Europe Refrigerated Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

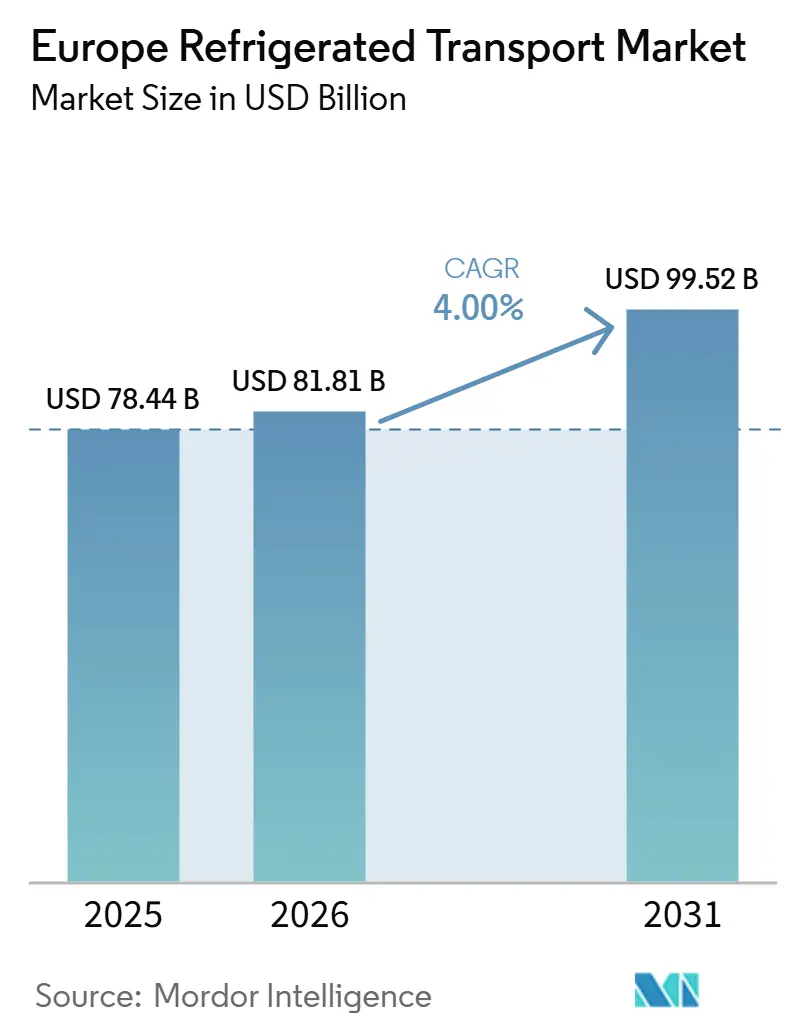

| Base Year Market Size (2025) | USD 78.44 Billion |

| Market Size (2026) | USD 81.81 Billion |

| Market Size (2031) | USD 99.52 Billion |

| Growth Rate (2026 - 2031) | 4.00% CAGR |

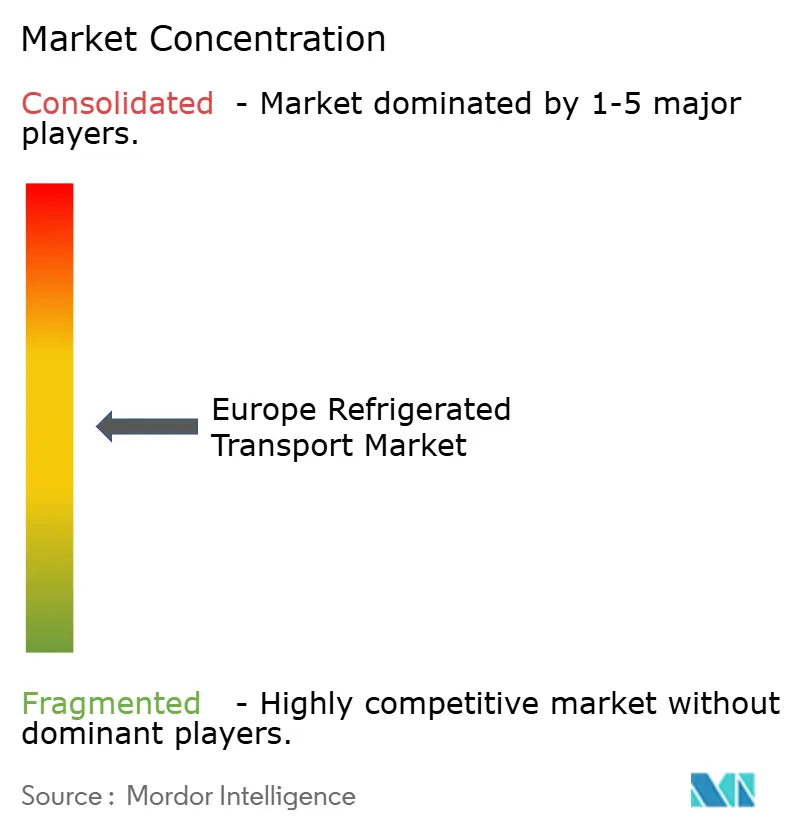

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Refrigerated Transport Market Analysis by Mordor Intelligence

The Europe refrigerated transport market size is projected to be USD 78.44 billion in 2025, USD 81.58 billion in 2026, and reach USD 99.52 billion by 2031, growing at a CAGR of 4.0% from 2026 to 2031.

Heightened demand for precise temperature control in pharmaceutical and meal-kit logistics, coupled with retailer net-zero commitments, is reshaping fleet specifications and route planning. Real-time IoT visibility is migrating from a niche feature to an operating prerequisite, while hydrogen fuel-cell prototypes point to long-haul decarbonization pathways. Operators are juggling peak-hour electricity tariffs that inflate e-reefer costs, and EU F-Gas quotas that accelerate the switch to natural refrigerants. These structural pressures are catalyzing consolidation as scale becomes vital to fund technology upgrades and meet diverse shipper requirements.

Key Report Takeaways

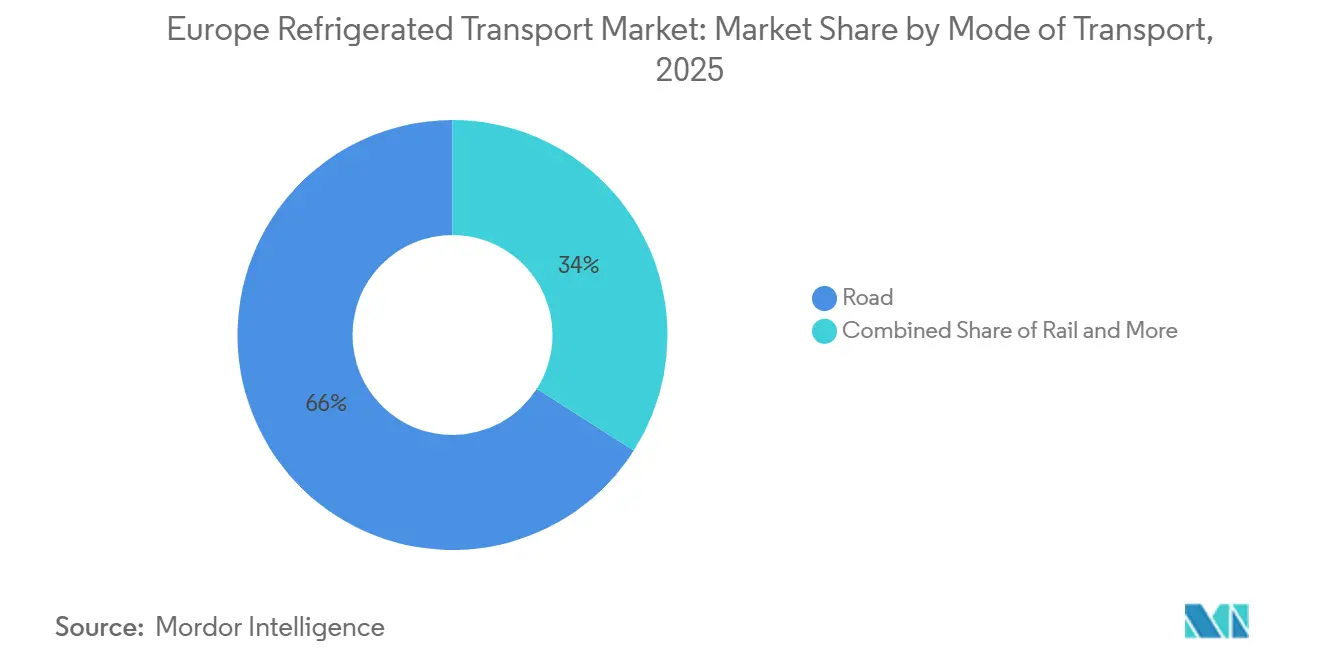

- By mode of transport, road held 65.97% of the Europe refrigerated transport market share in 2025, while air freight is advancing at a 7.66% CAGR through 2031.

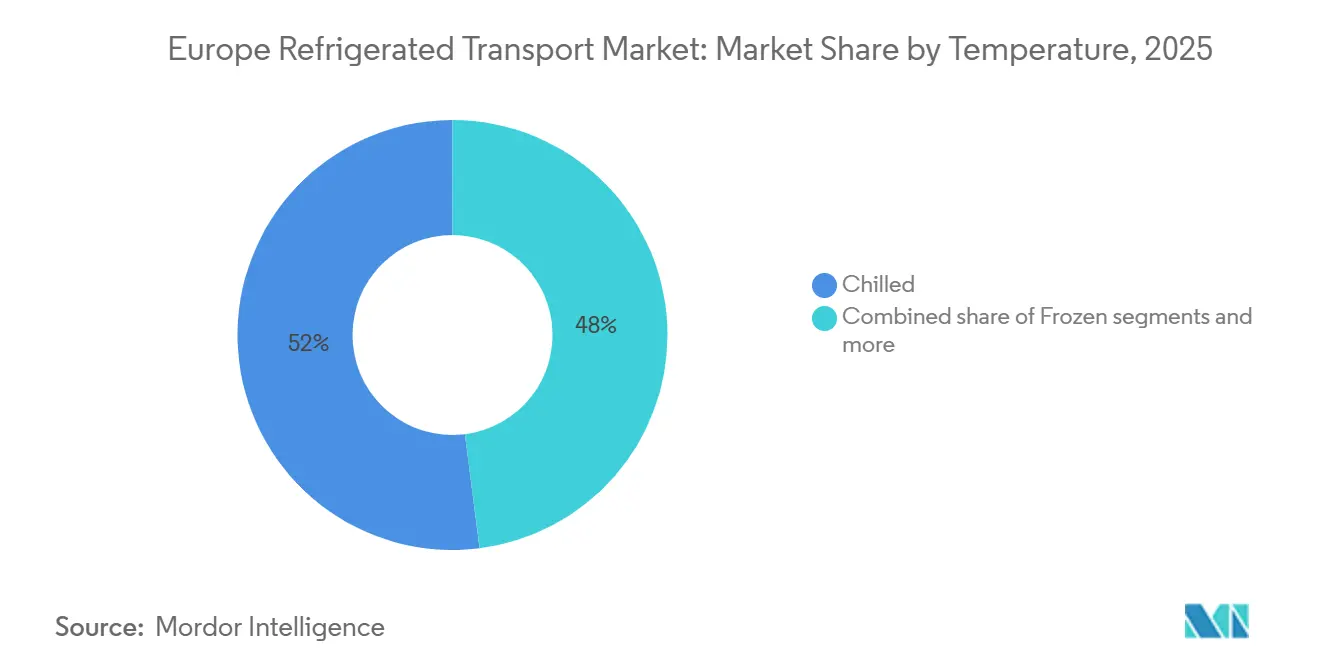

- By temperature range, the chilled segment captured 52.00% revenue share in 2025; the deep-frozen and ultra-low bracket is projected to expand at a 7.32% CAGR to 2031.

- By application, food and beverages accounted for 28.96% of the Europe refrigerated transport market size in 2025, and pharmaceuticals are growing at an 8.79% CAGR through 2031.

- By country, Germany led with 18.02% of the Europe refrigerated transport market share in 2025; Poland records the highest projected CAGR at 6.12% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Refrigerated Transport Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IoT-Enabled End-to-End Cold-Chain Visibility | +0.7% | Germany, Netherlands, United Kingdom | Short term (≤ 2 years) |

| Booster Immunization Campaigns Driving Pharma Flows | +0.9% | Germany, Belgium, France | Medium term (2-4 years) |

| Meal-Kit and Ready-to-Cook Subscription Boom | +0.5% | Urban Western Europe | Medium term (2-4 years) |

| Retailer Net-Zero Targets Accelerating Fleet Electrification | +0.6% | Northern to Southern Europe | Long term (≥ 4 years) |

| Hydrogen Fuel-Cell Power Packs for Trailer Refrigeration | +0.4% | Germany, Netherlands | Long term (≥ 4 years) |

| Liberalized Cross-Border Rail Paths for Temperature-Controlled Intermodal | +0.5% | Trans-European corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IoT-Enabled End-to-End Cold-Chain Visibility

5G-linked sensors now stream temperature, humidity, and location data across road, rail, sea, and air legs, cutting excursion incidents by up to 35% for fleets deploying platforms such as Carrier’s Lynx Fleet.[1]“Lynx Fleet Telematics,” Carrier Transicold, carrier.com Insurance firms are rewarding documented visibility with 10-15% premium discounts, improving return on technology spend. European Good Distribution Practice rules for medicines mandate continuous monitoring, pushing IoT uptake beyond early adopters. Trailer builders are integrating telematics at the factory, evidenced by Schmitz Cargobull’s Atlantis Global System purchase, which embeds tracking hardware into new reefers. Predictive analytics built on sensor streams now flag compressor faults before cargo risk escalates, trimming unplanned downtime by roughly a quarter.

Booster Immunization Campaigns Driving Pharma Flows

Continued COVID-19 and influenza booster programs, plus a surge of temperature-sensitive biologics, keep 2-8 °C lanes running near capacity. DHL has expanded GDP-certified hubs across Europe, adding validated storage zones to support multi-temperature breaks in transit. High-value GLP-1 drugs for diabetes and obesity therapy move under reinforced chain-of-custody protocols, justifying premium freight rates. Modal diversification is growing; stable products shift to ocean or rail to cut emissions, while cell and gene therapies stay in air corridors for speed. Reusable packaging with embedded data-loggers is gaining traction, cutting waste and slicing total packaging spend by nearly half over multi-cycle use.

Meal-Kit and Ready-to-Cook Subscription Boom

Urban consumers favor predictable home delivery windows, generating dense, short-haul drop routes that optimize reefer asset productivity. Surviving e-grocery platforms operate dark stores positioned within 3-5 km of customer clusters, demanding multiple chilled top-ups daily. Belgium’s dominance in frozen vegetable exports feeds subscription menus, encouraging high backhaul utilization on Benelux-to-metro lanes.[2]“Frozen Vegetable Trade Statistics,” CBI, cbi.eu Retailers now insource more of their cold chain to safeguard freshness, opening contract opportunities for carriers offering dedicated electric fleets. Subscription models also curb spoilage, with operators reporting 20-30% lower food waste than traditional retail channels.

Retailer Net-Zero Targets Accelerating Fleet Electrification

Supermarket groups have set zero-emission delivery deadlines between 2030 and 2040, compressing diesel phase-out timelines. Germany subsidizes up to 40% of depot charger costs, lowering capital hurdles for carriers. The Alternative Fuel Infrastructure Regulation compels high-power charging pools every 60 km on core corridors by 2030, ensuring network confidence for early movers. OEMs like Volvo and Daimler have pooled USD 550 million (EUR 500 million) to roll out 1,700 public chargers, complementing private depot installations. Battery packs such as Thermo King’s E-COOLPAC can save 10 t of CO₂ per truck yearly, strengthening the fleet business case.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peak-Hour Electricity Tariffs Inflating E-Reefer OPEX | -0.6% | Major urban centers | Short term (≤ 2 years) |

| EU F-Gas Quota Cuts Raising Low-GWP Refrigerant Prices | -0.8% | Entire European Union | Medium term (2-4 years) |

| ADR-Qualified Technician Shortage for Lithium Battery Reefers | -0.4% | Germany, France, Netherlands | Medium term (2-4 years) |

| Pallet Standard Mismatches Causing Reverse-Logistics Dead-Runs | -0.3% | UK-EU cross-border lanes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU F-Gas Quota Cuts Raising Low-GWP Refrigerant Prices

Regulation 2024/573 slashes hydrofluorocarbon availability by nearly 88% in 2027 and 95% in 2030, driving R452A prices toward USD 49 per kg (EUR 45) versus USD 6-17 for natural CO₂ or propane. Operators face retrofit bills of USD 16,000-37,000 per truck to adopt compliant systems. Carrier has introduced surcharges to offset steep input costs, yet promises 89% lower climate impact with next-gen refrigerants. Capital strain is harshest on small haulers that run older fleets.[3]European Commission, “Energy Prices and Tariffs,” europa.eu

High Fuel & Energy Prices

Diesel in Germany is expected to fluctuate between EUR 1.37-1.83 per liter (USD 1.58-2.11) through 2025, squeezing margins. The Eurovignette shift from time to distance charging will nearly double tolls for diesel trucks and introduce CO2 fees, accelerating electric adoption. Cold-chain operators shoulder dual energy burdens: traction fuel and refrigeration electricity, heightening exposure to volatility. Southern European fleets report cost surges equal to 2.5% of food-sector GDP, threatening small carrier viability. Zero-emission trucks enjoy temporary toll exemptions until 2026, yet high purchase prices and sparse chargers slow uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Intermodal Tilt Tests Road Dominance

Road transport captured 65.97% of the Europe refrigerated transport market share in 2025, anchored by flexible door-to-door service for grocery and pharma shippers. Driver shortages, such as 426,000 vacancies in early 2025 and steep toll hikes, are eroding cost advantages, but embedded telematics and expanded direct-store routes keep trucks indispensable. Rail and sea gain share where carbon targets are stringent; the Brenner Base Tunnel is forecast to increase the corridor's daily train capacity by over 50% (accommodating up to 400 trains per day) once fully opened, drawing frozen protein flows from Northern ports to Italian retailers. Air freight, paced by 7.66% CAGR, channels high-value biologics that justify premium lift prices, especially out of pharma clusters in Frankfurt and Basel. The ascent of controlled-atmosphere reefers on short-sea lanes also eases pressure on congested roads, extending shelf life by an extra week for citrus and berries.

Road’s relative margin narrows as electricity and diesel dynamics diverge. Battery trucks excel on sub-250 km milk runs but struggle with long-haul payload penalties, while hydrogen prototypes target the Hamburg–Munich spine. Fleet operators hedge through dual-fuel strategies, pairing battery last-mile vans with liquid gas line-haul tractors to meet emission caps without sacrificing range. Intermodal players market CO₂ savings of up to 75% versus truck-only delivery, a compelling figure for retailers reporting Scope 3 progress. As the value of visibility rises, carriers that integrate IoT telemetry across truck, rail, and vessel legs are winning new tenders from life-science shippers.

By Temperature-Control: Chilled Hegemony Meets Cryogenic Upsurge

Chilled cargo (0-5 °C) led with 52.00% share of the Europe refrigerated transport market in 2025, supplying dairy, meat, and produce flows into metropolitan distribution centers. Operators outfit trailers with multi-compartment systems to service diverse temperature bands on a single route, maximizing cube utilization. Despite dominance, chilled growth is steady rather than spectacular, whereas deep-frozen and ultra-low segments are tracking a 7.32% CAGR through 2031. Cryogenic logistics for cell and gene therapies at below -150 °C command rates that can exceed USD 5,500 per shipment, enticing carriers to add dry-shipper fleets and invest in redundant monitoring. UPS expanded cryo-storage in Germany after integrating Frigo-Trans, aligning assets with Europe’s expanding advanced-therapy pipeline.

Natural refrigerants are migrating from niche to mainstream across all bands. CO₂ systems show superior heat-exchange performance in ultra-low applications, while propane units deliver 10-15% energy savings for chilled loads. The EU F-Gas curve accelerates retrofit cycles, but total ownership costs fall once high-GWP gas purchases disappear. Meal-kit providers prioritize chilled precision, demanding ±0.5 °C variance to maintain shelf life and consumer trust. On the frozen side, vegetable exporters in Belgium rely on blast-freeze capacity near port clusters, then load controlled-atmosphere containers that keep texture intact on rail links into Central Europe. Dual-evaporation technology now allows a single reefer to toggle between -25 °C and +2 °C zones, supporting mixed fulfilment models and slashing empty returns.

By Application: Pharma Logistics Overtaking Commodity Food Flows

Food and beverages accounted for 28.96% of the Europe refrigerated transport market size in 2025, dominated by consolidated retailers sourcing meat and dairy under tightened animal-welfare rules. Margin pressure is high, nudging supermarket groups to renegotiate long-term haulage contracts and test collaborative inbound schemes that reduce partial loads. Pharmaceuticals and life sciences, expanding at an 8.79% CAGR through 2031, are on track to eclipse traditional food growth. 95% of European drugs now require some level of temperature control, and industry forecasts project biologics will account for 60% of new drug approvals by 2030. DHL’s rollout of GDP hubs in Leipzig and Milan demonstrates the capital intensity and certification depth demanded by shippers.

Chemical intermediates and specialty materials move steadily under ambient or cool conditions, supporting electronic and adhesive manufacturing. Flower logistics, centered in the Netherlands, face rivalry from emerging indoor farms that shorten supply chains, yet Mother’s Day peaks still flood air cargo lanes. Shippers are embedding sustainability clauses into tenders, rewarding carriers that publish verified CO₂ metrics. This pushes portfolio diversification; several food specialists are adding pharma-grade trailers with redundant power packs to smooth cyclical swings, while life-science hauliers back-load clean, high-value tech or dry goods to minimize empty-kilometer exposure.

Geography Analysis

Germany commanded 18.02% of the Europe refrigerated transport market revenue in 2025, thanks to its USD 263 billion (EUR 239 billion) food-processing sector and its standing as the fourth-largest global pharmaceutical producer.[4]“Germany Food Processing Industry,” Food Export Association, foodexport.org Central positioning along the Rhine-Danube corridor enables dense route networks into Benelux, Italy, and Eastern Europe. Recent investments, such as DACHSER’s USD 48.4 million (EUR 44 million) Unna facility with 22,000 pallet slots, reinforce infrastructure head-starts. The nation leads in electric-truck deployment after subsidizing depot chargers and highway megawatt pilots, though a 70,000-driver gap threatens capacity bottlenecks.

Poland posts the fastest expansion at 6.12% CAGR through 2030, underpinned by contract manufacturing in food preservation and generic drugs. The Warsaw-Duisburg lane held volume in early 2025 despite wider freight softness, reflecting resilient East-West trade. EU-funded Rail Baltica will trim Baltic transit times by a quarter, boosting refrigerated intermodal uptake. Global cold-store giant Lineage added capacity outside Warsaw, signaling long-term confidence in the corridor.

France remains a heavyweight, serving both domestic groceries and cross-Channel pharma flows, yet inflation and labor pressures compress margins. Italy and Spain benefit from Mediterranean produce exports, though both face aging driver pools, with 45% and 50% of hauliers over 55, respectively. The United Kingdom still struggles with post-Brexit border friction that lengthens clearance by up to 20 hours for perishables, complicating pallet alignment and cutting shelf life by a fifth. Dutch carriers report reluctance to serve British markets until administrative reforms take root.

Competitive Landscape

The Europe refrigerated transport market is moderately fragmented, but headline deals are redrawing the leaderboard. DSV closed a USD 15.7 billion (EUR 14.3 billion) takeover of DB Schenker in April 2025, pushing combined turnover to USD 43.2 billion and giving the group unmatched pan-continental density. Scale allows heavier spending on telematics and zero-emission pilots, raising barriers for sub-regional specialists.

Digital freight networks are also in play. Sennder acquired C.H. Robinson’s European surface arm for an undisclosed sum to create an entity with combined revenues of USD 1.54 billion (EUR 1.4 billion), layering its sennOS optimization engine on 18 000 reefer trucks and trimming empty kilometers by roughly one-sixth. Telematics integration differentiates asset-light brokers from commodity spot markets, and investors rewarded Lineage Logistics with a USD 4.4 billion IPO that funds cold-store roll-ups across second-tier cities.

Incumbent temperature-controlled specialists defend their share through service breadth. STEF runs 283 multi-temperature depots and posted USD 5.3 billion (EUR 4.8 billion) turnover in 2024, up 8.1% year-on-year, aided by proprietary last-mile platforms. Schmitz Cargobull, Europe’s largest reefer-trailer maker, purchased telematics firm AGS and expanded its Vreden site to cut logistics emissions by 150 t annually. White-space remains in hydrogen reefers and ultra-low pharma lanes, niches that nimble entrants can still penetrate before consolidation tightens further.

Europe Refrigerated Transport Industry Leaders

DFDS Logistics

STEF Group

Lineage Logistics

Girteka Logistics

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lineage published its "2026 Cold Chain Insights Survey" and concurrently announced a strategic push to deploy AI, predictive analytics, and automated warehouse robotics across its massive European footprint. Facing rising geopolitical tariffs and fluctuating demand for frozen foods in Europe, Lineage is positioning itself as a high-tech 3PL partner by offering enhanced real-time visibility and flexible storage solutions to help European food and beverage producers build supply chain resilience.

- February 2026: DHL significantly expanded its dedicated airfreight cold chain network under the "DHL Health Logistics" brand. The company introduced a dedicated Boeing 777 freighter to connect major European pharma hubs directly to the US Midwest. This strategic move aims to secure reliable, temperature-controlled capacity for time-critical biologics and cell therapies, reducing reliance on commercial passenger belly cargo as part of DHL's broader EUR 2 billion (USD 2.36 billion) global healthcare logistics investment.

- December 2025: In partnership with Volvo Trucks and supported by the UK Department for Transport/Innovate UK, DFDS successfully deployed commercial heavy-duty electric trucks specifically for cold chain transport in Shetland, UK. The initiative proved the operational viability of long-distance, zero-emission refrigerated logistics in harsh Northern European climates, paving the way for wider fleet electrification across its network.

- September 2025: STEF Group successfully finalized its acquisition of Christian Cavegn AG, one of Switzerland's most established logistics providers in the fresh, frozen, and dry food segments. The deal integrated 9 cold storage sites, 450 employees, and a fleet of roughly 400 refrigerated trucks and semi-trailers into STEF Group’s broader European temperature-controlled platform.

Europe Refrigerated Transport Market Report Scope

| Road |

| Rail |

| Sea |

| Air |

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (more than -20 °C) |

| Food and Beverages |

| Pharmaceuticals and Life-sciences |

| Chemicals and Specialty Materials |

| Floral & Nursery |

| Other Perishables |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Poland |

| Rest of Europe |

| By Mode of Transport | Road |

| Rail | |

| Sea | |

| Air | |

| By Temperature | Chilled (0–5 °C) |

| Frozen (-18–0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (more than -20 °C) | |

| By Application | Food and Beverages |

| Pharmaceuticals and Life-sciences | |

| Chemicals and Specialty Materials | |

| Floral & Nursery | |

| Other Perishables | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Netherlands | |

| Belgium | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe refrigerated transport market be by 2031?

Forecasts place it at USD 99.52 billion by 2031, up from USD 78.44 billion in 2025, at a 4.0% CAGR.

Which mode is expanding the fastest?

Air freight is projected to grow at 7.66% CAGR through 2031 due to biologics and cell therapy shipments.

Why is Germany the largest national market?

A USD 263 billion food-processing sector and dense pharma manufacturing make Germany a natural logistics hub.

What is driving demand for ultra-low temperature transport?

Cell and gene therapies that must remain below -150 °C are boosting cryogenic shipments across Europe.

How are EU F-Gas rules impacting operators?

Accelerated HFC phase-downs raise high-GWP refrigerant prices to nearly USD 49 per kg, pushing fleets toward natural alternatives.

Will hydrogen or battery technologies dominate zero-emission reefers?

Batteries lead in short-haul urban routes today, while hydrogen shows promise for long-haul trailers once refueling networks mature.

Page last updated on: