Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

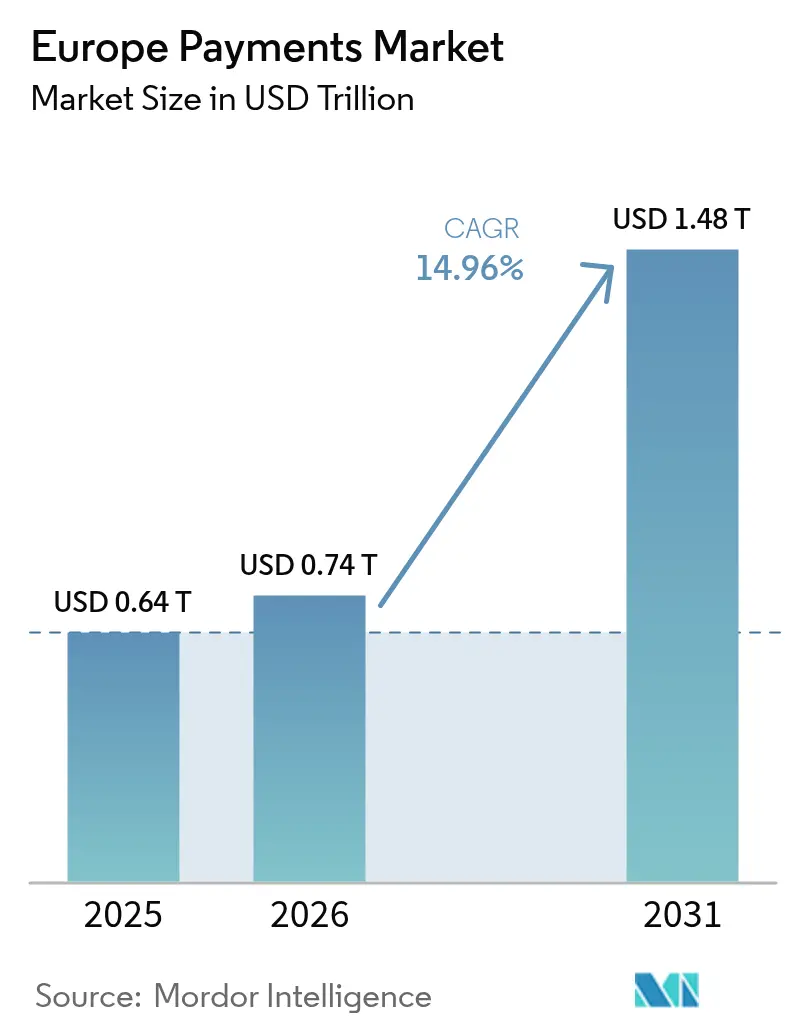

| Base Year Market Size (2025) | USD 0.64 Trillion |

| Market Size (2026) | USD 0.74 Trillion |

| Market Size (2031) | USD 1.48 Trillion |

| Growth Rate (2026 - 2031) | 14.96% CAGR |

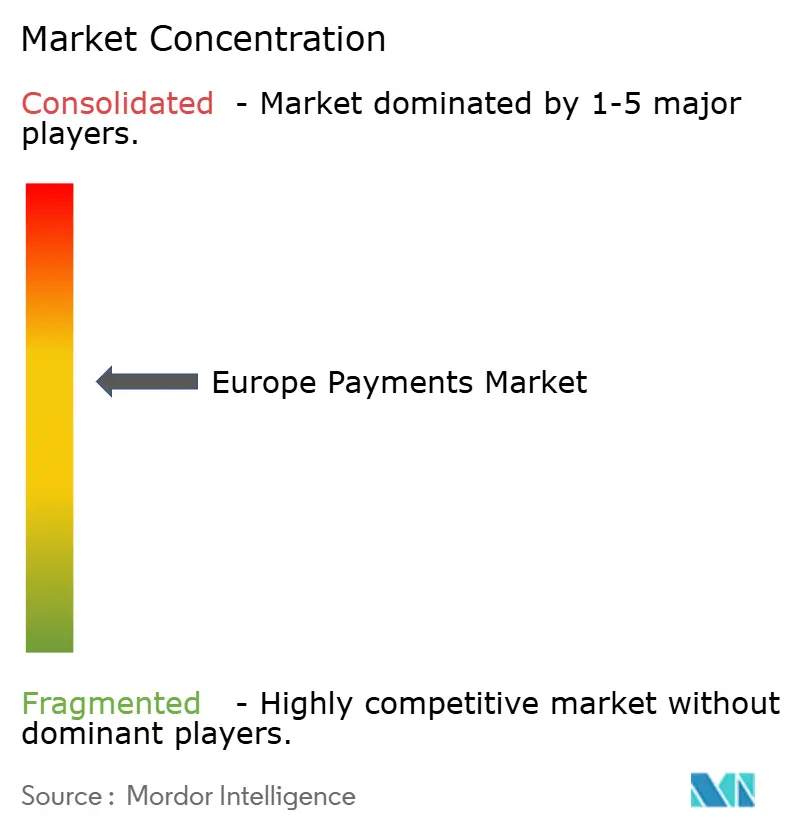

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Payments Market Analysis by Mordor Intelligence

The Europe payments market size was valued at USD 0.64 trillion in 2025 and estimated to grow from USD 0.74 trillion in 2026 to reach USD 1.48 trillion by 2031, at a CAGR of 14.96% during the forecast period (2026-2031). Expansion is anchored in the accelerating migration from cash to digital instruments, a trend underscored by the European Central Bank’s finding that cash accounted for 52% of point-of-sale transactions in 2024, down from 59% two years earlier.[1]Financial Express, “Zero MDR Policy Causing Annual Revenue Loss,” financialexpress.com Mandatory real-time payment availability under the Instant Payments Regulation, effective January 2025, is set to widen access to ten-second euro transfers at no extra cost. Surging mobile-wallet adoption—72% of Europeans used one in 2023—plus the roll-out of PSD2-enabled account-to-account rails are redrawing competitive lines.[2]Visa, “Decoding the European Mobile Wallet Evolution,” visa.co.uk Cross-border initiatives such as the G20 Roadmap cut remittance frictions, while domestic schemes like Poland’s BLIK showcase regional innovation. Incumbent banks are reacting through pan-European ventures (for example Wero) aimed at defending revenue pools from global card networks.

Key Report Takeaways

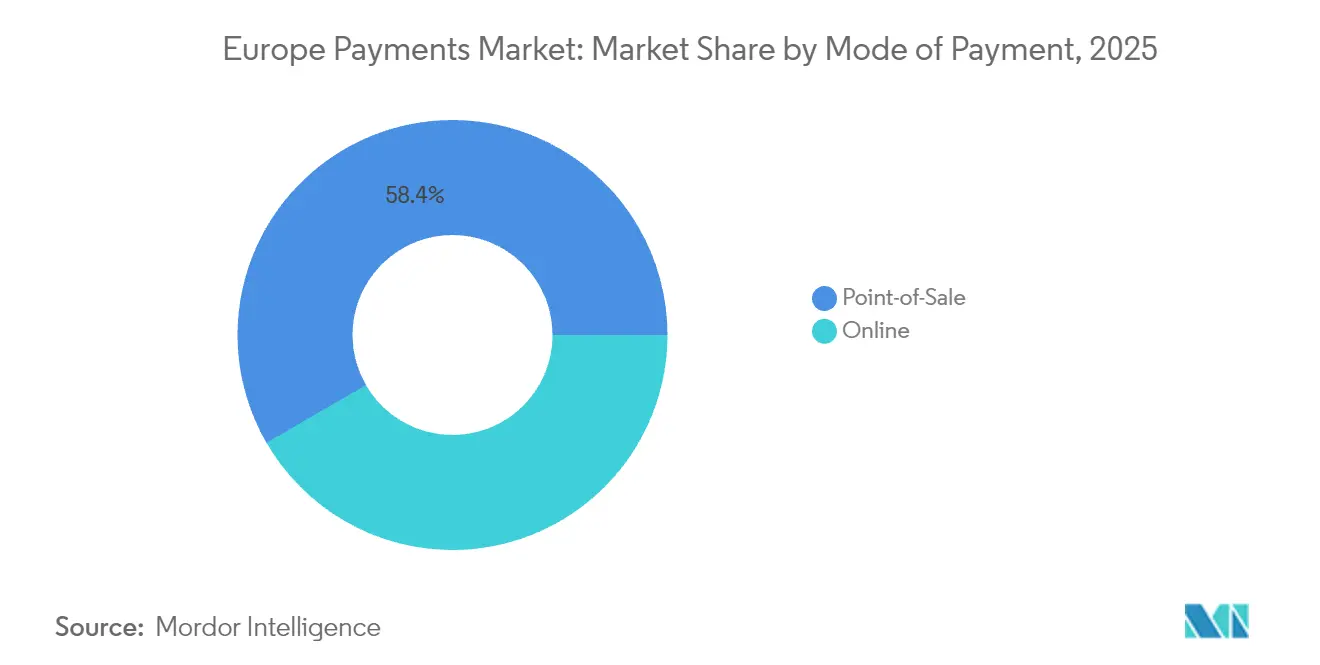

- By mode of payment, POS cards commanded 50.62% of Europe payments market share in 2025; online digital wallet & A2A payments are on course for an 17.74% CAGR through 2031. Overall Point-of-Sale led with 58.35% revenue share.

- By interaction channel, POS led with 70.45% revenue share in 2025, whereas e-commerce/m-commerce is forecast to expand at a 18.61% CAGR to 2031.

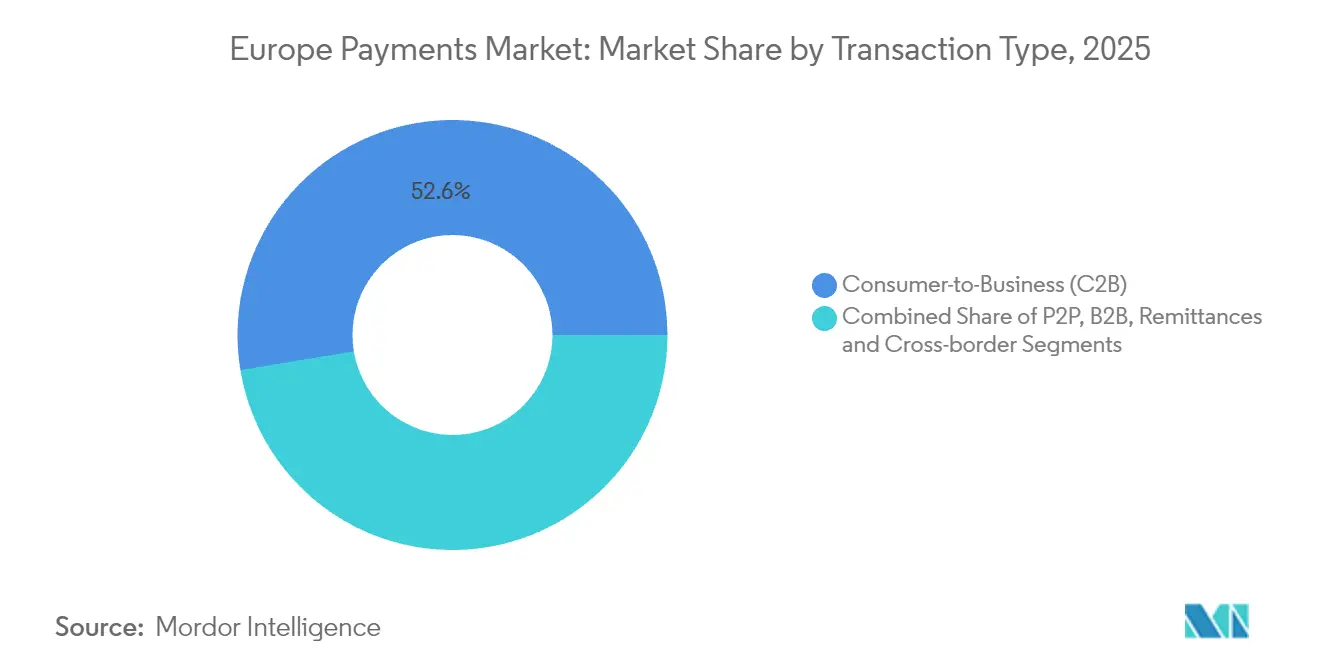

- By transaction type, consumer-to-business flows held 52.60% of Europe payments market size in 2025; remittances & cross-border payments are pacing highest at 15.76% CAGR.

- By end-user industry, retail represented 27.55% of market revenue in 2025, while healthcare payments are tracking an 17.89% CAGR through 2031.

- By country, the United Kingdom retained 17.70% of Europe payments market share in 2025; Poland is projected to be the fastest-growing country at a 15.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PSD2-Driven Open-Banking APIs Boosting Account-to-Account Payments | +3.2% | EU-wide, with stronger impact in UK, Nordics, and Germany | Medium term (2-4 years) |

| Pan-EU SEPA SCT Inst Rail Accelerating Real-Time Settlement | +2.8% | Eurozone countries, with gradual expansion to non-euro EU members | Short term (≤ 2 years) |

| Embedded Finance Adoption Among EU Retailers | +2.5% | Western Europe, with early adoption in UK, France, and Germany | Medium term (2-4 years) |

| Rapid E-commerce Expansion in Central & Eastern Europe | +2.1% | Poland, Czech Republic, Romania, and Baltic states | Medium term (2-4 years) |

| NFC Limit Hikes Fueling Contactless Card Usage | +1.8% | EU-wide, with higher impact in urban centers | Short term (≤ 2 years) |

| Merchant Uptake of BNPL Plug-ins Elevating AOV | +1.6% | Northern and Western Europe, with expansion to Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PSD2-Driven Open-Banking APIs Boosting Account-to-Account Payments

Open-banking rules under PSD2 let licensed third parties pull account data through secure APIs, unlocking low-cost, immediate A2A transactions that bypass card rails. UK usage leads, yet German and Nordic banks are rapidly scaling similar frameworks. Banks that move early are bundling white-label APIs for fintech collaboration, whereas laggards risk disintermediation. The forthcoming PSD3 package promises clearer data-access rules that will widen use cases, from payroll to subscription bill pay.[3]J.P. Morgan, “2024 Trends in Healthcare Payments Annual Report,” jpmorgan.com

Pan-EU SEPA SCT Inst Rail Accelerating Real-Time Settlement

The SEPA Instant Credit Transfer scheme delivers pan-European euro payments in under ten seconds and is mandatory for euro-area PSPs by January 2025. Volume growth is expected to cannibalize deferred batch card settlements, sharpening price competition and compressing interchange. PSPs are racing to overlay value-added fraud analytics and liquidity-management tools to safeguard revenue.

Embedded Finance Adoption Among EU Retailers

Retailers embed branded checkout, loyalty and financing journeys directly into their apps, trimming interchange costs and harvesting data. API-first gateways mean even mid-tier merchants can deploy pay-by-bank or split-pay at minimal lift. Large grocers in France and Germany have begun white-label debit programs, while fashion marketplaces are piloting own-brand wallets that dwell inside loyalty ecosystems.

Rapid E-commerce Expansion in Central & Eastern Europe

Poland illustrates the region’s trajectory: domestic scheme BLIK processed more than 420 million transactions in 2024 and is live in three neighboring countries. As regional GDP growth outpaces the EU average, cross-border sellers are localizing checkout to support domestic rails, mobile wallets and cash-on-delivery hybrids. Payment firms that master local regulation and consumer nuance capture incremental flow otherwise lost to global cards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange-Fee Fragmentation & Local Scheme Complexity | -1.9% | EU-wide, with greater impact in markets with strong domestic schemes | Medium term (2-4 years) |

| Fraud Exposure in Instant Payments Raising Provision Costs | -1.6% | EU-wide, with higher impact in early-adopting countries | Short term (≤ 2 years) |

| Legacy Core Banking Systems Slowing Instant Payments Adoption | -1.4% | EU-wide, with greater impact in markets with older banking infrastructure | Medium term (2-4 years) |

| GDPR-Driven Data-Localisation Constraints | -1.2% | EU-wide, with stricter enforcement in Germany, France, and Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interchange-Fee Fragmentation & Local Scheme Complexity

Capped consumer card interchange under the IFR still diverges in practice, forcing merchants to juggle Carte Bancaire, Bancontact and Girocard alongside global brands, raising compliance overhead. PSPs absorb duplicate certification and routing costs that dilute innovation budgets.

Fraud Exposure in Instant Payments Raising Provision Costs

Real-time irrevocable transfers magnify fraud liability; banks must deploy AI pattern-recognition tools and fund reimbursement schemes, lifting cost bases and creating scale advantages for large processors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Reshaping Payment Landscape

POS card payments retained the largest slice in 2025 at 50.62%, reflecting years of infrastructure investment and consumer habit. Overall Point-of-Sale led with 58.35% revenue share. Yet the Europe payments market is seeing digital wallets and A2A rails compound at an 17.74% CAGR, pulling share from cards online and at point of sale. A rising cohort of 72% of Europeans actively use a wallet, and global e-commerce share for wallets is set to surpass 52.5% by 2025. Cash usage is retreating, though it still holds niche strength for low-value or rural purchases. Wearable and QR-based options are gaining incremental share among early adopters. As consortium wallet Wero scales across major euro economies, incumbents are compelled to harmonize acceptance and loyalty integration.

Cards’ entrenched position ensures continued relevance, but issuers are enriching propositions with installment features and crypto reward tie-ins to stem outflow. The Europe payments market size for card-based flows is nevertheless expected to plateau as wallet-based A2A debits capture bill pay, subscription and micro-ticket use cases. Payment gateways that orchestrate a single integration for cards, bank-debited wallets and pay-by-bank are positioned to win merchant preference.

By Interaction Channel: E-commerce Acceleration Transforms Payment Dynamics

Point-of-sale transactions still dominated with 70.45% share in 2025, mirroring Europe’s sizeable brick-and-mortar footprint. Lockdowns accelerated digital engagement, and that momentum persisted: Europe payments market size for e-commerce and m-commerce is advancing at 18.61% CAGR through 2031. Omnichannel journeys blur channel lines, with click-and-collect, QR-initiated in-store pay and pay-by-link in chat fostering continuity. Payment providers that unify risk scoring and token management across channels shield merchants from fraud spikes and boost authorization rates.

Mobile accounts for a growing majority of e-commerce checkouts, led by embedded buttons inside social and gaming apps. The shift forces acquirers to master app-based one-click tokens and to support scheme-level network tokenization. Europe payments market share for purely in-app transactions is forecast to rise fastest within the channel mix, spurring demand for SDKs that compress integration effort for thousands of mid-size merchants.

By Transaction Type: Cross-Border Payments Gaining Momentum

Consumer-to-business flows represented 52.60% of transaction value in 2025, anchored by retail spending and recurring bill pay. The cross-border segment, however, is the growth standout at 15.76% CAGR, propelled by SME export activity and diaspora remittances. Enhanced corridors under the G20 Roadmap aim to cut cost and settlement time, encouraging wallet-to-wallet remittances that settle over regional instant-payment pipes. Person-to-person apps leveraging SCT Inst now offer near-zero-cost domestic transfers, eroding cash peer payments. Business-to-business volumes remain chunky, but process complexity leaves ample room for fintechs that can automate invoicing, reconcile data and embed trade-finance options.

In value terms, Europe payments market size tied to B2B remains substantial even if growth lags consumers, prompting banks to develop real-time ISO 20022 compatible request-to-pay modules. Regulation-driven e-invoicing mandates arriving in France, Germany and Poland will accelerate digitization and tie directly into these payment requests.

By End-User Industry: Healthcare Digitalization Drives Payment Innovation

Retail kept the largest 27.55% revenue share in 2025, fueled by contactless ubiquity and checkout-free pilots. Retailers increasingly deploy proprietary wallets and subscription bundles that fuse payment, loyalty and micro-financing, tightening grip on customer data. Healthcare, meanwhile, is tracking an 17.89% CAGR as tele-consultation, e-pharmacy and insurance reimbursement shift online. Europe payments market share captured by healthcare is small today but accelerating as hospitals mandate online co-pay and insurers push instant claim pay-out to wallets.

Entertainment & digital content ecosystems rely on recurring and micro-payment flows, pushing gateways to perfect low-value token billing and chargeback mitigation. Hospitality and travel rebound has nudged hoteliers into pre-arrival pay-by-link and biometric-verified check-in settlement. Government & utilities continue to phase out paper giro slips, moving citizens to QR invoices that settle via national instant rails, bolstered by EU digital public infrastructure grants.

Geography Analysis

The United Kingdom captured 17.70% of the Europe payments market in 2025, benefiting from near-universal contactless coverage and early open-banking penetration. Faster Payments, which already clears domestic transfers in seconds, provides a blueprint for the region’s instant payment ambitions. Regulatory focus on BNPL conduct points to a balanced innovation-protection stance, and the Bank of England’s work on a digital pound underscores the drive to future-proof public money.

Germany, France and Spain together account for a sizeable share of the Europe payments market. Germany’s habit of PayPal and invoice-after-delivery is gradually giving way to wallets and pay-by-bank as PSD2 flows become mainstream. France’s emphasis on biometric authentication, backed by local scheme Carte Bancaire, seeks to fortify consumer trust. Spain has observed double-digit e-commerce turnover growth, with wallets bundled into super-apps targeting Gen Z.

Italy and Poland form the vanguard of high-growth territories. Poland, recording a 15.05% CAGR forecast, leverages domestic scheme BLIK, which now extends to Romania and Slovakia. Supportive macro conditions—GDP seen rising 3.5% in 2025—bolster consumer spend. The Nordic cluster, nearly cash-free, showcases wallet consolidation: MobilePay and Vipps merged, amassing scale to negotiate interchange and acceptance.

The rest of Europe—Benelux, Balkans and Baltics—presents a patchwork of adoption stages. Baltic regulators encourage crypto-friendly policies, while Balkan countries prioritize card acceptance infrastructure. The European Central Bank’s retail payments strategy targets uniform access, advocating instant rails and prepping for a digital euro that could harmonize settlement across the bloc.

Competitive Landscape

Card networks Visa and Mastercard remain pivotal yet face fresh challenges. Sixteen leading European banks launched Wero to reclaim strategic control of wallet and P2P rails. Worldline, Europe’s largest acquirer, is embedding Google Cloud AI to sharpen fraud detection while rolling out its Power24 program that targets USD 200 million in savings by 2025.

Nexi S.p.A.’s EUR 4 billion (USD 4.3 billion) EMTN shelf arms it for consolidation and organic expansion from Italy into DACH and CEE corridors. BNP Paribas and BPCE formed Estreem to capture issuer-processor economics in France, aspiring to process 17 billion annual transactions.

Fintech disruptors accelerate specialization. Adyen scales unified commerce APIs, Satispay targets person-to-merchant micro-payments, and BLIK eyes regional expansion. Altogether, the top five processors command roughly 55% of the Europe payments market value, leaving space for niche players in verticalized SaaS and cross-border corridors.

Europe Payments Industry Leaders

Visa Inc.

Currence iDEAL BV

Melio Payments Inc.

Mastercard Incorporated

Giropay GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: BNP Paribas and BPCE created Estreem to consolidate French processing and target EU expansion, bundling instant-payment and multi-scheme support.

- January 2025: Worldline unveiled its Power24 transformation plan and entered a strategic AI partnership with Google, aligning cost discipline with product innovation.

- January 2025: Nexi S.p.A. set up a EUR 4 billion (USD 4.3 billion) EMTN programme to diversify funding for expansion.

- December 2024: The ECB reported cash used in 52% of POS payments, confirming the gradual shift toward digital.

Europe Payments Market Report Scope

Payments are increasingly becoming cashless, and the industry's role in fostering inclusion has become a top priority. Payments contribute to developing digital economies and drive innovation, all while serving as a stable backbone around the world.

The Europe Payments Market is Segmented by Mode of Payment (Point of Sale (Card Payments, Digital Wallet, Cash), Online Sale (Card Payments, Digital Wallet)), by End-user Industries (Retail, Entertainment, Healthcare, Hospitality), and by Country.

Segmentation by Mode of Payment

| Point-of-Sale | Card (Debit, Credit, Pre-paid) |

| Digital Wallets (Apple Pay, Google Pay, Interac Flash) | |

| Cash | |

| Other POS (Gift-cards, QR, Wearables) | |

| Online | Card (Card-Not-Present) |

| Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal) | |

| Other Online (COD, BNPL, Bank Transfer) |

Segmentation by Interaction Channel

| Point-of-Sale |

| E-commerce/M-commerce |

Segmentation by Transaction Type

| Person-to-Person (P2P) |

| Consumer-to-Business (C2B) |

| Business-to-Business (B2B) |

| Remittances and Cross-border |

Segmentation by End-user Industry

| Retail |

| Entertainment and Digital Content |

| Healthcare |

| Hospitality and Travel |

| Government and Utilities |

| Other End-user Industries |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Poland |

| Nordics |

| Rest of Europe (Eastern Europe, Benelux, Baltics, etc.) |

| Segmentation by Mode of Payment | Point-of-Sale | Card (Debit, Credit, Pre-paid) |

| Digital Wallets (Apple Pay, Google Pay, Interac Flash) | ||

| Cash | ||

| Other POS (Gift-cards, QR, Wearables) | ||

| Online | Card (Card-Not-Present) | |

| Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal) | ||

| Other Online (COD, BNPL, Bank Transfer) | ||

| Segmentation by Interaction Channel | Point-of-Sale | |

| E-commerce/M-commerce | ||

| Segmentation by Transaction Type | Person-to-Person (P2P) | |

| Consumer-to-Business (C2B) | ||

| Business-to-Business (B2B) | ||

| Remittances and Cross-border | ||

| Segmentation by End-user Industry | Retail | |

| Entertainment and Digital Content | ||

| Healthcare | ||

| Hospitality and Travel | ||

| Government and Utilities | ||

| Other End-user Industries | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Poland | ||

| Nordics | ||

| Rest of Europe (Eastern Europe, Benelux, Baltics, etc.) | ||

Key Questions Answered in the Report

What is the current value of the Europe payments market?

The market processed USD 0.74 trillion in 2026 and is on track to hit USD 1.48 trillion by 2031.

Which payment mode is growing fastest in Europe?

Digital wallets and account-to-account rails are expanding at an 17.74% CAGR, outpacing cards and cash.

How will the Instant Payments Regulation affect European businesses?

From January 2025, all euro transfers must settle in under ten seconds at no extra cost, lowering liquidity risk and enabling new real-time services.

Why is Poland considered a payments growth hotspot?

Strong GDP growth plus the success of domestic scheme BLIK position Poland for a 15.05% CAGR through 2031.

What role do embedded finance solutions play for retailers?

Embedded finance lets merchants control checkout, lower processing fees and generate new revenue through branded payment and loyalty programs.

Are BNPL products likely to face stricter regulation?

Yes. Draft rules in the UK and EU require clearer disclosures and affordability checks, which should enhance long-term consumer confidence while tempering near-term growth.

Page last updated on: