Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.19 Billion |

| Market Size (2026) | USD 4.41 Billion |

| Market Size (2031) | USD 5.67 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

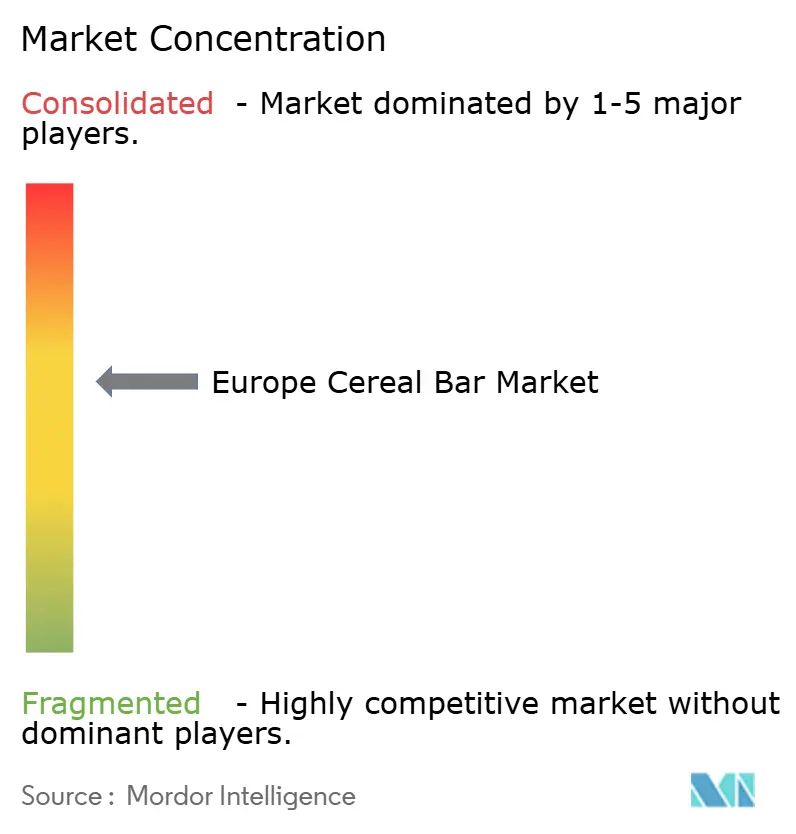

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Cereal Bar Market Analysis by Mordor Intelligence

The Europe cereal bars market size in 2026 is estimated at USD 4.41 billion, growing from 2025 value of USD 4.19 billion with 2031 projections showing USD 5.67 billion, growing at 5.17% CAGR over 2026-2031. The market's growth stems from changing consumer preferences toward convenient and nutritious snacking options. Key growth drivers include increased health awareness, demand for high-protein and fiber-rich products, fitness trends, and product innovations in flavors and formats. Germany and the United Kingdom represent major market shares, while countries like Poland demonstrate significant growth potential. While supermarkets and hypermarkets continue to be the primary distribution channels, e-commerce is experiencing rapid growth due to increased digital adoption. The market faces challenges including concerns about sugar content, competition from other snack categories, and regulatory requirements. However, the Europe cereal bars market continues to expand as manufacturers adapt to meet consumer demands for healthier snacking alternatives.

Key Report Takeaways

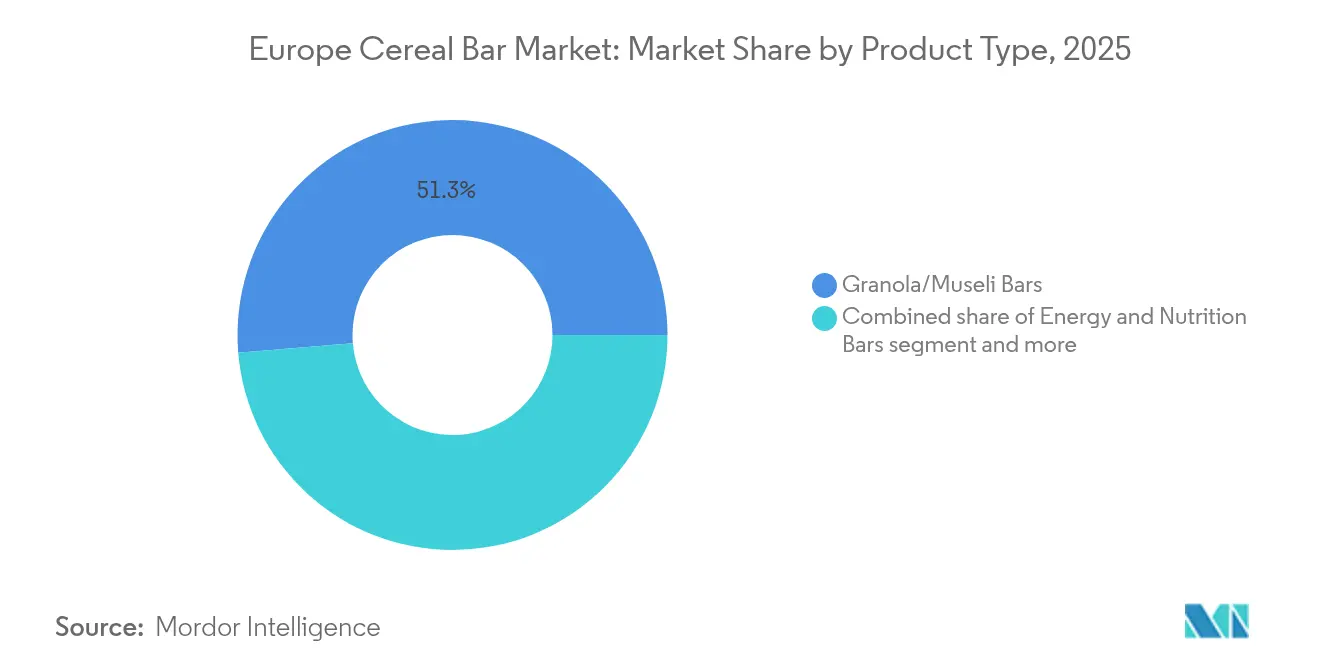

- Granola and muesli bars accounted for 51.32% of Europe's cereal bars market share in 2025; energy and nutrition bars are forecast to post a 6.13% CAGR to 2031.

- Conventional products held 72.65% revenue share in 2025; organic offerings are expected to grow at a 6.84% CAGR through 2031.

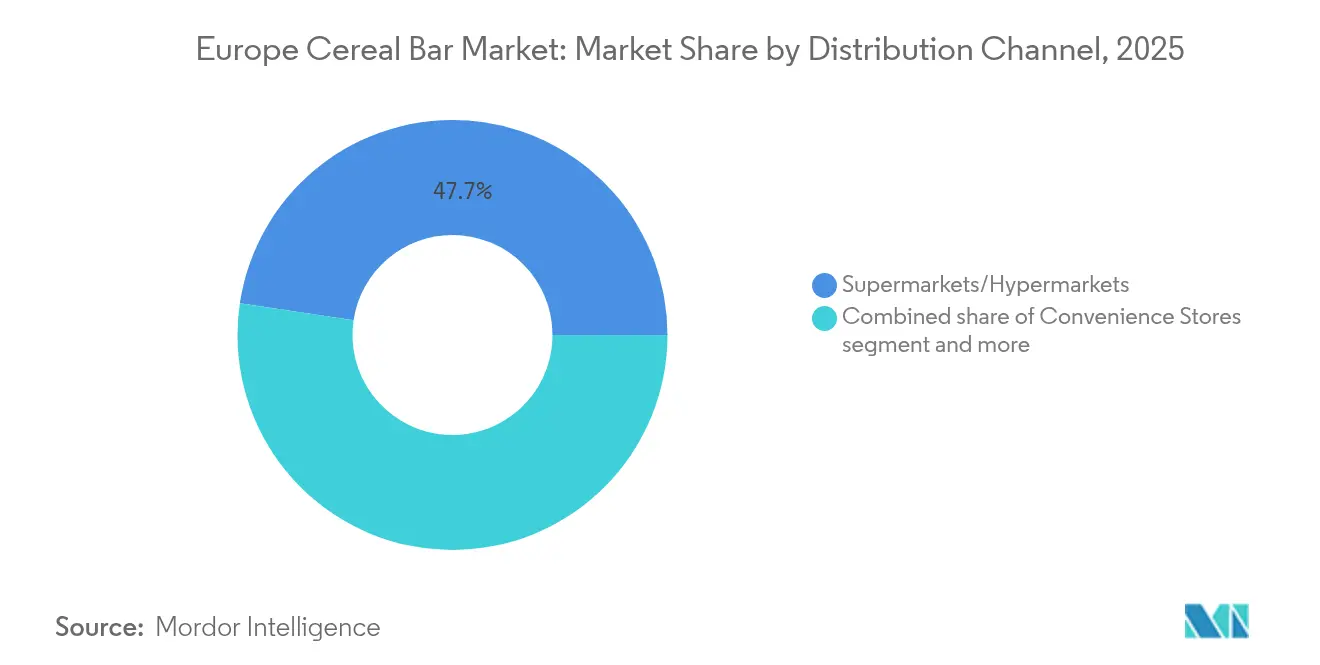

- Supermarkets and hypermarkets maintained a 47.65% revenue share in 2025; online stores are projected to register an 8.02% CAGR through 2031.

- Germany captured 18.05% of Europe's cereal bars market size in 2025; Poland is predicted to lead growth at a 6.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Cereal Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-driven on-the-go snacking trend | +1.2% | Global, strongest in Germany and the United Kingdom urban centers | Medium term (2-4 years) |

| Growing preference for high-protein and fiber-rich bars | +1.8% | Europe-wide, led by Nordic countries and Germany | Long term (≥ 4 years) |

| Growing fitness trends fuel the consumption of cereal bars | +1.1% | Western Europe core, expanding to Eastern Europe | Medium term (2-4 years) |

| Innovation in flavors and formats | +0.8% | Innovation hubs: Germany, Netherlands, the United Kingdom | Short term (≤ 2 years) |

| Rising awareness of dietary restrictions | +0.9% | Northern and Western Europe, gradual Eastern adoption | Long term (≥ 4 years) |

| Health and wellness trends | +1.4% | Pan-European with premium positioning | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-driven on-the-go snacking trend

The European cereal bar market is primarily driven by the increasing demand for convenient, on-the-go snacking options. As consumers manage busier lifestyles, they seek portable and nutritious snacks that integrate seamlessly into their daily schedules. Cereal bars meet these requirements through their practical packaging and nutritional benefits, making them a preferred choice for consumption outside homes and workplaces. This preference is particularly evident among young consumers and working professionals who prioritize products combining nutrition with convenience. According to the Italian National Institute of Statistics (Istat), in 2023, 65.2% of Italian children aged 11-13 consumed snacks at least once per week [1]Source: Italian National Institute of Statistics (Istat), "Share of individuals who consumed snacks", https://avvisi.istat.it. This high snacking frequency among the younger population reflects broader European consumption patterns favoring convenient options like cereal bars. The market's alignment with current consumer preferences for convenient and health-conscious snacking supports its continued growth across Europe.

Growing preference for high-protein and fiber-rich bars

The growing consumer preference for high-protein and fiber-rich bars drives the European cereal bar market. Health-conscious consumers seek convenient snack options that provide functional benefits, including sustained energy, digestive health, and satiety. Products containing protein and dietary fiber align with these nutritional goals, making cereal bars a preferred choice for individuals focusing on active lifestyles, weight management, and overall wellness. This emphasis on nutrient-dense formulations has encouraged manufacturers to enhance their product offerings to meet the demand for healthier snacking alternatives. For instance, in August 2025, Kellogg's expanded its United Kingdom presence by launching Oaties cereal bars, containing 55% wholegrain oats and serving as a fiber source. These bars, available in Chocolate & Oat and Honey and Oat flavors, combine taste with nutritional value. This product launch demonstrates how companies are responding to the demand for high-fiber and whole-grain-based cereal bars, strengthening their market position.

Growing Fitness Trends Fuel Consumption of Cereal bars

The rising fitness trend significantly drives cereal bar consumption in the European market. The increasing adoption of active and health-conscious lifestyles has created demand for convenient, nutritious snacks that support energy replenishment, muscle recovery, and wellness. Cereal bars, particularly those fortified with protein and functional ingredients, serve fitness enthusiasts and athletes seeking quick, portable snack options to complement their workout routines. According to Sport England, fitness class participation in England increased from 6.29 million people to 6.69 million between November 2023 and November 2024 [2]Source: Sport England, "Number of people participating in fitness classes in England", https://www.sportengland.org. This growth in fitness participation aligns with the broader European shift toward healthier living and physical activity, contributing to the increased consumption of cereal bars among active consumers. The expanding fitness-focused consumer base strengthens the market growth for cereal bars designed to provide nutritional support for active lifestyles.

Innovation in flavors and formats

Product innovation in flavor profiles and format diversification continues to be a significant growth driver in the European cereal bar market. Consumer preferences have evolved beyond fundamental nutritional requirements to encompass sophisticated taste experiences and distinctive textural elements in snack products. Manufacturing companies are implementing strategic product development initiatives to create differentiated flavor combinations and innovative formats, thereby expanding their market presence. These product developments align with current market trends, including clean-label ingredient incorporation and functional nutritional benefits, which strengthen competitive positioning. In August 2025, Cadbury introduced its Cadbury Brunch Choc Chip cereal bars, incorporating a structured combination of cereals such as oats, bran flakes, and rice crispies, honey integration, chocolate chip elements, and Cadbury milk chocolate coating. This product introduction exemplifies the industry's approach to developing nutritionally balanced convenience products with premium ingredients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content concerns | -1.1% | European Union-wide, strictest in Nordic countries | Medium term (2-4 years) |

| Competition from alternative snacks | -0.8% | Mature markets: Germany, the United Kingdom, and France | Short term (≤ 2 years) |

| Supply-chain volatility for specialty proteins | -0.7% | Import-dependent regions, Eastern Europe impact | Short term (≤ 2 years) |

| Saturated shelf space in mature retail markets | -0.6% | Western Europe retail concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Sugar Content Concerns

Health concerns regarding high sugar content constrain the growth of the European cereal bar market. Consumers are increasingly aware of the health risks associated with excessive sugar consumption, including obesity, diabetes, and cardiovascular diseases, leading to higher demand for low-sugar or sugar-free options. Consumers examine product labels more thoroughly and frequently avoid snacks with high sugar content. This consumer behavior shift creates challenges for manufacturers who must reformulate products while maintaining taste and texture, a process that involves technical complexity and increased costs. European regulatory requirements and public health initiatives focused on sugar reduction further pressure cereal bar manufacturers. These factors restrict market growth by reducing the appeal of conventional cereal bars and creating obstacles for companies dependent on sugar-based formulations.

Competition from Alternative Snacks

The European cereal bar market encounters substantial competition from alternative snack products. The market demonstrates an extensive range of convenient and nutritious snacking alternatives, encompassing nuts, seeds, fruit bars, vegetable chips, protein clusters, and fresh fruit, which directly compete with cereal bars in consumer expenditure allocation. Alternative snacks frequently address specific consumer requirements, including whole-food ingredient composition, minimal processing methodologies, and specialized dietary specifications. The increasing consumer preference for specialty snacks with enhanced nutritional compositions and innovative product formulations further intensifies market competition. This competitive landscape necessitates substantial investments from cereal bar manufacturers in product innovation and differentiation strategies, subsequently resulting in elevated production expenses and increased market volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Energy Bars Drive Premium Positioning

Granola and muesli bars dominate the European cereal bar market with a 51.32% market share in 2025. This dominance stems from consumer preference for wholesome ingredients and health benefits. These bars meet the increasing demand for convenient, nutritious snacking options, particularly among health-conscious consumers with active lifestyles. The products offer diverse flavors, textures, and ingredient combinations, incorporating oats, nuts, dried fruits, seeds, and natural sweeteners. The category benefits from consumer preferences for natural, organic, and functional food products, as these bars typically contain clean-label and minimally processed ingredients.

Energy and nutrition bars are projected to grow at a CAGR of 6.13% through 2031. This growth reflects increasing consumer demand for convenient options with enhanced nutritional benefits, including higher protein content, added vitamins, and sustained energy release. Rising health and fitness awareness has positioned these bars as popular meal supplements and portable energy sources. Manufacturers are developing new formulations with functional ingredients such as protein isolates, energy-boosting compounds, and natural sweeteners to address specific dietary requirements, including keto, paleo, and plant-based diets.

By Functional Claim: Organic Acceleration Despite Conventional Dominance

In the European cereal bar market, conventional products maintain a predominant market position, accounting for 72.65% market share in 2025. This substantial market presence is attributed to their extensive retail distribution, cost-effective pricing structures, and comprehensive flavor portfolios. Conventional cereal bars function as efficient nutritional solutions for consumers seeking convenient, portable sustenance. Major manufacturers sustain their market dominance through sophisticated distribution networks and established brand equity. Furthermore, established consumer purchasing patterns and product familiarity contribute significantly to maintaining the conventional segment's market supremacy.

The organic cereal bar segment in Europe demonstrates substantial growth prospects, with projections indicating a compound annual growth rate (CAGR) of 6.84% through 2031. This trajectory reflects an increasing consumer migration toward nutritionally superior, naturally derived, and environmentally sustainable food alternatives. Market demand is primarily driven by heightened food safety consciousness, environmental sustainability considerations, and consumer preferences for products free from synthetic agricultural chemicals and artificial additives. The German Organic Food Federation's statistical analysis reinforces this market development, documenting an increase in organic food revenues from EUR 16.06 billion in 2023 to EUR 16.99 billion in 2024, demonstrating enhanced market penetration of organic cereal bars among health-conscious consumers .

By Distribution Channel: E-commerce Transforms Retail Dynamics

Supermarkets and hypermarkets maintained a significant market share of 47.65% in 2025, establishing their position as primary distribution channels. These retail formats offer extensive reach and accessibility, serving consumers who prefer consolidated shopping experiences for their daily needs, including cereal bars. The prominence of these retail formats is strengthened through strategic partnerships and product launches that improve product visibility. In January 2024, Deliciously Ella expanded its distribution through major retailers Asda and The Co-op. The brand's product range, including granolas, cereal bars, and nut bites, is available in these stores, demonstrating effective market penetration through established retail channels. These partnerships enhance sales and build consumer confidence through association with established retail chains.

Online stores in the European cereal bar market are experiencing rapid growth, with a projected compound annual growth rate (CAGR) of 8.02% through 2031. This expansion stems from consumers' increasing preference for digital shopping and access to diverse cereal bar options not typically found in traditional retail outlets. E-commerce platforms enable consumers to purchase specialized, niche, and premium cereal bars, including organic, vegan, and functional varieties, directly from manufacturers or authorized sellers. The integration of online marketing tools, customized product suggestions, and subscription options has improved the digital shopping experience, resulting in increased customer retention and recurring purchases.

Geography Analysis

Germany holds an 18.05% market share in 2025, making it Europe's largest cereal bar market. The country's dominance stems from its established health-conscious culture, comprehensive retail infrastructure, and consumers' acceptance of premium pricing for functional nutrition products. The market's maturity and efficient distribution networks ensure wide product availability and consistent demand for wellness-oriented cereal bars.

Poland exhibits the highest growth rate in Europe, with a projected CAGR of 6.08% through 2031. Rising disposable income, urbanization, and shifting consumer preferences toward convenient nutrition drive this expansion. The growing middle class and increased health awareness are driving Polish consumers toward on-the-go snacking options, creating opportunities in the cereal bar segment.

The United Kingdom and France maintain stable markets with established consumption patterns, showing growth potential through premium products and functional innovations. Spain, the Netherlands, Belgium, and Sweden offer distinct growth opportunities based on local consumer preferences and regulations. The Netherlands shows notable progress in e-commerce adoption and sustainability awareness, with dietary surveys indicating trends toward reduced sugar and salt intake and increased fiber consumption, suggesting heightened demand for healthier cereal bars.

Competitive Landscape

The European cereal bars market shows moderate concentration, with competition driven by consolidation and innovation. Major players include General Mills, Inc., Nestlé S.A., Mars, Incorporated, Mondelēz International, Inc., and Hero Group. These companies influence market trends and consumer preferences through their established presence and extensive distribution networks.

Companies compete primarily through innovation, using their patent portfolios to develop new technologies. These include methods for extending shelf life, protein-sweetener binding systems, and incorporation of functional ingredients to improve product quality and meet consumer demands for healthy, convenient options.

Manufacturing and supply chain operations are evolving through increased technology adoption. Companies are investing in precision fermentation and alternative protein sources. These technological improvements enable product diversification, help manage ingredient costs, and address sustainability and nutritional requirements.

Europe Cereal Bar Industry Leaders

-

General Mills, Inc.

-

Nestlé S.A.

-

Mars, Incorporated

-

Mondelēz International, Inc.

-

Hero Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: 3Bears, a vegan oats brand, has partnered with Harry Kane to launch Crispy Cocoa and Salted Peanut protein bars. The bars, made from 100% wholegrain oats, contain 14-17g of protein per 100g and are free from refined sugar.

- July 2025: Dislog, a Moroccan FMCG distributor and manufacturer, has acquired the French snack brand Sundy, known for its chocolate-topped cereal bars. The acquisition adds to Dislog's expanding portfolio of snacks and its France-based brands.

- September 2024: Canadian brand MadeGood entered the United Kingdom market with its snack product range, including Granola Bars, Cookies, Crackers, Crispy Squares, and Soft Baked Oat Bars.

- April 2023: Ferrero acquired a snack-bar manufacturing facility in Faulbach, Bavaria, Germany, from Laurens Spethmann Holding (LSH). The Medin facility manufactures muesli and cereal bars, fruit bars, and sweetener tablets.

Europe Cereal Bar Market Report Scope

Europe cereal bar market is segmented by product type, distribution channel, and geography. On the basis of product type, the market is segmented into granola/muesli bars and others. On the basis of the distribution channels, the market is segmented into Convenience Stores, Supermarkets/Hypermarkets, Specialty Stores, Online Stores, and Other Distribution Channels. On the basis of geography, the report also provides regional analysis.

By Product Type

| Granola/Muesli Bars |

| Energy and Nutrition Bars |

| Others |

By Functional Claim

| Organic |

| Conventional |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Granola/Muesli Bars |

| Energy and Nutrition Bars | |

| Others | |

| By Functional Claim | Organic |

| Conventional | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe cereal bars market in 2031?

It is expected to reach USD 5.67 billion by 2031, up from USD 4.19 billion in 2025.

Which product segment is growing fastest in Europe?

Energy and nutrition bars are forecast to expand at a 6.13% CAGR through 2031.

How significant is organic certification in European cereal bars?

Organic variants are predicted to grow at a 6.84% CAGR, propelled by stricter EU rules that raise consumer trust.

Which country currently leads European cereal-bar sales?

Germany held 18.05% of 2025 sales, supported by high Nutri-Score awareness and mature retail infrastructure.

Page last updated on: