Europe Car Parking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

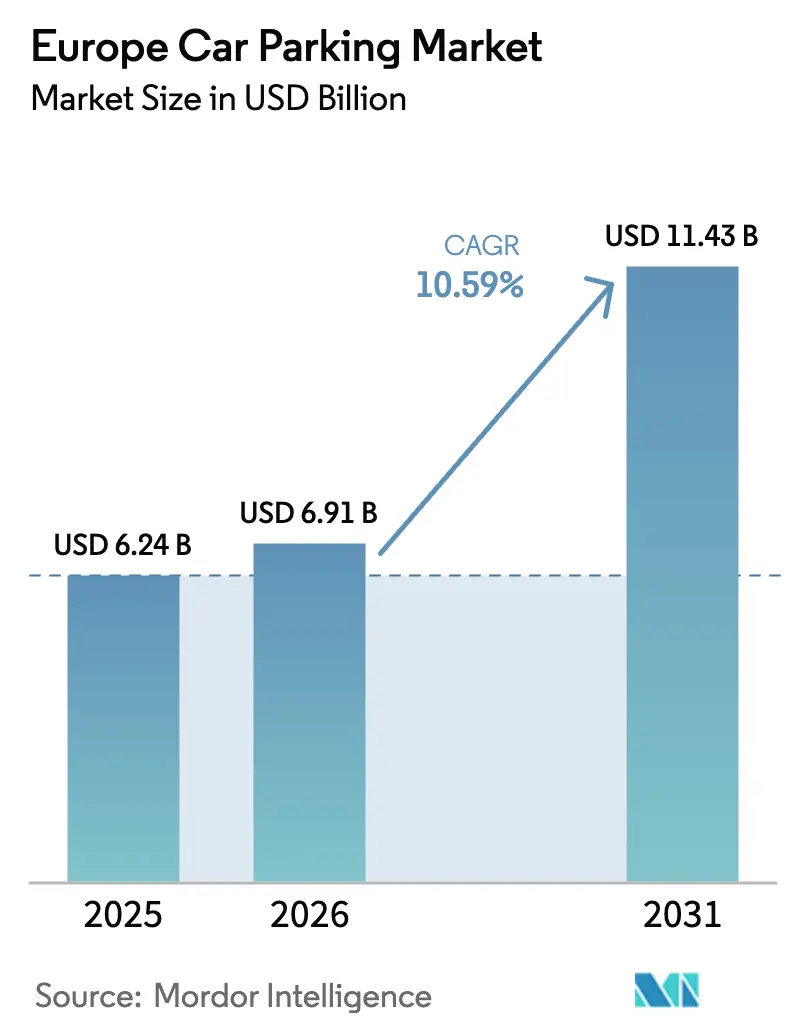

| Base Year Market Size (2025) | USD 6.24 Billion |

| Market Size (2026) | USD 6.91 Billion |

| Market Size (2031) | USD 11.43 Billion |

| Growth Rate (2026 - 2031) | 10.59% CAGR |

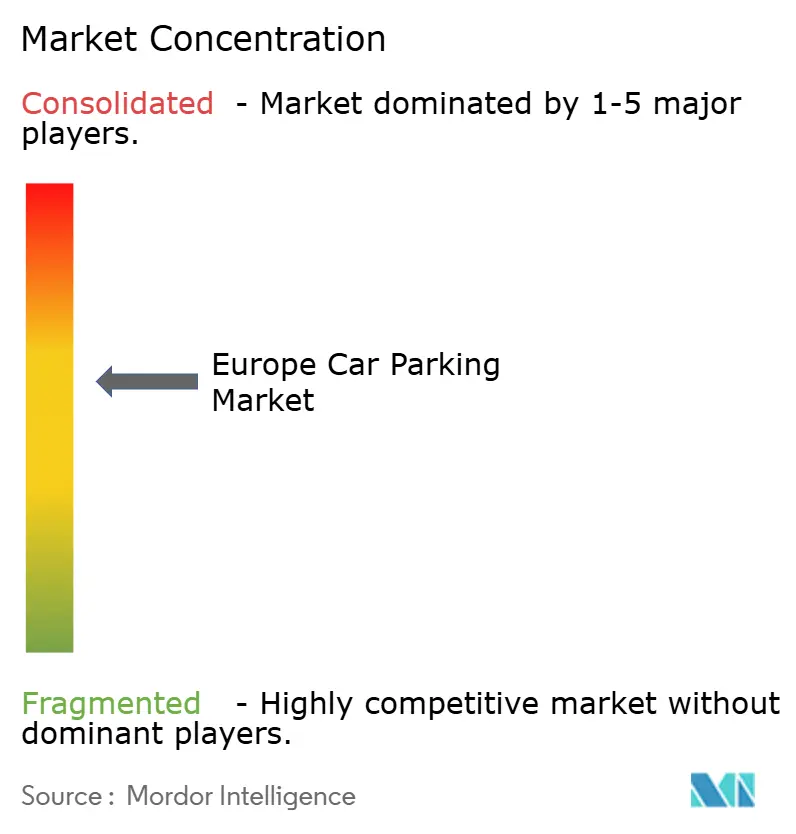

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Car Parking Market Analysis by Mordor Intelligence

The Europe Car Parking Market size is projected to expand from USD 6.24 billion in 2025 and USD 6.91 billion in 2026 to USD 11.43 billion by 2031, registering a CAGR of 10.59% between 2026 to 2031. This rapid expansion reflects the shift from passive space allocation to data-driven, electrification-ready assets that city governments and private operators now treat as a core element of urban-mobility strategy. AFIR-driven retrofit programs, the return of international visitors to pre-pandemic levels, and the roll-out of cashless, sensor-enabled curbside zones have combined to raise pricing power and unlock new revenue streams such as vehicle-to-grid (V2G) aggregation. Competition is intensifying as traditional garage owners defend share through long-term concessions and acquisitions of charging networks, while digital-first platforms convert idle residential and commercial capacity into bookable inventory. Operators that can blend physical capacity with predictive analytics are best placed to capture rising demand linked to e-commerce micro-fulfillment and EV adoption.

Key Report Takeaways

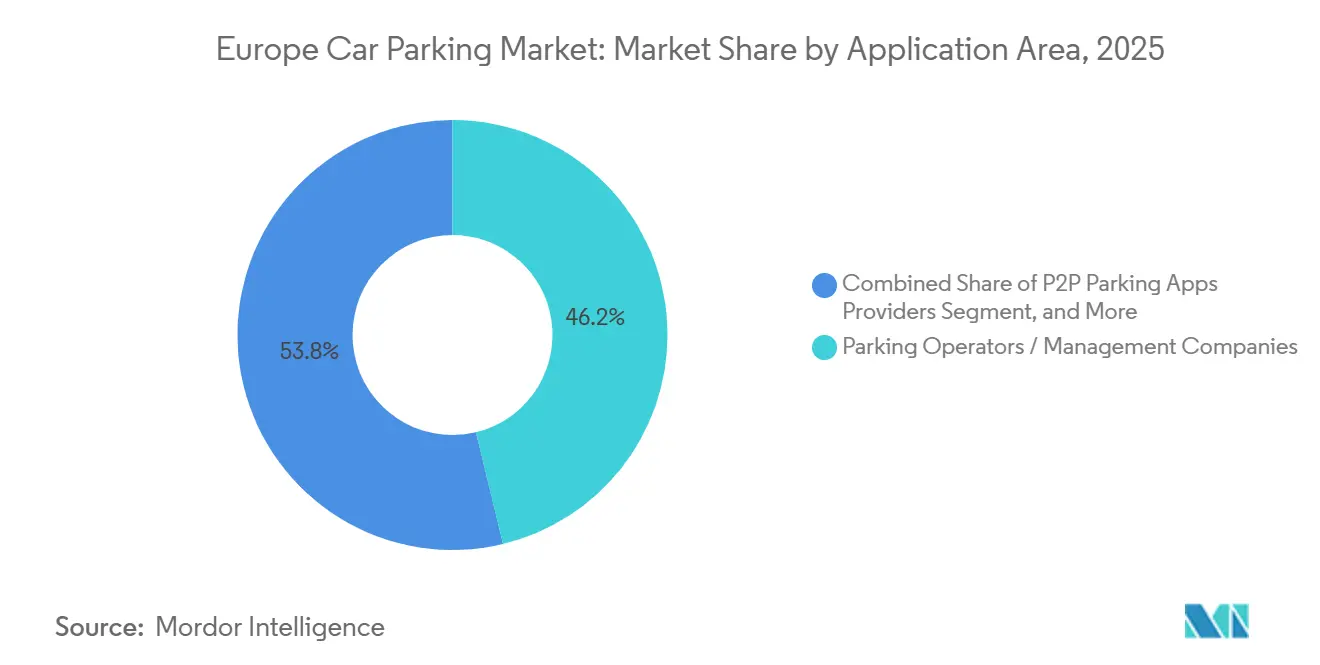

- By application area, parking operators and management companies led with 46.23% of the Europe car parking market share in 2025, while peer-to-peer app providers are advancing at a 11.26% CAGR through 2031.

- By parking site, off-street facilities captured 63.82% revenue in 2025; on-street assets are projected to expand at a 11.48% CAGR to 2031 as municipalities digitize the curb.

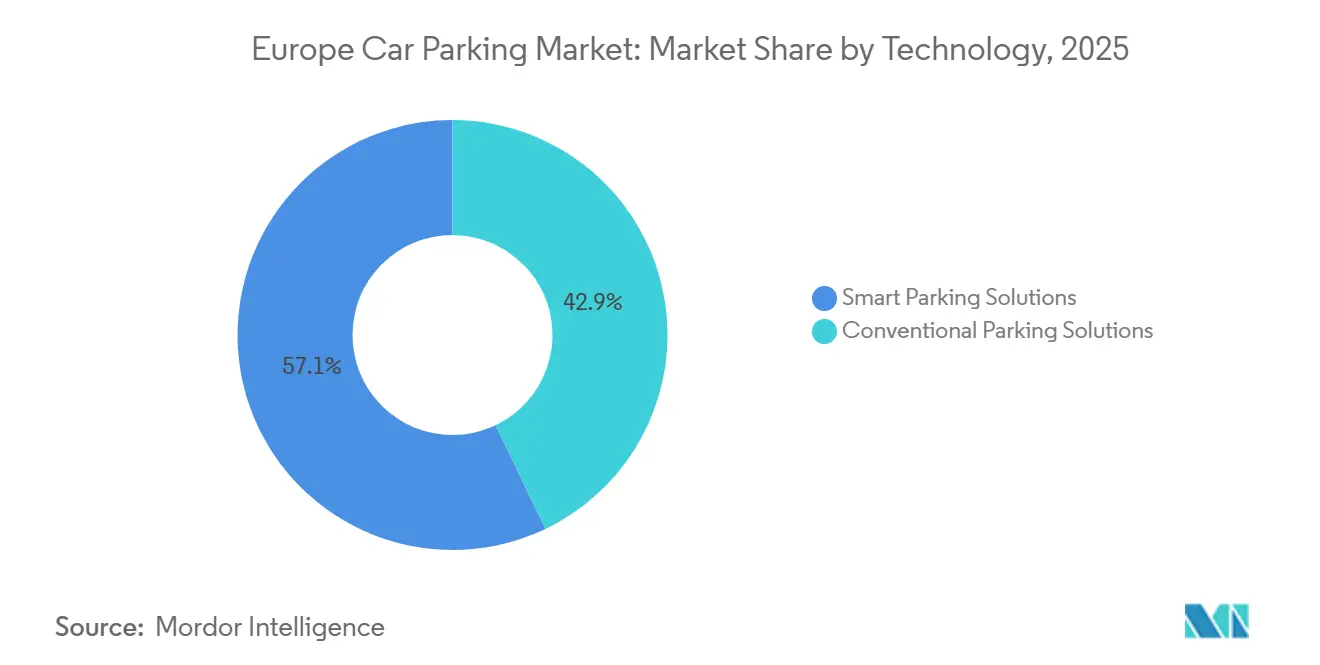

- By technology, smart parking solutions accounted for 57.11% of the Europe car parking market size in 2025 and are set to grow at 11.74% CAGR through 2031.

- By end-user type, municipalities held 38.22% share of the Europe car parking market in 2025, whereas residential complexes are the fastest-growing segment at a 12.01% CAGR.

- By country, Germany commanded 19.53% of regional revenue in 2025, while Poland is forecast to record the highest national CAGR at 11.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Car Parking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of EV-Charging Mandates | +2.8% | EU-wide, early enforcement in Germany, Netherlands, France | Medium term (2-4 years) |

| Recovery of Urban Tourism and Footfall | +2.1% | Spain, Italy, France, United Kingdom | Short term (≤ 2 years) |

| Municipal Adoption of Dynamic Pricing | +1.9% | Germany, United Kingdom, Netherlands, Sweden | Medium term (2-4 years) |

| Emergence of Curbside Logistics Hubs | +1.6% | Urban cores in Germany, France, United Kingdom, Netherlands | Medium term (2-4 years) |

| Integration of Parking Data into Digital Twins | +1.3% | Netherlands, Sweden, Germany, pilot cities in Spain | Long term (≥ 4 years) |

| Monetization of Idle Capacity via V2G | +1.1% | Netherlands, United Kingdom, Germany, Balearic Islands (Spain) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of EV-Charging Mandates In Parking Facilities

AFIR requires every European parking site with more than 20 spaces to install at least one charger, a rule that entered force in 2024.[1]European Commission, “Alternative Fuels Infrastructure,” energy.ec.europa.eu National add-ons magnify the effect, most notably Germany’s GEIG law obliging new non-residential buildings to pre-cable one in every five spaces. Compliance is accelerating joint ventures between garage owners and charge-point specialists such as Allego and Fastned, sharing capital outlays while granting operators upside from energy-services revenue. Utrecht’s 500-vehicle V2G pilot proved that parked EVs can supply power during evening peaks, creating a template for monetizing dwell time. Staggered enforcement France extended retrofit deadlines to 2027, Sweden pulled its target forward to 2025 creates a rolling procurement wave that benefits contractors and equipment makers across the decade.

Recovery Of Urban Tourism And Footfall

International arrivals exceeded 2019 levels in 2024, restoring congestion in historic centers and transport hubs. Airports such as Madrid-Barajas introduced 15-minute price recalibration, boosting revenue per space by 12% during Q1 2026. Retailers defend in-store traffic by subsidizing parking, while local ordinances shrinking curb capacity in Barcelona and Amsterdam paradoxically tighten supply even as demand climbs. The rebound is uneven, yet the net effect is upward pressure on hourly rates across tourist corridors.

Municipal Adoption Of Dynamic Pricing And Digital Payments

Cashless-only rules in London boroughs removed coin meters, routed every transaction through platforms like RingGo and JustPark, and linked ANPR enforcement for near-instant fines. Madrid’s SER scheme applies day-part pricing up to EUR 4.50 (USD 5.09) per hour, a level that lifts turnover without expanding physical capacity.[2]Transport for London, “Cashless Parking,” tfl.gov.uk App-based payments deliver granular occupancy data now shared with planners to rebalance curb allocations among parking, loading, and cycle lanes. That feedback loop embeds analytics at the heart of rate-setting and compliance policy.

Emergence Of Curbside Logistics Hubs For Micro-Fulfillment

Rapid-delivery operators need curb access measured in minutes rather than hours. Amsterdam and Berlin piloted dual-use loading bays that revert to public parking outside peak delivery windows. Garage owners lease under-utilized surface lots to 15-minute grocery services, trading low-margin daytime parking for higher-yield logistics contracts. Time-banded permits mitigate friction with taxis and residents but require new software layers to police usage windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit Costs For EV Readiness | -1.8% | EU-wide, acute in Italy, Spain, Poland | Short term (≤ 2 years) |

| Modal Shift To Active And Shared Mobility | -1.4% | Netherlands, Belgium, Germany, urban France | Medium term (2-4 years) |

| Stricter On-Street Space Removal | -1.1% | United Kingdom, France, Spain, Netherlands | Medium term (2-4 years) |

| AI-Based Enforcement Errors | -0.9% | United Kingdom, Germany, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs For EV-Ready Infrastructure

Many multi-story garages built before 2010 lack transformer capacity for multiple fast chargers, forcing pricey grid upgrades that can delay projects up to 18 months. Grant schemes in Italy and Spain reimburse up to 40% of capital outlay but suffer from oversubscription and complex paperwork. Smaller surface-lot owners in secondary cities struggle to finance retrofits without proven utilization forecasts. Software integration mandated by AFIR real-time pricing display and contactless payment acceptance adds further burden to legacy ticketing systems.

Modal Shift To Active And Shared Mobility

Bike-sharing trips grew at double-digit rates in 2024 and 2025, with Paris and Barcelona network bikes averaging more than five daily rides. E-scooter fleets exceeded 200,000 units by mid-2025, and car-sharing operators expanded vehicle pools 15% year on year. In Dutch cities where over 40% of commuters cycle, demand for short-stay parking contracts sharply, pushing operators toward suburban and residential niches that still favor private-car ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Area: Platforms Unlock Idle Inventory

Peer-to-peer platforms digitize fragmented capacity, letting property owners monetize spaces during evenings and weekends. The Europe car parking market size for parking operators stood at 46.23% in 2025, yet platform players are growing 11.26% annually, narrowing the gap. Traditional operators rely on long-term municipal concessions, but users increasingly favor app-based booking that can undercut posted rates by up to 30%. Integration APIs offered by infrastructure vendors now let incumbents white-label their own apps, blurring lines between categories. Compliance questions persist, as some cities classify P2P income as commercial activity subject to tax, while others treat it as ancillary property use, creating a patchwork regulatory map.

Second-order effects include rising adoption of dynamic pricing among asset-heavy operators keen to emulate the elasticity benefits enjoyed by digital rivals. JustPark surpassed 2 million registered spaces in 2025, proving that residential driveways and under-filled office lots can meaningfully expand urban inventory. Infrastructure suppliers capture upside across both camps, selling sensor kits, ANPR cameras, and reservation software that shorten payback periods even as hardware costs fall.

By Parking Site: Curb Digitization Accelerates On-Street Growth

Off-street facilities surface, multi-story, and underground held 63.82% share of the Europe car parking market in 2025. Underground garages command premium tariffs in heritage districts where above-ground development is restricted. However, on-street inventory is forecast to expand at a 11.48% CAGR, faster than any other site class, as sensor grids feed real-time data into municipal pricing engines. London’s cashless expansion in 2025 produced a visibility step-change, enabling boroughs to triage curb space among EV charging, bike lanes, and loading bays with minute-level precision.

Operators of private garages respond by upgrading user experience app pre-booking, frictionless entry, and bundled charging to justify higher hourly fees relative to increasingly convenient curb slots. Policies such as Paris’ plan to remove 60,000 on-street spaces by 2030 cut raw supply but push per-space revenue higher as scarcity intensifies. The competitive dynamic thus pivots on delivering convenience and ancillary services rather than pure capacity.

By Technology: Smart Platforms Become The Default

Smart solutions captured 57.11% of 2025 revenue and are projected to grow 11.74% annually through 2031. IoT sensors combine with mobile payments to cut average search time by up to 40%, directly improving city air quality by reducing circulation. GDPR compliance forces operators to anonymize license-plate data, a requirement that is accelerating consolidation toward vendors that can demonstrate privacy-by-design architectures.[3]European Commission, “GDPR,” ec.europa.eu Conventional ticket-driven systems linger in rural markets where payback horizons remain long, but AFIR’s contactless-payment clause and rising consumer intolerance for coins and paper tickets place an end-of-life timeline on legacy hardware.

Advertising on entrance screens, data licensing to mapping services, and V2G participation add incremental revenue layers that tilt return-on-investment math further in favor of smart platforms. Operators that upgrade now lock in optionality to bid into future flexibility markets once national regulators finalize compensation frameworks.

By End-User Type: Residential Demand Surges On Building Codes

Municipalities still dominate end-user demand at 38.22% because they control on-street assets and civic garages. Yet residential complexes post the fastest expansion, at 12.01% CAGR, propelled by codes obliging new multifamily blocks to install a minimum proportion of chargers. Germany’s GEIG stipulates one charger for every two spaces in larger developments, a rule mirrored in the Netherlands and France. ParkBee partners with developers to embed license-plate recognition at the design stage, eliminating physical keys and reducing operating costs.

Transportation hubs upgrade premium products valet, covered bays, guaranteed chargers to serve business travelers, while hospitals experiment with off-site satellite lots to relieve chronic congestion. Commercial malls hedge e-commerce risk by validating customer parking, subsidizing tariffs to preserve footfall. The divergent needs across end-user groups create a layered opportunity set for suppliers ranging from hardware installers to payment-service providers.

Geography Analysis

Germany held 19.53% of the Europe car parking market in 2025, anchored by national EV-readiness mandates and city-level smart-parking budgets. Berlin, Munich, Hamburg, and Frankfurt all expanded sensor grids in 2025, and EVs reached 30% of new registrations that year. Poland’s 11.74% CAGR outlook is buoyed by EU regional funds underwriting pilots in Warsaw, Kraków, and Wrocław, combined with rising household car ownership. The United Kingdom sustains momentum via the widening of ultra-low-emission zones and obligatory cashless payments, measures that standardize technology adoption despite post-Brexit regulatory divergence.

France’s national low-emission framework funnels demand into compliant urban cores but suppresses it in fringe zones where combustion vehicles still dominate. Italy and Spain leverage tourism rebounds to lift revenue, though historic-center retrofits face cost overruns due to narrow street grids and heritage protections. The Netherlands and Belgium run V2G pilots and host some of Europe’s most advanced digital-twin deployments, placing them at the cutting edge of data-centric management. Sweden’s congestion charges in Stockholm and Gothenburg stabilize volume growth, capping peaks while ensuring predictable weekday demand.

Smaller markets Austria, Denmark, Portugal, Czech Republic exhibit mixed trajectories. Denmark’s cycling culture curbs parking demand in Copenhagen, whereas Portugal’s Algarve posts strong seasonal spikes tied to beach tourism. AFIR supplies a harmonized foundation, yet municipal zoning, congestion pricing, and building codes dictate local ceilings, compelling operators to tailor strategies city by city.

Competitive Landscape

The top five operators APCOA Parking, Indigo Group, Q-Park, EuroCarParks, National Car Parks control roughly 35-40% of the Europe car parking market, leaving the remainder split among municipalities, independents, and digital apps. Incumbents shore up defenses by acquiring charge-point operators and software houses, bundling electrification with long-term concessions that secure cash flows for up to two decades. APCOA integrated EasyPark payments across its estate in 2025, while Indigo bought a majority stake in ParkVia to tap P2P growth.

Digital-first challengers JustPark, EasyPark, ParkMobile, RingGo win transient users through frictionless interfaces and algorithmic pricing. Smaller sensor vendors like Urbiotica seed under-utilized private garages with equipment, converting dormant real estate into app-bookable capacity without owning bricks and mortar. Compliance with ISO 15118 for bidirectional charging is emerging as table stakes for V2G aggregation, signaling that technical certification will join location and scale as a key competitive axis.

Litigation risk over ANPR misreads, especially in the United Kingdom where 30% of appeals were upheld in 2024, forces investment in audit trails and human review. Those additional overheads widen the gap between well-capitalized players and small proprietors using generic camera software, accelerating consolidation in the years ahead.

Europe Car Parking Industry Leaders

APCOA Parking Holdings GmbH

Indigo Group SA

Q-Park NV

Euro Car Parks Limited

National Car Parks Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: APCOA Parking partnered with Allego to deploy 1,000 fast chargers across sites in Germany, France, and the United Kingdom, targeting completion by end-2027.

- December 2025: Indigo Group acquired a 60% stake in ParkVia, adding 500,000 users and expanding digital reach.

- November 2025: Q-Park won a 15-year concession at Amsterdam Schiphol Airport covering 3,500 spaces and 400 future chargers.

- October 2025: EasyPark Group raised EUR 50 million (USD 56.5 million) to fund expansion into Poland, Czech Republic, and Romania.

Europe Car Parking Market Report Scope

The Europe Retail Analytics Market is witnessing significant growth, driven by the increasing adoption of advanced analytics tools to enhance decision-making processes, optimize operations, and improve customer experiences. Retailers across the region are leveraging analytics to gain insights into consumer behavior, streamline supply chains, and boost profitability. The market is also benefiting from the growing penetration of e-commerce and omnichannel retail strategies, which demand robust analytics solutions to manage complex operations effectively.

The Europe Car Parking Market Report is Segmented by Application Area (Parking Operators and Management Companies, Infrastructure Providers, P2P Parking Apps Providers), Parking Site (On-Street Parking, Off-Street Parking including Surface Lots, Multi-Storey Garages, Underground Facilities), Technology (Conventional Parking Solutions, Smart Parking Solutions), End-User Type (Municipalities and Local Councils, Commercial Establishments and Retail, Transportation Hubs, Residential Complexes, Healthcare Facilities), and Geography (United Kingdom, Germany, France, Italy, Spain, Netherlands, Belgium, Sweden, Poland, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Parking Operators / Management Companies |

| Infrastructure Providers (Hardware and Software) |

| P2P Parking Apps Providers |

| On-Street Parking | |

| Off-Street Parking | Surface Lots |

| Multi-Storey Garages | |

| Underground Facilities |

| Conventional Parking Solutions |

| Smart Parking Solutions |

| Municipalities and Local Councils |

| Commercial Establishments and Retail |

| Transportation Hubs (Airports, Rail, Ports) |

| Residential Complexes |

| Healthcare Facilities |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Sweden |

| Poland |

| Rest of Europe |

| By Application Area | Parking Operators / Management Companies | |

| Infrastructure Providers (Hardware and Software) | ||

| P2P Parking Apps Providers | ||

| By Parking Site | On-Street Parking | |

| Off-Street Parking | Surface Lots | |

| Multi-Storey Garages | ||

| Underground Facilities | ||

| By Technology | Conventional Parking Solutions | |

| Smart Parking Solutions | ||

| By End-User Type | Municipalities and Local Councils | |

| Commercial Establishments and Retail | ||

| Transportation Hubs (Airports, Rail, Ports) | ||

| Residential Complexes | ||

| Healthcare Facilities | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will the Europe car parking market be by 2031?

It is forecast to reach USD 11.43 billion by 2031 at a CAGR of 10.59% from 2026 to 2031.

Which technology segment is expanding the fastest?

Smart parking solutions are advancing at 11.74% CAGR as IoT sensors and mobile payments become standard across European cities.

Why is residential parking demand growing so quickly?

Building codes in Germany, France, and the Netherlands now mandate EV-ready spaces in new multifamily projects, driving a 12.01% CAGR for residential complexes.

What role do peer-to-peer platforms play in the market?

Platforms such as JustPark convert idle private spaces into inventory, growing 11.26% annually and challenging asset-heavy incumbents.

Which country is the fastest-growing national market?

Poland is expected to post a 11.74% CAGR, supported by EU co-financing for smart parking pilots and rising car ownership.

How are operators monetizing electric-vehicle charging assets?

Many now partner with charge-point companies and participate in V2G programs that pay for feeding power back to the grid during peak periods.

Page last updated on: