Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

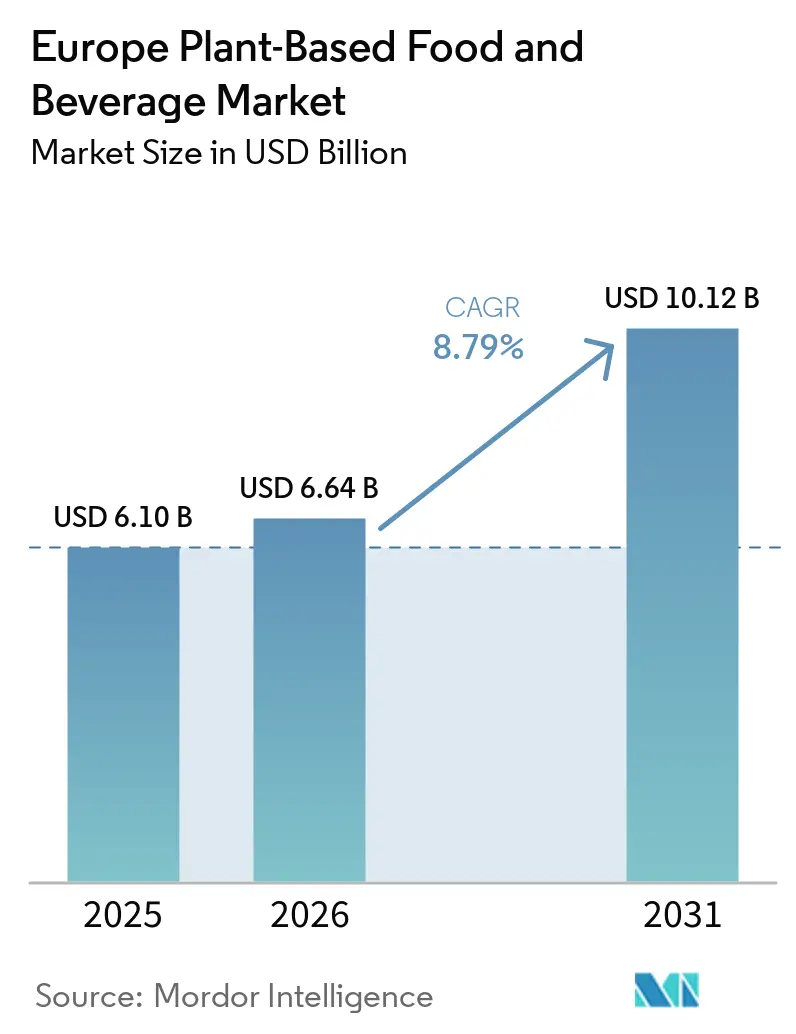

| Base Year Market Size (2025) | USD 6.10 Billion |

| Market Size (2026) | USD 6.64 Billion |

| Market Size (2031) | USD 10.12 Billion |

| Growth Rate (2026 - 2031) | 8.79% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Plant-Based Food and Beverage Market Analysis by Mordor Intelligence

By 2025, the European market size for plant-based food and beverages is set to hit USD 6.10 billion, with projections of USD 6.64 billion in 2026 and a leap to USD 10.12 billion by 2031. This marks a robust CAGR of 8.79% from 2026 to 2031. With steady policy backing, a broader product range, and evolving consumer preferences, it's evident that Europe's shift towards plant-based sources is more than just a fleeting trend. Retailers are increasingly allocating shelf, chiller, and freezer space to plant-based items, especially as private-label products edge closer in price to their animal-based counterparts. The EU Green Deal's sustainability regulations are tightening the financial reins on traditional meat and dairy, simultaneously incentivizing low-carbon food technologies. This dynamic bolsters the appeal of Europe's plant-based market. Foodservice operators are tailoring menus for flexitarian diners, while start-ups benefit from expedited EU novel-food reviews, shortening their development cycles. As investments surge, established players are turning to acquisitions for market defense. However, mid-tier firms without distinct differentiation or economies of scale continue to grapple with margin pressures.

Key Report Takeaways

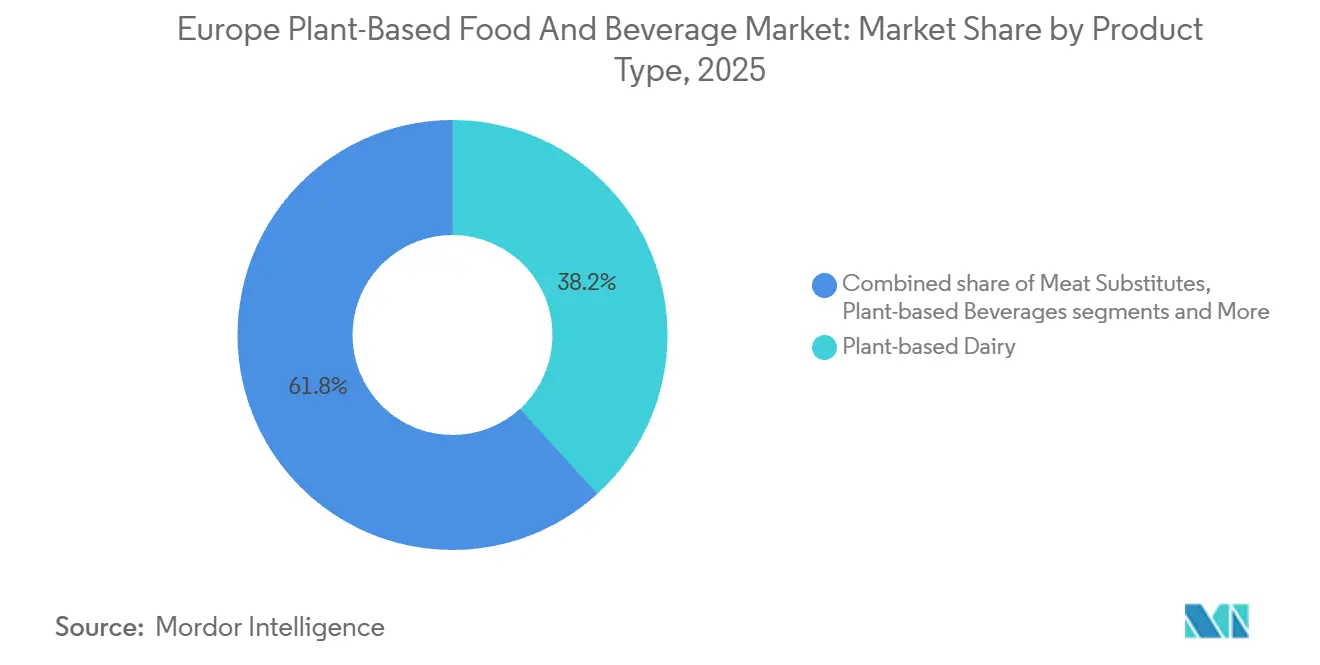

- By product type, plant-based dairy led with 38.24% of the Europe plant-based food and beverage market share in 2025, while plant-based bakery is forecast to expand at an 8.97% CAGR through 2031.

- By ingredient, soy commanded 45.05% of the Europe plant-based food and beverage market size in 2025, but rice-based formulations are advancing at a 9.02% CAGR over 2026-2031.

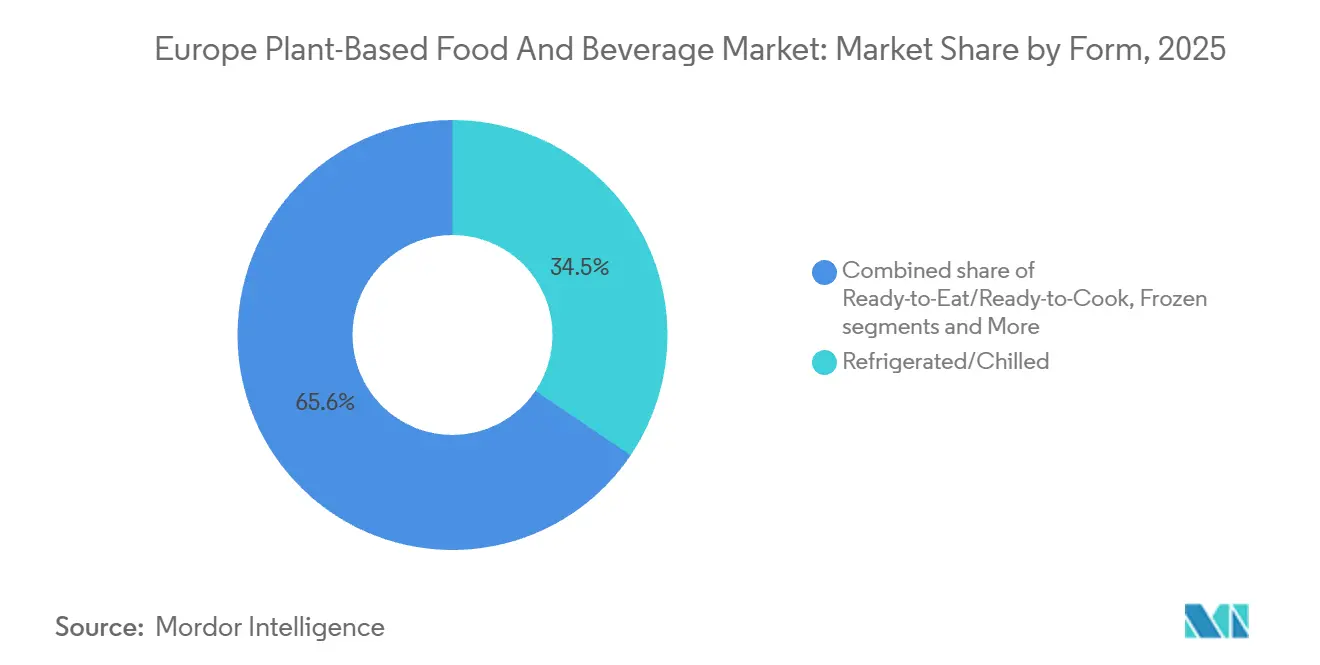

- By form, refrigerated products represented 34.45% value share in 2025, whereas frozen formats are projected to advance at a 9.55% CAGR to 2031.

- By distribution channel, off-trade held 75.35% share of the Europe plant-based food and beverage market size in 2025, yet on-trade is pacing fastest at a 10.31% CAGR through 2031.

- By Country, Germany retained 35.68% revenue in 2025, while Spain is set to post a 9.35% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Plant-Based Food and Beverage Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising health consciousness and lactose intolerance prevalence | +2.1% | Germany, UK, Netherlands, Nordic countries | Medium term (2-4 years) |

| Demand for functional, fortified plant-based beverages | +1.8% | Germany, France, UK, urban centers across Europe | Medium term (2-4 years) |

| Shift toward vegan, vegetarian, and flexitarian diets | +1.5% | Germany, UK, Sweden, Netherlands, urban Spain and Italy | Long term (≥ 4 years) |

| EU Green Deal and sustainability regulations | +1.4% | EU-wide, strongest in Germany, France, Netherlands, Sweden | Long term (≥ 4 years) |

| Expanded retail and e-commerce availability | +1.2% | Germany, UK, France, Spain, Poland | Short term (≤ 2 years) |

| Influence of urban millennials and Gen Z wellness trends | +0.9% | Urban centers: Berlin, London, Paris, Amsterdam, Barcelona | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Lactose Intolerance Prevalence

European health systems are increasingly focusing on preventive care in their nutrition policies, driving plant-based diets from niche to mainstream adoption. According to the World Health Organization's 2025 European Regional Obesity Report, 59% of adults in the region are either overweight or obese[1]Source: World Health Organization, "WHO/Europe sets the course for reducing obesity in Southern European countries", who.int. To address this, national health agencies are promoting plant-forward diets as a cost-effective solution to improve public health. Lactose intolerance affects approximately 65% of the global adult population, with rates in Southern and Eastern Europe reaching as high as 70-90%. However, many cases remain undiagnosed because symptoms are often mistaken for irritable bowel syndrome. This misdiagnosis creates hidden demand, as individuals who try plant-based dairy products often experience symptom relief and continue their use. In 2024, Germany's Federal Ministry of Food and Agriculture introduced a program to include plant-based options in school meal plans. This initiative exposes 8 million children to non-dairy alternatives, encouraging healthier consumption habits from a young age. Similarly, in 2025, the UK's National Health Service updated its Eatwell Guide to recommend fortified plant-based milk as a source of calcium. This endorsement has further legitimized plant-based products in clinical nutrition discussions, reinforcing their role in balanced diets. These developments reflect a growing shift in European health strategies, emphasizing plant-based nutrition as a key component of preventive healthcare.

Demand for Functional, Fortified Plant-Based Beverages

Functional beverages are gaining popularity over traditional plant-based milks as consumers look for products offering multiple health benefits beyond basic nutrition. In 2025, Oatly introduced a barista-edition oat milk fortified with vitamin D3 derived from lichen and calcium carbonate. This “European functional beverage” is designed to address the vitamin D deficiency experienced by 40% of Northern Europeans during winter, positioning it as a preventive health solution rather than just a dairy alternative. This product is designed to address the vitamin D deficiency experienced by 40% of Northern Europeans during winter, positioning it as a preventive health solution rather than just a dairy alternative. Similarly, the European Academy of Allergy and Clinical Immunology updated its infant nutrition guidelines in 2024, allowing fortified plant-based formulas for infants with cow's milk protein allergy, a condition affecting 2-3% of infants. However, regulatory approvals for these formulas remain specific to each country. In the same year, Danone’s Alpro brand launched a high-protein soy drink containing 10 grams of protein per 250 ml serving. This product directly competes with whey-based sports nutrition drinks, expanding its reach to a broader audience beyond traditional plant-based consumers. Additionally, advancements in precision fermentation technology are driving innovation in fortification strategies. Startups are now producing animal-free whey proteins that can be added to plant-based beverages. These proteins enhance the amino acid profiles of the drinks without triggering allergen warnings, offering a significant advantage in the market. These developments highlight the growing demand for functional and fortified plant-based beverages.

Shift Toward Vegan, Vegetarian, and Flexitarian Diets

Flexitarians, individuals who reduce their consumption of animal products without eliminating them entirely, are the fastest-growing dietary group. In 2024, the World Animal Foundation reported that 3.2% of the European population identified as vegan[2]World Animal Foundation Organization, "Vegetarian Statistics 2026: Global Facts, Diet Trends & Market Growth", worldanimalfoundation.org. Unlike vegans, flexitarians focus on taste, texture, and price when choosing plant-based products, treating them as alternatives to animal products rather than ethical necessities. The UK's National Food Strategy, published in 2024, recommended reducing meat consumption by 30% by 2032 to meet climate goals, reinforcing the importance of flexitarian diets. Similarly, Sweden updated its dietary guidelines in 2025 to promote plant-based protein sources, equating legumes to meat in nutritional value. This shift has influenced public food policies, including school meal planning and procurement strategies. In Germany, ProVeg International reported in 2025 that 14% of the population identified as flexitarian, up from 9% in 2022. This growth is driven by increasing awareness of climate change and health benefits, with less emphasis on animal welfare. Meanwhile, in Spain and Italy, brands are leveraging the cultural appeal of the Mediterranean diet. They position plant-based products as modern versions of traditional legume-based dishes, helping to dispel the perception that plant-based eating is primarily a Northern European or Anglo-Saxon trend. This approach is making plant-based diets more appealing and accessible across diverse cultural contexts.

EU Green Deal and Sustainability Regulations

The EU's Green Deal framework aims to reduce greenhouse gas emissions by 55% by 2030, using 1990 levels as a baseline. This initiative promotes plant-based foods through carbon pricing, agricultural subsidies, and stricter labeling requirements. In 2024, the European Commission proposed extending carbon border adjustment mechanisms to agricultural imports, which will increase the cost of non-EU soy and palm oil. This policy encourages regional ingredient sourcing and supports crops like oats, peas, and fava beans, which thrive in temperate climates. France's Agri-Food Climate Law, enacted in 2024, requires large retailers to dedicate at least 20% of shelf space to plant-based alternatives by 2027. This regulation is reshaping product assortments, pushing established companies to diversify their offerings or lose shelf space to specialized brands. The EU's Farm to Fork Strategy also aims to reduce pesticide use by 50% by 2030, posing challenges for conventional dairy and meat production, which rely heavily on feed crops, while organic plant-based producers face fewer compliance costs. In 2025, Germany's Federal Environment Agency reported that pea-based meat alternatives generate 75% fewer emissions than beef and 50% fewer than chicken. These findings are now influencing public procurement policies and corporate sustainability reporting, accelerating the shift toward plant-based foods.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Competition from established animal-based products | -1.1% | EU-wide, particularly strong in Italy, France, Poland, and rural regions with traditional dairy culture | Long term (≥ 4 years) |

| Supply chain disruptions and raw material price fluctuations | -1.3% | France, Germany, Poland, regions dependent on pea and oat imports | Short term (≤ 2 years) |

| Consumer skepticism and negative perception | -0.8% | Italy, Poland, France, rural and older demographic segments across Europe | Medium term (2-4 years) |

| Allergen issues with soy and tree nuts | -0.9% | EU-wide, particularly Germany, UK, France with strict labeling laws | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions and Raw Material Price Fluctuations

Raw material price volatility continues to challenge plant-based manufacturers, threatening both profit margins and production growth. Unlike established dairy and meat processors, plant-based producers often lack vertical integration and effective hedging mechanisms. In early 2025, oat prices surged by 15% due to poor harvests in Sweden and Finland, which together account for 35% of Europe’s food-grade oat supply. This highlights the sector’s susceptibility to climate-related supply disruptions. Similarly, almond prices remain high due to ongoing water scarcity in California, which produces 80% of the world’s almonds. This creates significant cost pressures for European manufacturers reliant on almond imports for their products. Smaller plant-based brands face additional challenges as they lack the purchasing power to negotiate long-term supply contracts with fixed prices, leaving them exposed to spot market price fluctuations and shrinking profit margins. To address these issues, the European Commission introduced a proposal in 2025 to subsidize domestic cultivation of peas and fava beans, aiming to reduce reliance on imports. However, achieving meaningful production levels to impact supply dynamics is expected to take 3-5 years. Until then, plant-based manufacturers must navigate these challenges while balancing costs and maintaining competitiveness in the market.

Allergen Issues with Soy and Tree Nuts

Allergen labeling requirements significantly hinder market expansion, as mandatory warnings for soy and tree nut ingredients discourage many consumers. In Europe, soy allergies affect around 0.4% of children, while tree nut allergies impact 1-2% of the population. Due to shared manufacturing equipment, approximately 40% of plant-based products include precautionary allergen labels like "may contain," which limits their appeal to allergy-sensitive households. The EU's Food Information to Consumers Regulation (EU) No 1169/2011 requires clear allergen disclosure. Proposed amendments for 2026 aim to introduce standardized, color-coded allergen labeling, making warnings more visible and potentially deterring cautious buyers further. A 2025 report by Germany's Federal Institute for Risk Assessment revealed that 12% of consumers avoid plant-based products over allergen concerns, even without diagnosed allergies, reflecting a growing risk-averse mindset. To address this, manufacturers are investing in allergen-free production lines and reformulating products with alternative proteins such as pea, rice, and potato. However, these efforts require significant capital and time, delaying product launches. Additionally, the lack of a unified EU framework for allergen risk assessment results in inconsistent precautionary labeling practices across countries, creating compliance challenges for brands operating in multiple markets. These factors collectively slow the growth of plant-based products in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Alternatives Anchor Leadership while Meat Substitutes Accelerate

In 2025, plant-based dairy accounted for 38.24% of the market value, emphasizing its role in introducing plant-based diets to mainstream consumers. Yogurt alternatives are gaining traction due to the increasing demand for probiotic-enriched products. For instance, Danone's Alpro launched a Greek-style coconut yogurt in 2025, containing 10 billion live cultures to cater to gut health-conscious consumers. Cheese alternatives remain a challenging segment, as replicating melt and stretch properties is complex. However, advancements in precision fermentation are enabling cow-free casein production, with several European startups conducting pilot-scale trials in 2025. Frozen desserts and ice creams are expanding rapidly, driven by innovations like hydrocolloid systems and coconut fat blends that replicate dairy-like textures. Unilever's Ben & Jerry's non-dairy range now represents 15% of the brand's European sales.

Plant-based bakery products are the fastest-growing category, with an 8.97% CAGR projected through 2031. This growth is driven by clean-label reformulations that remove eggs and dairy while maintaining taste and shelf life. Ingredient suppliers like Ingredion and Kerry Group introduced egg replacers made from aquafaba and pea protein in 2024-2025, which perform effectively in batter systems. Meat substitutes face challenges due to concerns over "ultra-processed" foods, prompting brands to simplify formulations and focus on whole-food ingredients. Meanwhile, plant-based beverages, including packaged milk, smoothies, coffee, and tea, are mature categories with slower growth in key markets like Germany and the UK. However, functional beverage innovations are creating new opportunities for growth.

By Ingredient: Soy Dominance Faces Allergen Pressure

In 2025, soy accounted for 45.05% of the ingredient market, driven by its complete amino acid profile, versatility, and established supply chains. However, its dominance is declining as manufacturers diversify to address allergen concerns and regional sourcing preferences. Europe relies heavily on soy imports from Brazil and the U.S., creating supply chain risks and exposing brands to deforestation-related reputational issues. The EU’s anti-deforestation regulation, effective in 2027, will require traceability documentation for all soy imports. Pea protein is gaining traction due to its hypoallergenic properties and local cultivation in Europe, with countries like France, Germany, and Poland increasing production. However, lower protein extraction yields compared to soy pose cost challenges. Oat-based products, known for their natural creaminess and heart-health benefits from beta-glucan, are primarily used in beverages.

Rice-based ingredients are growing at a 9.02% CAGR through 2031, the fastest among ingredient types, as they cater to consumers with multiple food sensitivities. Rice protein isolate is used in infant formulas and clinical nutrition, though its lower protein content requires higher inclusion rates, impacting costs. Almond and coconut ingredients are premium options due to their sensory appeal and clean-eating image, but high costs and import dependence limit growth. Almonds are mainly used in beverages, while coconuts are common in yogurt and ice cream. The ingredient market is evolving with advancements in precision fermentation and cellular agriculture. European startups are developing animal-identical proteins like casein and whey, which can blend with plant-based ingredients to enhance functionality without allergen risks.

By Form: Frozen Formats Capture Convenience Demand

In 2025, refrigerated and chilled products accounted for 34.45% of the market value, highlighting the strong demand for fresh milk alternatives and yogurt. These products are often seen as healthier and less processed compared to shelf-stable or frozen options. Western Europe’s advanced cold chain infrastructure supports the widespread availability of refrigerated plant-based products. Retailers are increasing chiller space to accommodate more product varieties, although rising energy costs due to carbon pricing mechanisms pose challenges. Shelf-stable products, such as UHT milk and ambient-stable meat alternatives, offer advantages like longer shelf life and simpler logistics, making them ideal for e-commerce and exports. However, in markets like Germany and the UK, consumers prefer fresh formats, limiting the growth of shelf-stable options.

Frozen plant-based products are projected to grow at a 9.55% CAGR through 2031, the fastest among all formats. Freezing helps preserve texture and flavor, offering convenient meal solutions. Products like frozen pizzas, ready meals, and appetizers are gaining popularity, with brands like Goodfella's and Dr. Oetker launching plant-based frozen pizzas in 2025 to cater to flexitarian households. The frozen format also allows the use of ingredients like jackfruit and mushrooms, which have short fresh shelf lives. Ready-to-eat and ready-to-cook products are growing as busy households seek quick meal options, with brands offering pre-marinated proteins and meal kits that compete with foodservice and delivery.

By Distribution Channel: On-Trade Rebounds Post-Pandemic

In 2025, off-trade channels accounted for 75.35% of the market value, highlighting the growing preference for at-home consumption. This trend, which gained momentum during the COVID-19 pandemic, continues due to remote work and cost-saving habits. Supermarkets and hypermarkets lead the off-trade segment, contributing approximately 60% of the volume. These outlets attract consumers with their wide product variety and cross-category shopping options, encouraging trials of plant-based products. Convenience stores are also expanding their ready-to-eat plant-based offerings to cater to on-the-go consumers. For instance, Żabka in Poland and Carrefour Express in France introduced plant-based sandwiches and salads in 2025. Online sales grew by 35% in 2025, driven by subscription models and direct-to-consumer brands offering personalized recommendations and auto-replenishment. However, e-commerce still represents only 12% of total plant-based food sales, as delivery costs and the preference for inspecting fresh products in-store remain barriers.

On-trade channels are growing rapidly, with a 10.31% CAGR projected through 2031, the highest among distribution types. Restaurants, cafes, and quick-service outlets are adding plant-based options to attract flexitarian customers and meet sustainability goals. In 2025, Starbucks expanded its plant-based menu across Europe, introducing items like a Beyond Meat breakfast sandwich and vegan pastries, which now make up 12% of its food sales in the region. Fast-casual chains such as Pret A Manger and Leon increased plant-based menu penetration to 40%, making these items mainstream rather than niche. On-trade channels also encourage home consumption, as positive dining experiences drive retail purchases. Additionally, foodservice operators are using plant-based proteins to manage food cost inflation, as these ingredients offer more stable pricing compared to animal proteins, which are affected by disease outbreaks and feed cost fluctuations.

Geography Analysis

Germany is projected to hold a 35.68% market share in 2025, driven by its strong vegan culture, advanced retail infrastructure, and supportive policies for sustainable food systems. Berlin, known as Europe’s vegan capital with over 60 fully plant-based restaurants, sets consumption trends nationwide and attracts global brands establishing European headquarters. In 2025, Aldi and Lidl expanded their private-label plant-based ranges by 40%, offering products at prices comparable to traditional dairy and meat. This strategy makes plant-based options more accessible, boosting demand beyond affluent urban areas. The German government’s 2024 school meal initiative, requiring plant-based options in public cafeterias, introduces 8 million children to non-dairy alternatives, fostering early adoption. Additionally, a 2025 report by Germany’s Federal Environment Agency revealed that pea-based meat alternatives produce 75% fewer emissions than beef, influencing public procurement and corporate sustainability practices. Germany’s expertise in food processing equipment also enables its companies to export plant-based production technologies across Europe, creating additional revenue streams.

Spain is expected to grow at a 9.35% CAGR through 2031, the fastest in Europe. This growth is fueled by Mediterranean diet-inspired plant-based products that combine traditional ingredients like chickpeas, lentils, and olive oil with modern formats. These familiar flavors help local brands compete with global players. Barcelona and Madrid are emerging as innovation hubs, with startups like Heura Foods achieving national distribution and expanding into France and Italy. Spain’s tourism sector, which welcomed 85 million visitors in 2024, is driving demand for plant-based options in hotels and restaurants catering to Northern European tourists. Meanwhile, regions like Andalusia and Castilla-La Mancha are increasing chickpea and lentil cultivation to support domestic processors and reduce imports.

The UK, France, Italy, Netherlands, Sweden, Poland, and Switzerland collectively account for the remaining market share, each with unique growth drivers. In the UK, Tesco and Sainsbury’s launched private-label plant-based ranges in 2024-2025, priced 20-30% lower than branded products. France’s 2024 Agri-Food Climate Law mandates 20% shelf space for plant-based products in large retailers by 2027, ensuring steady demand. Italy’s market is concentrated in Northern regions like Lombardy and Emilia-Romagna, where health consciousness is higher, but growth is limited by cultural preferences for traditional dairy products. The Netherlands leads in innovation, with companies like The Vegetarian Butcher and Mosa Meat advancing hybrid and cultivated meat technologies. Sweden’s updated 2025 dietary guidelines promote plant-based proteins, influencing public procurement and school meals. Poland’s market is growing rapidly, driven by urbanization and Western European food trends. Switzerland’s high-income consumers favor premium plant-based products, though the small market size relies on imports from Germany and France.

Competitive Landscape

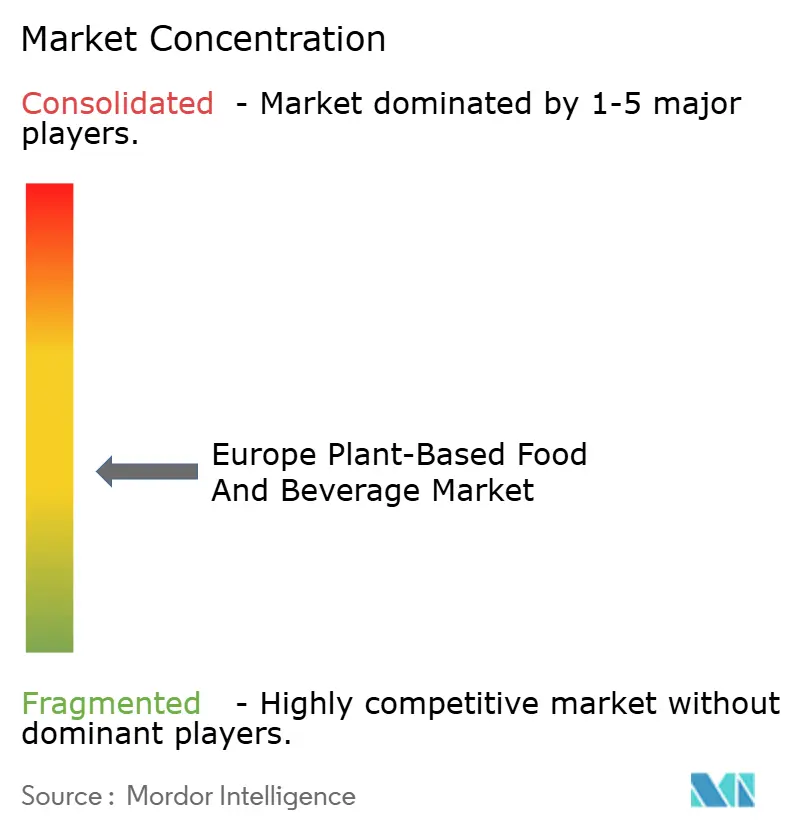

Europe's plant-based food and beverage market is a vibrant tapestry woven from established multinationals, strong regional brands, and a surge of niche startups. Industry giants such as Danone SA, Nestlé SA, Unilever plc, Oatly Group AB, and Conagra Brands Inc harness their expansive scale, extensive distribution networks, and state-of-the-art R&D. This prowess enables them to rapidly reformulate products, enhance nutritional profiles, and craft shelf-stable solutions. On the other hand, smaller players carve out their niche by championing unique ingredients, prioritizing local sourcing, and positioning their offerings as premium. While no single entity dominates the market, many shine in specific arenas, from dairy alternatives and meat substitutes to functional beverages.

Driving this demand are heightened health and wellness awareness, environmental and animal welfare concerns, and the surging popularity of flexitarian diets. These evolving preferences are expanding the consumer demographic, reaching well beyond the traditional vegan audience. Retailers are bolstering availability with private-label products and strategic placements in mainstream supermarkets. At the same time, foodservice and quick-service chains are rolling out plant-based options to resonate with the younger urban demographic. However, the journey isn't without hurdles: varying regulations across Europe, rising ingredient costs, and occasional supply shortages of specialty proteins and oils are all impacting pricing and profitability.

The market's fragmentation fuels innovation and niche targeting, yet it also sets the stage for potential consolidation. Major corporations eye regional innovators for acquisitions, aiming to fill portfolio gaps and accelerate market penetration. The roadmap for growth is evident: fine-tuning product taste and texture, enhancing affordability, and exploring the relatively uncharted Eastern and Southern European markets. This ever-evolving landscape not only fosters innovation but also lays the groundwork for strategic mergers, as companies vie for scale and dominance in their respective categories.

Europe Plant-Based Food and Beverage Industry Leaders

-

Danone SA

-

Nestlé SA

-

Unilever plc

-

Oatly Group AB

-

Conagra Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: French vegan cheese producer Jay&Joy launched its plant-based camembert alternative, 'Albert', in the United Kingdom market. The product, crafted from cashew nuts and French soy, aimed to cater to the growing demand for vegan cheese options.

- June 2025: Violife introduced what it claimed to be the United Kingdom’s first high-protein vegan cheddar. This launch aimed to cater to the growing demand for plant-based, protein-rich alternatives in the region.

- May 2025: Beyond Meat announced the launch of its vegan Beyond Steak pieces in the United Kingdom. The product, designed to mimic the taste and texture of traditional steak, became available exclusively at 650 Tesco stores across the country.

- March 2025: Silk has introduced a new plant-based beverage formula in Mexico, expanding its presence in the country’s growing market for dairy alternatives. According to the brand, the newly launched Silk formula includes six essential nutrients and offers an improved texture, alongside a neutral flavor that can be used in a variety of settings, from morning coffee to post-workout smoothies.

Europe Plant-Based Food and Beverage Market Report Scope

Foods and beverages "plant-based" contain only plant-based ingredients, such as fruits, vegetables, whole grains, legumes, nuts & seeds, herbs, and spices. These products don't include any animal-based products in them. The market studied is segmented based on product type, distribution channel, and country. Based on product type, the market " is segmented into meat substitutes, dairy-alternative beverages, non-dairy ice cream, non-dairy cheese, non-dairy yogurt, and non-dairy spreads. Dairy-alternative beverages are further segmented into soy and other drinks. almonddrinksSimilarly, meat substitutes are further segmented as textured vegetable protein, tofu, tempeh, and others. By distribution channel, the market studied is segmented into supermarkets/hypermarkets, convenience stores, online

media, and other distribution channels. The report also analyzes the Europe plant-based food and beverages market in emerging and established countries such as the United Kingdom, Germany, France, Italy, Spain, and the rest of Europe. The report offers market size and forecasts for the market in value (USD million) for all the above segments.

By Product Type

| Plant-based Dairy | Yogurt |

| Cheese | |

| Frozen Desserts and Ice-Cream | |

| Other Plant-based Dairy | |

| Meat Substitutes | Tofu |

| Tempeh | |

| Textured Vegetable Protein | |

| Other Meat Substitutes | |

| Plant-based Nutrition/Snack Bars | |

| Plant-based Bakery Products | |

| Plant-based Beverages | Packaged Milk |

| Packaged Smoothies | |

| Coffee | |

| Tea | |

| Other Plant-based Beverages | |

| Other Food and Beverages |

By Ingredient

| Soy |

| Almond |

| Pea |

| Oat |

| Rice |

| Coconut |

| Other Sources |

By Form

| Refrigerated/Chilled |

| Frozen |

| Shelf-stable/Ambient |

| Ready-to-Eat/Ready-to-Cook |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Off-Trade Channels |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Switzerland |

| Rest of Europe |

| By Product Type | Plant-based Dairy | Yogurt |

| Cheese | ||

| Frozen Desserts and Ice-Cream | ||

| Other Plant-based Dairy | ||

| Meat Substitutes | Tofu | |

| Tempeh | ||

| Textured Vegetable Protein | ||

| Other Meat Substitutes | ||

| Plant-based Nutrition/Snack Bars | ||

| Plant-based Bakery Products | ||

| Plant-based Beverages | Packaged Milk | |

| Packaged Smoothies | ||

| Coffee | ||

| Tea | ||

| Other Plant-based Beverages | ||

| Other Food and Beverages | ||

| By Ingredient | Soy | |

| Almond | ||

| Pea | ||

| Oat | ||

| Rice | ||

| Coconut | ||

| Other Sources | ||

| By Form | Refrigerated/Chilled | |

| Frozen | ||

| Shelf-stable/Ambient | ||

| Ready-to-Eat/Ready-to-Cook | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Off-Trade Channels | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Switzerland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How fast is the Europe plant-based food and beverage market expected to grow to 2031?

It is forecast to advance from USD 6.64 billion in 2026 to USD 10.12 billion by 2031 at an 8.79% CAGR.

Which product category currently leads sales value?

Plant-based dairy held 38.24% share in 2025, making it the region’s largest category.

Which European country will post the fastest growth?

Spain is projected to expand at a 9.35% CAGR through 2031 owing to Mediterranean-style legume and olive-oil-based innovations.

Which sales channel is gaining momentum after the pandemic?

On-trade foodservice, including restaurants and cafés, is rebounding at a 10.31% CAGR as menus add plant-based options.

Page last updated on: