Europe Real Estate Brokerage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

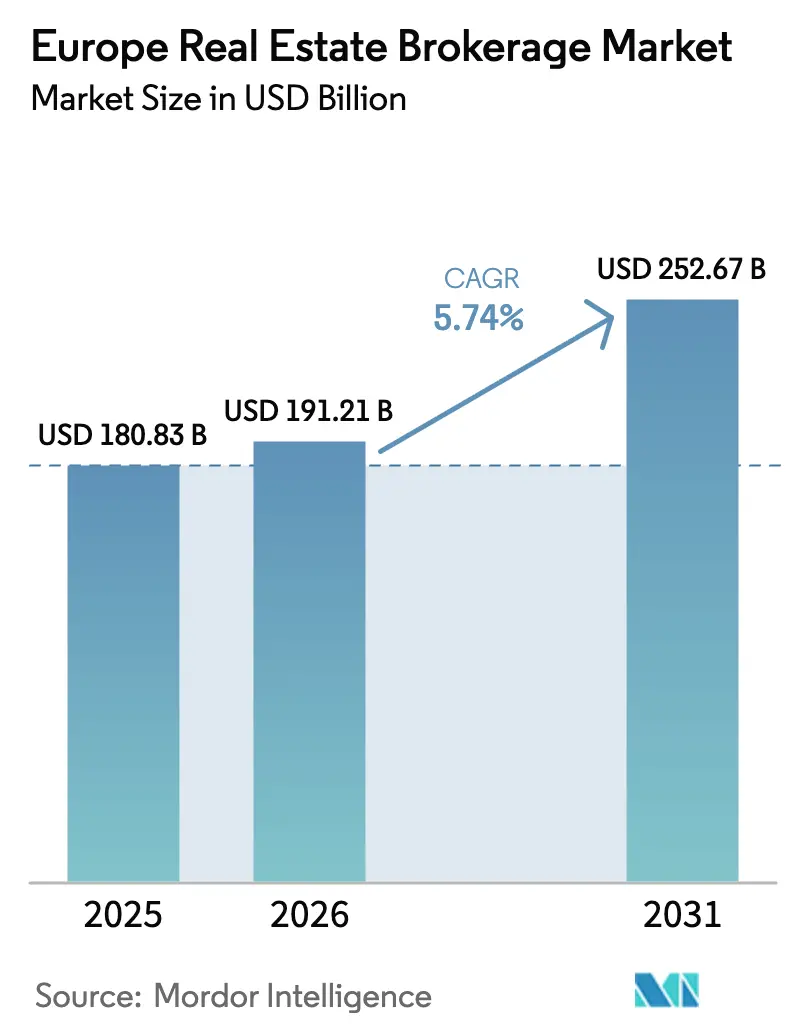

| Base Year Market Size (2025) | USD 180.83 Billion |

| Market Size (2026) | USD 191.21 Billion |

| Market Size (2031) | USD 252.67 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Real Estate Brokerage Market Analysis by Mordor Intelligence

The Europe Real Estate Brokerage Market size is expected to grow from USD 180.83 billion in 2025 to USD 191.21 billion in 2026 and is forecast to reach USD 252.67 billion by 2031 at 5.74% CAGR over 2026-2031. Fading mortgage-rate turbulence, growing cross-border private wealth inflows, and the European Union’s climate-renovation timetable are bringing a reliable pipeline of listings across the region. Leading brokerage houses are reinforcing balance sheets through technology investments that shorten deal cycles and widen investor reach. At the same time, institutional build-to-rent strategies, tokenization pilots, and AI-led lead-generation engines are opening revenue streams that did not exist five years ago. Germany, the United Kingdom, and France anchor the market’s core, yet Southern Europe is now posting the strongest volume expansion as lifestyle buyers and high-net-worth migrants seize price advantages.

Key Report Takeaways

- By property type, residential assets commanded 69.20% Europe real estate brokerage market revenue in 2025. The Europe real estate brokerage market for logistics & industrial properties is set to grow fastest at a 6.05% CAGR between 2026-2031.

- By service, sales transactions generated 62.30% Europe real estate brokerage market revenues in 2025. The Europe real estate brokerage market for rental/leasing brokerage is advancing at a 6.32% CAGR between 2026-2031.

- By client type, individuals and households formed 57.40% of the Europe real estate brokerage market customer base in 2025. The Europe real estate brokerage market for institutional investors shows the quickest rise at a 6.38% CAGR between 2026-2031.

- By geography, Germany led with a 22.70% Europe real estate brokerage market share in 2025. The Europe real estate brokerage market for Spain is projected to expand at a 6.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Real Estate Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stabilizing mortgage rates reviving transaction volumes | +1.2% | Germany, France | Medium term (2-4 years) |

| EU Green Deal renovation mandates driving listings | +1.1% | EU-wide | Medium term (2-4 years) |

| Institutional build-to-rent & SFR fund expansion | +0.9% | United Kingdom, Germany, Sweden | Long term (≥ 4 years) |

| Digital lead-generation & AI valuation tools | +0.8% | United Kingdom, Netherlands | Short term (≤ 2 years) |

| Cross-border HNWI relocation inflows | +0.7% | Core and Mediterranean Europe | Long term (≥ 4 years) |

| Blockchain-enabled property tokenization pilots | +0.4% | Switzerland, Luxembourg | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stabilizing Mortgage Rates Reviving Transaction Volumes

The European Central Bank’s composite cost-of-borrowing indicator for new housing loans held at 3.32% in March 2025, while floating-rate loan pricing slipped 8 basis points to 3.92%[1]European Central Bank, “Composite Cost of Borrowing Indicator: March 2025,” European Central Bank, ecb.europa.eu. This period of rate stability follows an eighteen-month spike that curtailed home financing and shrank brokerage pipelines. In France, outstanding housing credit contracted 0.65% year-on-year as households shelved purchase plans, a pattern now easing with clearer monetary guidance. Brokerages anticipate faster deal execution because 46% of borrowers who had previously cut discretionary spending are preparing to re-enter the market once financing clarity persists. The improving sentiment is most evident in Germany and France, where fixed-rate mortgage products dominate and affordability metrics are rebounding.

Digital Lead-Generation & AI Valuation Tools

JLL introduced Falcon, a proprietary generative-AI engine that taps decades of transactional data to automate prospecting and underwriting, cutting asset-pricing tasks from hours to minutes. CBRE’s Capital AI platform similarly sifts internal and third-party datasets to enlarge buyer pools by up to 20% and sharpen bid-recommendation algorithms. PropTech venture funding reached USD 3.2 billion in 2024, and European start-ups secured USD 700 million of that total, underscoring investor belief in data-centric brokerage models. The net effect is a wider transaction funnel and lower operating cost per deal, advantages that entrenched brands and new entrants alike are leveraging during listing presentations. As a result, AI-enabled houses are gaining share without escalating headcount.

EU Green Deal Renovation Mandates Driving Listings

The revised Energy Performance of Buildings Directive obliges owners to upgrade assets to energy class E (commercial) by 2027 and class D by 2030, or face sale/lease restrictions[2]European Parliament and Council of the European Union, “Revised Energy Performance of Buildings Directive,” Official Journal of the European Union, europarl.europa.eu. Anticipating high retrofit capital needs, many landlords are opting to list early. German legislation sweetens the process through accelerated depreciation on energy-efficient new builds, letting rental investors capture 15-25% annual pre-tax returns. Netherlands-based Energiesprong uses pre-fabricated facades to achieve net-zero upgrades in under 10 days, a solution being piloted in Germany’s EUR 120 billion (USD 141.07 billion) retrofit addressable market. For brokerages, compliance uncertainty becomes an advisory opportunity, as agents bundle contractors, financing sources, and certification services with their core transaction offering.

Blockchain-Enabled Property Tokenization Pilots

Switzerland’s regulator FINMA now recognizes “DLT-shares,” creating a legal wrapper for fractional real-estate ownership that can transfer peer-to-peer on licensed exchanges. Luxembourg is rolling out comparable protections under the Markets in Crypto-Assets Regulation to streamline pan-European passporting. Early pilots have tokenized student-housing blocks and office towers, reducing settlement cycles from weeks to real-time and lowering minimum investor tickets to USD 500. Brokerage houses are building partnerships with tokenization platforms to stay relevant in a scenario where blockchain could eventually disintermediate some conventional middle-office tasks.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mortgage-rate volatility curbing buyer confidence | -0.9% | Southern Europe | Short term (≤ 2 years) |

| EU caps on brokerage commissions | -0.6% | Germany, Netherlands | Medium term (2-4 years) |

| Self-service portals shrinking fee pool | -0.5% | United Kingdom, Nordics | Medium term (2-4 years) |

| Ageing demographics limiting new household formation | -0.3% | Germany, Italy, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mortgage-Rate Volatility Curbing Buyer Confidence

Eurozone mortgage lending grew only 1.5% in 2023 and a muted 2.4% in 2024, pressured by unpredictable financing costs that forced households to defer purchases[3]European Central Bank, “Consumer Expectations Survey: Housing Finance Module 2025,” European Central Bank, ecb.europa.eu. The European Central Bank’s consumer survey shows borrowers with variable-rate loans perceive worsening finances more acutely than fixed-rate peers, clouding transaction sentiment. Spain and Italy remain particularly exposed because floating-rate contracts dominate those markets. While recent rate stabilization is welcome, any renewed inflation shock could reignite hesitation. Brokerages, therefore, keep larger deal backlogs on file, ready to activate once pipeline conditions improve.

EU Caps on Brokerage Commissions

Germany’s 2020 reform splits commission equally between buyer and seller, altering a decades-old buyer-pays model and trimming aggregate fee pools. The Netherlands is debating similar caps, and other member states have signaled consumer-protection reviews. Traditional agents must now justify margins by layering in data analytics, ESG advisory, and relocation services. Digital-first challengers see an opening, but their ultra-low fees often leave sellers handling staging, viewings, and negotiation on their own. As policy harmonizes across the bloc, full-service brokerages face a margin squeeze unless they widen their value bundle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Residential Dominance Faces Commercial Disruption

Residential assets generated 69.20% of Europe's real estate brokerage market revenue in 2025, and the sub-sector is forecast to expand at a healthy clip owing to sustained urban demand and greener-living incentives. Apartments and condominiums remain the workhorse category, especially in Germany and France, where institutional players purchase entire blocks for long-term rental yield. Villas and landed homes cater to the luxury stratum, propelled by millionaire migration into Italy, Portugal, and Switzerland.

The logistics & industrial slice, while smaller today, is registering a 6.05% CAGR through 2031 as e-commerce and nearshoring reorder supply-chain footprints. Investors chase modern warehouses in Spain’s Valencia corridor and Poland’s Silesia hub, where vacancy sits below 4%. Office product shows a mixed outlook as occupiers seek ESG-certified space and right-size footprints for hybrid work. Select retail properties are reviving via adaptive reuse and experiential formats. These nuances allow specialized brokers to craft tailored strategies that defend commission margins even as broad residential competition intensifies.

By Service: Transaction Brokerage Leads Amid Rental Growth

Sales transactions collected 62.30% of 2025 revenue, reflecting the Europe real estate brokerage market size advantages in outright disposals. The segment benefits from owners offloading non-compliant stock ahead of 2030 efficiency deadlines, a process that frequently triggers portfolio rebalancing by institutional players.

Rental/leasing services, showing a 6.32% growth trajectory, capitalize on the region’s pivot toward professionally managed housing and corporate lease flexibility. Build-to-rent pipelines in the United Kingdom alone exceeded 102,000 units under construction in 2025, each requiring multi-year leasing mandates. Ancillary management and valuation add-ons enhance stickiness, offsetting thinner fee percentages relative to sales.

By Client Type: Institutional Investors Drive Market Evolution

Individuals and households provided 57.40% of the 2025 deal volume by count, underscoring their central role in day-to-day listings. Yet institutional investors are the fastest climbers, logging a 6.38% CAGR as pension funds, insurers, and sovereign vehicles allocate more weight to resilient income streams.

Blackstone Property Partners Europe holds a USD 132 billion portfolio spanning 13 countries with 93% occupancy, highlighting the scale and predictability that deep-capital clients offer. For brokers, catering to these investors calls for capital-markets desks, debt-advisory units, and technology that can underwrite thousands of apartments in seconds. Corporate clients, meanwhile, seek lease-renegotiation expertise amid hybrid work shifts, providing steady if slower-growing business.

Geography Analysis

Germany accounts for a commanding 22.70% slice of the Europe real estate brokerage market, underpinned by deep capital pools, transparent land registries, and tax breaks for eco-retrofits that yield 15-25% investor returns. Vonovia SE alone plans 3,000 new units in 2025 and targets 30% growth by 2028, a pipeline that heavily engages domestic brokers. Commission rules now oblige fee-sharing between buyer and seller, squeezing margins but lifting transparency. The United Kingdom remains the region’s top cross-border investment magnet. CBRE’s 2024 Investor Intentions Survey again placed the UK first for incoming global capital. London home prices advanced 4.8% in 2024, says Foxtons, thanks to mild rate relief and a resumption of Asian buyer visits. Challenges include the expiry of Stamp Duty relief in April 2025 and a forecast net outflow of 9,500 millionaires owing to changes in non-dom tax status. Even so, brokers are leveraging digital conveyancing and AI chatbots to cut completion times and preserve service differentials.

France is staging a cautious rebound: BNP Paribas Real Estate logged USD 3.6 billion (EUR 3.4 billion) of commercial deals in Q1 2025, 67% above Q1 2024 yet still 28% below the five-year norm. Spain offers the fastest growth at a 6.12% CAGR to 2031, buoyed by tourism-fueled rental demand and capital drawn from Latin American family offices. Italy benefits from investor-visa reforms that streamline high-net-worth arrivals, driving prime-residential trades in Milan and Lake Como. The Netherlands and Sweden illustrate cutting-edge green-building practices, while Switzerland pioneers tokenized property frameworks enforced by FINMA. Collectively, these sub-regions provide diversified deal flow that mitigates country-specific shocks and broadens brokerage revenue stability.

Competitive Landscape

The Europe real estate brokerage market is moderately fragmented. CBRE, JLL, and Savills lead in commercial deals, whereas regional champions dominate the residential sphere. CBRE’s USD 400 million share purchase in flex-office operator Industrious and its addition of Turner & Townsend expanded advisory capabilities across project management and cost consulting. JLL’s Falcon AI roll-out now covers valuation, leasing, and debt advisory, giving the firm a data edge that shrinks underwriting time.

Digital challengers add new dynamics: Scout24’s buyout of bulwiengesa AG layers valuation analytics atop Germany’s largest property portal. Baltic Classifieds Group acquired UNTU.lt, integrating automated appraisal tools across Baltic listings. In Spain, Tiko’s merger with Housell forged the nation’s biggest digital broker, promising same-day online offers for sellers. Despite headline noise, most pure-online models struggle to retain market share once homeowners confront the complexity of larger or cross-border transactions.

Compliance capability is emerging as a strategic moat. The new EU Regulation 2024/1624 obliges brokers to conduct enhanced due diligence on all deals exceeding USD 10,800 (EUR 10,000). Large incumbents already field specialist AML teams and reg-tech integrations, whereas smaller shops bear rising fixed costs. ESG advisory forms another battleground, with firms adding engineers and carbon-modeling software to help landlords hit 2030 energy-performance thresholds.

Europe Real Estate Brokerage Industry Leaders

CBRE Group

Jones Lang LaSalle (JLL)

Savills

Knight Frank

Colliers International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Baltic Classifieds Group purchased UNTU.lt, Lithuania’s premier digital valuation portal, broadening data services throughout the Baltic property ecosystem.

- February 2025: Scout24 SE acquired bulwiengesa AG, adding enterprise-grade valuation analytics to its residential and commercial listings in Germany.

- January 2025: BNP Paribas Real Estate completed its USD 5.5 billion (EUR 5.1 billion) acquisition of AXA Investment Managers’ real-estate arm, creating an asset-management platform overseeing USD 1.6 trillion across Europe.

- October 2024: Foxtons Group PLC bought two regional estate agencies for USD 17.0 million (GBP 12.6 million), extending its reach into London’s commuter belts.

Europe Real Estate Brokerage Market Report Scope

The real estate brokerage industry facilitates property transactions for individuals and businesses, covering buying, selling, renting, and leasing. It is staffed by licensed professionals, including brokers and agents, who act as intermediaries, linking buyers to sellers, landlords to tenants, and property owners to investors. A complete background analysis of the European real estate brokerage market, including the assessment of the economy and contribution of sectors in the economy, market overview, market dynamics, market size estimation for key segments, emerging trends in the market segments, and geographical trends, is covered in the report.

The European real estate brokerage market is segmented by type (residential and non-residential), service (sales and rental), and country (Germany, United Kingdom, France, and Rest of Europe). The report offers market sizes and forecasts for all the above segments in value (USD).

| Residential | Apartments & Condominiums |

| Villas & Landed Houses | |

| Commercial | Office |

| Retail | |

| Logistics & Industrial | |

| Other Commercial (Hospitality, Mixed-Use) |

| Sales |

| Rental / Leasing |

| Individuals / Households |

| Corporates & SMEs |

| Institutional Investors |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Russia |

| Rest of Europe |

| By Property Type | Residential | Apartments & Condominiums |

| Villas & Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Logistics & Industrial | ||

| Other Commercial (Hospitality, Mixed-Use) | ||

| By Service | Sales | |

| Rental / Leasing | ||

| By Client Type | Individuals / Households | |

| Corporates & SMEs | ||

| Institutional Investors | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current Europe real estate brokerage market size?

The Europe real estate brokerage market size is USD 191.21 billion in 2026 and is on track to reach USD 252.67 billion by 2031.

Which country holds the biggest share of the Europe real estate brokerage market?

Germany leads with 22.70% of the Europe real estate brokerage market share in 2025, thanks to deep capital pools and clear regulation.

Which property segment is growing the fastest?

Logistics & industrial real estate is the fastest-growing property segment, advancing at a 6.05% CAGR through 2031 as e-commerce and nearshoring lift demand.

How are EU energy-efficiency rules affecting brokerage activity?

The Energy Performance of Buildings Directive is prompting many owners to sell or upgrade before 2030 deadlines, increasing listing volumes and consultancy demand.

Why are institutional investors important to the market’s growth?

Pension funds, insurers, and private-equity houses are scaling build-to-rent and logistics portfolios, driving a 6.38% CAGR for the institutional client segment and pushing larger, fee-rich transactions into brokers’ pipelines.

Page last updated on: