Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.10 Billion |

| Market Size (2026) | USD 11.45 Billion |

| Market Size (2031) | USD 13.34 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Food Spread Market Analysis by Mordor Intelligence

European Food Spread market size in 2026 is estimated at USD 11.45 billion, growing from 2025 value of USD 11.10 billion with 2031 projections showing USD 13.34 billion, growing at 3.12% CAGR over 2026-2031. The market's moderate growth reflects its maturity while being sustained by product innovations and evolving consumer preferences. Food spreads have transformed from traditional breakfast accompaniments to versatile food solutions, finding applications in snacking and cooking. The market dynamics are significantly influenced by increasing health consciousness, with consumers gravitating toward nutritious options free from additives, preservatives, gluten, and trans-fat. This shift has amplified the demand for natural, low-sugar, and sugar-free variants. Additionally, the market's performance is closely linked to ethnic flavor preferences, consumer perceptions of raw materials, and bread consumption patterns across European households. Manufacturers are responding to these trends by developing premium and organic variants, particularly in established markets like Germany, France, and the United Kingdom. The rise of private label offerings and increased focus on sustainable packaging solutions further characterize the market's evolution in the region.

Key Report Takeaways

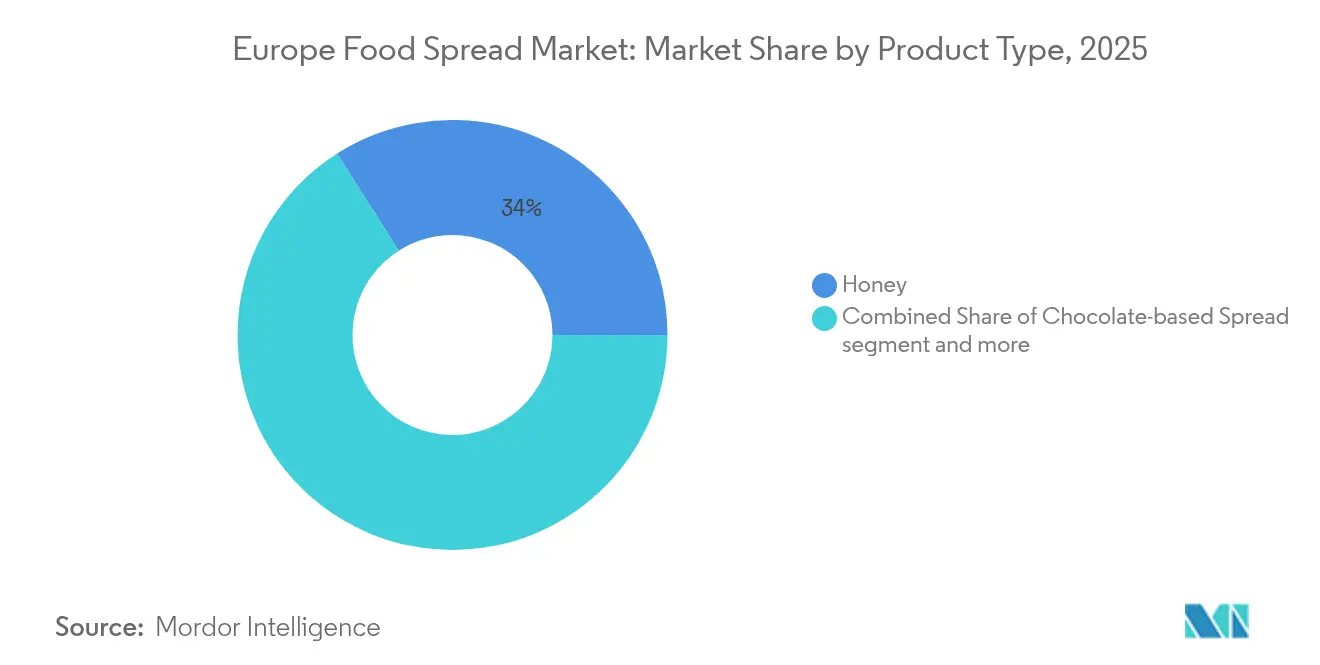

- By product type, honey captured 34.02% of the European food spread market share in 2025 and is poised to expand at an 8.25% CAGR between 2026-2031.

- By nature, the conventional segment retained 71.58% of the European food spread market in 2025; organic variants record the fastest growth at a 5.88% CAGR through 2031.

- By packaging type, jars led with 44.76% revenue in 2025, while sachets/pouches are forecast to post the highest 6.28% CAGR during 2026-2031.

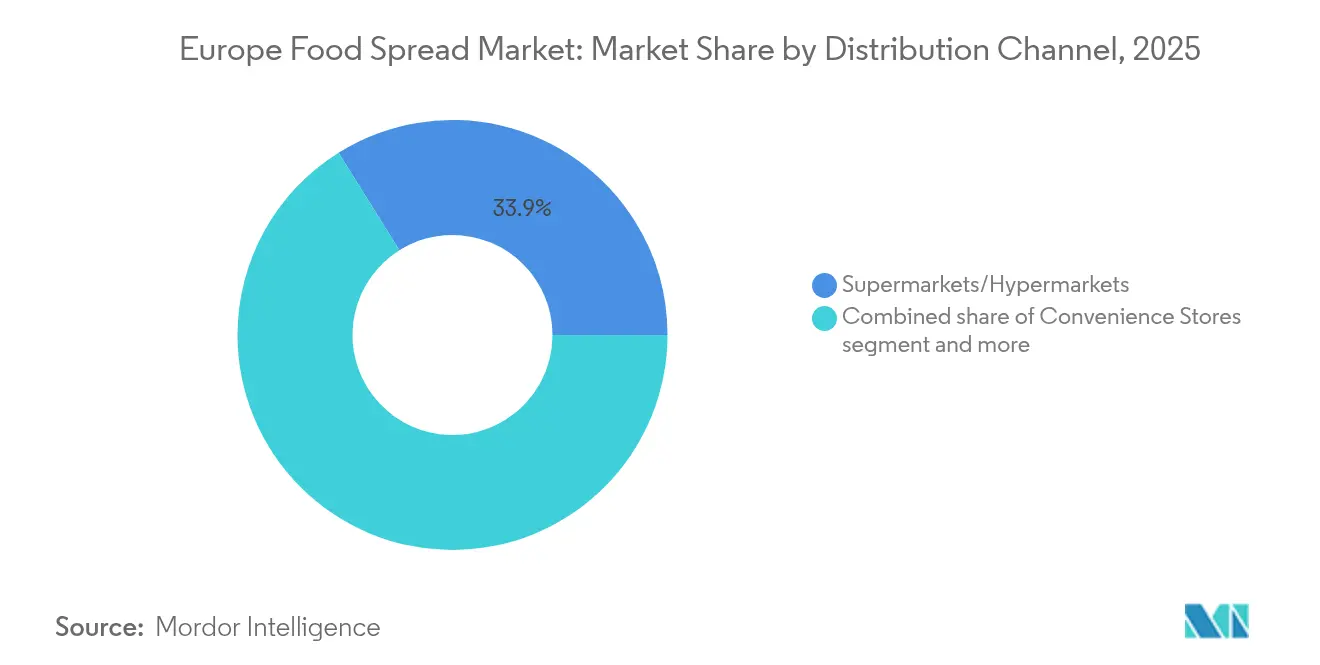

- By distribution channel, supermarkets/hypermarkets held 33.89% of the European food spread market size in 2025; online retail is projected to grow at a 7.22% CAGR to 2031.

- By geography, Germany commanded 14.05% revenue in 2025, whereas Poland is the fastest-growing market with a 5.94% CAGR outlook for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Food Spread Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Convenience-driven consumer lifestyles boost demand for versatile food options | +0.8% | Pan-European, with higher impact in Northern and Western Europe | Medium term (2-4 years) |

| Consumer interest in exotic and local fruit flavors stimulates product development | +0.7% | Western Europe, with spillover to Eastern Europe | Medium term (2-4 years) |

| Rise in plant-based diets increases demand for vegan spreads | +0.6% | Northern and Western Europe | Long term (≥ 4 years) |

| Strategic marketing and brand development impact market expansion | +0.5% | Pan-European | Medium term (2-4 years) |

| Growth in between-meal snacking expands spread usage occasions | +0.4% | Pan-European, with higher impact in urban centers | Short term (≤ 2 years) |

| Product innovation in flavors appeals to experimental consumers | +0.3% | Western and Northern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenience-driven Consumer Lifestyles Boost Demand for Versatile Food Options

The rise in fast-paced lifestyles across Europe has expanded the role of food spreads beyond breakfast items to versatile food products suitable for multiple consumption occasions. This adaptability supports market growth as consumers seek convenient, ready-to-use products for various uses, from morning toast to cooking and snacking. The demand for convenience is significant in dual-income households where time limitations increase the appeal of easy-to-use products. According to Eurostat, the EU's gross household adjusted disposable income reached EUR 12.63 trillion in 2023, enabling increased consumption of food spreads [1]Source: Eurostat, “Households – statistics on income, saving and investment,” ec.europa.eu. Product innovations that highlight multiple uses, such as spreads that function as dips, toppings, or cooking ingredients, have broadened the category's application across different meal occasions and consumer groups.

Consumer Interest in Exotic and Local Fruit Flavors Stimulates Product Development

European consumers' evolving preferences and growing interest in novel flavor experiences are driving innovation in fruit-based spreads. This trend manifests through exotic flavor exploration and hyperlocal ingredient sourcing, with tropical and international flavors appearing on European shelves alongside products emphasizing regional fruit varieties and traditional preparation methods. The March 2025 launch of Meghan Markle's As Ever Collection, featuring a signature raspberry spread, exemplifies this market evolution where manufacturers can create differentiation through both global exploration and local heritage narratives. This approach is particularly effective in the fruit spreads category, where sensory experiences and emotional connections significantly influence consumer purchase decisions.

Rise in Plant-based Diets Increases Demand for Vegan Spreads

The plant-based movement continues to reshape the European food landscape, with vegan spreads emerging as a high-growth segment that appeals beyond strict vegans to include flexitarians and health-conscious consumers. This growth is supported by innovations in ingredient technology that have significantly improved taste and texture profiles, enabling plant-based spreads to compete directly with conventional alternatives. A notable example is Arla's launch of a plant-based version of Lurpak butter in Denmark in August 2024, demonstrating how manufacturers are addressing previous barriers to adoption by focusing on sensory experience rather than solely ethical positioning. The market expansion is further driven by increased consumer awareness of environmental sustainability and animal welfare concerns, leading to a broader acceptance of plant-based alternatives in mainstream retail channels. Additionally, the development of clean-label formulations and the use of locally sourced ingredients have strengthened consumer trust and market penetration across European regions.

Strategic Marketing and Brand Development Impact Market Expansion

In the competitive food spread market, sophisticated brand storytelling and strategic marketing initiatives are becoming key differentiators. Ferrero's Nutella demonstrates this evolution from a product to a cultural phenomenon through consistent brand building and experiential marketing. The brand's strategic initiatives in 2025 included the celebration of World Nutella Day with a multi-faceted campaign featuring a new sonic identity, an exhibition at the MAXXI Museum in Rome, and a commemorative book detailing its history. Additionally, Nutella expanded its market presence by launching plant-based vegan spreads in September 2024. These comprehensive marketing efforts create emotional resonance beyond functional product attributes, fostering consumer loyalty that withstands competitive pressures.

Restraints Impact Analysis of Europe Food Spread Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising health concerns over sugar and fat content limit market growth | -0.4% | Pan-European, with higher impact in Northern Europe | Long term (≥ 4 years) |

| Fruit price fluctuations impact market development | -0.3% | Pan-European, with higher impact on Southern European producers | Medium term (2-4 years) |

| Consumer concerns about preservatives and palm oil affect product adoption | -0.3% | Western and Northern Europe, with strongest impact in Germany and Scandinavia | Medium term (2-4 years) |

| Private label competition and regional players challenge market share | -0.2% | Pan-European, with higher impact in price-sensitive Eastern European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health Concerns Over Sugar and Fat Content Limit Market Growth

Heightened consumer awareness of nutritional content and health implications challenges traditional food spreads manufacturers, as their products often contain high levels of sugar and fat that conflict with modern dietary guidelines. European consumers' increasing scrutiny of product labels, particularly regarding sugar content, stems from rising obesity rates and public health campaigns. The concern extends to fat composition, with palm oil in chocolate spreads facing criticism for both health and sustainability reasons. While manufacturers are reformulating products to reduce sugar, improve fat profiles, and incorporate functional ingredients, these modifications present cost and taste trade-offs that may affect consumer acceptance. The industry's ability to balance health demands with taste preferences will determine its success in maintaining market share in an increasingly health-conscious environment.

Fruit Price Fluctuations Impact Market Development

The volatility of fruit commodity prices introduces significant challenges for manufacturers of fruit-based spreads, affecting both production costs and planning capabilities. This instability stems from multiple factors, including climate change impacts on harvests, geopolitical disruptions to supply chains, and currency fluctuations affecting import costs. The situation is particularly critical in the European Union, which remains a net importer of many fruits used in sweet spreads, especially tropical varieties, as noted by the Centre for the Promotion of Imports from Developing Countries. This dependency on imported fruits exposes manufacturers to international market volatility, complicating long-term planning and potentially squeezing margins when cost increases cannot be fully passed to consumers, particularly in price-sensitive segments. These challenges can ultimately constrain product innovation and affect retail pricing strategies in the food spread sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Food Spread Market Segment Analysis

By Product Type:

Honey Dominates Through Perceived AuthenticityHoney dominates the European food spread market with a 34.02% share in 2025 and projects the highest category growth rate at 8.25% CAGR (2026-2031). This market leadership reflects honey's position as both a traditional food staple and a premium natural sweetener that meets current health-conscious consumer preferences. However, European honey production meets only 60% of market demand, requiring substantial imports from China and Ukraine to fill the supply gap, according to the EU Pollinator Hub, 2024 . The growing demand for organic and monofloral honey varieties has further strengthened honey's market position. Consumer awareness of honey's antibacterial and antioxidant properties has also contributed to its increased consumption as a functional food ingredient.

Chocolate-based spreads retain consumer preference through established brands like Nutella. Fruit-based spreads gain market share due to their health benefits and cooking versatility, while nut and seed-based spreads experience growth based on their protein content and health functionality. The market continues to develop with hybrid products that combine categories, such as cocoa-infused honey, attracting younger consumers seeking nutritious alternatives to traditional chocolate spreads. Premium and artisanal spread manufacturers are introducing innovative flavors and clean-label formulations to differentiate their products in the competitive market. The rise of breakfast-at-home trends during and after the pandemic has further boosted the consumption of various spread categories across European households.

By Nature:

Organic Growth Outpaces ConventionalConventional food spreads dominate the market with a 71.58% share in 2025, driven by established consumer preferences and widespread retail availability. However, the organic segment is experiencing faster growth, with a projected CAGR of 5.88% during 2026-2031. This growth reflects consumer preferences shifting toward products they consider healthier, sustainable, and of superior quality. The increasing awareness of ingredient sourcing and manufacturing processes has contributed to this trend, while competitive pricing strategies by manufacturers have made organic spreads more accessible to a broader consumer base.

The rise of organic food spreads aligns with EU initiatives like the Green Deal and Farm to Fork strategy, which aim to make 25% of farmland organic by 2030. These policies are boosting the availability of organic ingredients and driving innovation. Consumers are drawn to organic options mainly for health and safety reasons, with environmental benefits as a secondary factor. According to the CBI Ministry of Foreign Affairs, clean-label products are expected to make up over 70% of portfolios by 2025–2026, up from 52% in 2021 . As more farmers transition to organic methods, the supply of suitable raw materials for spread producers continues to grow.

By Packaging Type:

Jars Retain Premium ImageJars dominate the European food spread market with a 44.76% share in 2025, as consumers associate them with premium quality and sustainability. Their strong recyclability credentials align with environmental concerns and regulatory requirements, while sachets/pouches show the highest growth potential at 6.28% CAGR (2026-2031) by catering to convenience and portion control needs, particularly among younger consumers and urban professionals seeking portable options. Glass jars, in particular, maintain their market leadership position due to their ability to preserve product freshness and extend shelf life.

The packaging landscape is further shaped by tubs, which maintain steady market presence through resealability advantages, while cups, cans, and tetra packs serve specific distribution channels and niche applications. Across all formats, packaging innovation focuses on functionality and environmental considerations, emphasizing material reduction, recyclability, and renewable sourcing. Manufacturers are investing in smart packaging with tamper-evident features and better barrier properties. Easy-open and reclosure mechanisms are now standard, addressing convenience without compromising product protection.

By Distribution Channel:

Online Retail Disrupts Traditional DominanceSupermarkets and hypermarkets remain the dominant distribution channel for food spreads, holding a 33.89% market share in 2025. These retailers benefit from extensive product selections, promotional capabilities, and shopping convenience. The online retail segment is growing rapidly, with a projected CAGR of 7.22% during 2026-2031, challenging traditional retail dominance. The widespread presence of supermarket chains across urban and suburban areas enables easy access to a diverse range of food spread. Additionally, these retail formats offer competitive pricing and frequent discounts, making them attractive to price-conscious consumers.

Convenience stores cater to urban consumer demands with accessibility and quick purchases. Specialty food outlets and direct-to-consumer platforms are emerging as key avenues for premium and artisanal food spreads. Omnichannel strategies integrating physical stores with digital platforms enhance customer experiences. Mobile apps and loyalty programs reinforce the role of convenience stores, while specialty food stores create opportunities for local and regional food spread producers to reach niche markets.

Geography Analysis

Germany Food Spread Market

Germany maintains its leadership in the European food spread market with a 14.05% share in 2025, supported by its substantial population, high disposable incomes, and sophisticated retail infrastructure. The market shows a strong inclination toward premium and organic products, with sustainability becoming a key purchasing factor. This is exemplified by Zentis' collaboration with thyssenkrupp in August 2024, implementing CO2-reduced tinplate for NaturRein fruit spread closures, resulting in up to 69% lower emissions compared to traditional methods. German consumers particularly favor honey and chocolate spreads, with growing demand for artisanal and local products that offer unique flavors and authentic production narratives.

Broader European Markets

Poland stands out as the market's fastest-growing region, with an expected CAGR of 5.94% from 2026 to 2031, driven by increasing disposable incomes, westernization of consumption patterns, and retail sector modernization. The United Kingdom maintains its significant market position, particularly in breakfast spreads and premium nut butters. France and Italy's market strength stems from their rich culinary traditions, emphasizing high-quality ingredients and authentic production methods in sweet spread applications beyond breakfast consumption. Several European countries exhibit distinct market characteristics and growth patterns. Spain's market potential increases through growing health awareness and expanding retail distribution, while the Netherlands leverages its position as a major trade hub for spread ingredient imports. Belgium's market benefits from its chocolate manufacturing heritage, and Sweden shows strong performance in organic and health-focused variants. Other European markets, including Austria, Denmark, and emerging Eastern European nations, display varied growth trajectories influenced by their respective economic conditions, cultural preferences, and retail sector development.

Regulatory Landscape

Food spreads sold in Europe operate under the EU food law framework, with the European Commission (DG SANTE) setting horizontal rules and EFSA supporting risk assessment for food safety. Mandatory consumer information is governed by Regulation (EU) No 1169/2011, which drives label-led reformulation and portfolio choices across sweet and savory spreads through nutrition declarations and allergen information. Origin-related requirements also apply where primary ingredient origin differs from the food origin under Implementing Regulation (EU) 2018/775.

Product and claims positioning is further shaped by category-specific definitions for spreadable fats under Council Regulation (EC) No 2991/94, while hygiene compliance is anchored in EU hygiene rules such as Regulation (EC) No 852/2004. In 2025, the European Commission introduced a cross-cutting legislative simplification package (SWD(2025) 1030 final) covering multiple food regulations, signaling reduced administrative burden alongside unchanged safety expectations. The Commission also ran a 2026 EU labelling campaign focused on clarity, with enforcement attention on label accuracy and consumer understanding.

Competitive Landscape

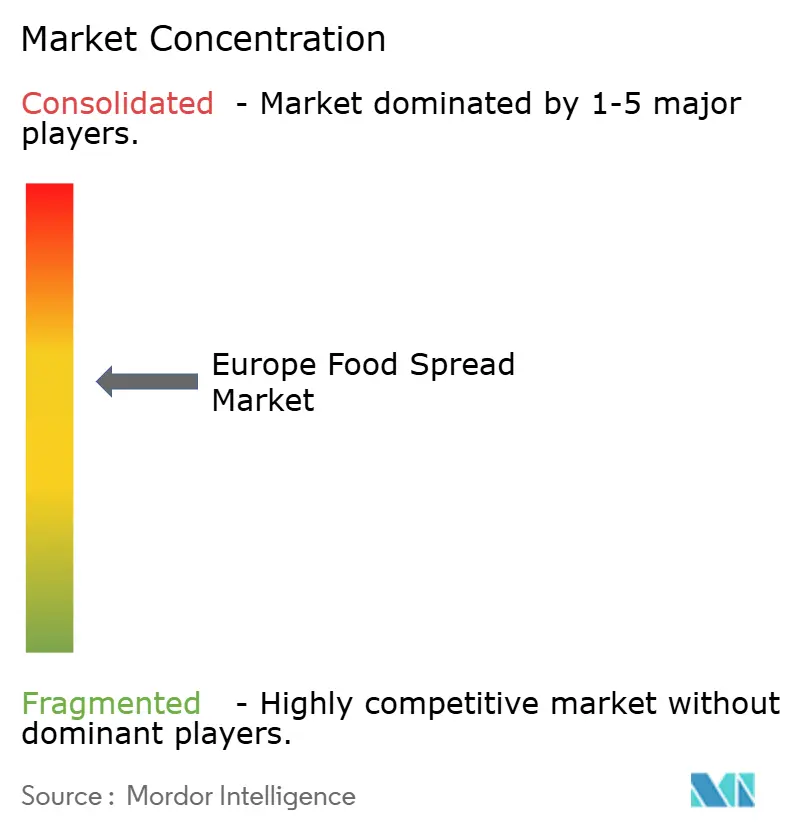

The European food spread market exhibits moderate consolidation, with a mix of established multinational companies, specialized regional producers, and growing private label offerings. Key market players include Hero Group, Unilever PLC, Andros, Ferrero International S.A., and Orkla ASA, which maintain significant market presence through their diverse product portfolios. These companies leverage their established distribution networks and brand recognition to maintain their competitive positions. The market also sees increasing participation from smaller, specialized manufacturers who focus on niche segments and regional preferences.

Market opportunities are emerging in several segments, particularly in functional spreads with enhanced nutritional benefits, plant-based alternatives catering to vegan and flexitarian consumers, and premium artisanal products featuring distinct ingredients and production techniques. These segments represent potential growth areas for both established players and new entrants. Consumer demand for clean-label products and transparent ingredient sourcing continues to drive innovation in the market. Additionally, the growing preference for sustainable packaging solutions presents opportunities for manufacturers to differentiate their offerings.

Companies are actively pursuing market expansion through strategic acquisitions, as demonstrated by KP Snacks' acquisition of Whole Earth Foods Limited from the Ecotone group in November 2024. This strategic move enhanced KP Snacks' presence in the European food spread market while expanding its healthy product range and complementing its existing snack brand portfolio. The acquisition trend reflects the industry's focus on portfolio diversification and market consolidation. Market players are also investing in research and development to introduce innovative products that align with evolving consumer preferences.

Europe Food Spread Industry Leaders

Hero Group

Unilever PLC

Ferrero International S.A.

Orkla ASA

Andros Group

- *Disclaimer: Major Players sorted in no particular order

Europe Food Spread Market Companies Covered in this Report

- Andros Group

- Ferrero International S.A.

- Hero Group

- Unilever PLC

- Orkla ASA

- Lindt & Sprüngli AG

- Intersnack Group GmbH & Co. KG

- The Hershey Company

- Nestle S.A.

- Hormel Foods Corp.

- Kraft Heinz Company

- Dr. August Oetker KG

- Menz & Gasser

- Mars, Incorporated

- Lotus Bakeries

- Rigoni di Asiago

- Valeo Foods

- Zentis GmbH

- Barilla G. e R. F.lli S.p.A.

- Ebro Foods, S.A

Market Opportunities and Future Outlook

Plant-based and better-for-you spreads offer a clear space for manufacturers to combine clean-label positioning with scalable production, alongside ongoing capacity moves in Europe. In March 2026, Oatly announced a USD 16 million investment in its Landskrona, Sweden facility to lift capacity by more than 33%, reinforcing supplier-side expansion for oat-based ingredients that can be formulated into spreadable products. In May 2026, Karwendel expanded production capacity for its NOA plant-based spreads and hummus by taking over an existing production hall in Landsberg am Lech, Germany, strengthening local manufacturing for chilled spread formats and adding headroom for retail and foodservice listings.

Ingredient and process innovation around European-grown pulses and lower-impact processing also supports routes to new textures and protein-enriched spreads. In July 2026, Crespel and Deiters partnered with Happy Plant Protein to implement a one-step dry extrusion process at its Helmond, Netherlands facility to produce textured vegetable proteins from European-grown pulses, and in April 2026 Happy Plant Protein announced development of a crop-based protein facility in Latvia using licensed dry extrusion technology. These moves align with the shift toward vegan and flexitarian spreads, and they can reduce reliance on imported proteins while supporting differentiated nut-, seed-, and pulse-based formulations with simpler ingredient statements.

Recent Industry Developments in Europe Food Spread Market

- July 2026: Crespel and Deiters partnered with Happy Plant Protein to implement a one-step dry extrusion process at its Helmond, Netherlands facility for producing textured vegetable proteins from European-grown pulses. The added capability supports cleaner-label, regional protein inputs that can be used in vegan and protein-enriched spreads, helping brands diversify beyond dairy and traditional nut bases.

- June 2025: Bel UK announced The Laughing Cow Spicy Chilli, the brand's first chilli-flavoured cheese portion in the UK, with roll-out via major grocers and online. The launch expands flavor-led differentiation in dairy spreads while keeping a clean-label message around no artificial colours or flavours.

- March 2024: Dreamfarm expanded its almond-based cheese spreads into Belgium following traction in Italy. The cross-border move highlights how plant-based spread brands are extending distribution in Western Europe to capture flexitarian demand and build retail footprint.

Europe Food Spread Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the Europe food spreads market is defined as packaged sweet and savory spreadable products that are typically applied on bread, crackers, or similar carriers, and sold for home consumption and food-service use across Europe.

Scope exclusions: This sizing excludes salted table butter, frying margarines, and industrial fat blends that are mainly used as functional ingredients in bakery or food manufacturing.

Segments Covered in This Report

- By Product Type

- Honey

- Chocolate-based Spreads

- Fruit-based Spreads

- Nut- and Seed-based Spreads

- Dairy and Cheese Spreads

- Other Product Types

- By Nature

- Conventional

- Organic

- By Packaging Type

- Jars

- Tubs

- Sachets/Pouches

- Others

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

- By Geography

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the category frame and to make sure our model inputs match how the market behaves across European countries. We relied on public sources such as Eurostat and national statistical offices for food manufacturing and retail indicators, and we also reviewed FAOSTAT for agriculture-linked inputs that influence spread categories like honey and fruit preserves.

To ground the discussion on diets, claims, and product composition, we referred to sources such as EFSA publications, the European Commission regulatory and labeling references, and peer-reviewed nutrition and food science journals. Company annual reports, investor presentations, and reputable trade press were used to interpret pricing actions, portfolio shifts, and capacity announcements. In a few places, we also used paid subscriptions for company financials and for cross-checking patent activity linked to reformulation, and this was done only to confirm the direction of change rather than replace public statistics. These sources are illustrative, and many other public and paid references were also reviewed to collect data, validate assumptions, and clear up open questions.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with brand owners, ingredient suppliers, contract manufacturers, distributors, and retail facing category teams across Europe, so that pricing, pack size moves, and channel mix could be validated beyond what is visible in public data. We also tested our assumptions with functional leaders and managers who track promotions, private label activity, and consumer downtrading, which helped close gaps in penetration and value growth assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 34% | |

| Smaller Players: 18% | Managers: 54% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production and trade data are used to reconstruct the available spread category value pool for Europe, which is then aligned to what is actually sold as packaged spreads in retail and food-service. Once that structure is in place, selective bottom-up checks are run using sampled brand and private label price points, observed pack sizes, and volume proxies from channel discussions, and totals are adjusted when the two views do not reconcile.

Key model inputs include category level pricing and promotional intensity, private label share movement, raw material signals that influence spreads (such as dairy fat, cocoa, nuts, fruit, and honey), and country level consumption and retail turnover indicators. We also track how shoppers shift between sweet and savory spreads during inflation periods, since that changes mix and average selling prices in a visible way. Forecasting is run using scenario analysis supported by trend lines in the inputs, and the forward view is then tested with expert feedback on expected price normalization, reformulation, and channel strategies. Where bottom-up coverage is incomplete for smaller countries or niche subcategories, the gap is handled through calibrated country ratios and by applying validated price ladders rather than forcing false precision.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including public macro and food category indicators, company commentary, and the direction confirmed in interviews. Large variances are flagged for review, and the assumptions that drive them are rechecked, followed by a second pass from another analyst before internal sign-off.

The report is refreshed on an annual cycle, and interim updates are made when material events occur, such as major price resets, regulatory changes, or visible shifts in private label penetration. Before delivery, a final check is performed to ensure the model reflects the most recent data points and that any late breaking changes are applied consistently across countries and the forecast.

Mordor Intelligence's Europe Food Spreads Market Market Size Versus Other Published Estimates

Published estimates for Europe food spreads can look far apart even when they appear to talk about the same category, because scope choices and pricing logic are not consistent across publishers. Differences usually come from which products are counted as spreads, whether values are tracked at retail or factory level, and how currency timing and inflation are treated in the base year.

Some published figures treat the market as a broad spreads bucket that leans heavily into butter, margarine, and other fat-based spreads, which lifts the starting value and also changes the mix of growth drivers. In Mordor Intelligence, the 2025 value is tied to packaged food spreads like honey, fruit preserves, nut and seed pastes, chocolate creams, and dairy or cheese spreads, and it excludes salted table butter, frying margarines, and industrial fat blends used mainly for baking inputs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.10 B (2025) | |

| Global Consultancy A | USD 15.85 B (2024) | Uses a wider spreads definition that is weighted toward butter and cheese style spreads, and the base year is set at 2024 with revenue reported at a broader Europe spreads level rather than a food spreads only basket. |

| Regional Consultancy B | USD 15.17 B (2024) | Positions spreads as a fat-based category that can include margarine and plant-based spreads, and the longer forecast window can embed different inflation and mix assumptions compared with a packaged food spread focus. |

The comparison shows that most of the spread is explained by category scope first, and then by the year chosen and how price and mix are carried into value. By keeping the inputs linked to clear spread categories and by cross-checking pricing and mix changes with Europe based practitioners, the final number stays easier to trace and repeat when the model is updated.

Key Questions Answered in the Report

What is the current size and growth outlook for the European food spreads market?

The market generated USD 11.45 billion in 2026 and is forecast to reach USD 13.34 billion by 2031, reflecting a 3.12% CAGR

What packaging format offers the greatest growth potential?

Sachets and pouches are poised for a 6.28% CAGR because they meet demand for portion control and on-the-go snacking.

Which country generates the most sales and which is growing fastest?

Germany contributes 14.05% of total revenue in 2025, while Poland shows the highest growth outlook at a 5.94% CAGR for 2026-2031.

How are health trends influencing product reformulation?

Brands are lowering sugar, removing palm oil, and launching vegan variants to counter a health-related drag on category growth.

Page last updated on: