Radiation Detection, Monitoring, And Safety Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.85 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radiation Detection, Monitoring, And Safety Market Analysis by Mordor Intelligence

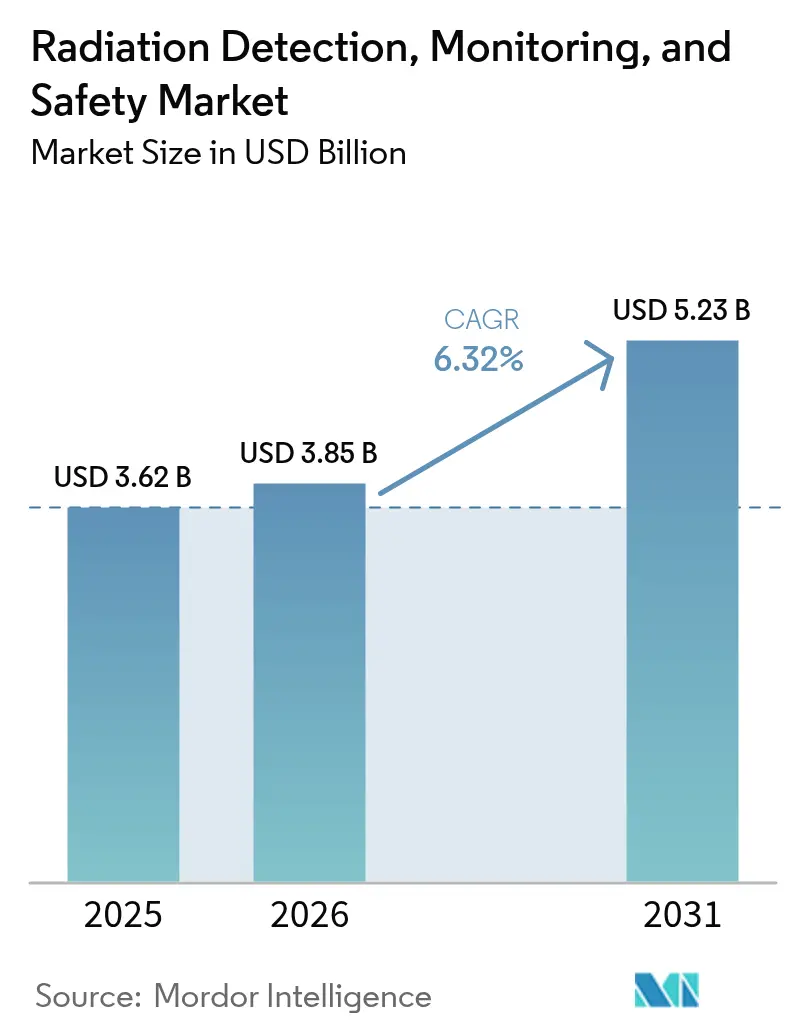

The radiation detection, monitoring, and safety market size in 2026 is estimated at USD 3.85 billion, growing from 2025 value of USD 3.62 billion with 2031 projections showing USD 5.23 billion, growing at 6.32% CAGR over 2026-2031. The expansion of nuclear-medicine procedures, regulatory mandates for continuous environmental surveillance, and rapid advancements in semiconductor-based detector performance underpin this trajectory. Heightened security concerns reinforce demand across border control, first-responder, and critical infrastructure segments, while aging reactor fleets drive the need for decommissioning-linked monitoring deployments. The radiation detection, monitoring, and safety market benefits from a dual-use value proposition that aligns civilian healthcare investments with national-security spending, creating a resilient revenue base. North American utilities, European nuclear-phase-out programs, and Asia-Pacific build-outs collectively accelerate replacement cycles for legacy detection platforms. Digital connectivity, predictive analytics, and cloud-native architectures now distinguish premium offerings, supporting aftermarket software revenues and recurring service contracts.

Key Report Takeaways

- By product type, detection and monitoring solutions held 50.74% of the radiation detection, monitoring, and safety market share in 2025, while safety equipment is poised to grow at a 7.55% CAGR through 2031.

- By detector technology, scintillation systems commanded 41.05% share of the radiation detection, monitoring, and safety market size in 2025, whereas semiconductor detectors are projected to expand at an 7.88% CAGR between 2026 and 2031.

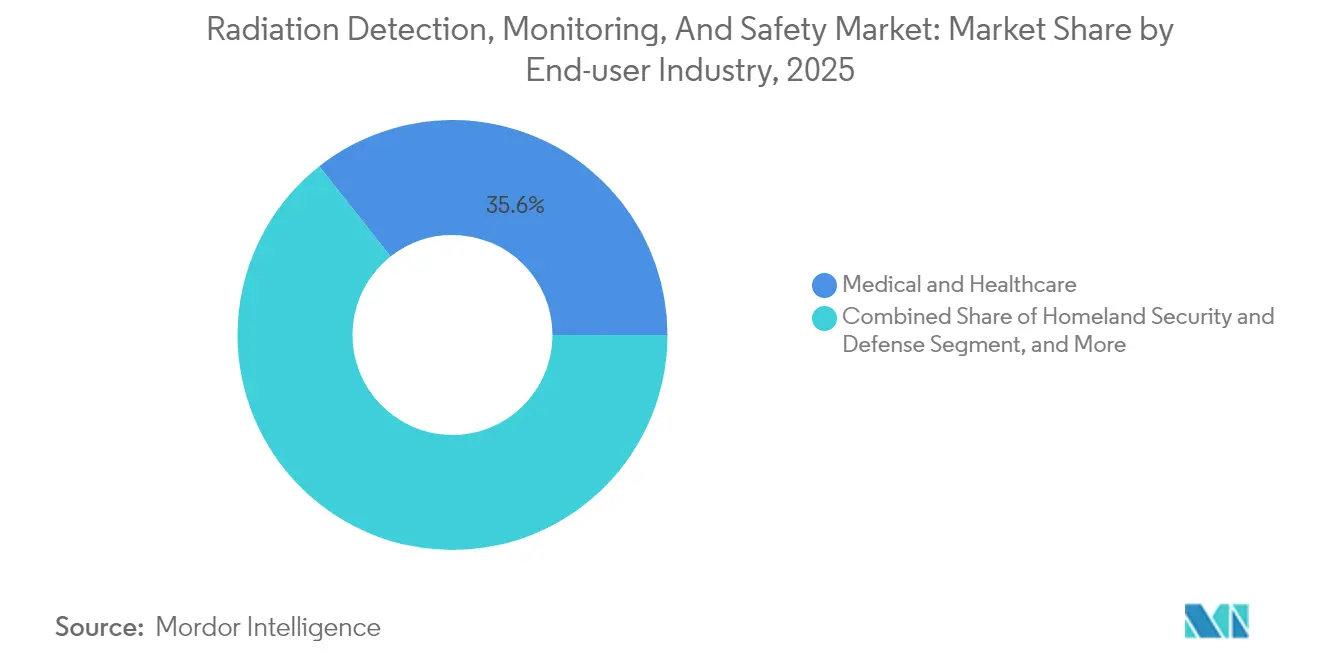

- By end-user industry, the medical and healthcare sector accounted for a 35.64% share of the radiation detection, monitoring, and safety market size in 2025; homeland security and defense are projected to advance at a 7.18% CAGR through 2031.

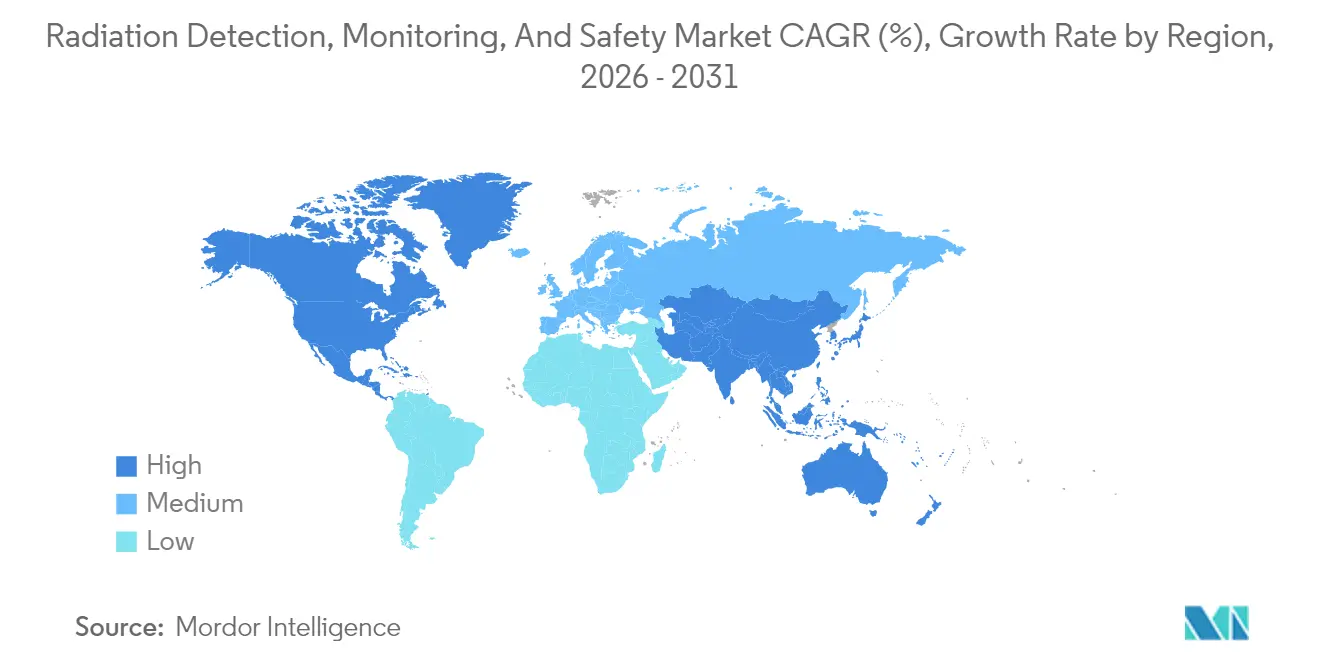

- By geography, North America led the radiation detection, monitoring, and safety market with a 30.05% market share in 2025, while the Asia-Pacific region is forecast to post an 8.05% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radiation Detection, Monitoring, And Safety Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising incidence of cancer and chronic diseases | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Expanding nuclear medicine and radiotherapy procedures | +1.5% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Regulatory push for real-time environmental monitoring | +0.9% | Global, led by Europe and North America | Short term (≤ 2 years) |

| Miniaturization and IoT-enabled dosimeters | +0.8% | Global, early adoption in developed markets | Medium term (2-4 years) |

| UAV-based wide-area radiation mapping | +0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| De-commissioning of aging nuclear reactors worldwide | +0.7% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Cancer and Chronic Diseases

Cancer prevalence is climbing toward 35 million global cases by 2050, enlarging the addressable base for precision dosimetry systems.[1]Source: World Health Organization, “Global Cancer Statistics 2024,” WHO, who.int Radiotherapy departments now specify sub-millisecond beam-monitoring accuracy, favoring semiconductor detectors that capture high-frequency fluctuations in dose rate. Adaptive treatment planning platforms amplify data-generation volumes, and clinicians increasingly rely on real-time feedback loops to tune fractionated doses. Health systems, therefore, budget for multi-channel dose-verification racks, redundant field calibrators, and cloud-hosted dose-registry software, an ecosystem that broadens the radiation detection, monitoring, and safety market. Vendor strategies focus on modular detector heads and AI-assisted QA dashboards that enhance linear-accelerator uptime.

Expanding Nuclear Medicine and Radiotherapy Procedures

Nuclear medicine examinations grew 12% year-over-year in 2024, propelled by theranostic isotopes such as actinium-225 and lutetium-177.[2]Source: Journal of Nuclear Medicine Editorial Board, “Theranostic Applications in Nuclear Medicine: 2024 Review,” Journal of Nuclear Medicine, snmjournals.org Radiopharmaceutical hubs require air-borne alpha-particle monitors, hot-cell gamma spectrometers, and personal dosimeters that auto-synchronize with facility LIMS databases. Decentralized cyclotron networks, positioned closer to patient populations, multiply procurement nodes for shielding cabinets, de-contamination portals, and leak-testing kits. Standardization under U.S. FDA 21 CFR Part 361 obliges isotope-specific calibration protocols, ensuring recurring outsourcing opportunities for detector-recalibration service providers. These trends elevate ASPs (average selling prices) and extend aftermarket revenue visibility.

Regulatory Push for Real-Time Environmental Monitoring

The European Euratom 2013/59 directive mandates continuous environmental surveillance at reactor perimeters; comparable rules emanate from the U.S. NRC’s Part 20 revisions.[3]Source: U.S. Nuclear Regulatory Commission, “Radiation Protection Standards,” NRC, nrc.gov Utilities now deploy mesh-networked spectroscopic portals that transmit one-minute dose-rate averages to cloud dashboards. Automated threshold alarms integrate with emergency-response playbooks, shortening alert-to-action intervals. Detector OEMs differentiate themselves through weatherized enclosures certified for temperatures ranging from −40 °C to +60 °C and battery-backup runtimes exceeding seven days. Compliance spending cascades to municipal and academic labs that mirror reactor monitoring standards, broadening addressable end-markets.

Miniaturization and IoT-Enabled Dosimeters

Wearable badges, scarcely thicker than a credit card, transmit dose logs via Bluetooth Low Energy to secured hospital servers. Automated record-keeping alleviates staff shortages among radiation-safety officers, particularly in Asia-Pacific oncology clinics. Integration with workforce-management apps supports geofencing, prompting alerts when personnel enter restricted zones without active dosimeters. The feature set converts compliance policing into a preventive-safety culture, expanding replacement cycles for consumable TLD pellets toward connected dosimetry subscriptions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent multi-jurisdictional compliance burden | -0.8% | Global, most complex in Europe and North America | Short term (≤ 2 years) |

| Shortage of certified radiation safety officers | -0.6% | Global, acute in Asia-Pacific and developing markets | Medium term (2-4 years) |

| High capex for spectroscopic-grade detectors | -0.5% | Global, constraining smaller end-users | Medium term (2-4 years) |

| Supply-chain volatility for He-3 and scintillator crystals | -0.7% | Global, affecting neutron-detection applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdictional Compliance Burden

Detector OEMs must clear FDA 510(k) dossiers, satisfy IEC 60601-2-45 performance metrics, and attain CE marking conformity, each requiring discrete biocompatibility, EMC, and radiation pattern tests.[4]Source: U.S. Food and Drug Administration, “Medical Device 510(k) Clearances Database,” FDA, fda.gov Documentation alone inflates research and development budgets, steering smaller innovators toward licensing deals or niche academic markets. Parallel certification tracks hinder agile firmware updates once fielded devices enter multi-country footprints, slowing feature rollouts. The result is elongated design-win cycles that can exceed four years, diluting NPV on new technology investments and tempering near-term revenue acceleration within the radiation detection, monitoring, and safety market.

Shortage of Certified Radiation Safety Officers

Licensing frameworks, such as 10 CFR Part 35, stipulate minimum educational hours and supervised clinical practice for radiation safety officers; however, training pipelines remain undersized.[5]Source: Health Physics Society, “Radiation Safety Officer Workforce Analysis 2024,” Health Physics Society, hps.org Asia-Pacific oncology networks, growing at a double-digit rate, thus face staffing deficits that delay facility commissioning. Hospitals compensate by outsourcing compliance functions to equipment vendors, but liability clauses limit the scope of such engagements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Detection Drives Growth

Detection and monitoring systems generated 50.74% of 2025 revenue, anchoring procurement budgets for hospitals, utilities, and defense agencies that must continuously validate dose conditions. Within the radiation detection, monitoring, and safety market size, detection platforms are projected to grow alongside predictive analytics modules that recommend proactive maintenance intervals. Safety equipment, encompassing lead-lined apparel, decontamination booths, and automated containment doors, is outpacing historical norms with a 7.55% CAGR, buoyed by harmonized ISO 2919 protective device standards. Integrated offerings that unite real-time g-ray probes with motorized shielding curtains shorten alarm-to-containment times and improve ALARA (as low as reasonably achievable) compliance. Vendors leverage cross-selling synergies: hospitals ordering scintillation probes often append badge-dosimetry subscriptions, while reactor operators bundle perimeter portals with shelter-in-place ventilation systems. Price elasticity remains modest, as regulatory obligations heighten procurement urgency, ensuring premium SKUs maintain a steady pull-through across the radiation detection, monitoring, and safety industry.

The expanded functionality of cloud dashboards, geo-tagged alarm visualization, role-based access, and automated compliance report generation pushes detection gear beyond commodity status. SaaS overlays carry significant gross margin, outstripping hardware rates and encouraging hardware-agnostic ecosystems. Consequently, channel partners favor stocking multi-protocol gateways that integrate NaI(Tl), CZT, and neutron modules under one supervisory HMI. Real-time analytics further reduces false-positive occurrences, trimming costly evacuation incidents. Such value-added solutions reinforce the leadership of detection solutions within the broader radiation detection, monitoring, and safety market.

By Detector Technology: Semiconductors Surge

Scintillation detectors retained 41.05% revenue share in 2025, owing to their mature supply chain and favorable cost-performance profile across medical imaging and environmental monitoring. Nonetheless, semiconductor architectures are forecast to post an 7.88% CAGR, nearly 1.5 times the overall growth rate of the radiation detection, monitoring, and safety market. CZT modules offer room-temperature energy resolution of below 2%, enabling isotope discrimination crucial for homeland-security applications. Chip-scale fabrication techniques adapted from consumer CMOS foundries promise volume economies that can parry the high capex hurdle currently restraining adoption. Meanwhile, gas-filled detectors defend niches where ruggedness outranks resolution, such as oil-well logging tools operating at 200 °C down-hole. Personal dosimeters are transitioning from passive TLD cards to Bluetooth-enabled SiPM micro-counters that sync with cloud-based dose registries, reflecting the broader digitization trend within the radiation detection, monitoring, and safety market.

Cross-sector research and development spillovers accelerate semiconductor progress. Automotive LiDAR suppliers commercialize SiPM wafer stacks, whose multi-pixel arrays excel at capturing weak scintillation signatures, thereby reducing dark noise and yielding faster recovery times. Parallel advances in perovskite-based thin films suggest the potential for flexible, large-area panels suitable for drone wings and building façades. Standard bodies such as ISO 21909 have expanded performance classes to account for these novel materials, offering procurement officers clearly defined acceptance tests. Collectively, these breakthroughs cement the semiconductor segment as the innovation engine of the radiation detection, monitoring, and safety industry.

By End-User Industry: Medical Leadership

Medical facilities controlled 35.64% of 2025 spending, undergirded by rising radiotherapy caseloads and a steady pipeline of FDA-cleared radiopharmaceuticals. Automated hot-cell monitors document isotope purity levels down to parts per billion, safeguarding patient dosing accuracy. Linked patient-dose records feed into oncology big-data repositories, facilitating outcomes-benchmarking studies that, in turn, spur incremental equipment upgrades. Homeland security and defense agencies, which are expanding at a 7.18% CAGR, are procuring lightweight backpack spectrometers and UAV-borne sensors that can scan cargo yards without disrupting logistics flows. Utility-scale power companies and industrial NDT firms, although slower-growing, deliver steady replacement-cycle demand for perimeter monitors and fixed-area probes inside turbine halls, thereby supporting baseline growth for the radiation detection, monitoring, and safety market.

Academic and research institutes form a high-ASP niche because they commission bespoke spectrometers with ultra-high resolution and niche isotope calibration. Grant-funded procurement often stipulates the use of open-source firmware for data reproducibility, prompting vendors to decouple IP-sensitive processing logic into secure FPGA modules while exposing SDK hooks. Across user segments, the common thread is an intensifying preference for software-defined detection platforms, a shift that enables cross-vertical product extensions and maximizes recurring revenue streams.

Geography Analysis

North America retained a 30.05% revenue lead in 2025, reflecting entrenched nuclear-power fleets, extensive homeland-security infrastructures, and early-adopter healthcare systems. U.S. national laboratories are funneling research and development grants into CZT detector miniaturization, while the Canadian NRCan framework is subsidizing environmental-monitoring upgrades at research reactors. Mexico’s expanding radiopharmaceutical exports add incremental volume for isotope-production hot-cell monitors. Cross-border standardization under ANSI N42 enhances equipment interoperability, thereby reinforcing economies of scale within the regional radiation detection, monitoring, and safety market.

Asia-Pacific records the fastest trajectory at an 8.05% CAGR, underwritten by China’s plan to commission 150 reactors before 2060. The localization mandate embedded in Beijing’s Made-in-China 2025 policy promotes joint-venture fabrication plants for CZT wafers, reducing import tariffs and mitigating supply-chain fragility. Japan’s post-Fukushima regulatory regime finances perimeter gamma-ray meshes extending 20 km around reactor sites, while India’s Department of Atomic Energy funds low-cost survey meters for cancer-therapy wards in tier-two cities. South Korea’s expanding 18-MeV cyclotron network further widens the addressable hospital count, reinforcing the Asia-Pacific region’s status as the global growth engine for the radiation detection, monitoring, and safety market.

Europe exhibits balanced growth as decommissioning projects in Germany, Belgium, and Spain create specialized demand for alpha-in-air monitors and waste-drum assay systems. France, maintaining a strong nuclear-electricity share, focuses on life-extension upgrades that must meet ASN’s stringent seismic-risk criteria. The Euratom treaty standardizes procurement specifications, enabling cross-border volume contracts that leverage multi-year budget cycles. Central and Eastern European nations, modernizing Soviet-era research reactors, seek turnkey detection suites bundled with training services.

The Middle East and Africa, although nascent, are deploying neutron-cargo scanners at strategic ports and commissioning cyclotron-based radiopharmacy labs, foreshadowing medium-term momentum for the radiation detection, monitoring, and safety market in emerging geographies.

Regulatory Landscape

Regulatory requirements in the radiation detection, monitoring, and safety market reflect nuclear, medical, and security regimes. Compliance commonly spans U.S. NRC rules (10 CFR Part 20 for radiation protection standards and dose controls), medical-device pathways (FDA 510(k) for certain healthcare-use detectors and monitoring systems), and internationally referenced frameworks such as IAEA Safety Standards and Euratom 2013/59 for radiation protection and environmental surveillance obligations. These overlapping regimes create recurring needs for calibrated instruments, validated software reporting, and documented QA processes across medical and healthcare, energy and power, and homeland security and defense end users.

A notable 2026 regulatory inflection in the United States is the NRC proposed rulemaking around 10 CFR Part 20, which introduces a risk-informed, graded approach to dose management and includes changes referenced in the proposal documentation around dose limit constructs (including effluent dose limits). At the same time, other jurisdictions keep radiation protection rulebooks and guidance under review, including the Canadian Nuclear Safety Commission (CNSC) regulatory document framework and Australia's Radiation Protection and Nuclear Safety Regulations 2018 (compiled version in force). For vendors, these shifts strengthen multi-jurisdictional certification strategies (CE, IEC-aligned testing where applicable, and country-specific licensing rules such as 10 CFR Part 35-linked staffing and oversight requirements). They also increase the premium on software-enabled audit trails and remote monitoring to support continuous surveillance mandates.

Value Chain Analysis

The value chain runs from specialized upstream materials and components (scintillator crystals and assemblies, He-3 constrained neutron detection inputs, and semiconductor detector materials such as CZT, alongside photodetectors and readout ASICs) to midstream instrument manufacturing (handheld survey meters, spectrometers, portal monitors, fixed-area monitors, and electronic dosimeters). Downstream integration, calibration, and lifecycle services sit close to end users, since many procurement decisions combine hardware with ongoing compliance support. Standards and documentary guidance from bodies such as NIST (Radiation Detection Documentary Standards Program), CIRMS, and IEEE TC-45 influence design targets and acceptance testing, while U.S. DHS technical capability standards shape performance expectations for radiological detection in security applications.

System integrators and OEM service networks are key downstream nodes because many end users buy complete solutions, including sensors plus communications gateways, cloud dashboards, alarm management, and maintenance contracts. Recent activity reflects this structure, including Mirion contracts tied to the TerraPower Natrium reactor demonstration for radiation monitoring and nuclear instrumentation systems, and port-security deployments such as Dubai Customs unveiling an AI-enabled integrated radiation protection and monitoring system for air, land, and sea ports. Consolidation also appears in adjacent workflow tools, illustrated by Radnostix acquiring Lucerno Dynamics assets (including LARA System technology and ELLEXA Explorer software) to broaden radiopharmaceutical-related device capabilities and intensify data integration across detectors, facility systems, and compliance documentation.

Competitive Landscape

The competitive field remains moderately concentrated. Mirion Technologies leverages vertical integration that spans crystal growth, software analytics, and field-service networks, enabling one-stop turnkey bids. Thermo Fisher Scientific differentiates through reagent-grade radiopharmaceutical QC analyzers that feed instrument utilization data back to cloud dashboards, driving consumables pull-through. Teledyne-FLIR focuses on defense-grade handheld spectrometers hardened to MIL-STD disaster-response specs, securing multiyear DHS contracts.

Specialist challengers pursue niche wedges: Kromek commercializes CZT detector ASICs optimized for UAV payloads, while Fuji Electric offers healthcare dosimeters with NFC dose-log aggregation suited to high-throughput radiology departments. Crystal-fabrication bottlenecks encourage supply-side alliances Mirion’s recent acquisition of Advanced Measurement Technology illustrates a strategy to hedge raw-material risk while enlarging product breadth.

Pricing power hinges on software ecosystems that lock-in recurring analytics revenue; therefore, open-API strategies are limited. Multi-jurisdictional regulatory fluency acts as a competitive moat, as companies capable of navigating FDA, CE, and PMDA requirements accelerate global roll-outs. Finally, after-sales service footprints spare-part depots, field-engineer density, and 24/7 remote-monitoring centers play a decisive role in high-uptime verticals such as nuclear-power generation, shaping purchasing decisions and reinforcing brand loyalty within the radiation detection, monitoring and safety market.

Radiation Detection, Monitoring, And Safety Industry Leaders

Kromek Group plc

Teledyne FLIR LLC

Fuji Electric Co., Ltd.

Mirion Technologies Inc.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Environmental surveillance modernization remains a clear whitespace for networked monitoring hardware and software, supported by active public programs. For example, Taiwan's Nuclear Safety Commission initiated its Environmental Radiation Monitoring Plan 2026 (covering January 1, 2026 to December 31, 2026), spanning monitoring near nuclear facilities, fallout detection, and food and water checks. This plan fits the broader move toward always-on sensing, automated reporting, and multi-matrix sampling workflows, which creates room for vendors that package fixed and mobile detectors with calibration services, tamper-resistant data logging, and dashboards that simplify regulator-facing reporting.

Homeland security and defense procurement also anchor opportunity for ruggedized, interoperable instruments and integrated platforms. In the U.S., cargo scanning mandates under 6 U.S. Code 921 and DHS capability frameworks are pushing upgrades from legacy systems toward next-generation nonintrusive imaging and radiation detection. The DoD JPEO-CBRND Radiological Detection System program targets replacement of legacy radiological survey meters across multiple U.S. services under an IDIQ-style approach. On the technology side, published roadmaps and technical programs, including the IEEE NSS MIC RTSD 2026 emphasis on room-temperature compound semiconductor detectors and European radiation protection metrology roadmaps supporting Euratom 2013/59 compliance, point to near-term product focus on semiconductor-based detectors, lower false-alarm analytics, and tighter integration of detection data into operational command-and-control and clinical quality systems.

Recent Industry Developments

- June 2026: Teledyne FLIR Defense announced an USD 11.2 million U.S. Army contract (CPE CBRND) to deliver more than 45 CBRN sensor drone kits integrated with the R80D SkyRaider UAS. The award advances radiological detection closer to the point of need by combining unmanned systems with fielded sensing kits. It also reinforces defense-driven demand for lightweight, deployable detection architectures that can be scaled across units.

- April 2025: Teledyne FLIR Defense received a four-year, USD 74.2 million U.S. Army contract for development of Capability Set 2.2 under the Nuclear, Biological and Chemical Reconnaissance Vehicle (NBCRV) Sensor Suite Upgrade Program. The program work strengthens the company's role in integrated CBRN sensing and software for reconnaissance platforms. Such vehicle-centric upgrades influence procurement specifications for detectors, onboard analytics, and interoperable data links used across military CBRN workflows.

- September 2024: Mirion Technologies completed its USD 45 million acquisition of Advanced Measurement Technology, expanding its continuous air monitoring portfolio and extending reach in Asia-Pacific. The deal broadens Mirion's offering across environmental and facility monitoring use cases where continuous surveillance is mandatory. A wider installed base and expanded product breadth also supports pull-through of calibration, service, and software contracts tied to compliance reporting.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from equipment and supporting solutions that detect, measure, monitor, and protect people and sites from ionizing radiation in medical, industrial, energy, research, and security settings.

Scope exclusions: This sizing does not count radiation therapy systems and imaging modality sales (for example CT or nuclear medicine scanners) except where stand-alone radiation monitoring, dosimetry, or safety products are purchased.

Segmentation Overview

- By Product Type

- Detection and Monitoring

- Safety

- By Detector Technology

- Gas-Filled (Geiger-Müller, Proportional, Ion-Chambers)

- Scintillation (NaI(Tl), CsI, LaBr₃, Plastic)

- Semiconductor (HPGe, CZT, SiPM)

- Personal Dosimeters (TLD, OSL, Electronic)

- By End-user Industry

- Medical and Healthcare

- Energy and Power (Nuclear, Conventional)

- Homeland Security and Defence

- Industrial (Oil and Gas, Mining, Manufacturing)

- Research and Academic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where radiation exposure is regulated, and where monitoring spend typically shows up, then aligning that with how products are actually deployed. Public sources such as the IAEA, the US NRC, the US FDA, the EPA, and Eurostat were used to understand safety rules, nuclear activity signals, and healthcare procedure context. Those inputs were used to shape realistic demand indicators.

We also reviewed company annual reports and investor presentations to understand revenue mix patterns, product positioning, and regional emphasis, which supports guardrails for ASP and adoption assumptions. For patent and technology direction checks, we referenced a paid patent database. For cross-checking trade movement of relevant instrument categories, we used an import and export shipment-level database where it was applicable. The desk sources listed here are illustrative only, and many other public documents and datasets were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with manufacturers, distributors, service partners, and end-user procurement and safety teams across healthcare, nuclear and energy, industrial users, and security agencies. We used these discussions to confirm what gets bought as a system versus a component, how replacement cycles behave in practice, and where service and calibration revenues are counted. Assumptions were then adjusted until they reflected on-the-ground buying patterns across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 37% |

| Mid tier: 57% | Functional/Unit leaders: 42% | EMEA: 37% |

| Smaller Players: 17% | Managers: 45% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic together, with the main model anchored in demand pools that can be tracked each year. In practice, procedure and installed-base signals in medical and research settings, nuclear power and fuel-cycle activity, and security screening intensity were used to reconstruct a spend envelope, which was then split into product and technology buckets using adoption shares validated in interviews.

To keep the numbers realistic, we used selective bottom-up approximations, such as sampled unit volumes for personal dosimeters and area monitors multiplied by practical ASP bands, then checked those against supplier revenue exposure and channel feedback before totals were finalized. Key inputs used in the model include installed base and replacement cycles for detectors and dosimeters, calibration and service attach rates, regulatory monitoring frequency for workplaces and sites, public nuclear capacity and outage and maintenance patterns, and procurement timing effects in security and defense purchases. For the forecast, scenario analysis was used to reflect different procurement cycles and policy intensity, and then the yearly path was smoothed using expert consensus on adoption and pricing progression. Where direct volume signals were thin in a country or end-user group, gaps were handled through proxy indicators (for example similar regulatory regimes and comparable installed-base density), followed by rechecks with local interviews.

Data Validation & Update Cycle

Validation is done by comparing model outputs against independent signals that should move in the same direction, such as nuclear generation activity, healthcare procedure trends, and reported safety compliance activity where available. When a segment outcome looks off, we revisit the input drivers, re-check currency timing and price bands, and then re-contact a few respondents to confirm whether the change is real or a modeling artifact.

Before sign-off, the work goes through multi-step analyst review, including variance checks across regions and cross-links between product demand and end-user activity. The report is refreshed annually, and interim updates are made when material events occur, such as major policy changes, supply disruptions, or notable procurement shifts. Right before delivery, a final pass is completed so clients receive the most current view aligned with the latest available information.

Mordor Intelligence's Radiation Detection Monitoring and Safety Market Market Size Measured Against Other Published Estimates

Published market sizes for this space often do not match because the category boundary is not handled the same way across studies, and because pricing and service revenues get treated differently. Differences also come from base year selection, currency conversion timing, and whether security and defense purchases are modeled as smooth demand or as lumpy procurement.

In this study, the key gap drivers were checked around what counts as safety gear versus general industrial PPE, whether calibration and after-sales services are included, and how mixed-use detectors are assigned when they are sold into both medical and non-medical settings. We also saw that some approaches assume faster ASP erosion for detectors, while others assume steady pricing tied to compliance requirements, which can materially change the 2025 to 2026 step-up.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.62 B (2025) | |

| Industry Publisher A | USD 3.68 B (2025) | This estimate appears to use a slightly broader product list around monitoring platforms and related solutions, and it can also apply a different exchange-rate timing for the base year, which shifts the USD total. |

| Research Outlet B | USD 1.74 B (2025) | This estimate is consistent with a narrower counted revenue pool, where parts of medical and industrial monitoring spend and service and calibration revenues may be excluded or only partially captured. |

The table shows a wide spread, and under Mordor Intelligence's scope the value is tied to stand-alone radiation detection and monitoring equipment plus associated safety products and related services as they are purchased by end users, which avoids mixing in adjacent imaging or therapy system revenues. After the scope is locked, the totals remain traceable to practical drivers like installed base, replacement cycles, and service attach rates, so the result is repeatable when assumptions are updated.

Key Questions Answered in the Report

How large is the global radiation detection, monitoring, and safety market in 2026?

It stands at USD 3.85 billion and is forecast to reach USD 5.23 billion by 2031, representing a 6.32% CAGR forecast.

Which product category generates the bulk of current revenue?

Detection and monitoring solutions account for 50.74% of 2025 revenue, reflecting their central role in healthcare, industrial, and security settings.

Which detector technology is growing the fastest through 2031?

Semiconductor-based detectors, such as cadmium zinc telluride and silicon photomultipliers, are projected to post an 7.88% CAGR, driven by improvements in energy resolution and miniaturization.

Why is Asia-Pacific viewed as the growth epicenter?

China’s aggressive nuclear-reactor build-out, Japan’s post-Fukushima monitoring upgrades, and India’s radiopharmaceutical manufacturing expansion drive an anticipated 8.05% regional CAGR.

What supply-chain challenge most affects neutron detection instruments?

Intermittent availability and rising prices of helium-3 gas continue to pressure OEMs toward boron-lined or lithium-enriched alternatives.

Page last updated on: