Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

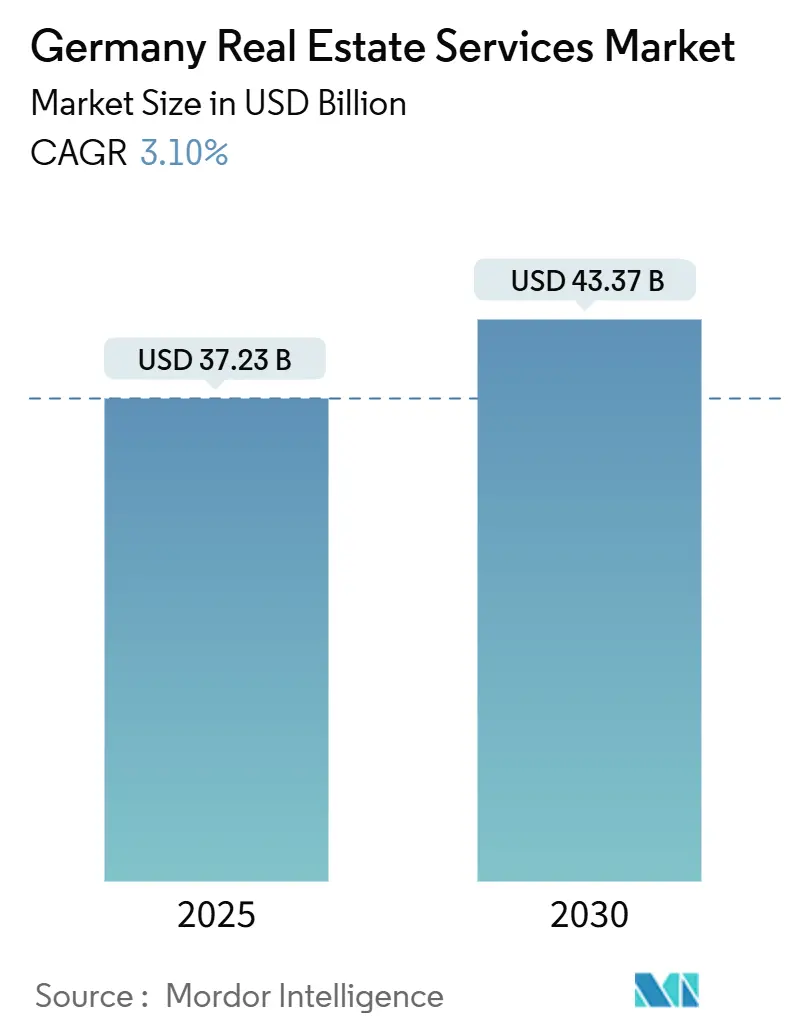

| Market Size (2025) | USD 37.23 Billion |

| Market Size (2030) | USD 43.37 Billion |

| Growth Rate (2025 - 2030) | 3.10% CAGR |

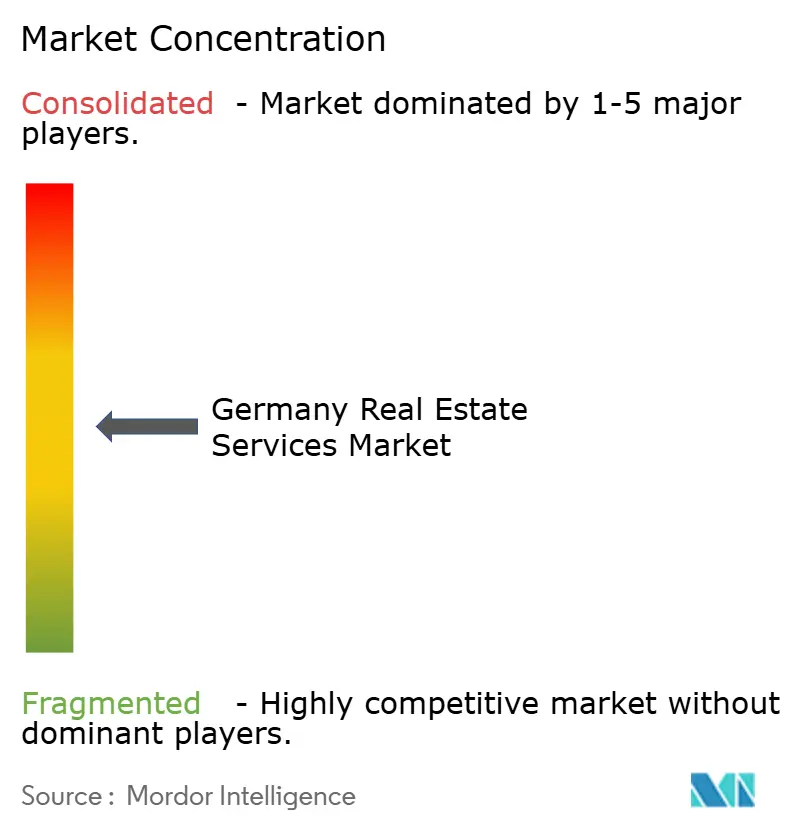

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Real Estate Services Market Analysis by Mordor Intelligence

The Germany Real Estate Services Market size is estimated at USD 37.23 billion in 2025, and is expected to reach USD 43.37 billion by 2030, at a CAGR of 3.10% during the forecast period (2025-2030). Recent growth is powered by institutional capital rotation into ESG-compliant assets, steady demand for project management linked to mandatory energy-efficiency upgrades, and rapid digitalization of property workflows. Brokerage fee reforms and lingering affordability pressures have tempered transaction-led revenues, yet recurring income from property and facility management continues to underpin sector resilience. Competitive conditions remain moderate as large, full-service providers leverage scale, while PropTech entrants press for share through data-rich, software-enabled offerings. Policy tools such as degressive depreciation allowances for new housing and expanded infrastructure quotas for regulated investors signal sustained government support and will likely reinforce medium-term service demand.

Key Report Takeaways

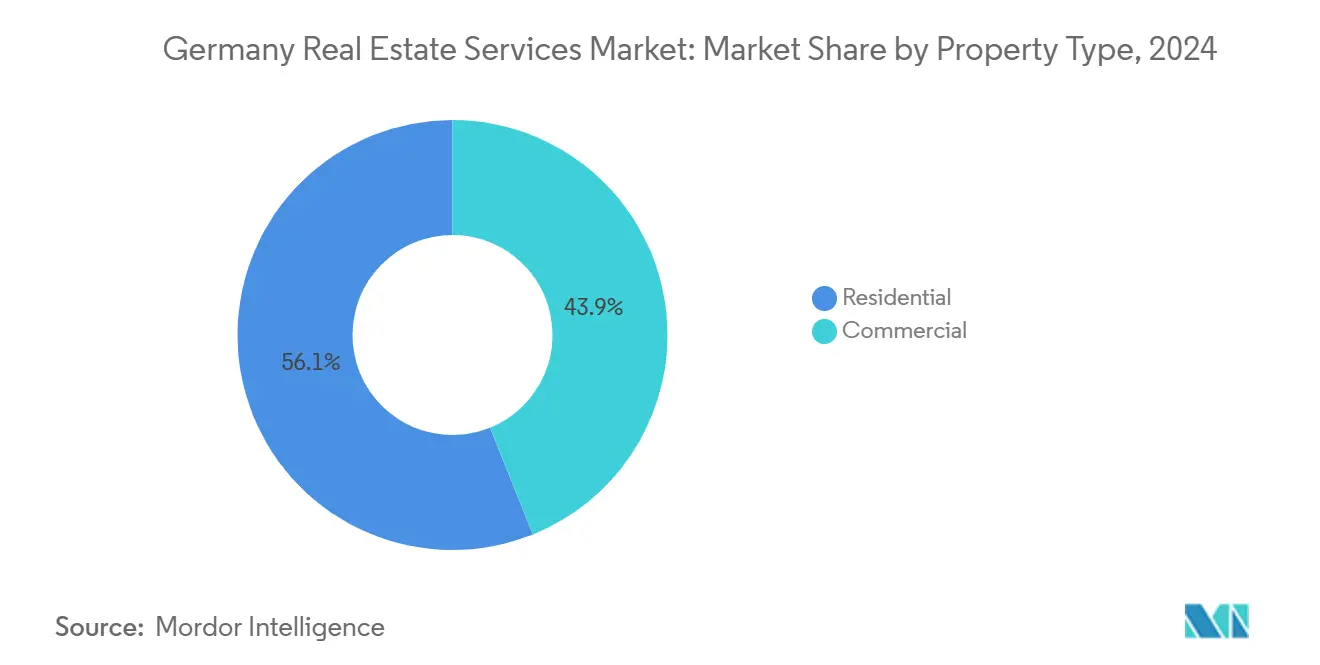

- By property type, residential retained 56.1% of the Germany real estate services market revenue share in 2024. The Germany real estate services market for commercial recorded the fastest 3.56% CAGR between 2025-2030.

- By service, property management led with 42.3% of the Germany real estate services market share in 2024. The Germany real estate services market for valuation services is projected to expand at a 4.15% CAGR between 2025-2030.

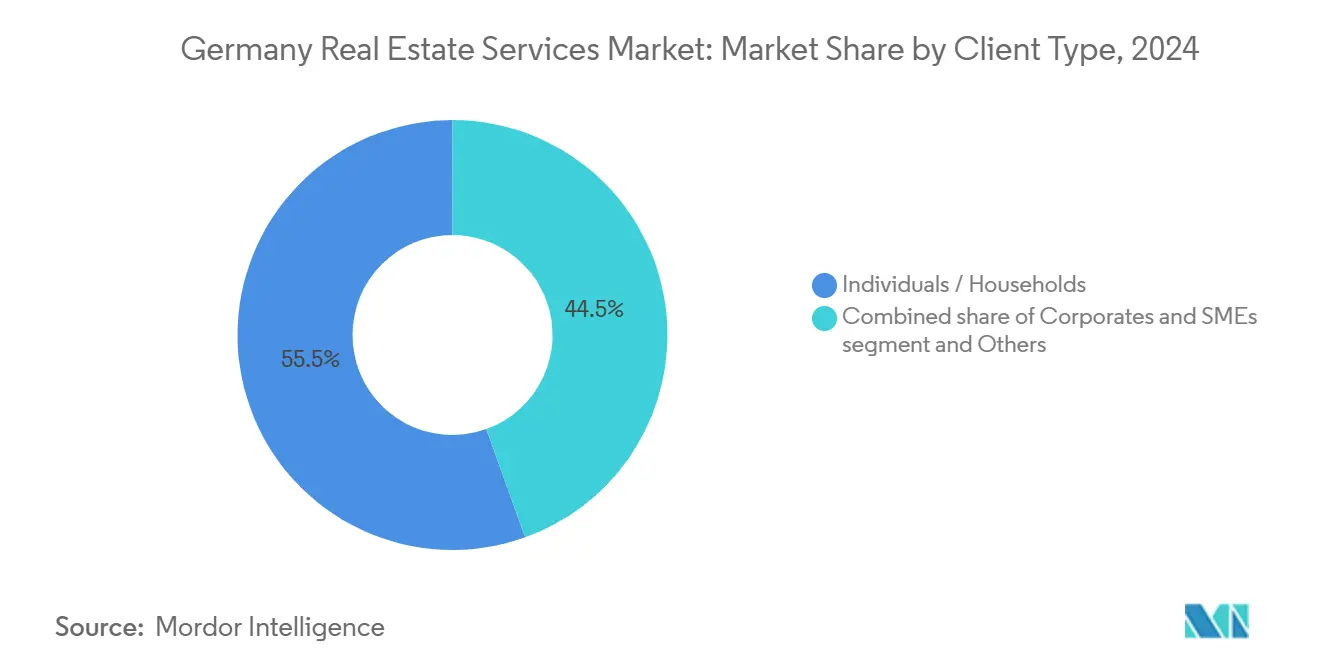

- By client type, individual households generated 55.5% of the Germany real estate services market size in 2024. The Germany real estate services market for corporate & SME clients shows the highest 3.91% CAGR between 2025-2030.

- By city, Berlin captured 26.7% of the Germany real estate services market’s 2024 revenues. The Germany real estate services market for Frankfurt posts the strongest 4.02% CAGR between 2025-2030.

Germany Real Estate Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Institutional demand for outsourced facility and property management | +0.8% | National; Berlin, Munich, Frankfurt | Medium term (2-4 years) |

| Rising retrofit demand under energy-efficiency targets | +0.7% | Urban centers nationwide | Medium term (2-4 years) |

| Expansion of ESG reporting mandates | +0.6% | National; early adoption in major metros | Short term (≤ 2 years) |

| Digital transformation across real-estate portfolios | +0.5% | National; commercial first movers | Short term (≤ 2 years) |

| Greater pension-fund capital for core office & logistics | +0.4% | Top-7 cities | Medium term (2-4 years) |

| ADU-friendly zoning reforms | +0.3% | Baden-Württemberg, Berlin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Institutional Demand for Outsourced Facility and Property Management

Hospitals and public agencies are moving non-core real-estate operations to specialist providers to manage complexity and regulatory risk. Fresenius Helios illustrates the shift by prioritizing external expertise for energy management and digital building systems, securing predictable cost structures and compliance benefits. Municipal authorities, facing budget pressure, adopt similar strategies, creating long-term contracts that stabilize revenues for facility managers. As outsourcing scales, providers broaden technical depth, from HVAC optimization to smart-sensor maintenance, to meet performance guarantees. This driver will keep recurring income streams buoyant across the Germany real estate services market as public and healthcare assets grow.

Expansion of ESG Reporting Mandates Boosting Valuation and Advisory Volumes

Disclosure rules now require granular data on carbon intensity and social impact, prompting insurers holding 13.1% of portfolios in real estate to seek deeper due diligence services. Advisory firms equipped with climate-risk analytics gain share because investors must substantiate acquisitions against evolving taxonomy criteria. Valuers incorporate flood, heat-stress, and green-capex metrics, positioning ESG-savvy practices for premium pricing. Enhanced reporting complexity raises entry barriers, cementing the advantage of firms with established sustainability credentials. Rising regulatory clarity should accelerate assessment demand over the next two years.

Rising Demand for Retrofit Project Management Under Energy-Efficiency Targets

Germany’s Bundesförderung für effiziente Gebäude program subsidizes up to 40% of renovation costs, pushing landlords to upgrade thermal envelopes and mechanical systems[1]Federal Ministry for Economic Affairs and Climate Action, “Bundesförderung Für Effiziente Gebäude Program Overview,” BMWK, bmwk.de. Specialist project managers coordinate contractors, financing, and ESG reporting, capturing significant fee pools. Techniques such as Energiesprong’s prefabricated façades cut on-site disruption and meet net-zero standards. Continuous funding and regulatory deadlines keep retrofit pipelines broad, ensuring medium-term growth in advisory and construction oversight services[2]Claudia Kemfert, “Energy-Efficient Building Retrofits and Economic Growth,” DIW Weekly Report, diw.de. Providers with proven track records in occupied-building projects hold a competitive edge.

Greater Pension-Fund Capital Deployment into Core Assets

Regulatory expansion of infrastructure quotas to 5% lets pension funds reallocate toward logistics parks and prime offices, boosting deal sizes and asset-management mandates[3]Deutsche Bundesbank, “Institutional Investors’ Asset Allocation Statistics 2025,” Bundesbank, bundesbank.de. Institutions demand full-service partners who deliver acquisition due diligence, ongoing facility optimization, and ESG compliance. Larger tickets support multi-year revenue visibility for service providers. Concentrated allocations in the top seven cities also intensify competition for class-A management contracts, uplifting standards across the Germany real estate services market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak residential transactions from affordability strain | -0.7% | National; high-cost metros | Medium term (2-4 years) |

| Commission compression after brokerage-fee reform | -0.5% | Nationwide | Short term (≤ 2 years) |

| Tight labor market for skilled FM technicians | -0.4% | Major cities nationwide | Long term (≥ 4 years) |

| Lengthy permitting cycles slowing advisory pipelines | -0.3% | Baden-Württemberg, Berlin | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Weakness in Residential Transactions Due to Affordability Pressures

Higher interest rates and construction costs have sidelined first-time buyers, shrinking deal volumes and elongating sales cycles. Broking firms now split commissions equally with buyers under the 2020 reform, reducing gross margins just as transaction counts fall. Knock-on effects hit mortgage advisory, conveyancing, and ancillary valuation work. Recovery requires interest-rate stability and expanded housing supply, making this headwind likely to persist through 2027. Service providers are diversifying toward rental-focused and asset-management income to offset the mismatch.

Tight Labor Market for Skilled FM Technicians and Asset Managers

Smart buildings need technicians versed in digital twins, ESG data, and complex HVAC systems, yet apprenticeship pipelines lag demand. Wage escalation is most acute in Berlin, Munich, and Frankfurt, eroding provider margins where service-level agreements lock fees. Asset-management roles demand analytics capability plus regulatory fluency, intensifying the talent scramble. Limited workforce growth constrains contract onboarding capacity, capping near-term market expansion. Companies invest in upskilling programs, but time-to-competency keeps supply tight for several years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Commercial Gains Despite Residential Dominance

Residential services contributed 56.1% of 2024 revenues, led by multi-family rental demand, yet commercial contracts are expanding fastest at a 3.56% CAGR to 2030. Logistics growth rides e-commerce fulfillment needs, while core offices in Frankfurt and Munich attract ESG-compliant capital seeking stable yields. Data-center square footage is forecast to double by 2030, driving high-margin facility-management and power-quality advisory work. Conversely, single-family brokerage lags as affordability weighs on first-time buyers, though ADU reforms may add incremental listings over the long run.

Market participants diversify by pairing residential management platforms with specialized commercial advisory teams to capture the full asset lifecycle. ESG retrofits, particularly in older offices, spur bundled project-management and valuation mandates. Residential providers deploy tech-enabled solutions such as virtual property inspections to trim costs and sustain margins amid slower sales. Meanwhile, the Germany real estate services market continues to allocate more capital to warehousing and data-center clusters, where long-lease tenures stabilize income and offset cyclical swings in retail and hospitality assets.

By Service: Valuation Services Accelerate Amid Management Stability

Property management preserved a 42.3% revenue share in 2024, reflecting sticky contracts and the recurring nature of rent-collection and maintenance tasks. Valuation, however, is set to outpace all services with a 4.15% CAGR as investors need climate-risk scoring and social-impact benchmarking. Scout24’s integration of bulwiengesa aligns with this trend, adding dense data sets and AI-driven comparables that streamline appraisal turnarounds.

Facility-management firms embed IoT dashboards to prove service-level compliance, creating upsell paths into energy-performance contracting. Brokerage teams adopt virtual tours and predictive lead-scoring, preserving productivity despite thinner commissions. Across offerings, digitalization trims back-office costs and underpins competitive fees, ensuring that the Germany real estate services market remains accessible to midsize enterprises while raising the bar on service quality.

By Client Type: Corporate Outsourcing Drives Growth

Individual households still account for 55.5% of 2024 demand, but corporate and SME customers are the fastest risers at 3.91% CAGR. Healthcare group Fresenius Helios outsources integrated facility management to tighten operational budgets and meet stringent hygiene standards. Public-sector landlords shift energy-performance risk to contractors, spurring multi-year agreements that lock in predictable cash flows.

Service providers bundle advisory, maintenance, and regulatory reporting into single-source contracts, creating higher switching costs and longer retention. Individual homeowner services pivot to self-service portals and automated valuation models to stay cost-competitive. Corporate clients seek real-time portfolio dashboards, ESG compliance alerts, and decarbonization roadmaps, raising the sophistication bar and enlarging wallet share per account. This tilt toward enterprise outsourcing underpins steady expansion even if consumer transactions remain subdued.

Geography Analysis

Berlin retained a 26.7% revenue share in 2024 on the back of diverse demand from federal agencies, embassies, and a vibrant rental market. Energy-efficiency upgrade mandates and streamlined digital permitting are generating advisory backlogs, while public-private regeneration schemes expand the pipeline for project managers. However, rising land prices and rent caps keep pressure on brokerage income, incentivizing managers to diversify into retrofit consulting and asset-monitoring services.

Frankfurt is the growth pacesetter with a 4.02% CAGR to 2030, buoyed by record office take-up of 198,100 sqm in Q1 2025 and accelerating data-center builds. Prime office rents reached EUR 51.00 (USD 55.6) per sqm per month, indicating deep demand for class-A space. Financial institutions favor energy-efficient towers, generating premium management and valuation assignments. The city’s evolving skyline also attracts pension-fund capital, entrenching long-term service contracts.

Munich benefits from technology-sector clustering, supporting steady office and life-science facility management work. Hamburg leverages port logistics to drive warehouse and cold-chain advisory needs. Secondary metros like Stuttgart, Düsseldorf, and Leipzig, grouped under Rest-of-Germany, collectively rival any single top-tier city in volume. Their polycentric economic profiles mean tailored service bundles—from student-housing management in university towns to light industrial valuation—making geographic diversification a hedge against localized slowdowns. Overall, city-level competition pushes providers to sharpen sector specializations and deploy tech platforms that scale across urban contexts, ensuring the Germany real estate services market keeps momentum nationwide.

Competitive Landscape

The Germany real estate services market shows moderate concentration. Vonovia leverages a 546,000-unit residential portfolio to integrate in-house maintenance, energy services, and tenant apps, supporting scale economies. CBRE Germany capitalizes on global capital markets expertise to win cross-border mandates, recently advising on several Frankfurt skyscraper disposals. JLL extends its global ESG consulting tool set to German clients, positioning itself for regulatory-driven advisory growth.

Scout24’s 2024 purchase of bulwiengesa gave the firm a data moat that strengthens valuation products and deepens client stickiness within its ImmoScout24 ecosystem. Smaller PropTechs focus on niche pain points—such as rental deposit management or IoT-based leak detection—often partnering with incumbents rather than challenging them head-on. Healthcare and data-center facility management represent attractive white spaces, demanding specialized compliance and uptime guarantees. Across the board, digital adoption, ESG fluency, and integrated service suites are the core strategic differentiators shaping competitive outcomes in the Germany real estate services market.

Germany Real Estate Services Industry Leaders

Vonovia SE

Deutsche Wohnen

LEG Immobilien SE

Instone Group

Vivawest Wohnen GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vonovia SE acquired 820 residential units and 261 commercial units from QUARTERBACK Immobilien-Gruppe. Strengthening core residential portfolio and property-management services.

- January 2025: Vonovia SE Acquired 19 care properties and agreed to purchase PFLEGEN & WOHNEN HAMBURG GmbH (13 care-home locations) for EUR 380 million (USD 414 million). Expanding into healthcare real-estate services sector.

- December 2024: Scout24 SE acquired bulwiengesa AG, a leading valuation and data-services provider. Enhancing Scout24’s analytics capabilities and market transparency via ImmoScout24 ecosystem.

- December 2024: Scout24 SE acquired neubau kompass AG, a digital marketing platform for newly built residential properties in Germany and Austria. Extending Scout24’s reach in the new-construction segment.

Germany Real Estate Services Market Report Scope

By Property Type

| Residential | Single-Family |

| Multi-Family | |

| Commercial | Office |

| Retail | |

| Logistics | |

| Others |

By Service

| Brokerage Services |

| Property Management Services |

| Valuation Services |

| Others |

By Client Type

| Individuals / Households |

| Corporates & SMEs |

| Others |

By City

| Berlin |

| Munich |

| Frankfurt |

| Hamburg |

| Rest of Germany |

| By Property Type | Residential | Single-Family |

| Multi-Family | ||

| Commercial | Office | |

| Retail | ||

| Logistics | ||

| Others | ||

| By Service | Brokerage Services | |

| Property Management Services | ||

| Valuation Services | ||

| Others | ||

| By Client Type | Individuals / Households | |

| Corporates & SMEs | ||

| Others | ||

| By City | Berlin | |

| Munich | ||

| Frankfurt | ||

| Hamburg | ||

| Rest of Germany | ||

Key Questions Answered in the Report

What is the current value of the Germany real estate services market?

The market is valued at USD 37.23 billion in 2025, with a forecast to reach USD 43.37 billion by 2030.

Which property type is expanding fastest?

Commercial real-estate services are projected to grow at a 3.56% CAGR, outpacing residential services through 2030.

Why are valuation services gaining momentum?

Intensifying ESG disclosure rules require detailed climate-risk and social-impact assessments, pushing valuation revenue to a 4.15% CAGR.

How are brokerage fee reforms affecting service providers?

The 2020 law that splits commissions evenly between buyers and sellers has compressed margins, driving consolidation among smaller brokers.

Which city offers the strongest growth outlook?

Frankfurt leads with a projected 4.02% CAGR thanks to robust office demand and rapid data-center development.

What technologies are shaping the industry’s future?

IoT sensors, digital twins, and data-rich valuation platforms are enabling predictive maintenance, real-time portfolio monitoring, and faster due-diligence cycles across the sector.

Page last updated on: