection accuracy yet hindered by costly civil works. Camera-based systems promise lower installation complexity and richer enforcement data, but GDPR constraints require robust consent and anonymization workflows, adding compliance overhead. Connectivity layers leveraging LoRaWAN and NB-IoT improve battery life and coverage, though signal attenuation inside multi-story garages remains a technical hurdle.

EV-charging-ready bays are the clear breakout, expected to post a 12.27% CAGR through 2031. Utilities, automakers, and parking operators are co-investing in integrated stalls that monetize both kilowatt-hours delivered and parking duration, creating dual revenue streams in the Europe smart parking market. Standards battles around roaming protocols and billing interoperability persist, yet early adopters like the Netherlands are proving that bundled parking-and-charging propositions can achieve faster payback than standalone chargers or meters.

By End User: Corporate Campuses Embrace Smart Parking

Municipalities and government entities still represent the largest spending bloc at 41.74% of 2025 outlays, but budget rigidity often limits the scope of projects to pilot corridors. Corporate campuses are emerging as the fastest-growing segment, predicted to climb at a 10.43% CAGR, because ESG reporting frameworks now demand granular commute data. Reservation-based systems that allocate bays according to carpool status or vehicle type optimize real-estate utilization while feeding Scope 3 dashboards.

Transport hubs, malls, and mixed-use developers also intensify investments as they compete for footfall in post-pandemic retail environments. Residential complexes, once reluctant to spend on parking technology, are rolling out app-based guest management to enhance security and property valuations. This broadening demand base underscores how the Europe smart parking market is evolving from a municipal service into a cross-sector digital utility.

Geography Analysis

Germany remains the revenue anchor, holding 36.12% of regional takings in 2025 thanks to early automatic number-plate recognition (ANPR) adoption and close ties between software providers and automotive OEMs. Berlin alone digitized more than 35,000 curbside spaces, and a 2026 pilot with PayByPhone and Goldbeck is testing demand-responsive tariffs across 118,500 bays, signaling scale readiness. Nevertheless, growth momentum is shifting southward. Italy is poised to log an 11.02% CAGR through 2031 on the back of EUR 561 million (USD 633 million) in MaaS grants and aggressive pilots in Milan, Rome, and Turin, each integrating parking APIs into multimodal planners that cut search time and pollution.

France benefits from Paris’s 15-minute-city zoning, which reallocates curb inventory from commuter storage to shared mobility, compelling the remaining bays to adopt rigorous dynamic-pricing logic. Spain channelled EUR 150 million (USD 169.5 million) into smart-mobility infrastructure, with Barcelona layering parking data into future congestion-charge schemes. The Netherlands punches above its weight in digital payments and EV adoption, yet limited absolute population caps its revenue potential compared with Germany. Nordic capitals demonstrate high technological readiness but face seasonal maintenance costs that lengthen sensor replacement cycles.

Central and Eastern Europe, including Poland, the Czech Republic, Hungary, and Romania, remains underpenetrated but registers rising interest in low-cost sensor grids and mobile payments as car ownership climbs. Pardubice’s example, where 3,421 hybrid sensors boosted annual parking income from CZK 23 million (USD 1.1 million) to CZK 40 million (USD 1.9 million), is prompting neighboring cities to launch similar tenders. Although starting from a smaller base, these markets could provide upside beyond 2028 as EU cohesion funds become available for digital infrastructure.

Competitive Landscape

No vendor controls even a tenth of the Europe smart parking market, making the arena moderately competitive but highly fragmented. Incumbent operators such as APCOA (1.8 million spaces), Indigo Group (2.3 million globally), and EasyPark Group (250 million annual transactions) are leveraging scale to negotiate multi-city concessions while layering analytics onto existing estates. Their combined share still sits below 30%, leaving ample headroom for agile newcomers. Asset-light disruptors like ParkBee, JustPark, and Parclick curate underused private inventory and monetize via dynamic pricing, scaling without concrete or steel.

Technology specialists pursue two playbooks: sensor innovation and software-as-a-service. Fleximodo’s hybrid magnetometer-nanoradar device achieved 99% accuracy in the Czech Republic, raising the performance bar for ultrasonic legacy fleets. Cloud-native platforms are winning municipal RFPs because they interoperate with mixed sensor environments and comply with GDPR by design. Regulatory clarity on ANPR processing, issued by the European Data Protection Board in 2024, is a double-edged sword, it deters undercapitalized entrants yet rewards firms that invest early in privacy-by-default architectures.

Strategic moves include January 2026’s PayByPhone-Goldbeck alliance to roll out smart parking across German and Austrian campuses, and December 2025’s Autopay acquisition of Simplyture, bolstering free-flow ANPR capabilities in airports. Services integrators like Hitachi Rail are bundling AI cameras and ticketless entry into turnkey packages, evidenced by the 13-facility upgrade for METPARK Bordeaux. As municipalities mandate open data and outcome-based contracting, the battleground is shifting from hardware margins to recurring analytics and payment revenues, elevating software fluency as the key differentiator in the Europe smart parking market.

Europe Smart Parking Industry Leaders

Daimler Mobility

Flowbird SASU (Parkeon SA)

Urbiotica SL

BMW i Ventures (ParkNow heritage assets)

Q-Park NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: PayByPhone and Goldbeck formed a partnership to deploy mobile payments, occupancy sensors, and dynamic pricing across 118,500 spaces in Germany and Austria, launching a pilot in Nuremberg.

- December 2025: METPARK teamed with Hitachi Rail to modernize 13 Bordeaux facilities with ticketless entry and AI cameras, completing the rollout in 11 months.

- December 2025: Autopay Technologies migrated to a cloud platform and acquired Simplyture to extend free-flow ANPR at more than 600 European locations.

- October 2025: E.ON introduced its AMPECO software in the Czech Republic, blending EV-charging management with parking reservations and dynamic pricing.

Europe Smart Parking Market Report Scope

Smart parking solutions are defined as digital tools that enable riders to find and book a parking space by providing real-time information on availability. Recent technological advancements help the related stakeholders collaborate and provide a bundled offering that involves a combination of mobile apps, payment platforms, dynamic signs, sensors, and other localized solutions.

The Europe Smart Parking Market Report is Segmented by Offerer Type (Parking Operators, Parking Management Companies, Infrastructure Providers, Peer-to-Peer Platforms, Aggregators and Marketplaces), Solution (Hardware, Software, Services), Technology (In-Ground and Ultrasonic Sensors, Camera and Computer-Vision and ANPR, IoT Connectivity Platforms, Mobile Apps and Digital Payments, EV-Charging Integrated Parking), End-User (Municipalities and Government, Commercial Car-Parks and Malls, Transport Hubs, Corporate Campuses and Business Parks, Residential and Mixed-Use Developments), and Geography (Germany, United Kingdom, France, Spain, Italy, Netherlands, Nordics, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Parking Operators |

| Parking Management Companies |

| Infrastructure Providers (HW and SW) |

| Peer-to-Peer (P2P) Parking Platforms |

| Aggregators and Marketplaces |

| Hardware |

| Software |

| Services |

| In-Ground and Ultrasonic Sensors |

| Camera and Computer-Vision and ANPR |

| IoT Connectivity Platforms |

| Mobile Apps and Digital Payments |

| EV-Charging Integrated Parking |

| Municipalities and Government |

| Commercial Car-Parks and Malls |

| Transport Hubs (Airports, Rail) |

| Corporate Campuses and Business Parks |

| Residential and Mixed-Use Developments |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Nordics |

| Rest of Europe |

| By Provider Type | Parking Operators |

| Parking Management Companies | |

| Infrastructure Providers (HW and SW) | |

| Peer-to-Peer (P2P) Parking Platforms | |

| Aggregators and Marketplaces | |

| By Solution | Hardware |

| Software | |

| Services | |

| By Technology | In-Ground and Ultrasonic Sensors |

| Camera and Computer-Vision and ANPR | |

| IoT Connectivity Platforms | |

| Mobile Apps and Digital Payments | |

| EV-Charging Integrated Parking | |

| By End-User | Municipalities and Government |

| Commercial Car-Parks and Malls | |

| Transport Hubs (Airports, Rail) | |

| Corporate Campuses and Business Parks | |

| Residential and Mixed-Use Developments | |

| By Region | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Nordics | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe smart parking market?

It stands at USD 4.71 billion in 2026 and is projected to reach USD 7.34 billion by 2031.

Which technology segment is growing fastest?

EV-charging-integrated parking technology is expected to post a 12.27% CAGR through 2031.

Why is Italy the fastest-growing geography?

National MaaS grants of EUR 561 million (USD 633 million) and ambitious city pilots in Milan, Rome, and Turin drive an 11.02% CAGR to 2031.

How do peer-to-peer platforms impact traditional operators?

Asset-light models grow at an 11.02% CAGR, eroding operator margins by offering dynamic pricing and real-time availability to drivers.

What restrains adoption in smaller municipalities?

Up-front sensor costs of USD 300-500 per bay and fragmented 18-24-month procurement cycles slow full-scale deployments.

How are corporates using smart parking for ESG goals?

Enterprises deploy reservation-based systems that track vehicle type and charging data, feeding Scope 3 emissions reports and supporting decarbonization targets.

Page last updated on: