Europe Sesame Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

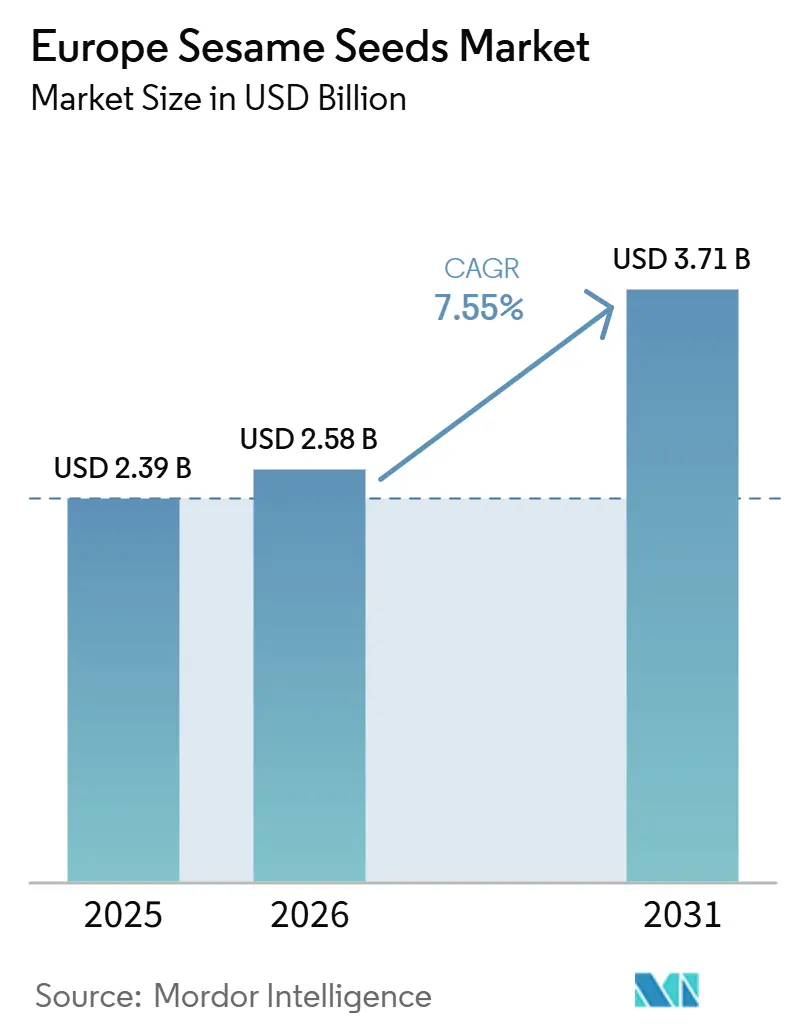

| Base Year Market Size (2025) | USD 2.39 Billion |

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

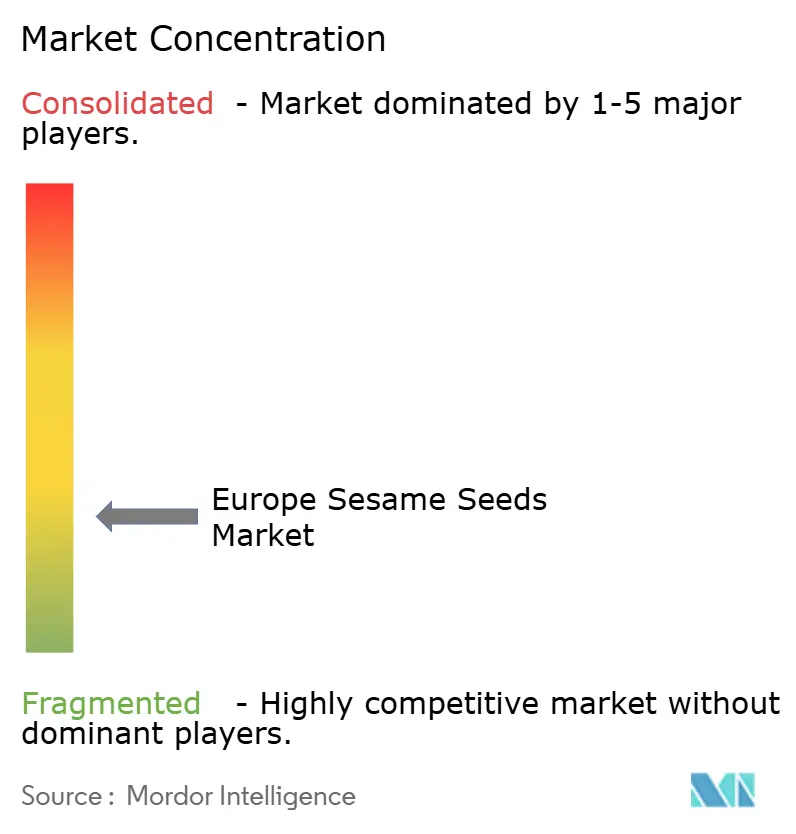

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Sesame Seeds Market Analysis by Mordor Intelligence

The Europe sesame seeds market size is projected to expand from USD 2.39 billion in 2025 and reach USD 2.58 billion in 2026 and USD 3.71 billion by 2031, registering a CAGR of 7.55% between 2026 and 2031. This growth trajectory reflects the increasing integration of sesame seeds into European food systems, driven by rising health consciousness and the expansion of ethnic cuisines across the continent. The market's resilience stems from sesame's dual role as both a traditional Mediterranean ingredient and an emerging superfood in Northern European markets. Germany’s strong bakery industry, expanding vegan product lines, and extensive import infrastructure anchor demand, while Poland’s rising disposable incomes and westernizing diets accelerate adoption. Suppliers gain pricing power in premium sub-segments such as black and organic variants, and processors capture value through upgraded post-harvest technologies that safeguard quality. Meanwhile, tightening EU food-safety rules and climate-induced crop risks add cost pressures that favor efficient, compliant operators.

Key Report Takeaways

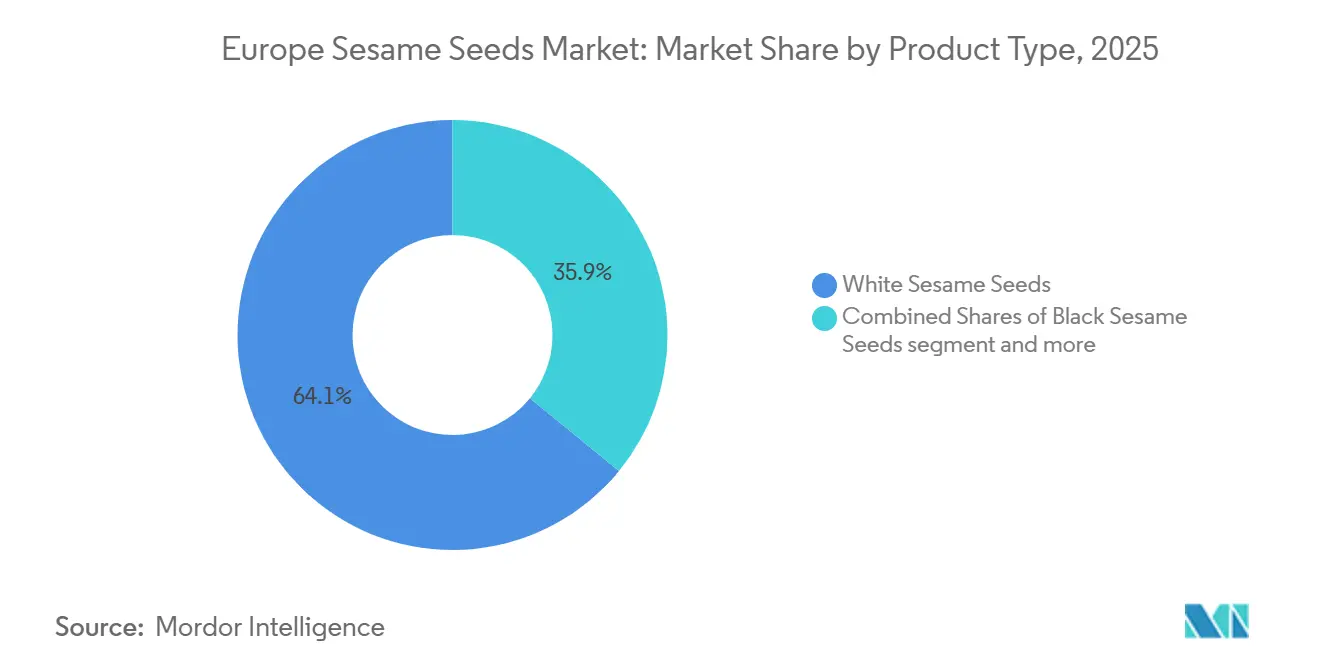

- By product type, consumer preference kept white seeds in the lead with 64.11% of the sesame seeds market share in 2025, whereas black sesame advanced at a 7.76% CAGR through 2031.

- By category, conventional offerings held 84.37% share of the sesame seeds market size in 2025, while certified organic variants are projected to expand at a 8.33% CAGR to 2031.

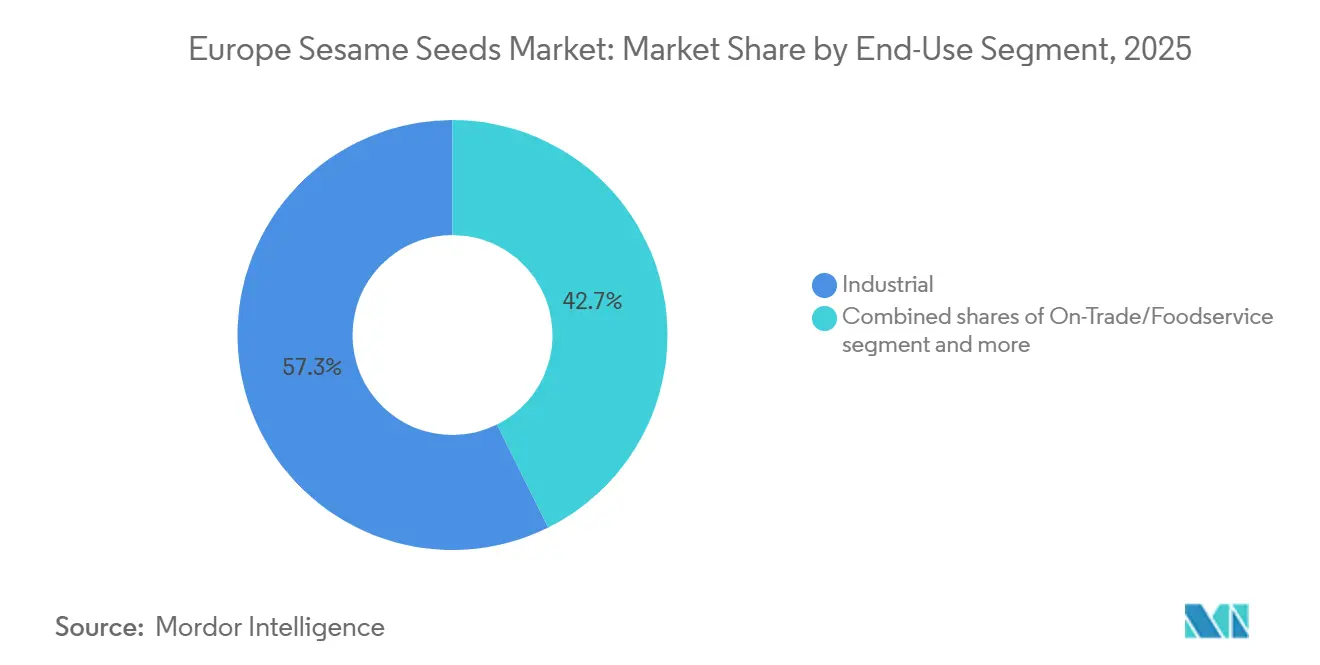

- By end-use segment, industrial segment controlled 57.34% of the sesame seeds market share in 2025; on-trade foodservice posts the fastest 9.04% CAGR to 2031.

- By geography, Germany dominated with 40.77% sesame seeds market share in 2025, whereas Poland posted the quickest 9.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on sesame seed market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Sesame Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in antioxidant-rich superfood demand | +1.5% | Global, with strongest uptake in Germany, Netherlands, United Kingdom | Medium term (2-4 years) |

| Expanding use in bakery and confectionery items within foodservice | +1.2% | Western Europe core, expanding to Eastern Europe | Short term (≤ 2 years) |

| Rising demand for organic and sustainable products | +0.8% | Global, with early adoption in Netherlands, Germany | Long term (≥ 4 years) |

| Surge in demand for sesame oil | +0.6% | Northern Europe lead, spreading to Southern Europe | Medium term (2-4 years) |

| Rising demand for tahini and sesame paste | +0.4% | Processing hubs in Netherlands, Germany, Belgium | Long term (≥ 4 years) |

| Increasing investment in modern processing facilities | +0.3% | Urban centers across Europe, strongest in United Kingdom, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in antioxidant-rich superfood demand

European consumers increasingly prioritize functional foods that deliver measurable health benefits, positioning sesame seeds as a strategic ingredient for manufacturers targeting the wellness segment. Sesame's rich profile of lignans, healthy fats, and plant proteins aligns with consumer demands for natural alternatives to synthetic supplements. The shift toward plant-based diets has elevated sesame from a garnish to a core ingredient in protein-rich formulations, particularly in Germany and the Netherlands, where health-conscious consumption patterns are most established. Research indicates that sesame's unique combination of sesamin and sesamolin compounds provides cardiovascular benefits that resonate with aging European populations. This health positioning creates pricing power for premium sesame products, enabling suppliers to capture higher margins while expanding market penetration beyond traditional ethnic food channels.

Expanding use in bakery and confectionery items within foodservice

The European foodservice sector's embrace of sesame seeds reflects broader menu diversification strategies aimed at differentiating offerings in competitive urban markets. Artisanal bakeries increasingly incorporate sesame into signature bread formulations, while confectionery manufacturers leverage sesame's nutty flavor profile to create premium chocolate and dessert products. This trend extends beyond traditional Mediterranean markets into Northern European cities, where Asian fusion concepts drive sesame adoption in unexpected applications. McCormick & Company's 2024 SEC filing highlights significant EMEA operations growth, with the company noting increased demand for specialty seeds and spices across European foodservice channels. The foodservice channel's willingness to pay premium prices for consistent quality creates opportunities for suppliers to establish long-term partnerships that stabilize revenue streams while building brand recognition among end consumers.

Surge in demand for sesame oil

A surge in demand for sesame oil directly increases the requirement for raw sesame seeds, as oil extraction is one of the largest consumption applications. Rising use of sesame oil in cooking, especially in Asian and Middle Eastern cuisines, is boosting processing volumes. Additionally, growing consumer preference for healthy, plant-based oils rich in antioxidants and unsaturated fats is further driving demand. This leads to higher procurement by oil manufacturers, strengthening the supply chain for sesame seeds. As oil consumption expands globally, it creates consistent, large-scale demand, thereby supporting overall sesame seed market growth. It also encourages farmers to increase sesame cultivation, improving overall production volumes. Furthermore, higher oil demand can lead to price stability or upward price trends, making sesame farming more economically attractive.

Rising demand for organic and sustainable products

The European Union's ambitious target of converting 25% of agricultural land to organic farming by 2030 creates structural demand growth for certified organic sesame seeds, particularly as new regulations effective January 2025 tighten certification requirements [1]Source: CBI (Centre for the Promotion of Imports from developing countries), "New EU organic rules put a mark on small producers of grains and oilseeds", cbi.eu. Organic sesame imports to Europe grew from 15,000 to 22,000 tonnes between 2019 and 2022, representing 6.7% of total sesame oil imports, indicating strong consumer willingness to pay premiums for certified products [2]Source: CBI (Centre for the Promotion of Imports from developing countries), "The European market potential for sesame oil for food", cbi.eu. This growth trajectory accelerates as major food manufacturers integrate sustainability commitments into procurement strategies, creating predictable demand for certified suppliers. The regulatory framework's emphasis on traceability and environmental impact measurement favors established suppliers with robust certification systems, potentially consolidating market share among compliant producers while creating barriers for smaller, uncertified competitors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate change and weather variability impacting crop yields | -0.9% | Global production regions, affecting European imports | Long term (≥ 4 years) |

| Strict international food safety and quality standards | -0.7% | European Union-wide, with strictest enforcement in Germany, Netherlands | Short term (≤ 2 years) |

| Competition from alternative plant-based seeds and oils | -0.5% | Northern Europe primarily, spreading to Western Europe | Medium term (2-4 years) |

| Consumers have concerns over potential contamination | -0.3% | European Union-wide, heightened in countries with recent incidents | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate change and weather variability impacting crop yields

Climate variability increasingly disrupts sesame production in key supply regions, creating price volatility that constrains European market growth by making sesame less competitive against stable-priced alternatives. Research indicates that climate change affects seed morphological, physiological, and biochemical quality, with dicotyledonous crops like sesame showing particular vulnerability to temperature and drought stresses. Poland's agricultural sector faces drought risks affecting a significant portion of farmland, illustrating the broader European vulnerability to climate impacts that could affect future local sesame cultivation attempts. Production disruptions in major exporting countries like India and Nigeria create supply chain uncertainties that European buyers increasingly factor into procurement strategies, potentially favoring more expensive but reliable suppliers. The resulting price premiums may limit sesame adoption in price-sensitive applications, constraining overall market expansion despite growing demand for healthy ingredients.

Strict international food safety and quality standards

European food safety regulations create compliance costs and market access barriers that particularly impact smaller sesame suppliers, potentially limiting supply diversity and increasing prices for European buyers. Recent Salmonella outbreaks linked to sesame-based products from Syria affected 121 cases across 5 EU countries, demonstrating the ongoing contamination risks that drive regulatory scrutiny [3]Source: European Centre for Disease Prevention and Control, " Multi-country outbreak of multiple Salmonella enterica serotypes linked to imported sesame-based products", ecdc.europa.eu. The February 2025 detection of mycotoxins in sesame seeds from Mexico highlights persistent quality control challenges that trigger regulatory responses and supply chain disruptions. New allergen labeling requirements for unpackaged and bulk foods, including sesame, add compliance complexity for foodservice operators and retailers. These regulatory pressures favour large, established suppliers with robust quality systems while potentially excluding smaller producers who cannot meet stringent certification requirements, ultimately constraining supply competition and maintaining higher prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Black Sesame Commands Premium Growth

Black sesame seeds drive the fastest segment growth at 7.76% CAGR through 2031, despite white sesame maintaining a dominant 64.11% market share in 2025. The premium positioning of black sesame reflects consumer perception of superior nutritional density and antioxidant content, enabling price premiums that attract quality-focused suppliers. White sesame's market leadership stems from its versatility across applications, from traditional Mediterranean tahini production to modern bakery formulations where neutral color profiles are preferred. Brown and mixed varieties occupy niche positions, primarily serving specialty ethnic food channels and artisanal producers seeking differentiated offerings.

The color-based segmentation reveals strategic opportunities for suppliers to capture value through product positioning rather than volume competition. Research on sesame oil cake applications in pasta demonstrates how even by-products from sesame processing can enhance nutritional profiles, with sesame oil cake addition significantly increasing protein and fiber content while maintaining acceptable sensory characteristics. This innovation potential extends across the product spectrum, where black sesame's visual appeal and perceived health benefits create opportunities for premium product development in categories ranging from confectionery to functional foods.

By Category: Organic Certification Drives Value Migration

Conventional sesame seeds maintain 84.37% market share in 2025, reflecting the category's price sensitivity and established supply chains, while organic sesame achieves 8.33% CAGR growth through 2031 as regulatory changes and consumer preferences align. The EU's stricter organic regulations, effective January 2025, create both opportunities and challenges, potentially constraining supply from smaller producers while rewarding established organic suppliers with premium pricing power. Organic sesame imports to Europe grew from 15,000 to 22,000 tonnes between 2019 and 2022, demonstrating sustained demand growth despite higher prices.

The organic premium reflects more than consumer willingness to pay higher prices; it represents a fundamental shift toward supply chain transparency and environmental accountability that reshapes competitive dynamics. The EU's target of 25% organic farmland by 2030 creates structural demand that exceeds current organic sesame supply capacity, suggesting sustained pricing power for certified producers. This supply-demand imbalance favors suppliers who can navigate complex certification requirements while maintaining consistent quality and traceability standards that meet European regulatory expectations.

By End-Use Segment: Foodservice Expansion Outpaces Retail

On-trade channels achieve 9.04% CAGR growth through 2031, outpacing off-trade retail despite Industrial's dominant 57.34% market share in 2025. This growth differential reflects the foodservice sector's role as an innovation driver, where chefs and menu developers introduce sesame applications that later migrate to retail channels. The foodservice channel's willingness to pay premiums for consistent quality and specialized varieties creates opportunities for suppliers to establish relationships that provide market intelligence and product development insights. Within retail channels, supermarkets and hypermarkets maintain dominant positions, while online retail stores show accelerated growth driven by convenience and specialty product access.

The industrial segment is the largest end-user of sesame seeds due to its extensive use in large-scale food processing applications such as oil extraction, bakery products, confectionery, and tahini production. Sesame oil manufacturing alone consumes a significant share of global sesame output, driving bulk demand from processors. Additionally, food manufacturers use sesame seeds as ingredients, toppings, and flavor enhancers across a wide range of packaged foods. Industrial buyers procure in large volumes through long-term contracts, ensuring consistent demand. The scalability and continuous production requirements of the food processing industry further strengthen its dominance over retail and foodservice segments.

Geography Analysis

Poland leads geographic growth at 9.25% CAGR through 2031, while Germany maintains market leadership with 40.77% share in 2025, illustrating the market's expansion from established Western European bases into emerging Eastern European markets. Germany's dominance reflects its economic scale, diverse food industry, and established import infrastructure that positions it as a distribution hub for broader European markets. The Netherlands, France, and Italy represent mature markets with stable consumption patterns, while Spain shows growing adoption driven by increasing ethnic diversity and culinary experimentation. Belgium and Sweden occupy smaller but strategically important positions as gateway markets for Nordic and Benelux expansion.

The geographic expansion pattern reveals opportunities for suppliers to capture growth by adapting to regional preferences and regulatory requirements. Poland's rapid growth reflects broader Eastern European economic development and dietary westernization trends that favor premium ingredients like sesame seeds. However, climate risks affect agricultural productivity across Europe, with Greece facing potential annual losses by 2060 due to climate change impacts on agriculture. These regional vulnerabilities suggest that successful suppliers must develop flexible sourcing strategies that can adapt to changing production patterns while maintaining consistent supply to growing markets.

The United Kingdom, Italy, France, Spain, Netherlands, Belgium, and Sweden represent mature markets with distinct characteristics that influence sesame consumption patterns. The UK's diverse population and established ethnic food markets create steady demand for traditional sesame applications, while Italy's culinary innovation drives adoption in Mediterranean fusion concepts. France's premium food culture supports high-quality sesame products, particularly in artisanal and organic segments. Spain shows growing consumption driven by increasing cultural diversity and health consciousness among urban populations. The Netherlands serves as a key trade hub with sophisticated import and distribution infrastructure, while Belgium's central location and food processing expertise create opportunities for value-added sesame products. Sweden represents Nordic market potential where health-focused consumers show increasing interest in functional ingredients like sesame seeds.

Competitive Landscape

The European sesame seeds market operates with low concentration, reflecting significant fragmentation among suppliers, processors, and distributors who compete across multiple value chain segments. This fragmentation creates opportunities for both large multinational companies and specialized regional players to capture market share through differentiated strategies. Some of the significant players include Dipasa Europe B.V., SunOpta, Olam Group, Haitoglou Bros S.A., and NOW® Foods, among others. Increasing demand for clean-label and sustainably sourced ingredients is pushing players to invest in certification and transparent sourcing practices. Competitive intensity is further shaped by price volatility and the need for consistent quality to meet stringent European food safety standards.

Major players like Cargill leverage global sourcing capabilities and processing scale to serve large industrial customers, while companies like Olam Group focus on sustainable sourcing and traceability systems that appeal to quality-conscious European buyers. The competitive dynamics favor suppliers who can navigate complex regulatory requirements while maintaining consistent quality and competitive pricing across diverse product applications. Europe relies heavily on imports from countries such as Sudan, Ethiopia, and India, making supply chain partnerships and traceability critical competitive factors. Companies differentiate through value-added offerings like organic, hulled, and ready-to-use sesame products for bakery and food processing industries.

Strategic patterns in the market emphasize vertical integration and sustainability credentials as key differentiators, with successful companies investing in direct farmer relationships and certification systems that ensure supply chain transparency. Olam Group's 2023 annual report highlights double-digit EBIT growth and significant sustainability initiatives, including the largest certified regenerative agriculture program in cotton supply chains, demonstrating how environmental commitments translate into competitive advantages . Technology adoption focuses on post-harvest processing innovations that improve yield, quality, and shelf life, while digital platforms enable direct customer relationships that bypass traditional distribution intermediaries. Opportunities exist in organic certification, specialty variety development, and value-added processing that transforms commodity sesame into premium ingredients for specific applications.

Europe Sesame Seeds Industry Leaders

-

Dipasa Europe B.V.

-

Haitoglou Bros S.A.

-

NOW® Foods

-

Olam International

-

SunOpta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazing Sesame, a brand celebrated for modernizing Asian culinary staples, launched its Black Sesame Sauce. This rich and aromatic condiment, rooted in centuries-old Taiwanese craftsmanship, promises a versatile and elevated flavor experience.

- January 2025: Elephant Harvest Brand unveiled its White Hulled Sesame seeds. This standout product came in various sizes: 1kg, 2kg, 5kg, and 25kg, catering to the diverse needs of its customers. The company marketed these seeds under the Elephant Harvest brand and also provided packaging services for several esteemed brands in the United Kingdom.

Europe Sesame Seeds Market Report Scope

The sesame seed market refers to the trade and consumption of sesame seeds used as raw materials in food processing, culinary applications, and oil extraction. The Europe Sesame Seeds Market is Segmented by Product Type (White, Black, and Others), Category (Organic and Conventional), End-Use Segment (Horeca/Foodservice, Industrial, and Off-Trade/Retail), Geography (Germany, United Kingdom, Italy, France, Spain, Netherlands, Poland, Belgium, Sweden, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| White |

| Black |

| Others |

| Organic |

| Conventional |

| Foodservice/HoReCa | |

| Industrial | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | White | |

| Black | ||

| Others | ||

| By Category | Organic | |

| Conventional | ||

| By End-Use Segment | Foodservice/HoReCa | |

| Industrial | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the European sesame sector in 2025?

The sesame seeds market size reached USD 2.39 billion in 2025 and is on track for a 7.55% CAGR to 2031.

Which country buys the most sesame in Europe?

Germany leads with 40.77% of regional demand owing to its sizable bakery and food-processing industries.

Which segment grows fastest through 2031?

On-trade foodservice rises at a 9.04% CAGR as Asian and Mediterranean restaurants add sesame-based dishes.

Why is black sesame gaining popularity?

Black seeds command a 7.76% CAGR because consumers perceive higher antioxidant content and chefs value their striking color.

Page last updated on: