Advanced Phase Change Materials Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

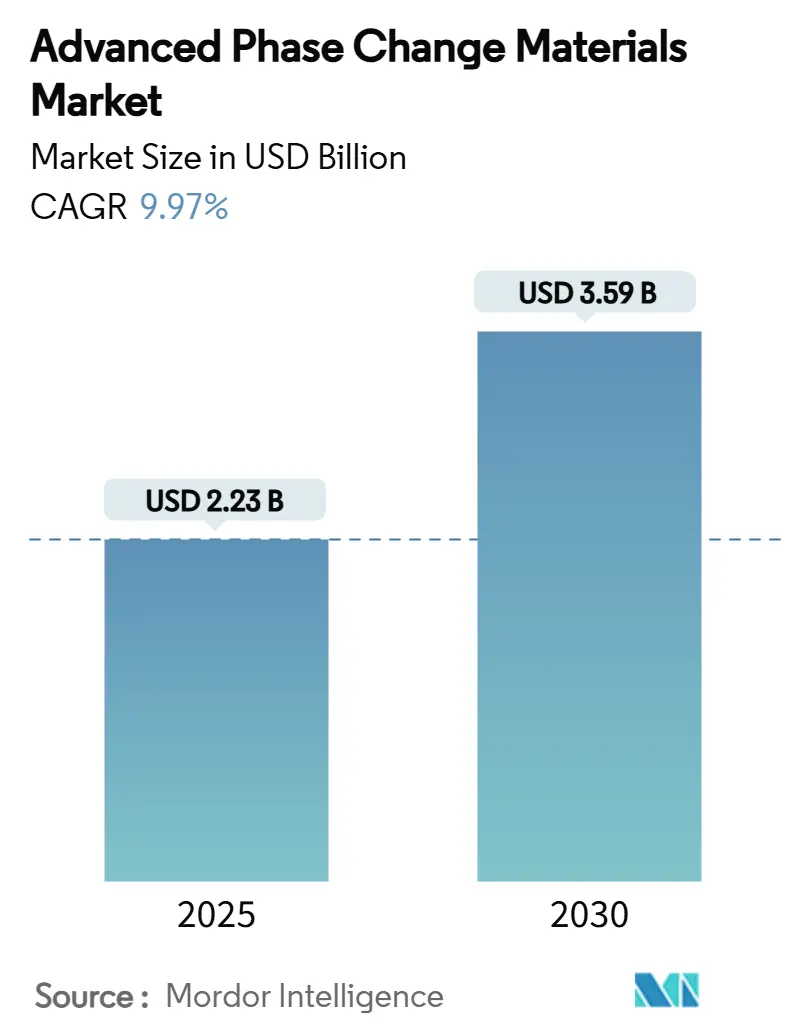

| Market Size (2025) | USD 2.23 Billion |

| Market Size (2030) | USD 3.59 Billion |

| Growth Rate (2025 - 2030) | 9.97% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Phase Change Materials Market Analysis by Mordor Intelligence

The Advanced Phase Change Materials Market size is estimated at USD 2.23 billion in 2025, and is expected to reach USD 3.59 billion by 2030, at a CAGR of 9.97% during the forecast period (2025-2030). This sustained expansion reflects growing reliance on passive thermal energy storage to cut peak electricity loads, stabilize renewable power, and meet stricter efficiency codes worldwide. Demand gains concentrate in building envelopes, battery packs, cold-chain packaging, and grid-level thermal buffers as users seek turnkey solutions integrating encapsulation, containment, and fire-safe additives. Europe anchors current revenue leadership on the back of binding net-zero building mandates, while Asia-Pacific supplies the fastest incremental demand thanks to large-scale electronics manufacturing, electric-vehicle adoption, and cold-chain infrastructure build-outs. Competition centers on materials science innovation, particularly polymer composites and microencapsulation, that close historic gaps in thermal conductivity and leakage control, even as volatile bio-feedstock costs and tightening flammability rules temper near-term margins.

Key Report Takeaways

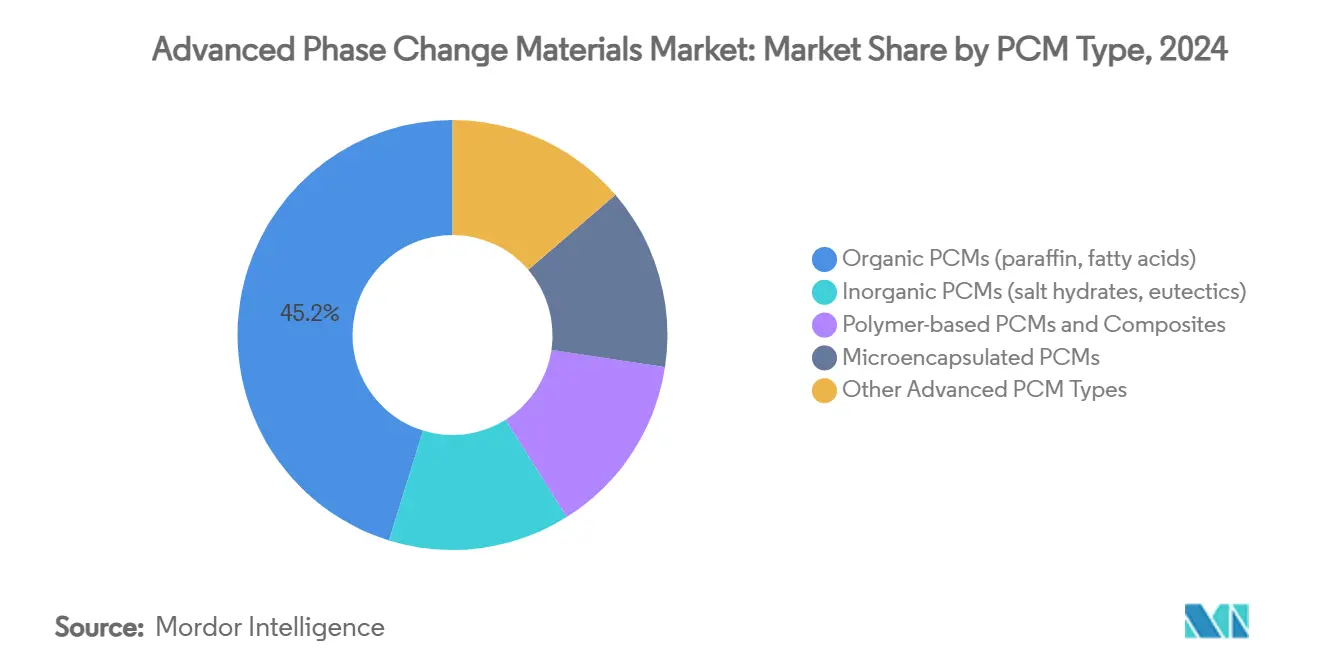

- By PCM type, organic paraffin and fatty acids held 45.23% of the Advanced Phase Change Materials market share in 2024, whereas polymer-based PCMs and composites are projected to expand at a 10.45% CAGR through 2030.

- By application, building insulation and thermal accumulation accounted for 31.12% share of the Advanced Phase Change Materials market size in 2024, while packaging and cold-chain transport is advancing at an 11.04% CAGR to 2030.

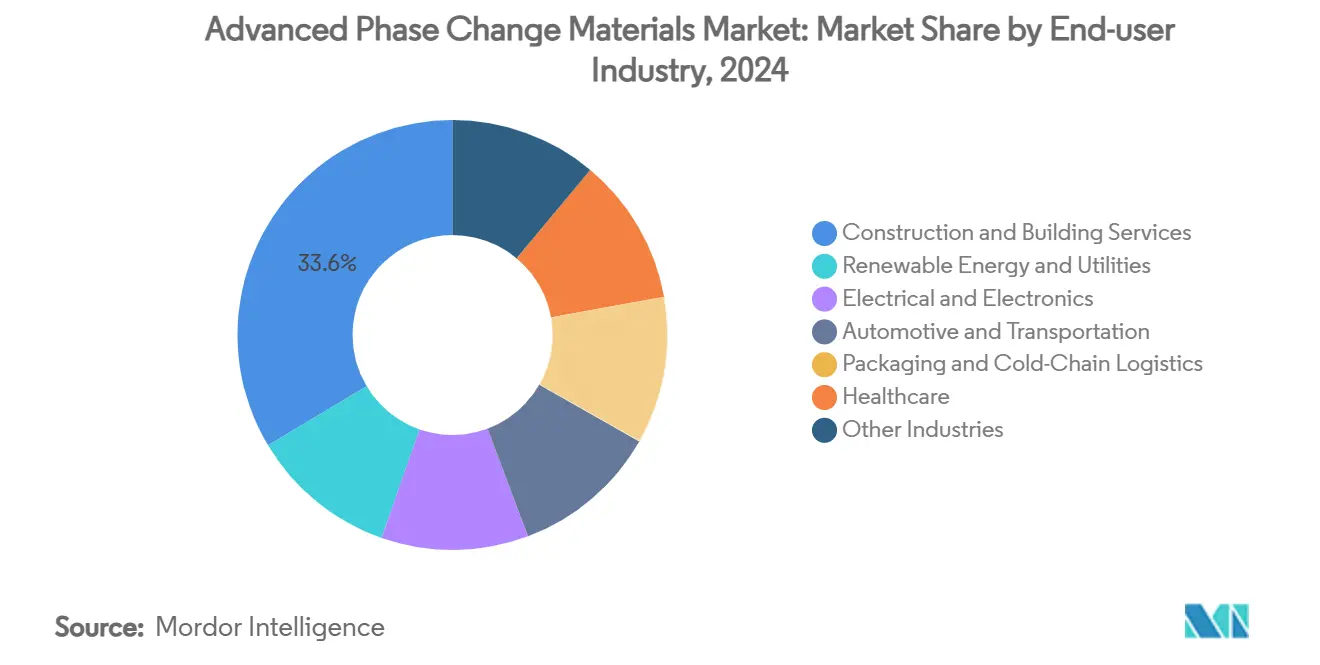

- By end-user industry, construction and building services captured 33.56% revenue share in 2024; healthcare registers the highest projected CAGR at 11.12% through 2030.

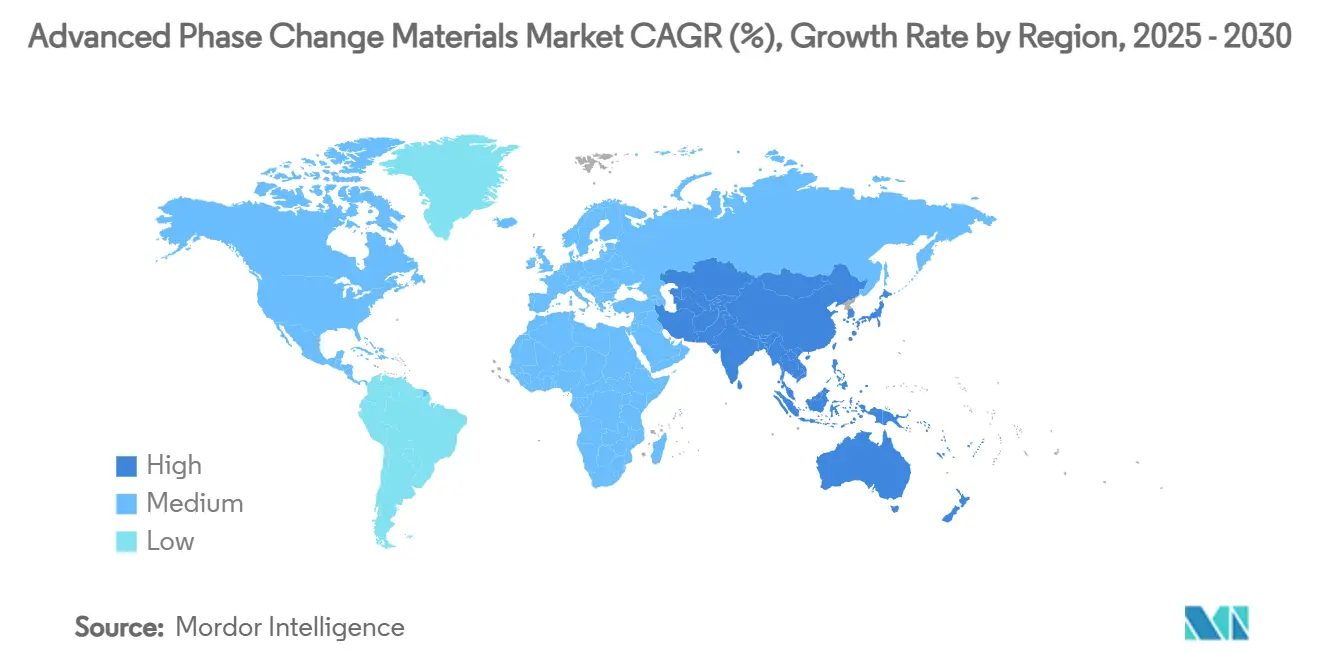

- By geography, Europe led with 34.56% of the Advanced Phase Change Materials market share in 2024, whereas Asia-Pacific is forecast to grow at an 11.23% CAGR between 2025-2030.

Market Trends and Insights

Drivers Impact Analysis of Advanced Phase Change Materials Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for thermal energy storage in HVAC and building envelopes | +2.8% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Expansion of renewable-powered heating/cooling and TES integration | +2.1% | Global, led by Europe, expanding to APAC | Long term (≥ 4 years) |

| Rapid adoption of battery and electronics thermal management solutions | +1.9% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Government net-zero carbon mandates boosting energy-efficient materials | +1.7% | Europe and North America, emerging in APAC | Medium term (2-4 years) |

| Surge in refrigerated last-mile delivery requiring passive cold-chain liners | +1.2% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Thermal Energy Storage in HVAC and Building Envelopes

Developers increasingly embed PCMs into walls and ceilings to flatten interior temperature swings and shave peak HVAC loads. Field tests in California confirmed ceiling panels infused with PCMs lowered cooling energy up to 52% during peak hours, helping projects comply with R-value upgrades in the 2021 International Energy Conservation Code. European retrofits echo similar savings as builders seek passive solutions that offset urban heat-island stresses without larger mechanical equipment. Public funding supports deployment, exemplified by the California Energy Commission’s USD 1.88 million grant to Stasis Energy Group in 2024 to validate thermal storage modules in multifamily housing[1]California Energy Commission, “Item 13b Stasis Energy Group LLC,” energy.ca.gov. With climate adaptation costs mounting, passive PCM layers offer cost-effective compliance paths toward net-zero performance goals.

Expansion of Renewable-Powered Heating/Cooling and TES Integration

Higher renewable penetration pushes utilities to decouple generation from consumption, and large-volume thermal tanks filled with salt- or paraffin-based PCMs are emerging as the buffer of choice. Finland’s 90 GWh Varanto facility underscores the scale now feasible, enabling solar and wind fleets to deliver round-the-clock heat. U.S. Department of Energy projects show modular PCM tanks trimming building electricity use by 40% while doubling as a low-cost alternative to electrochemical batteries[2]U.S. Department of Energy, “Low-Cost and High-Performance Modular Thermal Energy Storage,” energy.gov. Coupled with heat pumps, PCMs absorb surplus solar power as heat and discharge it when evening demand peaks, improving renewable economics once grid shares top 30%.

Rapid Adoption of Battery and Electronics Thermal Management Solutions

Automakers prioritize PCM sleeves around lithium-ion cells to curb thermal runaway, with SAE tests reporting 7.3 °C peak-temperature cuts during fast charging. Chinese laboratories advanced aerogel-PCM composites that pair 122 J/g latent capacity with electromagnetic shielding, ideal for 5G devices. Smartphone and tablet makers now exploit microcapsules holding 91.3% PCM payload to dissipate short-lived processor surges. Data centers deploying AI workloads adopt rack-level PCM cold plates that smooth hot-spot spikes without extra airflow, removing barriers that prevented dense server configurations.

Government Net-Zero Carbon Mandates Boosting Energy-Efficient Materials

Regulations targeting fluorinated greenhouse gases accelerate the shift to passive cooling and heating. The European Union’s 2024 F-gas Regulation limits high-GWP refrigerants, indirectly lifting PCM demand in chillers and building envelopes. In the United States, the Environmental Protection Agency’s latest HFC rule adds USD 1.3 billion in compliance costs, prompting supermarkets and cold-storage operators to trial PCM liners instead of retrofitting compressors. Embodied-carbon calculations in public procurement now reward bio-based PCMs, encouraging producers to scale up fatty-acid feedstocks despite price swings.

Restraints Impact Analysis of Advanced Phase Change Materials Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced encapsulation and system integration | -1.4% | Global, particularly acute in price-sensitive markets | Medium term (2-4 years) |

| Material flammability / leakage concerns tightening safety regulation | -0.9% | Europe and North America, spreading to APAC | Long term (≥ 4 years) |

| Supply volatility of high-purity bio-based fatty-acid feedstocks | -0.7% | Global, concentrated in palm oil producing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Encapsulation and System Integration

Microencapsulation adds 200-300% to base PCM costs because melamine-formaldehyde or polyurea shell synthesis requires batch reactors, solvent recovery, and strict particle-size control. Shape-stabilized composites that embed carbon nanotubes or expanded graphite deliver higher conductivity but introduce premium additives that inflate the bill of materials. Rubitherm’s life-cycle audit shows an individual storage module embodies 5.81 kg CO₂e, with the aluminum casing driving 79% of the impact, signalling how cost and environmental burden intertwine. Retrofit projects further face structural and mechanical alterations that extend payback periods in low-tariff regions.

Material Flammability/Leakage Concerns Tightening Safety Regulation

Most organic PCMs achieve Euroclass E fire ratings, below the C threshold now mandatory for facade insulation in several EU states. Leakage under repetitive cycling erodes encapsulant integrity, encouraging regulators to demand accelerated aging tests that lengthen certification timelines. Users balancing high latent heat with low flame-spread increasingly turn to aluminum honeycomb composites or polymer shells infused with graphite flame retardants, but these solutions raise mass and cost. Insurers are also requesting full-scale fire-propagation data before underwriting PCM-enhanced buildings, slowing adoption in commercial real-estate retrofits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Advanced Phase Change Materials Market Segment Analysis

By PCM Type:

Organic Leadership Persists while Polymer Composites SurgeOrganic PCMs retained 45.23% revenue in 2024 on the strength of mature supply chains and broad temperature spans from -10 °C to 90 °C. However, polymer-based PCMs and composites head the growth table with a 10.45% CAGR as nanotube-reinforced shells raise thermal conductivity 25% and curb leakage. The Advanced Phase Change Materials market size for polymer variants is forecast to widen steadily, reflecting the shift to encapsulated pellets that integrate easily into gypsum boards or battery housings. Inorganics such as salt hydrates lag due to supercooling, yet remain relevant where high-temperature storage is critical. Microencapsulation continues to blur categorical lines: gallium-core microcapsules target cryogenic electronics, whereas bio-fatty-acid capsules answer embodied-carbon targets. Suppliers winning share embed safety additives and graphite networks, bundling them as system kits rather than bulk drums, a move that raises switching barriers and secures service contracts.

By Application:

Cold-Chain Outpaces Construction MainstayBuilding insulation and thermal accumulation held 31.12% of revenue in 2024 as energy codes formally recognize PCM thermal mass, enabling smaller chillers and furnaces. Yet packaging and cold-chain transport will add the greatest new dollars, climbing at 11.04% CAGR through 2030. Multi-zone boxes employing dual-temperature PCMs keep biologics within 2-8 °C while maintaining frozen compartments for ice cream, extending route flexibility. Thermal energy storage tanks pairing with concentrated solar power plants form a rising third pillar, as utilities favor 15-year life cycles over battery replacements.

Electronics cooling also gains momentum as AI accelerators push rack densities past 100 kW. PCM gap-fillers inserted between chips and heat-spreaders soak transients that liquid loops cannot capture instantly. Textile and wearable innovators embed microcapsules into yarns, producing active sports apparel now retailed in Japan and Germany. Cost hurdles remain, but co-branding with sportswear majors signals route-to-scale viability. Across applications, integrated module suppliers winning tenders ship complete assemblies, liners, sensors, and telemetry, framing PCMs as part of broader thermal-management ecosystems.

By End-User Industry:

Healthcare Sets the PaceConstruction and building services accounted for 33.56% of spend in 2024, testament to strict envelope codes in Europe and North America. Healthcare, though smaller, logs the highest 11.12% CAGR as temperature-sensitive biologics proliferate. The Advanced Phase Change Materials market share tied to pharma packaging will therefore widen, with cold-chain service providers procuring bio-based PCMs from Croda that guarantee 2-8 °C stability for 96 hours.

Automakers integrate PCM pads between battery modules to damp thermal runaway, aligning with UNECE safety rules effective 2026. Electronics assemblers embed microcapsules in silicone gap-fillers for 5G base stations, where passive regulation halves fan noise and power draw. Food shippers trial PCM pallets that reduce reefer diesel hours, helping meet scope-3 emissions targets. Suppliers expand catalogs to span -40 °C vaccines up to 180 °C industrial waste-heat capture as each sector values different temperature bands, reinforcing solution-selling strategies.

Geography Analysis

Europe Advanced Phase Change Materials Market

Europe commanded 34.56% revenue in 2024, a lead built on mandatory efficiency codes and the 2024 F-gas Regulation that incentivizes passive cooling alternatives. Projects such as Finland’s 90 GWh Varanto thermal store spotlight grid-scale ambition, while German retrofits rely on PCM wallboards to preserve heritage facades under tight carbon ceilings. Supply chains are mature, and clients accept high unit costs for certified flame-retardant grades. Nordic utilities pilot hybrid heat-pump-PCM loops to extend renewables beyond seasonal intermittency, underscoring the region’s system-integration appetite.

APAC Advanced Phase Change Materials Market

Asia-Pacific posts the strongest 11.23% CAGR to 2030, driven by electronics production, EV battery deployment, and fresh-food e-commerce. China’s Suzhou Panji Zhichu Energy Technology unlocked nano-capsules yielding 20 W/(m·K) conductivity and 20,000 cycles, showcasing indigenous innovation.

North America Advanced Phase Change Materials Market

North America grows steadily as state energy codes sharpen and federal incentives reward thermal storage. California’s backed field pilots show large multifamily dwellings cutting peak power up to half with ceiling PCMs, reinforcing utility interest. Canada targets cold-climate swing mitigation, testing salt-hydrate blends that absorb daytime solar for night-time release. Mexico’s retail cold-chain expansion adopts PCM tote inserts to bypass infrastructure gaps, broadening regional uptake.

Competitive Landscape

Market structure remains moderately fragmented as diversified chemical majors and specialist formulators vie on technical depth, supply reliability, and application engineering. Intellectual-property barriers tighten around shell chemistries that balance flame retardancy with high latent heat. Joint-development agreements proliferate; for instance, a European constructor works with a PCM supplier and fire-testing lab to certify class-B facade panels, shortening go-to-market time. Supply risk from bio-feedstock price spikes triggers dual-sourcing strategies, with synthetic paraffin producers winning long-term contracts despite higher footprints.

Advanced Phase Change Materials Industry Leaders

BASF

Croda International plc

Phase Change Solutions

PureTemp LLC

Rubitherm Technologies GmbH

- *Disclaimer: Major Players sorted in no particular order

Advanced Phase Change Materials Market Companies Covered in this Report

- BASF

- AXIOTHERM GmbH

- Climator

- Croda International plc

- Cryopak

- Dow

- Honeywell International Inc.

- Laird Technologies, Inc.

- Outlast Technologies GmbH

- PCM Products Ltd

- Phase Change Solutions

- Phasestor

- Pluss Advanced Technologies

- PureTemp LLC

- Ru Entropy

- Rubitherm Technologies GmbH

- Sunamp Ltd

Recent Industry Developments in Advanced Phase Change Materials Market

- August 2024: Pluss Advanced Technology launched Form-Stable PCM at LogiPharma 2024 in Lyon. The organic 2 °C-8 °C blend broadens pharmaceutical-logistics options by eliminating leakage risk while meeting WHO stability criteria.

- March 2023: Phase Change Solutions expanded its portfolio with shape-stable BioPCM Bricks. The extruded BioPCM Brick is reusable, durable, and retains its shape up to +60⁰C.

Global Advanced Phase Change Materials Market Report Scope

Segmentation Overview

| Organic PCMs (paraffin, fatty acids) |

| Inorganic PCMs (salt hydrates, eutectics) |

| Polymer-based PCMs and Composites |

| Microencapsulated PCMs |

| Other Advanced PCM Types |

| Building Insulation and Thermal Accumulation |

| Thermal Energy Storage (TES) Systems |

| Battery and Electronics Thermal Management |

| Textile and Wearable Cooling / Heating |

| Packaging - Cold Chain / Food Transport |

| Other Applications (medical devices, aerospace) |

| Construction and Building Services |

| Renewable Energy and Utilities |

| Electrical and Electronics |

| Automotive and Transportation |

| Packaging and Cold-Chain Logistics |

| Healthcare |

| Other Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle-East and Africa |

| By PCM Type | Organic PCMs (paraffin, fatty acids) | |

| Inorganic PCMs (salt hydrates, eutectics) | ||

| Polymer-based PCMs and Composites | ||

| Microencapsulated PCMs | ||

| Other Advanced PCM Types | ||

| By Application | Building Insulation and Thermal Accumulation | |

| Thermal Energy Storage (TES) Systems | ||

| Battery and Electronics Thermal Management | ||

| Textile and Wearable Cooling / Heating | ||

| Packaging - Cold Chain / Food Transport | ||

| Other Applications (medical devices, aerospace) | ||

| By End-user Industry | Construction and Building Services | |

| Renewable Energy and Utilities | ||

| Electrical and Electronics | ||

| Automotive and Transportation | ||

| Packaging and Cold-Chain Logistics | ||

| Healthcare | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Advanced Phase Change Materials market?

It is valued at USD 2.23 billion in 2025, with a forecast to reach USD 3.59 billion by 2030.

How fast is demand growing in Asia-Pacific?

Asia-Pacific revenue is expected to expand at an 11.23% CAGR through 2030, the quickest among all regions.

Which PCM type holds the largest share today?

Organic paraffin and fatty-acid PCMs lead with 45.23% of 2024 revenue thanks to mature supply chains.

Why are PCMs important for cold-chain logistics?

Packaging lined with PCMs sustains 2-8 °C for 8.8 hours longer than conventional insulation, supporting vaccine and grocery deliveries without active refrigeration.

What is the biggest barrier to PCM adoption in buildings?

Achieving higher fire-safety classifications and containing leakage raise upfront encapsulation costs, extending payback periods in price-sensitive markets.

Page last updated on: