Europe Pharmaceutical Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

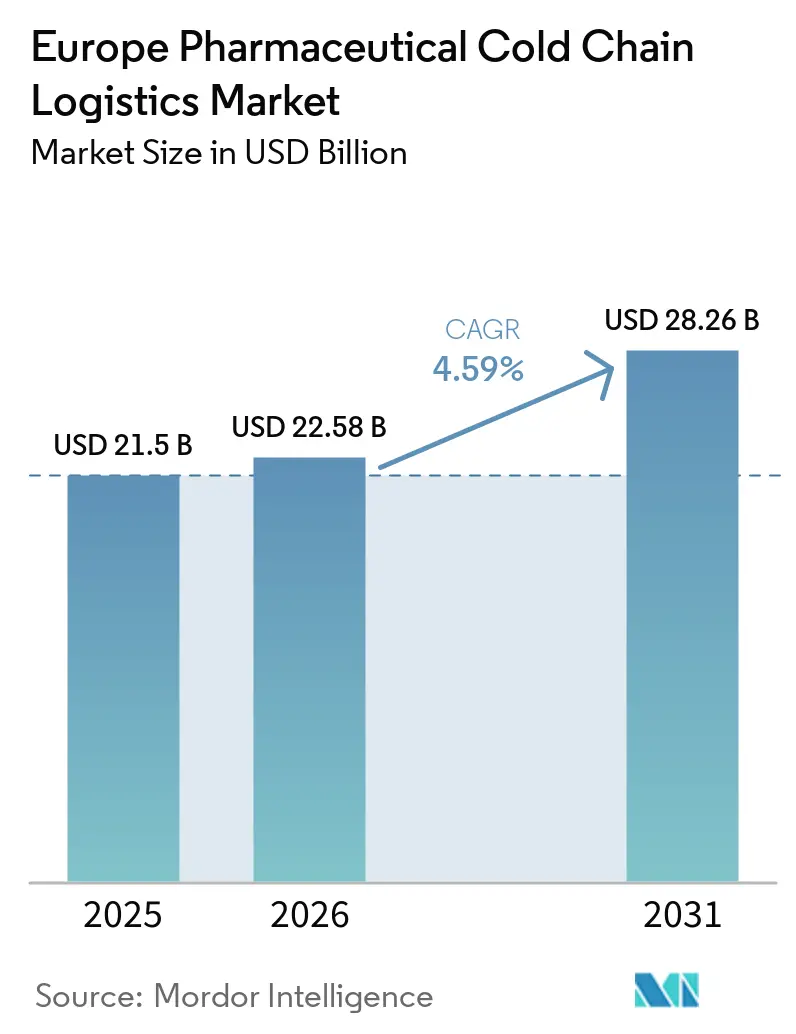

| Base Year Market Size (2025) | USD 21.5 Billion |

| Market Size (2026) | USD 22.58 Billion |

| Market Size (2031) | USD 28.26 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

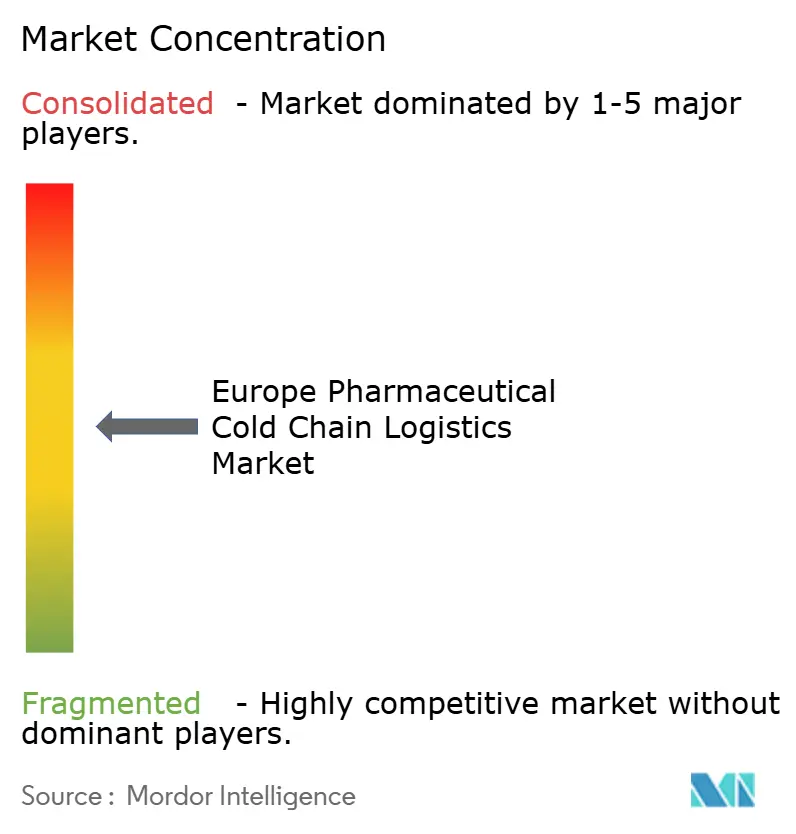

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pharmaceutical Cold Chain Logistics Market Analysis by Mordor Intelligence

The Europe pharmaceutical cold chain logistics market size is projected to expand from USD 21.50 billion in 2025 and USD 22.58 billion in 2026 to USD 28.26 billion by 2031, registering a CAGR of 4.59% between 2026 and 2031.

Demand grows as maternal immunization and respiratory syncytial virus vaccine roll-outs transform year-round distribution patterns, while cell and gene therapy approvals push requirements for ultra-low temperature handling. Serialization mandates under EU legislation elevate the need for value-added tracking and relabelling, and the EU Corporate Sustainability Reporting Directive spurs a shift toward reusable passive packaging that rewards providers with capital for green investments. At the same time, the F-gas phase-down obliges operators to phase out hydrofluorocarbon systems, tilting competitive advantage to firms able to finance natural-refrigerant retrofits. Automation, robotics, and IoT visibility tools drive productivity gains, but growing cyber-risks demand hardened digital infrastructure across the entire Europe pharmaceutical cold chain logistics market.

Key Report Takeaways

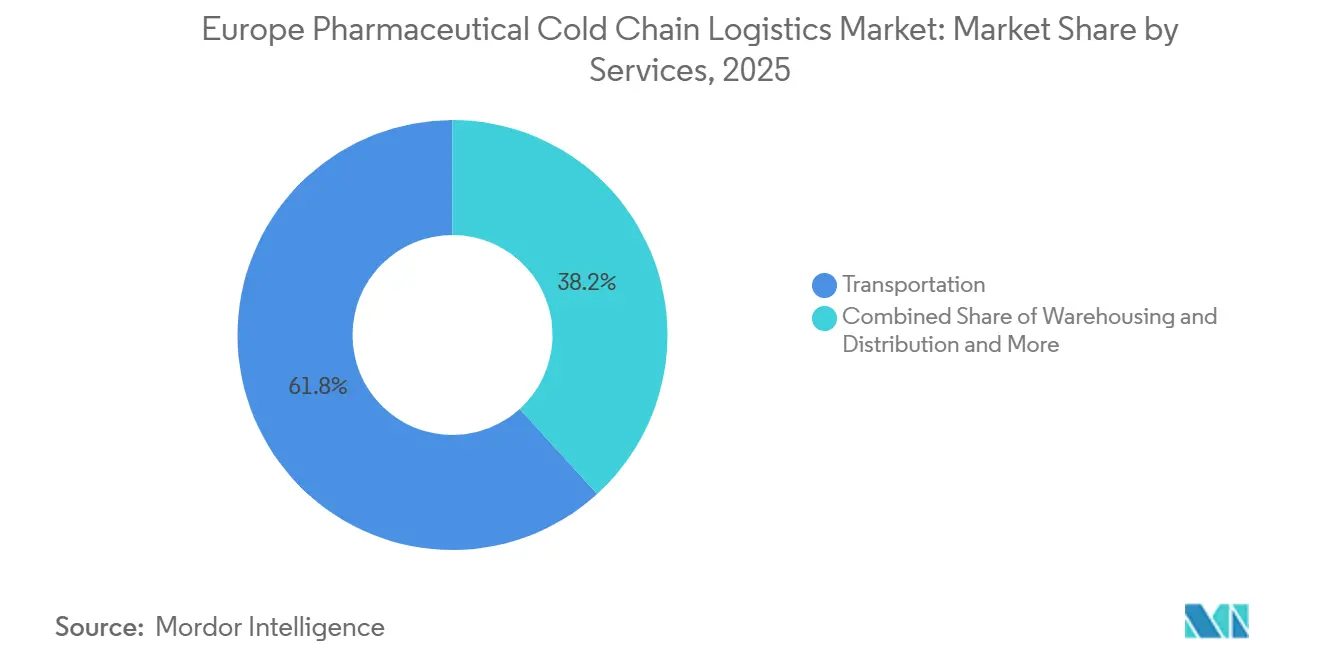

- By services, transportation services held 61.76% of the Europe pharmaceutical cold chain logistics market share in 2025, while value-added services are forecast to expand at a 5.27% CAGR through 2031.

- By temperature type, chilled products commanded 40.88% of the Europe pharmaceutical cold chain logistics market size in 2025, yet deep-frozen and ultra-low services are projected to advance at a 5.61% CAGR between 2026 and 2031.

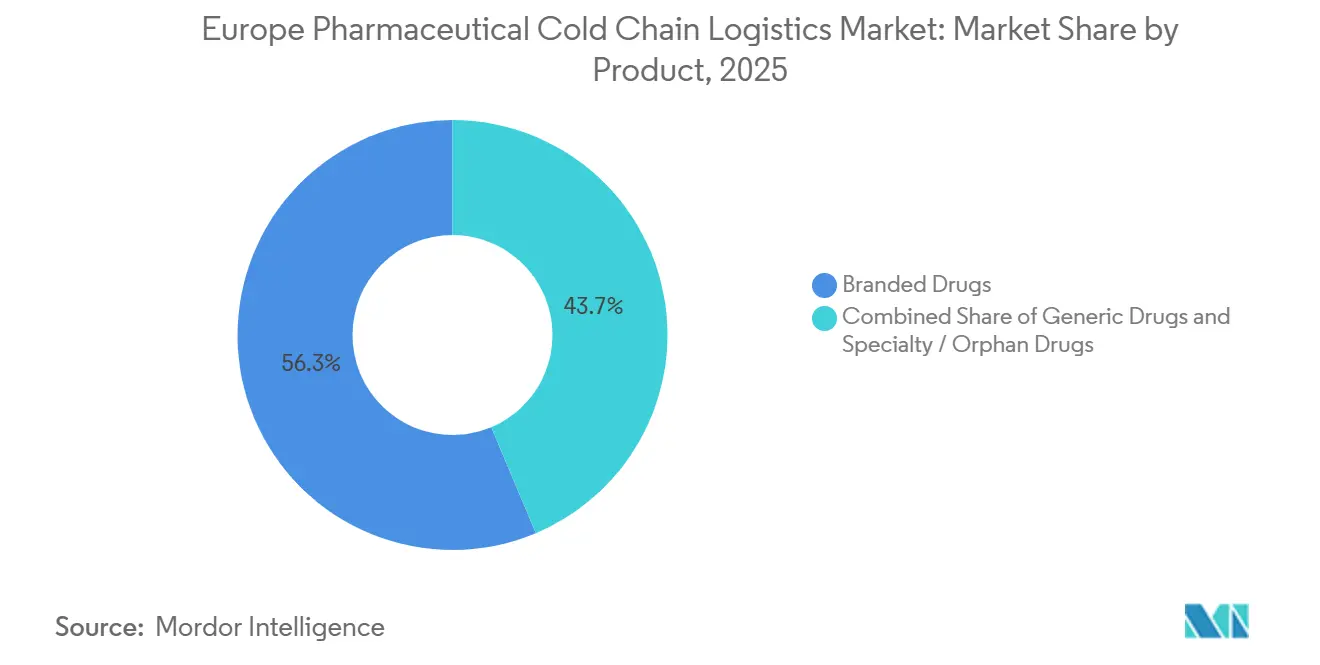

- By product, branded drugs led with a 56.34% market share in 2025, whereas specialty and orphan drugs are set to post the fastest growth at a 5.91% CAGR to 2031.

- By end user, pharmaceutical manufacturers accounted for 40.69% of the Europe pharmaceutical cold chain logistics market size in 2025, but biotech and biosimilar manufacturers are expected to register a 6.27% CAGR over 2026-2031.

- By geography, Germany held 21.05% of the market share in 2025, whereas the Netherlands is poised to grow at a 5.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Pharmaceutical Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in RSV and maternal vaccine launches | +0.9% | EU-wide, led by Germany, France, United Kingdom, Spain | Medium term (2-4 years) |

| Expansion of specialty pharmacy and home infusion networks | +0.7% | Nordic countries, Netherlands, Germany, United Kingdom | Medium term (2-4 years) |

| Investment boom in automated cold warehouses and robotics | +0.8% | Germany, Netherlands, Belgium, France | Long term (≥ 4 years) |

| Cross-border Brexit corridor relabelling hubs | +0.5% | Netherlands, Belgium, Ireland, France | Short term (≤ 2 years) |

| EU-CSRD push toward reusable passive packaging | +0.4% | EU-wide, led by Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Near-shoring of API and fill-finish to Central-Eastern Europe | +0.6% | Poland, Czech Republic, Hungary, Romania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in RSV and Maternal Vaccine Launches

Respiratory syncytial virus vaccines approved in 2024 reshape demand patterns by creating steady, non-seasonal flows that overlay influenza and COVID-19 volumes. Pfizer’s Abrysvo requires 2-8 °C storage and tight administration windows, spurring upgrades in tracking to minimize wastage. Spain’s 2025 immunization schedules now integrate RSV vaccination alongside influenza, reinforcing procurement regularity. Continuous maternal programs demand year-round capacity, expanding the Europe pharmaceutical cold chain logistics market base load. The high unit value of RSV vaccines elevates the cost of temperature excursions, pushing providers to adopt real-time IoT monitoring. These dynamics collectively lift service sophistication standards across the continent[1]“New COVID-19 vaccination recommendations in Spain,” Enfermedades Infecciosas y Microbiología Clínica, elsevier.es.

Expansion of Specialty Pharmacy and Home Infusion Networks

Direct-to-patient models spread in the Nordic region, where digital health infrastructures enable precision scheduling of biologics to households at 2-8 °C. High-value orphan drugs require documented chain-of-custody compliance, triggering growth in value-added services such as patient-specific packaging. German specialty pharmacies increasingly bundle logistics with adherence counseling, shifting volume away from traditional wholesalers. The model’s frequent, small-batch deliveries raise last-mile complexity, rewarding operators with fleets of temperature-controlled vans equipped with active refrigeration. Integration of electronic proof-of-delivery strengthens audit trails and supports reimbursement processes within fragmented European payer systems.

Investment Boom in Automated Cold Warehouses and Robotics

AutoStore cubes, autonomous mobile robots, and AI-driven inventory platforms drive double-digit productivity gains in Dutch and German hubs. Breda’s pharmaceutical campus showcases robotic picking at minus 20 °C, reducing labor exposure to harsh environments and lowering pick errors. Capital outlays surpass USD 50 million for high-throughput facilities, creating scale thresholds that deter smaller entrants. Predictive maintenance algorithms adjust refrigeration loads based on real-time occupancy, trimming energy use amid rising European electricity tariffs. The shortening payback now under five years for top-tier throughput fuels a pipeline of projects announced across Benelux and Bavaria for completion by 2027.

Cross-border Brexit Corridor Relabeling Hubs

Language-specific relabelling and serialization updates for United Kingdom-bound stock cluster in Netherlands and Belgium. Facilities integrate clean-rooms with 2-8 °C storage so packs remain within validated ranges during label changeovers. Centralizing modifications avoids duplicating manufacturing lines, preserving economies of scale for origin plants in Germany and France. Road-feeder services connect Dutch depots with Heathrow and East Midlands airports, bypassing constrained capacity at continental hubs. The segment adds sticky, service-rich revenue that augments the Europe pharmaceutical cold chain logistics market by monetizing regulatory complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Air-cargo cool-chain capacity crunch at major EU hubs | -0.6% | Germany (Frankfurt), Netherlands (Amsterdam), France (Paris CDG) | Short term (≤ 2 years) |

| F-gas phase-out regulations escalating refrigeration CAPEX | -0.8% | EU-wide, especially Southern Europe | Medium term (2-4 years) |

| Rising cyber-attacks on IoT temperature-monitoring platforms | -0.4% | Digitally advanced EU markets | Short term (≤ 2 years) |

| Demand uncertainty from emerging thermostable vaccines | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Air-cargo Cool-chain Capacity Crunch at Major EU Hubs

Frankfurt, Schiphol, and Charles de Gaulle confront limited GDP-certified storage and cool-dolly fleets, causing bottlenecks when multiple wide-body flights carrying vaccines arrive simultaneously. Pharmaceuticals cannot queue on the apron, forcing premium bookings and longer lead times. Seasonal vaccine peaks aggravate congestion, prompting shippers to route through smaller airports or shift to road-feeder services. Infrastructure expansion faces multi-year approval processes, so constrained slots will persist into 2028. Logistics providers hedge by diversifying gateways and investing in cross-dock facilities near secondary airports.

F-gas Phase-out Regulations Escalating Refrigeration CAPEX

EU Regulation 517/2014 mandates a 79% cut in hydrofluorocarbon use by 2030, triggering steep price rises for legacy refrigerants. Operators must retrofit warehouses and vehicles with ammonia or CO₂ systems that demand new safety protocols. Smaller firms struggle to finance conversions, risking exit or acquisition. Southern European depots built before 2010 often need full system replacements, creating capex spikes that delay other modernization projects. Transition timelines squeeze procurement markets already stretched by semiconductor shortages in control electronics[2]“F-gas Regulation,” European Commission, europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Value-Added Capabilities Outpace Core Transport

Transportation services generated 61.76% of the Europe pharmaceutical cold chain logistics market share in 2025, underpinned by the continent’s dense road networks and short haul times. Yet value-added services are forecast to compound at 5.27% CAGR, elevating their contribution to the Europe pharmaceutical cold chain logistics market size, as serialization, kitting, and temperature-monitoring dashboards embed themselves in standard contracts. Road remains the workhorse for 0-8 °C shipments across Schengen borders, while air moves high-value cell therapies under -150 °C.

Acceleration in value-added tasks stems from compliance complexity and the proliferation of direct-to-patient models. Providers now bundle packaging engineering, data analytics, and product recall management, capturing higher margins than commoditized line-haul moves. Warehousing experiences stable but slower growth, with robotics squeezing space needs. Sea and rail expand slowly on sustainability grounds, but speed limits constrain their share to long-shelf-life APIs. Overall, integrated solutions dominate new tenders, forcing smaller carriers to partner or exit[3]European Medicines Agency, “CAR-T Cell Therapies,” EMA, ema.europa.eu.

By Temperature Type: Ultra-Low Segment Captures Therapy Innovation

Chilled products held 40.88% of the Europe pharmaceutical cold chain logistics market size in 2025, reflecting the dominance of vaccines and monoclonal antibodies shipped at 2-8 °C. Deep-frozen and ultra-low lanes, however, are projected to post a 5.61% CAGR through 2031, fuelled by cell and gene therapy scaling. Liquid nitrogen shippers and dry-ice alternatives enable excursion-free transits even on multimodal routes.

Growth concentrates in centers certified for advanced therapy medicinal products, where cryogenic chambers integrate chain-of-identity controls. Frozen (-18 °C) volumes remain niche, supporting select biologics[4]European Medicines Agency, “Advanced Therapy Medicinal Products,” EMA, ema.europa.eu. Ambient holdings lose share as R&D pivots to temperature-sensitive modalities. Investments in ultra-low capex protect incumbents, since entry requires specialized staff comfortable with -80 °C handling and elaborate safety protocols.

By Product: Orphan Drugs Drive Premium Logistics Demand

Branded drugs supplied 56.34% of the market share in 2025 and continue to anchor route density. Specialty and orphan drugs, benefiting from EU incentive frameworks, are forecast to expand at 5.91% CAGR, outstripping the broader Europe pharmaceutical cold chain logistics market. Their high per-dose values demand near-zero spoilage and tight delivery windows, boosting uptake of real-time data loggers and premium white-glove services.

Generic volumes drift toward lower-cost ambient lanes as formulations mature. For autologous therapies, shipments originate and terminate at the same patient, imposing absolute traceability standards. Providers winning these contracts secure sticky, multi-year revenue as switching risk compromises patient safety.

By End User: Biotech Manufacturers Reshape Distribution Models

Pharmaceutical manufacturers retained 40.69% of the market size in 2025, yet biotech and biosimilar players are set to grow at 6.27% CAGR as pipeline richness accelerates. Many emerging biotechs outsource logistics entirely, opting for turnkey solutions from GDP-certified specialists. Biosimilar launches in oncology and immunology intensify intra-EU bulk movements between production and packaging sites, swelling the Europe pharmaceutical cold chain logistics market size.

Hospitals and retail pharmacies adapt to home-care trends, demanding last-mile services that combine delivery with device training. Wholesalers consolidate to preserve bargaining power against manufacturers that favour direct channels. End-user diversification benefits providers with modular service menus, enabling tailored offerings without duplicative overhead.

Geography Analysis

The Netherlands is projected to register a 5.70% CAGR through 2031, propelled by Breda’s A+++ cold-chain campus launched in 2024 and Rotterdam’s role as the EU’s primary seaport for healthcare products. Dutch multilingual talent and streamlined customs processes attract United Kingdom suppliers seeking post-Brexit gateways, embedding sustained volume growth.

Germany, with 21.05% of the 2025 market share, remains the anchor market. Rhine-Neckar manufacturing clusters feed Frankfurt Airport, which, despite slot limits, handles the EU’s highest pharmaceutical tonnage. Government incentives for on-shore API production and robust autobahn connectivity reinforce domestic throughput. The United Kingdom adapts to divergent regulatory frameworks by expanding relabelling depots near Dover and Felixstowe, adding cost layers but preserving market access.

Southern Europe, led by Italy and Spain, experiences steady biologics uptake tied to rising healthcare budgets, though fragmented regional health authorities necessitate multi-node distribution. Central-Eastern Europe enjoys capacity infusions as Poland and the Czech Republic lure fill-finish lines, lengthening intra-EU cold corridors. Nordic countries pioneer home-infusion logistics, piloting drone-assisted deliveries in rural Sweden, innovations likely to diffuse southward over the next decade.

Competitive Landscape

DHL Supply Chain, Kuehne + Nagel, and UPS head the field with continent-wide GDP networks and capital to automate warehouses. DHL’s EUR 2 billion (USD 2.35 billion) program adds Pharma Hubs equipped for multi-temperature docking and AI route optimization. UPS strengthened European reach via the CAD 2.2 billion (USD 1.60 billion) acquisition of Andlauer Healthcare in 2025.

Regional specialists like Movianto and Trans-o-flex capture therapeutic niches, leveraging bespoke packaging and last-mile fleets to differentiate. Cold Chain Technologies’ energy-positive shipper plant in Breda aligns with EU-CSRD goals, appealing to sustainability-focused tenders. F-gas compliance accelerates consolidation, as retrofits exceed EUR 5 million (USD 5.88 million) for mid-sized depots, unaffordable for some independents.

Technological rivalry intensifies around IoT telemetry, blockchain traceability, and warehouse robotics. Cyber-risk resilience becomes a selling point after the 2024 ransomware incident that froze customer portals. Providers offering end-to-end dashboards and 24/7 security operations command premium pricing, reinforcing a moderate-to-high concentration structure for the Europe pharmaceutical cold chain logistics market.

Europe Pharmaceutical Cold Chain Logistics Industry Leaders

DHL Group

Kuehne+Nagel

United Parcel Service of America, Inc. (UPS)

DSV A/S

CMA CGM Group (including CEVA Logistics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: In Poland, Nagel-Group strengthened its temperature-controlled logistics network. Collaborating with LemonTree, the newly established facility enhanced operational efficiency and provided advanced infrastructure for handling delicate food products.

- April 2025: DHL Group announced a EUR 2 billion (USD 2.35 billion) plan to expand GDP-certified Pharma Hubs and temperature-controlled fleets across Europe.

- April 2025: UPS completed its CAD 2.2 billion (USD 1.60 billion) purchase of Andlauer Healthcare Group, boosting global pharma logistics capacity.

- March 2025: DHL Group acquired CRYOPDP, adding 600,000 annual cell-and-gene shipments to its network.

Europe Pharmaceutical Cold Chain Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Chilled (0-5 °C) |

| Frozen (-18 - 0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (Less than-20 °C) |

| Generic Drugs |

| Branded Drugs |

| Specialty / Orphan Drugs |

| Pharmaceutical Manufacturers |

| Biotech and Biosimilar Manufacturers |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Poland |

| Sweden |

| Rest of Europe |

| By Services | Transportation | Road |

| Air | ||

| Sea | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18 - 0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (Less than-20 °C) | ||

| By Product | Generic Drugs | |

| Branded Drugs | ||

| Specialty / Orphan Drugs | ||

| By End User | Pharmaceutical Manufacturers | |

| Biotech and Biosimilar Manufacturers | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Poland | ||

| Sweden | ||

| Rest of Europe |

Key Questions Answered in the Report

What growth rate is forecast for the Europe pharmaceutical cold chain logistics market between 2026 and 2031?

The market is projected to expand at a 4.59% CAGR over 2026-2031.

Which service category is expected to grow fastest?

Value-added services, covering serialization and real-time monitoring, are forecast to register a 5.27% CAGR.

Why is the Netherlands the fastest-growing country market?

Post-Brexit relabelling demand and new A+++ cold-chain campuses are driving a 5.70% CAGR outlook for the Netherlands.

How will EU F-gas rules affect logistics providers?

Operators must replace HFC systems with natural refrigerants, lifting capital expenditure and favoring well-capitalized firms.

Which temperature band is expanding quickest?

Deep-frozen and ultra-low logistics for cell and gene therapies are set to rise at a 5.61% CAGR.

Which end-user group will contribute most to incremental demand?

Biotech and biosimilar manufacturers, growing at a 6.27% CAGR, will drive new contract wins for specialized providers.

Page last updated on: