Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

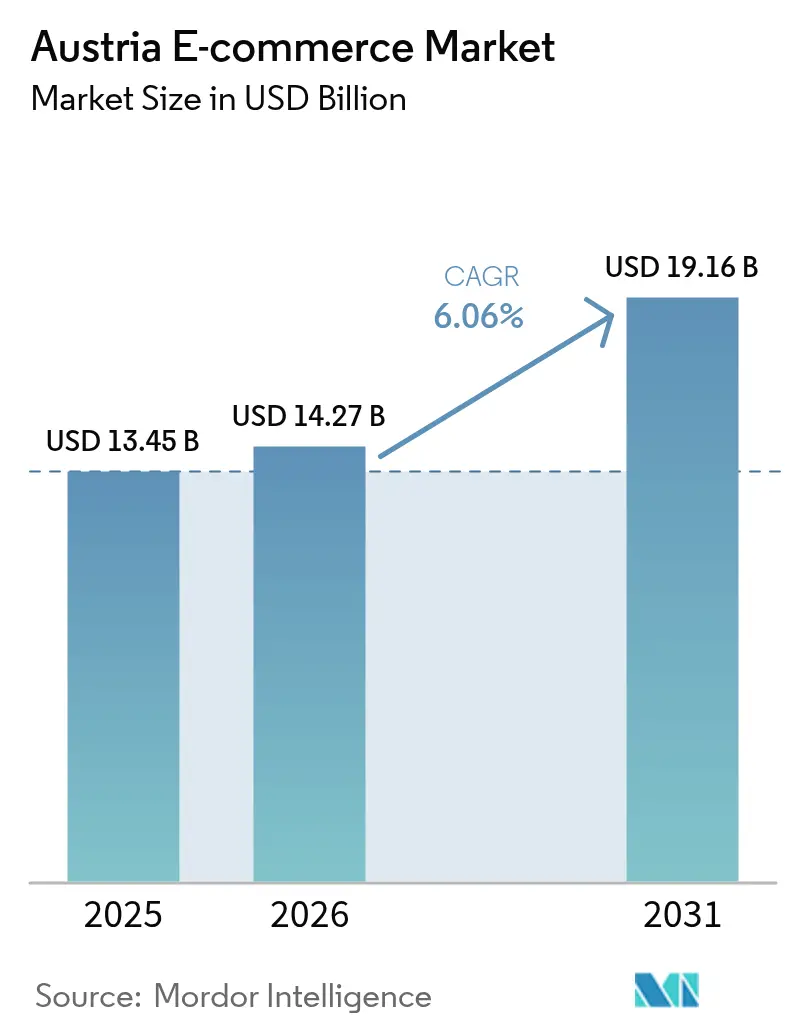

| Base Year Market Size (2025) | USD 13.45 Billion |

| Market Size (2026) | USD 14.27 Billion |

| Market Size (2031) | USD 19.16 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria E-commerce Market Analysis by Mordor Intelligence

The Austria E-commerce market size was valued at USD 13.45 billion in 2025 and estimated to grow from USD 14.27 billion in 2026 to reach USD 19.16 billion by 2031, at a CAGR of 6.06% during the forecast period (2026-2031). This steady trajectory reflects balanced momentum rather than explosive expansion, underpinned by nationwide gigabit connectivity targets, post-pandemic shifts toward mobile shopping, and widening acceptance of digital wallets and Buy-Now-Pay-Later (BNPL) services. German cross-border marketplaces deepen product variety and sharpen price competition, while Vienna-centred warehouse constraints raise fulfillment costs and widen the urban–rural service gap. Policy reforms such as Austria’s Verpackungsverordnung packaging ordinance intensify compliance spending, yet the same regulatory focus on sustainability positions re-commerce as a future growth lever. Collectively, these forces anchor the Austria E-commerce market as a stable albeit competitive digital commerce arena within Central Europe.

Key Report Takeaways

- By business model, B2C led with 84.30% revenue share in 2025; B2B is projected to expand at a 9.02% CAGR through 2031.

- By device type, smartphones commanded 58.45% of the Austria E-commerce market share in 2025 and are advancing at an 8.34% CAGR through 2031.

- By payment method, digital wallets retained 35.35% share of the Austria E-commerce market size in 2025, while BNPL records the fastest growth at 9.63% CAGR to 2031.

- By B2C product category, fashion & apparel held 27.60% share of the Austria E-commerce market size in 2025; food & beverage is expanding at a 10.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border SKU Expansion by German Marketplaces | +1.2% | National, with concentration in Vienna and border regions | Medium term (2-4 years) |

| BNPL Adoption Among Gen-Z Shoppers | +0.8% | National, with urban concentration | Short term (≤ 2 years) |

| Broadband Austria 2030 Rural Fibre Roll-out | +1.5% | Rural areas, expanding to national coverage | Long term (≥ 4 years) |

| Dual-Income Households Fuel Premium Fashion Demand | +0.7% | Urban centers, particularly Vienna and Salzburg | Medium term (2-4 years) |

| EU Digital Product Passport Boosts Re-commerce | +0.6% | National, with early adoption in fashion and electronics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cross-border SKU expansion by German marketplaces

German marketplaces inject a broader assortment and sharper pricing into the Austria E-commerce market, with Amazon.de alone registering USD 922.4 million Austrian sales in 2022.[1]International Trade Administration, “Austria – eCommerce,” trade.gov Consumers benefit from wider choice while domestic retailers feel margin pressure, prompting pivots toward niche product curation, localised customer service and omnichannel pick-up points. Harmonised VAT rules since 2021 streamline check-out flows, keeping cross-border friction low and reinforcing the medium-term uplift.

BNPL adoption among Gen-Z shoppers

BNPL’s 9.8% CAGR mirrors Gen-Z preference for flexibility, elevating conversion rates in high-ticket fashion and electronics baskets. EU draft directives to fold BNPL into consumer-credit law should temper irresponsible lending, yet Austrian merchants embedding credit-risk analytics expect sustained cart-value gains once guardrails crystallise.

Broadband Austria 2030 rural fibre roll-out drives the market

The EUR 10-12 billion (USD 10.8-13 billion) public-private programme aims for nationwide gigabit speeds by 2030. New fibre backbones unlock rural demand where slow lines once deterred check-out, adding roughly 200,000 households to the reachable customer pool.[2]European Commission, “Digital connectivity in Austria,” digital-strategy.ec.europa.eu Retailers anticipate AR-enabled product views and high-definition livestream selling to flourish as bandwidth widens.

Dual-income households fuel premium fashion demand

A 74.1% employment rate and GDP per capita of EUR 49,400 (USD 53,300) in 2024 empower dual-income Austrian households to trade up to premium fashion online.[3]EURES European Union, “Labour Market Information: Austria,” eures.europa.eu Retailers that emphasise quality fabrics, limited editions and next-day delivery capture wallet share without deep discounting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Verpackungsverordnung Compliance Costs | -0.9% | National, with higher impact on smaller retailers | Short term (≤ 2 years) |

| Vienna-Area Warehouse Capacity Shortage | -0.6% | Vienna metropolitan area, affecting national distribution | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Verpackungsverordnung compliance costs hinders the market

Expanded packaging obligations oblige each e-commerce seller to finance collection schemes and appoint local agents. Several Asia-based merchants suspended Austrian deliveries when fees erased profit on low-value SKUs. Bigger platforms leverage scale to dilute per-unit cost, widening the moat against smaller rivals.

Vienna-area warehouse capacity shortage hinders the market

Vacancy below 2% and escalating rents near the capital push fulfillment centres to peripheral zones, adding last-mile kilometres and fuel outlay [colliers.com](). Same-day promises become harder for SMEs, nudging consumers toward cross-border sites whose regional mega-hubs feed Austria overnight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B emerges as growth engine

The B2C stream maintained 84.30% of Austria E-commerce market size in 2025, yet the B2B channel is forecast to compound at 9.02% through 2031. Bulk order values, contract-based replenishment and workflow integrations translate into steadier cash flows for platforms courting enterprise buyers. Manufacturers located in Upper Austria and Styria embed punch-out catalogues and e-invoicing to cut procurement lead times, positioning the Austria E-commerce market for deeper penetration of industrial MRO and office supplies. Foreign buyers sourcing Austrian precision components further stretch addressable volumes. Meanwhile, consumer-oriented players defend share by layering experiential content, loyalty tiers and seamless returns, maintaining the broad appeal that sustains the Austria E-commerce market.

By Device Type: Mobile commerce dominance accelerates

Smartphones generated 58.45% Austria E-commerce market share in 2025 and headline the growth table with an 8.34% CAGR. App-first interfaces, biometric log-in and one-tap wallet checkout transform scrolling sessions into paid carts. Desktop traffic slips but retains relevance for complex B2B tender uploads. Tablets and connected TVs remain niche entertainment-driven gateways. Retailers embed video try-ons and AI chat to personalise mobile journeys, fuelling incremental spend and reinforcing the Austria E-commerce market’s mobile-first orientation.

By Payment Method: Digital transformation reshapes preferences

Digital wallets commanded 35.35% of Austria E-commerce market size in 2025, providing frictionless tokenised payments. BNPL options, despite a smaller base, advance at 9.63% CAGR by offering budget predictability to younger cohorts. Card rails still underpin many wallet or BNPL back-ends, but direct card share erodes as consumers migrate to embedded finance. Merchants that cascade three or more payment modes report double-digit declines in cart abandonment, evidencing how payment diversity now dictates competitive edge within the Austria E-commerce market.

By B2C Product Category: Food & Beverage disrupts traditional leaders

Fashion & apparel kept pole position at 27.60% Austria E-commerce market size in 2025, yet online groceries and meal kits post a 10.22% CAGR that will close the gap. Parcel carriers that rolled out insulated last-mile assets now service rural households alongside Vienna apartment blocks, broadening delivery density. Subscription snack boxes and regional farm produce tap Austria’s provenance-driven food culture. Electronics and furniture log mid-single-digit uplifts as replacement cycles lengthen, but upselling accessories helps sustain basket value across the Austria E-commerce market.

Geography Analysis

Vienna accounted for nearly 38.90% of 2025 online spend, buoyed by superior fibre coverage, dense courier fleets and high disposable incomes. Salzburg and Tyrol show elevated conversion rates thanks to tourism-funded logistics corridors that interface seamlessly with German supply hubs. Eastern provinces such as Burgenland trail on absolute volume yet are posting double-digit growth as Broadband Austria 2030 narrows the speed gap. Border districts record above-average cross-border shopping; 51% of Austrian e-purchases originate abroad, with German storefronts capitalising on language affinity. Alpine terrain complicates last-mile routing, though drone testbeds and parcel lockers along rail stations present mitigations that extend the Austria E-commerce market reach. As rural penetration rises, merchants anticipate more uniform demand curves across the nine federal states, diluting Vienna’s historic dominance but enlarging the overall Austria E-commerce market.

Competitive Landscape

International multi-category platforms capture 65% of Austrian online spend, reflecting a moderate concentration where scale in logistics, cloud infrastructure and seller ecosystems sets the competitive tone. Amazon leverages its EUR 320 billion European investment blueprint to embed same-day capabilities and loyalty bundles that lift retention. Zalando’s acquisition of ABOUT YOU consolidates fashion traffic and enriches B2B fulfilment APIs, reinforcing category leadership. MediaMarktSaturn’s marketplace pivot aligns its bricks-and-mortar fleet with a 29% online revenue mix, demonstrating how omnichannel synergies counter pure-play rivals.

Domestic champions exploit regulatory know-how and last-mile density. Austrian Post’s Shöpping.at scales cross-border seller onboarding while its parcel unit handled over 500 million packages in 2024. Grocery leaders Spar and Billa Plus use micro-fulfillment nodes inside supermarkets to tighten delivery windows. Furniture specialist XXXLutz deploys augmented-reality room planners, cushioning the bulky-goods delivery challenge. Across the Austria E-commerce market, emerging differentiators include retail-media monetisation, AI-driven dynamic pricing and carbon-neutral delivery commitments, areas where scale players currently outrun niche operators.

Austria E-commerce Industry Leaders

Amazon.com Inc.

Zalando SE

MediaMarkt Saturn Retail Group

Otto GmbH (Universal.at)

H&M Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zalando SE completed its acquisition of ABOUT YOU, strengthening its position in the European fashion e-commerce market with combined GMV of EUR 15.3 billion (USD 17.76 billion). The acquisition enhances Zalando's technology capabilities and customer base while expanding its B2B platform services for fashion retailers.

- December 2024: European Central Bank published payment behavior data showing digital payment adoption reaching 48% of online transactions, with mobile apps and payment wallets accounting for 29% of e-commerce purchases across the eurozone including Austria.

- June 2024: Otto Group reported challenging financial performance with EUR 15 billion (USD 17.41 billion) revenue and approximately EUR 11 billion (USD 12.77 billion) e-commerce sales, while emphasizing strategic investments in AI technologies and logistics optimization to enhance competitive positioning.

- May 2024: Austrian Post announced Shöpping.at platform expansion into Germany, enabling merchants to sell to both German and Austrian customers while introducing cloud-based data integration tools for retailers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the Austria e-commerce market as all B2C and B2B transactions in which ordering and payment are completed online, via desktop, mobile, or app, and the product or service is physically fulfilled or digitally delivered inside Austria. Values are expressed in gross merchandise value (GMV) and include cross-border purchases delivered to Austrian addresses.

Scope Exclusion: C2C classifieds, purely digital media streaming, ticketing, and in-store click-and-collect sales are excluded.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with Austrian online retailers, logistics providers, and payment gateways across Vienna, Salzburg, and Tyrol. These conversations clarified domestic versus cross-border shares, return rates, and emerging BNPL adoption, helping us reconcile model assumptions that secondary data alone could not fully explain.

Desk Research

Our team first collects core inputs from Statistik Austria household ICT surveys, Eurostat retail turnover, Austrian Post parcel statistics, and Customs tariff data, which together anchor shopper penetration, spending, and import flows. We add insights from trade bodies such as Handelsverband Österreich and the European Central Bank for payment method splits, plus company filings and investor decks to sense-check category mix and average selling prices.

Subscription databases, including D&B Hoovers for retailer revenues and Dow Jones Factiva for deal flow, supply further validation on market shares and growth pockets. The sources listed are illustrative; several additional public and paid references informed the final dataset.

Market-Sizing & Forecasting

A top-down build starts with official retail sales, then applies e-commerce penetration by category, shopper cohort, and device. Bottom-up checks, sampled retailer GMV roll-ups and parcel volume back-calculations, temper the totals. Key model variables include internet user growth, smartphone share of checkouts, average basket values, parcel return ratios, VAT rule changes, and cross-border spend leakage. Forecasts use multivariate regression blended with scenario analysis for macro shocks; coefficients are stress tested with our primary research panel before finalization.

Data Validation & Update Cycle

Outputs undergo variance scans against trade flow anomalies and third-party benchmarks, followed by a two-stage internal peer review. Reports refresh annually, with interim updates triggered by material events such as tax revisions or platform M&A, ensuring clients always receive the most up-to-date view.

Why Mordor's Austria E-commerce Baseline Stand Apart

Published estimates often differ because firms pick dissimilar scopes, base years, and refresh rhythms. Our disciplined inclusion rules, dual-layer model, and yearly update cadence mitigate those gaps.

Key Gap Drivers: several publishers fold travel, food delivery, or marketplace fees into GMV, apply aggressive marketplace mark-ups, or extrapolate from limited card processor panels, which inflates or deflates totals relative to Mordor's matched-scope baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.45 B (2025) | Mordor Intelligence | - |

| USD 19.6 B (2024) | Global Consultancy A | Includes travel, media streaming, and assumes all foreign-sourced orders are domestic value |

| USD 10.9 B (2024) | Data Platform B | Excludes B2B flows and adjusts GMV to net sales minus returns only |

| USD 12.0 B (2024) | Market Analytics C | Relies on limited retailer survey sample; mobile-only sales modeled from global ratios |

The comparison shows that Mordor's numbers strike a balanced midpoint, comprehensive yet not inflated, because they trace directly to transparent variables, blended methods, and continuous validation, giving decision-makers a dependable baseline for planning.

Key Questions Answered in the Report

What is the current size of the Austria E-commerce market?

The Austria E-commerce market is worth USD 14.27 billion in 2026 and is set to grow steadily at a 6.06% CAGR toward 2031.

Which segment is expanding the fastest?

B2B digital procurement is the fastest, advancing at a 9.02% CAGR as Austrian firms automate purchasing workflows.

How important is mobile shopping in Austria?

Smartphones already account for 58.45% of Austria E-commerce market share and lead growth with an 8.34% CAGR, underscoring a decisive mobile-first shift.

Why is BNPL so popular among Austrian consumers?

BNPL offers flexible instalments that resonate with Gen-Z shoppers, driving a 9.63% CAGR and boosting cart conversions for higher-ticket items.

What challenges do smaller Austrian e-retailers face?

They grapple with rising packaging-compliance costs and scarce Vienna warehouse capacity, both of which inflate operating expenses and lengthen delivery times.

How will rural broadband upgrades influence future growth?

Gigabit roll-outs under Broadband Austria 2030 will connect 200,000 additional households, enlarging the customer base and enabling bandwidth-intensive shopping experiences outside urban cores.

Page last updated on: