Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

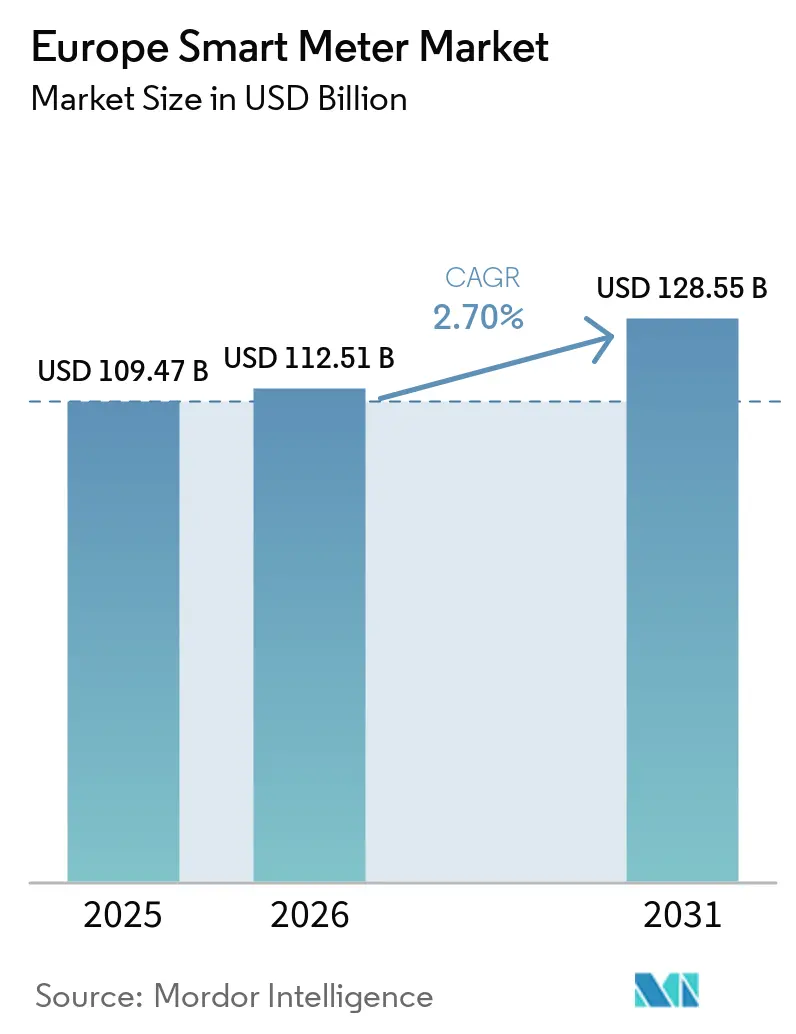

| Base Year Market Size (2025) | USD 109.47 Billion |

| Market Size (2026) | USD 112.51 Billion |

| Market Size (2031) | USD 128.55 Billion |

| Growth Rate (2026 - 2031) | 2.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Smart Meter Market Analysis by Mordor Intelligence

The Europe smart meter market size is expected to increase from USD 112.51 million in 2026 to USD 128.55 million by 2031, growing at a CAGR of 2.70% over 2026-2031. Utilities that completed mass-rollout mandates before 2025 now concentrate on retrofitting first-generation meters, integrating distributed-energy resources and monetizing interval data. Budget reallocations favour head-end software, cyber-security upgrades and multi-utility contracts instead of new hardware alone. Nation-specific policy updates, such as the revised Gas Directive 2024/1788 and country-level net-zero targets, continue to unlock replacement demand even where household penetration already exceeds 80%. Vendor competition intensifies around cellular NB-IoT and LTE-M connectivity, edge analytics and managed-service offerings that promise higher lifetime margins than commoditized meter hardware.

Key Report Takeaways

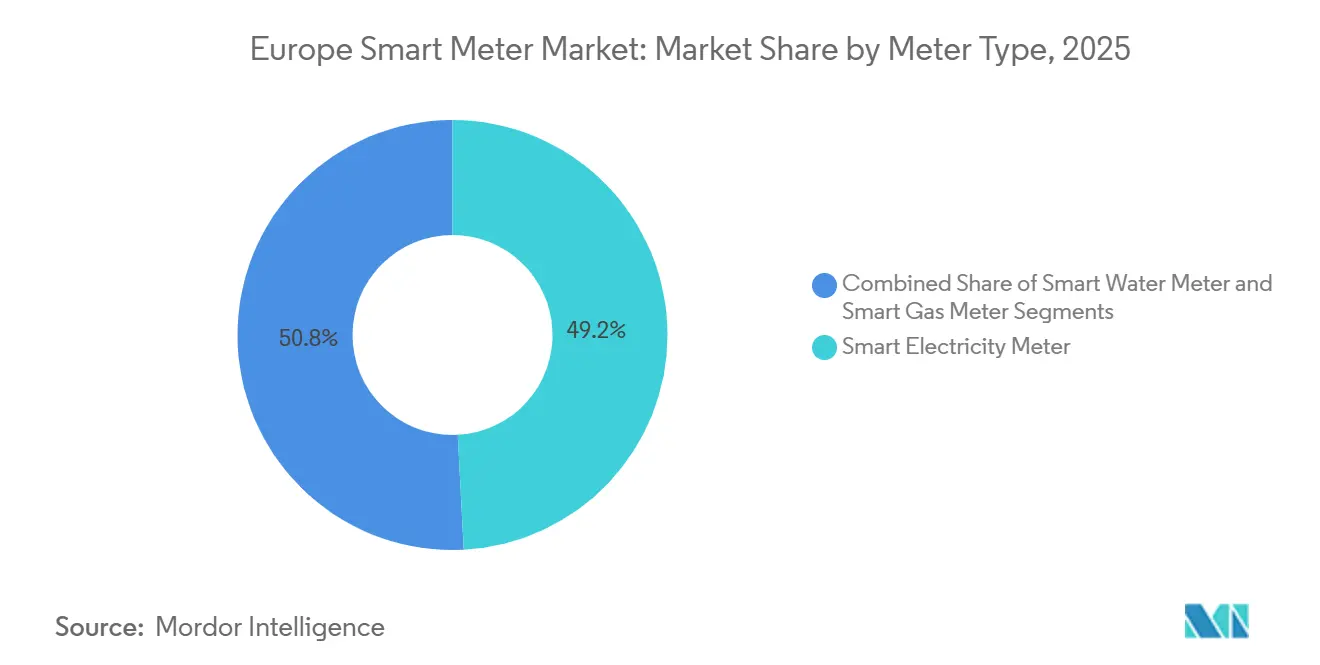

- By meter type, smart electricity meters led with 49.17% of the Europe smart meter market share in 2025, while smart gas meters are projected to expand at a 3.62% CAGR through 2031.

- By communication technology, power-line communication captured 42.19% of the revenue share in 2025; cellular NB-IoT and LTE-M variants recorded the fastest growth at 3.22% to 2031.

- By component, hardware accounted for 63.22% of the European smart meter market size in 2025, whereas software and analytics platforms advanced at a 3.29% CAGR through 2031.

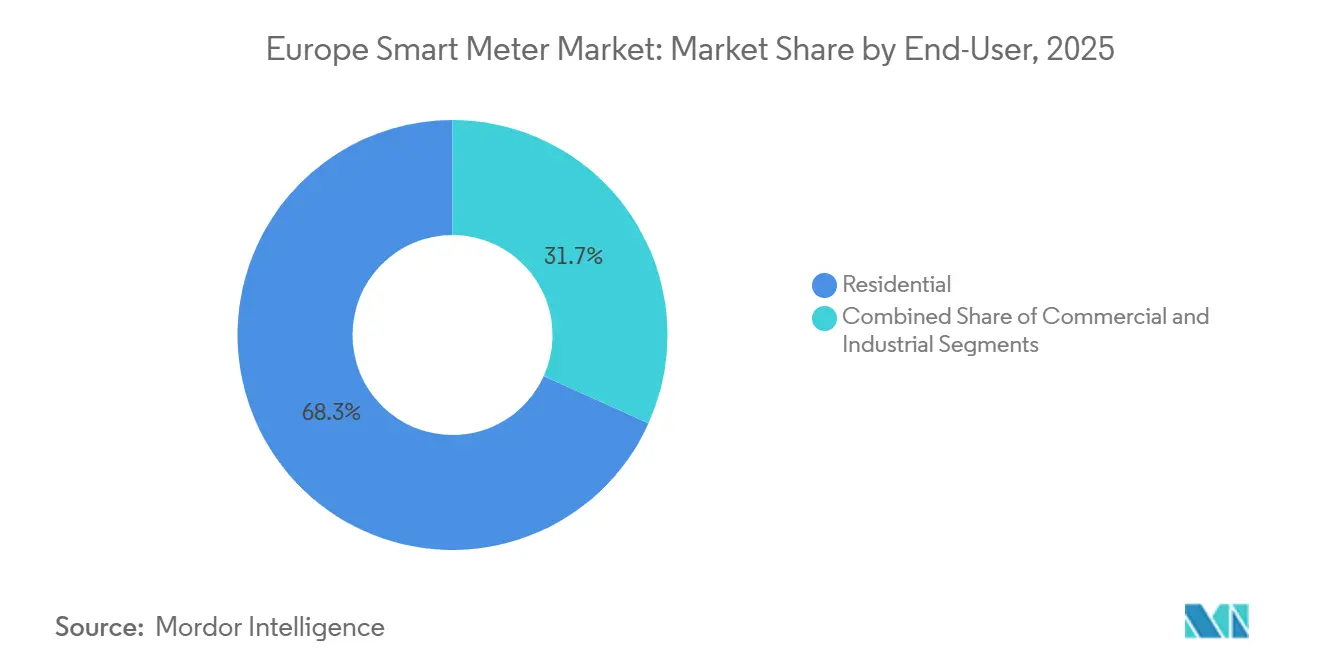

- By end-user, residential installations represented 68.26% of shipments in 2025, yet commercial deployments attained the highest growth trajectory at 3.55% to 2031.

- By phase, single-phase meters held 71.09% of installed units in 2025, but three-phase models enjoy the fastest expansion at 3.89% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Smart Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-Wide Mandatory Rollout Targets (Directive 2019/944) | +0.80% | Pan-European, strongest in Germany, France, Spain, Italy | Medium term (2-4 years) |

| Growing Smart-Grid and DER Integration Needs | +0.60% | Germany, Netherlands, Belgium, Denmark | Long term (≥4 years) |

| Smart-City Digitalisation Programs | +0.50% | Urban centers in France, UK, Spain | Medium term (2-4 years) |

| Transactive-Energy Pilot Schemes | +0.30% | Netherlands, Germany, select UK municipalities | Long term (≥4 years) |

| Real-Time Flexibility-Market Data Demand | +0.40% | Germany, France, Nordic grid operators | Short term (≤2 years) |

| IoT Leak-Detection Bundling With Retrofits | +0.20% | Italy, Spain, Southern Europe water utilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU-Wide Mandatory Rollout Targets

Directive 2019/944 obliged member states to equip at least 80% of consumers with smart meters by 2025, creating the bedrock for the current Europe smart meter market.[1]European Commission, “Directive 2019/944 on Common Rules for the Internal Market for Electricity,” europa.eu Germany reached 72% penetration, France surpassed 85% and Spain exceeded 90% by end-2025, yet several Eastern European utilities still trail the target, sustaining installation work through 2028.[2]Bundesnetzagentur, “Smart-Meter Rollout Status Report 2025,” bundesnetzagentur.de Article 19 of the directive also requires the retirement of non-compliant first-generation units, thereby extending replacement demand even in saturated regions. Italy’s procurement rules now require DLMS Blue Book conformity, disqualifying roughly 30% of legacy SKU catalogues and widening entry opportunities for challengers. Parallel obligations for natural-gas networks under Directive 2024/1788 accelerate gas-meter uptake in Belgium and the Netherlands.

Growing Smart-Grid and DER Integration Needs

Distributed-energy resources represented 38% of Germany’s installed capacity in 2025, forcing distribution operators to seek fine-grained voltage and frequency data unavailable from classic SCADA systems.[3]Fraunhofer ISE, “Renewable Energy Data for Germany 2025,” fraunhofer.de E.ON cut transformer overload events by 22% after installing meters with embedded power-quality analytics in Bavaria. Dutch regulator Netbeheer Nederland now mandates IEC 61850-capable meters so that inverters and EV chargers can be synchronized natively. Itron’s 2025 firmware update allows open-API integrations, reflecting the market’s pivot to edge intelligence. France’s Enedis remotely upgraded 1.2 million Linky units in 2025 to participate in demand-response contracts with Voltalis and EDF.

Smart-City Digitalisation Programs

Cities like Barcelona, Amsterdam and Lyon funnel smart-meter data into wider IoT platforms to optimize lighting, mobility and waste services, raising permissible meter price points. Spain’s Red.es earmarked EUR 180 million (USD 203 million) in 2024 for small-town deployments, boosting adoption where business cases were marginal. The United Kingdom’s Local Energy Hubs program provided GBP 120 million (USD 152 million) in 2025 for urban flexibility pilots. ADEME showed French municipalities cut energy spending by 14% after integrating smart-meter feeds with building-management systems, prompting mandatory retrofits in public facilities. Vendors increasingly bundle analytics dashboards and predictive maintenance into multi-year service contracts to align with municipal procurement preferences.

Transactive-Energy Pilot Schemes

Peer-to-peer trading requires sub-second timestamps and cryptographic signing, yet roughly 60% of installed European meters lack such firmware. Rotterdam’s Jouliette pilot equipped 800 households with Kamstrup Omnipower units, cutting peak-demand charges by 9% during 2025 trials. Energy Brainpool and Elia Group launched a 1 200-site initiative in North Rhine-Westphalia that settles intra-day trades every five minutes. Horizon Europe has reserved EUR 50 million (USD 56.5 million) for twelve pilots that will inform future network codes. Regulatory gaps remain, illustrated by Belgium’s CREG, which has not yet approved compatible tariff models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Cyber-Security Risk | -0.50% | Eastern Europe, Southern Italy, rural Spain | Short term (≤2 years) |

| Legacy-System Interoperability Gaps | -0.40% | UK, Germany, France (utilities with pre-2015 AMI) | Medium term (2-4 years) |

| Consumer Privacy Backlash Versus Data Granularity | -0.20% | Germany, Austria, Nordic countries | Short term (≤2 years) |

| Semiconductor Supply-Chain Bottlenecks | -0.30% | Pan-European, acute in Belgium, Netherlands | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Cyber-Security Risk

Average fully loaded rollout expenses of EUR 250-350 (USD 282-395) per endpoint strain small municipal utilities, forcing many to seek concessional finance. Electrica disclosed that smart-meter projects would absorb 18% of its five-year capex, delaying grid-reinforcement work. ENISA recorded 23 ransomware attacks on AMI networks in 2024, with average remediation costs exceeding EUR 2 million (USD 2.26 million). Italy’s regulator now mandates IEC 62351 encryption, adding EUR 8-12 (USD 9-13.5) to meter bills but protecting consumer data. Financial models therefore increasingly bundle cyber-monitoring subscriptions to recoup the higher hardware spend.

Legacy-System Interoperability Gaps

Roughly 8 million SMETS1 meters in the United Kingdom cannot yet support full supplier switching, undermining dynamic-tariff adoption. A firmware-upgrade campaign launched in 2024 failed on 18% of devices, leaving them non-communicating. German utilities still contend with divergent DLMS object models deployed before 2023, adding middleware costs. Enedis found only 60% of tested third-party devices fully interoperable with Linky’s customer-interface module, prompting a EUR 15 million (USD 16.95 million) standardization fund. These gaps postpone monetization of high-value services such as vehicle-to-grid and on-site storage coordination.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Meter Type: Gas Uptake Accelerates Under Carbon Rules

Smart electricity meters dominated the Europe smart meter market in 2025, delivering 49.17% Europe smart meter market share, yet their growth rate is tapering as household penetration nears saturation. Smart gas meters, riding on leak-detection analytics and EU methane-reduction law, are forecast to expand at 3.62% annually, the quickest pace among major categories. Italy’s Snam installed 320 000 Diehl gas meters that trimmed unaccounted-for volumes by 12%, illustrating the value proposition. Water-meter adoption is smaller but rising in drought-prone Southern Europe, backed by the European Investment Bank’s Blue Infrastructure Fund.

Momentum for gas meters is strongest in Belgium and the Netherlands, where operators have tied hydrogen-blending pilots to smart-meter rollouts. Electricity-meter activity has pivoted toward firmware upgrades rather than greenfield installs, keeping Europe smart meter market size expansion modest on that front. Utilities increasingly stipulate modular designs that accept future sensor add-ons, blurring demarcations between meter classes. Smart water meter deployments broaden vendor portfolios and hedge revenue as electrical hardware commoditizes.

By Communication Technology: Cellular Networks Win Reliability Debate

Power-line communication accounted for 42.19% of 2025 installations thanks to sunk infrastructure, but performance issues under high harmonic distortion spur a gradual shift to NB-IoT and LTE-M. Germany’s Westnetz pilot achieved 99.7% service uptime on cellular compared with 96.2% for PLC. Europe smart meter market size for cellular deployments is projected to grow prominently through 2031 as telcos offer discounted machine-type data plans.

Mesh RF remains relevant in rural settings where cellular dead zones persist, while fiber backhaul serves data-sensitive industrial sites. Utilities now mandate dual-mode options to future-proof against 2G sunsets. Vendors respond with plug-in modems, driving Europe smart meter industry partnerships between meter makers and telecom operators.

By Component: Software and Services Capture Value Migration

Hardware generated 63.22% of total Europe smart meter market size in 2025, yet margins compress under price pressure from Asian entrants. Consequently, utilities channel more budget toward analytics, outage management and cyber-monitoring platforms that guarantee recurring fees. Itron’s Temetra suite posted a 19% revenue jump in 2024, mirroring this preference.

Managed services expand fastest as regulators tighten data-protection rules, obliging utilities to outsource GDPR compliance. Siemens’ Cyber Defense Center charges EUR 0.50 (USD 0.56) per meter per year for threat monitoring, a cost many distribution operators accept as insurance. Software’s role in proactive asset maintenance also reduces truck rolls, lowering total cost of ownership and amplifying vendor lock-in.

By End-User: Commercial Sites Monetize Flexibility

Households still account for 68.26% of installations, but volume growth has slowed in markets such as France and the United Kingdom that neared full penetration by 2025. Commercial properties now turn interval data into revenue via demand-response aggregators, making them the fastest-growing customer class at 3.55% CAGR. France’s Voltalis secured EUR 8.2 million in 2025 capacity payments by curtailing commercial HVAC loads.

Industrial facilities install three-phase meters to verify Scope 2 emissions and optimize on-site cogeneration, aligning with EU taxonomy disclosure rules. Subscription-based “meter-as-a-service” propositions, such as Iberdrola’s 2025 launch, further illustrate how commercial customers prefer bundled analytics over hardware procurement.

By Phase: Three-Phase Designs Enable Electrification at Scale

Single-phase models retain 71.09% of units thanks to their residential focus, yet three-phase meters will log the quickest growth at 3.89% through 2031. Industrial decarbonization subsidies from Germany’s KfW and the Netherlands’ SDE++ spur adoption in factories and greenhouses. Enhanced meters capable of 1-second reads qualify assets for frequency-containment reserve income, expanding business cases beyond basic billing.

Residential upgradability also supports three-phase momentum. Utilities increasingly specify base units that can convert from single to three phase on site, extending asset life and protecting Europe smart meter market size investments. New product lines embed harmonic distortion and voltage-sag analytics to safeguard sensitive electronics in data centers and semiconductor fabs.

Geography Analysis

Germany, France and the United Kingdom collectively commanded the largest portion of the Europe smart meter market in 2025, underpinned by established rollout mandates and generous grid-modernization budgets. Germany’s certification delays slowed its household penetration to 72% by late 2025, but heavy investment in three-phase industrial meters sustains near-term growth. France surpassed 85% penetration after completing the 38 million-unit Linky program; Enedis now prioritizes firmware upgrades for vehicle-to-grid functionality. The United Kingdom’s 32 million smart meters face SMETS1 interoperability fixes, yet Ofgem expects dynamic pricing to become universal by 2027, reviving downstream service revenues.

Spain led penetration rates at 90% for electricity by 2025, while gas-meter mandates promise upside through 2031. Italy enforces second-generation meter installation by 2026, catalysing bulk orders with enhanced encryption. Belgium and the Netherlands pursue cellular-first communication strategies and high three-phase uptake to enable hydrogen blends and industrial flexibility.

Eastern European nations, funded by EU cohesion grants, present the highest percentage growth despite smaller absolute bases. Divergent certification processes mean deployment speed varies considerably, but the overarching Clean Energy Package harmonizes minimum functionality, keeping cross-border equipment designs largely uniform.

Competitive Landscape

The top five vendors captured about 55% of 2025 shipments, reflecting a moderately concentrated Europe smart meter market. Landis+Gyr, Itron and Kamstrup leverage multi-utility platform contracts, combined hardware and analytics bundles and DLMS/COSEM certifications to secure repeat orders. Mid-tier firms such as Diehl Metering and Apator gain regional share by offering modular firmware that extends asset life beyond 15 years, appealing to budget-constrained municipal utilities. Chinese entrants Holley Technology and Wasion Group undercut incumbent pricing by 15-20% but must still demonstrate cybersecurity parity and supply-chain resilience to convert pilot wins into long-term contracts.

Technological differentiation is migrating toward edge computing and encryption. Siemens embeds machine learning in firmware to predict transformer overheating, while STMicroelectronics’ STSAFE chip has become the de facto secure element in 60% of new European designs. Intellectual-property filings, such as Landis+Gyr’s field-upgradeable module patent, underscore the premium on adaptability. White-space opportunities center on transactive-energy pilots in which only 10% of installed meters meet latency requirements, opening partnership avenues for blockchain software firms.

Strategic moves during 2025-2026 emphasize service revenue. Itron’s USD 120 million managed-service deal with Enedis and Siemens’ Cyber Defense Center exemplify the pivot to recurring-fee models. Vendors also court cellular carriers to offer turnkey AMI-as-a-service propositions, bundling NB-IoT connectivity and threat monitoring under multi-year contracts.

Europe Smart Meter Industry Leaders

Landis+Gyr Group AG

Itron, Inc.

Kamstrup A/S

Sensus USA Inc. (Xylem)

Elster GmbH (Honeywell)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Landis+Gyr won an EUR 85 million contract with Naturgy to supply 1.2 million NB-IoT E360 meters over three years.

- December 2025: Itron secured a five-year USD 120 million agreement with Enedis to manage Temetra analytics for 38 million Linky meters.

- November 2025: Kamstrup introduced the Omnipower LTE-M variant and booked 300,000-unit orders from Liander.

- October 2025: Siemens inaugurated a EUR 40 million Cyber Defense Center in Munich, signing E.ON, Vattenfall, and Enel as launch customers.

Europe Smart Meter Market Report Scope

The Europe Smart Meter Market Report is Segmented by Meter Type (Smart Electricity Meter, Smart Gas Meter, Smart Water Meter), Communication Technology (Power-Line Communication (PLC), Radio Frequency (RF Mesh), Cellular (2G/4G/NB-IoT), Wired Ethernet/Fiber), Component (Hardware, Software And Analytics, Services (Deployment, AMI-Managed)), End User (Residential, Industrial, Commercial), Phase (Single Phase, Three Phase), and Country (United Kingdom, Germany, France, Italy, Spain, Belgium, Netherlands, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Meter Type

| Smart Electricity Meter |

| Smart Gas Meter |

| Smart Water Meter |

By Communication Technology

| Power-Line Communication (PLC) |

| Radio Frequency (RF Mesh) |

| Cellular (2G/4G/NB-IoT) |

| Wired Ethernet/Fiber |

By Component

| Hardware |

| Software And Analytics |

| Services (Deployment, AMI-Managed) |

By End-User

| Residential |

| Commercial |

| Industrial |

By Phase

| Single-Phase |

| Three-Phase |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Belgium |

| Netherlands |

| Rest Of Europe |

| By Meter Type | Smart Electricity Meter |

| Smart Gas Meter | |

| Smart Water Meter | |

| By Communication Technology | Power-Line Communication (PLC) |

| Radio Frequency (RF Mesh) | |

| Cellular (2G/4G/NB-IoT) | |

| Wired Ethernet/Fiber | |

| By Component | Hardware |

| Software And Analytics | |

| Services (Deployment, AMI-Managed) | |

| By End-User | Residential |

| Commercial | |

| Industrial | |

| By Phase | Single-Phase |

| Three-Phase | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Belgium | |

| Netherlands | |

| Rest Of Europe |

Key Questions Answered in the Report

How large is the Europe smart meter market in 2026?

It stands at USD 112.51 million and is projected to reach USD 128.55 million by 2031.

What is the forecast CAGR for European smart meters?

The market is set to grow at 2.70% from 2026 to 2031.

Which meter type is expanding fastest?

Smart gas meters are forecast to grow at a 3.62% CAGR through 2031 under methane-reduction mandates.

Why are cellular technologies gaining share over PLC?

Utilities prefer NB-IoT and LTE-M for higher uptime and to avoid signal interference affecting legacy PLC networks.

Which countries show the most untapped growth potential?

Spain and Italy for gas meters and Eastern European nations for overall penetration due to delayed initial rollouts.

What risks could slow future deployments?

High upfront capex, cyber-security threats and lingering interoperability issues with first-generation devices.

Page last updated on: